Market Definition

The Global Agricultural Sprayers Market encompasses the design, manufacturing, distribution, and servicing of mechanical and electrostatic equipment systems used to apply liquid agrochemicals including herbicides, fungicides, insecticides, foliar fertilizers, plant growth regulators, and biological crop protection agents onto field crops, orchard and vineyard crops, greenhouse production systems, and turf and landscaping areas across smallholder, commercial, and large-scale industrial agricultural production environments worldwide. Agricultural sprayers are purpose-engineered delivery systems that convert liquid formulations into droplet spectra precisely calibrated to achieve optimal canopy coverage, agrochemical deposit retention, biological efficacy, and drift minimization outcomes across the full range of crop architectures, field topographies, and operational conditions encountered in global crop production.

The market encompasses knapsack and backpack sprayers used by smallholder farmers for manual field application; wheel-mounted and tractor-trailed boom sprayers serving medium and large-scale arable crop production; self-propelled high-clearance sprayers deployed across extensive row crop production systems in North America, South America, and Australia; orchard and vineyard air-blast and tunnel sprayers designed for three-dimensional canopy penetration in perennial specialty crop production; unmanned aerial vehicle sprayers providing aerial application capability for large field areas and difficult terrain; and electrostatic and precision application system technologies enabling targeted, reduced-volume agrochemical delivery. The market further encompasses sprayer precision application technology components including GPS-guided boom section control systems, variable rate application controllers, individual nozzle control systems, flow meters and pressure sensors, and AI-powered weed detection and spot spraying systems that are progressively transforming sprayer platforms from uniform broadcast application equipment into precision, spatially differentiated agrochemical delivery systems. Key participants include global agricultural machinery manufacturers, specialized sprayer engineering companies, precision agriculture technology providers integrating sensing and control systems into sprayer platforms, agrochemical companies influencing application technology adoption through agronomic recommendation programs, and the global distribution and dealer networks through which sprayer equipment reaches farmer end users across diverse agricultural markets spanning North America, Europe, South America, Asia-Pacific, and Africa.

Market Insights

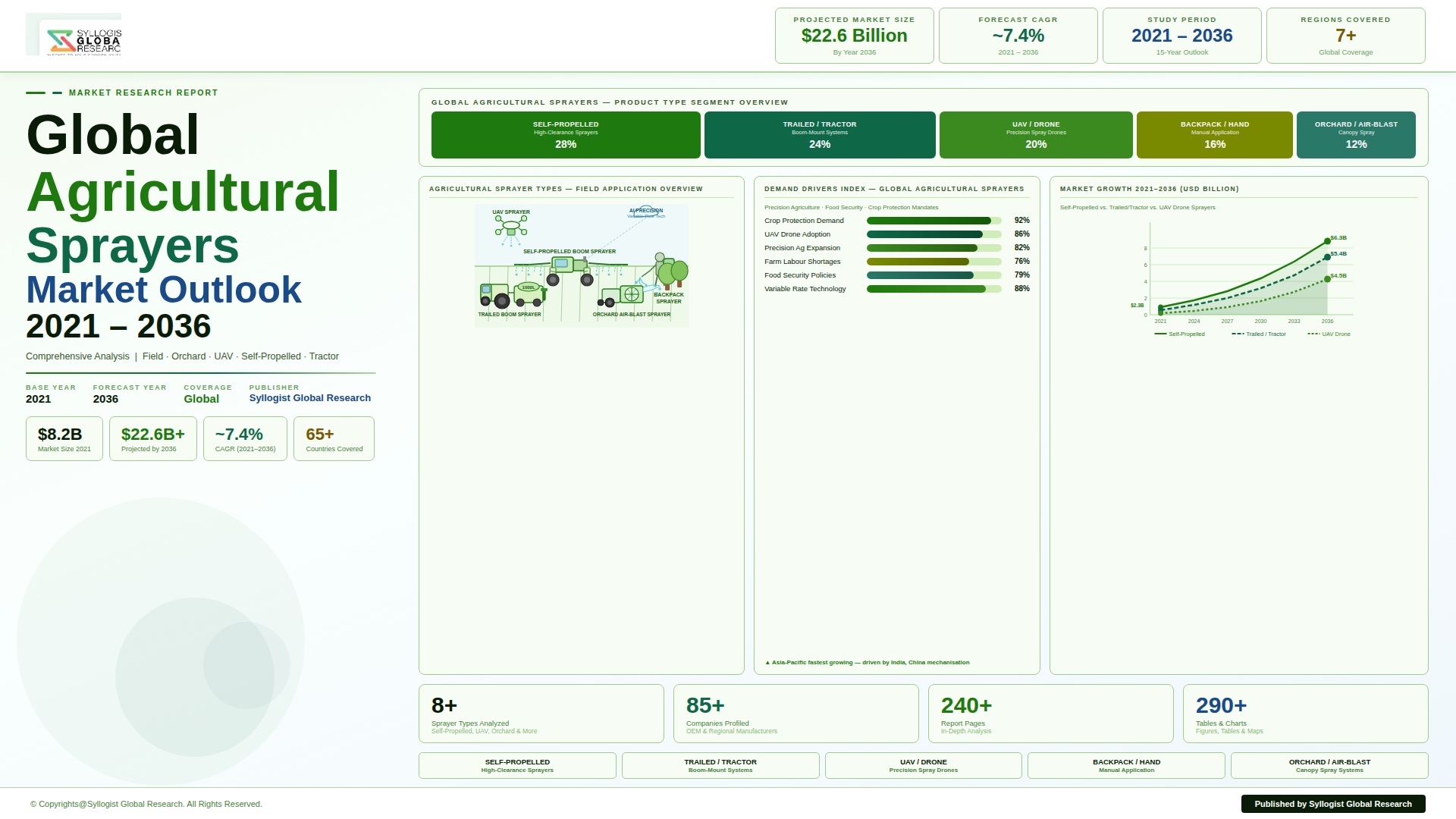

The global agricultural sprayers market is experiencing a period of sustained structural growth and accelerating technological transformation driven by the simultaneous intensification of global crop protection chemical application requirements as pest and disease pressure increases with climate change, the tightening of environmental and regulatory frameworks governing agrochemical use efficiency and drift control that are compelling investment in precision sprayer technology upgrades, and the progressive adoption of autonomous and UAV-based sprayer platforms that are expanding the operational boundaries of agrochemical application into terrain, crop, and scale contexts previously inaccessible to conventional ground-based equipment. The global agricultural sprayers market was valued at approximately USD 4.7 billion in 2025 and is projected to reach USD 7.6 billion by 2034, advancing at a compound annual growth rate of 5.5% over the forecast period from 2027 to 2034, supported by expanding agricultural mechanization in Asian, African, and Latin American developing markets, the replacement cycle demand from the large installed base of aging self-propelled and trailed sprayer equipment in North American and European commercial farming operations, and the premium value contribution of precision application technology components including individual nozzle control, real-time flow regulation, and AI-driven spot spraying systems that are substantially increasing the average selling price of new sprayer units delivered to professional agricultural customers globally.

The self-propelled sprayer segment represents the highest revenue-generating product category within the global agricultural sprayers market, accounting for approximately 38% of total market revenue in 2025, dominated by the large-format, high-clearance self-propelled boom sprayer platforms deployed across the extensive corn, soybean, wheat, and cotton production areas of the United States, Canada, Brazil, Argentina, and Australia where field scale, seasonal application window constraints, and agronomic timeliness requirements justify the premium capital cost of self-propelled equipment over tractor-mounted alternatives. The competitive landscape of the self-propelled sprayer segment is defined by a small number of dominant global manufacturers including CNH Industrial through its Case IH Patriot and New Holland Guardian brands, AGCO through its RoGator and TerraGator platforms, John Deere through its R-Series sprayers, and Hagie Manufacturing, whose engineering platforms are progressively incorporating precision application technology as standard equipment rather than optional upgrades, including individual nozzle control systems delivering section-level application shutoff at sub-meter resolution, automatic boom height control maintaining optimal nozzle-to-canopy distance across undulating terrain, and telematics connectivity enabling remote fleet monitoring and agronomic prescriptive delivery management. The average selling price of a fully equipped self-propelled sprayer with a 36-meter boom, 4,000-liter tank, and precision technology package has increased from approximately USD 280,000 in 2018 to approximately USD 410,000 in 2025, reflecting both material and manufacturing cost inflation and the premium value of integrated precision application technology that is now a standard customer expectation in professional North American and Australian agricultural markets.

The UAV and drone sprayer segment is the most dynamically growing category within the global agricultural sprayers market, expanding at approximately 22.4% annually as the combination of Chinese agricultural drone technology commercialization led by DJI Agras and XAG, expanding regulatory approval frameworks across Asian, Latin American, and increasingly European markets for agricultural UAV operations, and the operational advantages of aerial application in paddy rice, hillside orchard, and terrain-constrained crop production environments that are inaccessible or operationally hazardous for ground-based sprayer equipment collectively drive adoption across a broadening range of agricultural contexts and geographies. China represents the most advanced agricultural drone sprayer market globally by deployment scale, with the agricultural drone fleet in China having reached approximately 200,000 registered agricultural UAVs in 2025 treating over 700 million mu of cropland annually, reflecting the rapid commercialization of DJI Agras T-series and XAG P-series multi-rotor spray platforms across China’s rice, wheat, corn, and fruit crop production areas where the small field size, irregular field geometry, and labor cost escalation of Chinese agriculture create a particularly favorable commercial environment for UAV sprayer adoption. Outside China, South Korea, Japan, and increasingly Vietnam, India, and Brazil are establishing commercially active agricultural drone sprayer markets supported by government subsidy programs, regulatory framework development, and domestic agricultural drone manufacturing investment that are collectively accelerating UAV sprayer adoption beyond the Chinese market into a genuinely global commercial growth trajectory. The regulatory evolution in the European Union, where the European Union Aviation Safety Agency has progressively developed the UAS regulation framework enabling commercial agricultural drone operations across member states, is opening the European market to agricultural UAV sprayer deployment in specialty crop, viticulture, and difficult terrain applications where ground-based equipment access is limited.

The precision application technology retrofit and integration segment is generating a structurally significant revenue stream within the global agricultural sprayers market as the large installed base of existing boom sprayer platforms in North America, Europe, and South America becomes a target market for aftermarket precision technology upgrades including individual nozzle control systems, section control modules, variable rate application controllers, and AI-powered camera-based weed detection systems that transform existing sprayer equipment into precision delivery platforms without the capital commitment of complete machine replacement. Trimble Agriculture, Raven Industries acquired by CNH, Topcon Agriculture, and John Deere’s Precision Ag division are the principal technology suppliers competing in the precision sprayer technology integration market, with their respective individual nozzle control systems including the Trimble WeedSeeker 2, Raven Hawkeye, and John Deere See and Spray systems representing the most commercially significant precision application technology categories whose adoption is being driven by herbicide cost savings, resistance management benefits, and regulatory compliance advantages that deliver measurable return on technology investment within two to three growing seasons for growers applying herbicides across large arable areas with mixed weed populations. From a regional standpoint, Asia-Pacific is both the largest volume market for agricultural sprayers by unit count, dominated by the massive knapsack and backpack sprayer demand of smallholder farming systems across South Asia and Southeast Asia, and simultaneously the fastest-growing market for advanced sprayer technology through the Chinese agricultural drone and the Indian tractor-mounted boom sprayer mechanization investment waves that are reshaping the sprayer demand structure of the region toward higher-value equipment categories.

Key Drivers

Escalating Global Crop Protection Demand and Intensifying Agrochemical Application Requirements Sustaining Structural Sprayer Equipment Demand Across All Agricultural Regions

The structural growth in global agrochemical application volumes driven by the intensification of crop production on a constrained agricultural land base, the expanding geographic range and seasonal activity window of established pest and disease threats attributable to climate-driven growing season extension and temperature boundary shifts, and the emergence of new invasive pest species requiring emergency agrochemical response programs is generating a durable and expanding demand foundation for agricultural sprayer equipment across all major agricultural production regions. Global pesticide use has grown by approximately 3.1% annually over the past decade, reaching an estimated 4.1 million tonnes of active ingredient applied worldwide in 2024, and the correlation between agrochemical application volume and sprayer equipment utilization, replacement cycle acceleration, and new equipment investment creates a structurally positive demand environment for the agricultural sprayers market that is reinforced by the growing adoption of multi-pass, differentiated spray programs applying fungicides, insecticides, and foliar nutrients in separate spray events rather than combined tank mixes that increase the total annual sprayer utilization hours and equipment wear rate at commercial farm operations. The shift of global agricultural production toward higher-value specialty crops including fruits, vegetables, and wine grapes, which characteristically require more intensive and frequent agrochemical spray programs than staple cereal crops to maintain marketable product quality, is increasing the average per-hectare sprayer equipment investment and annual operating cost in the specialty crop segments that represent the fastest-growing agricultural production value categories globally, generating above-average growth in the orchard, vineyard, and horticultural sprayer equipment segments.

Precision Agriculture Adoption and Regulatory Mandates for Reduced Agrochemical Drift and Environmental Contamination Driving Technology Upgrade Investment in Sprayer Platforms

The convergence of farmer economic incentives to reduce agrochemical input costs through precision application efficiency and regulatory mandates requiring demonstrable agrochemical use reduction, drift control compliance, and buffer zone management across European, North American, and increasingly Asian agricultural production systems is compelling a technology upgrade cycle across the global sprayer equipment base that is substantially increasing the average value content of new sprayer sales and generating a large retrofit market for precision application components across the installed equipment base. The European Union’s Farm to Fork Strategy target of achieving a 50% reduction in pesticide use by 2030, implemented through national action plans under the Sustainable Use of Pesticides Directive revision that impose mandatory no-spray buffer zones, drift-reducing nozzle requirements, and in some member states blanket bans on specific active ingredients in environmentally sensitive areas, is creating direct regulatory compliance investment drivers for European farmers who must upgrade their spray equipment with low-drift nozzle technology, section control systems minimizing overlap application, and precision application documentation capabilities that satisfy regulatory compliance demonstration requirements. The commercial case for AI-powered spot spraying technology, which applies herbicide only to detected weed locations rather than broadcasting across entire field areas, is quantifiably compelling given that weed populations typically occupy only 5% to 30% of total field area in established arable systems, implying herbicide savings of 70% to 95% from precision spot application relative to broadcast treatment that translate directly into input cost reductions of several hundred USD per hectare per season across large-scale arable operations.

Agricultural Mechanization Acceleration in Developing Markets and the Replacement of Manual Knapsack Application with Tractor-Mounted and UAV Sprayer Technology

The structural transition of smallholder and emerging commercial agricultural systems across South Asia, Southeast Asia, Sub-Saharan Africa, and Latin America from manual knapsack sprayer application toward mechanized tractor-mounted boom sprayers and UAV platforms is generating a large and rapidly expanding addressable market for mid-range and advanced sprayer technology in agricultural economies that have historically been dominated by low-value manual application equipment, driven by rural labor cost escalation, expanding tractor ownership and hire service availability, government mechanization subsidy programs, and the demonstrated productivity and agronomic timeliness advantages of mechanized application over manual spray operations. India represents the most commercially significant emerging mechanized sprayer market, with the government’s Sub-Mission on Agricultural Mechanization providing purchase subsidies of 40% to 50% for tractor-mounted boom sprayers and drone sprayers through the agricultural mechanization program, and with Indian tractor sales reaching approximately 960,000 units in fiscal year 2024-25 providing an expanding prime mover base whose operators are progressively adding tractor-mounted sprayer implements to their equipment complement as herbicide and fungicide adoption in Indian cereal, pulse, and oilseed farming increases. Sub-Saharan Africa represents the longest-runway emerging sprayer market given its combination of approximately 600 million hectares of potentially arable land, rapidly growing commercial farming sector investment, and current sprayer mechanization levels that remain well below the mechanization density of comparable South American agricultural economies at equivalent stages of commercialization, with FAO and bilateral development finance institution programs actively supporting agricultural mechanization investment including sprayer equipment access across East African and West African commercial farming development corridors.

Key Challenges

Stringent and Divergent Pesticide Application Regulatory Frameworks Across Global Markets Creating Compliance Complexity and Restricting Equipment Operational Flexibility

Agricultural sprayer operators and equipment manufacturers are confronted with an increasingly complex and geographically fragmented regulatory landscape governing the registration, use conditions, buffer zone requirements, meteorological application constraints, and operator safety standards applicable to pesticide application equipment, with regulatory frameworks varying materially between the European Union, United States, Australia, and major Asian agricultural economies in ways that restrict the operational parameters under which sprayer equipment can be legally deployed, require market-specific equipment certifications and compliance documentation, and create design specification divergence requirements for sprayer manufacturers seeking to sell common equipment platforms across multiple regulatory jurisdictions. The EU Sustainable Use of Pesticides Regulation, currently progressing through the legislative process following the European Commission’s revised proposal, proposes binding quantitative targets for pesticide use reduction that, if enacted in their proposed form, would impose mandatory restrictions on spray operations in defined environmentally sensitive areas, require the use of precision application technology capable of demonstrating compliance with reduced application volume targets, and mandate the digital recording and reporting of all commercial spray operations in a format accessible to regulatory inspection authorities, creating a compliance technology requirement that goes beyond agronomic best practice into mandated equipment specification and data management system investment for every professional sprayer operator in the EU. The proliferation of national and sub-national drone sprayer regulatory frameworks across Asia, Latin America, and Africa, each with distinct operator licensing requirements, maximum operating altitude limits, no-fly zone definitions, and payload weight restrictions, creates market fragmentation complexity for global agricultural UAV sprayer manufacturers seeking to build scalable commercial distribution and support operations across multiple regulatory environments simultaneously.

High Capital Cost of Advanced Self-Propelled and Precision Sprayer Technology Limiting Adoption Among Small and Medium-Scale Farm Operators

The rapid incorporation of precision application technology, advanced boom control systems, telematics connectivity, and AI-powered weed detection capabilities into new self-propelled and trailed boom sprayer platforms has substantially elevated the entry-level price point of professional-specification sprayer equipment to levels that create significant capital access barriers for the small and medium-scale farm operators who collectively represent the largest segment of the global agricultural production enterprise population by number, constraining the diffusion of precision sprayer technology beyond the large-scale commercial farming operations in North America, Australia, and Western Europe whose farm sizes and production economics generate the revenue scale needed to justify premium equipment investment on conventional return on investment criteria. The total cost of ownership of a fully equipped self-propelled precision sprayer, including finance costs, annual depreciation, insurance, maintenance, and precision technology subscription fees for data services and AI weed detection algorithm updates that are increasingly structured as recurring revenue components of the overall product offer by technology providers, creates an annual equipment operating cost burden that is commercially sustainable only for farm enterprises with sufficient arable hectarage to distribute these fixed costs across a production revenue base of adequate scale. Agricultural equipment dealer financing programs, cooperative equipment sharing schemes, and custom application contracting service business models that allow smaller farm operators to access precision application capability without direct equipment ownership are partially addressing this affordability barrier, but the geographic distribution and financial depth of these access mechanism alternatives remains insufficient to bring precision sprayer technology within commercial reach of the majority of farm operators in developing and transitional agricultural economies.

Operator Skill Requirements and Technical Complexity of Precision Sprayer Systems Creating Adoption Barriers and Operational Performance Shortfalls in Developing Markets

The effective deployment of modern precision agricultural sprayer platforms, particularly self-propelled boom sprayers equipped with GPS section control, variable rate application, individual nozzle management, and integrated telematics systems, requires a level of operator technical competency, digital literacy, and system calibration understanding that significantly exceeds the skill set historically required for conventional sprayer operation, creating a human capital barrier to precision technology adoption that is distinct from and in some agricultural market contexts more constraining than the capital cost barrier, particularly in emerging market agricultural systems where formal agricultural education levels, digital technology familiarity, and access to qualified technical service and training support from equipment dealers are limited. The calibration, maintenance, and troubleshooting of precision spray systems, including the correct setup of GPS variable rate controllers, the regular cleaning and function testing of individual nozzle control solenoids, the interpretation of flow meter and pressure sensor diagnostic data, and the management of agrochemical prescription file creation and transfer workflows from farm management software to sprayer display terminals, constitutes a technical workload that overwhelms the operational management capacity of many farm operators who lack formal training and dealer proximity support, resulting in precision systems being operated in override or manual mode that negates the efficiency and compliance benefits for which the technology investment was justified. Manufacturer and dealer training infrastructure investment, the development of simplified user interface designs that reduce operator cognitive load during spray operations, and the expansion of remote diagnostics and technical support capabilities enabling dealer technicians to assist operators in real time during spray season are the principal industry responses to the operator skill challenge, but their deployment at sufficient scale and geographic coverage to address the global adoption barrier remains a work in progress across the agricultural sprayer industry.

Market Segmentation

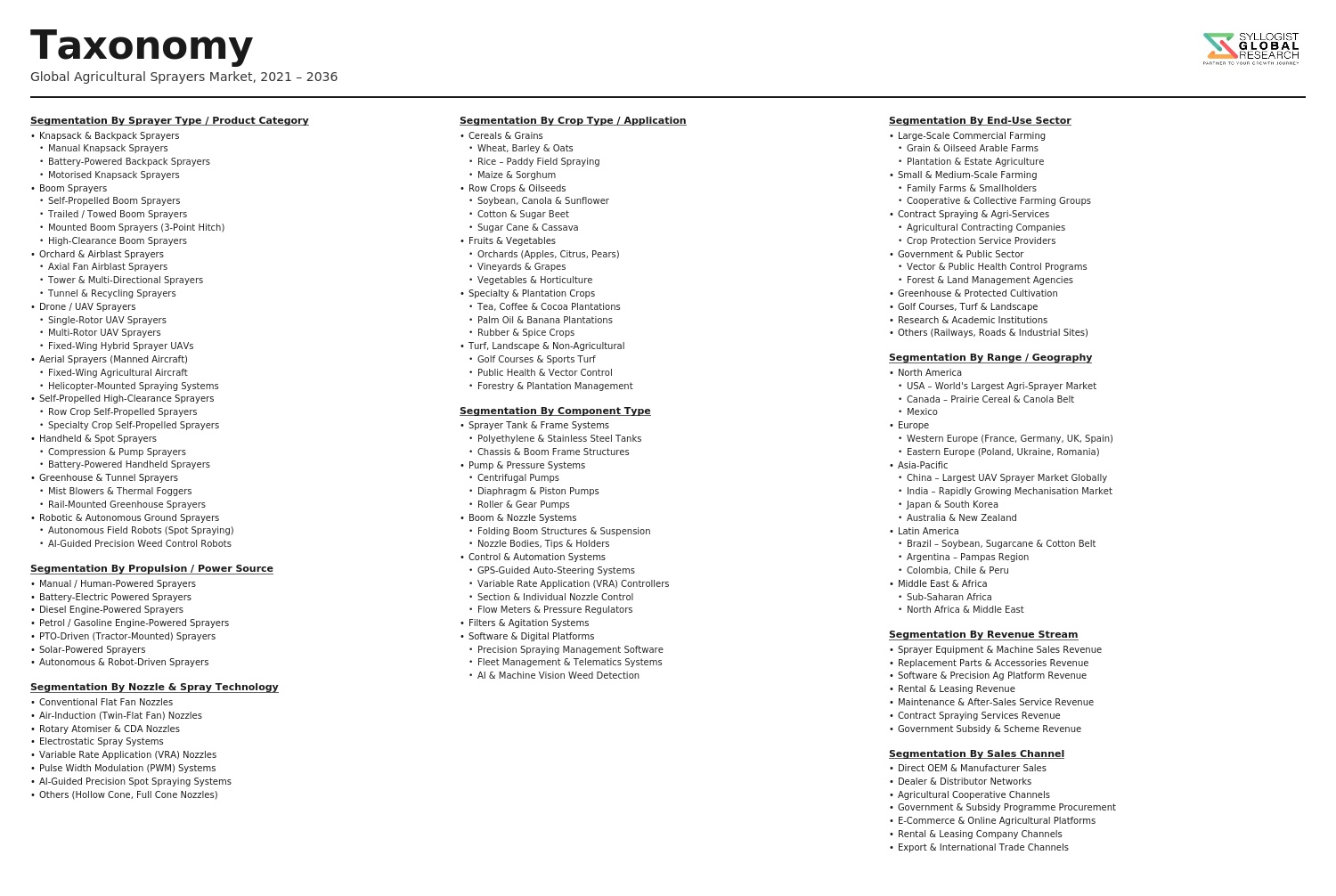

Segmentation By Product Type

- Self-Propelled Boom Sprayers

- Tractor-Mounted and Trailed Boom Sprayers

- Knapsack and Backpack Sprayers (Manual and Motorized)

- UAV and Drone Sprayers

- Orchard and Vineyard Air-Blast Sprayers

- Tunnel and Recycling Sprayers

- Handheld and Compression Sprayers

- Electrostatic Sprayers

- Others

Segmentation By Technology

- Conventional Broadcast Sprayers

- GPS-Guided Section Control Boom Sprayers

- Variable Rate Application (VRA) Sprayer Systems

- Individual Nozzle Control (INC) Precision Sprayers

- AI-Powered Weed Detection and Spot Spraying Systems

- Automatic Boom Height Control Systems

- Drift Reduction and Air-Induction Nozzle Systems

- Telematics and Remote Fleet Management Platforms

- Others

Segmentation By Power Source

- Tractor Power Take-Off (PTO) Driven

- Self-Propelled Engine-Powered (Diesel)

- Battery Electric Powered

- Manual and Human-Powered

- UAV Battery and Hybrid Power Systems

- Others

Segmentation By Application

- Herbicide Application

- Fungicide Application

- Insecticide Application

- Foliar Fertilizer and Micronutrient Application

- Biological and Biopesticide Application

- Plant Growth Regulator Application

- Others

Segmentation By Crop Type

- Cereals and Grains (Wheat, Corn, Rice, Barley)

- Oilseeds (Soybean, Canola, Sunflower)

- Fruits and Orchards (Apple, Citrus, Stone Fruit)

- Vineyards and Wine Grapes

- Vegetables and Horticulture

- Cotton and Fiber Crops

- Sugarcane and Sugar Beet

- Pulses and Legumes

- Others

Segmentation By Farm Size

- Smallholder Farms (Below 2 Hectares)

- Small to Medium Farms (2 to 50 Hectares)

- Large Commercial Farms (50 to 500 Hectares)

- Industrial and Corporate Farms (Above 500 Hectares)

- Custom Application Service Contractors

- Others

Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Direct Sales

- Authorized Dealer and Distributor Network

- Agricultural Cooperative Procurement

- Online and E-Commerce Platforms

- Government and Subsidy Program Procurement

- Rental and Equipment Hire Services

- Others

Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Agricultural Sprayers Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, technology, crop type, farm size, and region, to enable agricultural machinery manufacturers, precision agriculture technology developers, agrochemical companies, and investors to identify which sprayer equipment categories and geographic markets will generate the highest absolute revenue and the most sustained demand growth across the forecast period?

- How is the adoption of precision application technologies including GPS boom section control, variable rate application, individual nozzle control, and AI-powered weed detection and spot spraying systems progressing across North American, European, South American, and Asian commercial farming operations, what quantifiable input cost savings and regulatory compliance benefits are documented adopters realizing from precision sprayer technology investments, and what technology cost reduction and user interface simplification milestones are required to extend precision sprayer adoption to medium and smaller scale farm operators in developing agricultural markets?

- What is the current global deployment scale, projected growth trajectory, regulatory approval status, and competitive technology landscape of UAV and drone agricultural sprayer platforms across China, South Korea, Japan, India, Latin America, and European markets through 2034, which crop types and terrain categories generate the most compelling operational case for UAV versus ground-based sprayer application, and how are the leading agricultural drone sprayer manufacturers including DJI Agras and XAG positioned against emerging domestic competitors in key regional markets?

- How are the European Union Sustainable Use of Pesticides Regulation revision targets, North American Environmental Protection Agency spray drift label requirements, and national pesticide use reduction mandates across major agricultural markets reshaping the technical specifications, nozzle technology standards, buffer zone management capabilities, and digital compliance documentation requirements of professional boom sprayer platforms, and what is the projected aggregate equipment upgrade and retrofit investment driven by regulatory compliance requirements across the European and North American sprayer installed base through 2034?

- Who are the leading global self-propelled and trailed boom sprayer manufacturers, UAV agricultural sprayer developers, precision application technology providers, and orchard and specialty crop sprayer specialists currently defining the competitive landscape of the global agricultural sprayers market, and what are their respective product portfolios, technology development roadmaps for autonomous and electric sprayer platforms, regional manufacturing and distribution footprints, dealer network depth and technical service infrastructure, strategic partnerships with agrochemical and precision agriculture data companies, and competitive responses to the structural market opportunity presented by agricultural mechanization acceleration in Asia, Africa, and Latin America through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Agrochemical Regulation Tightening, Pesticide Use Reduction Mandates & Demand Impact Risk for Conventional Sprayers

- Commodity Price Volatility, Farmer Income Variability & Discretionary Capital Equipment Spending Risk

- Raw Material Cost Inflation, Steel & Polymer Supply Chain Disruption & Manufacturing Cost Risk

- Technology Disruption: UAV, Autonomous & AI-Driven Sprayer Substitution Risk for Conventional Equipment

- Counterfeit Equipment, Low-Cost Import Competition & After-Sales Service Quality Risk in Emerging Markets

- Regulatory Framework & Standards

- EU Sustainable Use of Pesticides Regulation (SUR), Farm to Fork Pesticide Reduction Targets & Sprayer Inspection & Certification Requirements

- US EPA Pesticide Application Equipment Standards, FIFRA Requirements & State-Level Sprayer Regulation Frameworks

- ISO 16119 Series (Agricultural Sprayer Safety & Testing Standards) & Regional Type Approval Requirements

- Drone & UAV Agricultural Spraying Regulations: EASA, FAA & National Civil Aviation Authority Frameworks

- Environmental Compliance: Drift Management Standards, Buffer Zone Requirements, Water Body Protection & Agrochemical Run-Off Regulations

- Global Agricultural Sprayers Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Sold)

- Market Size & Forecast by Sprayer Type

- Knapsack & Backpack Sprayers (Manual & Motorised)

- Hand-Carried & Compression Sprayers

- Tractor-Mounted Boom Sprayers

- Self-Propelled Boom Sprayers

- Trailed Boom Sprayers

- Orchard & Vineyard Airblast Sprayers

- UAV & Drone Sprayers

- Aerial Application Sprayers (Fixed-Wing & Helicopter)

- Autonomous & Robotic Ground Sprayers

- Irrigation-Based Chemigation & Fertigation Systems

- Market Size & Forecast by Propulsion Type

- Manual & Hand-Operated Sprayers

- Engine-Powered (Petrol & Diesel) Sprayers

- Battery-Electric & Hybrid Sprayers

- Tractor PTO-Driven Sprayers

- Autonomous & AI-Guided Sprayer Systems

- Market Size & Forecast by Nozzle & Application Technology

- Flat Fan & Standard Nozzle Systems

- Air-Induction & Venturi Nozzle Systems

- Pulse Width Modulation (PWM) Variable Rate Nozzle Systems

- Electrostatic Spraying Systems

- Precision Spot & Band Spraying Systems

- AI-Based Weed Detection & Targeted Micro-Dosing Systems

- Market Size & Forecast by Tank Capacity

- Small Capacity (Below 200 Litres)

- Medium Capacity (200 to 1,000 Litres)

- Large Capacity (1,000 to 4,000 Litres)

- Extra-Large Capacity (Above 4,000 Litres)

- Market Size & Forecast by Boom Width

- Narrow Boom (Below 12 Metres)

- Standard Boom (12 to 24 Metres)

- Wide Boom (24 to 36 Metres)

- Extra-Wide Boom (Above 36 Metres)

- Market Size & Forecast by Crop Type

- Cereals & Grains (Wheat, Rice, Maize & Barley)

- Oilseeds & Pulses (Soybean, Canola & Sunflower)

- Fruits & Orchards (Apples, Citrus, Grapes & Stone Fruit)

- Vegetables & Horticultural Crops

- Cotton, Sugarcane & Plantation Crops

- Turf, Amenity & Non-Agricultural Applications

- Market Size & Forecast by Application

- Herbicide Application

- Fungicide Application

- Insecticide Application

- Fertiliser & Plant Growth Regulator Application

- Biological & Bio-Stimulant Application

- Market Size & Forecast by End-User

- Individual Farmers & Small-Scale Growers

- Large Commercial Farms & Agricultural Enterprises

- Contract Spraying & Agricultural Service Providers

- Government & Public Agricultural Agencies

- Research Institutes & Agricultural Universities

- Market Size & Forecast by Sales Channel

- Dealer & Distributor Network

- Original Equipment Manufacturer (OEM) Direct Sales

- Agri-Input Retailer & Cooperative

- Online & E-Commerce Platform

- Rental, Leasing & Sprayer-as-a-Service Model

- North America Agricultural Sprayers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Sprayer Type

- By Propulsion Type

- By Nozzle & Application Technology

- By Crop Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Agricultural Sprayers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Sprayer Type

- By Propulsion Type

- By Nozzle & Application Technology

- By Crop Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Agricultural Sprayers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Sprayer Type

- By Propulsion Type

- By Nozzle & Application Technology

- By Crop Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Agricultural Sprayers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Sprayer Type

- By Propulsion Type

- By Nozzle & Application Technology

- By Crop Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Agricultural Sprayers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Sprayer Type

- By Propulsion Type

- By Nozzle & Application Technology

- By Crop Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Agricultural Sprayers Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Sprayer Type

- By Propulsion Type

- By Nozzle & Application Technology

- By Crop Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Precision Boom Sprayer Technology: Section Control, Variable Rate Application & GPS-Guided Boom Management Deep-Dive

- AI-Based Weed Detection, Camera-Guided Spot Spraying & Machine Vision Technology for Herbicide Use Reduction

- UAV & Drone Agricultural Sprayer Technology: Payload Capacity, Swath Width, Nozzle Design & Autonomous Mission Planning

- Autonomous & Robotic Ground Sprayer Technology: Navigation, Obstacle Avoidance & Multi-Row Crop Adaptation

- Electrostatic Spraying & Charged Droplet Technology for Improved Coverage & Chemical Use Efficiency

- Battery-Electric & Hybrid Propulsion Technology for Agricultural Sprayers: Power Management & Field Endurance

- Sprayer Telematics, Fleet Management & IoT-Connected Sprayer Data Platform Technology

- Patent & IP Landscape in Agricultural Sprayer Technologies

- Value Chain & Supply Chain Analysis

- Steel, Stainless Steel, Polymer & Composite Material Supply Chain for Sprayer Manufacturing

- Pump, Nozzle, Boom, Control Valve & Hydraulic Component Manufacturing Supply Chain

- Electronics, GPS, Sensor & Precision Application System Supply Chain

- Sprayer Assembly, Quality Testing & Certification Manufacturing Supply Chain

- Dealer, Distributor & Agri-Input Retailer Sales Channel

- After-Sales Service, Spare Parts & Maintenance Network

- End-of-Life Equipment Recycling, Chemical Residue Management & Disposal Value Chain

- Pricing Analysis

- Knapsack & Manual Sprayer Unit Price Benchmarking Across Key Markets

- Tractor-Mounted & Self-Propelled Boom Sprayer Capital Cost & Total Cost of Ownership (TCO) Analysis

- UAV & Drone Sprayer Purchase, Leasing & Spraying-as-a-Service Fee Structure Analysis

- Precision & Variable Rate Sprayer Premium vs. Conventional Sprayer Cost-Benefit Analysis

- After-Sales Service, Spare Parts & Annual Maintenance Cost Analysis

- Total Spraying Cost per Hectare Across Sprayer Types & Markets

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Agricultural Sprayers: Carbon Footprint, Energy Consumption & Material Use Across Sprayer Categories

- Precision & AI-Guided Sprayer Contribution to Pesticide Use Reduction, Chemical Run-Off & Environmental Load Minimisation

- Drift Reduction Technology & Nozzle Innovation: Environmental Compliance & Off-Target Application Risk Mitigation

- Electric & Autonomous Sprayer Role in Farm Decarbonisation, Fuel Saving & Carbon Footprint Reduction

- Regulatory-Driven Sustainability, SDG 2 (Zero Hunger), SDG 3 (Good Health), SDG 15 (Life on Land) & ESG Disclosure Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Sprayer Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Sprayer Type, Crop Type & Geography

- Player Classification

- Global Integrated Agricultural Machinery & Sprayer OEM Majors

- Specialist Self-Propelled & High-Clearance Boom Sprayer Manufacturers

- Knapsack, Backpack & Small-Scale Sprayer Manufacturers

- UAV & Drone Agricultural Sprayer Manufacturers

- Autonomous & Robotic Ground Sprayer Start-Ups & Developers

- Precision Application, Nozzle & Sprayer Technology Component Suppliers

- Orchard & Specialty Crop Airblast Sprayer Manufacturers

- Sprayer Dealer Networks, Rental & Spraying Service Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Sprayer Type, Region & Crop Application

- Company Profile

- Company Overview & Headquarters

- Agricultural Sprayer Products & Technology Portfolio

- Key Customer Relationships & Reference Markets

- Manufacturing Footprint & Production Capacity

- Revenue (Agricultural Sprayer Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (New Product Launches, Capacity Expansion, Contract Wins)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Sprayer Type, Propulsion Type, Crop Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output