Market Definition

The India Refinery Catalysts Market encompasses the development, manufacturing, supply, regeneration, and technical servicing of heterogeneous and homogeneous catalyst systems deployed across crude oil refining process units at Indian public sector and private sector refineries to enable, accelerate, and control the chemical transformation reactions that convert crude oil fractions into transportation fuels, petrochemical feedstocks, lubricant base oils, and specialty hydrocarbon products meeting increasingly stringent quality, emission, and performance specifications mandated by Indian regulatory authorities and export market requirements. Refinery catalysts are engineered functional materials, typically comprising active metal components including platinum, palladium, molybdenum, nickel, cobalt, and tungsten supported on high-surface-area alumina, silica-alumina, zeolite, or titania carrier substrates, whose precise composition, pore architecture, acidity profile, and surface chemistry determine the selectivity, activity, and operational stability of the refining process unit to which they are applied.

The market encompasses fluid catalytic cracking catalysts and additives used to convert heavy vacuum gas oil into gasoline and light olefin products; hydroprocessing catalysts including hydrotreating and hydrocracking catalysts used to remove sulfur, nitrogen, and metal contaminants and upgrade distillate and residue fractions; catalytic reforming catalysts used to produce high-octane gasoline components and aromatics; isomerization catalysts for light naphtha octane improvement; alkylation catalysts for high-octane blending component production; and residue upgrading catalysts for processing opportunity crudes and heavy residue streams. The market further includes catalyst regeneration services, spent catalyst reclamation and metals recovery programs, and technical service agreements providing refinery operators with catalyst performance monitoring, operational optimization, and end-of-run management support. Key participants include global catalyst technology licensors and manufacturers, domestic Indian catalyst producers, refinery operating companies including Indian Oil Corporation, Bharat Petroleum Corporation, Hindustan Petroleum Corporation, Reliance Industries, Nayara Energy, and HPCL-Mittal Energy, and catalyst service companies providing regeneration and performance analytics across the Indian refining industry.

Market Insights

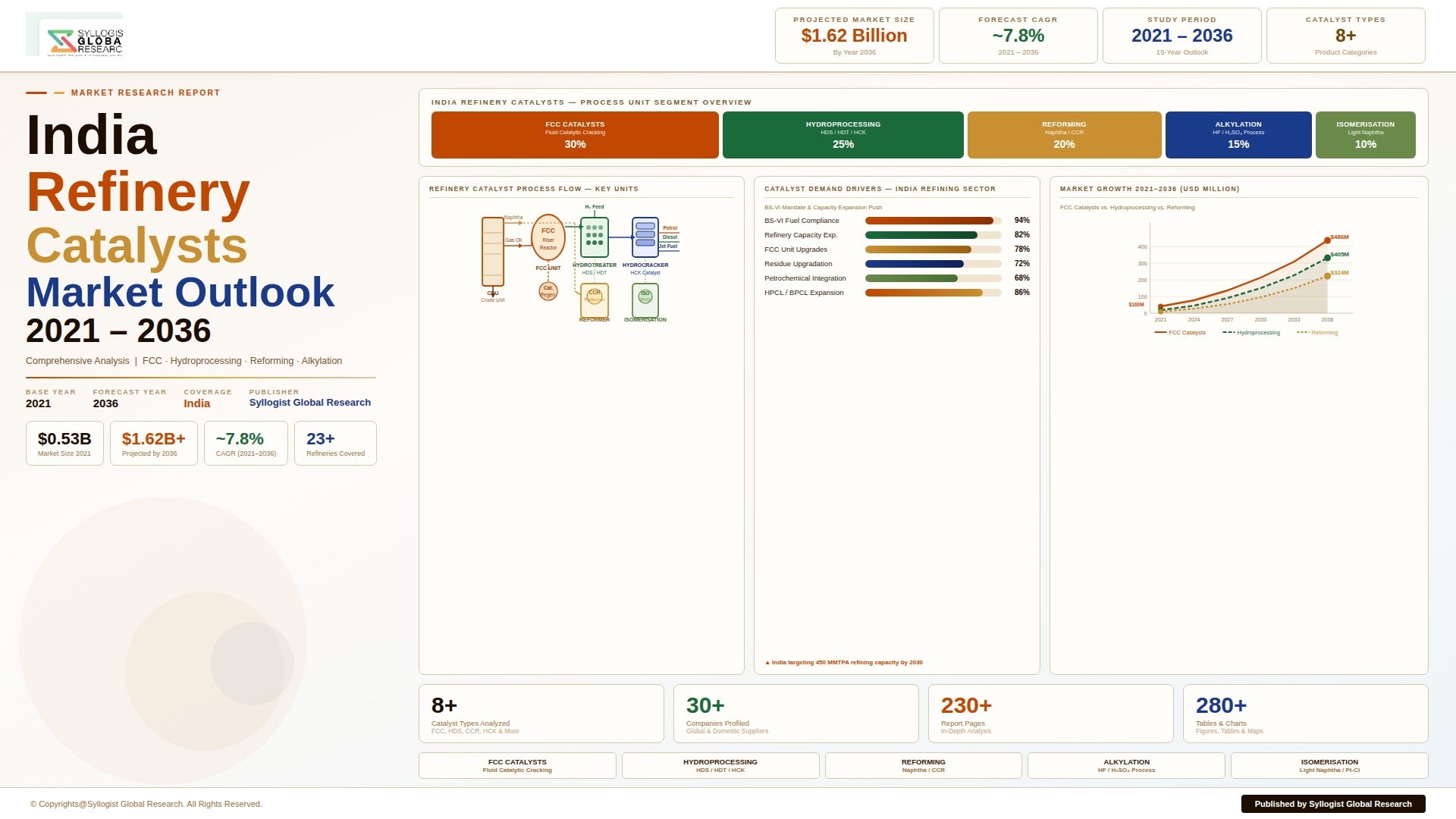

The India refinery catalysts market is structurally positioned for sustained growth underpinned by the country’s ongoing refinery capacity expansion program, the mandatory nationwide transition to Bharat Stage VI emission norms that has fundamentally transformed the hydroprocessing catalyst demand profile of Indian refineries, and the strategic shift of the Indian refining sector toward processing a more diverse and increasingly challenging crude slate incorporating heavier, higher-sulfur opportunity crudes whose economic attractiveness demands more sophisticated and active catalyst systems across hydroprocessing, fluid catalytic cracking, and residue conversion process units. The India refinery catalysts market was valued at approximately USD 620 million in 2025 and is projected to reach USD 1.04 billion by 2034, advancing at a compound annual growth rate of 5.9% over the forecast period from 2027 to 2034, driven by new refinery capacity additions, accelerating secondary processing unit investments oriented toward petrochemical integration, and the growing technical sophistication of catalyst procurement by Indian refinery operators pursuing margin improvement through catalyst performance optimization across both grassroots and revamped process units.

Hydroprocessing catalysts constitute the largest and most rapidly expanding product segment of the India refinery catalysts market, accounting for approximately 43% of total market revenue in 2025, a structural dominance directly attributable to the transformative impact of the nationwide Bharat Stage VI fuel quality transition implemented in April 2020, which required Indian refineries to reduce automotive diesel sulfur content from 50 parts per million under BS IV norms to 10 parts per million, necessitating extensive capital investment in new and revamped diesel hydrotreating units and the adoption of high-activity catalyst systems capable of achieving ultra-low sulfur diesel specifications across the full range of straight-run and cracked distillate streams processed in Indian refinery configurations. The BS VI transition compressed into a period of less than four years a level of hydroprocessing catalyst technology upgrade that took over a decade to accomplish in the European and North American refining industries, and the resulting installation of advanced cobalt-molybdenum and nickel-molybdenum hydrotreating catalyst systems across Indian public sector and private sector refineries has materially elevated the technical baseline of hydroprocessing catalyst demand and created a recurring replacement market for high-activity catalyst reloads that will sustain hydroprocessing catalyst demand growth well beyond the initial transition capital expenditure cycle. Indian Oil Corporation’s Panipat, Mathura, Barauni, and Gujarat refineries, Bharat Petroleum’s Mumbai and Kochi refineries, and Hindustan Petroleum’s Mumbai and Visakhapatanam refineries have each undergone substantial hydroprocessing unit capacity additions or catalyst technology upgrades to meet BS VI specifications, generating multi-hundred-crore rupee catalyst procurement commitments at each major refinery reload cycle.

Fluid catalytic cracking remains the most strategically consequential process unit in the Indian refining industry’s configuration, with the FCC unit functioning as the primary conversion workhorse at the majority of Indian refineries by determining the gasoline yield, olefin production, and bottoms upgrading performance that together define refinery gross margin across varying crude input and product market conditions. Indian refineries operate a combined fluid catalytic cracking capacity of approximately 41 million metric tonnes per year across 23 FCC and RFCC units at major public and private sector refineries, making India the second-largest FCC catalyst consuming country in the Asia-Pacific region after China, with annual FCC catalyst and additive consumption valued at approximately USD 215 million in 2025. The progressive shift of the Indian refining industry toward processing heavier and higher-metals-content opportunity crudes from the Middle East, Latin America, and West Africa, incentivized by the attractive price discount these crude grades trade at relative to Indian basket crude, is intensifying the metals tolerance, bottoms cracking activity, and vanadium passivation performance requirements of FCC catalyst systems deployed at Indian refineries, driving a sustained technical upgrade in the catalyst formulations specified by Indian refinery operators and creating growing demand for advanced rare earth-loaded zeolitic catalyst systems and specialized metal trap additive products. The integration of FCC units with propylene recovery and petrochemical downstream facilities at Reliance Industries’ Jamnagar complex and at several Indian Oil Corporation refineries is further driving demand for high-propylene-selectivity ZSM-5 additive systems and deep catalytic cracking catalyst formulations that maximize light olefin yields for petrochemical feedstock production rather than optimizing conventional motor fuel yield.

The catalytic reforming and isomerization catalyst segment, while smaller in absolute volume terms than hydroprocessing and FCC catalysts, occupies a strategically important position in the Indian refinery catalysts market as refineries seek to maximize octane pool quality and reduce benzene content in the gasoline blend following the BS VI implementation of a 1% volume benzene cap in motor spirit specifications, compelling operational adjustments to reformer severity management and the adoption of improved platinum-rhenium and platinum-tin bimetallic catalyst formulations that deliver superior reformate octane at reduced benzene precursor yield. India’s ongoing refinery capacity expansion program, which includes the three-way merger and greenfield development of the proposed 60 million metric tonnes per year Ratnagiri Refinery and Petrochemicals Limited project on the Maharashtra coast, the expansion of HPCL’s Rajasthan Refinery at Barmer from 9 to 18 million metric tonnes per year capacity, and multiple debottlenecking and secondary unit expansion programs at existing refineries, will progressively add new catalyst inventories across all major process unit categories, creating a long-cycle demand growth driver for the Indian refinery catalysts market that extends through the late 2030s as new capacity enters service and fresh catalyst loadings are required at startup and at subsequent operational reload intervals. The growing emphasis of Indian refinery operators on catalyst lifecycle management, including mid-cycle rejuvenation treatments, in-situ regeneration optimization, and ex-situ regeneration service utilization to extend catalyst operational life and defer fresh catalyst procurement expenditure, is creating an adjacent and expanding demand stream for catalyst regeneration and performance management services alongside fresh catalyst supply.

Key Drivers

India’s Refinery Capacity Expansion and Petrochemical Integration Programs Creating Sustained Greenfield and Brownfield Catalyst Demand

India’s strategic objective of expanding total domestic refining capacity from approximately 256 million metric tonnes per year in 2025 to over 310 million metric tonnes per year by 2030 is generating a multi-year pipeline of greenfield refinery construction projects, brownfield capacity expansion programs, and secondary processing unit additions that will each require initial fresh catalyst loadings across all major process units at startup, followed by recurring reload purchases at catalyst cycle end intervals typically ranging from two to five years depending on process unit type and operating severity. The proposed Ratnagiri Refinery and Petrochemicals Limited project, representing the most ambitious single refinery development in India’s history at a planned capacity of 60 million metric tonnes per year integrated with a world-scale petrochemical complex, will upon commissioning become the largest single catalyst procurement event in Indian refining history, creating demand for FCC catalysts, hydroprocessing catalysts, reforming catalysts, and specialty petrochemical process catalysts across dozens of process units simultaneously. HPCL’s Rajasthan Refinery project at Barmer, designed to process Rajasthan crude with a Nelson Complexity Index of approximately 12.5 reflecting its heavy secondary processing orientation, will require high-activity residue hydroprocessing catalysts, RFCC catalyst systems optimized for Rajasthan crude’s high metals and asphaltene content, and integrated petrochemical process unit catalyst loadings that together represent a catalyst procurement program valued at several billion rupees at initial startup. The expansion of petrochemical integration at existing refineries, driven by the Indian government’s Chemicals and Petrochemicals Policy and the downstream demand growth generated by India’s manufacturing sector expansion, is adding dehydrogenation, metathesis, and specialty conversion process unit catalyst requirements to the demand portfolio of the Indian refinery catalysts market beyond its traditional transportation fuels process unit focus.

Opportunity Crude Processing Intensification and Nelson Complexity Upgrades Driving Demand for Advanced Residue Upgrading and Hydroprocessing Catalysts

The compelling economics of processing price-discounted heavy, high-sulfur, and high-acid opportunity crude grades from the Middle East, Latin American, and West African producing regions relative to the lighter and sweeter crude grades India’s refining system was originally configured to process are motivating Indian refinery operators to invest in residue hydroprocessing units, delayed coking additions, solvent deasphalting installations, and RFCC unit revamps that increase the proportion of opportunity crude that can be profitably processed, fundamentally upgrading the Nelson Complexity Index of the Indian refining system and expanding the installed base of process units demanding sophisticated and higher-value catalyst systems. The installation of residue hydrotreating and hydrodesulfurization units at Indian Oil Corporation’s Paradip refinery, Bharat Petroleum’s Kochi refinery IREP project, and HPCL’s Visakhapatanam refinery is creating demand for ebullated bed and fixed bed residue hydroprocessing catalyst systems whose per-unit-volume cost and technical performance requirements are substantially greater than conventional distillate hydrotreating catalysts, and whose reload cycles generate large individual catalyst procurement transactions that are commercially significant for both catalyst suppliers and refinery procurement organizations. The increasing processing of Iranian, Venezuelan, and Canadian heavy crude equivalents from alternative Middle Eastern and Latin American sources containing vanadium concentrations above 100 parts per million and nickel concentrations above 50 parts per million is intensifying the metals deactivation management requirements of both FCC and residue hydroprocessing catalyst systems at Indian refineries, driving demand for higher-activity, higher-metals-tolerance catalyst formulations and associated metals passivation additive products from global catalyst technology leaders with the formulation expertise to address the specific deactivation challenges of Indian refinery opportunity crude processing programs.

Bharat Stage VI Compliance Legacy and Future Fuel Quality Upgrading Requirements Sustaining Hydroprocessing Catalyst Reload Demand

The Bharat Stage VI fuel quality transition permanently elevated the technical baseline of hydroprocessing catalyst demand across the Indian refining industry by establishing 10 parts per million sulfur as the mandatory specification for both motor spirit and high-speed diesel, and the catalyst reload cycles now recurring at the hydrotreating and hydrocracking units installed or revamped for BS VI compliance are generating a structurally durable and growing annual catalyst procurement requirement that did not exist at comparable scale prior to 2018. Indian refineries that installed new diesel hydrotreating units or upgraded existing units to achieve BS VI specifications between 2017 and 2020 are now entering their second and third catalyst reload cycles, and the accumulated operational experience with cobalt-molybdenum and nickel-molybdenum catalyst system performance at Indian refinery conditions is enabling more sophisticated catalyst selection decisions that increasingly favor premium-activity catalyst formulations from global leaders over lower-cost alternatives where the incremental catalyst cost is justified by measurable improvements in cycle length, hydrogen consumption efficiency, or product sulfur consistency. The potential future tightening of Indian fuel quality specifications beyond current BS VI parameters, including the possible introduction of 5 parts per million sulfur limits for certain vehicle categories, aromatics content restrictions for gasoline, and polycyclic aromatic hydrocarbon limits for diesel that are under regulatory consideration, would require further hydroprocessing unit severity increases or catalyst activity enhancements that represent an additional future demand catalyst for premium hydrotreating catalyst formulations at Indian refineries across the forecast period.

Key Challenges

Dependence on Imported Catalyst Technologies and Critical Raw Materials Exposing Indian Refineries to Foreign Exchange Volatility and Supply Chain Risk

The Indian refinery catalysts market is characterized by a pronounced structural dependence on imported catalyst formulations and the critical raw material inputs required for domestic catalyst manufacturing, with the majority of high-performance fluid catalytic cracking catalysts, advanced hydroprocessing catalyst systems, and specialty reforming and isomerization catalysts consumed by Indian refineries sourced from the global technology leaders including BASF, Honeywell UOP, Albemarle, Haldor Topsoe, Criterion Catalysts, and Grace Davison, whose proprietary zeolite formulations, metal loading technologies, and support material compositions are protected by extensive intellectual property portfolios that constrain the ability of domestic Indian manufacturers to produce equivalent-performance alternatives without licensing arrangements. The precious and base metals that constitute the active components of refinery catalysts, including platinum, palladium, molybdenum, cobalt, nickel, and tungsten, are predominantly mined and refined outside India, with molybdenum supply concentrated in China, Chile, and the United States, cobalt supply concentrated in the Democratic Republic of Congo, and platinum group metals supply concentrated in South Africa and Russia, creating supply chain exposure to geopolitical disruptions, export restriction policies, and commodity price volatility that directly affects Indian catalyst manufacturing and import costs. The depreciation of the Indian rupee against the US dollar during periods of global financial market stress adds a structural cost escalation dimension to catalyst import expenditure for Indian refinery operators who budget in rupee terms but procure catalysts at dollar-denominated international prices, compressing refinery margins at precisely the moments when broader macroeconomic pressures are already challenging operational profitability.

Limited Domestic Catalyst Manufacturing Capability Constraining Indigenization and Creating Technology Access Concentration Risk

India’s domestic catalyst manufacturing industry, while possessing meaningful capability in the production of commodity-grade alumina supports, basic hydrotreating catalysts for non-critical applications, and adsorbent materials for gas processing, lacks the research infrastructure, zeolite synthesis expertise, advanced characterization capabilities, and pilot plant testing facilities required to develop and manufacture performance-equivalent alternatives to the proprietary catalyst formulations that constitute the technically demanding and highest-value segments of the Indian refinery catalysts market, creating a technology access concentration risk where the majority of Indian refinery catalyst procurement is dependent on a small number of global suppliers whose licensing terms, pricing structures, and supply allocation decisions are largely outside the influence of Indian refinery operators or government policy instruments. The absence of a world-class domestic FCC catalyst manufacturing facility capable of producing fresh equilibrium catalyst at the quality and consistency standards required by Indian FCC unit operations represents the most commercially significant gap in Indian refinery catalyst self-sufficiency, given that FCC catalyst constitutes the highest annual consumption volume catalyst category at the majority of Indian refineries and that fresh FCC catalyst additions occur on a continuous basis rather than the discrete periodic reload cycle that characterizes fixed bed hydroprocessing and reforming catalyst procurement. Indian Oil Corporation’s R and D Centre at Faridabad has developed indigenous catalyst formulations in collaboration with academic and research institutions, but the transition from laboratory-scale development to commercially proven, refinery-scale production and deployment of advanced catalyst systems remains constrained by the investment requirements, technical risk tolerance, and procurement qualification standards that govern catalyst selection decisions at Indian refinery operating organizations accountable for refinery margin and operational continuity.

Spent Catalyst Waste Management, Environmental Compliance, and Hazardous Materials Handling Regulations Adding Operational Complexity and Cost

Spent refinery catalysts, particularly those discharged from hydroprocessing units that accumulate metals including vanadium, nickel, arsenic, and iron deposited from processed crude oil streams, and from FCC units where equilibrium catalyst contains concentrated metals from continuous heavy crude feed processing, are classified as hazardous waste under India’s Hazardous and Other Wastes Management and Transboundary Movement Rules, imposing regulatory obligations on refinery operators for segregated storage, manifested transportation, licensed disposal or treatment, and detailed waste tracking documentation that add operational complexity and compliance cost to catalyst change-out operations at Indian refineries. The limited availability of certified hazardous waste management and spent catalyst reclamation facilities within India capable of recovering commercially valuable metals including molybdenum, vanadium, cobalt, and nickel from spent hydroprocessing catalysts to globally accepted recovery efficiency and environmental compliance standards means that the majority of Indian refineries export spent hydroprocessing catalyst to specialist reclamation facilities in Europe and South Korea, incurring significant international logistics costs, regulatory compliance requirements for transboundary hazardous waste movement under the Basel Convention, and extended reclamation settlement timelines that affect the working capital management of Indian refinery catalyst procurement programs. The tightening of hazardous waste storage and disposal regulations by India’s Central Pollution Control Board, combined with the increasing volumes of spent catalyst generated as Indian refineries process higher proportions of metals-contaminated opportunity crudes and expand their installed hydroprocessing unit capacity, is progressively increasing the environmental compliance burden and associated cost of catalyst end-of-life management across the Indian refining industry through the forecast period.

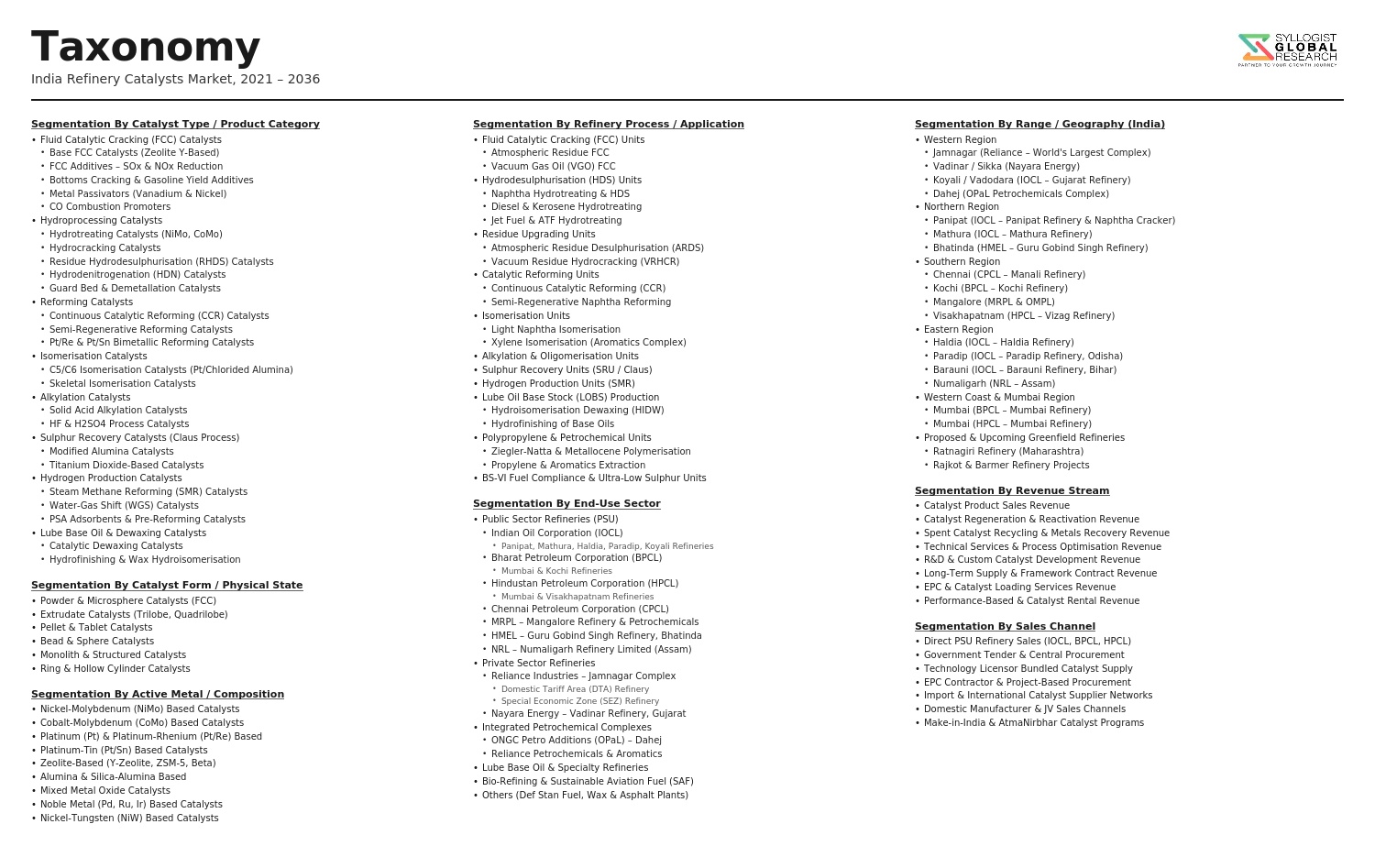

Market Segmentation

- Segmentation By Catalyst Type

- Fluid Catalytic Cracking (FCC) Catalysts and Additives

- Hydrotreating Catalysts (Cobalt-Molybdenum and Nickel-Molybdenum Systems)

- Hydrocracking Catalysts (Amorphous and Zeolitic Systems)

- Residue Hydroprocessing Catalysts (Fixed Bed and Ebullated Bed)

- Catalytic Reforming Catalysts (Platinum-Rhenium and Platinum-Tin Systems)

- Isomerization Catalysts (Chlorinated Alumina and Zeolitic Systems)

- Alkylation Catalysts (Liquid Acid and Solid Acid Systems)

- Selective Hydrogenation and Saturation Catalysts

- Specialty Petrochemical Integration Process Catalysts

- Others

- Segmentation By Application

- Naphtha and Gasoline Pool Upgrading

- Diesel and Distillate Hydroprocessing

- Vacuum Gas Oil Conversion and Hydrocracking

- Residue Conversion and Heavy Oil Upgrading

- Aromatics and Reformate Production

- Light Naphtha Isomerization

- Petrochemical Feedstock Production (Propylene, Ethylene, BTX)

- Lube Base Oil Production

- Others

- Segmentation By Process Unit

- Fluid Catalytic Cracking (FCC) and Residue FCC (RFCC) Units

- Diesel Hydrotreating Units

- Naphtha Hydrotreating Units

- Vacuum Gas Oil Hydrotreating and Hydrocracking Units

- Residue Hydrotreating and Hydrodesulfurization Units

- Continuous Catalytic Reforming (CCR) and Semi-Regenerative Reformer Units

- Isomerization Units

- Delayed Coking and Visbreaking Support Units

- Others

- Segmentation By Refinery Operator Type

- Public Sector Undertaking Refineries (IOC, BPCL, HPCL, NRL, CPCL, MRPL)

- Private Sector Refineries (Reliance Industries, Nayara Energy)

- Joint Venture Refineries (HPCL-Mittal Energy, ONGC Petro Additions)

- Others

- Segmentation By Catalyst Form

- Microspheroidal Particles (FCC Catalysts)

- Extrudate and Trilobe Pellets (Hydroprocessing Catalysts)

- Spherical Pellets (Reforming and Isomerization Catalysts)

- Powdered and Granular Forms

- Others

- Segmentation By Supply Model

- Direct Fresh Catalyst Supply

- Catalyst Lease and Exchange Programs

- Ex-Situ Catalyst Regeneration Services

- In-Situ Catalyst Regeneration and Rejuvenation Services

- Spent Catalyst Reclamation and Metals Recovery Services

- Integrated Catalyst Management and Technical Service Contracts

- Others

- Segmentation By Crude Slate Compatibility

- Light and Medium Sweet Crude Processing Catalysts

- Heavy and High-Sulfur Opportunity Crude Processing Catalysts

- High-Metals and High-Acid Crude Tolerance Catalyst Systems

- Others

- Segmentation By Region

- Western India (Gujarat, Mumbai, Rajasthan)

- Northern India (Panipat, Mathura, Barauni, Bongaigaon)

- Southern India (Kochi, Visakhapatanam, Chennai, Mangalore)

- Eastern India (Haldia, Paradip, Numaligarh)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Refinery Catalysts Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by catalyst type, application, process unit, and refinery operator type, to enable global and domestic catalyst manufacturers, technology licensors, refinery operators, and investors to identify which catalyst segments and refinery configurations will generate the highest absolute procurement volumes and the most durable demand growth across the forecast period?

- How are the ongoing capacity expansion programs at Indian public sector refineries including Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum, and the proposed greenfield Ratnagiri and Barmer refinery projects, expected to translate into incremental fresh catalyst demand volumes and procurement expenditure by process unit type and catalyst category through 2034, and what is the projected timeline and scale of major initial startup catalyst loading events associated with new refinery units entering service?

- How is the Indian refining industry’s progressive shift toward processing heavier and higher-metals opportunity crude grades reshaping the technical performance requirements, metals tolerance specifications, and procurement preferences of FCC catalyst, residue hydroprocessing catalyst, and metals passivation additive systems at major Indian refineries, and which global and domestic catalyst suppliers are best positioned to capture the growing opportunity crude processing catalyst demand through technically differentiated formulations with demonstrated field performance in comparable international refinery applications?

- What is the current state of domestic Indian refinery catalyst manufacturing capability, which catalyst categories are realistically addressable through indigenization programs supported by Indian government policy incentives and public sector R and D investment, what investment levels and technology development timelines are required to establish credible domestic manufacturing competency in FCC catalysts and advanced hydroprocessing catalysts, and how does the competitive landscape between imported and domestically produced catalyst formulations evolve through 2034 under different indigenization policy scenarios?

- Who are the leading global catalyst technology licensors and manufacturers, domestic Indian catalyst producers, and catalyst service companies currently supplying and supporting the India refinery catalysts market, and what are their respective product portfolios, technology licensing relationships with Indian refineries, manufacturing and supply chain infrastructure in India, technical service capabilities, spent catalyst reclamation service offerings, and strategic positioning in response to the structural growth opportunity presented by India’s refinery expansion and petrochemical integration investment pipeline through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil Price Volatility, Refinery Throughput Variability & Catalyst Demand Cyclicality Risk

- Raw Material Scarcity, Rare Earth & Precious Metal Price Volatility Risk for Catalyst Manufacturers

- Regulatory, BS VI & Clean Fuel Mandate Compliance Timeline & Reformulation Risk

- Technology Substitution, Catalyst Lifetime Extension & Regeneration Impact on Fresh Catalyst Demand Risk

- Import Dependency, China Supply Chain Concentration & Geopolitical Disruption Risk

- Regulatory Framework & Standards

- MoPNG Refinery Expansion Policy, Fuel Quality Upgradation Mandates & BS VI Implementation Framework

- BIS Standards, BPC & HPCL Product Quality Specifications Driving Catalyst Performance Requirements

- CPCB & MoEFCC Environmental Norms: SOx, NOx, Particulate & Spent Catalyst Waste Management Regulations

- DGFT Import Licensing, Customs Duty Structure & Anti-Dumping Regulations Applicable to Refinery Catalysts

- Green Hydrogen, Biofuel Blending & Renewable Fuel Policy Frameworks Creating New Catalyst Demand in Indian Refineries

- India Refinery Catalysts Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Catalyst Type

- Fluid Catalytic Cracking (FCC) Catalysts & Additives

- Hydroprocessing Catalysts (Hydrotreating & Hydrocracking)

- Catalytic Reforming Catalysts

- Alkylation Catalysts

- Isomerisation Catalysts

- Naphtha Reforming Catalysts

- Residue Upgradation & Delayed Coking Catalysts

- Polymerisation & Oligomerisation Catalysts

- Sulphur Recovery (Claus Process) Catalysts

- DeNOx (SCR) & SOx Reduction Catalysts

- Hydrogen Production (Steam Methane Reforming) Catalysts

- Lube Oil Processing Catalysts

- Market Size & Forecast by Refinery Process Unit

- Fluid Catalytic Cracking (FCC) Unit

- Hydrotreating Unit (Naphtha, Diesel & Residue Hydrotreaters)

- Hydrocracking Unit

- Catalytic Reforming Unit

- Isomerisation Unit

- Alkylation Unit

- Residue Desulphurisation (RDS) & Vacuum Residue Desulphurisation (VRDS) Unit

- Delayed Coking Unit

- Sulphur Recovery Unit (SRU)

- Hydrogen Generation Unit (HGU)

- Lube Oil Base Stock (LOBS) Processing Unit

- Market Size & Forecast by Catalyst Function

- Cracking Catalysts

- Hydrotreating & Desulphurisation Catalysts

- Reforming & Isomerisation Catalysts

- Hydrogenation Catalysts

- Dehydrogenation Catalysts

- Oxidation & Combustion Catalysts

- Emission Control & Flue Gas Treatment Catalysts

- Market Size & Forecast by Catalyst Form

- Powder & Microsphere Catalysts (FCC)

- Extrudate & Pellet Catalysts

- Sphere & Bead Catalysts

- Monolith & Structured Catalysts

- Market Size & Forecast by Catalyst Metal / Active Component

- Zeolite-Based Catalysts

- Molybdenum & Cobalt (CoMo) Based Catalysts

- Nickel & Molybdenum (NiMo) Based Catalysts

- Platinum & Palladium (Pt/Pd) Based Catalysts

- Nickel & Tungsten (NiW) Based Catalysts

- Rare Earth & Mixed Metal Oxide Catalysts

- Vanadium & Titanium Oxide Based Catalysts

- Market Size & Forecast by Catalyst Status

- Fresh / Virgin Catalyst

- Regenerated Catalyst

- Remanufactured & Rejuvenated Catalyst

- Market Size & Forecast by End-User

- Public Sector Refineries (IOC, BPCL, HPCL, NRL, CPCL, MRPL)

- Private Sector Refineries (Reliance Industries, Nayara Energy)

- Joint Venture & Upcoming Greenfield Refineries

- Petrochemical Integrated Refineries

- Market Size & Forecast by Sales Channel

- Direct Supply from Global Catalyst Manufacturer to Refinery

- Indian Distributor, Agent & Authorised Representative

- Long-Term Catalyst Supply & Performance Contract

- Catalyst Regeneration & Recycling Service Contract

- Western India Refinery Catalysts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Catalyst Type

- By Refinery Process Unit

- By Catalyst Function

- By End-User

- By Refinery / State

- By Sales Channel

- Market Size & Forecast

- Northern India Refinery Catalysts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Catalyst Type

- By Refinery Process Unit

- By Catalyst Function

- By End-User

- By Refinery / State

- By Sales Channel

- Market Size & Forecast

- Southern India Refinery Catalysts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Catalyst Type

- By Refinery Process Unit

- By Catalyst Function

- By End-User

- By Refinery / State

- By Sales Channel

- Market Size & Forecast

- Eastern & North-Eastern India Refinery Catalysts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Catalyst Type

- By Refinery Process Unit

- By Catalyst Function

- By End-User

- By Refinery / State

- By Sales Channel

- Market Size & Forecast

- Coastal & Export-Oriented Refinery Catalysts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Catalyst Type

- By Refinery Process Unit

- By Catalyst Function

- By End-User

- By Refinery / State

- By Sales Channel

- Market Size & Forecast

- Refinery-Wise* Catalysts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Catalyst Type

- By Refinery Process Unit

- By Catalyst Function

- By End-User

- By Refinery / State

- By Sales Channel

- Market Size & Forecast

- *Key Refineries Analyzed in the Syllogist Global Research Portfolio: IOC Panipat, IOC Mathura, IOC Barauni, IOC Guwahati, IOC Haldia, IOC Paradip, IOC Bongaigaon, IOC Digboi, BPCL Mumbai, BPCL Kochi, HPCL Mumbai, HPCL Visakhapatnam, CPCL Chennai, MRPL Mangalore, NRL Numaligarh, Reliance Jamnagar, Nayara Energy Vadinar

- Technology Landscape & Innovation Analysis

- Next-Generation FCC Catalyst & Additive Technology: High Octane, Maximum Propylene & Residue Cracking

- Ultra-Low Sulphur Diesel (ULSD) & BS VI Hydrotreating Catalyst Technology Deep-Dive

- Single-Stage & Two-Stage Hydrocracking Catalyst Technology for Middle Distillate Maximisation

- Continuous Catalytic Reforming (CCR) & Semi-Regenerative Reformer Catalyst Technology

- Residue Upgradation: RFCC, RDS, VRDS & Ebullated Bed Hydrocracking Catalyst Technology

- Catalyst Regeneration, Rejuvenation & Metals Reclamation Technology

- Green Hydrogen & Renewable Fuel (HVO, SAF) Catalyst Technology Emerging in Indian Refineries

- Patent & IP Landscape in Refinery Catalyst Technologies Relevant to India

- Value Chain & Supply Chain Analysis

- Catalyst Raw Material & Precursor Supply Chain: Rare Earths, Alumina, Zeolite & Precious Metals

- Catalyst Manufacturing, Calcination & Quality Control Supply Chain

- Catalyst Packaging, Drumming & Hazardous Goods Logistics Supply Chain

- Catalyst Distribution, Stocking & Authorised Representative Channel in India

- Refinery Catalyst Loading, Unloading & In-Situ Activation Services

- Spent Catalyst Collection, Metals Reclamation & Recycling Value Chain

- Catalyst Performance Monitoring, Technical Service & R&D Support Channel

- Pricing Analysis

- FCC Catalyst & Additive Unit Price, Consumption Rate & Total Cost per Barrel Analysis

- Hydrotreating & Hydrocracking Catalyst Capital Cost, Cycle Length & Replacement Cost Analysis

- Reforming & Isomerisation Catalyst Pricing: Precious Metal Loading & Lease vs. Purchase Model Analysis

- Regeneration vs. Fresh Catalyst Total Cost of Ownership (TCO) Comparison

- Import Tariff, Logistics Cost & Domestic Manufacturing Cost Comparison

- Total Refinery Catalyst Cost per Tonne of Crude Processed Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Refinery Catalysts: Carbon Footprint, Energy Intensity & Spent Catalyst Waste Generation

- Spent Catalyst Hazardous Waste Management, CPCB Compliance & Metals Reclamation Sustainability

- Catalyst Role in BS VI Fuel Quality Compliance: SOx, NOx & Particulate Emission Reduction Contribution

- Green Hydrogen, HVO & Sustainable Aviation Fuel (SAF) Catalyst Demand: Refinery Decarbonisation Pathway

- Regulatory-Driven Sustainability, SDG 13 (Climate Action) & SDG 9 (Industry & Innovation) Alignment & ESG Disclosure Requirements

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Catalyst Type & End-User)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Catalyst Type, Process Unit & Refinery

- Player Classification

- Global Integrated Refinery Catalyst Majors with India Supply Operations

- Specialist FCC Catalyst & Additive Manufacturers

- Hydroprocessing Catalyst Specialists

- Reforming & Isomerisation Catalyst Manufacturers

- Domestic Indian Catalyst Manufacturers & Formulators

- Catalyst Regeneration & Metals Reclamation Service Providers

- Catalyst Distributors & Authorised Representatives in India

- R&D Institutions & Public Sector Undertakings with Catalyst Development Capabilities

- Competitive Analysis Frameworks

- Market Share Analysis by Catalyst Type, Process Unit & Refinery

- Company Profile

- Company Overview & Headquarters

- Refinery Catalyst Products & Solutions Portfolio

- Key Customer Relationships & Reference Refinery Installations in India

- Manufacturing Footprint & Production Capacity

- Revenue (India Refinery Catalyst Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Catalyst Type, Process Unit, Catalyst Function, End-User & Refinery

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output