Global Farm Advisory Platforms Market By Platform Type, By Delivery Mode, By Component, By Deployment, By Pricing Model, By Crop Type, By Farm Size, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Farm Advisory Platforms Market encompasses the design, deployment, and operation of digital platforms, software-as-a-service applications, and integrated data services that deliver crop-specific, livestock-specific, and farm-level decision-support recommendations to farmers, agribusinesses, cooperatives, and rural enterprises. The market covers crop advisory systems, soil and nutrient management platforms, pest and disease detection and forecasting solutions, irrigation and water-use advisory tools, weather and climate-risk advisory services, market price intelligence applications, livestock health and feed-management advisory platforms, and integrated farm management systems that unify agronomy, financial, and operational data within a single digital workflow. The scope includes platform-as-a-service offerings hosted on public, private, and hybrid cloud architectures, embedded analytics modules delivered through smartphone applications, voice-enabled and SMS-based services tailored to low-bandwidth rural users, IoT-integrated platforms drawing data from sensors, drones, and farm machinery, and outcome-linked advisory models that bundle recommendations with input supply, credit, or crop insurance. End users include individual smallholder and commercial farmers, farmer producer organizations, agricultural input manufacturers, food and beverage supply chains, agri-finance and insurance providers, retail aggregators, and public-sector extension agencies. The market includes standalone advisory platforms operated by independent agritech firms and embedded advisory modules offered by seed, crop protection, fertilizer, farm machinery, and digital agriculture majors as part of their broader product portfolios. Revenue streams comprise subscription and SaaS fees, transaction-based commissions, advisory service charges, data licensing fees, and outcome-based revenue sharing arrangements across North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa.

Market Insights

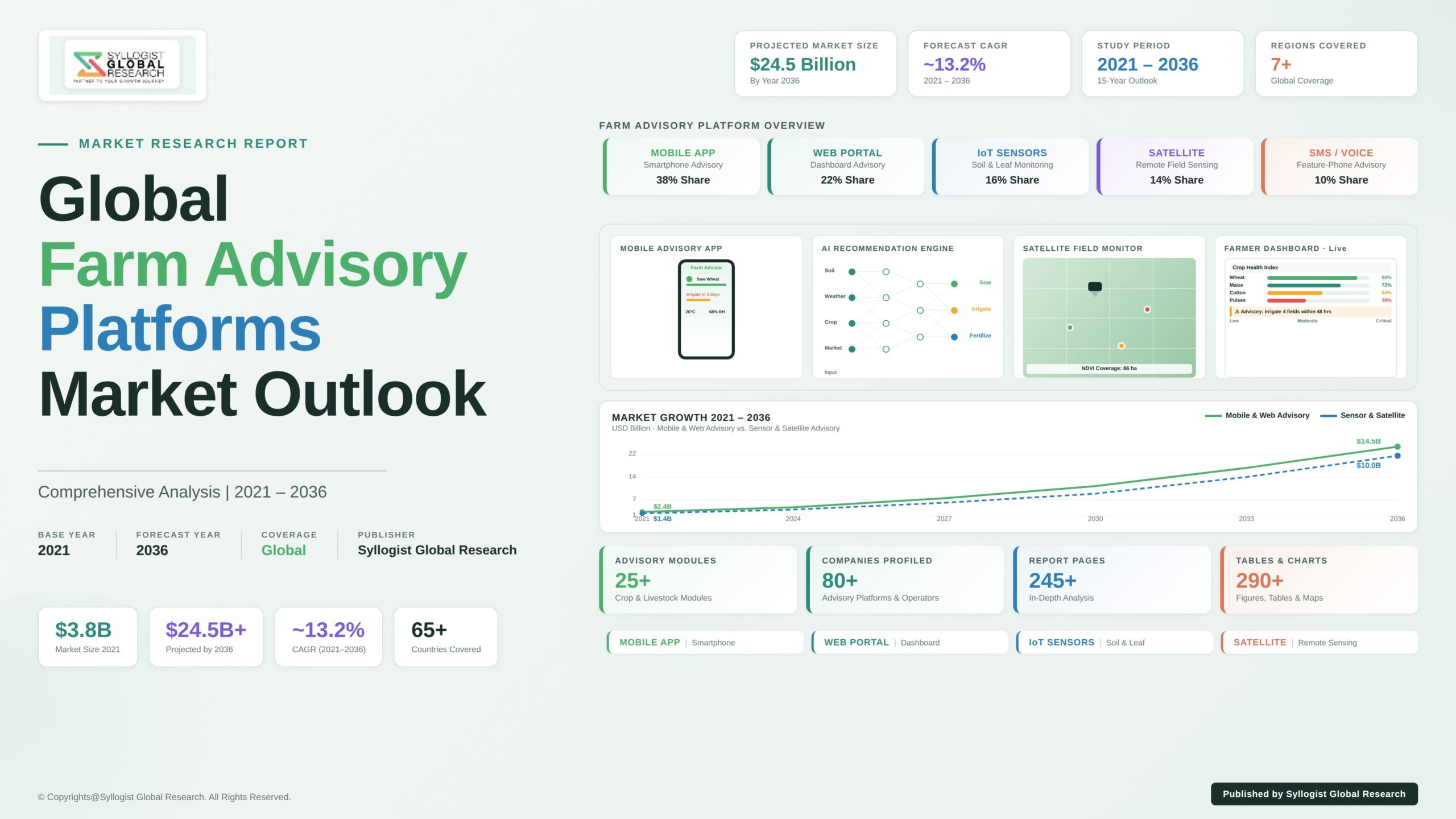

The global farm advisory platforms market is approaching a structural inflection point, shaped by accelerating climate volatility, the proliferation of low-cost smartphones across rural geographies, and rising farmer demand for data-driven recommendations that reduce input waste, improve yield outcomes, and stabilize farm-level economics in increasingly unpredictable growing conditions. The market was valued at approximately USD 3.42 billion in 2025 and is projected to reach USD 11.27 billion by 2034, advancing at a compound annual growth rate of 14.2% through the forecast period, as digital advisory platforms transition from pilot deployments into mainstream adoption across smallholder, mid-size, and large commercial farming operations spanning cereals, horticulture, plantation crops, and livestock value chains.

The strategic imperatives shaping this acceleration are reinforced by intensifying climate-related crop losses, where unseasonal rainfall, prolonged dry spells, heat stress, and emerging pest pressures have compressed planning windows and elevated the value of timely, location-specific agronomic advice that traditional extension systems are structurally unequipped to deliver at scale. Governments across India, Brazil, Indonesia, Nigeria, Kenya, and the European Union are channeling sustained policy support and direct subsidies into national digital agriculture missions, farmer registries, and unified digital agriculture stacks that lower the platform onboarding cost for downstream advisory providers. Global crop input majors and farm machinery OEMs are simultaneously expanding their proprietary farm advisory ecosystems, reshaping the competitive landscape through embedded advisory bundling, outcome guarantees, and integration with seed, crop protection, fertilizer, and financing products.

The integrated farm management platforms segment, which unifies agronomy advisory, machinery telematics, financial recordkeeping, and traceability within a single digital workflow, is the fastest-growing category within the global farm advisory platforms market, driven by rising farmer expectations for unified decision-making interfaces and platform stickiness among commercial growers managing complex multi-crop, multi-plot operations. Pest and disease detection platforms leveraging smartphone-based image recognition, AI-driven diagnostic engines, and crowd-sourced reporting represent among the most commercially dynamic sub-segments of the global farm advisory platforms market, attracting strong investment from venture capital, strategic crop protection partners, and impact-oriented agri-finance institutions. Mobile-first and voice-enabled advisory delivery, including IVR, SMS, vernacular-language chatbots, and short video formats, is rapidly emerging as the dominant delivery mode in Asia-Pacific, Africa, and Latin America.

Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, underpinned by sustained farm advisory platforms market investment in India, China, Indonesia, Vietnam, and the Philippines, each driven by smallholder digitization priorities, climate adaptation imperatives, and rising agri-input cost pressures. North America maintains its position as the largest absolute revenue market by farm advisory platform spending, with United States and Canadian commercial growers providing unmatched per-farm SaaS subscription value, advanced agronomy data integration, and prescription-based input management adoption. Europe represents the third major regional market, with EU Common Agricultural Policy reforms, sustainability and traceability mandates, and carbon-credit accounting requirements driving materially accelerated farm advisory platforms market procurement across France, Germany, the Netherlands, Italy, and Spain, while Latin America, particularly Brazil and Argentina, anchors strong commercial farm advisory adoption tied to large-scale soybean, maize, and sugarcane operations, and Middle East and Africa is gaining traction through food security programs, irrigation modernization, and donor-funded smallholder advisory deployments across Kenya, Egypt, Morocco, Saudi Arabia, and Nigeria.

Key Drivers

Climate Volatility, Yield Risk, and Resource-Efficiency Imperatives Driving Sustained Adoption of Data-Backed Farm Advisory Platforms

Intensifying climate variability, unseasonal rainfall, and rising pest pressure are compressing crop-planning windows and creating durable demand for timely, location-specific agronomic recommendations across the farm advisory platforms market. Farmers managing yield volatility, water restrictions, and input cost inflation are adopting subscription and embedded advisory platforms that deliver actionable irrigation, fertilizer, and pest-management decisions, supporting multi-year renewal economics across smallholder and commercial segments.

Smartphone Penetration, Vernacular Mobile Interfaces, and National Digital Agriculture Missions Accelerating Last-Mile Advisory Platform Reach

Rapid rural smartphone penetration, vernacular voice and IVR interfaces, and government-led digital agriculture missions in India, Brazil, Indonesia, Kenya, Nigeria, and the European Union are dismantling the last-mile barrier that historically constrained farm advisory platforms market adoption. Unified farmer registries, e-extension portals, and benefit-transfer-linked advisory bundles are lowering acquisition costs for platform operators while expanding the addressable smallholder pool by hundreds of millions of farmers.

Input Cost Inflation, Sustainability Mandates, and Embedded Advisory Bundling by Crop Input Majors Generating Structural Demand Tailwinds

Persistent input cost inflation across fertilizer, crop protection, and seed, combined with retailer-led sustainability mandates, carbon-accounting requirements, and outcome-linked supply contracts, is reshaping the economics of farm advisory adoption across commercial and smallholder operations. Crop input majors and farm machinery OEMs are bundling proprietary advisory platforms with seed, fertilizer, and equipment sales, embedding advisory consumption into procurement workflows and creating durable, contract-anchored revenue pools.

Key Challenges

Last-Mile Connectivity Gaps, Smallholder Digital Literacy, and Trust Deficit Constraining Platform Uptake in Emerging Markets

Inconsistent rural broadband, limited smartphone affordability among marginal smallholders, vernacular content gaps, and persistent trust deficits in algorithmic recommendations continue to constrain farm advisory platforms market adoption across emerging geographies. Farmers accustomed to in-person extension officers, peer networks, and locally calibrated traditional knowledge often discount generic, non-localized advice, limiting recommendation uptake, retention, and the unit economics of free-to-farmer advisory models.

Fragmented Agronomy Data, Interoperability Gaps, and Integration Complexity Across Farm Equipment, Sensors, and Legacy Farm Management Systems

The farm advisory platforms market faces structural friction from fragmented agronomy datasets, inconsistent soil and yield records, restrictive farm equipment data-sharing policies, and limited interoperability between competing farm management systems. Platform developers building integrated workflows confront prolonged integration cycles with planter, sprayer, and harvester telematics, soil-test laboratories, and remote-sensing data vendors, elevating engineering costs and constraining the depth of data-driven personalization.

Subscription Willingness-to-Pay, Monetization Headwinds, and Unit Economics Pressure on Free-to-Farmer Advisory Models

Smallholder willingness to pay for standalone advisory subscriptions remains limited across emerging markets, with most farmers preferring advisory consumption bundled with inputs, credit, or output procurement rather than direct subscription payments. Free-to-farmer advisory models supported by venture funding or agribusiness sponsorship frequently face elevated customer acquisition costs, modest engagement-to-monetization conversion, and sustained pressure on long-term commercialization economics within the farm advisory platforms market.

Market Segmentation

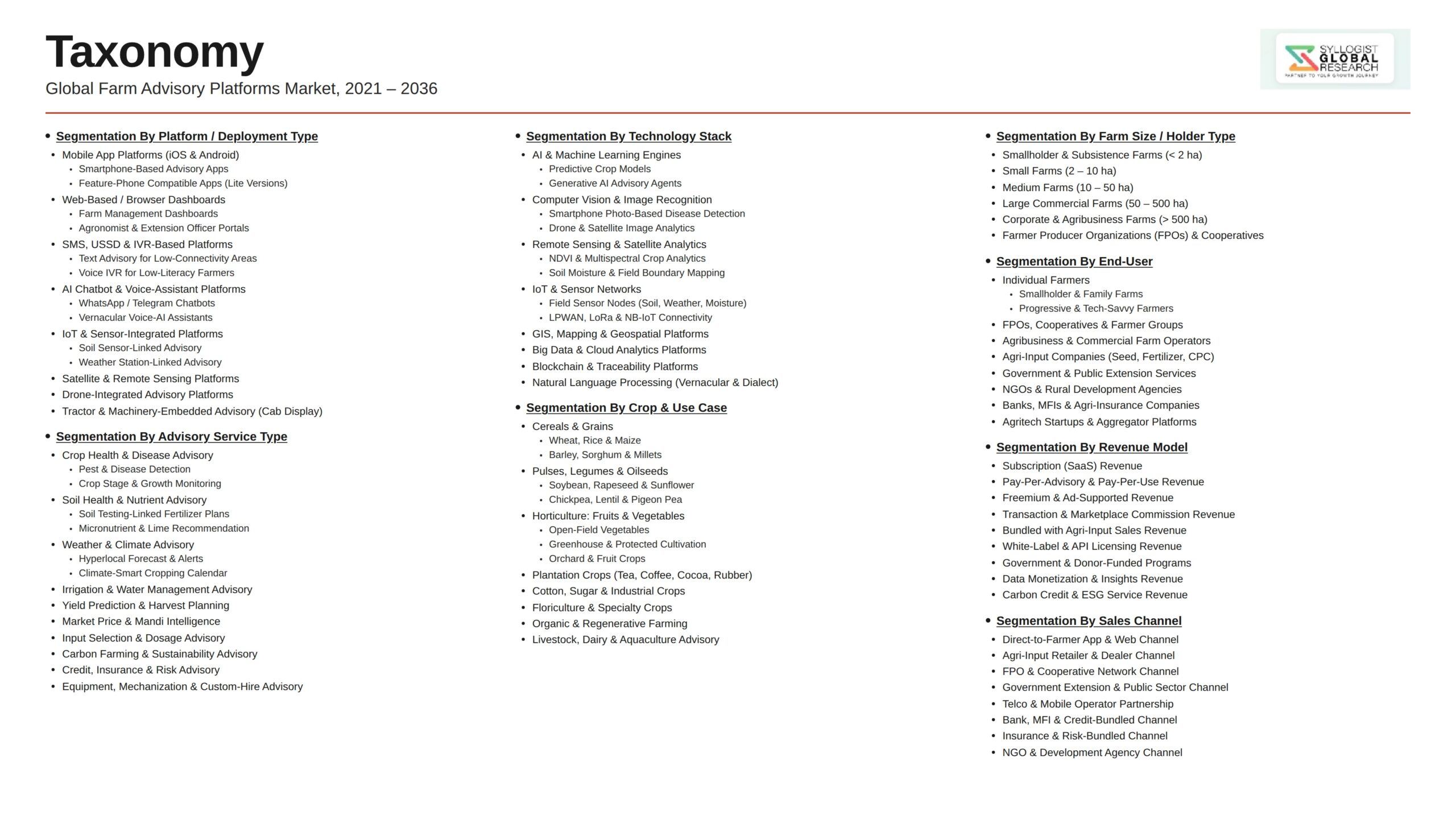

- Segmentation By Platform Type

- Crop Advisory Platforms

- Soil and Nutrient Management Platforms

- Pest and Disease Detection and Forecasting Platforms

- Irrigation and Water-Use Advisory Platforms

- Weather and Climate-Risk Advisory Platforms

- Market Price and Output Linkage Advisory Platforms

- Livestock Health and Feed Management Advisory Platforms

- Integrated Farm Management Platforms

- Others

- Segmentation By Delivery Mode

- Web-Based Platforms

- Native Smartphone Mobile Applications

- SMS, IVR, and Voice-Based Advisory Services

- Field Agent-Enabled Advisory Delivery

- IoT, Sensor, and Farm Machinery-Integrated Platforms

- Drone and Satellite Imagery-Linked Advisory Services

- Others

- Segmentation By Component

- Software Platforms and Advisory Engines

- Hardware Integration Modules and Edge Devices

- Advisory Services and Field Support

- Data, Analytics, and Modelling Services

- Others

- Segmentation By Deployment

- Public Cloud Deployment

- Private Cloud and On-Premise Deployment

- Hybrid Cloud Deployment

- Segmentation By Pricing Model

- Subscription and SaaS Pricing

- Freemium and Ad-Supported Models

- Pay-Per-Use and Transaction-Based Models

- Outcome-Linked and Yield-Sharing Models

- Bundled with Input, Credit, or Insurance Products

- Others

- Segmentation By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Oilseeds and Pulses

- Plantation and Industrial Crops

- Specialty and High-Value Crops

- Livestock and Dairy

- Others

- Segmentation By Farm Size

- Smallholder Farms (Below 5 Hectares)

- Mid-Size Farms (5 to 50 Hectares)

- Large Commercial Farms (Above 50 Hectares)

- Segmentation By End User

- Individual Farmers and Growers

- Farmer Producer Organizations and Cooperatives

- Agribusinesses, Seed, and Crop Input Suppliers

- Food and Beverage Supply Chains and Off-Takers

- Agri-Finance, Insurance, and Credit Institutions

- Government Agencies and Public Extension Services

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Farm Advisory Platforms Market in 2025, projected through 2034, disaggregated by platform type, delivery mode, and end user, enabling agritech operators, crop input majors, investors, and policy planners to identify highest-growth segments and most durable revenue opportunities across the digital agriculture advisory landscape?

- How are India, the United States, Brazil, Indonesia, Kenya, and the European Union allocating digital agriculture and farm advisory platform investment across smallholder advisory, integrated farm management, and crop-specific decision-support applications, and which national digital agriculture stacks are defining the technical and procurement benchmarks shaping the global farm advisory platforms market through 2034?

- What pricing models, monetization architectures, and farmer willingness-to-pay benchmarks are emerging across smallholder, mid-size, and commercial farm segments, and how are advisory platform operators balancing subscription, transaction-based, outcome-linked, and bundled pricing to achieve sustainable unit economics across the global farm advisory platforms market?

- Which platform segments, including integrated farm management, pest and disease detection, soil and nutrient advisory, livestock advisory, and weather and climate-risk advisory, are generating the highest growth rates through 2034, and what data, AI, and remote-sensing technologies are most critical to advisory accuracy, farmer retention, and platform stickiness in each category?

- How is the competitive landscape structured among independent agritech operators, crop input majors, farm machinery OEMs, and dual-use digital agriculture platforms pursuing farm advisory revenue, and what partnership, acquisition, and embedded-bundling strategies are enabling new entrants to compete against established advisory ecosystems across regional markets?

- What are the most significant data privacy, agronomy data ownership, and interoperability constraints affecting farm advisory platforms in commercial deployment, and how are platform developers, farm equipment OEMs, and policy authorities addressing data portability, farmer data rights, and standardized data exchange architectures across the global farm advisory platforms market?

- Which regional markets, specifically Asia-Pacific, Latin America, and Middle East and Africa, are expected to generate the most substantial incremental farm advisory platform revenue through 2034, and what smartphone penetration, smallholder demographics, climate adaptation, and agri-input ecosystem factors are driving advisory adoption priorities and supplier selection decisions in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Smallholder Farmer Digital Adoption, Smartphone Penetration & Rural Internet Connectivity Risk

- Advisory Accuracy, Localised Crop Recommendation & Farmer Trust Risk

- Data Privacy, Farmer Data Ownership & Cross-Border Agricultural Data Transfer Risk

- Government Policy Continuity, Public Extension Service Substitution & Subsidy Funding Risk

- Business Model Sustainability, User Retention, Pricing & Monetisation Risk

- Regulatory Framework & Standards

- Digital Public Infrastructure, Open Network for Digital Agriculture & Farmer Registry Frameworks

- Personal Data Protection, Agricultural Data Ownership & Cross-Border Data Transfer Regulations

- Crop Insurance Integration, Public Subsidy Advisory & Government Scheme Linkage Standards

- Advisory Quality Assurance, Liability Frameworks & Agricultural Extension Service Certification Standards

- Sustainability, Climate-Smart Agriculture, Carbon Credit Advisory & ESG Disclosure Compliance Frameworks

- Global Farm Advisory Platforms Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Active Users in Millions and Hectares Under Coverage in Million Hectares)

- Market Size & Forecast by Platform Type

- Mobile Application (Smartphone Native and Cross-Platform Apps)

- Web Portal & Browser-Based Platforms

- USSD & SMS-Based Advisory Services

- Interactive Voice Response (IVR) & Voice-Based Advisory Platforms

- AI Chatbot & Conversational Advisory Platforms

- Multi-Channel & Omnichannel Integrated Platforms

- Satellite & Remote Sensing Integrated Platforms

- IoT & Sensor-Enabled Advisory Platforms

- Market Size & Forecast by Service Type

- Crop Advisory (Planting, Irrigation, Fertilisation, Harvest Timing)

- Weather Forecasting & Climate Advisory Services

- Pest & Disease Detection, Diagnosis & Management Advisory

- Soil Health Monitoring & Nutrient Management Advisory

- Market Intelligence, Price Forecasting & Trade Advisory

- Financial Advisory (Credit, Crop Insurance, Subsidy Schemes)

- Sustainability, Climate-Smart Agriculture & Carbon Credit Advisory

- Government Scheme, Policy & Compliance Advisory

- Livestock, Dairy & Aquaculture Farming Advisory

- Market Size & Forecast by Technology

- Artificial Intelligence, Machine Learning & Predictive Analytics

- Satellite Imagery, Remote Sensing & Geographic Information Systems (GIS)

- Internet of Things (IoT) & Field Sensor Integration

- Computer Vision, Drone Imagery & Aerial Crop Monitoring

- Generative AI & Large Language Model Based Advisory

- Mobile Cloud Computing & Edge Computing for Rural Connectivity

- Blockchain-Enabled Traceability & Smart Contracts

- Voice Recognition & Multilingual Natural Language Processing

- Market Size & Forecast by Crop Type

- Cereals & Grains (Wheat, Rice, Maize, Sorghum, Millet)

- Pulses, Legumes & Oilseeds

- Fruits & Vegetables (Horticulture)

- Cash Crops (Cotton, Sugarcane, Tobacco)

- Plantation Crops (Tea, Coffee, Rubber, Coconut)

- Floriculture, Aromatic & Medicinal Plants

- Market Size & Forecast by Farm Size

- Smallholder Farms (Below 2 Hectares)

- Medium-Sized Farms (2 to 10 Hectares)

- Large Commercial Farms (Above 10 Hectares)

- Market Size & Forecast by Deployment Mode

- Cloud-Based Software-as-a-Service (SaaS)

- On-Premise Deployment

- Hybrid Cloud Deployment

- Market Size & Forecast by Business Model

- Free & Freemium Advisory Services

- Subscription-Based Pricing Models

- Pay-Per-Use & Transactional Models

- Enterprise & Institutional Licensing

- Outcome-Based & Performance-Linked Pricing

- Market Size & Forecast by Application

- Individual Farmer Advisory

- Farmer Producer Organisation (FPO) & Cooperative Advisory

- Agribusiness, Input Company & Output Buyer Advisory

- Government & Public Extension Service Augmentation

- Crop Insurance & Financial Services Advisory

- Carbon Credit, Sustainability & ESG Reporting Advisory

- Market Size & Forecast by End-User

- Individual Farmers

- Farmer Producer Organisations & Agricultural Cooperatives

- Agricultural Input Companies (Seed, Fertilizer, Crop Protection)

- Agricultural Output Buyers, Processors & Aggregators

- Government Agricultural Departments & Public Extension Services

- Banks, NBFCs & Crop Insurance Providers

- NGOs, Development Agencies & Donor Programmes

- Market Size & Forecast by Sales Channel

- Direct-to-Farmer Subscription Model

- Government & Public Sector Procurement Channel

- B2B Channel (Input Companies, Output Buyers, FPOs)

- Channel Partner & Reseller Network Model

- Bundled with Input or Output Marketplace Services

- North America Farm Advisory Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Users in Millions and Hectares Under Coverage in Million Hectares)

- By Platform Type

- By Service Type

- By Technology

- By Crop Type

- By Farm Size

- By Deployment Mode

- By Business Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Farm Advisory Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Users in Millions and Hectares Under Coverage in Million Hectares)

- By Platform Type

- By Service Type

- By Technology

- By Crop Type

- By Farm Size

- By Deployment Mode

- By Business Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Farm Advisory Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Users in Millions and Hectares Under Coverage in Million Hectares)

- By Platform Type

- By Service Type

- By Technology

- By Crop Type

- By Farm Size

- By Deployment Mode

- By Business Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Farm Advisory Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Users in Millions and Hectares Under Coverage in Million Hectares)

- By Platform Type

- By Service Type

- By Technology

- By Crop Type

- By Farm Size

- By Deployment Mode

- By Business Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Farm Advisory Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Users in Millions and Hectares Under Coverage in Million Hectares)

- By Platform Type

- By Service Type

- By Technology

- By Crop Type

- By Farm Size

- By Deployment Mode

- By Business Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Farm Advisory Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Users in Millions and Hectares Under Coverage in Million Hectares)

- By Platform Type

- By Service Type

- By Technology

- By Crop Type

- By Farm Size

- By Deployment Mode

- By Business Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Artificial Intelligence, Machine Learning & Predictive Analytics Technology Deep-Dive

- Satellite Imagery, Remote Sensing & GIS Integration Technology

- IoT Field Sensor, Soil Probe & Weather Station Integration Technology

- Computer Vision, Drone-Based Crop Monitoring & Aerial Imagery Technology

- Generative AI, Large Language Model & Multilingual Conversational Advisory Technology

- Mobile Cloud, Edge Computing & Offline-First Architecture for Rural Connectivity

- Blockchain-Enabled Traceability, Smart Contracts & Digital Identity for Farmers

- Patent & IP Landscape in Farm Advisory Platforms Technologies

- Value Chain & Supply Chain Analysis

- Software Development, Cloud Infrastructure & Hosting Service Supply Chain

- Satellite Data, Weather Data & Agricultural Data Aggregator Supply Chain

- IoT Hardware, Field Sensor & Connectivity Equipment Manufacturing Supply Chain

- AI Model Development, Training Data & Localised Advisory Content Supply Chain

- Channel Partner, Farmer Aggregator & Last-Mile Service Provider Network

- Government, Public Extension Service & Donor Programme Partnership Channel

- Input Company, Output Buyer & Financial Services Bundling Partnership

- Pricing Analysis

- Free & Freemium Advisory Service Monetisation and Conversion Funnel Analysis

- Subscription-Based Pricing Tier Analysis & Average Revenue Per User (ARPU) Benchmarks

- Pay-Per-Use & Transactional Pricing Economics for Specialised Advisory Services

- Enterprise & Institutional Licensing Pricing Analysis for FPOs, Agribusinesses & Government Programmes

- Outcome-Based & Performance-Linked Pricing Economics for Yield-Linked Advisory Contracts

- Total Customer Acquisition Cost (CAC), Customer Lifetime Value (LTV) and Unit Economics Analysis for Farm Advisory Platforms Operators

- Sustainability & Environmental Analysis

- Climate-Smart Agriculture Contribution: Reduced Input Use, Water Efficiency & Yield Resilience Through Advisory Service Adoption

- Carbon Credit Generation, Monitoring, Reporting & Verification Capability of Farm Advisory Platforms

- Soil Health Improvement, Regenerative Agriculture Adoption & Biodiversity Enhancement Through Advisory Services

- Reduction in Chemical Input Misuse, Water Wastage & Greenhouse Gas Emissions From Precision Advisory

- Regulatory-Driven Sustainability, SDG 2 (Zero Hunger) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Service Type & Geography

- Player Classification

- Integrated Digital Agriculture Platform Companies

- Specialist Crop Advisory & Pest Management Technology Providers

- Satellite Data & Geospatial Analytics Solution Providers

- Weather Forecasting & Climate Advisory Service Providers

- Input Companies with Digital Advisory Platform Capability

- Telecommunications Operators with Agricultural Advisory Service Offerings

- Government Technology Platform Providers & Public Digital Agriculture Initiatives

- AI, Generative AI & Conversational Advisory Platform Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Service Type & Region

- Company Profile

- Company Overview & Headquarters

- Farm Advisory Products & Technology Portfolio

- Key Customer Relationships & Reference Deployments

- Geographic Footprint & Active User Base

- Revenue (Farm Advisory Segment) & Subscription Base

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Geographic Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Service Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Platform Development & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Climate-Smart Agriculture Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)