Market Definition

The India Fuel Additives Market encompasses the formulation, manufacturing, blending, supply, and application of specialty chemical compounds incorporated into petrol, diesel, aviation turbine fuel, compressed natural gas, liquefied petroleum gas, and alternative fuel streams at the refinery production stage, fuel terminal blending stage, and point-of-sale aftermarket retail level to enhance combustion performance, protect engine and fuel system components, meet mandatory fuel quality specifications, extend fuel storage stability, and reduce harmful exhaust emissions from the vehicle and equipment fleet operating across India’s transportation, agricultural, industrial, and power generation sectors. Fuel additives are performance-enhancing chemical substances added to hydrocarbon and alternative fuel bases at treat rates typically ranging from a few parts per million to several hundred parts per million by volume, whose precise chemical composition, molecular architecture, and concentration determine their functional effectiveness in modifying the physical, chemical, and combustion properties of the base fuel to which they are applied.

The market encompasses refinery-applied fuel additives including octane improvers and anti-knock agents for petrol, cetane improvers for diesel, lubricity additives compensating for the reduced natural lubricity of ultra-low sulfur diesel, antioxidants and metal deactivators for fuel oxidation stability, corrosion inhibitors for pipeline and storage tank protection, static dissipator additives, and detergent-dispersant packages maintaining fuel injector and intake valve cleanliness; terminal and distribution additives including flow improvers, wax anti-settling agents, demulsifiers, and marker dyes for fuel authentication; and aftermarket performance additives sold through automotive accessory retail channels for consumer application to vehicle fuel tanks, encompassing injector cleaners, combustion chamber deposit removers, fuel economy enhancers, smoke suppressants, and multi-functional fuel system treatment products. Key participants include global specialty additive companies, domestic Indian chemical manufacturers, petroleum refining companies blending additive packages into finished fuels, fuel marketing companies, and the downstream automotive aftermarket retail channel distributing consumer fuel additive products across India’s rapidly expanding vehicle ownership base.

Market Insights

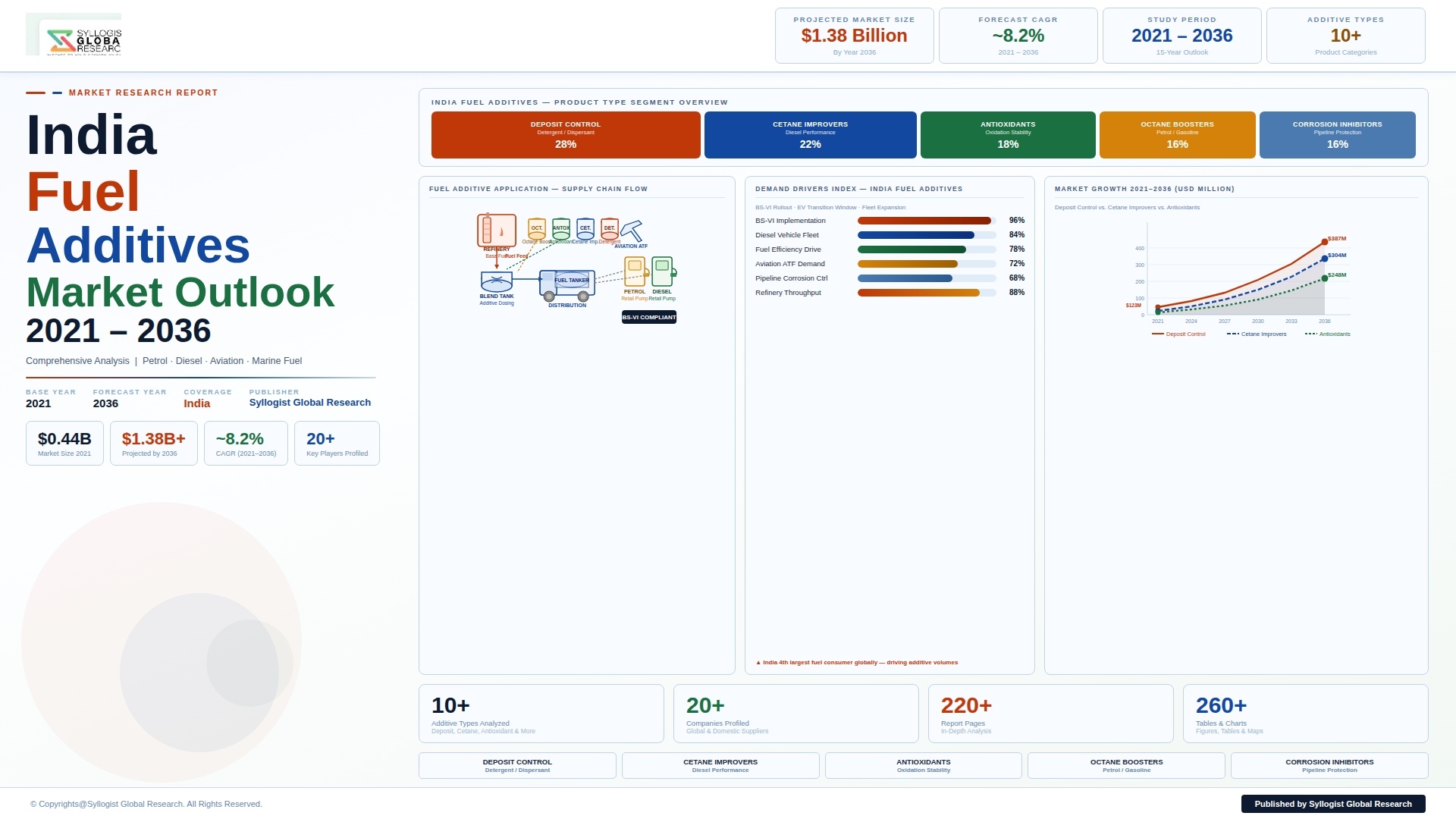

The India fuel additives market is experiencing a structurally favorable demand environment shaped by the intersection of four converging forces: the permanent elevation of fuel quality specifications enforced through the nationwide Bharat Stage VI implementation, the continuing rapid expansion of India’s vehicle parc across two-wheelers, passenger cars, and commercial vehicles driving total fuel consumption growth, the intensifying consumer and fleet operator awareness of fuel additive performance benefits for engine protection and fuel economy in the context of rising fuel prices, and the progressive replacement of older vehicle technology with modern direct injection gasoline and common rail diesel engine platforms whose tighter manufacturing tolerances and higher injection pressures create greater sensitivity to fuel deposit formation and lubricity inadequacy that makes additive treatment commercially compelling. The India fuel additives market was valued at approximately USD 480 million in 2025 and is projected to reach USD 810 million by 2034, advancing at a compound annual growth rate of 6.0% over the forecast period from 2027 to 2034, supported by growing refinery-applied additive volumes as Indian refineries process increasingly challenging crude slates requiring additive intervention to meet finished fuel specifications, and by the expansion of the organized aftermarket additive retail channel across India’s tier-2 and tier-3 cities driven by rising vehicle ownership and consumer fuel additive brand awareness.

Diesel fuel additives constitute the largest revenue segment of the India fuel additives market, reflecting the structural dominance of diesel as the primary transportation fuel for India’s commercial vehicle fleet, agricultural tractor and irrigation pump applications, and a substantial segment of the passenger car market, with total high-speed diesel consumption in India reaching approximately 97 billion liters in fiscal year 2024-25 and providing the largest single base fuel volume against which additive treat rates translate into absolute additive consumption volumes. The mandatory transition to Bharat Stage VI high-speed diesel with 10 parts per million sulfur has created a structurally permanent and commercially significant lubricity additive demand requirement at Indian refineries, as the hydrodesulfurization severity required to achieve ultra-low sulfur specifications strips the natural lubricity-providing polar compounds from the diesel fuel matrix, leaving BS VI diesel with inherently inadequate lubricity for protecting the precision-machined fuel injection system components of modern common rail diesel engines unless lubricity additives are incorporated at treat rates of 100 to 300 parts per million. Indian Oil Corporation, Bharat Petroleum, Hindustan Petroleum, and Nayara Energy each incorporate lubricity additive packages into their BS VI diesel production at their respective refineries and blending terminals, generating continuous and volume-significant lubricity additive procurement requirements that constitute a major demand anchor for the diesel additives segment of the Indian fuel additives market. The cetane improver segment, while smaller in absolute volume than lubricity additives, is growing at an above-average rate as Indian refineries blend increasing proportions of cracked distillate streams including light cycle oil and hydrocracker unconverted oil into the diesel pool to maximize distillate yield from the opportunity crudes they process, with these cracked components characteristically exhibiting lower natural cetane numbers than straight-run kerosene and diesel fractions, creating a recurring blending requirement for 2-ethylhexyl nitrate cetane improver to achieve the minimum 51 cetane number mandated by BS VI diesel specifications.

The petrol fuel additives segment is undergoing a qualitative transformation in its demand profile driven by the rapid growth in India’s passenger car fleet equipped with port fuel injection and gasoline direct injection engine technology, with the national passenger car fleet having surpassed 42 million registered vehicles in 2025 and adding approximately 4.1 million new passenger vehicles annually, the majority of which are equipped with modern fuel injection systems whose injector and intake valve deposit sensitivity creates ongoing demand for detergent-dispersant additive treatment in the petrol supply chain to protect engine performance, maintain fuel economy, and ensure emissions compliance across the vehicle service life. The premium petrol segment, represented by branded high-octane fuel products marketed by Indian Oil Corporation under the XtraMile brand, Bharat Petroleum under the Speed brand, and Hindustan Petroleum under the Power brand, incorporates proprietary multi-functional detergent additive packages at treat rates significantly above the minimum additive requirement, and these premium differentiated fuel products command a price premium of approximately INR 5 to INR 10 per litre above standard petrol while generating disproportionately higher additive consumption value per litre that benefits additive suppliers positioned in the premium fuel segment. The aftermarket petrol additive segment, addressing consumer demand for periodic fuel system cleaning treatments, octane booster products, and multi-function fuel conditioners available through automotive spare parts retailers, oil company retail outlets, and e-commerce platforms, is expanding at approximately 8.3% annually as rising vehicle ownership, increasing consumer awareness of engine maintenance benefits, and the growth of organized automotive retail distribution networks extend the commercial reach of branded aftermarket fuel additive products beyond India’s metropolitan markets into secondary cities and rural districts.

The aviation turbine fuel additive segment, while representing a smaller absolute market value compared to road transport fuel additives, occupies a strategically significant position within the India fuel additives market as India’s civil aviation sector experiences rapid passenger traffic growth that is driving ATF consumption toward approximately 8.2 billion liters annually by 2025 at a growth rate of approximately 9.1% per year, with ATF additives including thermal stability improvers, antioxidants, metal deactivators, static dissipator additives, icing inhibitors, lubricity improvers, and corrosion inhibitors representing technically exacting and specification-critical additive categories whose supply is governed by stringent international aviation fuel standards that constrain supplier qualification and additive product approval to a limited number of globally certified specialty chemical companies. The emerging demand for fuel additives compatible with sustainable aviation fuel blends, as Indian carriers and the Ministry of Civil Aviation advance toward the government’s target of 1% SAF blending in domestic aviation fuel by 2027 and 5% by 2030, is creating an additional technical requirement dimension for the Indian ATF additives market as additive performance in SAF-blended fuels must be independently validated given that the distinct molecular composition of SAF-derived fuel fractions can affect antioxidant consumption rates, thermal stability margins, and lubricity additive effectiveness relative to conventional Jet A-1 kerosene. The agricultural diesel and off-road equipment fuel additive segment represents a growing and commercially underserved market opportunity, with India’s 65 million registered tractors and several million diesel generator sets, irrigation pump sets, and construction equipment units consuming substantial volumes of high-speed diesel and agricultural pump sets diesel annually, and the progressive replacement of older mechanical injection systems with modern common rail and unit injection technology in agricultural and off-road equipment creating new deposit sensitivity and lubricity additive requirements in application environments that have historically received minimal additive treatment.

Key Drivers

Bharat Stage VI Fuel Quality Mandate Creating Structural and Permanent Demand for Lubricity, Cetane, and Detergent Additive Treatment Across Indian Refinery and Terminal Operations

The nationwide implementation of Bharat Stage VI fuel quality specifications in April 2020 represented the single most consequential regulatory event in the history of the India fuel additives market, permanently establishing additive treatment as a mandatory rather than discretionary component of Indian fuel blending across the petrol and diesel supply chains, and generating a structurally durable and growing annual additive procurement requirement at Indian refineries and blending terminals that did not exist at comparable technical and commercial scale under the preceding BS IV fuel quality framework. The reduction of diesel sulfur content from 50 parts per million under BS IV to 10 parts per million under BS VI mandates the incorporation of lubricity additives at every refinery and terminal blending point across India’s national fuel distribution network, as the hydrodesulfurization processing required to achieve 10 parts per million sulfur specifications eliminates the natural boundary film lubricity of diesel to levels that would cause accelerated wear of fuel injection pump and injector components in modern common rail diesel engines without compensating additive treatment. The BS VI petrol specifications, incorporating a maximum 1% benzene limit, a 35% maximum aromatics content, and a 10% maximum olefin content alongside the 10 parts per million sulfur ceiling, create a more constrained blending space for Indian refiners that increases the importance of octane improver additives and oxygenate blending to achieve the minimum 91 Research Octane Number required for standard petrol without relying on the aromatics and olefins that historically contributed octane value under lower-specification fuel regimes. The refinery-level additive treatment requirements established by BS VI specifications generate annual lubricity additive, cetane improver, antioxidant, and detergent package procurement commitments across Indian Oil Corporation’s eleven refineries, Bharat Petroleum’s three refineries, and Hindustan Petroleum’s two refineries that collectively represent the dominant share of organized sector fuel additive demand in the Indian market.

India’s Rapidly Expanding Vehicle Parc and the Growing Penetration of Modern High-Sensitivity Engine Technologies Intensifying Additive Demand Across Petrol and Diesel Segments

India’s vehicle ownership trajectory represents one of the most powerful structural demand drivers for fuel additives globally, with the total registered vehicle population having exceeded 340 million units in 2025, adding approximately 20 to 22 million new vehicles annually across two-wheelers, three-wheelers, passenger cars, and commercial vehicles, and with vehicle density per thousand population still substantially below global emerging market averages, implying that the Indian vehicle parc will continue to expand at robust rates through the forecast period as rising household incomes and improving rural road infrastructure extend vehicle ownership to a broader population base. The automotive technology upgrade cycle associated with BS VI compliance has simultaneously increased the fuel deposit sensitivity of the Indian vehicle fleet by installing fuel injection systems with tighter manufacturing tolerances and higher operating pressures that are more susceptible to performance degradation from injector deposit formation, intake valve fouling, and combustion chamber carbon accumulation than the carbureted and earlier-generation port fuel injection systems they have replaced, creating an expanding and technically motivated base of consumers and fleet operators for whom fuel detergent additive treatment offers a measurable and demonstrable engine performance and fuel economy benefit. The commercial vehicle segment, encompassing approximately 12 million registered trucks, buses, and light commercial vehicles in India consuming diesel fuel in high-mileage applications where injector deposit accumulation and fuel system wear directly translate into elevated maintenance costs and reduced operational reliability, represents a commercially significant and technically motivated segment for diesel fuel additive programs targeting fleet operators whose total cost of ownership accounting makes the economic case for premium additive-treated fuel or periodic fuel system treatment products financially compelling relative to the avoided maintenance expenditure.

Growing Ethanol Blending Program and Alternative Fuel Transition Creating New Additive Formulation Requirements Across the Indian Fuel Supply Chain

The Indian government’s Ethanol Blended Petrol programme, which achieved a national average blending level of approximately 15% ethanol in petrol during fiscal year 2024-25 and targets 20% ethanol blending by 2025-26, is generating a structurally new and commercially significant additive requirement dimension in the Indian petrol market, as high-ethanol blended petrol exhibits materially different fuel stability, phase separation susceptibility, corrosion activity toward fuel system materials, and vapour pressure characteristics relative to conventional petrol that necessitate the reformulation of antioxidant packages, corrosion inhibitor treatments, and co-solvent stabilizers specifically designed to maintain the performance and storage stability of ethanol blended petrol through the multi-stage Indian fuel distribution system from refinery gate to end consumer. The accelerated use of ethanol from domestic sugarcane and grain surplus sources in the petrol blend pool is requiring Indian refineries and blending terminals to incorporate phase separation inhibitors, metal deactivators specific to ethanol fuel mixtures, and modified antioxidant packages whose performance in high-ethanol fuel matrices has been validated against the distinct oxidative and corrosive chemistry of ethanol blends rather than simply applying additive formulations developed for conventional petrol. The government’s parallel push to expand compressed natural gas vehicle penetration through the city gas distribution network expansion program, the introduction of flex-fuel vehicle mandates for new two-wheelers, and the pilot deployment of hydrogen blended CNG fuel in select urban bus fleet applications is cumulatively expanding the variety of fuel types in active commercial use in India, each presenting distinct additive chemistry requirements for odorant treatment, corrosion protection, combustion enhancement, and storage stability management that collectively broaden the technical scope and commercial opportunity of the India fuel additives market beyond its historical hydrocarbon fuel base.

Key Challenges

Counterfeit and Substandard Fuel Additive Products in the Aftermarket Retail Channel Undermining Consumer Confidence and Market Quality Integrity

The India aftermarket fuel additive retail market is significantly impacted by the widespread availability of counterfeit, diluted, and substandard additive products sold through unorganized automotive spare parts markets, roadside fuel stations, and increasingly through unregulated e-commerce marketplace listings at price points substantially below those of genuine branded products, creating a market quality integrity challenge that undermines consumer confidence in fuel additive efficacy, erodes the commercial viability of legitimate branded additive suppliers investing in product development and quality assurance, and poses real risks of engine damage and fuel system malfunction to vehicle owners applying substandard chemical treatments to sensitive modern fuel injection systems. The absence of a mandatory product registration and quality certification framework specifically governing aftermarket fuel additive products sold to end consumers in India, comparable to the Bureau of Indian Standards certification requirements applicable to lubricating oils, means that the aftermarket fuel additive shelf space is accessible to any formulator or trader capable of packaging a liquid product in an automotive aftermarket container with performance claims that cannot be independently verified by consumers lacking access to fuel chemistry testing capabilities. The proliferation of counterfeit additive products is particularly concentrated in the two-wheeler fuel additive and diesel performance treatment segments, which together represent the highest volume aftermarket additive categories and whose consumer base in tier-2, tier-3, and rural markets has limited brand familiarity and price sensitivity that makes it susceptible to counterfeit products offering superficially similar packaging and performance claims to genuine branded products at significantly lower retail prices.

Raw Material Import Dependency and Specialty Chemical Intermediate Price Volatility Compressing Additive Manufacturer Margins

Indian fuel additive manufacturers, whether operating as domestic formulators or as local blending subsidiaries of global specialty chemical companies, are exposed to significant input cost volatility arising from their dependence on imported specialty chemical intermediates and active ingredient concentrates whose prices are governed by global petrochemical feedstock markets, manufacturing capacity utilization at a small number of concentrated global production sites, and foreign exchange fluctuations between the Indian rupee and major trading currencies that together create a structurally unpredictable cost base for fuel additive formulation businesses operating under the competitive pricing pressure of the Indian market. The key chemical intermediates for major fuel additive categories including polyisobutylene succinimide detergent packages, alkyl phenol ethoxylate-based antioxidants, fatty acid ester lubricity additives, and 2-ethylhexyl nitrate cetane improver are produced at scale by a limited number of global chemical manufacturers including BASF, Afton Chemical, Infineum, and Clariant, with limited domestic Indian production capability across most of these specialty intermediate categories, creating supply concentration risk and limited negotiating leverage for Indian additive formulators seeking competitive input material pricing. The rupee depreciation episodes experienced during periods of global financial market stress, most notably during the 2022 dollar strengthening cycle when the rupee weakened from approximately INR 74 to INR 83 per US dollar within a twelve-month period, materially increased the landed cost of imported additive intermediates at a time when competitive market pricing constraints and government-regulated pump prices limited the ability of additive formulators and fuel marketing companies to pass through the full input cost increase to downstream customers.

Fuel Adulteration and Malpractice in the Distribution Chain Distorting Additive Demand and Undermining Performance Additive Market Development

The persistent problem of fuel adulteration in segments of India’s fuel retail and distribution network, involving the blending of kerosene, solvent, and industrial naphtha into petrol and diesel at unauthorized mixing points within the distribution chain, directly undermines the effectiveness of performance additives incorporated into genuine fuel at the refinery and terminal blending stage by diluting additive concentrations below their functional treat rate thresholds, contaminating the fuel chemical environment with compounds that can deactivate or compete with additive active molecules, and creating consumer experiences of poor fuel performance and engine problems that are incorrectly attributed to the base fuel or additive treatment rather than to the adulteration that has occurred downstream of the legitimate blending operation. The economic incentive for fuel adulteration is structurally related to the differential between the subsidized retail price of kerosene historically distributed through the public distribution system and the market price of petrol and diesel, and while the progressive reduction of kerosene subsidies and the direct benefit transfer mechanism for LPG distribution have reduced the kerosene-to-diesel price differential that historically made adulteration economically attractive, unauthorized diversion and blending of industrial solvents, duty-free agricultural diesel, and bootleg naphtha continues to affect a meaningful proportion of fuel retail volume in certain geographic markets, particularly in rural and semi-urban areas with limited regulatory inspection coverage. Fuel marker and tracer additive technologies, which are incorporated into legitimate fuel supplies by oil marketing companies to enable adulteration detection at retail dispensing points, represent a growing specialized additive demand category that is directly stimulated by the adulteration challenge, but the overall impact of adulteration on the performance additive market is net negative in terms of consumer willingness to pay premium prices for high-quality additive-treated fuel products.

Market Segmentation

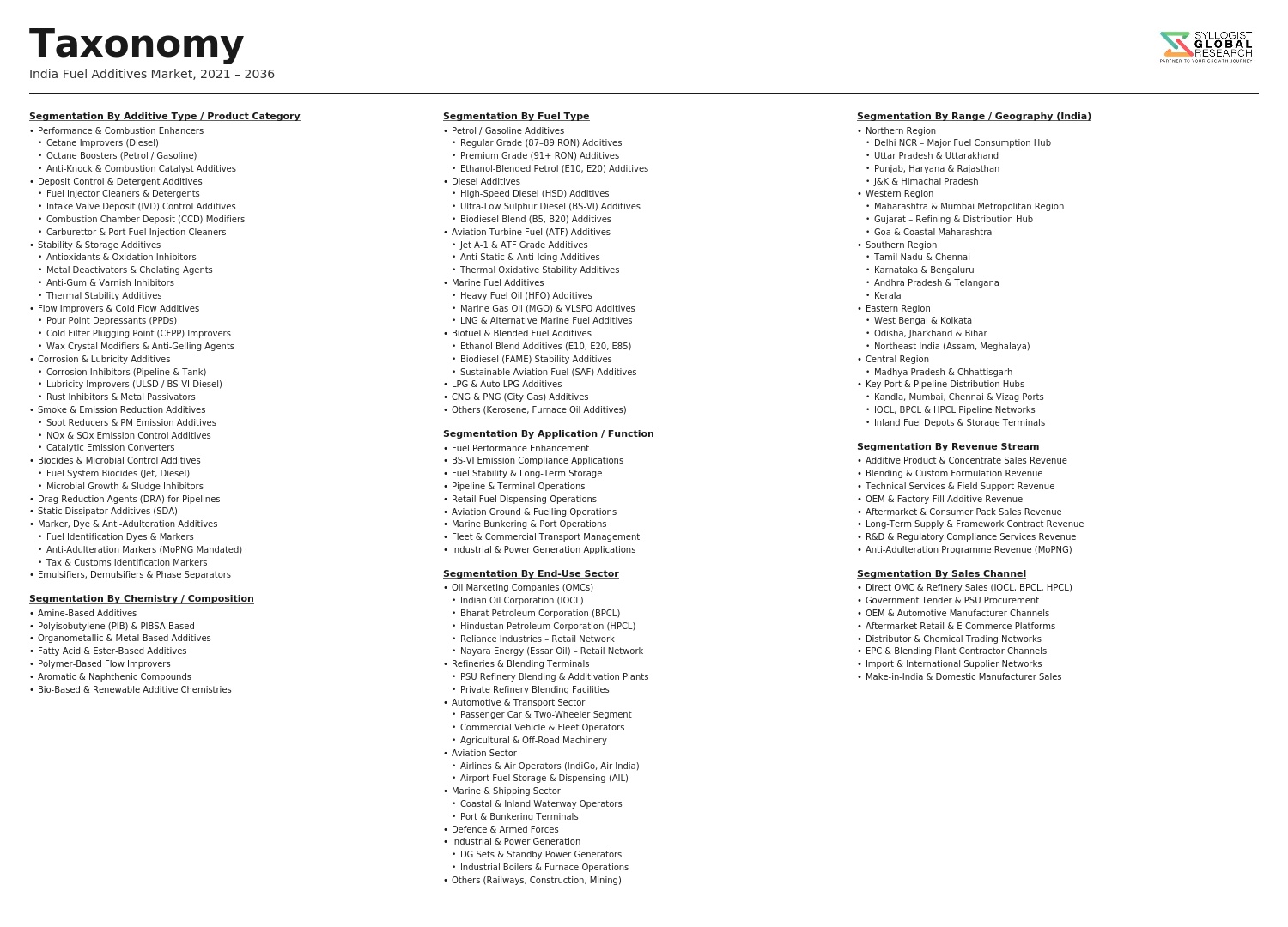

- Segmentation By Additive Type

- Detergent and Deposit Control Additives (Injector Cleaners, Intake Valve Deposit Inhibitors, Combustion Chamber Cleaners)

- Lubricity Additives (Fatty Acid Esters, Fatty Acid Amides)

- Cetane Improvers (2-Ethylhexyl Nitrate, Di-Tert-Butyl Peroxide)

- Octane Improvers and Anti-Knock Additives (MMT, Ferrocene, Oxygenates)

- Antioxidants and Stabilizers (Hindered Phenols, Phenylenediamines)

- Corrosion Inhibitors (Carboxylic Acid Derivatives, Amine-Based Inhibitors)

- Flow Improvers and Cold Flow Additives (Ethylene-Vinyl Acetate Copolymers, PIBSI)

- Static Dissipator Additives

- Demulsifiers and Water Separation Additives

- Thermal Stability and Antioxidant Additives for Aviation Turbine Fuel

- Marker Dyes and Fuel Authentication Additives

- Smoke Suppressants and Emission Reduction Additives

- Multi-Functional Additive Packages

- Others

- Segmentation By Fuel Type

- Petrol (Motor Spirit) Additives

- Diesel (High-Speed Diesel) Additives

- Aviation Turbine Fuel (ATF) Additives

- Compressed Natural Gas (CNG) Additives

- Liquefied Petroleum Gas (LPG) Additives

- Ethanol and Ethanol-Blended Petrol Additives

- Biodiesel and Biodiesel-Blended Diesel Additives

- Others

- Segmentation By Application Stage

- Refinery Production-Stage Additives

- Terminal and Pipeline Blending-Stage Additives

- Retail Fuel Station Point-of-Dispense Additives

- Aftermarket Consumer and Fleet Additives

- Others

- Segmentation By End-Use Sector

- Passenger Vehicles (Two-Wheelers, Three-Wheelers, Cars)

- Commercial Vehicles (Trucks, Buses, Light Commercial Vehicles)

- Agricultural Equipment (Tractors, Irrigation Pump Sets)

- Aviation and Aerospace

- Marine and Inland Waterway Transport

- Industrial Engines and Generators

- Construction and Off-Road Equipment

- Railways

- Others

- Segmentation By Distribution Channel

- Direct Supply to Oil Marketing Companies and Refineries

- Fuel Terminal and Blending Depot Supply

- Organized Automotive Retail (Franchised Dealers, OEM Accessories)

- Independent Automotive Spare Parts Retailers

- Fleet Operator Direct Supply Agreements

- E-Commerce and Online Retail Platforms

- Others

- Segmentation By Formulation Origin

- Domestically Formulated Additives (Indian Manufacturers)

- Imported Additive Concentrates and Finished Products

- Local Blending of Imported Active Ingredients

- Others

- Segmentation By Region

- Northern India (Delhi NCR, Uttar Pradesh, Punjab, Haryana)

- Western India (Maharashtra, Gujarat, Rajasthan)

- Southern India (Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala)

- Eastern India (West Bengal, Odisha, Bihar, Jharkhand)

- Central India (Madhya Pradesh, Chhattisgarh)

- Northeastern India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Fuel Additives Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by additive type, fuel type, application stage, and end-use sector, to enable global specialty chemical manufacturers, domestic additive formulators, oil marketing companies, and automotive aftermarket distributors to identify which additive product categories and fuel application segments will generate the highest absolute revenue and most sustained demand growth across the forecast period?

- How are the mandatory Bharat Stage VI fuel quality specifications governing sulfur content, lubricity, cetane number, octane rating, and detergency performance shaping the structured additive treatment requirements of Indian refineries and fuel terminal blending operations across the petrol and diesel supply chains, and what is the projected annual procurement volume and expenditure for each mandated additive category by oil marketing company and refinery through 2034 as total fuel throughput grows with India’s expanding vehicle parc and energy consumption?

- What is the projected impact of the Indian government’s Ethanol Blended Petrol programme achieving 20% blending targets, the expansion of compressed natural gas vehicle penetration through the city gas distribution network, and the introduction of flex-fuel vehicle mandates on the technical reformulation requirements, active ingredient specifications, and volume demand trajectories of petrol antioxidant, corrosion inhibitor, phase separation inhibitor, and multi-functional additive packages across the Indian fuel supply chain through 2034?

- How is the aftermarket fuel additive retail segment evolving in India across organized and unorganized distribution channels, what are the projected market volumes and value growth trajectories for petrol performance additives, diesel injector cleaners, and multi-function fuel treatment products sold through automotive retail, fuel station forecourt, and e-commerce channels through 2034, and what strategies are leading domestic and global branded additive companies deploying to compete with counterfeit and substandard products in price-sensitive tier-2 and tier-3 market segments?

- Who are the leading global specialty fuel additive companies, domestic Indian additive formulators, and oil marketing company captive additive blending operations currently defining the competitive landscape of the India fuel additives market, and what are their respective product portfolios, technical service capabilities, supply chain infrastructure, oil marketing company approval and qualification status, aftermarket brand presence, pricing strategies, and competitive positioning in response to the structural growth opportunity presented by India’s accelerating fuel quality upgrade trajectory and vehicle parc expansion through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil Price Volatility, Refinery Output Fluctuation & Fuel Additive Demand Cyclicality Risk

- BS VI & Future Emission Norm Reformulation, Additive Compatibility & Re-Qualification Risk

- Raw Material Price Volatility, Import Dependency & Chemical Feedstock Supply Chain Risk

- Electric Vehicle Adoption, Alternative Fuel Penetration & Long-Term Fossil Fuel Demand Erosion Risk

- Regulatory, BIS Compliance, Adulteration Control & Counterfeit Additive Market Risk

- Regulatory Framework & Standards

- BS VI Fuel Quality Standards, MoPNG Notification & Auto Fuel Policy Framework Governing Fuel Additive Use in India

- BIS Standards (IS 1447, IS 2796 & Related Specifications) & Bureau of Indian Standards Certification for Fuel Additives

- CPCB & MoEFCC Vehicular Emission Norms, Fuel Efficiency Regulations & Environmental Compliance Requirements

- Petroleum & Explosives Safety Organisation (PESO) Regulations for Additive Handling, Storage & Transportation

- FSSAI, Adulteration Control & Petroleum Act Provisions Governing Fuel Additive Addition at Retail & Bulk Supply Points

- India Fuel Additives Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Additive Type

- Deposit Control & Detergent Additives

- Antioxidants & Stability Additives

- Corrosion Inhibitors

- Lubricity Improvers

- Cold Flow Improvers & Pour Point Depressants

- Cetane Improvers

- Octane Boosters & Anti-Knock Additives

- Demulsifiers & Water Separating Additives

- Antistatic Additives

- Dyes, Markers & Identification Additives

- Multifunctional Fuel Additive Packages

- Biocides & Microbial Growth Inhibitors for Fuel

- Market Size & Forecast by Fuel Type

- Motor Spirit (Petrol / Gasoline) Additives

- High Speed Diesel (HSD) Additives

- Aviation Turbine Fuel (ATF) Additives

- Marine Fuel & Bunker Fuel Additives

- Compressed Natural Gas (CNG) & Liquefied Natural Gas (LNG) Additives

- Ethanol Blend & Flex-Fuel Additives

- Biodiesel & FAME Blend Additives

- Market Size & Forecast by Application

- Refinery & Terminal Blending (Bulk Additive Dosing at Point of Production)

- Pipeline & Storage Terminal Additive Injection

- Retail Outlet & Pump Additive Dosing

- Aftermarket & Consumer Fuel Additive Treatment

- Fleet & Commercial Vehicle Bulk Fuel Treatment

- Aviation Fuel Handling & Fuelling Infrastructure Treatment

- Market Size & Forecast by End-User

- Public Sector Oil Marketing Companies (IOC, BPCL, HPCL)

- Private Refineries & Fuel Marketers (Reliance, Nayara Energy)

- Aviation Fuel Suppliers & Airport Operators

- Fleet Operators, Transport & Logistics Companies

- Automotive OEMs & Authorised Service Networks

- Industrial & Agricultural Equipment Operators

- Retail Consumers & Passenger Vehicle Owners

- Market Size & Forecast by Sales Channel

- Direct Supply to Oil Marketing Companies & Refineries

- Authorised Distributor & Stockist Network

- Automotive Spare Parts & Lubricant Retail Channel

- E-Commerce & Online Retail Channel

- Integrated Additive Supply & Technical Service Contract

- Northern India Fuel Additives Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Additive Type

- By Fuel Type

- By Application

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Western India Fuel Additives Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Additive Type

- By Fuel Type

- By Application

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Southern India Fuel Additives Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Additive Type

- By Fuel Type

- By Application

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Eastern India Fuel Additives Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Additive Type

- By Fuel Type

- By Application

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- Central India Fuel Additives Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Additive Type

- By Fuel Type

- By Application

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- State-Wise* Fuel Additives Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Additive Type

- By Fuel Type

- By Application

- By End-User

- By State / Zone

- By Sales Channel

- Market Size & Forecast

- *Key States & Union Territories Analyzed in the Syllogist Global Research Portfolio: Maharashtra, Gujarat, Rajasthan, Delhi NCT, Uttar Pradesh, Punjab, Haryana, Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala, West Bengal, Odisha, Madhya Pradesh, Chhattisgarh, Bihar, Jharkhand, Assam

- Technology Landscape & Innovation Analysis

- Next-Generation Deposit Control & Intake Valve Deposit (IVD) Prevention Additive Technology for BS VI Petrol & Diesel

- Advanced Cold Flow Improver & Wax Anti-Settling Additive Technology for Indian Diesel Grades

- Cetane Improver & Diesel Combustion Efficiency Additive Technology Deep-Dive

- Ethanol & Biofuel Blend Compatibility Additive Technology: Corrosion Inhibition, Phase Separation & Stability

- Multifunctional Fuel Additive Package Formulation Technology for Petrol & Diesel Performance Enhancement

- Fuel Dye, Marker & Anti-Adulteration Additive Technology for Regulatory Compliance in India

- Digital Dosing, Additive Injection Monitoring & Fuel Quality Assurance Technology at Terminals & Depots

- Patent & IP Landscape in Fuel Additive Technologies Relevant to India

- Value Chain & Supply Chain Analysis

- Petrochemical & Specialty Chemical Feedstock & Raw Material Supply Chain for Fuel Additives

- Fuel Additive Active Ingredient Synthesis & Intermediate Manufacturing Supply Chain

- Additive Blending, Package Formulation & Quality Control Supply Chain in India

- Bulk Packaging, Drumming & Hazardous Chemical Logistics Supply Chain

- Oil Marketing Company & Refinery Direct Supply & Tender Channel

- Distributor, Dealer & Retail Aftermarket Channel

- Waste & Off-Specification Additive Treatment & Disposal Value Chain

- Pricing Analysis

- Deposit Control & Detergent Additive Pricing: Treat Rate, Dosage Cost & Value-in-Use Analysis

- Cetane Improver & Cold Flow Improver Unit Price & Treat Cost per Litre of Diesel Analysis

- Multifunctional Additive Package Pricing: Petrol vs. Diesel Cost Comparison

- Aftermarket Consumer Additive Retail Pricing vs. Bulk Supply Pricing Analysis

- Import vs. Domestic Manufacturing Cost Comparison & Make-in-India Premium Analysis

- Total Fuel Additive Cost per Litre of Finished Fuel Analysis across Fuel Types

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Fuel Additives: Carbon Footprint, Toxicity & Biodegradability Across Additive Categories

- Fuel Additive Contribution to BS VI Vehicular Emission Compliance: NOx, PM, HC & CO Reduction Benefits

- Biofuel Blend Additive Role in India’s Ethanol Blending Programme (EBP) & Biodiesel Policy

- Green Chemistry & Bio-Based Fuel Additive Innovation: Renewable Feedstock & Low-Toxicity Formulations

- Regulatory-Driven Sustainability, SDG 7 (Affordable Energy), SDG 13 (Climate Action) & ESG Disclosure Alignment for Fuel Additive Suppliers

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Additive Type & End-User)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Additive Type, Fuel Type & Channel

- Player Classification

- Global Integrated Fuel Additive Majors with India Operations

- Domestic Indian Fuel Additive Manufacturers & Formulators

- Specialty Chemical Companies with Fuel Additive Divisions

- Oil Marketing Company In-House Additive Blending & Procurement Units

- Aftermarket & Consumer Fuel Additive Brands

- Fuel Additive Distributors, Stockists & Trading Companies

- Emerging Bio-Based & Green Fuel Additive Start-Ups

- Additive Dosing Equipment & Injection System Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Additive Type, Fuel Type & Sales Channel

- Company Profile

- Company Overview & Headquarters

- Fuel Additive Products & Solutions Portfolio

- Key Customer Relationships & Reference Accounts in India

- Manufacturing Footprint & Production Capacity in India

- Revenue (India Fuel Additive Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Product Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Additive Type, Fuel Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output