Market Definition

The Global Autonomous Logistics and Delivery Vehicles Market encompasses the development, manufacturing, deployment, and commercial operation of self-driving ground vehicles, autonomous mobile robots, unmanned aerial delivery systems, and autonomous marine freight vessels used for goods movement, last-mile parcel delivery, warehouse logistics, port and terminal operations, and long-haul freight transport. The market includes associated perception sensor suites, AI navigation software, vehicle-to-infrastructure communication hardware, fleet orchestration platforms, and remote monitoring systems procured by logistics operators, e-commerce companies, retailers, port authorities, and third-party delivery service providers globally.

Market Insights

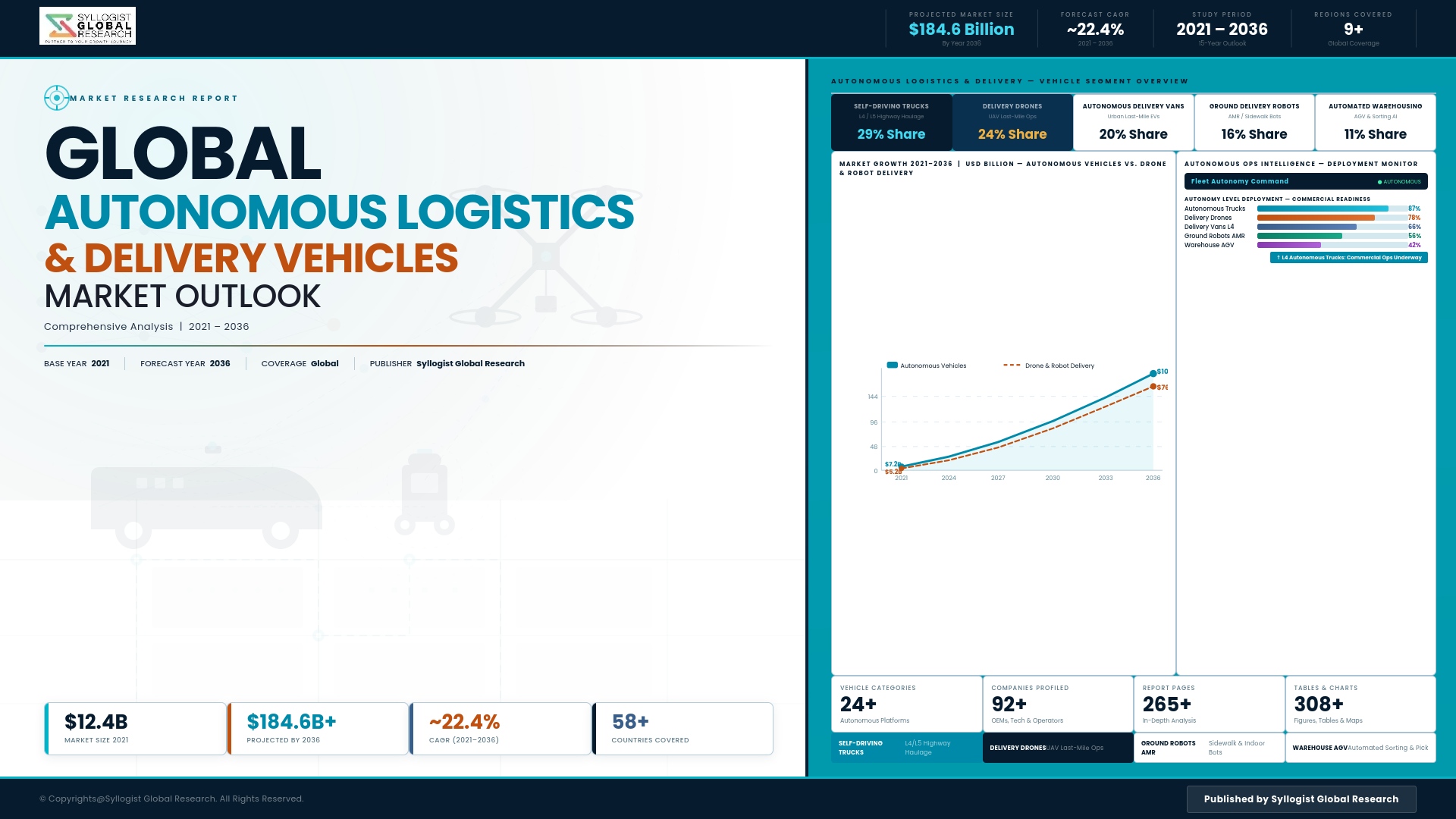

The global autonomous logistics and delivery vehicles market is approaching a pivotal commercial inflection point, shaped by the convergence of sensor cost deflation enabling affordable perception system deployment, AI navigation software maturity reaching operationally viable performance thresholds across constrained delivery environments, and an e-commerce volume growth trajectory that is generating last-mile delivery cost pressures of a magnitude that makes autonomous vehicle deployment a financially compelling response to structural labor shortage and wage inflation dynamics across major logistics markets. The market was valued at approximately USD 17.4 billion in 2025 and is projected to reach USD 108.6 billion by 2034, advancing at a compound annual growth rate of 22.6% through the forecast period, as autonomous ground delivery vehicles, sidewalk robots, autonomous mobile robots within fulfillment centers, and long-haul autonomous freight trucks each transition from geographically constrained pilot operations into commercially scaled deployments across major metropolitan and freight corridor markets in North America, Europe, and Asia-Pacific.

The warehouse and fulfillment center segment currently represents the most commercially mature autonomous vehicle deployment category, with autonomous mobile robots performing goods-to-person picking, intralogistics transport, sortation, and inventory management functions at commercially validated performance levels across large-scale fulfillment operations run by leading e-commerce and third-party logistics providers. The operational predictability of structured warehouse environments, combined with the absence of regulatory barriers governing indoor autonomous vehicle deployment, has enabled rapid scaling of warehouse autonomous mobile robot deployments that are delivering measurable throughput improvements, labor cost reductions, and order accuracy gains that generate payback periods sufficiently short to justify accelerating capital deployment into autonomous intralogistics systems across the global fulfillment infrastructure investment cycle. Last-mile autonomous ground delivery, encompassing both sidewalk delivery robots and autonomous delivery vans operating on public roads, is the segment generating the greatest commercial investor interest, driven by the structural economics of last-mile parcel delivery where labor represents the dominant cost component and the density of urban delivery stop concentrations in major metropolitan markets creates operationally favorable deployment conditions for autonomous vehicle unit economics.

Long-haul autonomous freight trucking is advancing along a distinct commercial trajectory characterized by geographically defined highway corridor deployments where consistent operating domain conditions allow current-generation autonomous driving systems to achieve safety and reliability performance meeting carrier and shipper acceptance thresholds, with commercial operations expanding across defined freight corridors in the United States Sun Belt, European motorway networks, and Chinese expressways. Autonomous drone delivery is simultaneously scaling from single-operator pilot programs into multi-vehicle fleet operations serving rural healthcare logistics, offshore supply chain management, and low-density suburban parcel delivery use cases where the absence of viable conventional delivery infrastructure creates a commercially addressable market for aerial autonomous delivery at near-term economics that do not require the ultra-high volume density necessary to justify autonomous ground vehicle deployment. North America maintains the largest absolute market share, anchored by substantial e-commerce logistics investment, progressive autonomous vehicle regulatory frameworks, and the concentration of autonomous vehicle technology developers. Asia-Pacific is projected to record the highest compound annual growth rate through 2034, driven by China’s national autonomous vehicle commercialization program, India’s rapidly expanding e-commerce logistics infrastructure, and Southeast Asian urban delivery markets presenting high autonomous vehicle deployment potential. Europe represents the third major contributor, with structured regulatory harmonization under the EU autonomous vehicle framework supporting cross-border autonomous freight operations and fulfillment automation investment across major logistics hub markets.

Key Drivers

Structural Last-Mile Delivery Labor Shortages, Chronic Driver Deficits, and Sustained Wage Inflation Generating Financially Compelling Economics for Autonomous Delivery Vehicle Deployment

The logistics and delivery sector across North America, Europe, and increasingly Asia-Pacific is confronting a structural deficit of qualified commercial drivers, warehouse pickers, and last-mile delivery personnel that is simultaneously constraining service capacity expansion and driving wage inflation that materially compresses operating margins across parcel delivery, freight transport, and fulfillment operations. The structural nature of this labor challenge, rooted in demographic trends, competing employment alternatives, and the physically demanding conditions of logistics roles, means that autonomous vehicle deployment is increasingly evaluated not merely as a cost optimization lever but as a capacity enablement strategy for logistics operators whose growth ambitions are fundamentally constrained by the inability to recruit sufficient human workforce at commercially viable compensation levels within competitive labor markets.

Exponential E-Commerce Volume Growth and the Compounding Unit Economics Pressure on Last-Mile Delivery Networks Driving Autonomous Vehicle Commercialization Investment at Scale

The sustained exponential growth of e-commerce parcel volumes, accelerated by pandemic-driven behavioral shifts that have structurally elevated online purchasing penetration across consumer demographics and product categories, is generating last-mile delivery volume densities in major metropolitan markets that both create operationally favorable conditions for autonomous vehicle deployment and impose unit economics pressure on delivery network operators severe enough to justify the capital investment and operational transformation required to transition from human-operated to autonomous delivery at commercial scale. The cost per delivery trajectory of autonomous vehicles at mature deployment scale across high-density urban routes is compelling enough to drive investment despite near-term technology and regulatory uncertainty, with leading logistics operators and e-commerce companies treating autonomous delivery capability development as a strategic competitive imperative.

Sensor Cost Deflation, AI Navigation Software Maturity, and Compute Hardware Performance Advancement Collectively Enabling Commercially Viable Autonomous Vehicle System Economics Across Multiple Deployment Categories

The dramatic reduction in LiDAR, radar, and camera sensor unit costs achieved through technology maturation and manufacturing scale, combined with AI navigation software capability reaching operationally acceptable safety and reliability performance thresholds in defined operational design domains, and the continued improvement in autonomous driving compute hardware performance per watt and per unit cost, are collectively enabling autonomous logistics vehicle system economics to cross commercial viability thresholds across warehouse robotics, sidewalk delivery, and highway freight applications simultaneously. This convergence of enabling technology cost curves reaching commercial feasibility within overlapping timeframes is compressing the sequential deployment timeline that characterized earlier autonomous vehicle commercialization forecasts and creating parallel commercial scaling opportunity across multiple autonomous logistics vehicle categories.

Key Challenges

Regulatory Framework Fragmentation, Autonomous Vehicle Certification Complexity, and Public Road Operational Approval Timelines Constraining Geographic Deployment Expansion Pace

The absence of harmonized international regulatory frameworks governing the certification, registration, insurance, and public road operation of autonomous commercial vehicles across national and subnational jurisdictions is creating a fragmented approval landscape that forces autonomous vehicle operators and developers to pursue jurisdiction-specific regulatory engagement processes of substantial complexity, cost, and elapsed time, constraining the pace at which commercially validated autonomous logistics operations can be replicated and scaled across new geographic markets. Regulatory uncertainty regarding liability allocation in autonomous vehicle incidents, the absence of standardized safety certification testing protocols accepted across major markets, and inconsistent municipal permitting requirements for sidewalk robot and autonomous delivery van operations collectively impose deployment timeline extensions that slow commercial revenue scaling relative to technology readiness milestones.

Edge Case Perception Failures, Operational Design Domain Constraints, and Adverse Weather Performance Limitations Restricting Autonomous Vehicle All-Condition Commercial Reliability

Current-generation autonomous logistics vehicle perception and navigation systems demonstrate performance degradation in adverse weather conditions including heavy precipitation, snow accumulation, fog, and direct solar glare that constrains all-weather operational availability to levels below the continuous delivery service reliability standards that logistics customers and operators require for commercial deployment without human fallback capability. The long-tail distribution of rare but operationally critical edge case scenarios encountered in public road delivery environments, including novel obstacle configurations, unexpected pedestrian behavior, road infrastructure deterioration, and emergency vehicle interactions, continues to challenge AI navigation system robustness in ways that require either expanded operational design domain constraints limiting commercial addressable market or continued software development investment before unrestricted commercial deployment becomes operationally viable.

High Capital Expenditure Requirements, Vehicle Unit Cost Elevation Above Human-Operated Alternatives, and Extended Payback Period Uncertainty Constraining Private Investment Deployment Rate

Autonomous logistics and delivery vehicles carry substantially higher unit acquisition costs than equivalent human-operated vehicle platforms due to the sensor suites, compute hardware, redundant safety systems, and specialized software licensing embedded within each autonomous vehicle unit, creating capital expenditure requirements that impose challenging payback period economics for logistics operators whose return on investment modeling is sensitive to uncertain autonomous vehicle uptime performance, software maintenance cost trajectories, and the pace of volume density scaling within initially limited deployment geographies. The capital intensity of autonomous vehicle fleet deployment at commercially relevant scale, combined with the ongoing operational expenditure associated with remote monitoring, software updates, and vehicle maintenance, limits near-term autonomous vehicle economics to use cases with the highest delivery density, labor cost exposure, or strategic differentiation value.

Market Segmentation

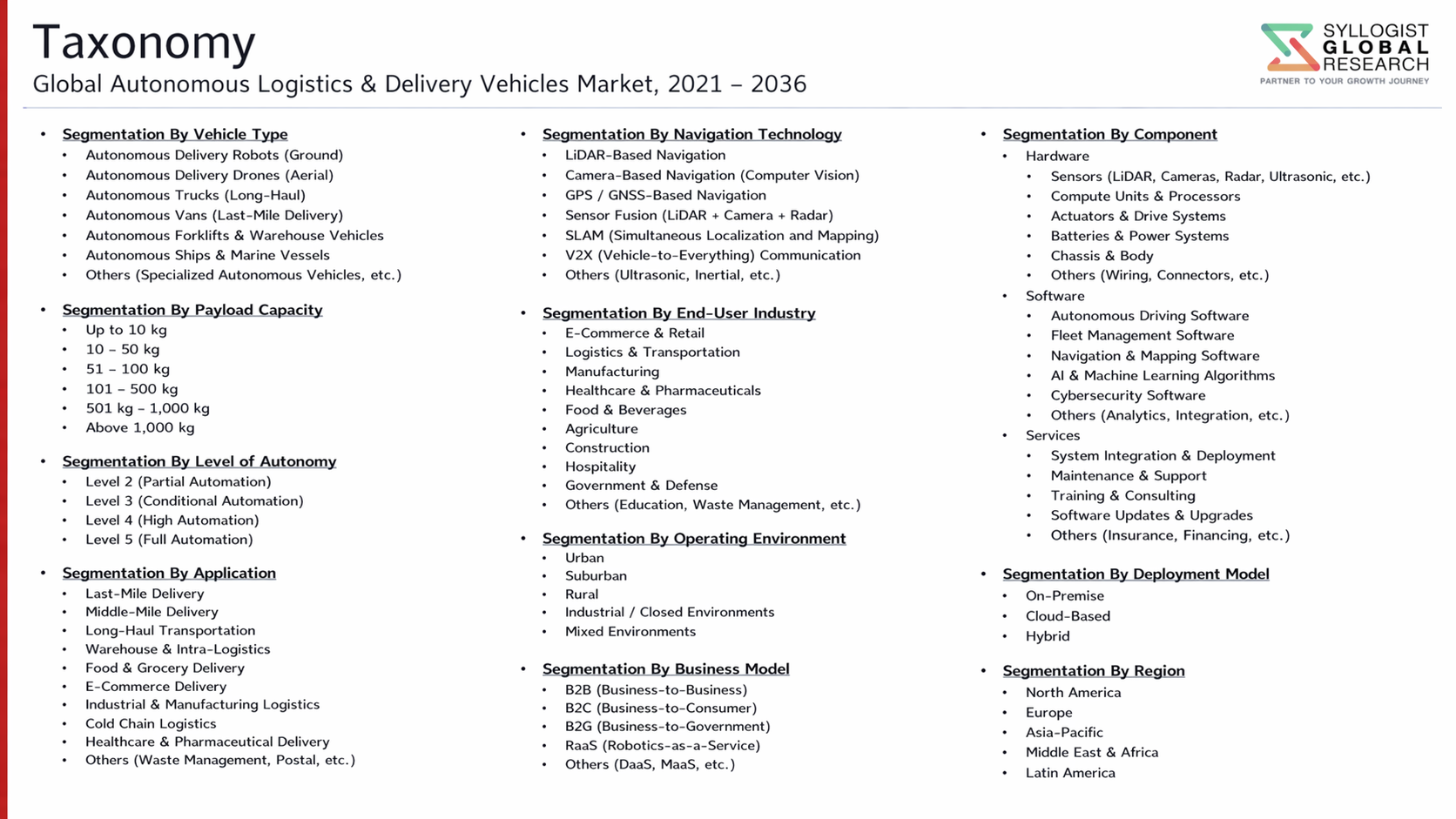

- Segmentation By Vehicle Type

- Autonomous Ground Delivery Vehicles and Vans

- Sidewalk Delivery Robots and Micro-Mobility Bots

- Autonomous Mobile Robots (AMR) for Warehouse and Fulfillment

- Autonomous Long-Haul Freight Trucks

- Unmanned Aerial Delivery Drones

- Autonomous Port and Terminal Handling Vehicles

- Autonomous Marine and Inland Waterway Freight Vessels

- Others

- Segmentation By Autonomy Level

- Level 2 and Level 3 Partial Automation with Human Supervision

- Level 4 High Automation within Defined Operational Design Domains

- Level 5 Full Automation without Human Intervention

- Segmentation By Technology

- LiDAR-Based Perception and Navigation Systems

- Camera and Computer Vision Navigation Systems

- Radar and Sensor Fusion Architectures

- AI and Deep Learning Navigation Software Platforms

- Vehicle-to-Infrastructure (V2I) Communication Systems

- Fleet Orchestration and Remote Monitoring Platforms

- Others

- Segmentation By Application

- Last-Mile Urban and Suburban Parcel Delivery

- Warehouse Intralogistics and Order Fulfillment

- Long-Haul and Middle-Mile Freight Transport

- Grocery and Food Delivery Logistics

- Healthcare and Pharmaceutical Supply Chain Delivery

- Port, Terminal, and Intermodal Freight Handling

- Rural and Remote Area Supply Chain Delivery

- Others

- Segmentation By Payload Capacity

- Ultra-Light Payload (Below 5 kg)

- Light Payload (5 kg to 100 kg)

- Medium Payload (100 kg to 1,000 kg)

- Heavy Payload (Above 1,000 kg)

- Segmentation By End User

- E-Commerce and Online Retail Operators

- Third-Party Logistics and Courier Companies

- Grocery Retailers and Food Service Providers

- Healthcare and Pharmaceutical Distributors

- Port Authorities and Terminal Operators

- Manufacturing and Industrial Supply Chain Operators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Autonomous Logistics and Delivery Vehicles Market in 2025, projected through 2034, disaggregated by vehicle type, autonomy level, and application, enabling logistics operators, technology developers, and investors to identify the highest-growth deployment segments and most durable revenue opportunities across the autonomous logistics value chain?

- How are leading e-commerce operators, third-party logistics companies, and freight carriers structuring autonomous vehicle deployment programs across last-mile delivery, warehouse fulfillment, and long-haul freight applications, and which vehicle categories and operational design domains are generating commercially validated unit economics that support accelerated fleet scaling through 2034?

- What is the current regulatory approval status of autonomous commercial vehicle operations across the United States, European Union, China, and key Asia-Pacific markets, and how are technology developers and logistics operators navigating certification complexity, liability frameworks, and municipal permitting requirements to expand geographic deployment coverage within active commercial programs?

- Which autonomous logistics vehicle segments, including warehouse AMRs, sidewalk delivery robots, autonomous freight trucks, and aerial delivery drones, are generating the highest near-term revenue growth and commercial deployment activity, and what perception technology, AI software, and operational design domain capabilities are most critical to achieving reliable all-condition performance?

- How is the competitive landscape structured among autonomous vehicle technology developers, commercial vehicle manufacturers, logistics operator in-house development programs, and robotics platform companies, and what partnership, acquisition, and ecosystem integration strategies are enabling leading players to establish durable commercial positions across autonomous logistics vehicle categories?

- What capital expenditure requirements, payback period economics, and adverse weather performance limitations are constraining autonomous logistics vehicle deployment rates, and how are technology developers, logistics operators, and investors addressing unit cost reduction pathways, operational availability improvement, and financing structures to accelerate commercial scaling?

- Which regional autonomous logistics markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most substantial incremental deployment activity through 2034, and what e-commerce growth trajectories, autonomous vehicle regulatory frameworks, labor market conditions, and infrastructure investment programs are shaping deployment priorities and technology procurement decisions in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Regulatory Approval, Autonomous Vehicle Certification & Jurisdiction-by-Jurisdiction Operational Permit Risk

- Safety Validation, Edge Case Failure, Liability Attribution & Insurance Framework Risk for Autonomous Logistics Operations

- Cybersecurity, Remote Vehicle Hijacking & Autonomous Fleet Data Breach Risk

- Technology Readiness, Sensor Degradation in Adverse Weather & Operational Design Domain (ODD) Limitation Risk

- Public Acceptance, Labour Displacement Backlash & Workforce Transition Risk in Logistics & Delivery Sectors

- Regulatory Framework & Standards

- SAE J3016 Automation Levels, UN WP.29 ALKS Regulation & National Autonomous Vehicle Legislation Governing Logistics Platforms

- FMCSA Autonomous Trucking Regulations, NHTSA AV Guidance & US State-Level Autonomous Delivery Vehicle Permit Frameworks

- EU Automated Driving Regulation (2019/2144), Type-Approval Framework & UNECE WP.29 Standards for Autonomous Commercial Vehicles

- Drone & UAV Delivery Regulatory Frameworks: FAA Part 135, EASA U-Space, BVLOS Authorisation & Urban Air Mobility Integration Rules

- Sidewalk Robot, Autonomous Mobile Robot (AMR) & Low-Speed Autonomous Delivery Device Regulations Across Municipal Jurisdictions

- Global Autonomous Logistics & Delivery Vehicles Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Autonomous Vehicles & Delivery Units Deployed)

- Market Size & Forecast by Vehicle Type

- Autonomous Long-Haul Trucking & Highway Freight Vehicles (SAE Level 3 and Above)

- Autonomous Middle-Mile & Regional Distribution Trucks

- Autonomous Last-Mile Delivery Vans & Light Commercial Vehicles

- Autonomous Ground Delivery Robots (Sidewalk & Low-Speed Delivery Devices)

- Autonomous Mobile Robots (AMRs) for Warehouse & Distribution Centre Intralogistics

- Delivery Drones & Unmanned Aerial Vehicles (UAVs) for Last-Mile Aerial Delivery

- Autonomous Yard Trucks, Port Tractors & Intermodal Terminal Vehicles

- Autonomous Forklifts, Pallet Movers & Goods-to-Person Fulfilment Robots

- Market Size & Forecast by Automation Level

- SAE Level 2: Advanced Driver Assistance Systems (ADAS) with Partial Automation

- SAE Level 3: Conditional Automation with Driver on Standby

- SAE Level 4: High Automation within Defined Operational Design Domain (ODD)

- SAE Level 5: Full Automation without Human Intervention

- Market Size & Forecast by Technology

- LiDAR Sensor Technology: Mechanical Spinning, Solid-State & MEMS LiDAR

- Radar Sensor Technology: Short-Range, Medium-Range & Long-Range Automotive Radar

- Camera & Computer Vision Technology: Monocular, Stereo & 360-Degree Perception

- AI & Deep Learning: Perception, Sensor Fusion, Path Planning & Decision-Making Algorithms

- High-Definition (HD) Mapping, Localisation & Simultaneous Localisation and Mapping (SLAM) Technology

- V2X Communication Technology: Vehicle-to-Infrastructure (V2I) & Vehicle-to-Network (V2N) for Autonomous Logistics

- Edge Computing, Autonomous Drive Computer (ADC) & In-Vehicle AI Processing Technology

- Fleet Orchestration, Autonomous Vehicle Operations (AVO) Platform & Remote Assistance Technology

- Market Size & Forecast by Component

- Perception Hardware: LiDAR, Radar, Camera & Ultrasonic Sensor Suite

- Autonomous Driving Computer (ADC), Centralised Compute Platform & Domain Controller

- HD Map, Localisation Module & GNSS Positioning Hardware

- Drive-by-Wire Actuation System: Steer-by-Wire, Brake-by-Wire & Throttle-by-Wire

- Connectivity Module: 4G LTE, 5G, DSRC & C-V2X Communication Unit

- Autonomous Vehicle Software Stack: Perception, Planning, Control & Safety Middleware

- Fleet Management & Autonomous Vehicle Operations (AVO) Platform Software

- Market Size & Forecast by Propulsion Type

- Battery Electric (BEV) Autonomous Logistics Vehicle

- Fuel Cell Electric (FCEV) & Hydrogen-Powered Autonomous Logistics Vehicle

- Internal Combustion Engine (ICE) Autonomous Logistics Vehicle

- Hybrid Electric Autonomous Logistics Vehicle

- Market Size & Forecast by Application

- Long-Haul Highway Freight & Intercity Goods Transport

- Middle-Mile Regional Distribution & Hub-to-Spoke Freight

- Urban Last-Mile Parcel & E-Commerce Delivery

- Cold Chain, Pharmaceutical & Temperature-Sensitive Goods Delivery

- Warehouse & Distribution Centre Intralogistics & Fulfilment Automation

- Port, Intermodal Terminal & Airport Ground Logistics

- On-Demand Grocery, Food & Convenience Goods Delivery

- Market Size & Forecast by End-User

- Road Freight Carriers, Trucking Companies & Third-Party Logistics (3PL) Providers

- E-Commerce Retailers & Parcel Delivery & Courier Companies

- Grocery, Food Delivery & Quick-Commerce Operators

- Warehouse Operators, Fulfilment Centres & Contract Logistics Providers

- Port Authorities, Intermodal Terminal Operators & Freight Forwarders

- Pharmaceutical, Healthcare & Cold Chain Logistics Operators

- Automotive OEMs, Mobility-as-a-Service (MaaS) Operators & Autonomous Vehicle Developers

- Market Size & Forecast by Sales Channel

- Direct OEM & Autonomous Vehicle Developer Sales

- Robotics-as-a-Service (RaaS) & Autonomous Logistics-as-a-Service Subscription Model

- Systems Integrator & Logistics Technology Partner Channel

- Government Pilot Program, Smart City Initiative & Public Procurement Channel

- North America Autonomous Logistics & Delivery Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Autonomous Vehicles & Delivery Units Deployed)

- By Vehicle Type

- By Automation Level

- By Technology

- By Component

- By Propulsion Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Autonomous Logistics & Delivery Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Autonomous Vehicles & Delivery Units Deployed)

- By Vehicle Type

- By Automation Level

- By Technology

- By Component

- By Propulsion Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Autonomous Logistics & Delivery Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Autonomous Vehicles & Delivery Units Deployed)

- By Vehicle Type

- By Automation Level

- By Technology

- By Component

- By Propulsion Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Autonomous Logistics & Delivery Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Autonomous Vehicles & Delivery Units Deployed)

- By Vehicle Type

- By Automation Level

- By Technology

- By Component

- By Propulsion Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Autonomous Logistics & Delivery Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Autonomous Vehicles & Delivery Units Deployed)

- By Vehicle Type

- By Automation Level

- By Technology

- By Component

- By Propulsion Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Autonomous Logistics & Delivery Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Autonomous Vehicles & Delivery Units Deployed)

- By Vehicle Type

- By Automation Level

- By Technology

- By Component

- By Propulsion Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- LiDAR, Solid-State LiDAR & Sensor Technology Deep-Dive for Autonomous Logistics Perception Systems

- AI Perception, Deep Learning Object Detection & Sensor Fusion Architecture for Autonomous Logistics Vehicles

- HD Mapping, Simultaneous Localisation and Mapping (SLAM) & High-Precision GNSS Localisation Technology

- Autonomous Driving Software Stack: Path Planning, Decision-Making, Behaviour Prediction & Safety Assurance Technology

- Fleet Orchestration, Remote Assistance, Teleoperation & Autonomous Vehicle Operations (AVO) Platform Technology

- Delivery Drone, UAV Swarm & Urban Air Logistics Platform Technology

- Autonomous Mobile Robot (AMR) & Warehouse Robotics Navigation, Manipulation & Intralogistics Technology

- Patent & IP Landscape in Autonomous Logistics, Delivery Vehicle & Robotics Technologies

- Value Chain & Supply Chain Analysis

- LiDAR, Radar, Camera & Perception Sensor Component Manufacturing Supply Chain

- Autonomous Driving Computer (ADC), Centralised Compute & AI Chip Supply Chain

- Drive-by-Wire Actuation, Steering, Braking & Chassis Hardware Supply Chain

- Battery, Electric Drivetrain & Fuel Cell Propulsion System Supply Chain

- Autonomous Vehicle Software Stack, AI Algorithm & AVO Platform Development Supply Chain

- OEM Vehicle Integrator, Tier 1 Supplier & Autonomous Logistics Platform Developer Channel

- Logistics Operator, Fleet Buyer, RaaS Subscriber & End-User Deployment Channel

- Pricing Analysis

- Autonomous Logistics Vehicle Unit Cost Analysis by Vehicle Type & Automation Level

- Perception Sensor Suite Cost Benchmarking: LiDAR, Radar, Camera & Sensor Fusion System Pricing Trajectory

- Autonomous Driving Computer (ADC) & AI Compute Module Capital Cost Analysis

- Robotics-as-a-Service (RaaS) & Autonomous Logistics-as-a-Service Subscription Pricing Benchmarking

- Total Cost of Ownership (TCO) Analysis: Autonomous vs. Conventional Driver-Operated Logistics Vehicle Benchmarking

- Cost Trajectory & Economies of Scale Analysis: Sensor Cost Reduction, Software Amortisation & Fleet Scale Economics

- Sustainability & Environmental Analysis

- Lifecycle CO2 Emissions Assessment: Manufacturing, In-Service Operations & End-of-Life for Autonomous Logistics Vehicles by Propulsion Type

- AI Route Optimisation, Platooning & Eco-Driving in Autonomous Trucks: Fuel Consumption & Emission Reduction Quantification

- Electrification of Autonomous Logistics Fleets: Grid Impact, Renewable Energy Integration & Fleet Decarbonisation Pathway

- Warehouse AMR & Autonomous Intralogistics: Energy Efficiency, Facility Carbon Footprint Reduction & Operational Sustainability

- Regulatory-Driven Sustainability: EU Green Deal Freight Targets, EPA GHG Phase 3 Rules & Net Zero Logistics Transition Roadmap Support

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Vehicle Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Vehicle Type, Technology & Geography

- Player Classification

- Autonomous Long-Haul & Highway Trucking Technology Developers & OEM Partners

- Autonomous Last-Mile Delivery Van & Light Commercial Vehicle Developers

- Sidewalk Delivery Robot & Low-Speed Autonomous Delivery Device Manufacturers

- Warehouse AMR, Autonomous Forklift & Intralogistics Robot Manufacturers

- Delivery Drone & UAV Last-Mile Aerial Logistics Platform Operators

- Autonomous Yard Truck, Port Vehicle & Intermodal Terminal Automation Providers

- LiDAR, Radar & Perception Sensor Suppliers for Autonomous Logistics Platforms

- Autonomous Vehicle Software Stack, AI Perception & Fleet Orchestration Platform Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Vehicle Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Autonomous Logistics & Delivery Vehicle Products & Technology Portfolio

- Key Customer Relationships & Reference Deployment Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Autonomous Logistics & Delivery Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Market Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Vehicle Type, Automation Level, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)