Market Definition

The Global Agri Robotics Market encompasses the design, development, manufacture, deployment, and operational service of autonomous and semi-autonomous robotic systems, unmanned aerial vehicles, ground-based mobile platforms, and stationary robotic installations specifically engineered to perform agricultural tasks across field crop cultivation, specialty crop production, livestock management, greenhouse and controlled environment agriculture, post-harvest handling, and precision agrochemical application with greater consistency, speed, data capture capability, and labor independence than human-operated or conventional mechanized alternatives. Agricultural robotics integrates mechanical engineering with computer vision, machine learning, global navigation satellite systems, sensor fusion, actuator precision, and agronomic intelligence to create systems capable of detecting, classifying, and responding to the biological variability of living plants and animals in unstructured outdoor and semi-controlled environments, distinguishing agri robots from simpler agricultural automation by their capacity for autonomous decision-making based on real-time environmental data rather than pre-programmed fixed sequences. The market encompasses autonomous field robots for weeding, thinning, transplanting, and inter-row cultivation, robotic harvesting systems for strawberries, apples, tomatoes, lettuce, asparagus, and other specialty crops requiring selective picking based on ripeness assessment, drone platforms for crop scouting, multispectral imaging, precision pesticide and fertilizer spraying, and pollination assistance, autonomous tractors and orchard platforms for soil preparation, spraying, and mechanical harvesting support, robotic milking systems and automated livestock monitoring platforms, robotic seeding and planting systems for high-precision seed placement, robotic greenhouse platforms for climate monitoring and plant care, post-harvest sorting and grading robots, and the supporting digital infrastructure of farm management software, connectivity platforms, and data analytics systems that enable agri robots to deliver actionable agronomic intelligence alongside their physical task execution. Key participants include agri robotics hardware developers, computer vision and artificial intelligence software companies, agricultural machinery manufacturers integrating robotics capabilities, venture-backed agricultural technology startups, drone manufacturers, precision agriculture service providers, and farming cooperatives and large-scale farm operators deploying robotic systems.

Market Insights

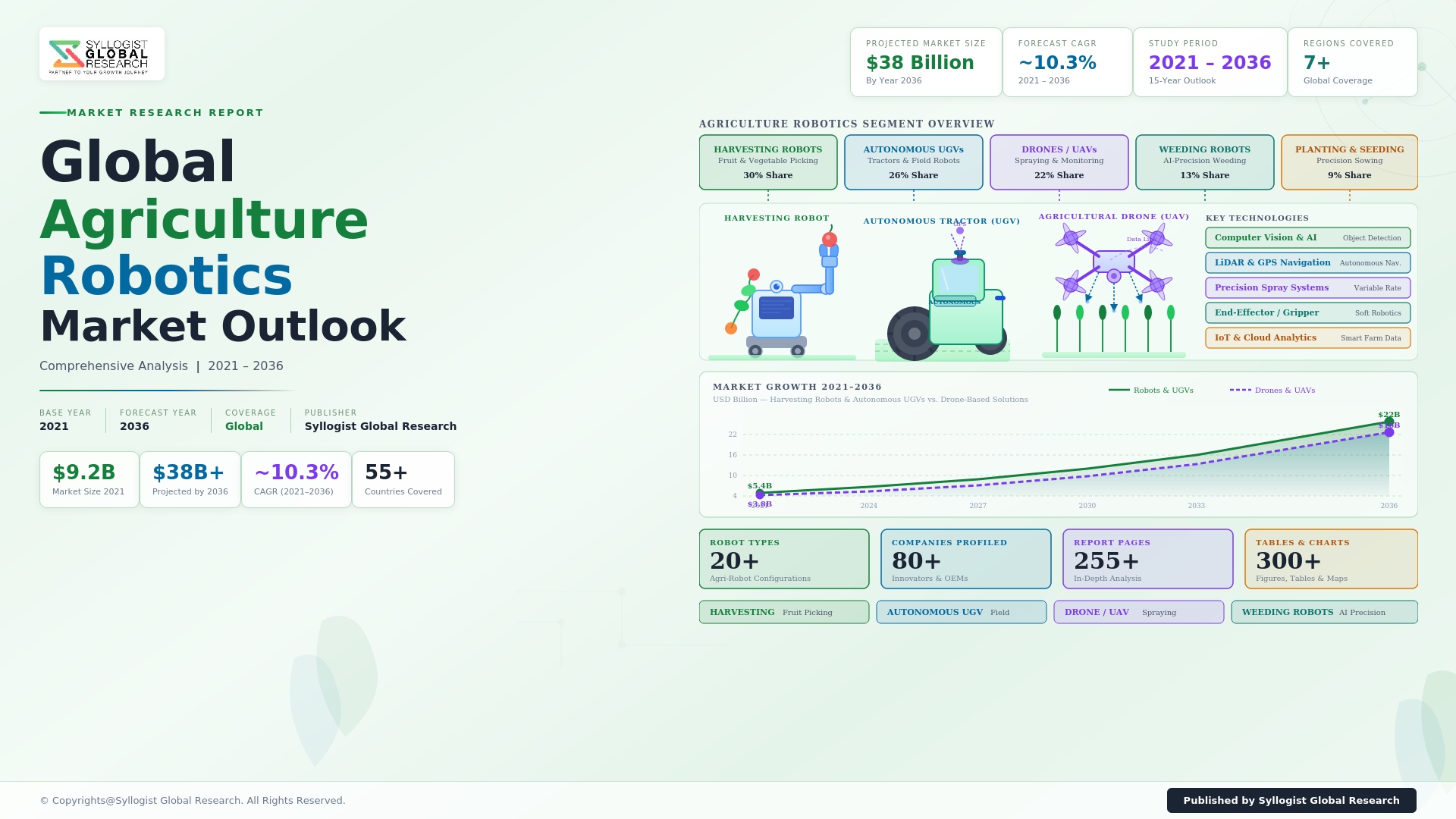

The global agri robotics market was valued at approximately USD 9.4 billion in 2025 and is projected to reach USD 32.6 billion by 2034, advancing at a compound annual growth rate of 14.8% over the forecast period from 2027 to 2034, driven by the accelerating convergence of structural agricultural labor shortages in developed economies, the continuous cost reduction and capability improvement of enabling technologies including computer vision, edge computing, battery energy density, and lightweight actuator systems, the growing commercial viability of robotic systems in high-value specialty crop segments where return on investment justification is most accessible, and the urgent imperative to reduce chemical pesticide and fertilizer input volumes in response to environmental regulations, consumer demand for residue-free produce, and corporate sustainability commitments that make precision robotic application economically and regulatorily superior to conventional broadcast chemical management. The total global agricultural labor force contracted by approximately 8.4% between 2018 and 2025 in developed economies including the United States, Germany, France, Australia, Japan, South Korea, and the United Kingdom, with seasonal peak harvest labor for specialty crops including tree fruits, berries, and vegetables experiencing the most acute availability constraints as immigration policy tightening, competing urban employment opportunities, and demographic aging of the traditional agricultural seasonal workforce collectively reduced the reliability and affordability of human harvest labor at the exact time when production volumes and quality standards were increasing. The robotic milking and livestock management segment reached approximately USD 1.8 billion in 2025, representing the most commercially mature agri robotics category with voluntary milking systems deployed in approximately 48,000 dairy farms globally at an average capital investment of approximately USD 180,000 to USD 250,000 per milking unit, demonstrating a proven return on investment through twenty-four hour milking availability, reduced labor dependency, improved individual cow health monitoring, and milk yield optimization that has driven adoption penetration to approximately 22% of eligible commercial dairy farms in Northern Europe and approximately 12% in North America.

The agricultural drone segment represents the largest component of the global agri robotics market by deployment volume, accounting for approximately 34% of total market revenue in 2025 at approximately USD 3.2 billion, driven by the rapid commercial scaling of agricultural drone applications from crop scouting and multispectral imagery capture toward active agrochemical application using precision spray drones that deliver pesticides, herbicides, fungicides, and liquid fertilizers with application accuracy and drift reduction that reduces chemical usage by approximately 30% to 50% relative to conventional ground-based sprayer equipment or manned aerial application. China accounts for approximately 46% of global agricultural drone deployment by fleet size, with DJI Agriculture’s Agras T-series spray drones operating across approximately 180 million acres of Chinese agricultural land annually and Chinese drone operators providing contracted application services at approximately USD 8 to USD 15 per acre for rice, wheat, and corn crops whose large contiguous field patterns and regulatory support for agricultural drone operation create the most economically favorable deployment conditions globally. Agricultural drone adoption is accelerating rapidly in the United States, Brazil, India, Japan, South Korea, and Australia as regulatory frameworks including United States Federal Aviation Administration Beyond Visual Line of Sight authorization programs, India’s Drone Rules 2021 liberalization, and European Union Aviation Safety Agency agricultural drone operational category standards progressively create clearer and more permissive operating environments that enable commercial agricultural drone service operators and farm-direct drone operators to scale deployment beyond the early adopter farm customer base toward mainstream commodity crop application programs. The transition from multirotor spray drones to fixed-wing hybrid vertical takeoff and landing designs capable of covering 400 to 800 acres per flight at payloads of 20 to 40 kilograms is extending the economic efficiency of drone application to larger field scales that represent the majority of global crop area and where the per-acre economics of drone application can compete with conventional tractor-based application on total cost of ownership including labor, chemical, and equipment depreciation components.

The specialty crop robotic harvesting segment, targeting the mechanization of selective harvest operations for strawberries, raspberries, blueberries, apples, pears, tomatoes, cucumbers, sweet peppers, and lettuce that collectively represent the highest-value and most labor-intensive components of the global horticultural production system, has achieved critical commercial milestones over the past three years that are transitioning the segment from development-stage technology demonstration to deployable commercial systems generating measurable returns for early-adopter farm operators. Tortuga AgTech’s strawberry harvesting robot, Abundant Robotics’ apple vacuum harvesting system, Root AI’s Virgo tomato harvesting platform, and Dogtooth Technologies’ strawberry picker have each achieved commercial field deployment generating operational performance data demonstrating harvest rates of 8 to 15 seconds per fruit across the best-performing systems, approaching the economic threshold at which robotic harvest labor cost per kilogram of harvested produce becomes competitive with human picker labor in high-wage markets including the United States West Coast, Netherlands, Germany, and Australia where seasonal picker wages have increased to approximately USD 18 to USD 28 per hour and total harvest labor cost represents 40% to 65% of farm-gate production cost for premium berry and salad vegetable categories. The controlled environment agriculture segment, encompassing greenhouse vegetable and herb production, vertical farming, and indoor berry production facilities, provides the most technically accessible environment for agri robotics deployment given the structured physical environment, consistent lighting, defined row spacing, and high crop density that enable robotic systems to achieve higher task completion rates and lower mechanical error rates than in the variable outdoor field environment, with automated greenhouse platforms from companies including AppHarvest, Bowery Farming, and Revol Greens deploying robotic transplanting, climate monitoring, irrigation, and harvest assist systems across an expanding commercial greenhouse footprint.

The autonomous tractor and field robot segment, which automates soil preparation, precision planting, mechanical weeding, and crop scouting operations across arable crop production at scales relevant to large commercial farms in North America, Europe, Australia, and South America, is transitioning from technology demonstrations and small-fleet pilots toward commercial fleet deployments as major agricultural machinery manufacturers including John Deere, CNH Industrial, AGCO, and Kubota integrate autonomous navigation, obstacle avoidance, and precision guidance capabilities into production tractor platforms that are commercially available and supported through established dealer networks. John Deere’s autonomous 8R tractor, which delivers hands-free field operations using six pairs of stereo cameras and computer vision to identify obstacles and maintain precise field coverage, has accumulated commercial farm operating hours in the tens of thousands across early adopter farms in the United States corn belt and European arable farming regions, demonstrating the operational readiness of autonomous tractor technology at commercial farm scale and providing the reference performance data that risk-averse mainstream farm operators require before committing to fleet-scale autonomous equipment procurement. The precision weeding robot segment, in which robotic platforms including FarmWise, Carbon Robotics, and Naïo Technologies deploy computer vision and mechanical micro-cultivation or laser weeding actuators to identify and selectively eliminate weeds within crop rows at the individual plant level, is achieving commercial adoption at organic and pesticide-reduction farms where the elimination of herbicide applications through robotic weeding directly addresses regulatory compliance requirements and premium market positioning objectives that justify the higher operating cost of robotic weeding relative to conventional herbicide broadcast application in conventional farming systems.

Key Drivers

Structural Agricultural Labor Scarcity, Rising Seasonal Harvest Labor Costs, and Demographic Workforce Aging Creating an Economically Imperative Case for Robotic Task Automation in Labor-Intensive Crop Production

The structural and accelerating shortage of reliable, affordable seasonal agricultural labor in major food-producing economies represents the most commercially compelling and economically irreversible driver of agri robotics adoption, as the combination of immigration policy restriction, urban wage competition, agricultural workforce demographic aging, and the physical demanding nature of harvest work is creating a labor supply crisis for the specialty crop, horticultural, and dairy sectors whose production economics and quality standards fundamentally depend on the availability of large volumes of skilled seasonal workers at critical harvest windows that cannot be deferred without complete crop loss. In the United States, the agricultural sector experienced a shortage of approximately 240,000 seasonal farm workers in 2025 relative to peak demand requirements, with the H-2A agricultural guest worker visa program processing approximately 378,000 applications in 2025 at an average employer cost including housing, transportation, and wage guarantees of approximately USD 16,000 to USD 24,000 per worker per season, creating a total seasonal labor cost burden for the United States horticultural and specialty crop sector of approximately USD 6.1 billion annually that represents the primary economic justification for robotic harvesting capital investment. European specialty crop producers in the Netherlands, Spain, Italy, Germany, and Poland face structurally similar seasonal labor availability constraints following Brexit-related reduction in Eastern European worker mobility to the United Kingdom and tightening of third-country national agricultural worker visa programs, with strawberry and apple producers reporting peak harvest labor shortfalls of 15% to 30% in multiple recent seasons that directly resulted in crop waste and revenue losses that exceed the annual capital cost of robotic harvesting alternatives at commercial deployment scale.

Precision Agriculture Policy Mandates, Pesticide Reduction Regulations, and Environmental Sustainability Requirements Driving Demand for Precision Robotic Application Technologies

The regulatory trajectory across the European Union, United Kingdom, United States, and several Asia-Pacific markets toward mandatory reductions in chemical pesticide application volumes, stricter maximum residue limits on fresh produce, and enforcement of integrated pest management requirements that prioritize targeted application over preventive broadcast treatment is creating a structural and compliance-driven demand for agri robotics whose precision application and individual plant-level targeting capabilities enable farmers to achieve regulatory compliance with pesticide reduction mandates while maintaining crop protection efficacy that broadcast reduction alone cannot achieve. The European Union’s Farm to Fork strategy mandates a 50% reduction in chemical pesticide use and risk by 2030, a regulatory target that is practically unachievable for most horticultural and specialty crop producers through dosage reduction on conventional broadcast spray equipment without unacceptable crop protection performance degradation, but is technically achievable through robotic spot application systems that apply pesticide only to detected disease or pest locations rather than the entire field area, effectively achieving the required 50% or greater reduction in total pesticide volume while maintaining the same crop protection outcome per treated plant. The growing adoption of integrated pest management practices incentivized through European Union agri-environment scheme payments, United States Department of Agriculture Environmental Quality Incentives Program funding, and organic certification price premiums is creating a commercial reward for precision pesticide application practices that agri robotics uniquely enables, making environmental compliance an economically positive driver of robotic adoption rather than a cost-only regulatory burden for farm operators who can access the premium markets and government payment programs associated with demonstrably reduced pesticide use.

Rapid Technology Cost Reduction in Computer Vision, Edge Computing, Battery Systems, and Lightweight Actuators Accelerating Agri Robot Commercial Viability Across an Expanding Range of Crop Tasks

The dramatic cost reduction and capability improvement in the enabling hardware and software technologies that underpin agricultural robotics is progressively closing the economic gap between robotic and human task completion across a widening range of agricultural applications, with computer vision system costs declining by approximately 65% between 2019 and 2025 as the agricultural adoption of industrial computer vision module architectures developed for automotive, logistics, and consumer electronics markets drives volume scale, while edge computing processing power available at agricultural machinery form factor and power budget has increased approximately eight-fold over the same period through the successive generations of neural network inference chips including NVIDIA Jetson, Google Edge TPU, and Hailo artificial intelligence accelerator modules. Battery energy density improvement from approximately 180 watt-hours per kilogram in 2018 to approximately 280 watt-hours per kilogram in 2025 for the lithium-ion battery formats applicable to ground-based agricultural robots is directly extending the continuous operating time of battery-powered field robots from approximately three to four hours to seven to ten hours per charge cycle, enabling robot work rates that cover commercially meaningful field areas per day without the diesel engine complexity, noise, and emissions of alternative power systems that complicate deployment in residential proximity horticultural production environments. Precision robotic actuator costs for the end-of-arm tooling, vision-guided positioning systems, and force feedback mechanisms required for delicate fruit and vegetable handling have declined from approximately USD 12,000 to USD 18,000 per robot arm assembly in 2020 to approximately USD 5,000 to USD 8,000 in 2025 as collaborative robot component manufacturing scale has expanded, reducing the capital cost per harvesting robot unit sufficiently to approach payback periods of three to five years at commercial farm labor cost benchmarks in North America and Northern Europe.

Key Challenges

Biological Variability, Unstructured Field Environment Complexity, and Crop Damage Risk Creating Persistent Technical and Commercial Reliability Barriers for Robotic Harvesting Systems

The fundamental technical challenge in agricultural robotics, and the primary reason why autonomous harvesting systems have proven substantially more difficult to commercialize than equivalent indoor logistics or manufacturing robots, is the extreme biological and environmental variability of living agricultural crops in field and greenhouse settings that generates an essentially infinite range of visual, mechanical, and spatial conditions that robotic systems must reliably navigate without damaging crop quality or inflicting unacceptable product loss rates. Fresh produce harvesting robots must identify and gently detach individual ripe fruits or vegetables from plants whose geometry, fruit positioning, occlusion by leaves and stems, color variation, and mechanical resistance to detachment vary continuously across plant growth stages, weather conditions, irrigation histories, and individual plant genetic variation in ways that create classification accuracy and mechanical interaction challenges that have resisted complete solution by current generation computer vision and robotic manipulation systems, with leading commercial strawberry harvesting robots achieving harvest efficiency rates of approximately 55% to 75% of manually harvestable yield at commercially acceptable damage rates, leaving 25% to 45% of ripe fruit undetected or undamaged for subsequent manual gleaning passes that reduce but do not eliminate the need for human labor in robotic harvesting operations. The reliability and uptime performance of agricultural robots in outdoor field environments is challenged by dust, mud, moisture, crop debris, and UV radiation exposure that accelerates component degradation, clogs sensors and actuators, and interrupts communications links in ways that require robust mechanical design, advanced sealing, and regular preventive maintenance routines whose complexity and cost add to the total ownership economics of robotic systems and require farm operators to develop new technical maintenance competencies that are not currently widespread in agricultural workforces.

High Capital Cost, Limited Access to Agricultural Finance, and Long Payback Periods Creating Adoption Barriers for Small and Medium Farm Operators Representing the Majority of Global Agricultural Landholding

The capital cost of commercially deployed agri robotic systems represents a substantial investment relative to the financial scale and credit access characteristics of the majority of global farm operators, with advanced specialty crop harvesting robots costing approximately USD 120,000 to USD 350,000 per unit, autonomous tractor upgrade packages for major row crop equipment priced at USD 25,000 to USD 75,000 per machine, and complete robotic milking installation for a 100-cow dairy unit costing approximately USD 220,000 to USD 380,000, creating upfront capital requirements that are prohibitive for the millions of small and medium-scale farm operations in developed economies who lack the balance sheet strength, collateral value, and credit history required to access the equipment financing or agricultural bank lending needed to acquire robotic systems at commercially available prices. Agricultural finance markets in most economies do not offer specific financing products adapted to the technology risk, maintenance uncertainty, and productivity improvement financing needs of first-generation agricultural robotic equipment, leaving farm operators to rely on general agricultural equipment lending, lease arrangements from equipment manufacturers, or government subsidy programs whose eligibility criteria and processing timelines create adoption friction that extends payback period uncertainty and reduces the effective return on robotic investment relative to financial model projections. The seasonality of agricultural cash flows, in which farm revenue is concentrated in post-harvest periods while capital expenditure commitment must precede the growing season, creates a cash flow mismatch for robotic system procurement that is particularly challenging for horticultural producers whose high-value crop revenues provide the financial basis for robotic investment justification but whose in-season capital liquidity constraints require flexible financing structures that most agricultural equipment manufacturers and lenders have not yet fully developed to serve the specific requirements of the agri robotics customer segment.

Regulatory Fragmentation, Drone Operational Restrictions, and Field Robot Safety Standards Gaps Creating Market Access Complexity and Liability Uncertainty Across International Deployment Geographies

The regulatory environment governing agricultural drone operation, autonomous ground vehicle field deployment, and robotic pesticide application is fragmented across national jurisdictions whose distinct operational category definitions, airspace authorization requirements, operator licensing frameworks, and agricultural drone exemption provisions create compliance complexity for international agri robotics companies seeking to market and deploy their systems across multiple countries simultaneously, with the harmonized regulatory standards that would enable a single certified system to be deployed globally absent from the agricultural robotics sector despite the existence of international aviation and ground vehicle safety standard frameworks that could provide the foundation for such harmonization. Agricultural drone operators in the European Union must comply with European Union Aviation Safety Agency open, specific, and certified category operational requirements that vary significantly from the United States Federal Aviation Administration Part 107 framework and the Civil Aviation Administration of China’s agricultural drone operational standards, requiring manufacturers and service providers to develop separate operational documentation, pilot training programs, and operational risk assessments for each major market, adding regulatory compliance cost of approximately USD 200,000 to USD 800,000 per new national market entry for fully compliant agricultural drone service certification. The absence of widely adopted safety performance standards for ground-based agricultural robots operating in proximity to human farm workers, particularly for autonomous tractors, field robots, and harvest platforms that share the agricultural workspace with people during field operations, creates product liability uncertainty for manufacturers and deployment risk concerns for farm operators that are inhibiting adoption in occupational health and safety-conscious markets including the European Union and Australia where worker safety regulations impose legal obligations on farm operators that autonomous equipment manufacturers have not yet provided clear safety certification evidence to satisfy.

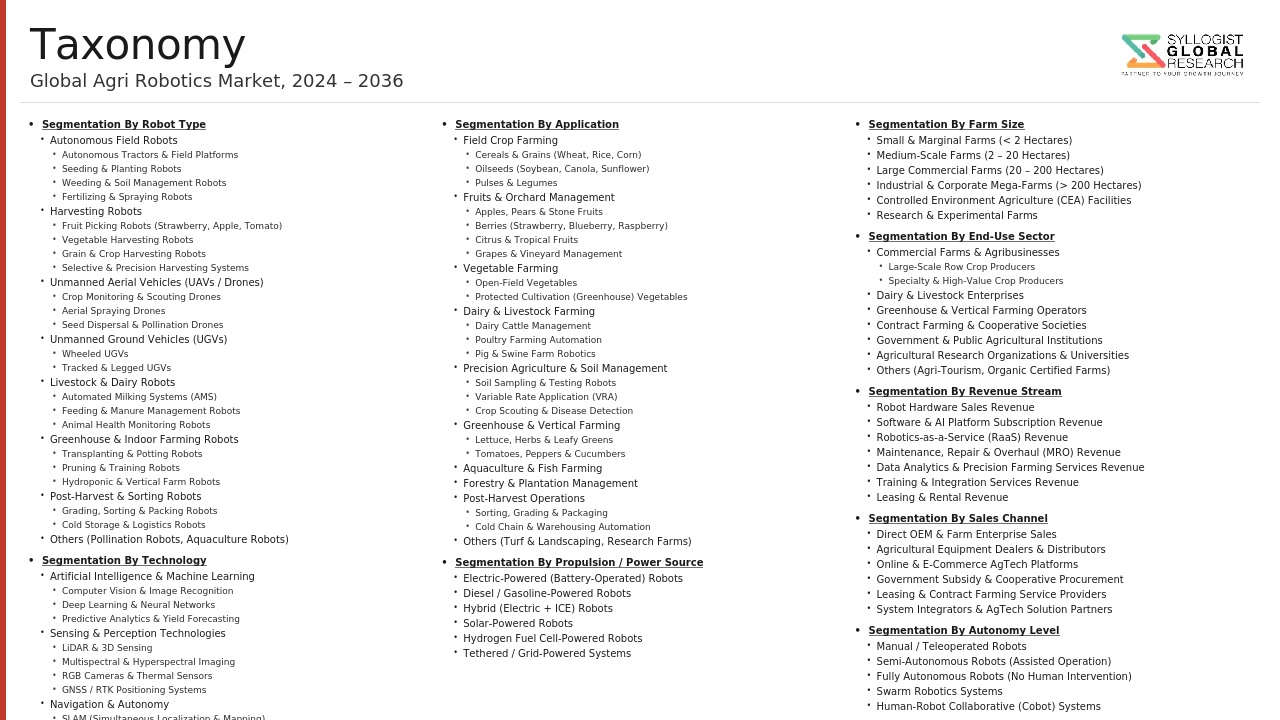

Market Segmentation

- Segmentation By Product Type

- Agricultural Drones and Unmanned Aerial Vehicles

- Autonomous Tractors and Orchard Platforms

- Robotic Harvesting Systems (Fruit, Vegetable, and Salad Crop)

- Robotic Weeding and Precision Cultivation Systems

- Robotic Milking and Livestock Management Systems

- Robotic Seeding and Transplanting Systems

- Precision Spraying and Fertilizing Robots

- Greenhouse and Controlled Environment Robotic Platforms

- Post-Harvest Sorting, Grading, and Packing Robots

- Robotic Soil Sampling and Analysis Systems

- Others

- Segmentation By Technology

- Computer Vision and Artificial Intelligence

- GPS and GNSS Precision Navigation

- LiDAR and Depth Sensing

- Multispectral and Hyperspectral Imaging

- Collaborative Robotics and Soft Gripper Actuators

- Internet of Things (IoT) and Farm Connectivity Platforms

- Swarm Robotics and Multi-Agent Coordination

- Others

- Segmentation By Application

- Planting and Seeding

- Crop Monitoring and Scouting

- Irrigation Management

- Spraying and Pesticide Application

- Weeding and Mechanical Cultivation

- Harvesting and Picking

- Soil Preparation and Tillage

- Post-Harvest Handling, Sorting, and Packaging

- Livestock Monitoring and Milking

- Others

- Segmentation By Crop Type

- Cereals and Grains (Wheat, Rice, Corn, and Soybean)

- Fruits (Apples, Strawberries, Blueberries, Citrus, and Grapes)

- Vegetables (Tomatoes, Peppers, Cucumbers, Lettuce, and Asparagus)

- Tree Nuts and Orchards

- Dairy and Livestock Farming

- Greenhouse and Controlled Environment Agriculture

- Others

- Segmentation By Farm Size

- Small-Scale Farms (Below 50 Hectares)

- Medium-Scale Farms (50 to 500 Hectares)

- Large-Scale and Corporate Farms (Above 500 Hectares)

- Cooperative and Contract Farming Entities

- Segmentation By Sales and Deployment Model

- Direct Equipment Sale and Purchase

- Robotics-as-a-Service (RaaS) and Subscription Models

- Contract Robotic Service Providers (Drone Application Services)

- Equipment Leasing and Financing

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Agri Robotics Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type including agricultural drones, autonomous tractors, robotic harvesting systems, weeding robots, robotic milking systems, precision spraying robots, and greenhouse platforms, by application including planting, crop monitoring, spraying, weeding, harvesting, and post-harvest handling, and by crop type including cereals, fruits, vegetables, tree nuts, and dairy, to enable agri robotics technology developers, agricultural machinery manufacturers, venture capital investors, farming cooperatives, large-scale farm operators, and agri-input companies to identify the highest-growth robot categories, application segments, and geographic markets generating the most commercially durable demand trajectories across the forecast period to 2034?

- What is the current commercial deployment scale, harvest efficiency rate relative to manual benchmarks, crop damage rate, capital cost per robot unit, operating cost per acre or per ton of harvested produce, projected payback period, and key technology development roadmap of leading specialty crop robotic harvesting systems for strawberries, apples, tomatoes, lettuce, and asparagus developed by technology innovators across North America, Europe, and Australia, and what specific technical performance thresholds in terms of fruit detection accuracy, picking rate, and damage rate must these systems achieve to generate payback periods below five years at prevailing specialty crop farm labor wage rates in the United States, Netherlands, Germany, and Australia, and how close are the leading commercial systems to achieving these performance thresholds at the scale and operational reliability required for mainstream farm operator adoption?

- How are agricultural drone regulatory frameworks including the European Union Aviation Safety Agency operational category standards, the United States Federal Aviation Administration Part 107 and Beyond Visual Line of Sight authorization programs, India’s Drone Rules 2021, China’s Civil Aviation Administration agricultural drone standards, and equivalent frameworks in Brazil, Australia, and Japan creating differentiated market access conditions, operational capability boundaries, and compliance cost structures across major agricultural drone markets, and what regulatory developments anticipated through 2034 including United States BVLOS rulemaking finalization, European Union specific category operational authorization standardization, and developing economy framework development are expected to accelerate or constrain agricultural drone deployment scale across commodity crop spraying, crop scouting, and precision fertilization application categories?

- How are the Robotics-as-a-Service subscription and pay-per-acre business models being deployed by agri robotics companies to reduce the upfront capital barrier for small and medium farm operators, what are the current service pricing levels, asset utilization rates, seasonal coverage capacity, and financial performance metrics of Robotics-as-a-Service deployment models in weeding, harvesting, and crop scouting robot categories, and how are agri robotics companies structuring their service delivery infrastructure including field service networks, operator training programs, remote monitoring capabilities, and performance guarantee frameworks to build the farm customer confidence and operational reliability evidence base required to accelerate Robotics-as-a-Service adoption beyond early innovator farms toward the mainstream farm operator market that represents the majority of total agricultural production volume and addressable market size?

- What are the technology development investment programs, product launch roadmaps, strategic partnership activities, and market positioning strategies of the leading global agri robotics companies across drone manufacturers including DJI Agriculture, XAG, and Yamaha Motor, autonomous tractor developers including John Deere, CNH Industrial, and AGCO, specialty crop harvesting robot companies, robotic milking system providers, and precision weeding robot developers, and how are established agricultural machinery manufacturers differentiating their robotics integration strategies from pure-play agri robotics startups in terms of distribution network leverage, farm customer relationship depth, dealer service infrastructure, precision agriculture data platform integration, and the ability to offer complete robotic farm management solutions versus single-task automation products that meet different points on the farm operator adoption readiness and financial capability spectrum?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology Maturity, Reliability & Field Performance Risk in Variable Agricultural Environments

- High Capital Cost, Farmer Adoption Barrier & Return on Investment Uncertainty Risk

- Agricultural Drone & Autonomous Vehicle Regulatory Approval & Airspace Management Risk

- Data Privacy, Farm Data Ownership, Cybersecurity & Connectivity Infrastructure Risk

- Labour Market Disruption, Social Acceptance & Just Transition Risk in Rural Agricultural Communities

- Regulatory Framework & Standards

- Agricultural Drone & UAV Regulation: FAA Part 107 (US), EU UAS Regulation (2019/947), DGCA RPAS Rules (India), CAAC UAV Rules (China) & National Airspace Management Frameworks

- Autonomous Agricultural Vehicle Safety & Functional Safety Standards: ISO 18497 (Agricultural Machinery Autonomous), IEC 61508, ISO 26262 Adaptation & ASABE Technical Standards

- Pesticide Application & Drone Spraying Regulations: EPA Label Compliance (US), EU Regulation 1107/2009, Machine-Specific Pesticide Registration & Aerial Application Permit Requirements

- Farm Data Governance, Agricultural Data Act (EU), GDPR Agricultural Data Application & National Precision Agriculture Data Ownership Policy Frameworks

- Agricultural Subsidy, Innovation Grant & Digital Agriculture Policy: EU CAP Digital Farm Incentive, USDA NRCS Conservation Technology Programme, India Digital Agriculture Mission & Japan Smart Agriculture Policy

- Global Agri Robotics Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Sold)

- Market Size & Forecast by Robot Type

- Autonomous Tractor & Field Navigation Robot

- Harvesting Robot (Fruit, Berry, Vegetable & Grain)

- Weeding & Mechanical Cultivation Robot

- Seeding, Planting & Transplanting Robot

- Crop Spraying & Precision Application Ground Robot

- Agricultural Drone & UAV (Aerial Imaging, Spraying & Mapping)

- Livestock Automation Robot (Robotic Milking, Feeding & Health Monitoring)

- Greenhouse & Indoor Farm Robot (Rail-Mounted, AMR & Gantry System)

- Post-Harvest Sorting, Grading & Packing Robot

- Soil Sampling, Sensing & In-Field Crop Monitoring Robot

- Market Size & Forecast by Technology

- Autonomous Navigation: GNSS/RTK, LiDAR & Sensor Fusion

- Computer Vision & AI-Based Crop & Weed Recognition

- Robotic Arm, Soft Gripper & Compliant End-Effector Technology

- Machine Learning, Predictive Analytics & Digital Farm Platform Integration

- Multispectral, Hyperspectral & Thermal Imaging Sensor Technology

- 5G, LoRaWAN, IoT Connectivity & Edge Computing for Field Robot Networks

- Market Size & Forecast by Propulsion & Power Source

- Battery Electric (Lithium-Ion & Next-Generation Battery)

- Diesel & Hybrid Powertrain

- Solar-Powered & Renewable Energy-Integrated

- Hydrogen Fuel Cell (Emerging)

- Market Size & Forecast by Application

- Crop Monitoring, Scouting, Field Mapping & Phenotyping

- Planting, Seeding & Transplanting

- Crop Protection: Spraying (Herbicide, Pesticide & Fungicide)

- Weeding, Mechanical Cultivation & Inter-Row Tillage

- Harvesting, Picking & Selective Yield Collection

- Post-Harvest Handling: Sorting, Grading, Packing & Storage

- Livestock Management: Milking, Feeding, Health Monitoring & Barn Cleaning

- Irrigation Management & Precision Fertigation

- Market Size & Forecast by Crop Type

- Fruits (Strawberry, Apple, Grape, Berry, Citrus & Stone Fruit)

- Vegetables (Tomato, Lettuce, Pepper, Cucumber & Leafy Greens)

- Field Crops (Wheat, Corn, Rice, Soybean & Cotton)

- Specialty & High-Value Crops (Herbs, Hops, Mushroom & Flowers)

- Livestock & Animal Husbandry (Dairy, Poultry, Swine & Beef Cattle)

- Market Size & Forecast by Farm Type

- Large-Scale Commercial & Corporate Farm

- Medium-Scale Family & Owner-Operated Farm

- Greenhouse & Controlled Environment Agriculture (CEA) Farm

- Vertical Farm & Indoor Hydroponic Operation

- Smallholder & Subsistence Farm (Emerging Market Adoption)

- Market Size & Forecast by End-User

- Commercial Farming Enterprise & Large Agribusiness

- Agricultural Cooperative & Farmer Group

- Greenhouse & Indoor Farm Operator

- Contract Farming & Managed Farm Service Provider

- Government Agricultural Programme & Public Research Farm

- Market Size & Forecast by Sales Channel

- Direct OEM Sale to Farm Operator

- Agricultural Equipment Dealer & Distributor Network

- AgTech Platform, Subscription & Robot-as-a-Service (RaaS) Channel

- Online B2B Platform & E-Commerce Channel

- North America Agri Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Robot Type

- By Technology

- By Application

- By Crop Type

- By Farm Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Agri Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Robot Type

- By Technology

- By Application

- By Crop Type

- By Farm Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Agri Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Robot Type

- By Technology

- By Application

- By Crop Type

- By Farm Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Agri Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Robot Type

- By Technology

- By Application

- By Crop Type

- By Farm Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Agri Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Robot Type

- By Technology

- By Application

- By Crop Type

- By Farm Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Agri Robotics Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold)

- By Robot Type

- By Technology

- By Application

- By Crop Type

- By Farm Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, Netherlands, Spain, Italy, United Kingdom, Belgium, Sweden, Japan, South Korea, China, India, Australia, New Zealand, Israel, Brazil, Argentina, Chile, South Africa, Mexico, UAE

- Technology Landscape & Innovation Analysis

- Harvesting Robot Arm, End-Effector, Soft Gripper & Force-Controlled Picking Technology Deep-Dive

- Autonomous Tractor, GNSS/RTK Field Navigation, Implement Control & Headland Management Technology

- Agricultural Drone (UAV): Multispectral Imaging, Variable-Rate Spraying, Swarm & BVLOS Technology

- Computer Vision, Deep Learning Crop Recognition, Disease Detection & Precision Phenotyping Technology

- Weeding Robot: Mechanical, Thermal, Laser & Micro-Targeted Micro-Herbicide Application Technology

- Livestock Automation: Robotic Milking System, Automated Feed Pusher & Animal Health Monitoring Technology

- Greenhouse & Indoor Farm Robot: Rail-Mounted Gantry, AMR Navigation & CEA Harvest Automation Technology

- Patent & IP Landscape in Agricultural Robotics Technologies

- Value Chain & Supply Chain Analysis

- Component Supply Chain: Actuator, Motor, Sensor, Camera, LiDAR & Battery Manufacturer Landscape

- Robotic Arm, End-Effector & Manipulator Specialist Supply Chain

- AI Chipset, Edge Computing Module & Embedded Vision Processor Supply Chain

- Agri Robot OEM Integrator, System Developer & Platform Company Landscape

- Agricultural Equipment Dealer, Distributor & Farm Machinery Retailer Channel

- Farmer, Agribusiness & Commercial Farm Operator Procurement & Adoption Channel

- Aftermarket Service, Repair, Spare Parts & Robot-as-a-Service (RaaS) Maintenance

- Pricing Analysis

- Harvesting Robot Average Selling Price (ASP) Analysis by Crop Type & Robot Throughput Capacity

- Autonomous Tractor & Field Navigation System Pricing vs. Conventional Tractor Upgrade Benchmark

- Agricultural Drone Pricing Analysis by Payload, Spray Tank Capacity & Intelligence Level

- Weeding Robot ASP Analysis by Working Width, Field Speed & Weed Control Technology Type

- Robotic Milking System Capital & Operating Cost Analysis vs. Conventional Milking Parlour Benchmark

- Robot-as-a-Service (RaaS) Subscription & Per-Hectare Service Fee Pricing Analysis vs. Outright Purchase Total Cost of Ownership

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Agri Robots: Carbon Footprint, Energy Intensity & Material Use vs. Conventional Farm Mechanisation

- Precision Application Co-Benefit: Chemical Input Reduction, Herbicide & Pesticide Use Minimisation & Soil Health Improvement from Robot-Based Spot Treatment

- Soil Compaction Reduction: Lightweight Robot Platform Environmental Benefit vs. Heavy Conventional Tractor in Field Crop Applications

- Labour Displacement, Rural Employment Impact & Just Transition: Social Sustainability of Agri Robotics Adoption in Developing & Developed Agricultural Economies

- Regulatory-Driven Sustainability: EU Farm to Fork Strategy, Green Deal Pesticide Reduction Target, USDA Climate-Smart Agriculture Initiative & SDG 2 (Zero Hunger) Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Robot Type & Application)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Robot Type, Crop Type & Geography

- Player Classification

- Global Diversified Agricultural Equipment OEM with Robotics & Automation Division

- Specialist Harvesting Robot & Picking Automation Company

- Autonomous Tractor & Field Navigation Technology Provider

- Agricultural Drone & UAV Manufacturer & Service Provider

- Weeding & Crop Protection Robot Specialist

- Livestock Automation & Robotic Milking System Manufacturer

- Greenhouse & Indoor Farm Automation & Robotics Specialist

- AgTech Platform, AI & Computer Vision Software Provider for Farm Robotics

- Competitive Analysis Frameworks

- Market Share Analysis by Robot Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Agri Robotics Products & Technology Portfolio

- Key Customer Relationships & Reference Farm Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Agri Robotics Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Field Trials, Commercial Deployments)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Robot Type, Technology, Application, Crop Type & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & Farmer Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)