Global Autonomous Shuttle Market By Vehicle Type, By Propulsion Type, By Level of Autonomy, By Application, By Component, By Capacity, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

Autonomous shuttles are driverless or semi-driverless transit vehicles purpose-built for short-distance, low-speed passenger movement, typically deployed across fixed or semi-fixed routes within controlled or geofenced operational environments. The Global Autonomous Shuttle Market encompasses the design, manufacturing, deployment, and operation of self-driving multi-passenger vehicles powered primarily by electric or hybrid propulsion systems, integrated with advanced sensor suites including light detection and ranging (LiDAR), radar, ultrasonic sensors, high-resolution cameras, global navigation satellite systems, and onboard artificial intelligence computing platforms enabling perception, localization, decision-making, and motion control. The autonomous shuttle market covers vehicles operating across multiple service environments including airports, corporate campuses, university transit systems, retirement communities, central business districts, hospital and healthcare shuttle services, tourist destinations, mining and industrial sites, and first-mile and last-mile public transit applications connecting commuters to mass transit hubs.

Market participants include autonomous shuttle original equipment manufacturers, autonomous driving software developers, sensor and component suppliers, fleet operators, mobility-as-a-service providers, public transit agencies, mixed-use real estate developers, and infrastructure providers supporting vehicle-to-everything (V2X) connectivity. The scope of the autonomous shuttle market also covers associated services including remote teleoperation, fleet monitoring, predictive maintenance, charging infrastructure, route optimization software, passenger information systems, and regulatory compliance management. Revenue streams within the autonomous shuttle market span vehicle sales, hardware components, software licensing, subscription-based mobility services, public-private partnership operating contracts, and aftermarket service agreements covering maintenance, software updates, and fleet management. The autonomous shuttle market explicitly excludes long-haul autonomous trucking, autonomous robotaxi services using sedan-class passenger vehicles, and personal-use autonomous passenger cars, focusing instead on purpose-built, low-speed, multi-passenger transit platforms designed for shared mobility applications.

Market Insights

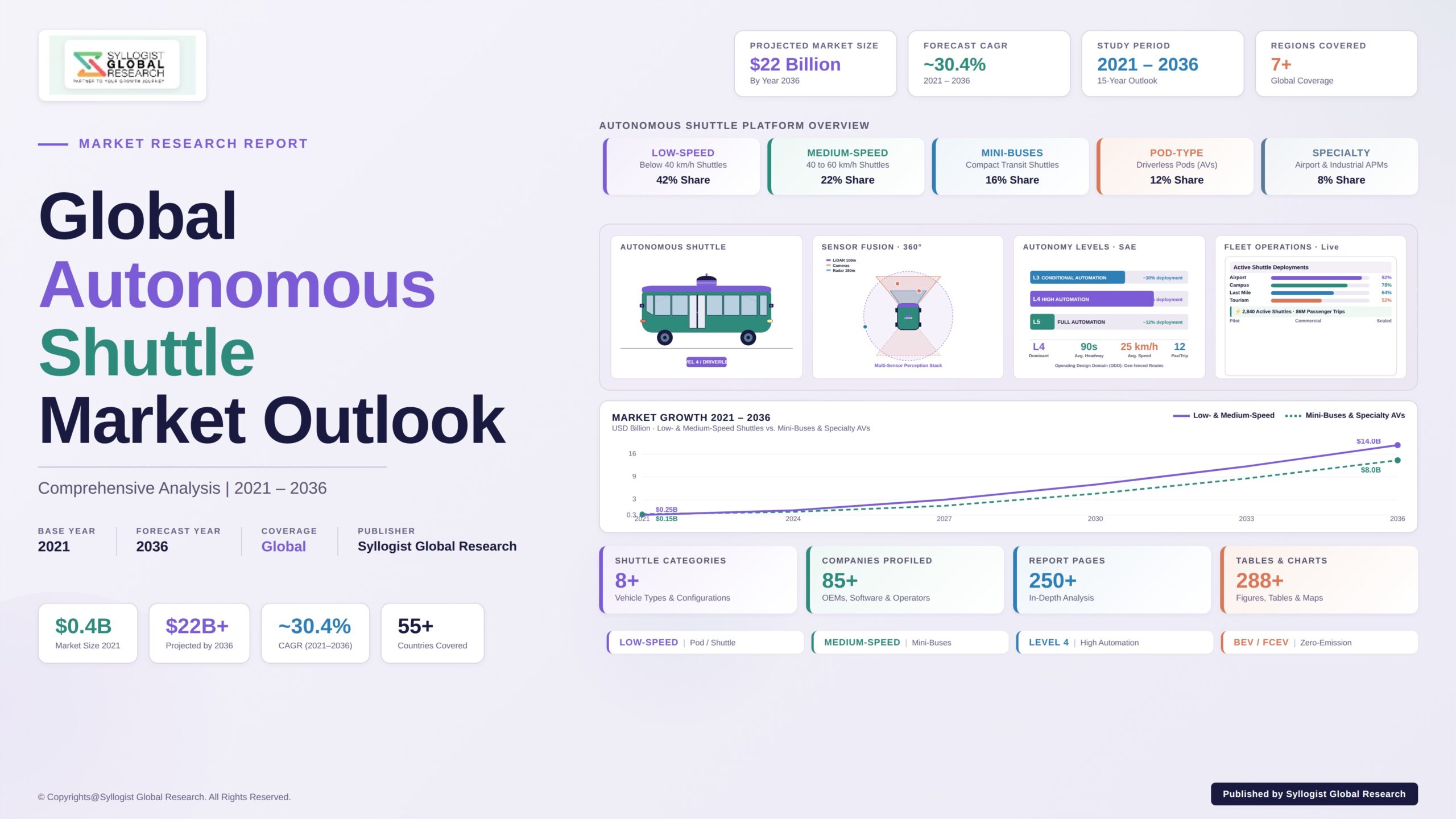

The global autonomous shuttle market is entering a transformational commercial scaling phase, shaped by accelerating urbanization, mounting pressure on aging public transit infrastructure, intensifying electrification mandates, and rapid maturation of perception, localization, and motion planning algorithms enabling commercially viable driverless operation in geofenced low-speed environments. The autonomous shuttle market was valued at approximately USD 1.6 billion in 2025 and is projected to reach USD 14.8 billion by 2034, advancing at a compound annual growth rate of 28.1% through the forecast period, as fleet operators, municipal transit agencies, airport authorities, corporate campus owners, and mobility-as-a-service providers transition autonomous shuttle deployments from pilot demonstrations into commercial revenue-generating service operations across North America, Europe, and Asia-Pacific transit corridors.

The strategic momentum driving the autonomous shuttle market is reinforced by tangible operational evidence from over 50 million kilometers of cumulative commercial pilot operation, generating safety performance data, passenger acceptance benchmarks, and total cost of ownership validation that procurement decision-makers in transit authorities and corporate campus operators now reference when structuring autonomous shuttle fleet investment decisions. Sensor stack costs have declined by over 75% since 2020, propelled by solid-state LiDAR commercialization, automotive-grade radar evolution, and cloud-based high-definition mapping models, with mainstream automotive-grade LiDAR units now available below USD 1,000 per sensor. Regulatory frameworks in Singapore, Japan, Germany, France, the United States, the United Arab Emirates, and China have established formal certification pathways for autonomous shuttle operation under defined operational design domains, providing the legal clarity that institutional buyers require before committing capital to multi-year autonomous shuttle fleet procurement programs.

First-mile and last-mile public transit applications represent the fastest growing autonomous shuttle deployment category, driven by transit agencies seeking cost-efficient solutions to bridge gaps between primary transit hubs and dispersed residential neighborhoods where conventional fixed-route bus economics remain commercially unviable. Battery electric propulsion accounts for over 92% of new autonomous shuttle deployments globally, reflecting natural alignment between purpose-built low-speed shuttle platforms and zero-emission mandates implemented by municipal authorities across mature transit markets. Airport and seaport shuttle applications have emerged as among the most commercially mature segments within the autonomous shuttle market, with controlled operating environments, predictable passenger flow patterns, and clearly defined route geometries supporting rapid scaling of driverless commercial operations. Level 4 autonomy configurations represent the dominant technical benchmark in commercial autonomous shuttle deployments, with fully driverless operation increasingly accepted within geofenced operational design domains across major deployment geographies.

Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034 within the autonomous shuttle market, underpinned by aggressive autonomous mobility investment programs in China, Singapore, Japan, and South Korea, where national governments are coordinating regulatory approval, infrastructure deployment, and domestic manufacturing capability scaling under integrated industrial policy frameworks. China hosts the largest concentration of autonomous shuttle pilot deployments globally, with over 60 cities operating driverless shuttle programs at varying commercial maturity levels. North America represents the second largest regional autonomous shuttle market, with the United States leading in private campus, corporate, airport, and university transit deployments, supported by venture capital investment and growing public-sector procurement participation. Europe occupies the third major regional position within the autonomous shuttle market, supported by extensive municipal transit pilot programs in France, Germany, the Netherlands, and the Nordic countries, where transit decarbonization mandates and aging public bus fleet replacement schedules are simultaneously accelerating commercial autonomous shuttle procurement timelines.

Key Drivers

Rising Urbanization, Aging Public Transit Infrastructure, and Acute Driver Shortages Generating Sustained Procurement Demand for Autonomous Shuttle Solutions

The intensifying pressures of global urbanization, combined with chronic public transit workforce shortages and aging fleet infrastructure approaching replacement across mature transit markets, are creating durable procurement demand for autonomous shuttle systems capable of sustainably reducing per-passenger operating costs while expanding service coverage into residential corridors that conventional fixed-route bus economics cannot support. Public transit authorities in the United States, Germany, France, the United Kingdom, and Japan are confronting structural driver shortages estimated above 15% of authorized workforce, accelerated by demographic aging, pandemic-induced workforce attrition, and competitive wage pressure from logistics and ride-hailing sectors. Autonomous shuttle deployments offer transit operators the capability to maintain or expand service levels without proportional workforce expansion, with operating cost reductions of 35% to 50% achievable at scaled fleet deployment within the autonomous shuttle market. Municipal procurement programs are increasingly structuring multi-year frameworks incorporating fleet replacement schedules, charging infrastructure development, and operational data integration into existing dispatch and fleet management systems, creating long-duration revenue commitments that anchor manufacturer production planning and component supplier capacity scaling decisions across the autonomous shuttle value chain.

Zero-Emission Transit Mandates and Electrification Procurement Policies Creating Strong Strategic Alignment with Autonomous Shuttle Technology Readiness

Aggressive zero-emission transit mandates implemented by national governments and municipal authorities across the European Union, California, New York, China, and select Asia-Pacific jurisdictions are generating procurement preference toward electric autonomous shuttles, which deliver integrated alignment with sustainability compliance frameworks while simultaneously providing autonomous mobility benefits within a single procurement decision. The European Union Clean Vehicles Directive mandates progressive zero-emission targets for public transit fleet procurement, with member states required to achieve at least 32.5% zero-emission share in new public sector bus and shuttle purchases by 2030. California has established a 100% zero-emission bus purchase requirement by 2029 for transit agencies, and New York City has committed to a fully electric municipal transit fleet by 2040. Over 92% of autonomous shuttles currently in commercial deployment globally use battery-electric propulsion, reflecting the natural fit between purpose-built low-speed shuttle platforms and electric powertrain economics. The combination of sustainability mandate compliance, reduced operating cost from electric propulsion energy economics, and autonomous operational savings creates a compelling total cost of ownership advantage for transit operators evaluating fleet modernization investments across multi-decade depreciation timelines within the autonomous shuttle market.

Maturing Sensor Hardware Cost Curves and Operational Design Domain Certification Frameworks Enabling Scalable Commercial Driverless Shuttle Deployment

The substantial cost reductions across LiDAR sensors, automotive-grade radar units, perception computing modules, and high-definition mapping infrastructure are progressively eliminating hardware cost barriers that previously constrained commercial viability of autonomous shuttle deployments at scale. Solid-state LiDAR unit costs have declined by over 75% since 2020, with mainstream automotive-grade units now available below USD 1,000 per sensor, and centralized perception compute platforms have similarly recorded 60% to 70% cost reductions through automotive-grade silicon integration and software efficiency gains. Concurrently, regulatory authorities in Germany, France, Japan, Singapore, the United Arab Emirates, China, and multiple United States states have established formal operational design domain certification frameworks permitting commercial driverless shuttle operation within defined geographic zones, speed envelopes, and operational conditions, providing the legal clarity and procurement assurance that public agency and corporate buyers require before committing capital to autonomous shuttle fleet investments. Insurance providers have introduced dedicated autonomous shuttle coverage products informed by accumulated safety performance data from over 50 million kilometers of commercial pilot operation, further reducing financial risk barriers to commercial autonomous shuttle procurement at fleet scale across the autonomous shuttle market.

Key Challenges

Fragmented Regulatory Approval Pathways, Cross-Jurisdictional Compliance Variability, and Extended Public Road Certification Timelines

The regulatory approval pathways governing commercial deployment of autonomous shuttles on public roads remain materially fragmented across national, state or provincial, and municipal jurisdictions, generating compliance complexity and procurement uncertainty that constrains the pace at which autonomous shuttle operators can scale fleet deployments across multi-city operating territories. Operational design domain certification requirements vary substantially across regulatory authorities, with some jurisdictions requiring exhaustive scenario-based safety validation, dedicated safety case documentation, and on-board safety operator presence during commercial operation, while other jurisdictions accept manufacturer self-certification supplemented by post-deployment safety reporting obligations. The absence of internationally harmonized type approval standards forces autonomous shuttle manufacturers to maintain region-specific software calibrations, sensor configurations, and validation evidence portfolios, increasing engineering overhead and constraining global platform scalability across the autonomous shuttle market. Public road certification timelines averaging 18 to 36 months across major jurisdictions limit the pace at which fleet operators can transition from controlled pilot environments into revenue-generating commercial deployment, depressing near-term return on investment metrics and complicating capital allocation decisions for both autonomous shuttle manufacturers and fleet operators evaluating geographic expansion strategies.

Persistent Operational Performance Limitations in Adverse Weather, Complex Urban Traffic Interactions, and Dense Mixed-Pedestrian Environments

Autonomous shuttles continue to encounter operational performance limitations when confronting adverse weather conditions including heavy rain, dense fog, snow accumulation, and direct sun glare affecting camera and LiDAR perception fidelity, alongside complex urban traffic scenarios involving unprotected left turns, dense pedestrian crossings, irregular cyclist behavior, and emergency vehicle interactions that current perception and behavior prediction algorithms cannot consistently navigate at human-equivalent reliability levels. Commercial deployments routinely incorporate operational design domain restrictions that suspend autonomous operation during defined weather thresholds, route segments with high pedestrian density, or specific times of day where lighting conditions exceed sensor performance envelopes, generating service reliability concerns and forcing operators to maintain backup human operator availability that erodes the labor cost reduction benefits motivating autonomous shuttle procurement. Mixed pedestrian environments in central business districts, university campuses, and tourist precincts generate particularly complex behavior prediction challenges within the autonomous shuttle market, with autonomous shuttles required to interpret nuanced pedestrian intent signals that experienced human drivers process intuitively but that machine learning perception systems continue to address inconsistently across diverse cultural and demographic operational contexts.

Public Acceptance Hesitancy, Safety Incident Sensitivity, and Insurance Liability Frameworks Complicating Commercial Scaling Decisions

Public passenger acceptance of fully driverless shuttle operation remains an evolving variable across the autonomous shuttle market, with consumer survey data indicating that approximately 40% to 55% of surveyed passengers across mature transit markets express continued hesitancy about boarding a shuttle without a visible safety operator, particularly during nighttime hours, in low-density geographic areas, or for journeys involving children or elderly family members. Individual safety incidents involving autonomous shuttles attract disproportionate media coverage relative to comparable conventional vehicle incidents, generating concentrated reputational risk that can suspend or terminate commercial deployments well in advance of formal regulatory determinations regarding causation or operator liability. Insurance liability frameworks governing autonomous shuttle operation remain inconsistently developed across jurisdictions, with continued ambiguity regarding liability allocation among vehicle manufacturers, autonomous software providers, fleet operators, and remote teleoperation service providers in incidents involving complex multi-actor causation chains. Insurance premium pricing for autonomous shuttle operation remains materially elevated relative to comparable conventional shuttle insurance pricing, partially offsetting labor cost savings that motivate autonomous procurement decisions and complicating financial modeling for fleet expansion proposals submitted to municipal procurement boards and corporate capital investment committees.

Market Segmentation

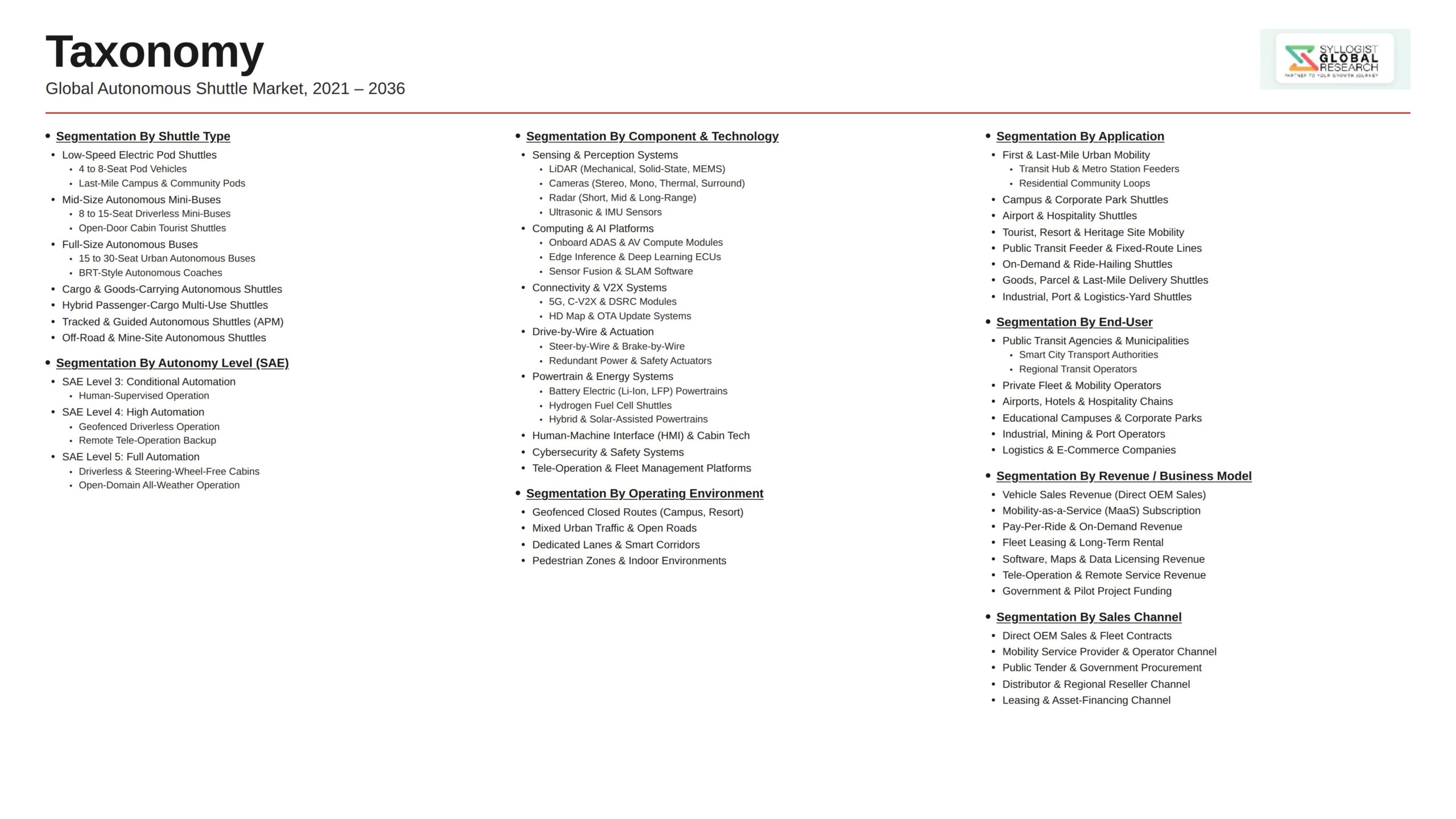

- Segmentation By Vehicle Type

- Low-Speed Shuttles (Below 40 km/h)

- Medium-Speed Shuttles (40-60 km/h)

- Mini-Buses and Compact Transit Shuttles

- Pod-Type Autonomous Vehicles

- Others

- Segmentation By Propulsion Type

- Battery Electric

- Hybrid Electric

- Fuel Cell Electric (Hydrogen)

- Internal Combustion Engine

- Segmentation By Level of Autonomy

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Segmentation By Application

- Airport and Seaport Shuttle Services

- Corporate Campus and Industrial Site Transit

- University and Educational Campus Mobility

- First-Mile and Last-Mile Public Transit

- Tourism, Theme Park, and Resort Transit

- Hospital and Healthcare Facility Shuttle

- Retirement Community and Senior Living Transit

- Mining and Industrial Worksite Shuttle

- Others

- Segmentation By Component

- LiDAR Sensors

- Radar Sensors

- Cameras and Imaging Systems

- Ultrasonic Sensors

- Global Navigation Satellite Systems

- Onboard Computing and AI Processors

- Vehicle-to-Everything (V2X) Communication Modules

- Software and Operating Systems

- Others

- Segmentation By Capacity

- Up to 8 Passengers

- 9 to 15 Passengers

- 16 to 25 Passengers

- Above 25 Passengers

- Segmentation By End User

- Public Transit Agencies and Municipal Authorities

- Airport and Seaport Operators

- Corporate Campus Operators

- Educational Institutions

- Hospitality and Tourism Operators

- Healthcare Facility Operators

- Industrial and Mining Site Operators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Autonomous Shuttle Market in 2025, projected through 2034, segmented by vehicle type, propulsion technology, and application, enabling vehicle manufacturers, fleet operators, public transit agencies, and infrastructure investors to identify highest-growth segments and most durable revenue opportunities across the autonomous shuttle market landscape?

- How are public transit agencies, airport operators, corporate campus owners, and mobility-as-a-service providers structuring procurement frameworks for autonomous shuttle fleets, and which operating models, including ownership, leasing, and outcome-based service contracts, are emerging as the dominant commercial structures shaping autonomous shuttle deployment economics through 2034?

- What operational design domain limitations, regulatory certification timelines, and adverse weather performance constraints are shaping commercial deployment pace and geographic scaling decisions for autonomous shuttle fleet operators across North America, Europe, and Asia-Pacific?

- Which propulsion technologies, including battery electric, hydrogen fuel cell, and hybrid configurations, are gaining the strongest procurement traction within autonomous shuttle programs, and how are charging and refueling infrastructure investment decisions aligning with autonomous shuttle fleet deployment roadmaps?

- How is the competitive landscape structured among autonomous shuttle original equipment manufacturers, perception software providers, sensor hardware suppliers, and integrated mobility service operators, and what partnership and acquisition strategies are enabling new entrants to compete against established autonomous mobility platform providers?

- What sensor configurations, computing architectures, and software platform decisions are emerging as the technical benchmarks shaping operational reliability, passenger safety performance, and total cost of ownership outcomes across commercial autonomous shuttle deployments globally?

- Which regional markets, including Asia-Pacific, Europe, and North America, are projected to generate the largest incremental autonomous shuttle deployment opportunities through 2034, and what regulatory, demographic, infrastructure, and economic factors are shaping capability investment priorities and supplier selection decisions in each regional autonomous shuttle market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Regulatory Approval Pathway, Operational Design Domain Certification & Cross-Jurisdictional Compliance Risk

- Operational Performance, Adverse Weather Limitation & Mixed-Pedestrian Environment Behavioural Prediction Risk

- Public Acceptance Hesitancy, Safety Incident Sensitivity & Brand Reputational Risk

- Insurance Liability Allocation, Multi-Actor Causation & Risk Underwriting Risk

- Charging Infrastructure Availability, Battery Range Constraint & Operational Continuity Risk

- Regulatory Framework & Standards

- Operational Design Domain (ODD) Certification & Driverless Operation Authorisation Frameworks

- Vehicle Type Approval, Functional Safety & Cybersecurity Standards (ISO 26262, ISO 21448, UNECE WP.29)

- Zero-Emission Transit Mandates, Low-Emission Zone Enforcement & Sustainability Procurement Policies

- Data Privacy, Cybersecurity & V2X Communication Compliance Standards

- Insurance, Liability Allocation & Cross-Border Operating Compliance Frameworks for Autonomous Shuttles

- Global Autonomous Shuttle Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Active Shuttles in Service and Annual Passenger Trips in Millions)

- Market Size & Forecast by Vehicle Type

- Low-Speed Shuttles (Below 40 km/h)

- Medium-Speed Shuttles (40 to 60 km/h)

- Mini-Buses & Compact Transit Shuttles

- Pod-Type Autonomous Vehicles

- Others

- Market Size & Forecast by Propulsion Type

- Battery Electric

- Hybrid Electric

- Fuel Cell Electric (Hydrogen)

- Internal Combustion Engine

- Market Size & Forecast by Level of Autonomy

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

- Market Size & Forecast by Application

- Airport & Seaport Shuttle Services

- Corporate Campus & Industrial Site Transit

- University & Educational Campus Mobility

- First-Mile & Last-Mile Public Transit

- Tourism, Theme Park & Resort Transit

- Hospital & Healthcare Facility Shuttle

- Retirement Community & Senior Living Transit

- Mining & Industrial Worksite Shuttle

- Others

- Market Size & Forecast by Component

- LiDAR Sensors

- Radar Sensors

- Cameras & Imaging Systems

- Ultrasonic Sensors

- Global Navigation Satellite Systems (GNSS)

- Onboard Computing & AI Processors

- Vehicle-to-Everything (V2X) Communication Modules

- Software & Operating Systems

- Others

- Market Size & Forecast by Capacity

- Up to 8 Passengers

- 9 to 15 Passengers

- 16 to 25 Passengers

- Above 25 Passengers

- Market Size & Forecast by End-User

- Public Transit Agencies & Municipal Authorities

- Airport & Seaport Operators

- Corporate Campus Operators

- Educational Institutions

- Hospitality & Tourism Operators

- Healthcare Facility Operators

- Industrial & Mining Site Operators

- Others

- Market Size & Forecast by Sales Channel

- Direct OEM Vehicle Sales to Fleet Operators

- Mobility-as-a-Service (MaaS) Operating Contracts

- Public-Private Partnership (PPP) & Concession Operating Models

- Lease, Rental & Subscription Fleet Procurement

- Aftermarket Service & Long-Term Maintenance Contracts

- North America Autonomous Shuttle Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Shuttles in Service and Annual Passenger Trips in Millions)

- By Vehicle Type

- By Propulsion Type

- By Level of Autonomy

- By Application

- By Component

- By Capacity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Autonomous Shuttle Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Shuttles in Service and Annual Passenger Trips in Millions)

- By Vehicle Type

- By Propulsion Type

- By Level of Autonomy

- By Application

- By Component

- By Capacity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Autonomous Shuttle Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Shuttles in Service and Annual Passenger Trips in Millions)

- By Vehicle Type

- By Propulsion Type

- By Level of Autonomy

- By Application

- By Component

- By Capacity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Autonomous Shuttle Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Shuttles in Service and Annual Passenger Trips in Millions)

- By Vehicle Type

- By Propulsion Type

- By Level of Autonomy

- By Application

- By Component

- By Capacity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Autonomous Shuttle Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Shuttles in Service and Annual Passenger Trips in Millions)

- By Vehicle Type

- By Propulsion Type

- By Level of Autonomy

- By Application

- By Component

- By Capacity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Autonomous Shuttle Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Shuttles in Service and Annual Passenger Trips in Millions)

- By Vehicle Type

- By Propulsion Type

- By Level of Autonomy

- By Application

- By Component

- By Capacity

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Perception, LiDAR, Radar, Camera & Multi-Sensor Fusion Technology Deep-Dive

- Autonomous Driving Software Stack, Localisation, Mapping & Path Planning Technology

- Vehicle-to-Everything (V2X), 5G Connectivity & Edge Computing Technology

- Battery Electric Propulsion, Charging Infrastructure & Hydrogen Fuel Cell Technology

- Remote Teleoperation, Fleet Monitoring & Predictive Maintenance Technology

- Machine Learning, Behaviour Prediction, Decision-Making Algorithm & Generative AI Technology

- Cybersecurity, Secure Software Updates & Functional Safety (ISO 26262, ISO 21448) Technology

- Patent & IP Landscape in Autonomous Shuttle Technologies

- Value Chain & Supply Chain Analysis

- LiDAR, Radar, Camera & Sensor Component Manufacturing Supply Chain

- Onboard Computing Platform, AI Processor & Automotive Semiconductor Supply Chain

- Autonomous Driving Software, High-Definition Map & AI Model Supply Chain

- Vehicle Chassis, Body Manufacturing & Final Assembly Supply Chain

- Battery, Charging Infrastructure, Hydrogen Refuelling & Electric Powertrain Supply Chain

- Fleet Operator, Mobility-as-a-Service Provider & Public Transit Agency Procurement Channel

- Aftermarket Service, Remote Teleoperation & Predictive Maintenance Provider Network

- Pricing Analysis

- Autonomous Shuttle Vehicle Capital Cost & Per-Unit Pricing Analysis Across Capacity Configurations

- Sensor Stack, Computing Platform & Software Pricing Analysis Across LiDAR, Radar, Camera & AI Compute

- Charging Infrastructure & Hydrogen Refuelling Infrastructure Capital and Operating Cost Analysis

- Fleet Operating Cost: Per Passenger-Kilometre, Per Vehicle-Day & Per Route Economics

- Subscription-Based & Mobility-as-a-Service Pricing Models for Autonomous Shuttle Deployment

- Total Cost of Ownership, Payback Period & Lifecycle Economics Analysis Across Use-Case Deployments

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Autonomous Shuttle Systems vs Conventional Bus, Private Vehicle & Alternative Transit Modes

- Zero-Emission Operation, Avoided Tailpipe Emissions & Net Climate Impact Contribution

- Battery Production, Recycling & Circular Economy Performance Across Autonomous Shuttle Fleets

- Urban Air Quality, Congestion Relief & Public Health Co-Benefits of Autonomous Shuttle Deployment

- Regulatory-Driven Sustainability, SDG 11 (Sustainable Cities) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Vehicle Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Vehicle Type, Application & Geography

- Player Classification

- Integrated Autonomous Shuttle Original Equipment Manufacturers (OEMs)

- Autonomous Driving Software & Perception Software Specialists

- LiDAR, Radar, Camera & Sensor Component Suppliers

- Mobility-as-a-Service Operators & Fleet Service Providers

- Remote Teleoperation & Fleet Monitoring Service Providers

- Battery, Charging Infrastructure & Hydrogen Refuelling Infrastructure Providers

- Public Transit Agencies, Municipal Authorities & PPP Operating Partners

- V2X Connectivity, Smart Infrastructure & 5G Network Technology Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Vehicle Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Autonomous Shuttle Products & Technology Portfolio

- Key Customer Relationships & Reference Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Autonomous Shuttle Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Vehicle Type, Application, Propulsion Type, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)