Global Agrochemical Contract Manufacturing Market By Product Type, By Service Type, By Crop Type, By Formulation Type, By Mode of Application, By Contract Type, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Agrochemical Contract Manufacturing Market refers to the outsourced production of crop protection chemicals, plant nutrition products, and specialty agricultural inputs delivered by third-party manufacturers for agrochemical innovator companies, generic producers, and integrated agribusiness organizations. The market includes contract synthesis of active ingredients, formulation development, toll manufacturing of herbicides, insecticides, fungicides, plant growth regulators, biopesticides, seed treatment chemistries, and adjuvants, along with associated services covering chemical intermediate production, custom synthesis, packaging, regulatory dossier preparation, and process development support. The scope extends across contract manufacturing organizations operating multi-purpose chemical facilities, dedicated formulation plants, and integrated contract development and manufacturing organizations providing end-to-end commercialization services from laboratory-scale process development through validated commercial-scale production. The market covers organic chemistry, organometallic chemistry, agro-biological fermentation, microencapsulation technologies, and water-dispersible granule production processes that constitute the core technical platforms supplying global crop protection supply chains. End-user demand spans patent-protected innovator molecules requiring exclusive contract production, post-patent generic active ingredients sourced through competitive contract networks, and emerging biological and biorational chemistries that require specialized fermentation and formulation infrastructure. Geographically, the market encompasses production capacity located in North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa, with materials and finished products flowing through global agrochemical distribution networks serving cereals, oilseeds, fruits and vegetables, plantation crops, and turf and ornamental applications. The market further includes contract regulatory and quality compliance services supporting registration filings under EPA, EU, MAFF, and local agrochemical regulatory authorities across the global crop protection ecosystem.

Market Insights

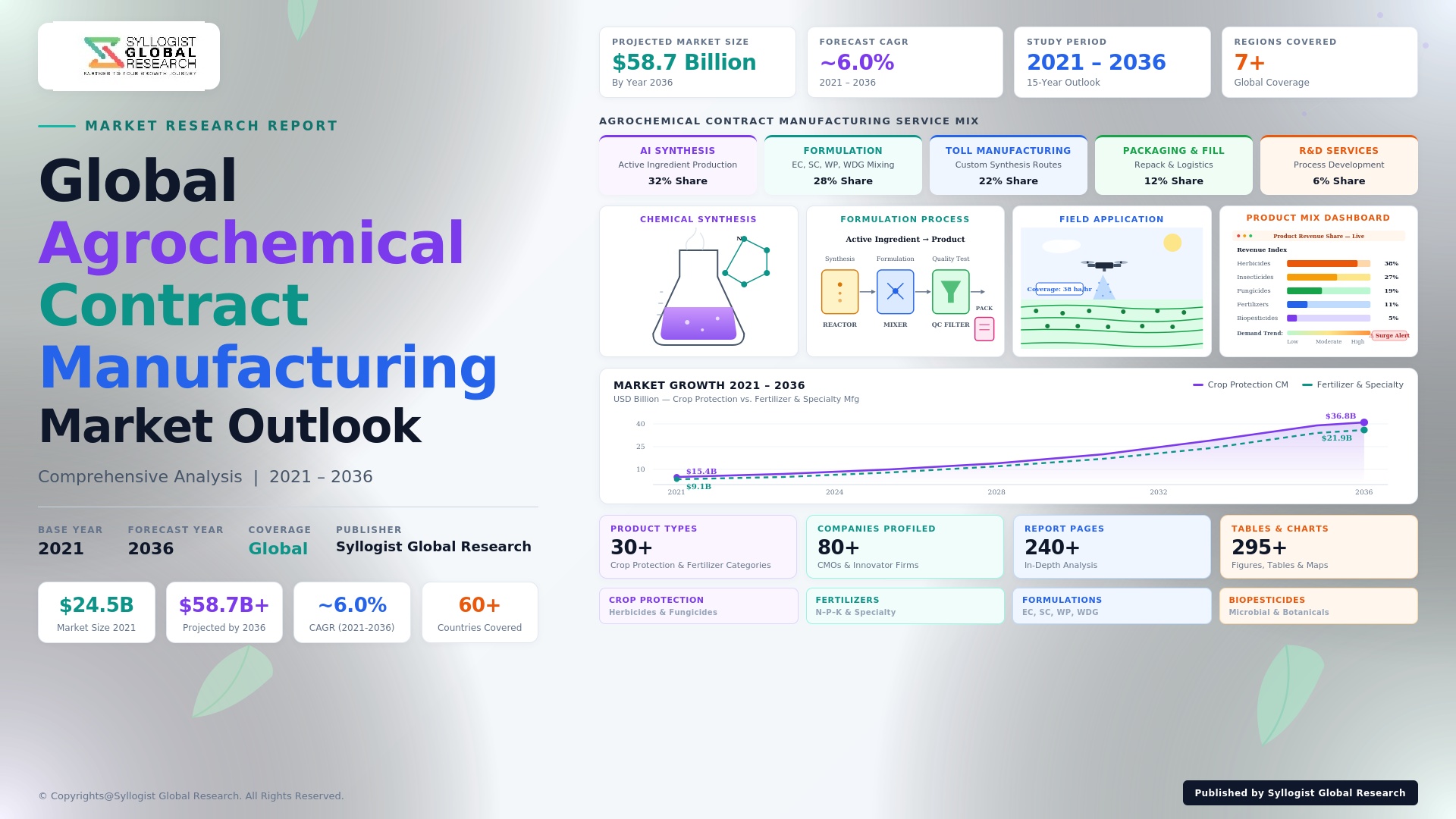

The global agrochemical contract manufacturing market has shifted from a peripheral capacity-balancing function into a central pillar of crop protection industry strategy, driven by the convergence of innovator portfolio rationalization, accelerating patent expirations across blockbuster active ingredients, and structural cost pressures compelling multinational agrochemical companies to monetize fixed manufacturing overhead through external production partnerships. The market was valued at USD 17.6 billion in 2025 and is projected to reach USD 33.8 billion by 2034, advancing at a compound annual growth rate of 7.5% across the forecast period, as innovator and generic agrochemical companies migrate progressively higher proportions of active ingredient synthesis, intermediate manufacturing, and finished formulation activity to specialized contract manufacturing partners with established regulatory track records and proven process safety credentials.

Asia-Pacific has consolidated its position as the dominant global hub for agrochemical contract manufacturing, with India and China collectively accounting for over 65% of global outsourced active ingredient production capacity, supported by mature fine chemistry ecosystems, integrated intermediate supply chains, and substantial cost advantages relative to comparable Western European and North American facilities. Indian contract manufacturers have advanced materially up the technical complexity curve, transitioning from low-margin generic synthesis into custom synthesis of patented intermediates, late-stage process development partnerships, and exclusive supply agreements with global innovators including Syngenta, Bayer Crop Science, FMC, and Corteva Agriscience. The China Plus One sourcing strategy adopted by global agrochemical purchasers in response to Chinese environmental shutdowns, energy curtailments, and geopolitical risk recalibration has materially redirected new outsourcing volumes toward Indian contract manufacturing operators with multi-purpose facilities, regulatory accreditation, and process safety performance meeting global pharmaceutical and agrochemical industry standards.

Innovator agrochemical companies are pursuing structural asset-light operating models, divesting captive intermediate production facilities, exiting non-strategic active ingredient manufacturing, and channeling capital previously committed to fixed manufacturing infrastructure toward research and development of new chemistry platforms, biological crop protection products, and digital agriculture capabilities. This portfolio rebalancing has created durable contract manufacturing demand for both proprietary patented molecules requiring exclusive supply arrangements and post-patent active ingredients moving into competitive generic production. Custom synthesis arrangements covering exclusive intermediate manufacturing, late-stage process intensification, and contract development partnerships now represent the highest-margin segment of the contract manufacturing market, with leading specialized providers such as PI Industries, SRF Limited, Hikal, and Heranba Industries operating multi-year exclusivity agreements with innovator companies covering single molecules through full life-cycle commercial production volumes.

The accelerating commercialization of biological crop protection products, biorational chemistries, and microbial inoculants is generating a structurally distinct contract manufacturing demand stream centered on fermentation infrastructure, downstream bioprocessing capability, and specialized formulation technologies that traditional agrochemical contract manufacturers must build through capital investment or strategic partnership. Environmental, social, and governance considerations are simultaneously reshaping global supplier selection, with multinational purchasers prioritizing contract manufacturing partners demonstrating credible decarbonization roadmaps, zero liquid discharge implementation, hazardous waste minimization, and process safety performance comparable with international chemical industry benchmarks. Regulatory tightening across the European Union under the Sustainable Use Regulation, evolving United States Environmental Protection Agency registration review timelines, and progressive Maximum Residue Limit harmonization across importing markets are concurrently elevating the technical, regulatory, and quality compliance bar required to participate in global agrochemical contract manufacturing supply chains.

Key Drivers

Patent Expirations of Major Active Ingredients Driving Generic Manufacturing Outsourcing Volumes

The forthcoming patent expiration cycle covering several blockbuster active ingredients with global revenue contributions exceeding USD 1 billion each is creating a structural pipeline of post-patent molecules transitioning into competitive generic production, with manufacturing volumes flowing predominantly to specialized contract operators in India and China possessing established multi-step organic synthesis capability, comprehensive regulatory documentation infrastructure, and demonstrated capacity to deliver active ingredient supply at the cost benchmarks demanded by global generic agrochemical purchasers and private-label distribution channels.

Asset-Light Operating Models Among Innovator Agrochemical Companies Accelerating Outsourced Manufacturing Adoption

Multinational innovator agrochemical companies are systematically divesting captive intermediate facilities and rationalizing fixed manufacturing footprints to redeploy capital toward research and development, biological crop protection acquisitions, and digital agriculture platform investment, generating durable demand for contract manufacturing partners capable of operating exclusive long-term supply arrangements covering proprietary chemistries, intermediate stages, and finished formulation production with full process safety, environmental, and quality compliance accountability transferred to the contract operator.

China Plus One Sourcing Diversification Redirecting Volumes Toward Indian Contract Manufacturing Capacity

Sustained Chinese environmental enforcement shutdowns, periodic energy curtailments affecting fine chemistry clusters, and progressive geopolitical risk recalibration among global agrochemical purchasers are redirecting incremental outsourcing volumes toward Indian contract manufacturing operators with multi-purpose facilities, robust regulatory documentation, and demonstrated capability to support global innovator and generic supply requirements at scale, with several Indian operators progressing into custom synthesis partnerships covering proprietary intermediates and exclusive late-stage active ingredient supply contracts.

Key Challenges

Tightening Global Regulatory Frameworks and Active Ingredient Re-Registration Cycles Increasing Compliance Cost Burdens

The progressive tightening of agrochemical registration frameworks across the European Union, United States Environmental Protection Agency, and major Asian regulatory authorities, including the introduction of cut-off criteria, endocrine disruptor screening requirements, and accelerated re-registration cycles covering legacy active ingredients, is increasing compliance, dossier maintenance, and analytical method validation costs across the contract manufacturing supply chain, with smaller regional operators facing disproportionate cost pressure and progressive consolidation toward larger compliance-mature contract platforms.

Raw Material Volatility, Intermediate Supply Concentration Risks, and Energy Cost Pressures Compressing Contract Manufacturing Margins

Concentrated upstream supply of key chemical intermediates within Chinese chemistry clusters, periodic disruptions to phosphorus, chlorine, and aromatic intermediate availability, and structural energy cost increases across European chemical production zones are introducing material volatility into contract manufacturing input cost structures, compressing operating margins and creating significant working capital pressure on contract operators required to absorb intermediate price escalation under fixed-price multi-year supply agreements with global agrochemical purchasers.

Environmental, Social, and Governance Compliance Requirements and Hazardous Waste Management Cost Escalation

Multinational agrochemical purchasers are progressively elevating environmental, social, and governance audit standards applicable to contract manufacturing partners, requiring documented decarbonization roadmaps, zero liquid discharge implementation, comprehensive hazardous waste tracking, and verifiable process safety performance, with non-compliant operators facing exclusion from preferred supplier rosters and material loss of access to high-value innovator and exclusive supply agreements that increasingly constitute the most profitable contract manufacturing revenue category globally.

Market Segmentation

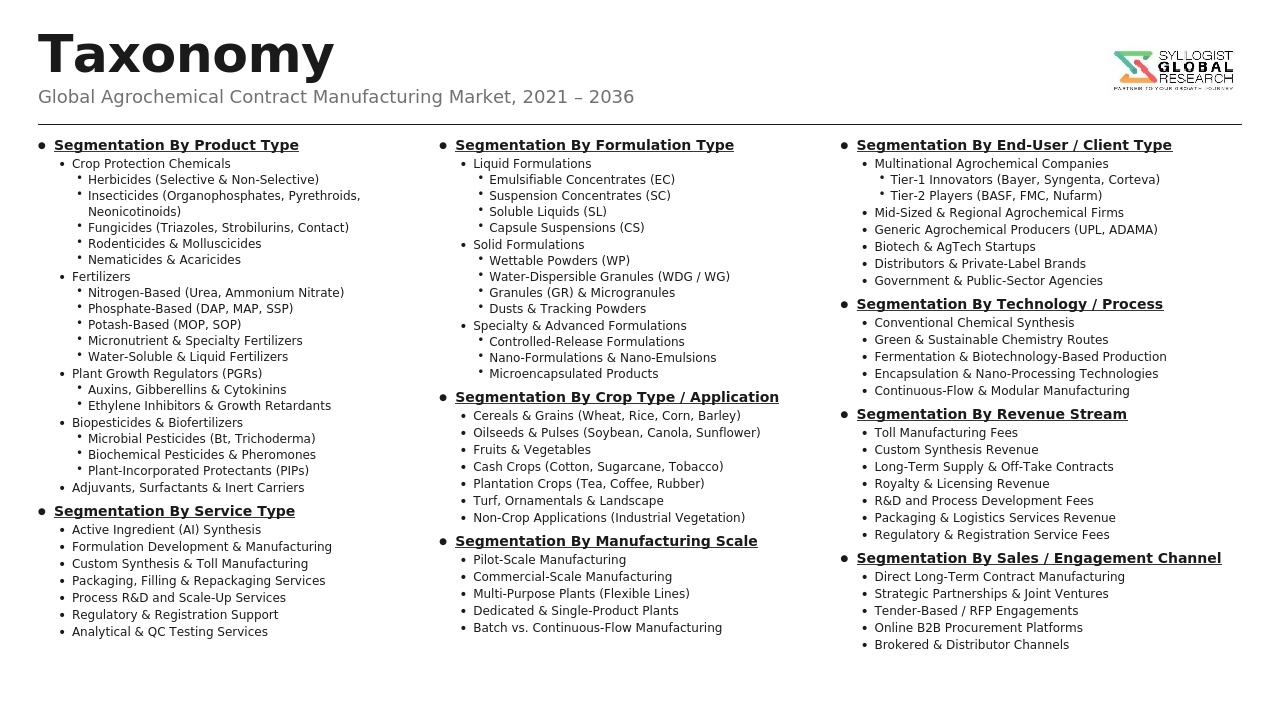

- Segmentation By Product Type

- Herbicides

- Insecticides

- Fungicides

- Biopesticides and Biocontrol Products

- Plant Growth Regulators

- Adjuvants and Surfactants

- Others

- Segmentation By Service Type

- Active Ingredient (AI) Synthesis

- Formulation Manufacturing

- Intermediate Manufacturing

- Custom Synthesis and Process Development

- Packaging and Filling Services

- Regulatory and Dossier Support Services

- Others

- Segmentation By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Plantation and Commercial Crops

- Turf and Ornamentals

- Others

- Segmentation By Formulation Type

- Liquid Formulations (EC, SC, SL)

- Solid and Powder Formulations (WP, WG)

- Granular Formulations (GR)

- Microencapsulated Formulations (CS)

- Suspension Concentrate and Oil Dispersion Formulations

- Others

- Segmentation By Mode of Application

- Foliar Spray

- Soil Treatment

- Seed Treatment

- Post-Harvest Treatment

- Others

- Segmentation By Contract Type

- Custom Synthesis Contracts

- Toll Manufacturing Contracts

- Long-Term Exclusive Supply Agreements

- Spot and Short-Term Manufacturing Contracts

- Segmentation By End User

- Multinational Innovator Agrochemical Companies

- Generic Agrochemical Producers

- Regional and Specialty Agrochemical Companies

- Biotech, Bioscience, and Biological Crop Protection Firms

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Agrochemical Contract Manufacturing Market in 2025, projected through 2034, disaggregated by product type, service type, and region, enabling contract manufacturers, innovator agrochemical companies, generic producers, and private equity investors to identify the highest-growth subsegments and most durable revenue opportunities across the global crop protection outsourcing landscape?

- How are India and China structurally positioning themselves within the global agrochemical contract manufacturing supply chain, what specific cost, regulatory, environmental enforcement, and technical capability factors are influencing innovator and generic purchaser sourcing decisions, and which Indian and Chinese contract operators are emerging as preferred long-term partners under China Plus One diversification strategies?

- Which active ingredient categories, including herbicides, insecticides, fungicides, biopesticides, and plant growth regulators, are generating the highest contract manufacturing growth rates through 2034, and what process chemistry, formulation, and quality compliance capabilities are most critical to securing innovator and generic supply contracts within each category?

- How are leading agrochemical innovator companies including Syngenta, Bayer Crop Science, BASF, Corteva Agriscience, FMC, and ADAMA structuring their contract manufacturing partnerships, exclusive supply agreements, and custom synthesis collaborations, and which contract operators are securing the largest share of high-margin proprietary and exclusive manufacturing volumes?

- What regulatory and registration framework changes across the European Union Sustainable Use Regulation, United States EPA registration review, and major Asian agrochemical regulatory authorities are most materially impacting contract manufacturing operating costs, supplier qualification timelines, and the ability of regional operators to compete for global innovator and generic contracts?

- How is the structural shift toward biological crop protection products, biorational chemistries, and microbial inoculants reshaping contract manufacturing capability requirements, and which contract operators are securing leading positions in fermentation-based active ingredient production, downstream bioprocessing, and specialized biological formulation technologies?

- What environmental, social, and governance benchmarks, decarbonization expectations, zero liquid discharge requirements, and hazardous waste management standards are global agrochemical purchasers applying to contract manufacturing supplier selection, and how are these requirements reshaping the competitive landscape between large compliance-mature contract platforms and smaller regional operators?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Active Ingredient Supply, Raw Material Volatility & Feedstock Concentration Risk

- Regulatory Compliance, Pesticide Registration & MRL Harmonisation Risk

- Manufacturing Quality, Cross-Contamination & GMP Compliance Risk

- Intellectual Property, Patent Cliff & Generic Competition Risk

- Geopolitical, Trade Policy & Cross-Border Sourcing Risk

- Regulatory Framework & Standards

- Pesticide Registration, EPA, EU REACH & National Agrochemical Approval Frameworks

- Good Manufacturing Practice (GMP), ISO Standards & Quality Management for Agrochemical Production

- Worker Safety, Occupational Exposure & Industrial Hygiene Regulations for Agrochemical Manufacturing

- Environmental, Effluent Discharge & Hazardous Waste Disposal Regulations for Agrochemical Plants

- Hazardous Material Transport, Packaging, Labeling & GHS Classification Standards

- Global Agrochemical Contract Manufacturing Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Tonnes and Kilolitres)

- Market Size & Forecast by Service Type

- Active Ingredient (Technical Grade) Synthesis & Manufacturing

- Formulation Development & Toll Manufacturing

- Packaging, Repackaging & Private-Label Filling Services

- Process Research, Scale-Up & Pilot Production Services

- Analytical Testing, Quality Control & Stability Studies Services

- Regulatory Affairs, Dossier Preparation & Registration Support Services

- Custom Synthesis & Intermediate Manufacturing Services

- End-to-End Integrated Contract Manufacturing & Outsourcing Solutions

- Market Size & Forecast by Product Type

- Herbicides (Selective, Non-Selective & Broad-Spectrum)

- Insecticides (Synthetic, Biological & Microbial-Based)

- Fungicides (Contact, Systemic & Seed Treatment)

- Plant Growth Regulators & Crop Protection Adjuvants

- Fertilizers (Specialty, Micronutrient & Water-Soluble)

- Biopesticides, Biostimulants & Biocontrol Agents

- Seed Treatment Chemicals & Coatings

- Public Health & Vector-Control Agrochemicals

- Market Size & Forecast by Formulation Type

- Liquid Formulations (Emulsifiable Concentrate, Suspension Concentrate & Soluble Liquid)

- Solid Formulations (Wettable Powder, Water-Dispersible Granule & Soluble Granule)

- Granular Formulations (Microgranule, Macrogranule & Coated Granule)

- Aerosol, Spray & Pressurised Container Formulations

- Microencapsulated, Controlled-Release & Nano-Formulations

- Market Size & Forecast by Crop Application

- Cereals & Grains (Wheat, Rice, Corn & Barley)

- Oilseeds & Pulses (Soybean, Canola, Cotton & Pulses)

- Fruits & Vegetables (Pome, Stone, Citrus, Leafy & Solanaceous)

- Plantation Crops (Sugarcane, Tea, Coffee, Rubber & Cocoa)

- Turf, Ornamental & Non-Crop Applications

- Market Size & Forecast by End-User

- Multinational Agrochemical Innovator Companies

- Regional & Generic Agrochemical Companies

- Specialty Crop Protection & Biological Solutions Companies

- Fertilizer & Specialty Plant Nutrition Companies

- Distributors, Private-Label Brands & Cooperatives

- Market Size & Forecast by Sales Channel

- Long-Term Strategic Manufacturing Partnership & Master Service Agreement

- Project-Based Toll Manufacturing & Custom Synthesis Contract

- Build-Operate-Transfer (BOT) & Dedicated Capacity Arrangement

- Direct Spot Procurement & Tender-Based Manufacturing Contract

- North America Agrochemical Contract Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes and Kilolitres)

- By Service Type

- By Product Type

- By Formulation Type

- By Crop Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Agrochemical Contract Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes and Kilolitres)

- By Service Type

- By Product Type

- By Formulation Type

- By Crop Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Agrochemical Contract Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes and Kilolitres)

- By Service Type

- By Product Type

- By Formulation Type

- By Crop Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Agrochemical Contract Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes and Kilolitres)

- By Service Type

- By Product Type

- By Formulation Type

- By Crop Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Agrochemical Contract Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes and Kilolitres)

- By Service Type

- By Product Type

- By Formulation Type

- By Crop Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Agrochemical Contract Manufacturing Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes and Kilolitres)

- By Service Type

- By Product Type

- By Formulation Type

- By Crop Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Active Ingredient Synthesis Process Technology Deep-Dive

- Continuous Flow Chemistry & Process Intensification Technology

- Green Chemistry, Solvent Recovery & Sustainable Synthesis Technology

- Microencapsulation, Controlled Release & Nano-Formulation Technology

- Biotechnology, Fermentation & Microbial Production Technology for Biopesticides

- Process Analytical Technology (PAT) & Real-Time Quality Monitoring

- Automation, Robotics & Industry 4.0 Technology in Agrochemical Plants

- Patent & IP Landscape in Agrochemical Contract Manufacturing Technologies

- Value Chain & Supply Chain Analysis

- Active Ingredient Intermediate & Building-Block Chemical Supply Chain

- Solvent, Adjuvant, Surfactant & Inert Carrier Supply Chain

- Packaging Material (Drum, IBC, Pouch & Bottle) & Closure Supply Chain

- Manufacturing Equipment, Reactor & Process Skid Supply Chain

- Logistics, Cold-Chain & Hazardous Material Transport Channel

- Distributor, Agent & Off-Take Partner Channel

- Hazardous Waste Treatment, Effluent Disposal & Circular Economy

- Pricing Analysis

- Active Ingredient Synthesis Toll Manufacturing Cost & Margin Analysis

- Formulation & Toll Filling Service Pricing Benchmark

- Custom Synthesis & Process Development Project Cost Analysis

- Packaging, Repackaging & Private-Label Service Pricing Analysis

- Long-Term Partnership vs. Spot Manufacturing Contract Pricing Comparison

- Total Landed Cost & Outsourcing vs. In-House Production Economic Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Agrochemical Manufacturing: Carbon Footprint, Energy & Water Intensity Across Process Routes

- Green Chemistry, Solvent Reduction & Atom-Economy Pathways in Active Ingredient Synthesis

- Hazardous Waste Minimisation, Effluent Treatment & Circular Solvent Recovery in Agrochemical Plants

- Worker Safety, Occupational Exposure Limits & Community Health Impact Considerations

- Regulatory-Driven Sustainability, EU Farm-to-Fork & SDG 12 (Responsible Production) Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Service Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Service Type, Product Type & Geography

- Player Classification

- Integrated Multinational Agrochemical Manufacturers with Toll Manufacturing Capacity

- Specialist Custom Synthesis & Active Ingredient Contract Manufacturers

- Formulation, Toll Filling & Packaging Specialist CMOs

- Biopesticide, Biological & Fermentation-Based Contract Manufacturers

- Generic & Off-Patent Agrochemical Contract Manufacturers

- Regional & Emerging-Market Agrochemical CMOs

- Specialty Chemicals Companies Diversifying into Agrochemical Contract Manufacturing

- Independent Process Development & Pilot Manufacturing Service Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Service Type, Product Type & Region

- Company Profile

- Company Overview & Headquarters

- Agrochemical Contract Manufacturing Services & Capability Portfolio

- Key Customer Relationships & Reference Manufacturing Programs

- Manufacturing Footprint & Production Capacity

- Revenue (Agrochemical Contract Manufacturing Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Capability Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Service Type, Product Type, Crop Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output