Market Definition

The Global AI-Driven Fleet Management Platforms Market encompasses the development, integration, and commercial deployment of artificial intelligence-powered software platforms, telematics systems, predictive analytics engines, route optimization tools, driver behavior monitoring solutions, and real-time asset tracking architectures used to manage commercial vehicle fleets across road freight, passenger transport, construction, agriculture, and emergency services operations. The market includes IoT-enabled onboard diagnostics hardware, edge computing modules, cloud-based fleet intelligence dashboards, and AI-driven maintenance scheduling systems procured by logistics operators, transportation companies, municipal authorities, and enterprise fleet owners globally.

Market Insights

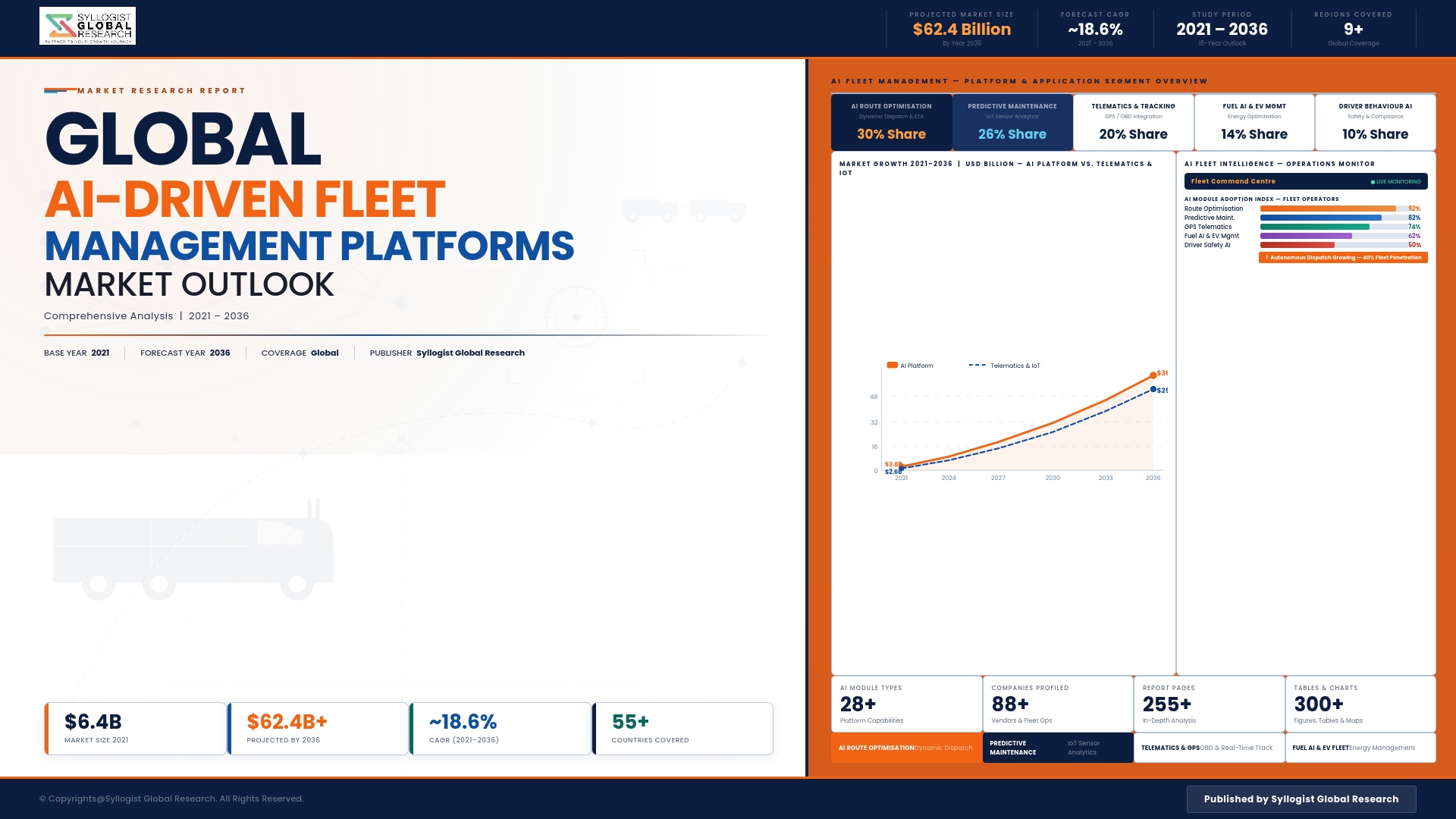

The global AI-driven fleet management platforms market is undergoing a fundamental transformation, propelled by the convergence of ubiquitous IoT sensor deployment across commercial vehicle fleets, maturing machine learning algorithms capable of generating operationally actionable intelligence from continuous vehicle data streams, and intensifying commercial pressure on fleet operators to reduce fuel expenditure, minimize unplanned downtime, improve driver safety compliance, and optimize asset utilization across increasingly complex multi-modal logistics networks. The market was valued at approximately USD 12.6 billion in 2025 and is projected to reach USD 52.3 billion by 2034, advancing at a compound annual growth rate of 17.1% through the forecast period, as AI-powered fleet intelligence transitions from premium capability adopted by large enterprise operators into a standard operational requirement across mid-market and emerging-market fleet organizations responding to competitive cost pressures and regulatory compliance mandates.

The predictive maintenance application is generating the most immediate and quantifiable return on investment across the AI fleet management platform landscape, with machine learning models trained on multi-parameter vehicle health data streams from engine sensors, transmission telemetry, brake system monitors, and tyre pressure management systems delivering component failure predictions that allow fleet maintenance teams to schedule interventions during planned downtime windows rather than responding to roadside breakdowns that generate disproportionate cost and service disruption relative to equivalent scheduled maintenance events. Leading logistics and freight operators deploying enterprise-grade AI fleet platforms are reporting measurable reductions in unplanned vehicle off-road time, maintenance cost per kilometre, and accident-related liability exposure through AI-powered driver behaviour scoring and real-time coaching interventions that identify and correct fatigue, harsh braking, aggressive acceleration, and distracted driving patterns before they generate safety incidents or regulatory compliance violations. The route optimization segment is simultaneously generating compelling efficiency gains across last-mile delivery, long-haul freight, and passenger transport operations through AI algorithms that dynamically recalculate optimal routes incorporating real-time traffic conditions, delivery time window constraints, vehicle load capacity, driver hours-of-service regulations, and fuel consumption parameters simultaneously rather than sequentially, delivering per-vehicle fuel and time savings that compound across large fleet deployments into material operating cost advantages.

The electric vehicle fleet management segment is emerging as the fastest-growing application category within the broader AI fleet platform market, driven by rapid commercial EV fleet adoption among parcel delivery operators, municipal transit agencies, and corporate mobility managers who require AI-powered charge scheduling, range anxiety management, and battery health monitoring capabilities not addressed by conventional fleet telematics platforms designed for internal combustion engine vehicle operations. Cloud-native AI fleet platform architectures are displacing legacy on-premises telematics systems at an accelerating pace, driven by the scalability, real-time processing capability, and continuous machine learning model improvement that cloud deployment enables relative to static on-premises software environments. North America maintains the largest absolute market share, anchored by the scale of commercial logistics operations, early AI platform adoption among leading freight carriers, and the concentration of fleet management technology developers. Europe represents the second major regional contributor, driven by stringent tachograph and hours-of-service compliance requirements, carbon emissions reporting mandates, and substantial commercial vehicle fleet density across Germany, France, the United Kingdom, and the Benelux logistics corridor. Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, underpinned by rapid logistics sector expansion in China, India, and Southeast Asia and accelerating commercial EV fleet deployment across urban delivery operations.

Key Drivers

Escalating Fleet Operating Cost Pressures and Fuel Efficiency Imperatives Compelling Logistics and Transport Operators to Deploy AI-Powered Optimization and Predictive Maintenance Capabilities

Persistent elevation of fuel costs, driver wage inflation, insurance premium increases, and tightening vehicle emission compliance expenditure are collectively compressing operating margins across commercial road freight, passenger transport, and logistics sectors to levels that make AI-driven fleet efficiency optimization a financially mandatory capability investment rather than an optional technology enhancement for operators managing fleets of commercially relevant scale. Fleet operators deploying AI-powered route optimization, predictive maintenance scheduling, and driver behaviour management systems are generating documented reductions in fuel consumption, unplanned maintenance expenditure, and accident-related liability costs that deliver payback periods sufficiently short to justify platform investment even in capital-constrained operating environments, creating a compelling commercial case that is driving adoption acceleration across fleet size categories and industry verticals globally.

Regulatory Compliance Complexity and Driver Safety Mandate Expansion Across Major Markets Driving Enterprise Demand for AI-Powered Monitoring, Reporting, and Violation Prevention Platforms

The expanding scope of commercial vehicle regulatory compliance obligations across tachograph recording, hours-of-service enforcement, emissions zone restriction compliance, dangerous goods transport documentation, and driver fatigue management is generating enterprise demand for AI fleet platforms capable of automating compliance monitoring, generating audit-ready regulatory reports, and proactively alerting fleet managers to potential violations before regulatory penalties are incurred. Progressive introduction of mandatory advanced driver assistance systems, intelligent speed assistance, and lane-keeping requirement frameworks across the European Union and other major regulatory jurisdictions is simultaneously creating hardware and software integration requirements that AI fleet management platform providers are well positioned to address through onboard telematics and driver monitoring system integration within unified fleet intelligence architectures.

Commercial Electric Vehicle Fleet Adoption and the Need for AI-Powered Charge Management, Range Optimization, and Battery Health Analytics Creating a Structurally New Platform Demand Category

The accelerating transition of commercial delivery, municipal transit, and corporate mobility fleets toward battery electric vehicles is generating a structurally new and rapidly expanding demand category for AI fleet management platforms capable of addressing the operationally distinct requirements of EV fleet management, including intelligent charge scheduling that minimizes energy cost while ensuring vehicle availability, real-time range prediction accounting for load weight, route topography, ambient temperature, and driver behaviour variables, and machine learning-driven battery degradation monitoring that optimizes charge cycles to extend battery pack service life and reduce total cost of ownership across multi-year commercial fleet deployment horizons.

Key Challenges

Data Integration Complexity Across Heterogeneous Vehicle Makes, Telematics Hardware Generations, and Legacy Fleet Management System Environments Constraining AI Platform Deployment Efficiency

Commercial fleet operators typically manage vehicle inventories spanning multiple manufacturers, model years, powertrain technologies, and installed telematics hardware generations, creating data integration environments of substantial heterogeneity where AI fleet platform providers must normalize inconsistent sensor data formats, communications protocols, and vehicle network standards before meaningful machine learning model training and real-time operational intelligence generation can be achieved. The absence of universally adopted vehicle data communication standards across original equipment manufacturers imposes platform development costs, integration timeline extensions, and ongoing data quality management burdens that disproportionately constrain AI fleet platform deployment among mid-market operators lacking the internal technical resources to manage complex multi-source vehicle data integration projects alongside core fleet operations responsibilities.

Driver Privacy Concerns, Labour Relations Opposition, and Data Governance Regulatory Complexity Surrounding Continuous AI-Powered Driver Monitoring and Behavioural Scoring Systems

The deployment of AI-powered driver behaviour monitoring systems incorporating continuous video recording, biometric fatigue detection, real-time location tracking, and individual performance scoring is generating significant driver privacy concerns, trade union opposition, and works council approval requirements across European and other jurisdictions with strong labour protection frameworks, creating organizational resistance and regulatory compliance burdens that extend platform implementation timelines and limit the behavioural monitoring feature scope that operators can deploy within applicable employment law and collective bargaining agreement constraints. Data protection regulatory requirements governing the collection, retention, processing, and cross-border transfer of individual driver monitoring data impose additional compliance obligations on AI fleet platform providers and fleet operator customers that are particularly complex to manage across multinational operations spanning jurisdictions with divergent data protection frameworks.

Cybersecurity Vulnerabilities in Connected Fleet Telematics Infrastructure and the Risk of AI Model Manipulation Threatening Operational Integrity and Safety-Critical Fleet Decisions

AI-driven fleet management platforms that aggregate real-time vehicle location, cargo contents, route scheduling, and driver identity data across enterprise-scale connected vehicle networks represent high-value cybersecurity targets whose compromise could expose commercially sensitive logistics intelligence, enable cargo theft through route interception, facilitate regulatory compliance fraud through tampered tachograph or hours-of-service data, or generate safety-critical fleet management errors through adversarial manipulation of AI route optimization and maintenance scheduling algorithms. The growing connectivity of commercial vehicles through multiple simultaneous communication channels including cellular telematics, satellite positioning, roadside infrastructure communication, and mobile device integration is expanding the attack surface available to sophisticated threat actors targeting fleet operations and the sensitive personal and commercial data that AI fleet platforms process and retain.

Market Segmentation

- Segmentation By Solution Type

- AI-Powered Predictive Maintenance Platforms

- Real-Time Route Optimization and Dispatch Systems

- Driver Behaviour Monitoring and Coaching Solutions

- Electric Vehicle Fleet Charge and Range Management Platforms

- Fleet Asset Tracking and Visibility Systems

- Fuel Management and Consumption Analytics Platforms

- Regulatory Compliance and Reporting Automation Solutions

- Others

- Segmentation By Fleet Type

- Long-Haul and Over-the-Road Freight Fleets

- Last-Mile and Urban Delivery Fleets

- Passenger Transport and Ride-Hailing Fleets

- Municipal and Public Transit Fleets

- Construction and Heavy Equipment Fleets

- Emergency Services and Government Fleets

- Agricultural and Off-Highway Vehicle Fleets

- Others

- Segmentation By Deployment Mode

- Cloud-Based SaaS Deployment

- On-Premises Deployment

- Hybrid Cloud and On-Premises Deployment

- Segmentation By Application

- Predictive and Condition-Based Maintenance Scheduling

- Dynamic Route Planning and Optimization

- Driver Safety Scoring and Real-Time Coaching

- EV Charge Scheduling and Battery Health Management

- Fuel Consumption Monitoring and Reduction

- Regulatory Compliance Monitoring and Reporting

- Fleet Utilization and Asset Lifecycle Management

- Others

- Segmentation By Component

- AI Analytics and Machine Learning Software Engines

- Telematics Hardware and Onboard Diagnostic Units

- IoT Sensors and Edge Computing Modules

- Fleet Management Dashboards and Mobile Applications

- API Integration and Data Connectivity Middleware

- Cybersecurity and Data Protection Solutions

- Others

- Segmentation By End User

- Third-Party Logistics and Freight Carriers

- E-Commerce and Parcel Delivery Operators

- Municipal and Government Transport Authorities

- Construction and Infrastructure Companies

- Oil, Gas, and Utilities Field Service Operators

- Corporate and Enterprise Fleet Owners

- Rental and Leasing Companies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the AI-Driven Fleet Management Platforms Market in 2025, projected through 2034, disaggregated by solution type, fleet type, and application, enabling logistics operators, technology developers, and investors to identify the highest-growth segments and most durable revenue opportunities across the AI fleet intelligence value chain?

- How are leading logistics carriers, parcel delivery operators, and municipal fleet authorities structuring AI platform investment across predictive maintenance, route optimization, and driver monitoring applications, and which deployment architectures and capability combinations are generating the most measurable operational cost reduction and return on investment across large commercial fleet environments?

- What specific AI fleet management capabilities are required to address the operationally distinct requirements of electric vehicle fleet operations, including charge scheduling, range prediction, and battery health analytics, and how are platform developers differentiating their EV fleet management offerings to capture the fastest-growing segment of the commercial vehicle transition?

- Which AI fleet management solution segments, including predictive maintenance, dynamic route optimization, and regulatory compliance automation, are generating the highest adoption and subscription revenue growth rates through 2034, and what AI model performance and integration capability benchmarks are most critical to platform selection across commercial fleet operator categories?

- How is the competitive landscape structured among enterprise telematics incumbents, cloud-native AI fleet platform startups, automotive OEM connected services divisions, and logistics technology companies, and what partnership, acquisition, and data ecosystem strategies are enabling leading developers to expand addressable market share across fleet size segments and geographies?

- What data integration complexity, driver privacy regulation, and cybersecurity challenges are constraining AI fleet platform deployment timelines and feature adoption rates, and how are platform providers and fleet operators addressing heterogeneous vehicle data standards, labour relations considerations, and connected vehicle security requirements within commercial implementation programs?

- Which regional fleet management markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most substantial incremental AI platform adoption through 2034, and what logistics sector growth trajectories, commercial EV deployment rates, and regulatory compliance frameworks are driving technology investment priorities and vendor selection decisions in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Data Privacy, Telematics Data Sovereignty & Driver Surveillance Regulatory Compliance Risk

- AI Model Accuracy, False Positive Maintenance Alerts & Liability Risk in Autonomous Fleet Decision Support

- Cybersecurity, Connected Vehicle Network Vulnerability & Fleet Platform Data Breach Risk

- Connectivity Dependency, Rural Coverage Gaps & Real-Time Fleet Visibility Disruption Risk

- Platform Vendor Lock-In, Integration Complexity with Legacy Telematics & Multi-OEM Fleet Interoperability Risk

- Regulatory Framework & Standards

- Electronic Logging Device (ELD) Mandate, Hours of Service (HOS) Rules & Commercial Vehicle Compliance Regulations in Key Markets

- GDPR, CCPA & Cross-Border Telematics Data Protection Regulations Governing Driver & Vehicle Data in Fleet Platforms

- Tachograph Regulation (EU 165/2014), Digital Tachograph & Smart Tachograph Requirements for Commercial Road Transport

- Vehicle Telematics, OBD-II & CAN Bus Data Access Standards: ISO 15765, SAE J1939 & AUTOSAR Fleet Data Interface Frameworks

- Road Safety, Driver Monitoring, Distracted Driving & In-Cab AI Surveillance Regulatory Frameworks Across Jurisdictions

- Global AI-Driven Fleet Management Platforms Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Connected Vehicles & Active Platform Subscriptions)

- Market Size & Forecast by Solution Type

- AI-Powered Predictive Maintenance & Vehicle Health Monitoring Platform

- Intelligent Route Optimisation, Dispatch & Real-Time Navigation Platform

- Driver Behaviour Analytics, Coaching & Safety Scoring Platform

- AI-Driven Fuel & Energy Consumption Management Platform

- Fleet Utilisation, Asset Tracking & Real-Time Visibility Platform

- Compliance Management, ELD, HOS & Regulatory Reporting Platform

- AI-Enabled Load Optimisation, Freight Matching & Last-Mile Delivery Platform

- Integrated Fleet Intelligence Suite: End-to-End AI Fleet Management Platform

- Market Size & Forecast by Component

- Software Platform: SaaS, Cloud-Native Fleet Management Application

- Telematics Hardware: On-Board Unit (OBU), GPS Tracker & Vehicle Gateway Device

- In-Cab Device: Driver-Facing Camera (DFC), Dashcam & Driver Monitoring System (DMS) Hardware

- IoT Sensors: Tyre Pressure Monitoring, Temperature Sensor & Cargo Condition Monitoring Hardware

- Connectivity Module: 4G LTE, 5G & Satellite Communication Unit

- Professional Services: Implementation, Integration, Training & Managed Services

- Market Size & Forecast by Technology

- Machine Learning (ML) & Deep Learning for Predictive Maintenance, Fault Detection & RUL Estimation

- Computer Vision & AI Video Analytics for Driver Behaviour Monitoring & Road Event Detection

- Natural Language Processing (NLP) & Conversational AI for Fleet Manager Decision Support

- Reinforcement Learning & AI Optimisation Algorithms for Dynamic Route & Dispatch Planning

- Digital Twin & Simulation Technology for Fleet Asset Lifecycle & Scenario Planning

- Edge AI & On-Board Processing for Real-Time In-Vehicle Analytics & Low-Latency Decision Making

- IoT & Industrial Internet of Things (IIoT) Sensor Fusion for Holistic Vehicle & Cargo Telemetry

- Generative AI & Large Language Model (LLM) Integration for Fleet Reporting & Insight Automation

- Market Size & Forecast by Fleet Type

- Light Commercial Vehicle (LCV) & Last-Mile Delivery Fleet

- Heavy-Duty Truck & Long-Haul Freight Fleet

- Bus, Coach & Public Transit Fleet

- Construction, Mining & Off-Highway Equipment Fleet

- Emergency Services, Ambulance & Government Vehicle Fleet

- Passenger Car & Ride-Hailing Fleet

- Electric Vehicle (EV) & Mixed-Fuel Fleet

- Rental, Leasing & Shared Mobility Fleet

- Market Size & Forecast by Deployment Mode

- Cloud-Based (SaaS) Deployment

- On-Premise Deployment

- Hybrid Deployment

- Market Size & Forecast by Organisation Size

- Large Enterprise Fleet (Above 500 Vehicles)

- Mid-Market Fleet (51 to 500 Vehicles)

- Small & Micro Fleet (Up to 50 Vehicles)

- Market Size & Forecast by Application

- Predictive Maintenance & Unplanned Downtime Reduction

- Route Optimisation & Fuel Cost Reduction

- Driver Safety, Risk Reduction & Insurance Telematics

- Regulatory Compliance, ELD & HOS Management

- Fleet Utilisation Improvement & Asset Lifecycle Management

- Cold Chain, Cargo Condition & Last-Mile Delivery Optimisation

- EV Fleet Charging Scheduling, Range Management & Battery Health Optimisation

- Market Size & Forecast by End-User

- Road Freight, Logistics & Third-Party Logistics (3PL) Operators

- Last-Mile Delivery, E-Commerce Fulfilment & Courier Companies

- Public Transit Authorities & Bus Fleet Operators

- Construction, Infrastructure & Mining Equipment Fleet Operators

- Utility, Field Service & Workforce Fleet Operators

- Emergency Services, Law Enforcement & Government Fleet Operators

- Car Rental, Leasing & Shared Mobility Operators

- Market Size & Forecast by Sales Channel

- Direct Software Vendor & Platform Provider Sales

- Telematics Hardware OEM & Vehicle Manufacturer Bundled Channel

- Systems Integrator, Value-Added Reseller (VAR) & Partner Channel

- Telecom Operator & Connectivity Provider Bundled Fleet Solution Channel

- North America AI-Driven Fleet Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Connected Vehicles & Active Platform Subscriptions)

- By Solution Type

- By Component

- By Technology

- By Fleet Type

- By Deployment Mode

- By Organisation Size

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe AI-Driven Fleet Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Connected Vehicles & Active Platform Subscriptions)

- By Solution Type

- By Component

- By Technology

- By Fleet Type

- By Deployment Mode

- By Organisation Size

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific AI-Driven Fleet Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Connected Vehicles & Active Platform Subscriptions)

- By Solution Type

- By Component

- By Technology

- By Fleet Type

- By Deployment Mode

- By Organisation Size

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America AI-Driven Fleet Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Connected Vehicles & Active Platform Subscriptions)

- By Solution Type

- By Component

- By Technology

- By Fleet Type

- By Deployment Mode

- By Organisation Size

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa AI-Driven Fleet Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Connected Vehicles & Active Platform Subscriptions)

- By Solution Type

- By Component

- By Technology

- By Fleet Type

- By Deployment Mode

- By Organisation Size

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* AI-Driven Fleet Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Connected Vehicles & Active Platform Subscriptions)

- By Solution Type

- By Component

- By Technology

- By Fleet Type

- By Deployment Mode

- By Organisation Size

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- AI Predictive Maintenance, Fault Prognostics & Remaining Useful Life (RUL) Estimation Technology Deep-Dive

- Computer Vision, AI Dashcam & Driver Monitoring System (DMS) Technology for Fleet Safety

- Reinforcement Learning, Dynamic Routing & AI-Powered Dispatch Optimisation Technology

- Digital Twin & Simulation Technology for Fleet Asset Lifecycle Modelling & Scenario Analysis

- Edge AI, On-Board Processing & Low-Latency In-Vehicle Analytics Technology

- Generative AI & LLM Integration for Fleet Reporting, Insight Automation & Natural Language Querying

- EV Fleet Intelligence: AI-Driven Battery Health Monitoring, Charging Optimisation & Range Prediction Technology

- Patent & IP Landscape in AI Fleet Management, Telematics & Connected Vehicle Analytics Technologies

- Value Chain & Supply Chain Analysis

- AI Algorithm, Machine Learning Model & Fleet Analytics Software Development Supply Chain

- Telematics Hardware: OBU, GPS Module, Vehicle Gateway & IoT Sensor Manufacturing Supply Chain

- In-Cab Camera, Driver-Facing Camera (DFC) & Video Telematics Hardware Supply Chain

- Connectivity Module: 4G LTE, 5G & Satellite Communication Component Supply Chain

- Cloud Infrastructure, Data Centre & Edge Computing Platform Supply Chain

- Systems Integrator, Value-Added Reseller (VAR) & Fleet Solution Implementation Partner Channel

- Fleet Operator, Transport Logistics & End-User Direct Subscription Channel

- Pricing Analysis

- Fleet Management SaaS Platform Subscription Pricing: Per-Vehicle Per-Month Benchmarking by Solution Tier & Feature Set

- Telematics Hardware Unit Cost Analysis: OBU, GPS Tracker, Video Telematics Camera & IoT Sensor Benchmarking

- Professional Services Pricing: Implementation, Integration, Customisation & Training Cost Analysis

- Connectivity Cost Analysis: 4G LTE, 5G & Satellite Data Plan Pricing per Connected Vehicle

- Total Cost of Ownership (TCO) & Return on Investment (ROI) Analysis for AI Fleet Management Platform Deployment

- Value-Based Pricing Models: Fuel Savings, Maintenance Cost Avoidance, Accident Reduction & Productivity Gain Quantification

- Sustainability & Environmental Analysis

- AI Route Optimisation & Eco-Driving Coaching: Fuel Consumption Reduction, CO2 Emission Abatement & Carbon Footprint Quantification

- Predictive Maintenance & Component Life Extension: Material Waste Reduction, Premature Part Replacement Avoidance & Circular Economy Contribution

- EV Fleet Management & Intelligent Charging Optimisation: Grid Load Management & Renewable Energy Integration Contribution

- Fleet Downsizing, Asset Utilisation Improvement & Vehicle km Travelled (VKT) Reduction Through AI Optimisation

- Regulatory-Driven Sustainability: Fleet Carbon Reporting, Scope 1 & Scope 3 Emission Disclosure & Net Zero Fleet Transition Roadmap Support

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Solution Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Solution Type, Technology & Geography

- Player Classification

- Integrated AI Fleet Management Platform Vendors: End-to-End Suite Providers

- Specialist AI Predictive Maintenance & Vehicle Health Analytics Platform Providers

- Video Telematics, Driver Safety & In-Cab AI Monitoring Solution Providers

- Route Optimisation, Dispatch & Last-Mile Delivery AI Platform Providers

- Telematics Hardware OEMs & Connected Vehicle Device Manufacturers

- Automotive OEMs & Vehicle Manufacturers with Embedded Fleet Management Platforms

- Telecom Operators & Connectivity Providers Offering Bundled Fleet Solutions

- EV-Specific Fleet Intelligence & Charging Management Platform Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Solution Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- AI Fleet Management Products & Technology Portfolio

- Key Customer Relationships & Reference Fleet Installations

- Manufacturing Footprint & Delivery Capacity

- Revenue (AI Fleet Management Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Market Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Solution Type, Technology, Fleet Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)