Market Definition

The South-East Asia Smart Water Purifier Market encompasses the design, manufacturing, distribution, installation, and after-sales servicing of internet-connected, sensor-integrated, and AI-enabled residential and commercial water purification systems that deliver real-time water quality monitoring, filter life management, usage analytics, remote diagnostics, and automated operational control through smartphone applications, voice assistant integration, and cloud-based data platforms, distinguishing smart purifiers from conventional filtration devices by their continuous digital intelligence layer that transforms passive water treatment into an actively managed household utility service across the urban and emerging middle-class consumer markets of Indonesia, Vietnam, Thailand, Malaysia, the Philippines, Singapore, and Myanmar. Smart water purifiers combine established water purification technologies including reverse osmosis membrane filtration, ultrafiltration, activated carbon adsorption, UV sterilization, and multi-stage sediment filtration with embedded IoT sensor arrays measuring turbidity, total dissolved solids, pH, chlorine residual, temperature, and flow rate parameters that collectively characterize source water quality and treatment system performance in real time.

The market encompasses countertop and under-sink smart RO and UF purifier systems for residential kitchen applications; whole-house smart filtration systems monitoring water quality at the building entry point; smart water dispenser and hot-cold purifier systems integrating heating and cooling with digital management; commercial smart purification systems serving offices, food service establishments, hotels, educational institutions, and healthcare facilities; and the digital service ecosystem including filter subscription and replacement programs delivered through IoT-enabled auto-replenishment, remote technician diagnostics reducing unnecessary service visits, and water quality data dashboards providing household and building managers with longitudinal drinking water safety records. Key participants include multinational consumer appliance companies with smart purifier product lines, domestic smart home technology companies integrating water purification with broader IoT home ecosystems, water treatment technology specialists expanding into connected product categories, e-commerce platforms driving direct-to-consumer smart purifier sales, and the water filter replacement subscription service providers whose recurring revenue models align commercial incentives with sustained consumer water quality outcomes across the South-East Asian markets where safe drinking water accessibility, rising household income, and smartphone penetration collectively create the consumer demand foundation for smart water purification adoption.

Market Insights

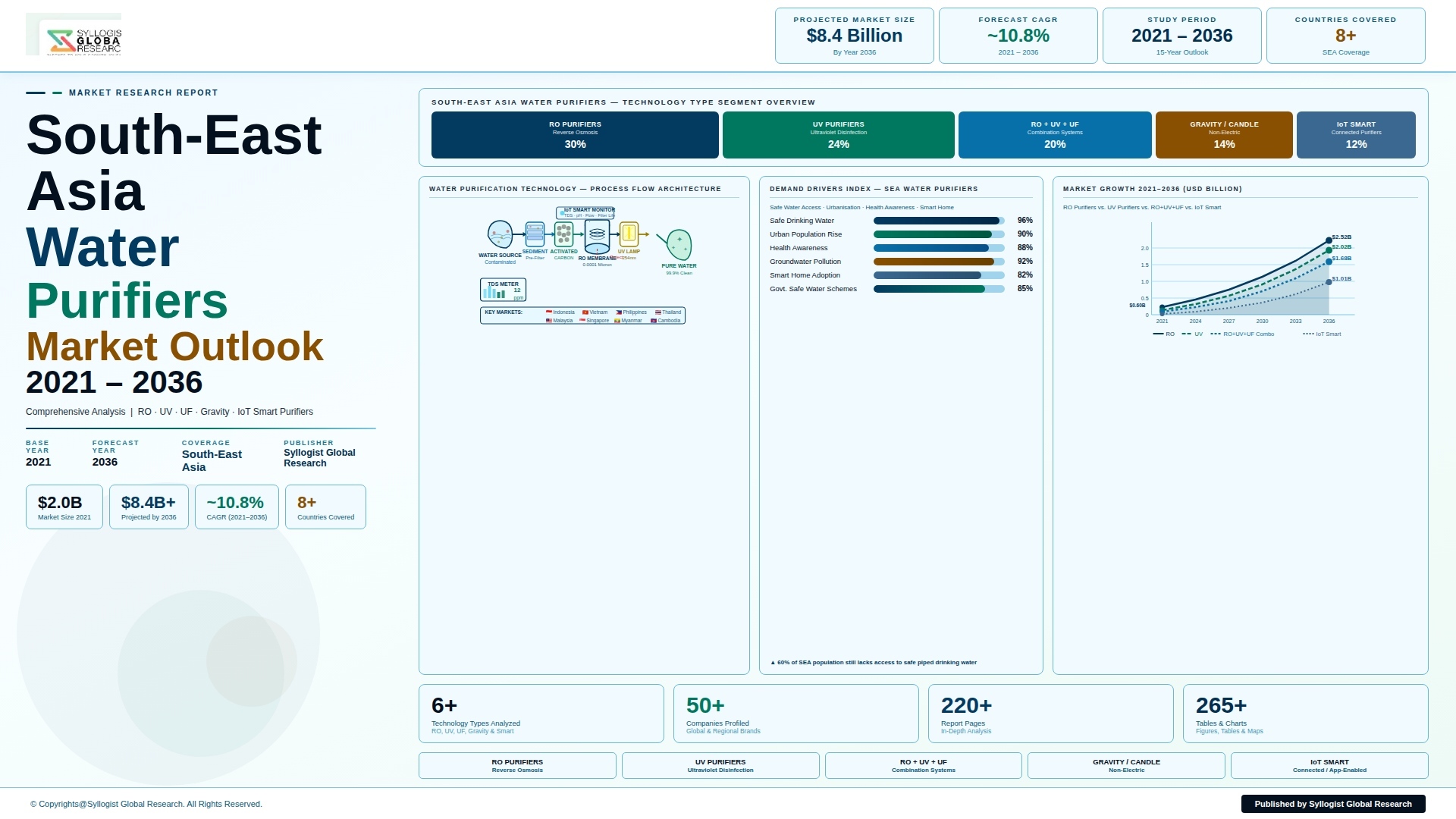

The South-East Asia smart water purifier market is experiencing a structural demand inflection driven by the convergence of persistently inadequate municipal water supply quality across the region’s rapidly urbanizing population centers, the extraordinary penetration of smartphone ownership and digital consumer services that has created the device and behavioral infrastructure for connected home appliance adoption, and the rising middle-class household aspiration for premium home technology that visibly improves family health and lifestyle quality in ways that are immediately demonstrable through digital water quality dashboards and safety certifications. The South-East Asia smart water purifier market was valued at approximately USD 1.4 billion in 2025 and is projected to reach USD 3.8 billion by 2034, advancing at a compound annual growth rate of 11.6% over the forecast period from 2027 to 2034, driven by the rapid expansion of smart purifier product availability and consumer awareness across Indonesia and Vietnam’s rapidly growing urban middle class, the premium appliance segment growth of Thailand and Malaysia whose higher household income levels support the price point of IoT-integrated purifier systems, and the progressive adoption of filter subscription and smart service models that transform purifier hardware sales into recurring service revenue streams generating long-term customer relationship value for manufacturers and distributors operating across the region.

Indonesia represents the largest and most commercially dynamic single country market within South-East Asia for smart water purifiers, driven by the combination of the world’s fourth-largest national population, a rapidly expanding urban middle class whose household income growth is driving premium appliance adoption across air conditioning, smart televisions, and water purification categories simultaneously, and a chronic municipal water supply quality challenge in Jakarta, Surabaya, Bandung, and secondary cities where pipe corrosion, contamination incidents, and treatment inconsistency generate persistent consumer anxiety about tap water safety that makes point-of-use purification a high-priority household investment. Indonesian smart water purifier penetration in the urban household segment reached approximately 8.3% in 2025, a level that remains significantly below the 25% to 35% penetration achieved in urban China and South Korea for smart purifier or advanced water purifier categories, indicating substantial adoption headroom whose capture will be driven by the combined forces of household income growth, product price reduction through manufacturing scale, e-commerce accessibility improvement, and growing consumer evidence of waterborne illness risk from unfiltered tap water consumption. The e-commerce channel has emerged as the dominant smart purifier distribution pathway in Indonesia, with Tokopedia, Shopee Indonesia, and Lazada Indonesia together generating approximately 54% of smart purifier unit sales in 2025 as consumer comfort with high-value appliance purchase through digital channels has grown with improved logistics reliability, comprehensive return policies, and manufacturer-direct brand store credibility on major marketplace platforms whose product authenticity guarantees address the counterfeit product concern that previously constrained premium appliance online purchase in the Indonesian market.

Vietnam is experiencing the most rapid smart water purifier adoption rate growth in South-East Asia, driven by the country’s extraordinary economic development trajectory that has elevated per capita income from approximately USD 2,800 in 2015 to approximately USD 4,600 in 2025 and is expanding the middle-class consumer segment accessible to premium home appliance products at a pace that is attracting substantial investment from multinational and domestic smart purifier brands seeking first-mover brand positioning in a rapidly growing market. Vietnam’s water quality challenge is structurally distinct from Indonesia’s in being concentrated in groundwater contamination from agricultural runoff, industrial discharge, and arsenic naturally occurring in Mekong Delta aquifer systems, creating a specific need for RO membrane filtration technology rather than the activated carbon and UV systems adequate for treated municipal water improvement, and generating consumer demand for smart purifiers with TDS monitoring capabilities that provide visible evidence of dissolved mineral and contaminant removal that reassures households dependent on locally variable groundwater sources. The smart purifier commercial ecosystem in Vietnam has benefited significantly from the entry of Chinese smart purifier manufacturers including Xiaomi through its Mi Water Purifier line, QNAP, and Haier whose competitive pricing strategies and e-commerce distribution through Shopee Vietnam and Lazada Vietnam have brought IoT-connected purifier technology to accessible price points of USD 80 to USD 200 for entry-level smart RO systems that compare favorably against the USD 350 to USD 600 price range of the Korean and Japanese smart purifier brands that previously defined the premium segment of the Vietnamese water purifier market.

The smart service and filter subscription business model, pioneered in South-East Asia by Coway’s rental and subscription model operating in Malaysia and Singapore and increasingly adopted by emerging regional players in Indonesia, Thailand, and Vietnam, represents the most commercially disruptive innovation reshaping the smart water purifier market’s competitive dynamics and unit economics by converting the traditionally lumpy capital expenditure of purifier hardware purchase into predictable monthly subscription payments that include hardware, filter replacement, maintenance visits, and water quality monitoring services at prices of USD 10 to USD 35 per month accessible to households whose capital budget constraints preclude upfront hardware investment but whose monthly income supports ongoing service subscription expenditure. The IoT connectivity embedded in smart purifier systems is commercially essential to the subscription model’s operational viability, as real-time filter saturation monitoring through TDS sensor arrays and flow rate tracking enables service providers to dispatch filter replacement technicians precisely when replacement is warranted rather than on fixed calendar schedules, reducing unnecessary service visits, eliminating prematurely replaced filters, and preventing the service lapses that previously generated customer complaints and subscription cancellations under calendar-based maintenance programs. Thailand and Malaysia represent the most commercially mature smart water purifier markets within South-East Asia in terms of premium product penetration, subscription model adoption, and consumer willingness to pay for connected water quality management services, with Bangkok and Kuala Lumpur households demonstrating smart purifier ownership rates of approximately 18% and 22% respectively among middle and upper-middle income urban households, providing commercial proof-of-concept evidence for the subscription and premium smart purifier business models that manufacturers are seeking to replicate across the broader South-East Asian market at lower price points accessible to the larger emerging middle-class consumer populations of Indonesia, Vietnam, and the Philippines.

Key Drivers

Persistent Municipal Water Quality Deficiencies and Consumer Health Awareness Driving Household Water Purification Investment Across South-East Asian Urban Markets

The structural inadequacy of piped municipal water supply quality across South-East Asia’s major urban centers, where aging distribution infrastructure, inadequate treatment capacity relative to population growth, industrial and agricultural contamination of source water, and inconsistent chlorination and chemical treatment practices collectively generate tap water quality that is widely regarded by regional consumers as unsafe for direct consumption without additional point-of-use treatment, creates a persistent and commercially powerful demand driver for water purification products whose relevance and urgency is continuously reinforced by media coverage of water contamination incidents, government advisories regarding tap water quality, and the lived experience of households whose unfiltered water consumption has been associated with gastrointestinal illness, dental health concerns, and aesthetic taste and odor complaints. The World Health Organization’s documented disease burden attributable to unsafe drinking water in South-East Asia, which accounts for a disproportionate share of childhood diarrheal illness, waterborne hepatitis A and E, and cholera outbreak incidence in the region, provides a public health evidence base whose communication through media, healthcare provider recommendation, and social media discussion progressively translates into household health consciousness that makes water purification investment a perceived family health protection priority rather than a discretionary lifestyle purchase. The growing consumer awareness of specific water contaminants including arsenic in Mekong Delta groundwater, heavy metals from industrial discharge into urban water sources in Vietnam and Indonesia, microplastic particles increasingly detected in treated municipal water supplies, and emerging contaminants including pharmaceutical residues that conventional municipal treatment does not fully remove, is creating demand for smart purifiers whose multi-parameter sensor suites provide visible reassurance of contaminant removal that single-technology conventional purifiers cannot document with equivalent digital transparency.

South-East Asia Smartphone Penetration and Smart Home Ecosystem Expansion Creating Consumer Readiness for IoT-Connected Home Appliance Adoption

South-East Asia has achieved among the world’s highest smartphone penetration growth rates over the past decade, with smartphone ownership reaching approximately 78% of the adult population across the six largest ASEAN economies in 2025 and mobile internet connectivity driving the region’s consumer adoption of digital services across e-commerce, digital banking, ride-hailing, and food delivery at adoption rates and speed that have consistently exceeded Western market precedents, creating a digitally literate and app-native consumer population whose comfort with smartphone-mediated device management makes the connectivity features of smart water purifiers a genuinely valued rather than merely marketed product differentiator. The rapid adoption of smart home ecosystems in South-East Asian urban households, driven by the market entry of affordable smart home platforms including Xiaomi Home, Samsung SmartThings, and Google Home alongside regional ecosystem developers in Indonesia and Thailand, is creating a smart home appliance adoption wave whose participants have demonstrated willingness to integrate multiple connected devices including smart speakers, smart lighting, smart air conditioners, and smart appliances into a unified digital home management experience, generating natural demand for smart water purifiers as a logical health-focused addition to the connected home appliance portfolio. The voice assistant integration capabilities increasingly embedded in South-East Asian smart purifier products, enabling water quality status queries, filter change reminders, and purification parameter adjustments through Google Assistant and Amazon Alexa voice commands in English, Bahasa Indonesia, Thai, and Vietnamese language support, create a hands-free interaction convenience that resonates particularly strongly with the young professional and dual-income household demographics who constitute the primary smart purifier adopter segment across the region’s tier-1 and tier-2 urban markets.

Rising Household Income and Health Expenditure Prioritization Among South-East Asian Middle-Class Consumers Elevating Smart Purifier Affordable Premium Positioning

The rapid income growth of South-East Asia’s emerging middle class, whose collective spending power is expanding as regional GDP per capita rises across Indonesia, Vietnam, the Philippines, and Thailand at rates substantially above global emerging market averages, is progressively expanding the consumer population capable of affording smart water purifier products whose price points have simultaneously been declining through Chinese manufacturing scale and supply chain efficiency, creating an accessibility convergence between rising consumer purchasing power and falling product prices that is the primary structural driver of smart purifier volume adoption growth across the region’s emerging urban middle-class markets. The health and wellness expenditure category has emerged as a priority spending domain among South-East Asian middle-class households, with consumer survey evidence across Indonesia, Vietnam, and Thailand consistently indicating that health-related home equipment including air purifiers, water purifiers, and health monitoring devices receive budget priority above discretionary entertainment and lifestyle expenditure among households with monthly incomes above USD 500 to USD 800, creating a commercially favorable consumer spending priority structure that shields smart water purifier demand from the discretionary spending retrenchment that affects lower-priority consumer categories during economic uncertainty. The parenting motivation dimension of smart water purifier adoption is commercially significant across South-East Asian markets where strong family health investment motivation drives consumer decisions, with market data indicating that households with children under 12 years demonstrate smart purifier adoption rates approximately 2.4 times higher than equivalent income households without children, as the perceived health vulnerability of young children to waterborne contaminants and the documentary proof of safe water quality provided by smart purifier digital dashboards align directly with parental health protection motivations.

Key Challenges

Consumer Price Sensitivity and Competitive Low-Cost Conventional Purifier Alternatives Limiting Smart Premium Adoption Beyond Affluent Urban Segments

The smart water purifier market in South-East Asia is significantly constrained by the price sensitivity of the large majority of the regional consumer population whose household income levels, while growing, remain below the threshold at which the USD 150 to USD 600 price premium of smart IoT-connected purifiers over functionally equivalent conventional filtration alternatives is commercially justifiable on perceived value grounds when the primary consumer objective is safe drinking water access rather than digital water quality monitoring and remote management sophistication. The availability of non-smart RO and UV purifiers at price points of USD 40 to USD 120 from Chinese and domestic manufacturers across Indonesia, Vietnam, and the Philippines creates a formidable low-cost competition challenge for smart purifier brands whose IoT feature premium requires consumer education and digital lifestyle aspiration motivation to justify at income levels where household appliance investment is driven primarily by functional necessity rather than premium feature differentiation. The after-sales service infrastructure challenge is particularly acute in South-East Asia’s secondary and tertiary cities and rural areas where the filter replacement, membrane servicing, and IoT connectivity troubleshooting requirements of smart purifier ownership demand a dense and technically capable service network whose establishment and maintenance cost creates a commercial barrier to smart purifier brand expansion beyond the tier-1 city core markets where service infrastructure investment can be justified by adequate installed base density, limiting addressable market coverage to a fraction of the total regional purifier market geography.

Inconsistent Internet Connectivity and IoT Infrastructure Reliability in Secondary Urban and Rural Markets Limiting Smart Feature Utility

The commercial proposition of smart water purifiers, whose differentiated value relative to conventional purifiers is entirely dependent on reliable internet connectivity enabling real-time water quality data transmission, smartphone app remote monitoring, cloud-based filter life analytics, and automated service scheduling, is materially compromised in South-East Asian market geographies where residential broadband and mobile internet connectivity remains unreliable, intermittent, or economically inaccessible, creating a smart feature utility gap between tier-1 city consumers who experience the full connected functionality for which they pay a premium and secondary market consumers whose smart purifier operates in effectively dumb mode for significant proportions of its operational time due to connectivity limitations beyond the consumer’s control. The heterogeneity of IoT infrastructure across South-East Asian national markets, where Singapore’s world-class fiber optic and 5G connectivity coexists with the patchy rural broadband coverage of Indonesia’s archipelago and the developing mobile internet infrastructure of Myanmar and Cambodia, requires smart purifier manufacturers to design products with robust offline functionality and graceful connectivity degradation capabilities whose engineering investment adds development cost and complexity relative to platforms designed for consistently connected operating environments. The data privacy regulatory environment governing IoT device data collection and cloud processing in South-East Asia, while less restrictive than European GDPR standards, is evolving through national personal data protection legislation in Thailand, Indonesia, Malaysia, and the Philippines whose compliance requirements for household IoT device operators including water quality data retention, cross-border data transfer consent, and device security certification add regulatory compliance cost and product development timeline complexity to smart purifier market entry and commercial scaling programs.

After-Sales Service Infrastructure Gaps and Filter Replacement Supply Chain Inconsistency Undermining Long-Term Consumer Satisfaction and Subscription Model Viability

The long-term commercial success of smart water purifier adoption in South-East Asia is critically dependent on the reliability of filter replacement supply chains and after-sales service networks that maintain purification performance and consumer confidence throughout the product ownership lifecycle, yet the regional after-sales infrastructure for water purifier servicing remains fragmented, geographically uneven, and technically inconsistent across the diverse market geographies where smart purifier adoption is growing, creating post-purchase consumer experience gaps that generate negative word-of-mouth, elevated subscription cancellation rates, and brand reputation damage that undermine the category growth momentum established by initial product adoption. The genuine filter replacement supply chain challenge, where substandard or counterfeit filter cartridges are widely available through unorganized retail channels at price discounts of 30% to 60% below genuine manufacturer replacements, creates an ongoing consumer decision point at each filter replacement cycle where cost-driven substitution of non-genuine filters compromises purification performance, potentially voids product warranties, and generates the consumer disappointment and health concern incidents that damage both individual brand reputations and broader smart purifier category credibility across the South-East Asian market. The technician training and certification gap within regional appliance service ecosystems, where the IoT diagnostic, membrane replacement, and sensor calibration technical requirements of smart purifier servicing exceed the competency of general appliance repair technicians trained on conventional water filter maintenance, creates service quality inconsistency that directly affects consumer satisfaction with subscription-based smart purifier service programs whose premium pricing relative to self-maintained conventional purifiers must be continuously justified through demonstrably superior service quality and water safety outcomes.

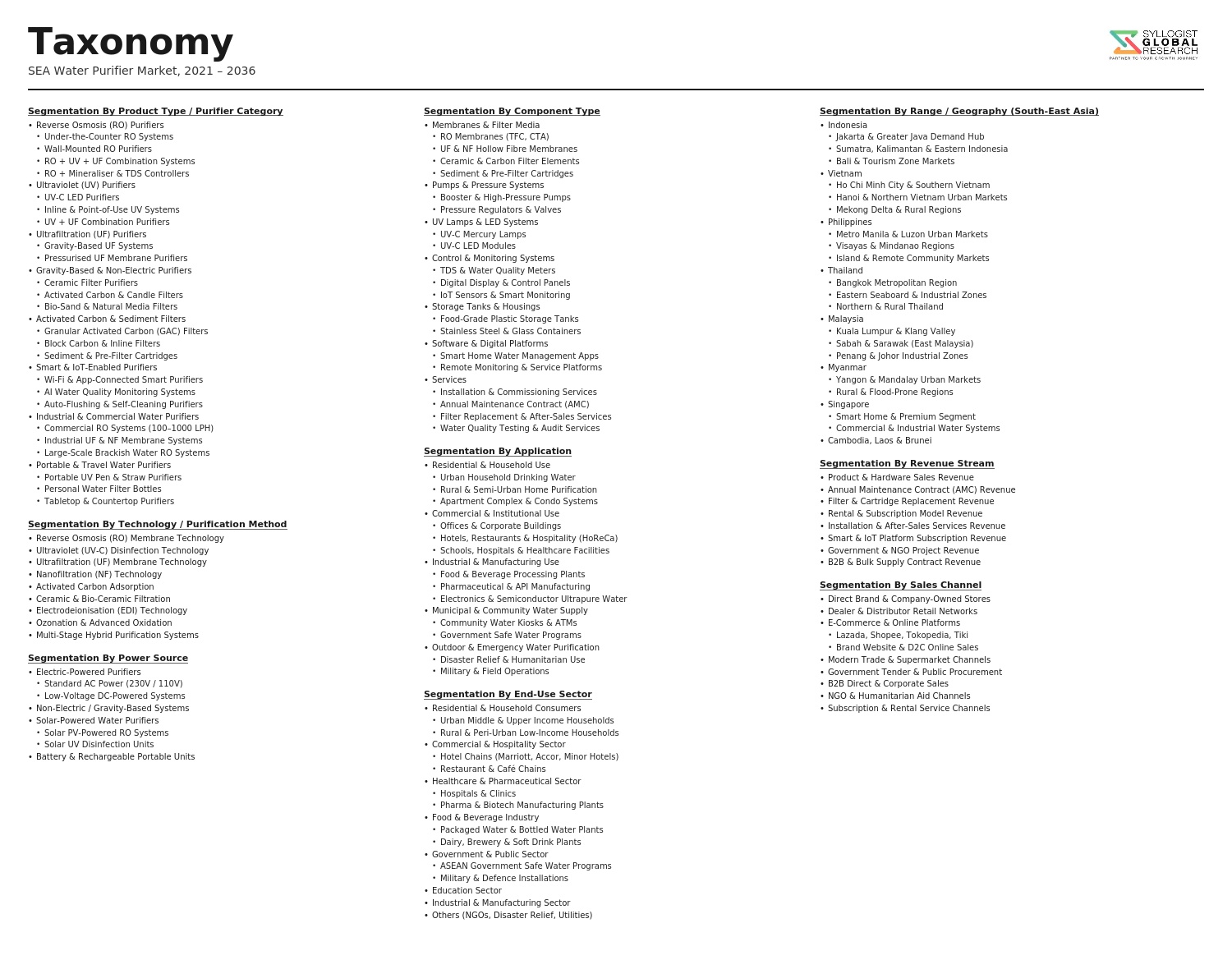

Market Segmentation

- Segmentation By Product Type

- Smart Reverse Osmosis (RO) Purifiers

- Smart Ultrafiltration (UF) Purifiers

- Smart UV Sterilization Purifiers

- Smart Multi-Stage and Combination Technology Purifiers

- Smart Hot and Cold Water Dispensers with Purification

- Smart Whole-House and Point-of-Entry Filtration Systems

- Others

- Segmentation By Technology

- IoT and Wi-Fi Connected Smart Purifiers

- AI-Powered Water Quality Analysis and Prediction

- Real-Time Multi-Parameter Sensor Monitoring (TDS, pH, Turbidity, Flow)

- Voice Assistant and Smart Home Integration (Alexa, Google Home)

- Auto Filter Life Monitoring and Replacement Notification

- Smartphone App Remote Monitoring and Control

- Cloud-Based Water Quality Data Analytics

- Others

- Segmentation By End-Use Application

- Residential Kitchen Under-Sink and Countertop Systems

- Commercial Office and Workplace Purification

- Hospitality (Hotels and Restaurants)

- Healthcare and Medical Facilities

- Educational Institutions

- Industrial and Manufacturing Facility Water Supply

- Others

- Segmentation By Business Model

- Outright Hardware Purchase

- Rental and Subscription Service Model

- Filter-as-a-Service and Auto-Replenishment

- Leasing and Pay-Per-Use Models

- Others

- Segmentation By Distribution Channel

- E-Commerce and Online Marketplaces (Shopee, Lazada, Tokopedia)

- Specialty Home Appliance Retail Chains

- Hypermarket and Consumer Electronics Stores

- Direct-to-Consumer Brand Stores and Showrooms

- B2B and Project Sales (Developers, Hotels, Offices)

- Others

- Segmentation By Price Range

- Entry-Level Smart Purifiers (Below USD 100)

- Mid-Range Smart Purifiers (USD 100 to USD 300)

- Premium Smart Purifiers (USD 300 to USD 600)

- Super-Premium and Commercial Grade (Above USD 600)

- Others

- Segmentation By Country

- Indonesia

- Vietnam

- Thailand

- Malaysia

- Philippines

- Singapore

- Rest of South-East Asia

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the South-East Asia Smart Water Purifier Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, technology, end-use application, business model, distribution channel, price range, and country, to enable smart purifier manufacturers, IoT technology providers, consumer appliance brands, subscription service operators, and investors to identify which product categories and national markets will generate the highest absolute revenue and the most commercially defensible growth trajectories across the forecast period?

- How is the filter subscription and rental business model pioneered by Coway in Malaysia and Singapore performing commercially across the South-East Asian market in terms of subscriber acquisition cost, monthly churn rate, lifetime customer value, and operational margin relative to the outright hardware sale model, and which market conditions including income level thresholds, consumer credit access, urbanization density, and service infrastructure maturity determine the markets where subscription models are commercially viable and preferable to hardware sale models for smart purifier brand operators?

- What is the current smart water purifier penetration rate across urban household income segments in Indonesia, Vietnam, Thailand, Malaysia, and the Philippines, and what is the projected penetration trajectory through 2034 under different income growth, price reduction, and consumer awareness scenarios, and which specific consumer triggers including waterborne illness incidents, media coverage of water quality issues, parenting health motivations, and smart home adoption are most effective in converting conventional purifier users and bottled water dependent households into smart purifier adopters?

- How are Chinese smart purifier manufacturers including Xiaomi, Haier, Midea, and A.O. Smith’s China operations competing with Korean brands including Coway and SK Magic, Japanese brands including Panasonic and Toshiba, and domestic South-East Asian brands in terms of price positioning, technology feature sets, after-sales service infrastructure, e-commerce distribution strength, and localization of product features including multi-language apps, local contaminant-specific filtration technology, and voltage compatibility across the diverse national markets of the South-East Asian region?

- Who are the leading smart water purifier manufacturers, IoT platform and sensor technology providers, filter subscription service operators, e-commerce distribution partners, and after-sales service network developers currently defining the competitive and commercial landscape of the South-East Asia smart water purifier market, and what are their respective product portfolios across RO, UF, and UV technology platforms, IoT connectivity and app feature capabilities, country-by-country market entry and distribution strategies, subscription model deployment plans, filter supply chain management approaches, and competitive positioning in response to the structural growth opportunity presented by South-East Asia’s water quality challenge, rising household income, and smartphone-enabled consumer connectivity through the forecast period?

- Table of Contents

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Water Quality Variability, Contamination Complexity & Source Water Treatment Challenge Risk Across SEA

- Counterfeit & Sub-Standard Water Purifier Products, Fraudulent Performance Claims & Consumer Safety Risk

- Price Sensitivity, Affordability Barrier & Low Market Penetration in Rural and Low-Income Segments Risk

- Regulatory Fragmentation, Varying National Water Quality Standards & Multi-Country Compliance Risk

- After-Sales Service, Filter Replacement Availability & Maintenance Infrastructure Limitation Risk

- Regulatory Framework & Standards

- National Drinking Water Quality Standards, NSF/ANSI Certification Equivalents & Potable Water Safety Regulations Across SEA Countries

- Product Safety, Electrical Equipment Certification & Mandatory Testing & Labelling Standards for Water Purifier Products

- Filter Media, RO Membrane, Activated Carbon & Chemical Disinfectant Material Safety & Product Registration Requirements

- Environmental, Plastic Waste & Filter Cartridge Disposal Regulations Applicable to Water Purifier Manufacturing & Distribution

- E-Commerce, Consumer Protection, Warranty Obligations & After-Sales Service Standards for Water Purifier Brands

- South-East Asia Water Purifiers Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Technology Type

- Reverse Osmosis (RO) Purifiers

- Ultraviolet (UV) Purifiers

- Ultrafiltration (UF) Purifiers

- Gravity & Candle Filters (Non-Electric)

- RO + UV + UF Multi-Stage Combination Purifiers

- IoT Smart & Connected Water Purifiers

- Market Size & Forecast by Product Type

- Under-Sink & Countertop Purifiers

- Wall-Mounted Purifiers

- Portable & Tabletop Purifiers

- Whole-House Water Treatment Systems

- Commercial & Industrial Water Purification Systems

- Market Size & Forecast by Capacity

- Household Capacity (Below 15 LPH)

- Light Commercial Capacity (15 to 50 LPH)

- Commercial Capacity (50 to 500 LPH)

- Industrial Capacity (Above 500 LPH)

- Market Size & Forecast by Application

- Residential

- Commercial (Offices, Retail & Hospitality)

- Institutional (Schools, Hospitals & Government Facilities)

- Industrial & Manufacturing

- Market Size & Forecast by Distribution Channel

- Offline Retail (Hypermarkets, Electronics Stores & Specialty Water Stores)

- Online & E-Commerce Platforms

- Direct Sales & Door-to-Door (D2C) Channel

- Institutional & B2B Procurement Channel

- Market Size & Forecast by End-User

- Households & Individual Consumers

- Offices & Commercial Buildings

- Hotels, Restaurants & Hospitality Sector

- Healthcare Facilities & Hospitals

- Educational Institutions

- Industrial & Manufacturing Plants

- Market Size & Forecast by Sales Channel

- OEM Brand Authorised Dealer & Service Network

- Multi-Brand Distributor & Retail Stockist

- Online Marketplace & Direct-to-Consumer (D2C) Platform

- Rental, Subscription & Pay-Per-Use Service Model

- B2B Institutional & Water Utility Partnership Channel

- Market Size & Forecast by Country

- Indonesia

- Vietnam

- Philippines

- Thailand

- Malaysia

- Singapore

- Myanmar

- Cambodia

- Indonesia Water Purifiers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Technology Type

- By Product Type

- By Capacity

- By Application

- By Distribution Channel

- By End-User

- By Sales Channel

- Market Size & Forecast

- Vietnam Water Purifiers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Technology Type

- By Product Type

- By Capacity

- By Application

- By Distribution Channel

- By End-User

- By Sales Channel

- Market Size & Forecast

- Philippines Water Purifiers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Technology Type

- By Product Type

- By Capacity

- By Application

- By Distribution Channel

- By End-User

- By Sales Channel

- Market Size & Forecast

- Thailand Water Purifiers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Technology Type

- By Product Type

- By Capacity

- By Application

- By Distribution Channel

- By End-User

- By Sales Channel

- Market Size & Forecast

- Malaysia Water Purifiers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Technology Type

- By Product Type

- By Capacity

- By Application

- By Distribution Channel

- By End-User

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Water Purifiers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Technology Type

- By Product Type

- By Capacity

- By Application

- By Distribution Channel

- By End-User

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: Indonesia, Vietnam, Philippines, Thailand, Malaysia, Singapore, Myanmar, Cambodia, Laos, Brunei, East Timor

- Technology Landscape & Innovation Analysis

- Reverse Osmosis (RO) Membrane Technology Deep-Dive: Thin Film Composite, Nano-Filtration & Advanced Membrane Material Trends

- Ultraviolet (UV) Disinfection Technology: Low-Pressure Mercury Lamp, UV-LED & Amalgam Lamp Technology Evolution

- Ultrafiltration (UF) & Hollow Fibre Membrane Technology for Point-of-Use Water Treatment

- Activated Carbon, Adsorption Media & Multi-Stage Filtration Technology for Taste, Odour & Chemical Removal

- IoT Smart Water Purifier Technology: App-Based Monitoring, Filter Life Alerts, Remote Diagnostics & Voice Integration

- Solar-Powered & Off-Grid Water Purification Technology for Rural & Underserved Community Applications

- Electrodeionisation (EDI), Electrolysis & Advanced Electrochemical Disinfection Technology

- Patent & IP Landscape in Water Purification Technologies

- Value Chain & Supply Chain Analysis

- RO Membrane, UV Lamp & Filter Cartridge Component Manufacturing Supply Chain

- Water Purifier OEM Assembly, System Integration & Branded Product Manufacturing

- Authorised Dealer, Distributor & Multi-Brand Retail Channel Network

- Online Platform, E-Commerce Marketplace & Direct-to-Consumer Digital Sales Channel

- After-Sales Service, Filter Replacement Subscription & Annual Maintenance Contract (AMC) Channel

- Institutional, B2B & Water Utility Partnership Procurement Channel

- Import, Customs Clearance & Cross-Border Regional Supply Chain Management

- Pricing Analysis

- Price Analysis by Technology Type (RO vs. UV vs. UF vs. Gravity vs. Smart IoT Purifiers)

- Price Analysis by Product Segment: Entry-Level, Mid-Range & Premium Water Purifier Categories

- Price Benchmarking: International Premium Brands vs. Regional Asian Brands vs. Local Manufacturers

- Distribution Margin, Dealer Mark-Up & Channel Pricing Structure Analysis

- Filter Replacement, AMC & Total Cost of Ownership (TCO) Analysis Across Technology Types

- Online vs. Offline Pricing Dynamics & E-Commerce Discount Impact on Market Pricing

- Sustainability & Environmental Analysis

- RO Wastewater Recovery, Reject Water Reduction & Zero-Liquid Discharge Design Initiatives in Water Purifier Technology

- Filter Cartridge & Membrane Waste Management, Recycling Programmes & Extended Producer Responsibility Obligations

- Energy Efficiency Comparison Across Purification Technologies: Gravity vs. UV vs. RO Power Consumption

- BPA-Free, NSF-Compliant & Food-Safe Material Standards in Water Purifier Component & Tank Manufacturing

- Access to Safe Water, SDG 6 Alignment & Social Impact of Affordable Water Purification in South-East Asia

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Global Premium Brands vs. Regional vs. Local Players by Country & Technology)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Type, Product Segment & Country

- Player Classification

- Global Premium Water Purifier Brands with SEA Presence & Local Operations

- Regional Asian Water Purifier Brands Operating Across Multiple SEA Markets

- Local Country-Specific Domestic Manufacturers & Brands

- Online-First, D2C & Digital-Native Water Purifier Brands

- Industrial & Commercial Water Treatment Equipment Providers

- Filter Cartridge, Membrane & Key Component Manufacturers

- Rental, Subscription & Water-as-a-Service Model Operators

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Product Segment & Country

- Company Profile

- Company Overview & Headquarters

- Water Purifier Product & Technology Portfolio

- Key Customer Relationships & Distribution Partnerships by Country

- Manufacturing Footprint & Production Capacity

- Revenue (Water Purifier Segment) & Installed Base

- Technology Differentiators, Certifications & Water Quality Compliance Claims

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Market Entry, Distribution Expansion)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Price Competitiveness)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Type, Product Type, Application, End-User & Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output