Market Definition

The Global Automotive Aftermarket encompasses the manufacturing, distribution, retailing, and installation of replacement parts, accessories, tools, consumables, and service solutions for passenger cars, light commercial vehicles, heavy trucks, motorcycles, and off-highway equipment after their original sale. The market includes mechanical replacement parts, electronic and electrical components, tyres, lubricants, collision repair materials, diagnostic equipment, vehicle care products, and associated repair and maintenance services supplied through independent workshops, authorized dealerships, online retail platforms, and mobile service providers to individual vehicle owners, fleet operators, and insurance-directed repair networks globally.

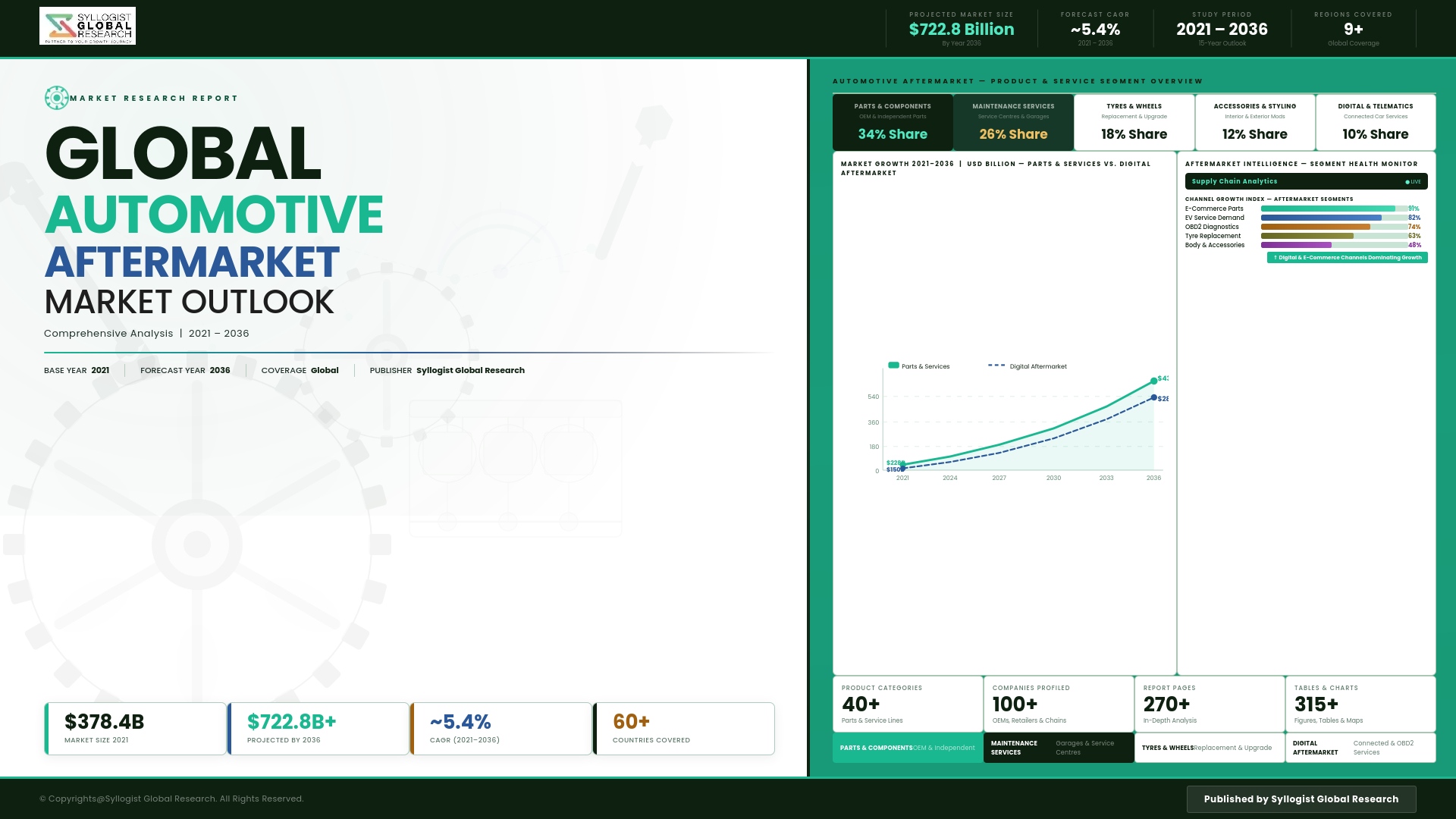

Market Insights

The global automotive aftermarket is one of the most resilient and structurally expansive segments within the broader automotive industry, generating consistent demand growth driven by an expanding global vehicle parc, increasing average vehicle age across major markets, and the non-discretionary nature of maintenance and repair expenditure that insulates aftermarket revenue from new vehicle production cycle volatility. The market was valued at approximately USD 482.6 billion in 2025 and is projected to reach USD 761.3 billion by 2034, advancing at a compound annual growth rate of 5.2% through the forecast period, as rising vehicle ownership across emerging economies, extended vehicle retention periods in developed markets, and the growing complexity of modern vehicle systems requiring specialized parts and diagnostic expertise collectively sustain multi-year revenue expansion across both the parts supply and vehicle servicing segments.

The average age of light vehicles in service across the United States, European Union, and key Asia-Pacific markets has extended progressively over the past decade, driven by improved vehicle build quality and durability, elevated new vehicle prices reducing replacement frequency, and consumer preference for maintaining existing vehicles during periods of economic uncertainty. This vehicle age elevation is structurally favorable for the independent aftermarket channel, as vehicles beyond their warranty period generate the highest aftermarket parts and service revenue intensity while migrating from authorized dealer service networks toward independent repair workshops and specialized service providers offering competitive labor rates and broad parts sourcing flexibility. The independent aftermarket is simultaneously benefiting from digital transformation across the parts distribution and service booking landscape, with e-commerce platforms, digital parts catalogues, and AI-powered vehicle diagnostic tools enabling faster parts identification, more efficient supply chain fulfillment, and enhanced consumer accessibility to aftermarket service options that were previously concentrated within geographically limited workshop networks.

The electrification transition represents the most structurally complex dynamic reshaping long-term aftermarket demand composition, as battery electric vehicles introduce fundamentally different service and parts replacement profiles compared with internal combustion engine vehicles, with lower scheduled maintenance frequency, reduced consumable wear rates across engine oil, filters, and exhaust components, but emerging high-value service categories in battery diagnostics, battery management system updates, electric motor servicing, and high-voltage system repair that require specialized technician training and capital-intensive workshop equipment investment. The transition to electrified vehicles is proceeding at differentiated rates across markets, and the combined ICE and EV vehicle parc dynamic means the traditional aftermarket will sustain robust demand volumes through the forecast period while progressive EV service capability represents the critical long-term positioning investment for aftermarket participants. Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, driven by rapid vehicle parc expansion in India, Southeast Asia, and China. North America and Europe maintain the largest absolute aftermarket revenue contributions, anchored by large installed vehicle fleets of advanced average age, mature independent workshop networks, and high per-vehicle maintenance and repair expenditure levels sustained by stringent vehicle inspection and roadworthiness regulation frameworks.

Key Drivers

Sustained Global Vehicle Parc Expansion and Rising Average Vehicle Age Across Major Markets Generating Structurally Growing Non-Discretionary Replacement Parts and Service Demand

The continuous expansion of the global vehicle parc, driven by increasing vehicle ownership penetration across rapidly motorizing emerging markets and sustained vehicle retention in developed economies where new vehicle purchase deferral trends are extending average vehicle age to historically elevated levels, is generating a structurally growing base of vehicles requiring regular maintenance, scheduled parts replacement, and unplanned repair services whose cumulative demand compounds into a large and highly resilient aftermarket revenue pool that is substantially insulated from new vehicle sales cycle volatility. Vehicles aged six years and above, which represent the highest-revenue cohort within the aftermarket parts and service demand distribution, are constituting an increasing proportion of the global vehicle parc across all major markets, creating a durable demand foundation for independent workshops, parts distributors, and aftermarket platform operators through the full forecast period.

Digital Commerce Transformation, E-Commerce Parts Distribution Growth, and AI-Powered Diagnostic Platforms Expanding Aftermarket Accessibility and Accelerating Independent Channel Market Share Gains

The rapid digitalization of automotive aftermarket parts sourcing, service booking, and vehicle diagnostic workflows is materially expanding consumer access to independent aftermarket service options, enabling price comparison, parts availability transparency, and workshop appointment convenience that is accelerating the migration of service spend from authorized dealer networks toward independent workshops and online parts retailers offering more competitive pricing and broader product assortment. AI-powered vehicle diagnostic platforms, digital parts catalogues with real-time inventory integration, and predictive maintenance notification systems delivered through connected vehicle data interfaces are generating new customer engagement channels for aftermarket participants while enabling more accurate first-time parts selection and faster workshop repair cycle times that improve customer satisfaction and workshop throughput economics simultaneously.

Increasing Vehicle System Complexity, Advanced Driver Assistance System Proliferation, and Connected Vehicle Technology Integration Elevating Specialized Parts and Service Revenue Per Vehicle

The progressive integration of advanced driver assistance systems, electronic control unit proliferation, connected vehicle software architectures, and sophisticated powertrain management systems into mainstream vehicle platforms is elevating the technical complexity and per-vehicle parts and service revenue intensity of modern vehicle maintenance and repair, as sensor recalibration requirements, software update procedures, and specialized component replacement protocols associated with ADAS, connectivity, and electrification systems demand higher-value parts, workshop equipment investment, and technician skill levels that generate materially higher average repair order values compared with equivalent maintenance events on simpler legacy vehicle architectures.

Key Challenges

Counterfeit and Sub-Standard Parts Proliferation Across Digital and Traditional Distribution Channels Threatening Consumer Safety, Brand Integrity, and Independent Workshop Liability Exposure

The global automotive aftermarket is confronted with a substantial and growing counterfeit parts problem across both traditional distribution channels and increasingly across e-commerce platforms where fraudulent parts listings exploit the price sensitivity of aftermarket consumers and the difficulty of authenticating product genuineness through digital commerce interfaces, creating consumer safety risks, product liability exposure for workshop operators installing unknowingly counterfeit components, and brand reputation damage for legitimate parts manufacturers whose product identities are misappropriated by counterfeit producers. The cross-border sourcing dynamics of global e-commerce supply chains make counterfeit parts interdiction particularly challenging for regulatory authorities and platform operators, while the technical sophistication of counterfeit packaging replication continues to improve in ways that make visual inspection an increasingly unreliable authentication tool for parts distributors and workshop technicians.

Electric Vehicle Service Transition Requiring Substantial Workshop Capital Investment, Technician Retraining Programs, and High-Voltage Safety Infrastructure That Many Independent Operators Cannot Finance

The technical requirements of electric vehicle servicing, including high-voltage system safety infrastructure, battery diagnostic and management equipment, electric motor servicing capability, and the ongoing investment in technician training across rapidly evolving EV platform architectures, are imposing capital expenditure and workforce development obligations on independent workshop operators that substantially exceed the investment required for equivalent internal combustion engine service capability expansion, creating a transition financing barrier that threatens to concentrate EV service capability within authorized dealer networks and well-capitalized independent chains at the expense of smaller independent workshops that serve the majority of vehicles in most regional aftermarket service markets. This capability concentration risk has meaningful competitive implications for the independent aftermarket channel structure as EV fleet penetration grows through the forecast period.

Right-to-Repair Legislative Uncertainty, OEM Telematics Data Access Restrictions, and Connected Vehicle Diagnostic Gatekeeping Constraining Independent Workshop Competitive Access to Modern Vehicle Service Information

Original equipment manufacturers are increasingly leveraging proprietary telematics data platforms, software-defined vehicle architectures, and restricted diagnostic interface protocols to channel vehicle service and software update activity toward authorized dealer networks, creating competitive access barriers for independent workshops that lack the licensed diagnostic software, OEM data portal credentials, and software update authorization required to service modern connected vehicle platforms at the functional completeness level that vehicle owners expect. While right-to-repair legislative initiatives in the European Union, the United States, and Australia are advancing frameworks to mandate independent workshop access to vehicle diagnostic data and repair information, the pace of regulatory implementation remains slower than the rate of OEM connected vehicle platform deployment, creating a near-term competitive disadvantage for independent aftermarket participants that grows in proportion to connected vehicle fleet penetration.

Market Segmentation

- Segmentation By Product Type

- Mechanical Replacement Parts

- Electronic and Electrical Components

- Tyres and Wheel Products

- Lubricants, Fluids, and Chemicals

- Collision Repair and Body Parts

- Vehicle Care and Appearance Products

- Diagnostic Tools and Workshop Equipment

- Others

- Segmentation By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles and Trucks

- Buses and Coaches

- Two-Wheelers and Motorcycles

- Electric and Hybrid Vehicles

- Off-Highway and Agricultural Vehicles

- Others

- Segmentation By Service Type

- Scheduled Maintenance and Servicing

- Mechanical Repair and Overhaul

- Collision and Body Repair

- Tyre Fitting and Wheel Alignment

- Electrical and Electronic Diagnostics

- EV Battery and High-Voltage System Servicing

- Vehicle Customization and Accessory Fitment

- Others

- Segmentation By Distribution Channel

- Independent Wholesale Distributors

- Authorized Dealer and OEM Aftersales Networks

- Online Retail and E-Commerce Platforms

- Retail Auto Parts Chains and Specialist Stores

- Mobile and On-Demand Service Providers

- Others

- Segmentation By Component Category

- Engine and Powertrain Components

- Brake System Components

- Suspension, Steering, and Chassis Parts

- Filters, Belts, and Scheduled Replacement Items

- Exhaust and Emissions System Components

- Lighting, Electrical, and Sensor Components

- Heating, Ventilation, and Air Conditioning Parts

- Others

- Segmentation By End User

- Individual Vehicle Owners (Do-It-Yourself)

- Independent Repair Workshops and Garages

- Authorized Dealer Service Centers

- Commercial and Municipal Fleet Operators

- Insurance-Directed Collision Repair Networks

- Tyre and Quick-Fit Service Chains

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Automotive Aftermarket in 2025, projected through 2034, disaggregated by product type, vehicle type, and distribution channel, enabling parts manufacturers, distributors, workshop operators, and investors to identify the highest-growth segments and most durable revenue opportunities across the global aftermarket value chain?

- How are rising average vehicle age, expanding global vehicle parc, and shifting consumer vehicle retention behavior influencing parts replacement demand intensity, independent workshop service volumes, and channel mix dynamics across North America, Europe, and Asia-Pacific through the forecast period to 2034?

- What impact is the accelerating adoption of battery electric vehicles having on aftermarket demand composition, independent workshop service capability requirements, and long-term parts revenue per vehicle, and how are leading aftermarket distributors and service providers positioning EV servicing capability investments to capture emerging opportunities?

- Which aftermarket product and service segments, including ADAS component replacement, EV battery diagnostics, digital parts distribution, and mobile service delivery, are generating the highest revenue growth through 2034, and what technology investment and distribution capability benchmarks are most critical to aftermarket participant competitiveness?

- How is the competitive landscape evolving among global parts manufacturers, independent distribution networks, authorized dealer aftersales operations, and e-commerce platform entrants, and what digital transformation, private label, and ecosystem partnership strategies are enabling leading participants to defend and expand market share across distribution and service channels?

- What challenges do counterfeit parts proliferation, OEM telematics data access restrictions, and right-to-repair legislative uncertainty present to independent aftermarket operators, and how are industry participants, trade associations, and regulators advancing frameworks to preserve competitive independent workshop access to modern vehicle diagnostic and repair information?

- Which regional automotive aftermarket markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most substantial incremental revenue growth through 2034, and what vehicle parc growth trajectories, average vehicle age dynamics, regulatory inspection requirements, and e-commerce adoption rates are shaping demand patterns and competitive positioning in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Counterfeit & Sub-Standard Parts Proliferation, Grey Market Penetration & Brand Reputation Risk

- EV Transition Impact: Reduced ICE Powertrain Aftermarket Demand, Changing Service Intervals & Revenue Mix Disruption Risk

- OEM Extended Warranty, Telematics-Linked Service Lock-In & Independent Workshop Access to Vehicle Data Risk

- Raw Material Price Volatility, Supply Chain Disruption & Parts Availability Risk Across Aftermarket Categories

- E-Commerce Platform Disintermediation, Pricing Transparency & Margin Compression Risk for Traditional Aftermarket Distributors

- Regulatory Framework & Standards

- Block Exemption Regulation (BER 461/2010), Right-to-Repair & Independent Aftermarket Access to Vehicle Repair Information & OBD Data in the EU

- US Right-to-Repair Act, NHTSA Telematics Data Access & FTC Repair Regulations Governing Independent Aftermarket Competition

- REACH, RoHS, End-of-Life Vehicle (ELV) Directive & Hazardous Substance Restrictions Applicable to Aftermarket Parts & Fluids

- ISO 9001, IATF 16949, SAE Quality Standards & OEM Approval Frameworks for Aftermarket Parts Manufacturers

- Remanufacturing Standards, Core Return Programs & Circular Economy Regulations: EU Remanufacturing Industry Guidelines & National Remanufactured Parts Certification Frameworks

- Global Automotive Aftermarket Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Units, Sets & Service Events)

- Market Size & Forecast by Product Category

- Wear & Maintenance Parts

- Mechanical & Drivetrain Parts

- Braking System Parts

- Suspension, Steering & Chassis Parts

- Electrical, Electronic & Lighting Parts

- Engine & Powertrain Parts

- Body, Exterior & Structural Parts

- HVAC, Thermal Management & Cabin Parts

- Tyres, Wheels & Wheel-End Parts

- Exhaust, Emission Control & Underbody Parts

- Transmission & Driveline Parts

- Fuel System & Induction Parts

- Lubricants, Fluids & Chemicals

- Accessories & Appearance Products

- Tools, Equipment & Workshop Consumables

- Market Size & Forecast by Wear & Maintenance Parts Sub-Segment

- Engine Oil Filters

- Air Filters & Air Intake Elements

- Cabin Air Filters & Pollen Filters

- Fuel Filters

- Spark Plugs & Glow Plugs

- Wiper Blades & Windscreen Wipers

- Drive Belts: Timing Belts, Timing Chains & Serpentine Belts

- Tensioners, Idlers & Belt Drive Components

- Coolant Hoses & Radiator Hoses

- Gaskets, Seals & O-Ring Kits

- Market Size & Forecast by Braking System Parts Sub-Segment

- Brake Pads & Friction Material

- Brake Discs & Rotors

- Brake Drums & Brake Shoes

- Brake Calipers: New & Remanufactured

- Brake Master Cylinders & Wheel Cylinders

- Brake Hoses, Lines & Fittings

- Brake Fluid & Hydraulic Fluid

- ABS Sensors, ABS Modulators & Electronic Brake Control Components

- Market Size & Forecast by Suspension, Steering & Chassis Parts Sub-Segment

- Shock Absorbers & Struts

- Coil Springs, Leaf Springs & Air Springs

- Control Arms, Wishbones & Trailing Arms

- Ball Joints & Tie Rod Ends

- Wheel Bearings & Hub Assemblies

- Bushings: Rubber, Polyurethane & Metal-Rubber

- Steering Racks, Steering Columns & Steering Pumps

- Sway Bars, End Links & Steering Linkage Components

- CV Joints, CV Boots & Axle Shafts

- Market Size & Forecast by Engine & Powertrain Parts Sub-Segment

- Pistons, Piston Rings & Cylinder Liners

- Engine Bearings: Main, Rod & Thrust Bearings

- Camshafts, Crankshafts & Valvetrain Components

- Cylinder Head Gaskets & Full Engine Gasket Sets

- Engine Mounts & Transmission Mounts

- Water Pumps & Coolant Pump Assemblies

- Oil Pumps & Oil Pump Assemblies

- Turbochargers & Supercharger Components: New & Remanufactured

- Intake Manifolds, Throttle Bodies & Fuel Injectors

- Market Size & Forecast by Transmission & Driveline Parts Sub-Segment

- Manual Transmission Parts: Clutch Kits, Pressure Plates & Flywheels

- Automatic Transmission Parts: Torque Converters, Solenoids & Valve Bodies

- Continuously Variable Transmission (CVT) Components & Belts

- Transfer Case Components & Four-Wheel Drive Parts

- Differentials, Axle Parts & Propeller Shafts

- Transmission Fluids & Gear Oils

- Market Size & Forecast by Electrical, Electronic & Lighting Parts Sub-Segment

- Starter Motors: New & Remanufactured

- Alternators & Generators: New & Remanufactured

- Batteries: Lead-Acid, AGM, EFB & Lithium-Ion 12V & 48V

- Oxygen Sensors, Lambda Sensors & Exhaust Gas Sensors

- Mass Airflow (MAF) Sensors, MAP Sensors & Throttle Position Sensors

- Crankshaft Position, Camshaft Position & Knock Sensors

- Temperature Sensors: Coolant, Intake Air & Exhaust Gas

- Headlights & Front Lighting Assemblies: Halogen, Xenon & LED

- Tail Lights, Rear Lighting & Indicator Assemblies

- Relays, Fuses, Switches & Electrical Connectors

- ECU, Body Control Module (BCM) & Powertrain Control Module (PCM): New & Remanufactured

- Ignition Coils, Ignition Leads & Distributor Components

- Market Size & Forecast by Exhaust, Emission Control & Underbody Parts Sub-Segment

- Catalytic Converters: New & Remanufactured

- Diesel Particulate Filters (DPF): New & Remanufactured

- Exhaust Manifolds, Downpipes & Mid-Pipes

- Mufflers, Silencers & Rear Exhaust Sections

- EGR Valves, EGR Coolers & Emission Control Components

- AdBlue / DEF Systems: SCR Catalysts, NOx Sensors & Dosing Units

- Exhaust Gaskets, Clamps & Hangers

- Market Size & Forecast by HVAC, Thermal Management & Cabin Parts Sub-Segment

- Radiators & Cooling System Heat Exchangers

- Condensers, Evaporators & Heater Cores

- AC Compressors: New & Remanufactured

- Thermostats & Expansion Valves

- Cooling Fans, Fan Clutches & Fan Modules

- Refrigerants: R-134a, R-1234yf & Compressor Oil

- Blower Motors, HVAC Controls & Climate Control Components

- Market Size & Forecast by Fuel System & Induction Parts Sub-Segment

- Fuel Pumps: Mechanical & Electric In-Tank

- Fuel Injectors: Petrol & Diesel

- Carburettors & Carburettor Rebuild Kits

- Fuel Pressure Regulators, Fuel Rails & Fuel Tanks

- Evaporative Emission Control (EVAP) Components & Charcoal Canisters

- Diesel Injection Pumps, Common Rail Components & Injector Nozzles

- Market Size & Forecast by Tyres, Wheels & Wheel-End Parts Sub-Segment

- Replacement Tyres: Passenger Car, SUV & Light Truck

- Replacement Tyres: Commercial Vehicle, Bus & Heavy Truck

- Tyre Pressure Monitoring System (TPMS) Sensors & Kits

- Alloy Wheels, Steel Wheels & Wheel Accessories

- Lug Nuts, Wheel Bolts & Hub Caps

- Tyre Repair & Inflation Products

- Market Size & Forecast by Body, Exterior & Structural Parts Sub-Segment

- Bumpers: Front & Rear Bumper Assemblies & Components

- Body Panels: Hoods, Fenders, Doors & Trunk Lids

- Windscreens, Side Glass & Rear Glass

- Mirrors: Door Mirrors, Glass Inserts & Mirror Motor Assemblies

- Grilles, Fascias & Exterior Trim Components

- Underbody & Structural Parts: Subframes, Crossmembers & Reinforcements

- Market Size & Forecast by Lubricants, Fluids & Chemicals Sub-Segment

- Engine Oils: Mineral, Semi-Synthetic & Fully Synthetic

- Transmission Fluids: ATF, MTF & CVT Fluid

- Coolants & Antifreeze

- Power Steering Fluid & Hydraulic Fluid

- Windscreen Washer Fluid & De-Icers

- Greases, Assembly Compounds & Penetrating Oils

- Fuel Additives, Oil Additives & Engine Cleaners

- Adhesives, Sealants & Thread-Locking Compounds

- Market Size & Forecast by Accessories & Appearance Products Sub-Segment

- Seat Covers, Floor Mats & Interior Accessories

- Car Care, Polishing, Waxing & Paint Protection Products

- Towing, Tow Bars & Trailer Accessories

- Roof Racks, Cargo Carriers & Van Racking Systems

- Dash Cameras, Parking Sensors & Reversing Cameras

- Navigation Systems, Infotainment & Head Unit Upgrades

- Performance Accessories: Suspension Kits, Exhausts & Air Intake Upgrades

- Market Size & Forecast by EV-Specific Aftermarket Parts Sub-Segment

- High-Voltage (HV) Battery Pack Replacement, Cell Replacement & Battery Reconditioning

- On-Board Charger (OBC) & Power Distribution Unit (PDU) Replacement Parts

- Electric Drive Motor, Inverter & Power Electronics Replacement Parts

- Thermal Management Components for EVs: Battery Cooling Plates, Chillers & Heat Pumps

- Regenerative Braking & Brake-by-Wire System Components for EVs

- EV-Specific Fluids: Dielectric Coolant, Thermal Interface Material & e-Axle Fluid

- Market Size & Forecast by Service Type

- Mechanical Repair & Maintenance Service

- Collision Repair & Body Shop Service

- Tyre Fitting, Balancing & Wheel Alignment Service

- Electrical & Electronic Diagnostics & Repair Service

- HVAC & Air Conditioning Service

- Quick Service: Oil Change, Filter Replacement & Fluid Top-Up

- Remanufacturing & Core Exchange Service

- Market Size & Forecast by Vehicle Type

- Passenger Cars & Light Duty Vehicles

- Light Commercial Vehicles (LCV) & Vans

- Medium & Heavy Commercial Vehicles (MHCV): Trucks & Buses

- Off-Highway, Construction & Agricultural Vehicles

- Two-Wheelers & Three-Wheelers

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV) & Hybrid Electric Vehicles (HEV)

- Market Size & Forecast by Vehicle Age

- 0 to 3 Years (New Vehicle Warranty Period)

- 4 to 7 Years (Post-Warranty Early Aftermarket Phase)

- 8 to 12 Years (Core Aftermarket Phase)

- Above 12 Years (Mature & Ageing Fleet Phase)

- Market Size & Forecast by Sales Channel

- Original Equipment Service (OES) & Authorised Dealer Network

- Independent Aftermarket (IAM) Distributor & Wholesaler

- Auto Parts Retail Chain & Specialist Retailer

- E-Commerce & Online Marketplace (B2C & B2B)

- Independent Workshop & Garage Direct Purchase

- Fleet Operator & Commercial Vehicle Operator Direct Channel

- Market Size & Forecast by End-User

- Independent Repair Workshops & Garages

- OEM Authorised Dealer Service Centres

- Tyre Fitting Centres & Wheel Specialists

- Fast-Fit & Quick-Service Centre Chains

- Collision Repair & Body Shop Operators

- Commercial Fleet Operators & Transport Companies

- DIY Vehicle Owners & Consumer Retail Buyers

- North America Automotive Aftermarket Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units, Sets & Service Events)

- By Product Category

- By Service Type

- By Vehicle Type

- By Vehicle Age

- By Sales Channel

- By End-User

- By Country

- Market Size & Forecast

- Europe Automotive Aftermarket Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units, Sets & Service Events)

- By Product Category

- By Service Type

- By Vehicle Type

- By Vehicle Age

- By Sales Channel

- By End-User

- By Country

- Market Size & Forecast

- Asia-Pacific Automotive Aftermarket Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units, Sets & Service Events)

- By Product Category

- By Service Type

- By Vehicle Type

- By Vehicle Age

- By Sales Channel

- By End-User

- By Country

- Market Size & Forecast

- Latin America Automotive Aftermarket Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units, Sets & Service Events)

- By Product Category

- By Service Type

- By Vehicle Type

- By Vehicle Age

- By Sales Channel

- By End-User

- By Country

- Market Size & Forecast

- Middle East & Africa Automotive Aftermarket Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units, Sets & Service Events)

- By Product Category

- By Service Type

- By Vehicle Type

- By Vehicle Age

- By Sales Channel

- By End-User

- By Country

- Market Size & Forecast

- Country-Wise* Automotive Aftermarket Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Units, Sets & Service Events)

- By Product Category

- By Service Type

- By Vehicle Type

- By Vehicle Age

- By Sales Channel

- By End-User

- By Country

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Telematics, Connected Vehicle Data & AI-Driven Predictive Maintenance Platform Technology for Aftermarket Service Triggering

- E-Commerce Platform Technology, Digital Catalogue, VIN-Based Parts Fitment & Online Parts Ordering Technology

- Augmented Reality (AR) Repair Guidance, Workshop Digitalisation & Remote Diagnostics Technology

- Remanufacturing Process Technology: Core Cleaning, Disassembly, Precision Remanufacture & Quality Validation

- 3D Printing, Additive Manufacturing & On-Demand Parts Production Technology for Slow-Moving & Obsolete Parts

- EV Aftermarket Technology: HV Battery Reconditioning, BMS Calibration & Electric Drivetrain Repair Technology

- OBD-II, OBD-III, Vehicle Data Standardisation & Independent Workshop Access to ECU Diagnostic Data Technology

- Patent & IP Landscape in Aftermarket Parts, Remanufacturing & Automotive Service Technologies

- Value Chain & Supply Chain Analysis

- OEM Parts Manufacturing, Brand Licensing & Authorised OES Parts Distribution Supply Chain

- Independent Aftermarket Parts Manufacturer & Generic Parts Production Supply Chain

- Remanufacturer, Core Collector & Remanufactured Parts Distribution Supply Chain

- National Distributor, Regional Warehouse Distributor & Programme Group Supply Chain

- Auto Parts Retail Chain, Independent Distributor & E-Commerce Fulfilment Supply Chain

- Independent Workshop, Fast-Fit Chain & Franchised Dealer Service Channel

- Tyre Distributor, Tyre Fitting Centre & Commercial Fleet Tyre Management Channel

- Pricing Analysis

- OES vs. IAM vs. Remanufactured Parts Price Positioning Analysis by Product Category

- E-Commerce Pricing Dynamics, Online vs. Offline Price Gap & Platform Pricing Algorithm Analysis

- Lubricant & Fluid Pricing: Viscosity Grade, Brand Tier & Private Label Benchmarking

- Tyre Pricing: Budget, Mid-Range & Premium Tier Benchmarking by Vehicle Segment & Region

- Labour Rate Benchmarking: Authorised Dealer, Fast-Fit Chain & Independent Workshop Service Pricing Analysis

- Remanufactured Parts Pricing: Core Charge, Exchange Pricing & Discount to New Part Benchmark Analysis

- Sustainability & Environmental Analysis

- Remanufacturing, Reconditioned Parts & Core Exchange Programs: CO2 Savings, Material Recovery & Circular Economy Contribution

- ELV Directive, End-of-Life Vehicle Recycling & Automotive Parts Reclamation: Regulatory Requirements & Sustainable Dismantling Practices

- Lubricant & Fluid Sustainability: Used Oil Collection, Re-Refining, Bio-Based Lubricant Adoption & Recycling Infrastructure

- Tyre Retreading, Sustainable Tyre Disposal & Tyre-Derived Fuel (TDF) & Rubber Recycling Programs

- Packaging Sustainability, Reduced Hazardous Substance Content & Green Aftermarket Parts Certification Frameworks

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Category & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Category, Sales Channel & Geography

- Player Classification

- Global Automotive Aftermarket Parts Manufacturers & OES Approved Suppliers

- Independent Aftermarket (IAM) Parts Brands & Generic Parts Manufacturers

- Automotive Remanufacturers: Powertrain, Braking, Electrical & Electronics

- Automotive Lubricant & Fluid Manufacturers

- Tyre Manufacturers & Replacement Tyre Brands

- Auto Parts Retail Chains & Specialist Parts Distributors

- E-Commerce & Digital Aftermarket Marketplace Platforms

- Fast-Fit Service Chains, Tyre Fitting Networks & Workshop Franchise Operators

- Competitive Analysis Frameworks

- Market Share Analysis by Product Category, Sales Channel & Region

- Company Profile

- Company Overview & Headquarters

- Automotive Aftermarket Products & Service Portfolio

- Key Customer Relationships & Reference Channel Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Automotive Aftermarket Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Market Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Category, Service Type, Vehicle Type, Sales Channel, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)