Global Methane Satellite Monitoring Technologies Market By Satellite Type, By Sensor Technology, By Monitoring Capability, By End Use Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Methane Satellite Monitoring Technologies Market encompasses the development, manufacture, launch, operation, and commercial data service provision of space-based remote sensing systems utilizing shortwave infrared spectrometers, thermal infrared sensors, and hyperspectral imaging instruments to detect, quantify, attribute, and continuously monitor atmospheric methane concentrations and emission sources at global, regional, and facility scales, serving oil and gas operators, regulatory agencies, financial institutions, agricultural bodies, and climate monitoring organizations requiring high-fidelity methane emission measurement data for compliance, abatement targeting, and carbon accounting purposes.

Market Insights

The global methane satellite monitoring technologies market is experiencing a defining period of commercial emergence, driven by the convergence of rapidly declining small satellite manufacturing and launch costs, escalating regulatory and financial sector demand for independent and verifiable methane emission measurement, and the growing recognition among climate scientists, policymakers, and energy sector operators that satellite-derived methane data provides an objective, globally comprehensive, and operationally scalable emission monitoring capability that ground-based measurement networks and self-reported emission inventories cannot replicate. The market was valued at approximately USD 1.8 billion in 2025 and is projected to expand at a compound annual growth rate of 24.3% through 2034, as methane monitoring transitions from a scientific research tool into a commercially essential infrastructure service underpinning regulatory compliance verification, voluntary carbon market integrity assurance, operational leak detection programs, and financial sector climate risk disclosure obligations across oil and gas, agriculture, waste management, and coal mining industries worldwide.

The oil and gas sector represents the largest and most immediately actionable commercial application for satellite methane monitoring, as the combination of regulatory methane emission reduction mandates, voluntary methane pledge commitments by major oil and gas producers, and the growing use of third-party satellite emission verification by natural gas buyers seeking supply chain methane intensity certification is creating robust procurement demand for continuous, high-resolution, facility-level methane detection and quantification data across upstream production fields, midstream pipeline and compression infrastructure, liquefaction facilities, and downstream distribution networks. Point source detection capability, which enables satellite-based systems to identify and attribute individual large emission events to specific facilities or equipment items at spatial resolutions sufficient for operational response, represents the highest-value monitoring capability within the commercial market, as operators can use point source detection data to prioritize maintenance interventions, verify repair effectiveness, and demonstrate regulatory compliance without deploying ground-based inspection teams across geographically vast and logistically challenging production asset portfolios.

The proliferation of commercial small satellite constellations dedicated to methane monitoring, featuring revisit frequencies ranging from daily to near-continuous coverage of major emission source regions, is fundamentally transforming the temporal resolution and geographic coverage of operational methane monitoring beyond what was achievable with the sparse constellation of government scientific instruments that constituted the methane monitoring satellite capability through the early 2020s. Commercial operators are deploying constellations specifically optimized for methane detection with shortwave infrared spectrometers achieving methane column sensitivity below one part per billion at spatial resolutions enabling attribution to individual facilities, generating commercially valuable emission data products including point source emission rate estimates, facility-level emission factor quantification, and basin-wide emission inventory validation that oil and gas operators, regulatory agencies, and carbon market participants are actively procuring under data subscription and monitoring service agreements. Artificial intelligence and machine learning algorithms applied to satellite methane imagery are accelerating emission source detection, plume attribution, and emission quantification processing at scales and speeds that manual analysis of the growing satellite data volumes cannot achieve, establishing AI-powered data processing as an essential enabling technology for extracting operational value from high-revisit satellite methane monitoring datasets.

North America leads the global methane satellite monitoring market by commercial revenue, driven by the largest concentration of oil and gas production assets subject to methane emission monitoring obligations, the most developed voluntary methane reduction commitment landscape among major operators, and the most active financial sector integration of methane monitoring data into climate risk assessment and ESG investment analysis frameworks. Europe represents the second largest regional market, anchored by the European Union Methane Regulation imposing measurement, reporting, and verification requirements on oil and gas operators and importers that are creating mandatory procurement demand for third-party satellite monitoring services. Asia-Pacific is the fastest-growing regional market, driven by expanding regulatory methane monitoring requirements in China, growing investor pressure on Asian oil and gas companies for emission transparency, and the scale of agricultural and coal sector methane emissions across the region that represent undermonitored sources requiring satellite-based measurement.

Key Drivers

Escalating Regulatory Methane Emission Measurement, Reporting, and Verification Mandates Creating Mandatory Commercial Demand for Independent Satellite-Based Monitoring Services Across Oil, Gas, and Coal Industries

The European Union Methane Regulation, United States Environmental Protection Agency methane emission reporting and reduction rules, and emerging methane monitoring frameworks across Canada, Australia, and major natural gas producing and consuming nations are imposing legally binding measurement, reporting, and verification obligations on oil and gas operators, coal mine operators, and natural gas importers that require emission quantification methodologies with credibility and spatial coverage that facility-level ground measurements alone cannot cost-effectively provide across geographically extensive asset portfolios. Satellite-derived methane emission data is gaining regulatory acceptance as a complementary and in some cases primary measurement approach within these frameworks, creating durable mandatory procurement demand for satellite monitoring data services that is independent of voluntary corporate sustainability commitments and provides a stable regulatory-driven revenue foundation for commercial satellite methane monitoring operators.

Voluntary Corporate Methane Reduction Pledges and Natural Gas Supply Chain Methane Intensity Certification Creating Commercial Incentives for Satellite Monitoring Adoption Among Oil and Gas Operators

Major oil and gas corporations, midstream operators, and natural gas distribution companies have made public methane emission reduction commitments under industry initiatives and international methane pledge frameworks that require systematic emission measurement and quantification infrastructure to track progress, verify abatement effectiveness, and report credibly to investors, regulators, and the public on emission reduction performance against stated targets. Growing buyer demand for certified low-methane-intensity natural gas and LNG supply, particularly from European utilities and industrial customers facing supply chain emission disclosure obligations under corporate sustainability reporting regulations, is motivating natural gas producers and exporters to invest in satellite monitoring programs that can generate the continuous, independent emission measurement data required to obtain and maintain recognized methane intensity certification from established certification programs.

Rapid Cost Reduction in Small Satellite Manufacturing and Launch Services Enabling Commercial Constellation Deployment Economics That Were Not Achievable With Earlier Generation Satellite Technology

The transformation of satellite manufacturing economics through small satellite standardized bus architectures, commercial off-the-shelf component integration, and high-volume production line manufacturing, combined with the dramatic reduction in launch costs enabled by reusable launch vehicle technology and rideshare launch service proliferation, has reduced the capital investment required to deploy a commercially viable methane monitoring satellite constellation by an order of magnitude compared to the costs that governed scientific methane monitoring satellite development in preceding decades, enabling commercial operators and venture-backed startups to build and operate methane monitoring constellations at capital expenditure levels and operational timescales that attract private investment without requiring government balance sheet support or scientific agency procurement contracts as the primary revenue foundation.

Key Challenges

Cloud Cover, Atmospheric Interference, and Measurement Uncertainty Limitations Constraining the Reliability and Completeness of Satellite Methane Monitoring Data in Tropical and High-Latitude Regions

Shortwave infrared spectrometer-based methane satellite instruments require sunlight reflection from the Earth surface to measure atmospheric methane columns, making them ineffective during nighttime periods, in high solar zenith angle conditions at high latitudes during winter months, and most significantly under cloud cover conditions that obstruct the optical measurement path and render data collection impossible for the affected ground area on any given satellite overpass. In regions combining high methane emission source density with persistent or frequent cloud cover, including tropical oil and gas production basins, Southeast Asian coal mining regions, and high-latitude Arctic permafrost and gas production areas, the practical satellite data availability rate can be substantially below the nominal constellation revisit frequency, creating monitoring gaps that limit the operational value of satellite data for time-sensitive emission event detection and response applications.

Regulatory Data Acceptance and Standardization Gaps for Satellite-Derived Methane Measurements Creating Uncertainty Over the Legal Status and Compliance Value of Commercial Satellite Monitoring Data

While regulatory acceptance of satellite-derived methane emission data is advancing in the European Union, United States, and select other jurisdictions, the specific data quality standards, measurement uncertainty thresholds, detection limit requirements, and attribution methodology specifications that satellite monitoring data must satisfy to be accepted as compliant measurement evidence under different national regulatory frameworks remain incompletely defined in many jurisdictions, creating legal uncertainty for operators seeking to rely on satellite monitoring data for regulatory compliance purposes and limiting the willingness of some regulatory agencies to accept satellite measurements as primary compliance evidence without corroborating ground-level measurements. The absence of internationally harmonized satellite methane measurement standards also complicates cross-border emission monitoring comparability and the acceptance of satellite data in multinational carbon market and climate disclosure frameworks.

Small Satellite Constellation Operational Reliability, Data Continuity Risk, and the Financial Sustainability Challenges Facing Commercial Methane Monitoring Operators in a Nascent Revenue Market

Commercial methane satellite monitoring operators must maintain constellation operational continuity and data service quality across satellite hardware that is subject to orbital degradation, instrument calibration drift, and potential component failures in the space environment, requiring satellite replenishment investment programs that impose ongoing capital expenditure obligations on operators whose revenue streams from commercial data subscriptions and monitoring service contracts are still scaling from relatively modest early adopter volumes toward the larger customer base required to support financially sustainable constellation operations without continued dependence on venture capital or government grant funding. The concentration of commercial methane satellite monitoring revenue among a limited number of large oil and gas operator customers creates customer concentration risk and commercial vulnerability to procurement budget cuts during commodity price downturns.

Market Segmentation

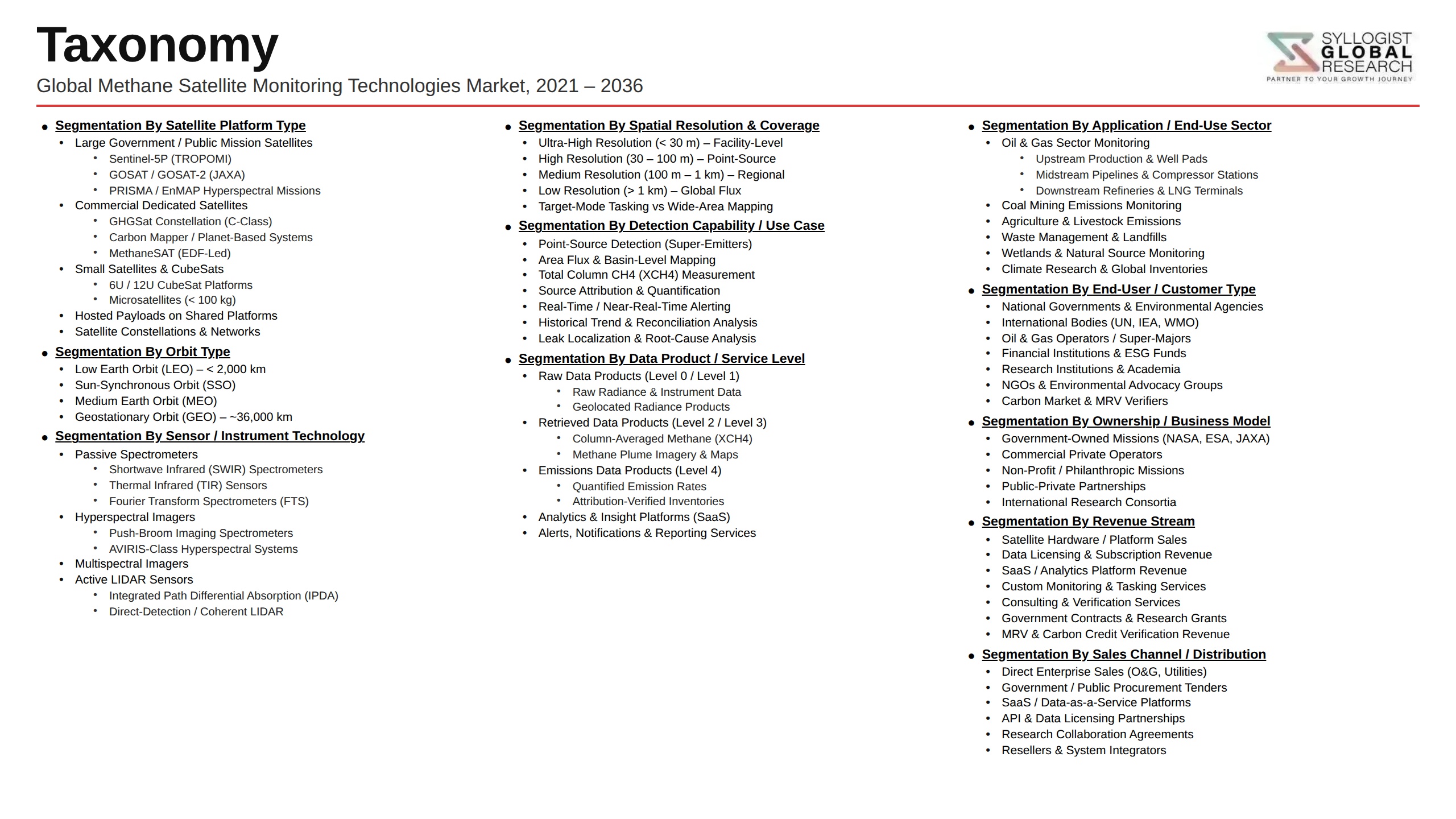

- Segmentation By Satellite Type

- Dedicated Commercial Methane Monitoring Constellations

- Government Scientific Methane Monitoring Satellites

- Multi-Purpose Earth Observation Satellites with Methane Capability

- Nanosatellites and CubeSat-Based Methane Sensors

- Geostationary Methane Monitoring Platforms

- Others

- Segmentation By Sensor Technology

- Shortwave Infrared Spectrometers

- Thermal Infrared Emission Sensors

- Hyperspectral Imaging Spectrometers

- Laser Absorption Spectroscopy Instruments

- Multispectral Imaging Systems

- Others

- Segmentation By Monitoring Capability

- Global Background Methane Column Monitoring

- Regional Emission Source Area Detection

- Facility-Level Point Source Detection and Quantification

- Super-Emitter Identification and Attribution

- Continuous High-Revisit Basin-Wide Surveillance

- Others

- Segmentation By End Use Application

- Oil and Gas Upstream Leak Detection and Monitoring

- Midstream Pipeline and Infrastructure Emission Surveillance

- LNG Liquefaction and Terminal Emission Verification

- Coal Mine Methane Emission Monitoring

- Agricultural and Livestock Methane Quantification

- Landfill and Waste Sector Emission Monitoring

- Climate Science and Atmospheric Research

- Others

- Segmentation By End User

- Oil and Gas Exploration and Production Companies

- Midstream Pipeline and Gas Transmission Operators

- National Environmental and Regulatory Agencies

- Financial Institutions and ESG Investors

- Carbon Market Verification and Certification Bodies

- Agricultural Ministries and Food Supply Chain Operators

- Academic and Climate Research Institutions

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global methane satellite monitoring technologies market valuation in 2025, projected through 2034, segmented by satellite type, sensor technology, and end use application, enabling satellite operators, data service providers, regulatory agencies, and oil and gas operators to identify the highest-growth monitoring capability categories and most commercially compelling service deployment opportunities across the global market?

- How are European Union Methane Regulation requirements, United States EPA methane monitoring rules, and emerging measurement, reporting, and verification frameworks in Canada, Australia, and major gas-producing nations shaping mandatory data procurement obligations for oil and gas operators and importers, and what satellite monitoring data quality standards and attribution methodology specifications are regulatory agencies establishing for compliance acceptance?

- Which satellite methane monitoring capabilities, specifically facility-level point source detection, super-emitter identification, continuous basin-wide surveillance, and agricultural and waste sector emission quantification, are generating the highest commercial revenue growth through 2034, and what detection sensitivity, spatial resolution, revisit frequency, and measurement uncertainty performance levels are required for each target application and customer segment?

- How is the competitive landscape structured among dedicated commercial methane monitoring satellite operators, multi-purpose Earth observation data providers, and AI-powered methane data analytics platform developers, and what constellation architecture design, sensor technology differentiation, data product development, regulatory engagement, and customer partnership strategies are enabling leading operators to build durable commercial positions in this emerging market?

- What cloud cover interference limitations, atmospheric correction methodology uncertainties, and measurement validation challenges are most constraining the practical data availability and quantification accuracy of commercial satellite methane monitoring systems across tropical, high-latitude, and persistently cloudy emission source regions, and what constellation design, sensor technology, and data fusion approaches are operators developing to mitigate these measurement gap challenges?

- How are natural gas buyers, LNG importers, and carbon market participants using satellite-derived methane emission data to inform natural gas supply chain methane intensity certification decisions, responsible sourcing procurement criteria, carbon credit integrity verification, and financial sector climate risk disclosure reporting, and what data product specifications and third-party verification frameworks are emerging to support these commercial applications?

- Which regional methane emission source landscapes, specifically North American oil and gas basins, Middle Eastern production infrastructure, South and Southeast Asian coal and agricultural sectors, and Latin American oil production regions, represent the most commercially significant undermonitored methane emission environments, and what combinations of regulatory framework development, operator procurement activity, and emission abatement urgency are defining the near-term commercial opportunity in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Satellite Data Accuracy, Detection Limit & Attribution Uncertainty Risk

- Cloud Cover, Atmospheric Interference & Retrieval Algorithm Performance Risk

- Launch Failure, Orbital Lifetime & Satellite Constellation Continuity Risk

- Data Privacy, National Sovereignty & Contested Airspace Regulatory Risk

- Commercial Adoption Barrier, Willingness-to-Pay & Regulatory Mandate Uncertainty Risk

- Competition from Airborne, Ground-Based & In-Situ Methane Monitoring Alternatives Risk

- Regulatory Framework & Standards

- EU Methane Regulation (2024/1787), MRV Requirements & Satellite Data Acceptance for Oil, Gas & Coal Operators

- US EPA Methane Rules, Waste Emissions Charge & OOOOa/OOOOb Standards for Monitoring, Reporting & Verification

- UNFCCC Global Methane Pledge, IMO & ICAO Methane Emission Reporting Frameworks

- OGMP 2.0, IPIECA & Methane Guiding Principles: Voluntary Industry MRV Standards & Satellite Data Integration

- Satellite Data Quality, Calibration & Validation Standards: ISO, WMO & CEOS QA4EO Frameworks

- Space Law, Remote Sensing Data Licensing, Export Controls & Commercial Satellite Operator Regulatory Frameworks

- Global Methane Satellite Monitoring Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Satellites & Data Subscriptions)

- Market Size & Forecast by Satellite Platform Type

- Government & Space Agency Methane Monitoring Satellites (TROPOMI, GHGSat-GV & Sentinel-5P)

- Commercial Small Satellite & CubeSat Methane Monitoring Constellations

- Geostationary (GEO) Methane Monitoring Satellites

- Low Earth Orbit (LEO) Methane Monitoring Satellites

- Medium Earth Orbit (MEO) & Sun-Synchronous Orbit Methane Satellites

- Multi-Gas & Greenhouse Gas Monitoring Satellites with Methane Detection Capability

- Market Size & Forecast by Sensing Technology

- Shortwave Infrared (SWIR) Spectrometer-Based Methane Detection

- Thermal Infrared (TIR) & Mid-Infrared (MIR) Radiometer-Based Detection

- Hyperspectral Imaging Spectrometer Technology

- Differential Absorption Lidar (DIAL) & Laser-Based Active Remote Sensing

- Multispectral & Broadband Passive Remote Sensing Technology

- Market Size & Forecast by Spatial Resolution & Detection Capability

- Regional-Scale Background Monitoring (Above 10 km Resolution)

- Basin & Country-Scale Monitoring (1 km to 10 km Resolution)

- Facility-Scale & Point Source Detection (100 m to 1 km Resolution)

- Super-Emitter & Ultra-High Resolution Pinpoint Detection (Below 100 m Resolution)

- Market Size & Forecast by Product & Service Type

- Raw Satellite Imagery & Level 1 Radiance Data Products

- Processed Methane Column Concentration (XCH4) & Flux Data Products

- Methane Emission Analytics, Attribution & Source Identification Services

- Continuous Monitoring Subscription & Alert Notification Services

- MRV Platform, Regulatory Reporting & Compliance Verification Services

- Integrated Satellite & Ground-Based Sensor Fusion Data Services

- Carbon Credit Verification, Methane Offset & ESG Disclosure Data Services

- Market Size & Forecast by Application

- Oil & Gas Upstream: Wellsite, Production Facility & Pipeline Leak Detection

- Oil & Gas Midstream: Compressor Station, Processing Plant & Transmission Pipeline Monitoring

- LNG Terminal, Liquefaction & Regasification Facility Monitoring

- Coal Mine Methane Monitoring (Surface & Underground Mines)

- Agriculture & Livestock Enteric Fermentation & Manure Methane Monitoring

- Landfill, Waste Treatment & Municipal Solid Waste Methane Monitoring

- Wetland, Permafrost & Natural Ecosystem Methane Flux Monitoring

- National Greenhouse Gas Inventory Verification & UNFCCC Reporting

- Market Size & Forecast by End-User

- Oil & Gas Exploration & Production (E&P) Companies

- LNG Producers, Midstream Operators & Gas Utilities

- Coal Mining Companies

- Government Environmental Agencies & National Regulators

- Climate Research Institutes, Universities & Space Agencies

- Carbon Market Registries, ESG Data Providers & Financial Institutions

- NGOs, Environmental Watchdog Organisations & Investigative Journalism

- Market Size & Forecast by Sales Channel

- Direct Satellite Operator & Data Provider Sales

- API-Based Platform, SaaS & Data Subscription Channel

- Government Agency & Space Programme Procurement Channel

- ESG Data Aggregator, Analytics Platform & Reseller Channel

- MRV Service Provider & Regulatory Compliance Consultant Channel

- North America Methane Satellite Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Data Subscriptions)

- By Satellite Platform Type

- By Sensing Technology

- By Spatial Resolution & Detection Capability

- By Product & Service Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Methane Satellite Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Data Subscriptions)

- By Satellite Platform Type

- By Sensing Technology

- By Spatial Resolution & Detection Capability

- By Product & Service Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Methane Satellite Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Data Subscriptions)

- By Satellite Platform Type

- By Sensing Technology

- By Spatial Resolution & Detection Capability

- By Product & Service Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Methane Satellite Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Data Subscriptions)

- By Satellite Platform Type

- By Sensing Technology

- By Spatial Resolution & Detection Capability

- By Product & Service Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Methane Satellite Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Data Subscriptions)

- By Satellite Platform Type

- By Sensing Technology

- By Spatial Resolution & Detection Capability

- By Product & Service Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Methane Satellite Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Data Subscriptions)

- By Satellite Platform Type

- By Sensing Technology

- By Spatial Resolution & Detection Capability

- By Product & Service Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Netherlands, Norway, Italy, Australia, Japan, China, India, South Korea, Singapore, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Qatar, Oman, Kazakhstan, Russia, South Africa, Nigeria

- Technology Landscape & Innovation Analysis

- SWIR Spectrometer Technology Deep-Dive: GHGSat, MethaneSAT, Carbon Mapper & EMIT Instrument Design & Detection Performance

- Hyperspectral Imaging Technology: Spectral Resolution, SNR, Calibration & On-Board Processing Advances for Methane Detection

- CubeSat & Small Satellite Constellation Technology: Mass Production, Launch Cadence, Revisit Rate & Cost-Per-Observation Economics

- AI & Machine Learning for Methane Plume Detection, Source Attribution, Flux Quantification & False Positive Reduction

- Satellite & Airborne Data Fusion Technology: Integrating TROPOMI, Sentinel-5P, Airborne AVIRIS-NG & Ground Sensor Networks

- Geostationary Methane Monitoring Technology: GeoCARB, GOSAT-GW & High-Temporal Resolution Diurnal Emission Tracking

- On-Board Processing, Edge AI & Direct-to-Ground Data Downlink Technology for Real-Time Methane Alerting

- Patent & IP Landscape in Methane Satellite Monitoring Technologies

- Value Chain & Supply Chain Analysis

- Satellite Bus, Structure, Thermal Control & Power System Supply Chain

- Imaging Spectrometer, Optical System, Detector Array & Cryocooler Supply Chain

- On-Board Computer, Data Handling, Communication Payload & RF System Supply Chain

- Launch Vehicle, Integration, Testing & Mission Assurance Supply Chain

- Ground Station, Telemetry, Data Downlink & Mission Operations Supply Chain

- Data Processing, Retrieval Algorithm, Cloud Computing & AI Analytics Platform Supply Chain

- API, SaaS Platform, MRV Integration & End-User Interface Supply Chain

- Pricing Analysis

- Satellite Data Subscription Pricing by Spatial Resolution, Coverage Frequency & Service Tier

- Methane Analytics, Attribution & MRV Platform Annual Subscription Pricing Analysis

- Per-Site, Per-Asset & Enterprise Licence Pricing Model Analysis

- Government & Space Agency Contract vs. Commercial Subscription Pricing Comparison

- Cost-per-Tonne Methane Detected & Economic Value of Leak Repair ROI Analysis

- Price Trend Analysis: Impact of Constellation Scale-Up, Competition & Regulatory Mandates on Data Pricing

- Sustainability & Environmental Analysis

- Quantified Climate Impact of Satellite Methane Monitoring: Emission Reductions Enabled, GWP Abatement & Carbon Equivalent Value

- Lifecycle Assessment (LCA) of Satellite Manufacturing & Launch: Carbon Footprint, Launch Emissions & Orbital Debris Impact

- Role of Methane Satellite Data in Supporting UNFCCC NDCs, Global Methane Pledge Accountability & Net Zero Pathways

- Democratisation of Methane Transparency: Public Data Access, Open Science & Civil Society Accountability Applications

- SDG 13 (Climate Action) & SDG 17 (Partnerships for Goals) Alignment & Green Finance Data Infrastructure Contribution

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Sensing Technology, Application & Geography

- Player Classification

- Commercial Methane Satellite Operators & Constellation Developers

- Government Space Agencies & National Methane Monitoring Satellite Programmes

- Methane Analytics, AI & MRV Platform Software Providers

- Integrated Satellite & Aerial Survey Methane Monitoring Service Providers

- ESG Data Aggregators & Carbon Market Data Platforms with Methane Data Integration

- Aerospace & Satellite System Integrators with Methane Payload Capability

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Service Type & Region

- Company Profile

- Company Overview & Headquarters

- Methane Monitoring Satellite Products, Constellation & Service Portfolio

- Key Customer Relationships & Reference Deployments

- Satellite Assets, Orbital Coverage & Data Resolution Capabilities

- Revenue (Methane Monitoring Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Satellite Launches, Contract Wins, Data Product Releases)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Detection Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Sensing Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Constellation Development & Technology Investment Strategy

- Data Product, Analytics Platform & MRV Service Development Strategy

- Geographic Expansion & New Sector Penetration Strategy

- Customer, Regulator & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Policy Engagement, Regulatory Advocacy & Data Standardisation Strategy

- Sustainability, Open Data & Climate Impact Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output