Market Definition

The Global Agricultural Carbon Credit Platforms Market encompasses the development and commercial operation of digital software ecosystems that facilitate the measurement, reporting, verification, issuance, and trading of carbon credits generated by agricultural and land management practices including soil carbon sequestration, enteric methane reduction, improved manure management, reduced tillage, cover cropping, agroforestry, wetland restoration, and avoided deforestation, connecting farm operators, aggregators, credit buyers, voluntary carbon market participants, and verification bodies through integrated data management, IoT and satellite monitoring, MRV workflow automation, and credit trading infrastructure globally.

Market Insights

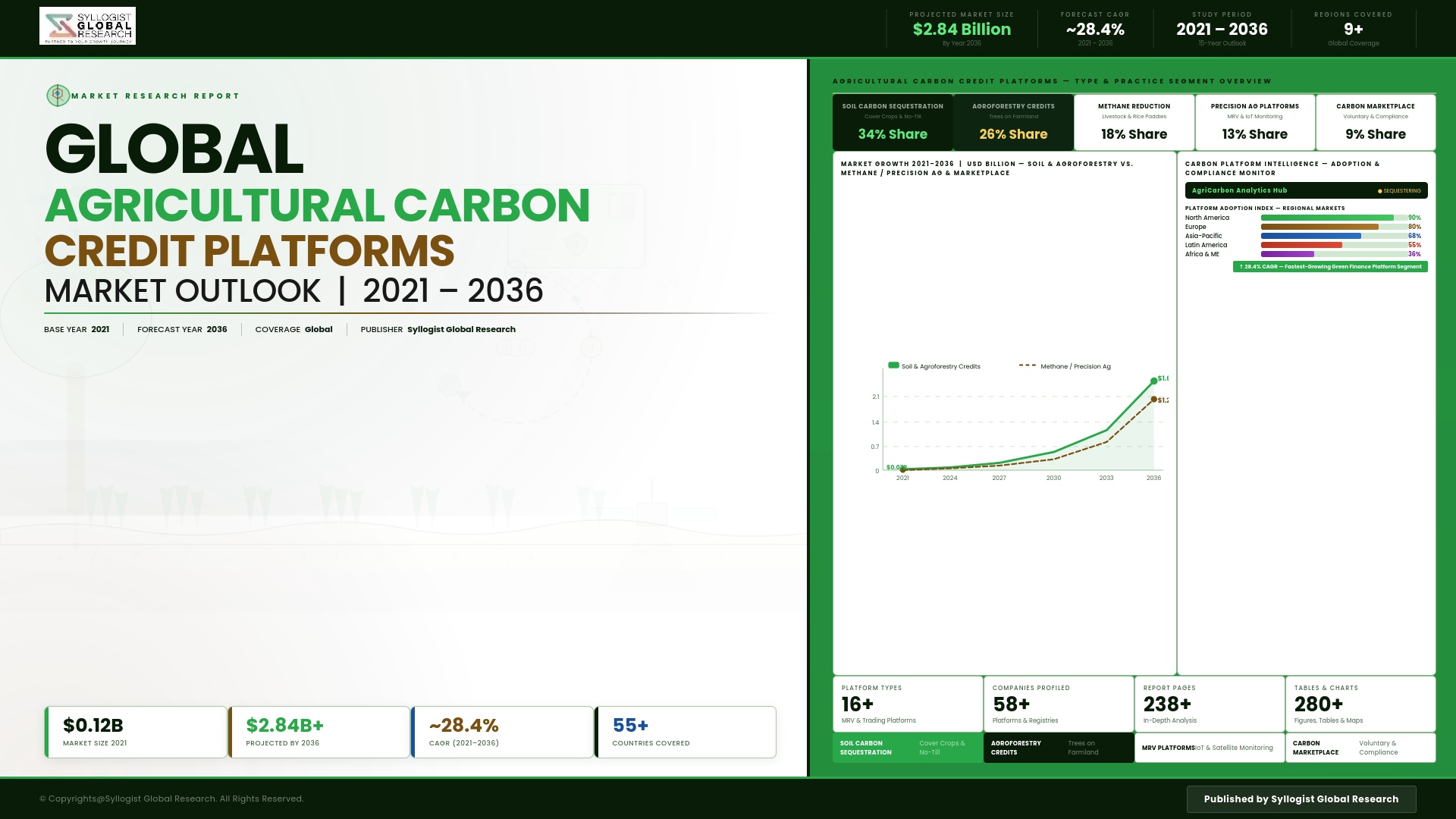

The global agricultural carbon credit platforms market is navigating a critical inflection point defined by the tension between the enormous theoretical carbon sequestration and emission reduction potential of global agricultural and land use systems and the persistent integrity, permanence, and additionality challenges that have undermined buyer confidence in the quality of agricultural carbon credits issued under voluntary market methodologies, compelling platform developers, credit standard bodies, and corporate buyers to invest in more rigorous monitoring, reporting, and verification infrastructure that can credibly demonstrate real, measurable, and durable emission reductions attributable to specific agricultural management changes. The market was valued at approximately USD 1.4 billion in 2025 and is projected to expand at a compound annual growth rate of 26.8% through 2034, as the voluntary carbon market for agricultural credits recovers from the integrity concerns that depressed transaction volumes in the 2023 to 2024 period, supported by improved satellite-based monitoring methodologies, more conservative credit issuance protocols, and the emergence of standardized measurement frameworks that reduce the methodological heterogeneity that previously undermined market trust in agricultural carbon credit quality.

Soil carbon sequestration through regenerative agriculture practices including reduced tillage, cover cropping, composting, and crop rotation improvement represents the largest theoretical credit generation opportunity within the agricultural carbon platform market and the most challenging to quantify with the temporal stability and measurement precision required for high-integrity credit issuance. The significant natural variability of soil carbon stocks across different soil types, climate zones, and management histories creates substantial measurement uncertainty that conservative crediting methodologies must account for through discount factors that reduce the number of credits issued per tonne of carbon change estimated, creating a structural tension between the credit volume that project developers and farmers require for economic viability and the methodological conservatism that buyers and verification bodies demand for credit quality assurance. Livestock methane reduction credits from enteric fermentation management through feed additive interventions, genetic improvement, and grazing management optimization are gaining commercial traction as a relatively more directly measurable agricultural carbon project category with well-established emission factor methodologies and growing corporate buyer interest from food and beverage companies with supply chain decarbonization commitments targeting Scope 3 livestock emissions.

The platform technology layer of the agricultural carbon credit ecosystem is advancing rapidly through the integration of satellite remote sensing for land use change detection and vegetation carbon stock monitoring, IoT soil sensor networks for direct soil carbon measurement validation, digital farm management record systems for agricultural practice verification, and blockchain-based credit registry infrastructure for transparent and tamper-resistant credit issuance and retirement tracking. AI-powered remote sensing analytics platforms capable of detecting land management practice changes at field parcel level from optical and synthetic aperture radar satellite imagery are enabling lower-cost, higher-coverage monitoring of enrolled farm parcels that reduces the per-project verification cost that has historically made small farm enrollment economically impractical under traditional ground-based measurement methodologies. Corporate buyers including food companies, agricultural input suppliers, and consumer goods corporations are developing direct procurement programs with platform operators to source agricultural carbon credits carrying specific supply chain co-benefits including farmer income uplift, biodiversity outcomes, and water quality improvements that align with their sustainability reporting narratives beyond pure carbon accounting value.

North America leads the global agricultural carbon credit platforms market by platform innovation, enrolled project acreage, and corporate buyer procurement activity, anchored by the large commercial grain and oilseed farming base in the United States and Canada where economies of scale in measurement, aggregation, and platform enrollment make soil carbon and cover crop projects commercially viable, and where the concentration of corporate food company headquarters creates geographically proximate buyer-seller relationships that facilitate direct agricultural carbon procurement programs. Europe represents the second largest regional market, driven by the European Union carbon farming initiative providing policy framework support for agricultural carbon credit development, strong corporate sustainability procurement demand, and well-developed agricultural sustainability certification infrastructure that complements carbon credit verification requirements. Asia-Pacific is the fastest-growing regional market, driven by the scale of rice paddy methane reduction opportunity in China, India, Vietnam, and Indonesia, growing agribusiness carbon program investment, and government-backed agricultural carbon market initiatives in Australia and New Zealand targeting farming sector emission reduction contributions to national climate commitments.

Key Drivers

Corporate Net Zero Commitments and Scope 3 Agricultural Supply Chain Emission Reduction Obligations Creating Structural Demand for High-Integrity Agricultural Carbon Credits from Food and Consumer Goods Buyers

The proliferation of science-based net zero targets and Scope 3 emission reduction commitments among major food and beverage corporations, agricultural input companies, retailers, and consumer goods manufacturers is creating growing demand for agricultural carbon credits that deliver verifiable emission reductions and sequestration outcomes within their direct supply chain farming systems, as corporate sustainability reporting frameworks require supply chain emission accountability that general market offset purchases from forestry or renewable energy projects cannot satisfy when agricultural Scope 3 emissions constitute the dominant share of total corporate carbon footprint. This demand is motivating investment in agricultural carbon platform development by food corporations seeking controlled supply chain carbon procurement programs and by agribusiness service companies positioned to aggregate farm-level carbon projects at the scale required for cost-efficient corporate procurement.

Advancing Satellite Monitoring and IoT Sensing Technologies Reducing Measurement Costs and Improving Credit Integrity for Agricultural Carbon Projects at Farm Parcel Scale

The rapid improvement of satellite-based agricultural monitoring capabilities through higher spatial resolution multispectral and hyperspectral imagery, synthetic aperture radar penetration of crop canopy for soil surface condition characterization, and AI-powered change detection algorithms that can identify tillage practice transitions, cover crop establishment, and vegetation carbon stock changes at individual field parcel resolution is enabling agricultural carbon platforms to implement scalable, lower-cost remote sensing monitoring programs that replace or substantially reduce the expensive and logistically complex ground-based soil sampling and farm visit verification protocols that previously constrained the economic viability of small farm enrollment in carbon credit programs. These technology advances are directly improving agricultural carbon credit integrity by enabling more frequent, independent, and objective monitoring of enrolled project management practices.

Government Agricultural Carbon Policy Frameworks and Payment-for-Ecosystem-Services Programs Creating Regulatory Market Infrastructure That Complements Voluntary Carbon Market Demand for Agricultural Credits

National and regional government agricultural carbon policy frameworks including the European Union carbon farming initiative, United States Department of Agriculture climate-smart agriculture program, Australian Emissions Reduction Fund methodology development for agricultural projects, and New Zealand agricultural emissions pricing scheme are creating regulated or semi-regulated payment mechanisms for agricultural emission reductions that complement voluntary carbon market demand and provide farm operators with diversified revenue streams that improve the economics of adopting climate-beneficial agricultural practices. These government programs are simultaneously developing the measurement methodology, verification protocol, and data infrastructure standards that raise the technical floor for agricultural carbon credit quality and reduce the methodological fragmentation that has historically constrained institutional buyer confidence in voluntary market agricultural credit integrity.

Key Challenges

Soil Carbon Measurement Uncertainty, Impermanence Risk, and Additionality Demonstration Complexity Undermining Credit Quality Credibility and Institutional Buyer Confidence in Agricultural Offsets

The scientific and methodological challenges of accurately quantifying soil organic carbon changes attributable to specific management interventions across the spatial and temporal variability of agricultural soils remain incompletely resolved, with measurement costs for statistically robust soil sampling protocols often exceeding the credit revenue generated by enrolled parcels and with the permanence of sequestered soil carbon vulnerable to reversal through extreme drought, flooding, fire, or management reversion events that can rapidly release accumulated carbon back to the atmosphere. Demonstrating additionality, meaning that enrolled management practices generate carbon outcomes that would not have occurred without carbon payment incentives, is particularly challenging in agricultural contexts where practice adoption is often driven by multiple agronomic, economic, and policy factors independent of carbon market participation.

Farmer Enrollment Fragmentation, Aggregation Cost Complexity, and Low Per-Farm Credit Revenue Constraining the Economic Viability of Platform Enrollment Programs for Small and Mid-Scale Farm Operations

Agricultural carbon credit platforms must aggregate carbon projects across large numbers of individual farm operators whose individual credit volumes at typical practice change rates are insufficient to justify the transaction, monitoring, verification, and registry costs of standalone credit issuance, requiring platform operators to develop economically viable aggregation models that spread fixed verification costs across enrolled farm cohorts while maintaining credit quality documentation at individual farm level. The complexity of managing large numbers of smallholder or mid-scale farm enrollments with diverse practice histories, varying soil types, different monitoring data availability, and heterogeneous contractual arrangements creates substantial platform operational overhead that constrains the per-tonne credit economics achievable by agricultural carbon program operators relative to the simpler project structures of forestry or industrial carbon abatement projects.

Voluntary Carbon Market Price Volatility and Corporate Buyer Credit Quality Scrutiny Creating Revenue Uncertainty That Weakens the Financial Incentive for Farmer Practice Change Adoption

The significant decline in voluntary carbon market credit prices following the integrity controversies of 2022 to 2024, which saw agricultural carbon credit prices in some market categories fall to levels insufficient to cover the measurement and verification costs of credit program participation, has materially undermined the financial attractiveness of agricultural carbon platform enrollment for farm operators who adopted climate-beneficial practices based on revenue projections built on higher credit price assumptions. The growing corporate buyer preference for high-integrity credits with robust third-party verification, transparent monitoring documentation, and co-benefit certification is simultaneously increasing the cost of credit issuance for platform operators competing to supply the premium quality segment of the market, creating a cost structure that further compresses the net carbon payment reaching enrolled farmers and reducing the behavioral incentive that credit revenue provides for continued practice adoption.

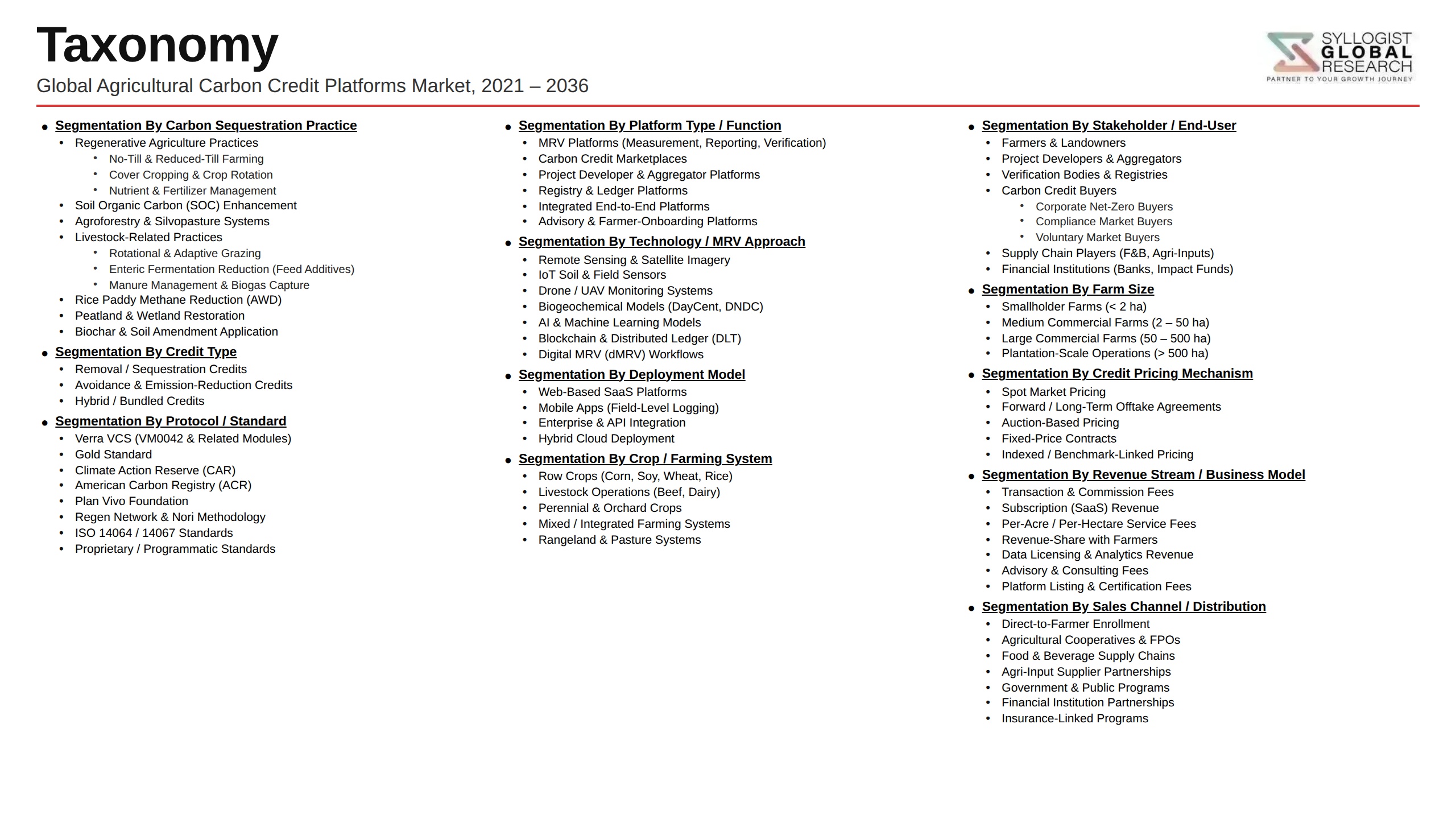

Market Segmentation

- Segmentation By Platform Type

- End-to-End Carbon Program Management Platforms

- MRV and Monitoring Verification Software

- Carbon Credit Registry and Trading Platforms

- Farm Data Aggregation and Enrollment Platforms

- Blockchain-Based Credit Issuance and Tracking Systems

- Others

- Segmentation By Carbon Project Type

- Soil Carbon Sequestration Projects

- Livestock Enteric Methane Reduction

- Manure Management and Biogas Capture

- Cover Cropping and Reduced Tillage Programs

- Agroforestry and Silvopastoral Projects

- Wetland Restoration and Peatland Conservation

- Avoided Deforestation and Land Use Change

- Others

- Segmentation By Monitoring Technology

- Satellite Remote Sensing and Earth Observation

- IoT Soil Sensors and In-Field Monitoring Networks

- Digital Farm Record and Practice Verification Systems

- AI-Powered Carbon Stock Estimation Models

- Ground-Based Soil Sampling and Laboratory Analysis

- Others

- Segmentation By Credit Standard

- Verified Carbon Standard and Verra Registry

- Gold Standard and Climate Community Biodiversity

- American Carbon Registry

- Government and Regulated Market Standards

- Proprietary Corporate Program Standards

- Others

- Segmentation By End User

- Farm Operators and Agricultural Cooperatives

- Carbon Aggregators and Project Developers

- Food and Beverage Corporations

- Agricultural Input and Agribusiness Companies

- Financial Institutions and Carbon Fund Managers

- Government Agricultural and Environmental Agencies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global agricultural carbon credit platforms market valuation in 2025, projected through 2034, segmented by platform type, carbon project type, and end user, enabling platform developers, carbon aggregators, corporate buyers, and investors to identify the highest-growth platform categories and most commercially viable agricultural carbon program investment opportunities across the global market?

- How are satellite remote sensing capabilities, IoT soil monitoring networks, AI-powered carbon stock estimation models, and blockchain-based credit registry systems combining to reduce per-tonne MRV costs and improve agricultural carbon credit integrity, and what technology performance milestones are required to make small farm enrollment and soil carbon project economics financially viable without premium credit price support?

- Which agricultural carbon project types, specifically soil carbon sequestration, livestock enteric methane reduction, cover cropping programs, agroforestry, and wetland restoration, offer the most credible and scalable credit generation opportunities under rigorous additionality and permanence criteria, and what measurement methodology advances are enabling higher-integrity credit issuance with lower monitoring costs in each project category?

- How is the competitive landscape structured among agricultural carbon platform operators, MRV technology providers, carbon aggregators, and corporate direct sourcing programs, and what data science capability, farmer relationship scale, verification methodology credibility, buyer network development, and geographic market coverage strategies are enabling leading platform operators to build commercially defensible positions in this fragmented and rapidly evolving market?

- What voluntary carbon market price recovery trajectory, corporate buyer credit quality demand evolution, and emerging high-integrity credit premium pricing dynamics are expected to reshape the agricultural carbon credit revenue landscape through 2034, and what credit standard, co-benefit certification, and monitoring transparency investments are platform operators and project developers making to position their credit supply for premium buyer procurement programs?

- How are government agricultural carbon policy frameworks in the European Union, United States, Australia, and New Zealand shaping the development of regulated or semi-regulated payment mechanisms for farm-level carbon outcomes, and how are these public sector programs interacting with voluntary carbon market demand to create blended revenue models that improve the economics of farmer practice change adoption?

- Which regional agricultural carbon markets, specifically North America, Europe, Latin America, and Asia-Pacific, are expected to generate the most significant platform enrollment growth and corporate buyer procurement activity through 2034, and what combinations of farm structure characteristics, corporate supply chain sustainability commitments, government program support, and monitoring infrastructure maturity are defining the pace and scale of agricultural carbon market development in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Carbon Credit Integrity, Additionality, Permanence & Greenwashing Credibility Risk

- Voluntary Carbon Market Price Volatility, Liquidity & Buyer Demand Uncertainty Risk

- Farmer Adoption Barrier, Low Willingness-to-Enrol & Smallholder Engagement Risk

- MRV Technology Accuracy, Remote Sensing Validation & Baseline Setting Methodology Risk

- Regulatory Fragmentation, Article 6 Rule-Making Uncertainty & Compliance Market Access Risk

- Platform Consolidation, Competitive Displacement & First-Mover Advantage Erosion Risk

- Regulatory Framework & Standards

- UNFCCC Article 6, Paris Agreement Corresponding Adjustments & Internationally Transferred Mitigation Outcomes (ITMOs) Frameworks

- Voluntary Carbon Market Standards: Verra VCS, Gold Standard, American Carbon Registry (ACR) & Climate Action Reserve (CAR)

- EU Carbon Removal Certification Framework (CRCF) & Agricultural Carbon Farming Methodology Requirements

- USDA Partnerships for Climate-Smart Commodities, 4per1000 Initiative & National Agricultural Carbon Programme Frameworks

- Science-Based Targets for Agriculture (SBTi FLAG), SBTN & Corporate Net Zero Agricultural Supply Chain Standards

- ICVCM Core Carbon Principles (CCPs), VCMI Claims Code & Agricultural Carbon Credit Quality Integrity Frameworks

- Global Agricultural Carbon Credit Platforms Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Carbon Credits Issued, MtCO2e & Enrolled Farm Area, Million Hectares)

- Market Size & Forecast by Platform Type

- End-to-End Agricultural Carbon Credit Platform (Enrolment, MRV, Issuance & Trading)

- MRV-Only & Carbon Quantification Platform

- Carbon Credit Registry & Issuance Platform

- Voluntary Carbon Market Trading & Exchange Platform

- Agri-Food Corporate Supply Chain Carbon Procurement Platform

- Farmer Enrolment, Programme Management & Payment Platform

- Integrated Farm Management & Carbon Accounting Platform

- Market Size & Forecast by Carbon Sequestration Practice

- Soil Organic Carbon Sequestration (Cover Crops, No-Till & Reduced Tillage)

- Agroforestry, Silvopasture & Perennial Crop Carbon Sequestration

- Wetland Restoration, Peatland Rewetting & Blue Carbon Agricultural Practices

- Enteric Fermentation & Livestock Methane Reduction Credits

- Manure Management, Biogas & Agricultural Waste Emission Reduction Credits

- Precision Fertiliser Management & Nitrous Oxide Emission Reduction Credits

- Rice Paddy Methane Mitigation Credits

- Regenerative Agriculture & Bundled Multi-Practice Carbon Credits

- Market Size & Forecast by MRV Technology

- Satellite Remote Sensing & Earth Observation-Based Carbon MRV

- Soil Sampling, Laboratory Analysis & Direct Measurement MRV

- Biogeochemical Process Models (DNDC, RothC, CENTURY & IPCC Tier 3 Models)

- IoT Field Sensors, Eddy Covariance Flux Tower & In-Situ Measurement MRV

- AI & Machine Learning-Driven Hybrid MRV & Predictive Carbon Accounting

- Blockchain-Based Data Integrity, Audit Trail & Credit Provenance MRV

- Market Size & Forecast by Farm Type

- Smallholder & Subsistence Farming (Below 2 Hectares)

- Small & Family Farms (2 to 50 Hectares)

- Medium Commercial Farms (50 to 500 Hectares)

- Large-Scale & Corporate Farms (Above 500 Hectares)

- Market Size & Forecast by Carbon Market Type

- Voluntary Carbon Market (VCM) Agricultural Credits

- Compliance & Regulated Carbon Market Agricultural Credits (ETS-Linked)

- Corporate Supply Chain Insetting & Value Chain Emission Reduction Credits

- Government-Sponsored & Nationally Determined Contribution (NDC)-Linked Agricultural Credits

- Market Size & Forecast by Application

- Corporate Net Zero & Science-Based Target (SBTi) Offsetting & Insetting

- Agri-Food Company Supply Chain Scope 3 Emission Reduction

- Financial Institution & ESG Investment Portfolio Decarbonisation

- Government Programme Farmer Payment & Rural Climate Finance

- Carbon Market Speculation, Investment & Portfolio Trading

- Market Size & Forecast by End-User

- Farmers, Growers & Landowners (Carbon Credit Sellers)

- Agri-Food Companies, Food Processors & Retailers (Buyers & Programme Sponsors)

- Financial Institutions, Investment Funds & Carbon Asset Managers

- Government Agencies & National Agricultural Ministries

- Carbon Brokers, Traders & Voluntary Carbon Market Intermediaries

- Technology & Data Companies Building on Platform APIs

- Market Size & Forecast by Sales & Revenue Model

- Credit Revenue Share & per-tonne Transaction Fee Model

- SaaS Platform Subscription & Licence Fee Model

- Data, Analytics & MRV Service Fee Model

- Programme Sponsor & Corporate Programme Management Fee Model

- North America Agricultural Carbon Credit Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Carbon Credits Issued, MtCO2e & Enrolled Farm Area, Million Hectares)

- By Platform Type

- By Carbon Sequestration Practice

- By MRV Technology

- By Farm Type

- By Carbon Market Type

- By Application

- By End-User

- By Country

- By Sales & Revenue Model

- Market Size & Forecast

- Europe Agricultural Carbon Credit Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Carbon Credits Issued, MtCO2e & Enrolled Farm Area, Million Hectares)

- By Platform Type

- By Carbon Sequestration Practice

- By MRV Technology

- By Farm Type

- By Carbon Market Type

- By Application

- By End-User

- By Country

- By Sales & Revenue Model

- Market Size & Forecast

- Asia-Pacific Agricultural Carbon Credit Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Carbon Credits Issued, MtCO2e & Enrolled Farm Area, Million Hectares)

- By Platform Type

- By Carbon Sequestration Practice

- By MRV Technology

- By Farm Type

- By Carbon Market Type

- By Application

- By End-User

- By Country

- By Sales & Revenue Model

- Market Size & Forecast

- Latin America Agricultural Carbon Credit Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Carbon Credits Issued, MtCO2e & Enrolled Farm Area, Million Hectares)

- By Platform Type

- By Carbon Sequestration Practice

- By MRV Technology

- By Farm Type

- By Carbon Market Type

- By Application

- By End-User

- By Country

- By Sales & Revenue Model

- Market Size & Forecast

- Middle East & Africa Agricultural Carbon Credit Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Carbon Credits Issued, MtCO2e & Enrolled Farm Area, Million Hectares)

- By Platform Type

- By Carbon Sequestration Practice

- By MRV Technology

- By Farm Type

- By Carbon Market Type

- By Application

- By End-User

- By Country

- By Sales & Revenue Model

- Market Size & Forecast

- Country-Wise* Agricultural Carbon Credit Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Carbon Credits Issued, MtCO2e & Enrolled Farm Area, Million Hectares)

- By Platform Type

- By Carbon Sequestration Practice

- By MRV Technology

- By Farm Type

- By Carbon Market Type

- By Application

- By End-User

- By Country

- By Sales & Revenue Model

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Australia, Germany, France, United Kingdom, Netherlands, Denmark, Sweden, Brazil, Argentina, Colombia, India, China, Indonesia, Kenya, Ghana, Nigeria, South Africa, New Zealand, Japan, South Korea

- Technology Landscape & Innovation Analysis

- Satellite-Based Soil Carbon MRV Technology: Multi-Spectral, Hyperspectral & SAR Remote Sensing for SOC Estimation & Validation

- Biogeochemical Model Technology: DNDC, RothC, CENTURY & Machine Learning-Enhanced Process Models for Field-Scale Carbon Accounting

- Blockchain & Distributed Ledger Technology for Agricultural Carbon Credit Issuance, Provenance & Double-Count Prevention

- AI-Driven Farmer Enrolment, Practice Change Monitoring, Additionality Testing & Automated Credit Issuance Platform Technology

- IoT Soil Sensor Networks, Eddy Covariance Flux Monitoring & Continuous Carbon Flux Measurement Technology

- Digital Agriculture Data Integration: Farm Management System (FMS), ERP & Agronomy App Data Interoperability for MRV

- Automated Baseline Setting, Leakage Accounting & Permanence Risk Buffer Calculation Technology

- Patent & IP Landscape in Agricultural Carbon Credit Platform Technologies

- Value Chain & Supply Chain Analysis

- Earth Observation Data, Satellite Imagery & Geospatial Data Provider Supply Chain

- Soil Laboratory, Analytical Testing & Field Sampling Service Supply Chain

- Cloud Computing, Data Processing & AI Model Infrastructure Supply Chain

- Carbon Standard Body, Methodology Developer & Third-Party Auditor Supply Chain

- Farmer Outreach, Agronomist Network & Extension Service Supply Chain

- Carbon Registry, Issuance Platform & Credit Custody Supply Chain

- Carbon Broker, Trader & Corporate Buyer Procurement Channel

- Pricing Analysis

- Agricultural Carbon Credit Price Analysis by Practice Type, Standard & Market (USD per tCO2e)

- Platform Revenue Share & Transaction Fee Structure Analysis

- MRV Cost per Hectare Analysis by Technology & Methodology

- Farmer Payment Rate, Net Revenue per Hectare & Participation Incentive Economics Analysis

- Corporate Programme Sponsor Cost: per-tonne Acquisition Cost, Programme Administration & Insetting Value Analysis

- Price Trajectory Analysis: VCM Demand Growth, Quality Premium & High-Integrity Credit Price Outlook

- Sustainability & Environmental Analysis

- Carbon Sequestration Potential of Agricultural Practices: Soil Carbon, Agroforestry & Livestock Emission Reduction Quantification

- Co-Benefits of Agricultural Carbon Programmes: Biodiversity, Water Quality, Soil Health & Rural Livelihood Improvement

- Additionality, Permanence & Leakage Assessment: Integrity Challenges & MRV Solutions for Agricultural Carbon Credits

- Smallholder Equity, Fair Benefit Sharing & Social Safeguards in Agricultural Carbon Programme Design

- SDG 2 (Zero Hunger), SDG 13 (Climate Action), SDG 15 (Life on Land) & SDG 1 (No Poverty) Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Carbon Practice & Geography

- Player Classification

- End-to-End Agricultural Carbon Credit Platform Operators

- MRV Technology & Carbon Quantification Software Providers

- Carbon Registry & Standard Bodies with Agricultural Methodology Programmes

- Agri-Food Corporate Carbon Insetting & Supply Chain Platform Providers

- Carbon Market Brokers, Exchanges & Trading Platforms with Agricultural Focus

- Agri-Tech, Farm Management & Precision Agriculture Companies Integrating Carbon

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Carbon Practice & Region

- Company Profile

- Company Overview & Headquarters

- Platform Products, Carbon Programme Portfolio & Methodology Coverage

- Key Customer Relationships, Farmer Enrolments & Corporate Buyer Partnerships

- Enrolled Farm Area, Credits Issued & Carbon Volume Under Management

- Revenue (Agricultural Carbon Platform Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Programme Launches, Methodology Approvals, Funding Rounds)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (MRV Rigour vs. Farmer Accessibility)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Carbon Practice, Farm Type, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Platform Product & Technology Investment Strategy

- MRV Rigour, Credit Integrity & Standard Certification Strategy

- Geographic Expansion & Emerging Market Farmer Enrolment Strategy

- Corporate Buyer, Agri-Food & Financial Institution Engagement Strategy

- Partnership, M&A & Carbon Ecosystem Strategy

- Policy Engagement, Regulatory Advocacy & Market Integrity Strategy

- Farmer Equity, Smallholder Access & Social Inclusion Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)