Market Definition

The Global Climate Analytics for Agriculture Market encompasses the development, deployment, and commercial provision of data-driven software platforms, predictive modeling systems, AI-powered decision support tools, satellite and IoT sensor data integration services, and advisory applications that analyze historical climate data, real-time weather observations, and long-range seasonal forecasts to deliver actionable agronomic insights for crop planning, irrigation scheduling, pest and disease risk management, yield prediction, climate risk assessment, and farm operational decision-making across field crop, horticulture, livestock, and aquaculture production systems globally.

Market Insights

The global climate analytics for agriculture market is experiencing a period of structurally accelerating demand, driven by the intensifying impact of climate change on agricultural production systems worldwide, the rapid proliferation of affordable IoT sensing and satellite earth observation data enabling unprecedented field-level environmental monitoring, and the growing adoption of precision agriculture technologies among commercial farm operators seeking to manage production risk, optimize input utilization, and sustain crop yields under increasingly unpredictable and extreme weather conditions. The market was valued at approximately USD 2.9 billion in 2025 and is projected to expand at a compound annual growth rate of 18.7% through 2034, as the convergence of worsening climate volatility, digital agriculture platform maturity, and the growing financial and reputational consequences of crop production failure for food companies, commodity traders, agricultural lenders, and crop insurance providers collectively elevate climate analytics from a supplementary decision support tool into a mission-critical operational intelligence infrastructure for agriculture sector participants across the entire value chain.

AI-powered yield prediction and crop stress forecasting models trained on multi-year datasets combining satellite-derived vegetation indices, soil moisture observations, local weather station records, and agronomic management data are enabling commercial farm operators to anticipate yield outcomes weeks ahead of harvest with accuracy levels that are transforming crop marketing, input management, and financial planning decisions across large-scale grain, oilseed, and specialty crop operations. The integration of hyperlocal weather forecast data at field resolution from numerical weather prediction models, coupled with crop growth simulation platforms that translate meteorological conditions into crop development stage trajectories and stress accumulation estimates, is providing growers with operational decision windows for planting timing, irrigation trigger management, fungicide application scheduling, and harvest logistics planning that reduce the yield loss and quality degradation consequences of adverse weather events that conventional farm management practices cannot adequately anticipate or mitigate.

The agricultural finance and crop insurance segment represents a rapidly growing and commercially significant demand driver for climate analytics platforms, as lenders providing crop production loans and insurers underwriting multi-peril crop insurance policies are investing in climate analytics infrastructure to improve the accuracy of loan risk assessment, refine actuarial models for climate-related yield loss estimation, detect fraudulent loss claims through satellite-based remote sensing verification, and build portfolio-level climate exposure monitoring capabilities that support regulatory climate risk disclosure obligations and investor reporting on agricultural portfolio climate resilience. Commodity trading companies and agricultural supply chain operators are similarly investing in climate analytics platforms that provide forward-looking production estimates across major growing regions, enabling supply availability forecasting, procurement timing optimization, and logistics planning under climate-driven production variability scenarios that direct market pricing and trading position management depend upon. Agrochemical and seed company agronomists are deploying climate analytics tools to optimize product recommendation timing, target field trials and new variety introductions to climate stress-relevant environments, and build advisory service differentiation that deepens customer relationships with commercial farm operators beyond transactional input sales.

North America represents the largest regional market for agricultural climate analytics, anchored by the high technology adoption rates of large commercial grain, oilseed, and specialty crop farms across the United States and Canada, the well-developed crop insurance market providing financial incentives for climate risk quantification, the concentration of agricultural technology venture investment, and the presence of major commodity trading companies and food corporations with sophisticated climate risk management programs driving enterprise-level analytics platform procurement. Europe represents the second largest regional market, driven by the European Union Farm to Fork strategy’s emphasis on precision agriculture adoption, growing regulatory reporting requirements for agricultural climate risk, and the high commercial intensity of European horticultural and specialty crop production where weather-driven quality and yield outcomes directly affect premium market positioning. Asia-Pacific is the fastest-growing regional market, driven by the scale and climate vulnerability of rice, wheat, and vegetable production across China, India, Southeast Asia, and Australia, where climate-related crop production disruption has severe food security and economic consequences that are motivating government and private sector climate analytics investment at growing scale.

Key Drivers

Accelerating Climate Change Impact on Agricultural Production Reliability Compelling Farm Operators and Agricultural Value Chain Participants to Invest in Predictive Climate Risk Management Capabilities

The measurably increasing frequency of extreme heat events, irregular precipitation patterns, intensified drought cycles, and unseasonal frost occurrences attributable to climate change is creating demonstrable yield volatility and quality degradation in crop production systems that previously relied on relatively predictable seasonal weather patterns for operational planning, compelling farm operators to invest in climate analytics platforms that provide the predictive lead time required to adapt planting schedules, manage irrigation infrastructure, deploy crop protection measures, and make harvest and marketing decisions with sufficient advance notice to minimize climate-related production losses. Agricultural lending institutions, crop insurers, food processors, and commodity traders simultaneously require climate analytics platforms to quantify, monitor, and manage the growing climate exposure embedded in their agricultural asset and revenue portfolios under worsening climate volatility.

Satellite Earth Observation Data Proliferation and IoT Sensor Network Expansion Enabling Unprecedented Field-Level Climate and Crop Monitoring at Commercially Viable Data Costs

The rapid expansion of commercial satellite earth observation constellations delivering daily to sub-daily multispectral and synthetic aperture radar imagery at field parcel spatial resolution, combined with the growing deployment of in-field IoT sensor networks measuring soil moisture, temperature, humidity, leaf wetness, and microclimate conditions, is providing agricultural climate analytics platforms with data inputs of breadth, spatial coverage, and temporal resolution that were unavailable to agricultural decision support systems a decade earlier. The declining cost of satellite imagery subscription access, improved on-farm connectivity enabling real-time sensor data transmission, and advancing AI capabilities for processing large multi-source earth observation datasets are making sophisticated climate analytics solutions accessible to mid-scale commercial farm operations that previously lacked the data infrastructure or technical resources to implement advanced climate monitoring programs.

Agricultural Climate Risk Disclosure Obligations and Sustainable Finance Frameworks Creating Institutional Demand for Quantitative Climate Analytics Across Agricultural Lenders, Insurers, and Investors

Growing regulatory requirements for climate-related financial risk disclosure under frameworks including the Task Force on Climate-related Financial Disclosures, the European Sustainability Reporting Standards, and national climate risk reporting mandates are compelling agricultural banks, crop insurers, pension funds with agricultural land investments, and food company supply chain sustainability reporting programs to adopt quantitative climate analytics platforms capable of generating the scenario-based climate risk assessments, portfolio exposure metrics, and forward-looking vulnerability indicators that regulatory disclosure frameworks and investor ESG reporting obligations require. The integration of climate analytics data into agricultural credit risk scoring, crop insurance premium calculation, and agricultural portfolio climate stress testing is creating enterprise-scale software procurement demand among financial institutions with large agricultural sector exposure that represents a high-value commercial segment for climate analytics platform providers.

Key Challenges

Data Quality, Spatial Resolution Limitations, and Forecast Accuracy Constraints in Developing Country Agricultural Environments Restricting Climate Analytics Platform Performance and Farmer Adoption

Agricultural climate analytics platforms in developing country markets including sub-Saharan Africa, South Asia, and Southeast Asia face significant data quality constraints arising from sparse ground-based weather station networks providing insufficient observational coverage for high-resolution meteorological modeling, limited soil survey and mapping data required for accurate crop growth simulation, low on-farm IoT sensor penetration, and inconsistent mobile and internet connectivity restricting real-time data transmission from remote agricultural areas. These data environment limitations reduce the spatial resolution, temporal frequency, and prediction accuracy of climate analytics outputs in precisely the markets where smallholder and subsistence farming populations face the highest climate vulnerability and would benefit most from accessible and affordable climate-informed agricultural advisory services.

Smallholder Farmer Digital Literacy Barriers, Low Technology Adoption Rates, and Limited Willingness to Pay Constraining Market Penetration in Developing Economy Agricultural Segments

The majority of global farm operators by number are smallholder farmers in developing economies who face significant barriers to climate analytics adoption including limited smartphone and internet access, low digital literacy, inadequate financial resources for software subscription fees, distrust of algorithm-generated recommendations without local agronomist validation, and language and interface accessibility constraints that prevent effective use of analytics platforms designed primarily for large commercial farm operators in developed markets. Bridging this adoption gap requires climate analytics providers to develop simplified, low-data-demand, vernacular-language mobile interfaces, integrate with existing farmer advisory service channels including extension workers and agricultural cooperatives, and design freemium or government-subsidized service delivery models that make climate intelligence economically accessible to resource-limited smallholder farming populations.

Climate Model Uncertainty and Long-Range Forecast Skill Limitations Reducing Decision Maker Confidence in Seasonal and Multi-Year Agricultural Climate Analytics Outputs

Agricultural decision-making at seasonal and multi-year planning horizons requires climate forecast inputs with sufficient accuracy and confidence intervals to justify the often irreversible or high-cost management decisions that planting, irrigation infrastructure, perennial crop investment, and market commitment choices represent, yet the inherent uncertainty of long-range climate predictions, the chaotic sensitivity of regional weather patterns to large-scale circulation anomalies, and the uneven skill performance of seasonal forecast models across different geographic regions and climate regimes create legitimate decision-maker skepticism about the actionability of probabilistic climate outlooks that may correctly characterize the distribution of possible outcomes but provide insufficient deterministic guidance for specific farm management timing and resource allocation decisions that require concrete operational answers rather than probabilistic scenario ranges.

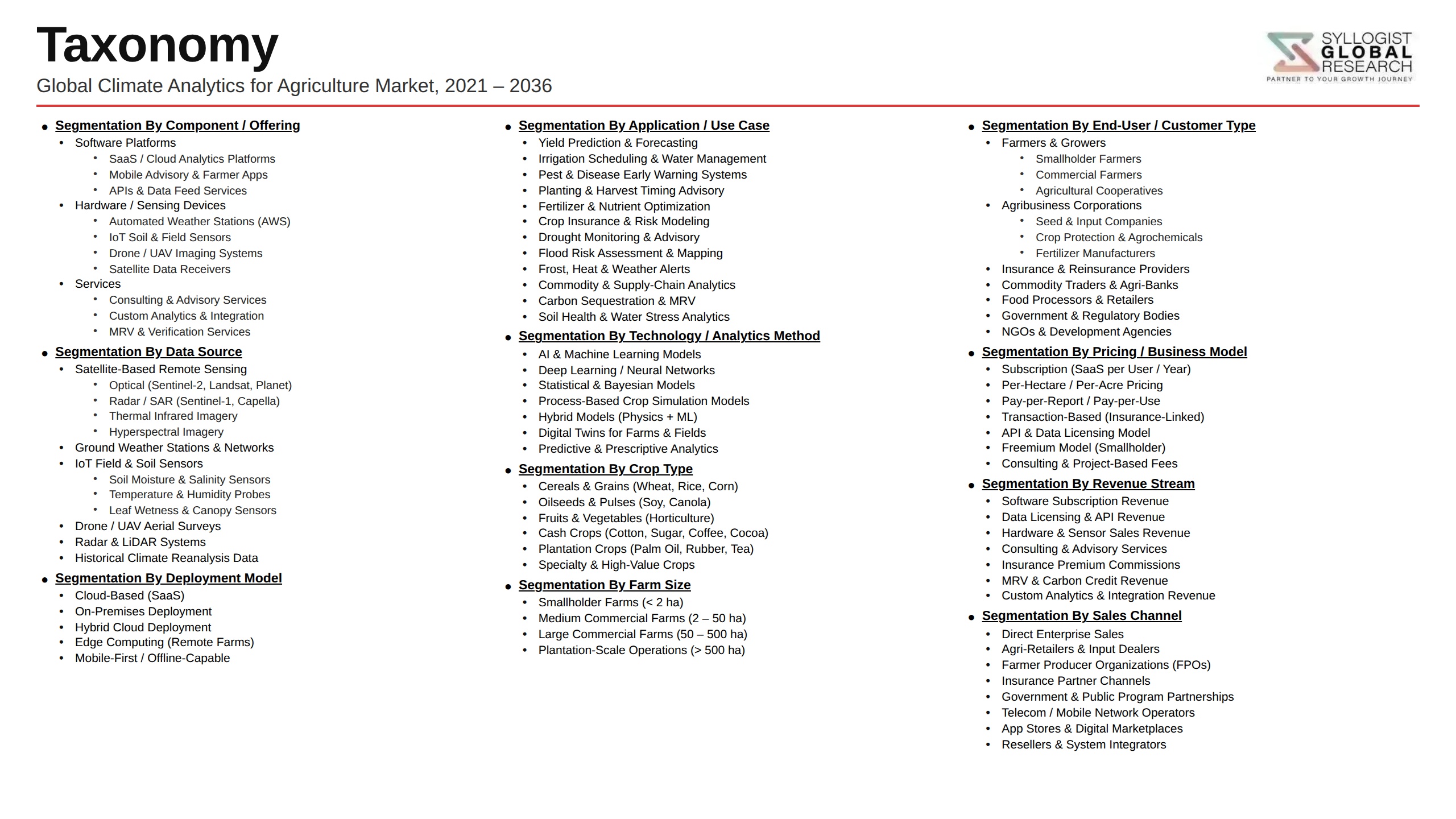

Market Segmentation

- Segmentation By Solution Type

- Weather Monitoring and Hyperlocal Forecast Platforms

- Crop Yield Prediction and Growth Modeling Systems

- Drought and Water Stress Monitoring Tools

- Pest and Disease Climate Risk Alert Platforms

- Seasonal Climate Outlook and Planning Advisory Services

- Climate Risk Assessment and Financial Exposure Analytics

- Others

- Segmentation By Technology

- Artificial Intelligence and Machine Learning Models

- Satellite and Remote Sensing Data Analytics

- IoT and In-Field Sensor Data Integration

- Numerical Weather Prediction and Crop Simulation Models

- Blockchain-Based Data Traceability and Verification

- Others

- Segmentation By Crop Type

- Cereals and Grains (Wheat, Rice, Maize)

- Oilseeds and Pulses

- Fruits and Vegetables

- Specialty and Cash Crops (Coffee, Cotton, Sugarcane)

- Livestock and Pasture Management

- Aquaculture

- Others

- Segmentation By Farm Size

- Smallholder and Subsistence Farms (Below 5 Hectares)

- Small-to-Medium Commercial Farms (5 to 100 Hectares)

- Large Commercial Farms (100 to 1000 Hectares)

- Large-Scale Industrial and Corporate Farming Operations

- Segmentation By Deployment Model

- Cloud-Based Software-as-a-Service Platforms

- Mobile Application and SMS Advisory Services

- On-Premises Enterprise Analytics Deployments

- API-Integrated Agricultural Management Systems

- Others

- Segmentation By End User

- Commercial Farm Operators and Agribusinesses

- Agricultural Lenders and Crop Insurance Providers

- Commodity Traders and Food Corporations

- Agrochemical and Seed Companies

- Government Agricultural Ministries and Extension Services

- NGOs and Development Finance Institutions

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global climate analytics for agriculture market valuation in 2025, projected through 2034, segmented by solution type, technology, and end user, enabling platform developers, agricultural technology investors, and institutional buyers to identify the highest-growth analytics categories and most commercially significant demand opportunities across the global agricultural climate intelligence landscape?

- How are AI-powered yield prediction models, satellite vegetation index analytics, hyperlocal weather forecast integration, and crop growth simulation platforms combining to improve the accuracy and operational lead time of climate-informed farm management decisions, and what performance benchmarks and prediction accuracy thresholds are commercial farm operators and agricultural lenders requiring before committing to enterprise-level climate analytics platform adoption?

- Which agricultural value chain segments beyond direct farm operators, specifically crop insurers, agricultural lenders, commodity traders, food processors, and supply chain sustainability reporting programs, are generating the fastest-growing institutional demand for climate analytics platforms, and what regulatory disclosure requirements and financial risk quantification needs are driving enterprise-level analytics procurement investment in each segment?

- How is the competitive landscape structured among global agricultural climate analytics platform providers, precision agriculture technology companies, weather intelligence services, and agri-fintech startups, and what data science capability, satellite data partnership, crop science expertise, farmer interface design, and geographic market expansion strategies are enabling leading platforms to build durable competitive advantages and customer retention in this rapidly evolving market?

- What data infrastructure gaps, weather station network density limitations, IoT sensor deployment constraints, and mobile connectivity deficiencies in developing country agricultural environments are most significantly restricting climate analytics platform accuracy and adoption in sub-Saharan Africa, South Asia, and Southeast Asia, and what public-private investment programs and technology adaptation strategies are being pursued to address these data environment constraints?

- How are government agricultural digital transformation programs, national food security climate adaptation strategies, development finance institution agricultural resilience investments, and international climate fund programs in India, China, Brazil, Kenya, and Ethiopia shaping climate analytics platform procurement volumes, technology specification requirements, and service delivery model design for large-scale government-backed agricultural advisory and risk management deployments?

- Which regional agricultural climate analytics markets, specifically North America, Asia-Pacific, and Latin America, are expected to generate the highest incremental revenue growth through 2034, and what combinations of climate change-driven production risk escalation, commercial farm technology adoption pace, crop insurance market development, and agricultural finance sector climate risk management investment are defining the market growth trajectory in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Data Quality, Satellite Coverage & Ground-Truth Validation Risk

- Climate Model Uncertainty, Forecast Skill & Predictive Accuracy Risk

- Customer Adoption, Smallholder Digital Divide & Last-Mile Risk

- Regulatory, Carbon Market Methodology & MRV Standard Evolution Risk

- Capital Investment, Subscription Churn & Unit Economics Risk

- Regulatory Framework & Standards

- Climate Disclosure (TCFD, CSRD, ISSB) & Mandatory Reporting Frameworks

- EU Deforestation Regulation (EUDR), CBAM & Sustainable Sourcing Compliance Standards

- Carbon Credit Methodology (Verra, Gold Standard & ART) & MRV Quality Standards

- Data Privacy, Farm Data Sovereignty & Agricultural Data Sharing Regulations

- Green Finance, ESG Disclosure & Climate-Smart Agriculture Procurement Standards

- Global Climate Analytics for Agriculture Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Hectares Covered and Active Subscribers)

- Market Size & Forecast by Solution Type

- Weather Forecasting & Hyperlocal Climate Data Platforms

- Climate Risk Assessment & Scenario Modelling Solutions

- Crop Yield Forecasting & Agronomic Climate Analytics

- Pest & Disease Pressure Forecasting Solutions

- Irrigation Scheduling & Soil Moisture Analytics Platforms

- Carbon Sequestration & GHG MRV Analytics Solutions

- Parametric Insurance & Climate Risk Underwriting Analytics

- Supply Chain Climate Risk & Sourcing Intelligence Platforms

- Climate Disclosure (TCFD, CSRD, EUDR) & Regulatory Reporting Solutions

- Market Size & Forecast by Technology

- Satellite Remote Sensing (Optical, SAR & Hyperspectral) Analytics Technology

- IoT Weather Station, Soil Sensor & Field Telemetry Technology

- Drone, UAV & Aerial Imagery Analytics Technology

- Artificial Intelligence, Machine Learning & Deep Learning Crop Modelling

- Process-Based Crop Models (DSSAT, APSIM & WOFOST) Technology

- Climate Downscaling, Reanalysis (ERA5, NOAA) & Numerical Weather Prediction Technology

- Digital Twin, Field Simulation & Virtual Agronomy Technology

- Generative AI, Advisory Chatbot & Agronomic Decision Support Technology

- Blockchain, MRV Data Integrity & Carbon Credit Verification Technology

- Market Size & Forecast by Output Type

- Real-Time Weather & Hyperlocal Forecast Output

- Long-Range Climate Risk Score & Scenario Output

- Crop Yield, Phenology & Productivity Forecast Output

- Carbon Sequestration, GHG Emission & MRV Reporting Output

- Climate Disclosure, Regulatory Compliance & Audit-Ready Output

- Market Size & Forecast by Deployment Scale

- Enterprise & Large Agribusiness Deployment (Above 100,000 Hectares Managed)

- Mid-Tier Cooperative & Aggregator Deployment (1,000 to 100,000 Hectares)

- Smallholder, Individual Farm & Pilot Deployment (Below 1,000 Hectares)

- Market Size & Forecast by Application

- Crop Production & On-Farm Decision Making

- Agricultural Insurance & Risk Underwriting

- Food & Beverage Brand Sustainability & Sourcing

- Agribusiness Trading, Procurement & Commodity Management

- Government, Policy & Regional Climate Adaptation Planning

- Agricultural Lending & Climate-Smart Finance

- Carbon Project Development & Regenerative Agriculture MRV

- Market Size & Forecast by End-User

- Farmer, Producer Group & Agricultural Cooperative

- Agribusiness, Input Supplier & Crop Protection Company

- Crop Insurance Company & Reinsurance Underwriter

- Food, Beverage Brand & Retail Sourcing Company

- Government Agency, Development Bank & Climate Policy Institution

- Market Size & Forecast by Sales Channel

- Direct Subscription & Enterprise Licensing

- Channel Partner, Reseller & Distributor Network

- Embedded API & White-Label Integration

- Consulting, Custom Analytics & Managed Service Engagement

- North America Climate Analytics for Agriculture Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Hectares Covered and Active Subscribers)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Climate Analytics for Agriculture Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Hectares Covered and Active Subscribers)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Climate Analytics for Agriculture Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Hectares Covered and Active Subscribers)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Climate Analytics for Agriculture Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Hectares Covered and Active Subscribers)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Climate Analytics for Agriculture Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Hectares Covered and Active Subscribers)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Climate Analytics for Agriculture Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Hectares Covered and Active Subscribers)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Satellite Remote Sensing (Optical, SAR & Hyperspectral) Analytics Technology Deep-Dive

- AI, Machine Learning & Deep Learning Crop Modelling Technology

- Process-Based Crop Simulation (DSSAT, APSIM & WOFOST) Technology

- Climate Downscaling, Reanalysis & Numerical Weather Prediction Technology

- IoT Weather Station, Soil Sensor & Field Telemetry Integration Technology

- Carbon Sequestration MRV & Soil Organic Carbon Modelling Technology

- Generative AI, Advisory Agent & Agronomic Decision Support Technology

- Patent & IP Landscape in Climate Analytics for Agriculture Technologies

- Value Chain & Supply Chain Analysis

- Satellite Imagery, Earth Observation Data & Commercial Constellation Supply Chain

- Weather Data, Reanalysis & Climate Model Output Provider Supply Chain

- IoT Sensor, Weather Station & Field Hardware Manufacturing Supply Chain

- Software Platform, Cloud Infrastructure & AI Compute Supply Chain

- Agronomic Knowledge, Crop Model & Domain Expertise Supply Chain

- Agribusiness, Insurance & Food Brand End-User Procurement Landscape

- Channel Partner, Reseller, Consulting & System Integrator Ecosystem

- Pricing Analysis

- Weather Forecasting & Hyperlocal Climate Data Subscription Pricing Analysis

- Climate Risk Assessment & Scenario Modelling Pricing Analysis

- Crop Yield Forecasting & Agronomic Analytics Pricing Analysis

- Carbon MRV, Sequestration Verification & Climate Disclosure Pricing Analysis

- Enterprise Licensing, API & White-Label Pricing Structure Analysis

- Total Climate Analytics Subscription Cost Economics: Cost per Hectare & Customer Lifetime Value Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Climate Analytics for Agriculture: Carbon Footprint, Energy Intensity & Compute Footprint Across Solution Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Climate-Smart Agriculture, Regenerative Practices and Soil Carbon Sequestration

- Responsible Data Use, Farmer Privacy & Indigenous Knowledge Due Diligence

- Environmental Compliance, Smallholder Inclusion & Equitable Climate Service Consideration

- Regulatory-Driven Sustainability, EUDR, SDG 2 (Zero Hunger) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Solution Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Solution Type, Technology & Geography

- Player Classification

- Integrated Climate & Agricultural Analytics Platform Companies

- Specialist Weather Forecasting & Hyperlocal Climate Data Providers

- Satellite Earth Observation & Remote Sensing Analytics Companies

- Crop Yield Forecasting & Agronomic Decision Support Vendors

- Carbon MRV, Sequestration Modelling & Climate Disclosure Specialists

- Parametric Insurance & Climate Risk Underwriting Analytics Providers

- Supply Chain Climate Risk & Sourcing Intelligence Platform Vendors

- Consulting, Custom Modelling & Climate Advisory Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Solution Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Climate Analytics for Agriculture Products & Technology Portfolio

- Key Customer Relationships & Reference Enterprise Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Climate Analytics for Agriculture Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Solution Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)