Market Definition

The Global Agricultural Equipment Market encompasses the design, engineering, manufacturing, distribution, sales, financing, and aftermarket service of powered and non-powered machinery, implements, and precision technology systems used across the complete agricultural production cycle for field crop cultivation, specialty and horticultural crop production, livestock farming, dairy operations, forestry, and post-harvest processing. Agricultural equipment spans a broad and technically diverse product spectrum from small hand-held and walk-behind implements serving smallholder subsistence farmers through medium-horsepower tractors serving developing country commercial agriculture to the largest high-horsepower row crop tractors, self-propelled combines, forage harvesters, and precision sprayers deployed across the large-scale grain production systems of North America, Europe, and South America. The market encompasses wheeled and tracked tractors across the full horsepower range from below 20 horsepower for garden tractors through 100 to 300 horsepower for mid-size field tractors to above 500 horsepower for large four-wheel-drive articulated row crop tractors, self-propelled combine harvesters and grain platforms, corn headers and specialty harvesting attachments, self-propelled and tractor-mounted sprayers, seeding and planting equipment including air seeders, precision planters, and row crop planters with variable-rate and individual row control capability, tillage equipment including primary tillage plows and secondary tillage cultivators, hay and forage equipment including mowers, tedders, rakes, and balers, loader tractors and telehandlers for materials handling, irrigation equipment, rice transplanters and harvesters, sugarcane harvesters, cotton pickers and strippers, and the precision agriculture technology layers including global navigation satellite system guidance, variable-rate technology controllers, yield monitors, machine telematics, and farm management information systems that are progressively transforming conventional agricultural equipment into connected, data-generating, and autonomy-capable platforms. Key participants include major global agricultural equipment original equipment manufacturers, regional and local machinery producers, precision agriculture technology companies, dealer and distribution networks, equipment financing providers, and the farming enterprises whose operational requirements and financial capacity define the demand structure of the global agricultural equipment market.

Market Insights

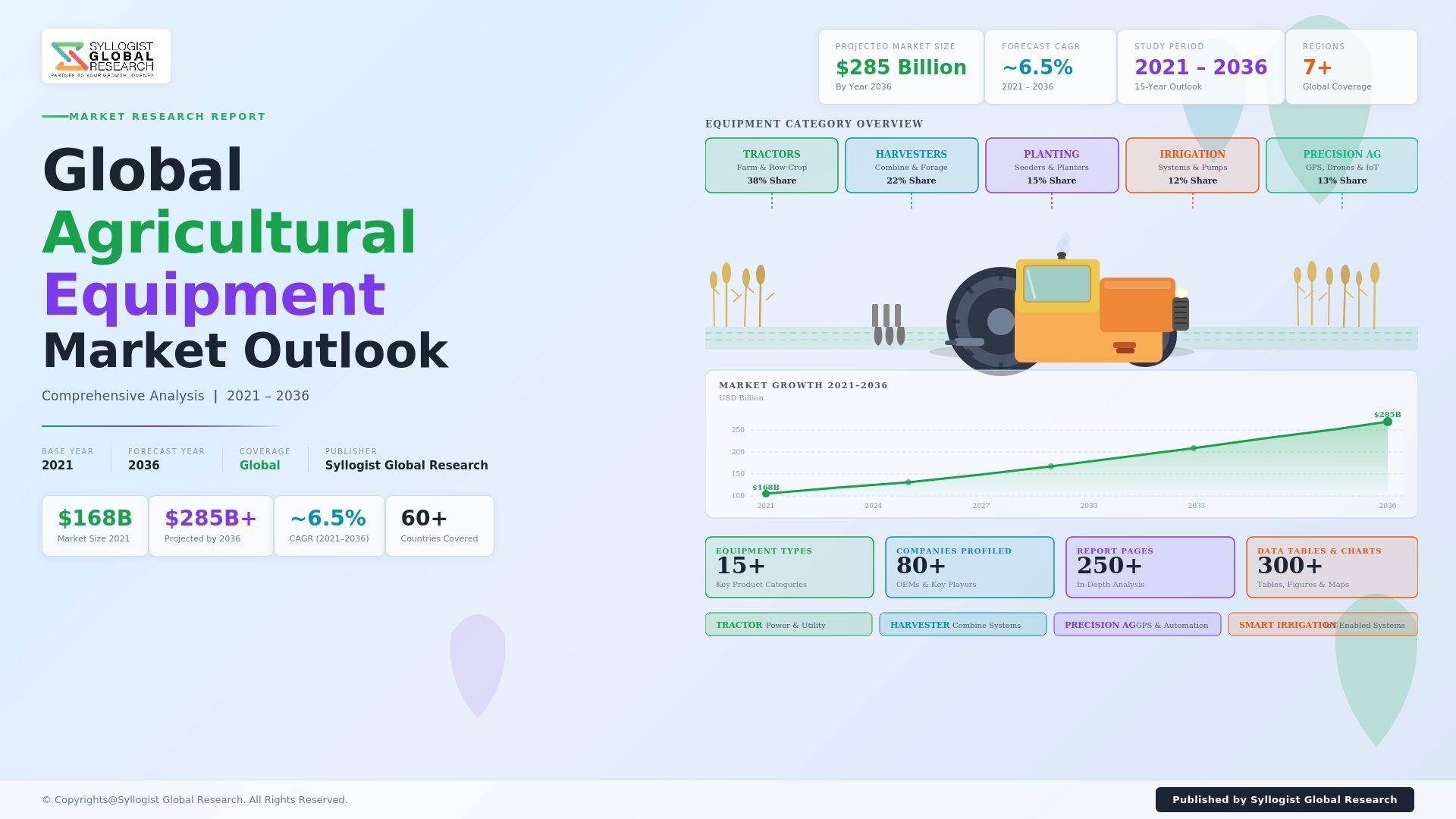

The global agricultural equipment market was valued at approximately USD 198.4 billion in 2025 and is projected to reach USD 328.6 billion by 2034, advancing at a compound annual growth rate of 5.8% over the forecast period from 2027 to 2034, driven by the fundamental requirement to increase global agricultural output by approximately 50% by 2050 to feed a projected 9.7 billion people on a diminishing per-capita arable land base, the accelerating mechanization of previously manual agricultural systems in India, Southeast Asia, Sub-Saharan Africa, and Latin America as rising rural wages make manual cultivation and harvest operations economically uncompetitive, the continued investment by established market farmers in precision agriculture-equipped replacement machinery that delivers lower input costs and higher yield precision, and the growing deployment of electrification, digital connectivity, and autonomous operation capabilities that are increasing the unit value of new agricultural equipment across all major product categories. The global tractor market, representing the foundational powered implement for worldwide agricultural mechanization, shipped approximately 2.84 million units in 2025 across all horsepower categories and global markets, with India representing the world’s largest single-country tractor market by unit volume at approximately 950,000 tractors annually, followed by China at approximately 420,000 units, the United States at approximately 210,000 units, and Europe at approximately 180,000 units, reflecting the structural dominance of smallholder and medium-scale commercial farming volumes over the high-horsepower precision technology-equipped large farm equipment markets that dominate by revenue contribution. The combine harvester segment reached approximately USD 14.8 billion in global market value in 2025, concentrated heavily in North America, Europe, and the expanding South American soybean and corn production belt where large field scales, high grain volumes, and competitive harvest window requirements create the strongest economic case for large self-propelled combines whose operational productivity exceeds manual or small machine alternatives by factors of fifty to one hundred times per working hour.

The precision agriculture technology integration within conventional agricultural equipment is the most commercially and strategically significant trend transforming the global agricultural equipment market’s revenue structure, as global navigation satellite system guidance, variable-rate application systems, yield mapping, machine telematics, and connectivity to farm management information platforms progressively shift from optional premium features to standard technology on replacement equipment purchases by commercial-scale farmers in developed markets, simultaneously increasing the per-unit average selling price of agricultural equipment at all horsepower classes and creating a growing data and software recurring revenue stream that is fundamentally altering the business model of major agricultural equipment manufacturers toward a services and technology company orientation alongside their traditional hardware manufacturing identity. John Deere’s Operations Center farm management platform, which aggregates telematics, yield data, application records, and field imagery from its equipment fleet, had approximately 400 million connected acres under management as of 2025, generating subscription and data analytics revenue and creating a proprietary agronomic intelligence ecosystem that increases customer switching costs and supports premium pricing for equipment incorporating Operations Center connectivity. CNH Industrial’s PLM Intelligence system and AGCO’s Fuse Technologies platform represent equivalent competitive responses to the precision agriculture data platform opportunity, with all three major manufacturers investing approximately USD 600 million to USD 1.2 billion annually each in precision agriculture research and development to advance automation, autonomy, and connectivity capabilities that differentiate their premium product lines and justify replacement cycle acceleration among farmers who recognize the operational and yield management benefits of the most current technology generations. The average selling price of a large row crop tractor exceeding 300 horsepower in the United States has increased from approximately USD 185,000 in 2015 to approximately USD 310,000 in 2025, driven predominantly by precision agriculture technology content addition including autonomous guidance, variable-rate section control, machine learning crop monitoring, and integrated digital farm management connectivity rather than changes in underlying mechanical drivetrain specifications.

Asia-Pacific, driven by the mechanization transformation of Indian, Chinese, Southeast Asian, and Australian agriculture, represents both the highest-volume regional market and the highest-growth commercial opportunity within the global agricultural equipment landscape, with India’s tractor market alone generating approximately USD 8.4 billion in equipment sales in 2025 and supporting an extensive domestic manufacturing industry including Mahindra and Mahindra, Escorts Kubota, TAFE, Sonalika International, Force Motors, and VST Tillers that collectively produce approximately 85% of the tractors sold in India from domestically manufactured components. The rapid mechanization of rice transplanting, harvesting, and threshing operations across the lowland rice production systems of India, Bangladesh, Vietnam, Thailand, and Indonesia is generating strong and growing demand for compact walk-behind rice transplanters, self-propelled paddy harvesters, and mini combine harvesters at price points of USD 3,000 to USD 15,000 that are accessible to smallholder farmers with the support of government mechanization subsidy programs, agriculture credit schemes, and custom hiring center models that enable shared access to mechanized equipment by multiple small-farm operators. The Chinese agricultural equipment market, while slowing from the exceptional mechanization investment decade of 2010 to 2020, continues to generate substantial demand for corn harvesters, wheat combines, cotton pickers, and large-horsepower tractors as the structural consolidation of Chinese agriculture toward larger operational units through land rental aggregation by commercial farm operators drives investment in higher-productivity equipment that improves competitiveness against imported food commodities, with Chinese agricultural equipment exports also growing at approximately 18.4% annually in 2025 as domestically competitive manufacturers including Yto Group, Lovol, ZOOMLION, and XCMG Agricultural Machinery target Southeast Asian, African, and Central Asian export markets with competitively priced equipment suited to smallholder and medium-scale commercial farming applications.

The electrification of agricultural equipment represents the most structurally significant technology transition underway in the industry, with major manufacturers introducing battery-electric and hydrogen fuel cell-powered tractor concepts and early commercial products that are attracting increasing farmer interest driven by fuel cost savings, reduced noise and vibration in livestock proximity operations, and the potential for zero-emission agricultural practices demanded by sustainability certification schemes and corporate food supply chain commitments, while simultaneously confronting the fundamental operational challenge that large agricultural tractors performing energy-intensive tillage and harvesting tasks cannot be powered by current battery technology at commercially viable costs, weights, and field-time durations without battery packs whose mass and charging logistics create practical limitations that the most demanding field applications cannot accommodate within currently available energy storage technology. John Deere’s 5R electric tractor demonstrator, Fendt’s e100 Vario fully electric compact tractor, and the Monarch MK-V autonomous electric tractor represent early commercial electric agricultural equipment introductions whose operational performance data is defining the battery-powered use case boundaries within lower-horsepower, lower-energy-intensity applications including vineyard and orchard operations, greenhouse tasks, and livestock farm utility work where shorter operating cycles and lower peak power requirements create the most favorable conditions for battery electric tractors at current energy density and charging infrastructure development levels. The aftermarket and parts segment of the global agricultural equipment market represents approximately USD 62.4 billion annually, accounting for approximately 31.4% of total market revenue and providing original equipment manufacturers and independent aftermarket parts suppliers with recurring revenue streams that are less cyclical than new equipment sales and whose scale reflects the twenty-to-thirty-year operational lifetimes of agricultural equipment whose mechanical reliability and parts availability are critical to farm operational continuity across the complete equipment lifecycle.

Key Drivers

Rapid Agricultural Mechanization in India, Southeast Asia, and Sub-Saharan Africa Driven by Rising Rural Wages, Government Mechanization Programs, and Custom Hiring Center Models

The structural transformation of agricultural production systems across emerging and developing economies from predominantly manual to mechanized operations is generating the most significant volume growth opportunity in the global agricultural equipment market, as rising rural wages driven by expanding urban employment alternatives make hand cultivation, manual transplanting, and manual harvest operations economically uncompetitive against mechanized alternatives even at equipment price points that require financing support and government subsidy to become accessible to smallholder farm operators. India’s National Mission on Agricultural Mechanization, which provides capital subsidies of 40% to 50% of equipment purchase cost for small and marginal farmers through state agricultural departments and allocates dedicated funding for custom hiring center establishment, has directly stimulated tractor, power tiller, harvester, and irrigation pump procurement at volumes that are sustaining above-market-average growth in the Indian agricultural equipment market at approximately 8.4% annually even through commodity price cycle fluctuations that typically suppress equipment investment in mature markets. The custom hiring center model, which operates a centralized pool of agricultural equipment available to multiple farmers on a pay-per-use basis without requiring individual ownership, has emerged as the most commercially scalable pathway for equipment adoption among land-fragmented smallholder farming communities in India, Bangladesh, Indonesia, Vietnam, and multiple African nations where the per-farmer land holding is insufficient to justify individual equipment ownership but the aggregate area served by a custom hiring center provides the utilization basis for equipment economics, with India’s custom hiring center network exceeding 68,000 centers in 2025 and the government targeting 50,000 additional centers through subsidy programs through 2027.

Precision Agriculture Adoption, Equipment Technology Upgrade Cycle Acceleration, and Average Selling Price Expansion Driven by Digital and Automation Capability Integration

The progressive integration of precision agriculture technologies including global navigation satellite system guidance, variable-rate seed and fertilizer application, machine learning crop monitoring, yield mapping, and autonomous field operation capabilities into standard production agricultural equipment is generating a technology upgrade cycle that accelerates replacement frequency among commercial-scale farmers seeking competitive productivity and input efficiency advantages, while simultaneously expanding the average selling price per unit of new equipment through technology content addition that is increasing manufacturer revenue at rates that exceed volume growth and improve the financial characteristics of the agricultural equipment industry toward a higher-margin, recurring-revenue business model with structural similarities to technology hardware and software companies. The economic justification for precision agriculture technology adoption is directly quantifiable through input savings of approximately USD 15 to USD 35 per acre from variable-rate fertilizer application, approximately USD 8 to USD 18 per acre from precision seed rate optimization, and yield improvement of approximately 3% to 7% from machine learning crop monitoring and agronomic prescription services that collectively generate a return on precision technology investment of approximately 120% to 180% annually over the cost of precision agriculture technology packages at typical commercial grain farm scales above 2,000 acres, creating a financially compelling case for technology upgrade that is independent of equipment age and mechanical condition and that sustains a replacement demand stream even when farm income conditions would otherwise support equipment life extension. Global navigation satellite system guidance adoption in new tractor sales has reached approximately 78% penetration in North American and European markets and approximately 42% in South American row crop production markets, with the incremental integration of section control, variable-rate application, and telematics connectivity at each subsequent technology adoption wave progressively increasing average transaction value per equipment sale.

Food Security Imperative, Global Crop Production Intensification Requirements, and Arable Land Constraint Driving Sustained Long-Term Investment in Productivity-Enhancing Agricultural Equipment

The fundamental demographic and agricultural resource challenge of producing approximately 50% more food by 2050 from an arable land base that is contracting due to urbanization, soil degradation, water stress, and climate change impacts is creating a multi-decade structural investment imperative in agricultural productivity enhancement that is the most durable and economically grounded demand driver for globally applicable agricultural equipment, as yield improvement per hectare through better mechanization, more precise input application, and more timely field operations is the primary agronomically proven pathway for expanding production capacity on limited land. The global grain storage and post-harvest loss challenge, in which approximately 14% of food production is estimated to be lost between harvest and retail in developing countries due to inadequate harvesting equipment, drying infrastructure, and storage facilities, represents a direct agricultural productivity improvement opportunity whose resolution through mechanized harvest, on-farm drying, and storage equipment investment would effectively increase food availability without additional land or input consumption, creating a compelling food security rationale for equipment investment in markets including Sub-Saharan Africa, South Asia, and Southeast Asia that is supported by multilateral development bank financing, government agricultural development programs, and private sector supply chain investment. Commodity grain price cycles that create periodic surges in farm income and equipment replacement investment capacity, as demonstrated during the 2020 to 2022 agricultural commodity price elevation that drove exceptional North American and European equipment demand and contributed to industry-wide order backlogs exceeding twelve months at major manufacturers, provide cyclical amplification of the structural demand trend whose long-term direction is unambiguously positive as global protein consumption growth in the rising middle class of Asia, Africa, and Latin America sustains elevated demand for grain crops and the equipment required to produce them.

Key Challenges

Agricultural Commodity Price Cyclicality, Farm Income Volatility, and Equipment Affordability Constraints Creating Boom-Bust Investment Cycles That Complicate Manufacturer Capacity Planning

The global agricultural equipment market is structurally exposed to the commodity price cycles of the agricultural sector whose farm income volatility creates pronounced boom and bust equipment investment cycles that require manufacturers to manage capacity, inventory, and workforce planning across swings in annual sales volume of 20% to 40% within single market cycles, as illustrated by the combination of COVID-19 pandemic supply chain disruption and the 2021 to 2022 agricultural commodity price surge that generated large order backlogs and production capacity constraints at John Deere, CNH Industrial, AGCO, and Kubota simultaneously followed by demand normalization in 2023 and 2024 as commodity prices moderated and farmers delayed purchases. Large row crop combine harvesters priced at approximately USD 600,000 to USD 850,000 in the United States represent the most capital-intensive and demand-volatile equipment category, with annual shipment volumes fluctuating by 25% to 45% across commodity price cycles as grain farmers time replacement decisions to align with farm income availability and tax planning considerations rather than mechanical necessity, creating inventory management challenges for dealers and production scheduling uncertainty for manufacturers whose long lead time supply chains require capacity commitments twelve to eighteen months before delivery. The affordability challenge is particularly acute in the transition from developing to commercial-scale mechanized agriculture in markets including India, Africa, and Southeast Asia where the income of smallholder farmers is insufficient to support financing of equipment at prices reflecting the material, manufacturing, and technology costs of modern agricultural equipment without government subsidy, financing concessions, or value engineering for cost reduction that can compromise the durability and performance characteristics of equipment deployed in challenging field conditions and after-sales service networks that may be inadequate for complex machinery maintenance.

Supply Chain Complexity, Steel and Component Cost Inflation, and Semiconductor Availability Constraints Increasing Manufacturing Cost and Delivery Lead Times for Agricultural Equipment

Agricultural equipment manufacturers operate complex global supply chains integrating steel forgings, castings, and stampings from specialized material suppliers, hydraulic components, transmissions, and axle assemblies from tier-one suppliers, diesel and alternative powertrain systems from engine manufacturers, and increasingly large volumes of electronics, sensors, and microcontrollers for precision agriculture technology systems, with the simultaneous cost inflation and availability disruption across multiple supply chain categories that characterized the 2021 to 2023 period generating input cost increases of approximately 18% to 28% per machine that manufacturers could only partially recover through selling price increases, compressing margins and contributing to dealer inventory normalization challenges as end-market demand moderated faster than supply chain adjustments could reduce production output. Steel and cast iron components, which represent approximately 55% to 65% of the material bill of materials for large agricultural equipment including tractors, combines, and sprayers, are subject to steel price volatility that directly impacts manufacturing cost, with hot-rolled coil steel prices fluctuating from approximately USD 500 per metric ton in 2020 to approximately USD 1,900 per metric ton at the 2021 peak and returning to approximately USD 780 per metric ton in 2025, generating margin management challenges and procurement strategy complexity for manufacturers whose long-term supply contracts, vertical integration decisions, and hedging capabilities determine their relative competitiveness through commodity cycle. The semiconductor and electronics component availability constraints that affected virtually all manufacturing industries from 2021 to 2023 had a particularly severe impact on precision agriculture technology-equipped equipment models whose advanced guidance, variable-rate control, and telematics systems contain hundreds of electronic components from specialized manufacturers whose capacity constraints delayed equipment delivery at precisely the period of peak farm demand, with some premium equipment configurations experiencing delivery delays of six to eighteen months that contributed to dealer customer satisfaction challenges and potentially accelerated purchases of competing brands with shorter lead times.

Electrification Technical Limitations, Charging Infrastructure Gaps, and Energy Density Constraints Impeding Battery-Powered Agricultural Equipment Adoption at Commercial Farm Scale

The agricultural equipment industry’s energy transition toward battery electric and alternative fuel powertrains faces fundamental technical and infrastructure challenges that are more severe than in other vehicle sectors due to the extremely high energy consumption of agricultural field operations including primary tillage, deep ripping, and high-draft soil preparation that require sustained peak power outputs of 200 to 500 kilowatts for operating periods of eight to twelve continuous hours per day across multi-week seasonal work windows, energy requirements that would necessitate battery packs of 600 to 1,200 kilowatt-hours in large tractors performing these tasks, with corresponding pack weights of 4,000 to 8,000 kilograms at current lithium-ion energy density that would impose excessive ballast on farm field soil compaction, exceed the gross vehicle weight of road-legal transport configurations, and require charging times of four to eight hours per operating day that create critical bottlenecks in seasonal field work scheduling where daylight hours and favorable weather windows determine total seasonal output. The rural location of agricultural operations presents a severe charging infrastructure challenge, as the multi-megawatt grid connections required to fast-charge a fleet of large battery electric tractors within operationally viable timeframes are unavailable at the majority of farm locations globally without substantial electrical grid reinforcement investment whose cost of USD 250,000 to USD 1.5 million per farm for distribution transformer upgrades and medium-voltage grid connections must be justified against the operational benefits of equipment electrification, a cost burden that falls on individual farm operators rather than being socialized across the charging network ecosystem as in urban electric vehicle charging infrastructure deployment. Alternative hydrogen fuel cell propulsion is attracting investment from manufacturers including New Holland, Kubota, and CNH Industrial for high-power agricultural tractor applications, but green hydrogen availability, storage infrastructure, and dispensing equipment at farm locations represent supply chain development requirements whose realization timeline extends beyond the near-term equipment replacement decisions of commercial farmers currently evaluating alternative powertrain equipment options.

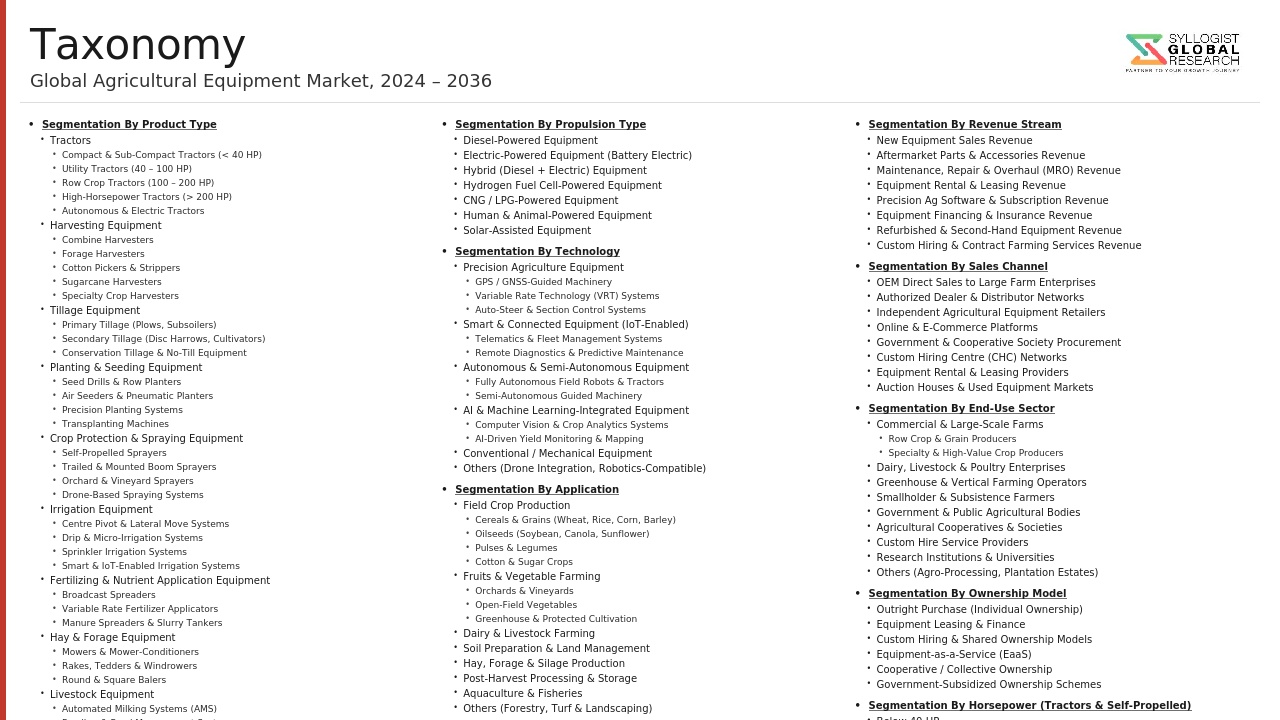

Market Segmentation

- Segmentation By Equipment Type

- Tractors (Sub-Compact, Compact, Utility, and High-Horsepower Row Crop)

- Combine Harvesters and Grain Platforms

- Self-Propelled Sprayers and Boom Sprayers

- Seeding and Planting Equipment (Planters, Air Seeders, and Drills)

- Tillage Equipment (Primary and Secondary Tillage)

- Hay and Forage Equipment (Mowers, Balers, and Forage Harvesters)

- Specialty Crop Harvesters (Cotton, Sugarcane, and Vegetables)

- Rice Transplanters and Paddy Harvesters

- Loader Tractors and Telehandlers

- Irrigation Equipment

- Precision Agriculture Technology Systems

- Others

- Segmentation By Power Source

- Diesel-Powered Equipment

- Battery Electric Agricultural Equipment

- Hydrogen Fuel Cell Agricultural Equipment

- Hybrid and Alternative Fuel Equipment

- Non-Motorized and Animal Draft Equipment

- Others

- Segmentation By Horsepower (Tractors)

- Below 40 HP (Compact and Sub-Compact Tractors)

- 41 to 100 HP (Utility Tractors)

- 101 to 200 HP (Mid-Range Field Tractors)

- 201 to 350 HP (High-Horsepower Row Crop Tractors)

- Above 350 HP (Large Four-Wheel-Drive Articulated Tractors)

- Segmentation By Application

- Arable and Grain Crop Production

- Specialty and Horticultural Crop Production

- Dairy and Livestock Farming

- Rice and Paddy Production

- Sugarcane and Tropical Crop Production

- Orchard and Vineyard Management

- Precision Agriculture and Data Management

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer Dealer Networks

- Independent Equipment Dealers and Distributors

- Custom Hiring Centers and Equipment Rental

- Direct Online and Digital Sales Platforms

- Government Procurement and Subsidy Channels

- Others

- Segmentation By Farm Size

- Smallholder Farms (Below 5 Hectares)

- Small to Medium Farms (5 to 100 Hectares)

- Large Commercial Farms (100 to 1,000 Hectares)

- Very Large and Corporate Farms (Above 1,000 Hectares)

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Agricultural Equipment Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by equipment type including tractors by horsepower category, combine harvesters, self-propelled sprayers, seeding and planting equipment, tillage equipment, specialty harvesters, and precision agriculture technology systems, by application including arable crop production, specialty and horticultural crops, dairy and livestock, rice paddy production, and sugarcane, and by region including North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa, to enable equipment manufacturers, dealer networks, precision agriculture technology companies, equipment financing providers, and institutional investors to identify the highest-growth equipment categories, application segments, and geographic markets generating the most commercially durable demand trajectories across the forecast period to 2034?

- What is the current penetration rate, average selling price impact, return on investment evidence base for farmers, and competitive differentiation importance of precision agriculture technology content including GNSS guidance, variable-rate application, machine telematics, yield mapping, and farm management information platform connectivity within new equipment sales across North American, European, and South American commercial grain farm markets, and how are the precision agriculture data platform strategies of major manufacturers including John Deere Operations Center, CNH Industrial PLM Intelligence, and AGCO Fuse Technologies creating data-driven customer retention advantages, subscription revenue streams, and artificial intelligence-enhanced agronomic service capabilities that are transforming the competitive differentiation basis of premium agricultural equipment from mechanical performance toward integrated digital intelligence that is progressively more difficult for smaller manufacturers and new market entrants to replicate?

- What is the size, growth trajectory, manufacturer competitive landscape, government subsidy program structure, financing scheme availability, custom hiring center penetration, and product technology level of the Indian tractor and agricultural equipment market, which is the world’s largest tractor market by volume at approximately 950,000 units annually, and how are domestic manufacturers including Mahindra and Mahindra, TAFE, Escorts Kubota, Sonalika, and Force Motors competing with international manufacturers including John Deere, CNH Industrial, Kubota, AGCO, and Claas for market share across the sub-40 horsepower, 41 to 100 horsepower, and above 100 horsepower tractor segments, and what is the outlook for Indian tractor market volume growth and average selling price expansion as farm mechanization depth increases and precision agriculture adoption among larger Indian commercial farmers creates demand for higher-specification and higher-value equipment through 2034?

- What are the technical performance benchmarks, energy storage capacity requirements, field operating time limitations, charging infrastructure challenges, soil compaction implications of battery pack weight, and commercial viability assessment for battery electric tractors and agricultural equipment at different horsepower classes and field application types, and how are the electrification programs of John Deere, CNH Industrial with New Holland, AGCO, Kubota, and startup electric agricultural equipment companies advancing toward commercial product launches and early adopter farm deployments, and what farm types, crop systems, operating environments, and horsepower ranges offer the most commercially viable near-term applications for battery electric agricultural equipment where the combination of energy requirements, daily operating duration, and infrastructure availability makes electrification economically competitive with conventional diesel alternatives?

- How are Chinese agricultural equipment manufacturers including YTO Group, Lovol, ZOOMLION, and XCMG Agricultural Machinery expanding their export market presence across Southeast Asia, Sub-Saharan Africa, Central Asia, and Latin America through competitive pricing strategies, government-to-government agricultural development financing programs, and product localization for smallholder and medium-scale commercial farming applications, and what competitive threat does the expansion of Chinese agricultural equipment exports at approximately 18.4% annual growth represent for established Western and Japanese agricultural equipment manufacturers in these developing country growth markets, and how are John Deere, CNH Industrial, AGCO, Kubota, and regional manufacturers responding through product line localization, financing facilitation, and dealer network development in markets where Chinese equipment is gaining share?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Agricultural Commodity Price Cyclicality & Farm Income Volatility Risk Impacting Equipment Demand

- Steel, Cast Iron, Hydraulic Fluid & Key Component Supply Chain Price Volatility & Availability Risk

- Geopolitical, Trade Tariff & Agricultural Equipment Export-Import Policy Risk

- Technology Transition Risk: OEM Investment in Electrification & Precision Agriculture vs. Conventional Equipment Revenue Base

- Climate Change, Erratic Monsoon & Adverse Weather Event Risk on Seasonal Equipment Demand in Key Agricultural Markets

- Regulatory Framework & Standards

- Emission Standards for Agricultural Equipment Engines: US EPA Tier 4 Final, EU Stage V, India CEV Stage V, China Nonroad Mobile Machinery (NRMM) Standards & Global Harmonisation

- Agricultural Equipment Safety Standards: ISO 11684 (Safety Signs), ISO 4254 Series (Agricultural Machinery Safety), OSHA Farmworker Safety Regulations & National Farm Machinery Testing Standards

- Farm Mechanisation Policy & Subsidy Frameworks: India Sub-Mission on Agricultural Mechanisation (SMAM), US USDA Conservation Reserve Programme, EU CAP Machinery Modernisation Grant & China Agricultural Machinery Purchase Subsidy

- Custom Hiring Centre (CHC), Cooperative & Government Farm Mechanisation Programme Regulation & Farmer Producer Organisation (FPO) Equipment Access Policy

- Precision Agriculture, GPS Guidance & Autonomous Equipment Regulation: FCC Spectrum Allocation, EU Autonomous Machinery Framework, GNSS Interference Standards & OTA Software Update Homologation Requirements

- Global Agricultural Equipment Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Sold)

- Market Size & Forecast by Equipment Type

- Tractors

- 2WD Tractor (Standard & Utility)

- 4WD & MFWD (Mechanical Front Wheel Drive) Tractor

- Compact & Sub-Compact Tractor (Below 40 HP)

- High-Horsepower Tractor (Above 100 HP: Row Crop, Articulated & Tracked)

- Mini Tractor & Power Tiller (Below 25 HP)

- Harvesting Equipment

- Combine Harvester (Self-Propelled & Track-Type)

- Rice Harvester & Paddy Reaper-Binder

- Sugarcane Harvester

- Forage Harvester & Maize Header

- Vegetable, Potato & Root Crop Harvester

- Tillage & Soil Preparation Equipment

- Mouldboard Plough, Disc Plough & Reversible Plough

- Rotavator, Rotary Tiller & Disc Harrow

- Cultivator, Chisel Plough & Subsoiler

- Planting & Seeding Equipment

- Seed Drill & Zero-Till Ferti-Seed Drill

- Rice Transplanter & Vegetable Transplanter

- Precision Planter (Maize, Soybean, Cotton & Sunflower)

- Irrigation Equipment

- Drip Irrigation & Micro-Sprinkler System

- Sprinkler & Centre Pivot Irrigation System

- Pump Set, Water Lifting & Pipeline Distribution

- Crop Protection & Spraying Equipment

- Tractor-Mounted & Trailed Boom Sprayer

- Self-Propelled High-Clearance Sprayer

- Knapsack, Backpack & Manual Sprayer

- Hay, Forage & Livestock Equipment

- Round & Square Baler

- Mower, Conditioner, Tedder & Rake

- Post-Harvest, Threshing & Storage Equipment

- Multi-Crop Thresher & Sheller

- Grain Dryer & Post-Harvest Processing Equipment

- Fertiliser Spreader, Loader, Baler Wrapper & Other Implements

- Market Size & Forecast by Power Source

- Diesel Engine (Conventional & Tier 4/Stage V Compliant)

- Battery Electric & Hybrid Electric Powertrain

- CNG & Alternative Fuel Engine

- PTO-Powered Tractor-Driven Implement

- Manual, Pedal-Operated & Animal-Drawn Equipment

- Market Size & Forecast by Horsepower Category

- Below 30 HP (Mini & Sub-Compact)

- 30 HP to 60 HP (Utility & Standard Tractor)

- 60 HP to 100 HP (Medium & Semi-High Tractor)

- Above 100 HP (High-Horsepower, Articulated & Tracked Tractor)

- Market Size & Forecast by Technology Level

- Conventional Mechanical Equipment

- Semi-Mechanised & Power-Assisted Equipment

- Precision Agriculture-Enabled Equipment (GPS, GNSS & Variable Rate Technology)

- Smart, Connected & Autonomous Equipment (AI, IoT, Auto-Steer & Telematics)

- Market Size & Forecast by Application

- Field Crop Production (Wheat, Corn, Rice, Soybean, Cotton & Oilseed)

- Horticulture & Specialty Crop (Fruit, Vegetable, Vineyard & Sugarcane)

- Livestock, Dairy & Animal Husbandry

- Paddy & Wet Field Cultivation

- Dryland & Rain-Fed Agriculture

- Market Size & Forecast by Farm Size

- Large Commercial Farm (Above 50 Hectares)

- Medium Farm (10 to 50 Hectares)

- Small & Marginal Farm (Below 10 Hectares)

- Market Size & Forecast by End-User

- Commercial & Corporate Farming Enterprise

- Individual Farmer & Family Farm Owner

- Agricultural Cooperative, Farmer Producer Organisation (FPO) & SHG

- Custom Hiring Centre (CHC), Farm Machinery Bank & Rental Service Provider

- Government, Public Sector Farm & Agricultural Research Institution

- Market Size & Forecast by Sales Channel

- OEM Direct Sale & Authorised Dealer Network

- Cooperative, Government Procurement & Subsidy-Linked Purchase

- Custom Hiring, Rental & Equipment Leasing Channel

- Online Platform, E-Commerce & Digital Agri Marketplace

- North America Agricultural Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Equipment Type

- By Power Source

- By Horsepower Category

- By Technology Level

- By Application

- By Farm Size

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Agricultural Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Equipment Type

- By Power Source

- By Horsepower Category

- By Technology Level

- By Application

- By Farm Size

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Agricultural Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Equipment Type

- By Power Source

- By Horsepower Category

- By Technology Level

- By Application

- By Farm Size

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Agricultural Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Equipment Type

- By Power Source

- By Horsepower Category

- By Technology Level

- By Application

- By Farm Size

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Agricultural Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Equipment Type

- By Power Source

- By Horsepower Category

- By Technology Level

- By Application

- By Farm Size

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Agricultural Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Equipment Type

- By Power Source

- By Horsepower Category

- By Technology Level

- By Application

- By Farm Size

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Italy, Poland, Netherlands, Russia, Ukraine, China, India, Japan, South Korea, Australia, Brazil, Argentina, Mexico, Turkey, South Africa, Indonesia, Thailand, Pakistan

- Technology Landscape & Innovation Analysis

- Tractor Engine, Transmission, Hydraulics & Powertrain Technology Deep-Dive

- Combine Harvester Threshing, Separation, Cleaning System & Grain Quality Monitoring Technology

- Precision Agriculture: GPS/GNSS Auto-Steer, Variable Rate Application (VRA), Section Control & Yield Mapping Technology

- Electric & Hybrid Agricultural Equipment Technology: Battery Tractor, Electric Implement & On-Board Energy Management

- Precision Planting & Seeding Technology: Individual Row Control, Electric Drive Seed Meter, Down-Force Control & Seed Singulation

- Irrigation Technology: Drip, Micro-Sprinkler, Centre Pivot Lateral Move, Soil Moisture Sensor & Cloud Irrigation Scheduling

- Telematics, Fleet Management, Remote Diagnostics, OTA Update & Farm Equipment Digital Platform Technology

- Patent & IP Landscape in Agricultural Equipment Technologies

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain: Steel, Cast Iron, Aluminium, Hydraulic Component & Engine Parts Manufacturer Landscape

- Engine, Transmission, Axle & Drivetrain Component Supplier Landscape

- Electronics, Sensor, Display, GNSS & Precision Agriculture Component Supply Chain

- OEM Assembly, Sub-Assembly & Tier-1 Agricultural Equipment Manufacturer Landscape

- Authorised Dealer, Distributor & National Import Agent Network

- End Farmer, Custom Hiring Centre, Government Programme & Cooperative Procurement Channel

- Aftermarket, Spare Parts, Service Network, Overhaul & Equipment Refurbishment

- Pricing Analysis

- Tractor Average Selling Price (ASP) Analysis by Horsepower Segment, 2WD vs. 4WD & Technology Level

- Combine Harvester Pricing Analysis by Header Width, Grain Tank Capacity & Throughput

- Precision Agriculture System Add-On Price Analysis: GPS Auto-Steer, VRA Controller & Yield Monitor Cost per Unit

- Electric Tractor Price Premium vs. Conventional Diesel Tractor: TCO & Payback Period Analysis

- Irrigation Equipment Capital Cost Analysis: Drip, Sprinkler & Centre Pivot per Hectare Installed Cost Benchmarking

- OEM Annual Price Movement, Input Cost Pass-Through & Dealer Margin Structure Analysis by Region

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Agricultural Equipment: Carbon Footprint of Tractor & Combine Manufacture, Operation & End-of-Life Across Key Markets

- Engine Emission Reduction: Tier 4 Final, EU Stage V & India CEV V Compliance Impact on Diesel Particulate, NOx & Carbon Monoxide Emission from Farm Equipment

- Precision Agriculture Sustainability Co-Benefit: Input Reduction (Fertiliser, Pesticide & Water) Through Site-Specific Management & Variable Rate Technology

- Electric & Alternative Fuel Agricultural Equipment: GHG Reduction Potential, Renewable Energy Charging & Net Zero Farm Operation Roadmap

- Circular Economy in Agricultural Equipment: Tractor & Combine Remanufacturing, Component Refurbishment, End-of-Life Steel Recovery & OEM Extended Producer Responsibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Equipment Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Equipment Type, Horsepower Segment & Geography

- Player Classification

- Global Full-Line Agricultural Equipment OEM (Tractor, Combine, Planter & Tillage)

- Specialist Tractor Manufacturer (Sub-Compact, Compact & Utility Tractor)

- Specialist Harvesting Equipment Manufacturer (Combine, Rice & Sugarcane Harvester)

- Precision Agriculture, GPS Guidance & Digital Farming System Provider

- Irrigation Equipment Manufacturer (Drip, Sprinkler & Centre Pivot)

- India & South Asia Domestic Tractor Manufacturer (Mahindra, Escorts Kubota, TAFE, Sonalika)

- China & Asia Domestic Agricultural Equipment Manufacturer

- Aftermarket Parts, Remanufacturing & Independent Service Provider

- Competitive Analysis Frameworks

- Market Share Analysis by Equipment Type, Horsepower Category & Region

- Company Profile

- Company Overview & Headquarters

- Agricultural Equipment Products & Technology Portfolio

- Key Customer Relationships & OEM Dealer Network

- Manufacturing Footprint & Annual Production Capacity (Units)

- Revenue (Agricultural Equipment Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (New Product Launches, Capacity Expansion, Market Entry)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Equipment Type, Power Source, Technology Level, Farm Size & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & Dealer Network Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)