Market Definition

The Europe Autonomous Greenhouse Farming Systems Market encompasses the design, engineering, integration, deployment, and servicing of automated and artificially intelligent controlled environment agriculture systems that operate greenhouse crop production processes with minimal or zero direct human intervention, utilizing robotics, machine vision, sensor fusion, artificial intelligence-driven decision engines, and precision actuation technologies to autonomously manage the full spectrum of greenhouse crop growth functions including climate control, irrigation and fertigation, pest and disease detection, crop harvesting, transplanting, grading, and logistics across commercial horticultural production facilities in European countries. Autonomous greenhouse farming systems represent the technological convergence of precision horticulture, industrial robotics, computer vision, the Internet of Things, and advanced data analytics into integrated production platforms that replicate, optimize, and continuously improve upon the skilled judgment of experienced growers through machine learning algorithms trained on extensive crop physiology, environmental response, and production outcome datasets.

The market encompasses autonomous climate management systems incorporating AI-driven heating, ventilation, cooling, CO2 enrichment, and supplemental lighting control that continuously optimize greenhouse microclimate conditions for crop growth and energy efficiency; precision irrigation and fertigation automation systems delivering individualized nutrient and water delivery to crop root zones based on real-time plant physiological and growing media sensor feedback; robotic harvesting, de-leafing, crop scouting, and transplanting systems operating autonomously within greenhouse growing lanes and gutter systems; machine vision and spectral imaging platforms providing continuous crop health monitoring, disease and pest identification, and growth stage assessment; autonomous logistics and internal transport systems including automated guided vehicles and rail-guided crop trolley systems; and overarching autonomous greenhouse management software platforms integrating all subsystem data streams into unified AI decision engines that orchestrate the complete production cycle. Key participants include precision horticulture technology companies, agricultural robotics developers, greenhouse construction and systems integration firms, climate computer and horticultural software developers, sensor and imaging technology providers, and large-scale greenhouse operators in the Netherlands, Belgium, Germany, Spain, France, and Scandinavia whose capital investment decisions and operational adoption of autonomous technologies define the commercial trajectory of the European market.

Market Insights

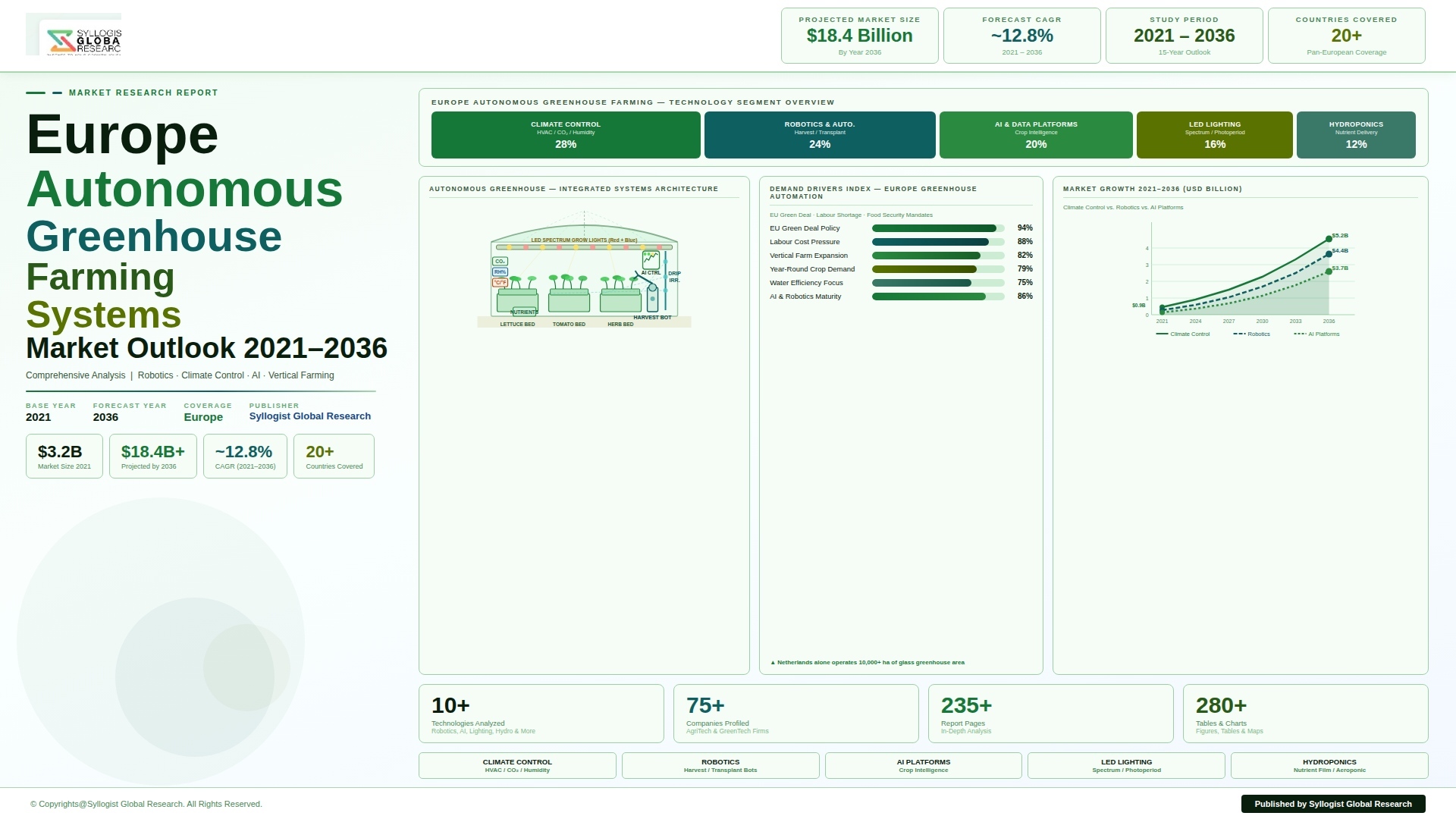

The Europe autonomous greenhouse farming systems market is experiencing a decisive inflection point at which the convergence of acute agricultural labor scarcity, escalating energy cost management imperatives, advancing artificial intelligence and robotics technology maturity, and expanding policy support for sustainable food production innovation is transforming autonomous greenhouse technology from a horizon aspiration of leading research institutions into a commercially deployed production reality across the Netherlands, Belgium, and progressively the broader European horticultural industry. The Europe autonomous greenhouse farming systems market was valued at approximately USD 2.1 billion in 2025 and is projected to reach USD 5.8 billion by 2034, advancing at a compound annual growth rate of 11.9% over the forecast period from 2027 to 2034, driven by the accelerating adoption of AI-driven climate management software across Dutch and Belgian Venlo-type glasshouse operations, the commercial scaling of robotic harvesting systems for tomato, cucumber, pepper, and sweet pepper crops, and the growing integration of autonomous production management platforms by large-scale greenhouse operators seeking to reduce labor dependency, optimize energy consumption, and improve crop consistency across expanding production footprints. The Netherlands, which operates approximately 9,800 hectares of commercial greenhouse production and contributes over USD 10.4 billion annually to Dutch agricultural export revenues, constitutes the single most commercially significant testbed and adoption market for autonomous greenhouse technologies globally, with Dutch growers and technology developers collectively representing the deepest concentration of precision horticulture expertise and autonomous system deployment experience in the world.

The AI-driven climate and crop management software segment constitutes the most commercially mature and widely deployed autonomous technology layer within the European greenhouse sector, with intelligent climate computer systems from companies including Priva, Ridder, Hoogendoorn Growth Management, and Metazet FormFlex already managing heating, ventilation, humidity, CO2 enrichment, and supplemental lighting schedules across several hundred thousand hectares of European glasshouse production through rule-based and increasingly machine learning-augmented control algorithms that process data from dense sensor networks to continuously optimize growing conditions against crop model targets. The transition from conventional expert-programmed climate management rules toward fully autonomous AI decision engines that learn from multi-season crop performance data and dynamically adapt management strategies to emerging crop stress signals, disease risk indicators, and energy price fluctuations represents the most commercially active frontier of this segment, with the Autonomous Greenhouse Challenge organized by Wageningen University having demonstrated in successive competition cycles since 2018 that AI-managed greenhouse compartments can achieve crop yields and resource efficiency outcomes that match or exceed those of experienced human growers on measurable key performance indicators. The integration of autonomous climate management with dynamic energy trading algorithms that respond in real-time to European electricity spot market price signals, enabling greenhouse energy-intensive operations including supplemental LED lighting and heating to be automatically modulated in response to grid price fluctuations, is generating demonstrable energy cost savings of 15% to 25% at participating Dutch and Belgian greenhouse operations and creating a commercially compelling autonomous system value proposition that extends beyond crop performance optimization into operational cost management of direct relevance to grower profitability under volatile European energy market conditions.

The robotic harvesting and in-greenhouse logistics automation segment is advancing from early commercial pilot deployments toward scalable commercial production system status across tomato, cucumber, and sweet pepper crops, driven by the structural intolerability of European greenhouse sector dependence on seasonal migrant labor for the highly repetitive and physically demanding harvesting and crop work operations that account for 40% to 60% of total production labor requirements at commercial scale greenhouse operations. Harvest CROO, Octinion, AppHarvest, and Root AI have demonstrated tomato harvesting robot platforms capable of achieving commercial harvest cycle times and damage rates approaching the performance thresholds required for deployment in production environments, while the Agrobot and FFRobotics systems are addressing strawberry and soft fruit harvesting applications whose gentle handling requirements present distinct engineering challenges relative to the firmer-fruited vine crops that have been the primary robotic harvesting development focus. The de-leafing and crop work robotics segment, addressing the labor-intensive practice of removing lower leaves from tall-growing vine crops to maintain plant health and light penetration, has reached commercial deployment status through the systems developed by Aris, Ridder, and Demtec, with de-leafing robots demonstrating cycle times and operational consistency that make them commercially viable replacements for manual de-leafing labor at scale glasshouse operations in the Netherlands and Belgium. Autonomous internal logistics systems including rail-guided crop transport trolleys, automated potting and transplanting lines, and autonomous guided vehicle systems for substrate bag handling and end-of-season crop removal represent the most commercially advanced automation layer within the European greenhouse sector, with Dutch systems integrators including Royal Brinkman and Meteor Systems having deployed several hundred automated internal transport systems across the Dutch glasshouse complex.

The geographic concentration of European autonomous greenhouse innovation and commercial deployment in the Netherlands and Belgium reflects the structural characteristics of these countries as intensive, export-oriented, and highly capital-efficient horticultural production systems whose grower culture, knowledge infrastructure, technology supplier ecosystem, and scale of production provide the conditions in which incremental automation investment is commercially justifiable against the avoided labor cost, improved product consistency, and resource efficiency gains that autonomous systems deliver. Beyond the Dutch and Belgian core, the autonomous greenhouse market is expanding into distinctly different national contexts including Spain’s Almeria region, which operates approximately 31,000 hectares of predominantly low-technology plastic tunnel greenhouse production and represents a vast potential addressable market for modular automation and precision management technology as Almeria growers face increasing labor cost pressure, water scarcity constraints, and export market quality demands that incentivize technology investment. The vertical farming intersection with greenhouse automation, while representing a distinct production system typology, is contributing to the European autonomous growing systems market through technology cross-pollination, with indoor vertical farm operators including Infarm, Plenty, and Nordic Harvest having advanced the development of autonomous seeding, growing, monitoring, and harvesting systems within their controlled environment production facilities whose technology architectures share significant engineering commonality with greenhouse autonomous system designs. Scandinavia is emerging as a regionally significant autonomous greenhouse market driven by the strategic imperative of extending local food production capability through harsh winter months using energy-efficient autonomous greenhouse systems, with Norwegian and Swedish greenhouse operators investing in AI climate management and robotic growing systems that maximize crop output per unit of supplemental lighting energy in high-latitude production environments where energy efficiency directly determines production economic viability.

Key Drivers

Structural Agricultural Labor Scarcity and Rising Seasonal Workforce Costs Compelling Greenhouse Operators Toward Autonomous System Investment

The European greenhouse horticultural sector is confronting a deepening and structurally irreversible agricultural labor crisis whose primary causes include the aging of rural European populations, the reorientation of migrant labor supply networks following post-Brexit UK immigration policy changes and EU freedom of movement adjustments, rising minimum wage legislation in the Netherlands, Belgium, Germany, and Spain that is progressively increasing the cost per hour of manual greenhouse operations, and the fundamental unattractiveness of repetitive, physically demanding greenhouse crop work to the domestic European labor market regardless of wage levels, collectively creating a cost and availability pressure on greenhouse labor that is directly translating into autonomous system investment decisions by growers who can no longer reliably staff their operations at the labor intensity levels required by manual production methods. Dutch greenhouse sector labor costs increased by approximately 34% between 2019 and 2024, driven by consecutive minimum wage increases and increased employer social contribution requirements, elevating the labor cost component of total greenhouse production operating expenditure to levels at which robotic harvesting systems with investment payback periods of four to seven years at current crop throughput performance specifications are clearing commercial investment hurdle rates at leading Dutch tomato, cucumber, and pepper operations. The post-COVID disruption to seasonal agricultural labor supply chains, which created acute harvest season labor shortages across multiple consecutive growing seasons, accelerated greenhouse operator awareness of labor dependency risk and catalyzed investment in automation feasibility assessments and pilot deployments that have in numerous cases progressed to commercial rollout commitments as robot system performance has proved sufficient for production integration. The combination of immediate labor cost reduction, elimination of recruitment and housing cost for seasonal migrant workforces, and the strategic labor risk mitigation value of autonomous systems is generating a multi-dimensional return on investment case for greenhouse automation that is strengthening investment justification across a broadening range of greenhouse scale, crop type, and operator sophistication levels.

European Energy Price Volatility and Greenhouse Carbon Footprint Reduction Mandates Driving Demand for AI-Optimized Climate Management Autonomy

The extraordinary natural gas price spike experienced across European energy markets between 2021 and 2023, which elevated Dutch greenhouse heating gas costs by over 300% at peak and pushed numerous smaller greenhouse operations into financial distress or forced temporary production curtailment, has permanently recalibrated the strategic priority assigned by European greenhouse operators to energy cost management and catalyzed investment in AI-driven autonomous climate management systems whose primary commercial value proposition has evolved from crop performance optimization to energy consumption minimization and operational cost stabilization in the context of structurally higher and more volatile European energy prices. AI autonomous climate management systems deployed at commercial Dutch and Belgian greenhouse operations have demonstrated energy consumption reductions of 20% to 35% compared to conventional expert-managed climate programming through the combined effect of predictive thermal buffer management that pre-heats greenhouse thermal mass during low energy price periods, dynamic window ventilation optimization that reduces heating demand through improved solar gain management, and machine learning-driven crop model refinement that identifies the minimum heating set-point temperatures at which crop development targets are achieved without the conservative safety margins that human growers typically apply. The EU taxonomy for sustainable activities and the European Green Deal’s Farm to Fork emission reduction targets are creating pressure on large-scale greenhouse operators and their retail supply chain customers to reduce the carbon intensity of greenhouse-grown produce, with autonomous energy management systems that optimize the deployment of renewable energy inputs, waste heat recovery, and geothermal energy sources within greenhouse climate management schedules representing a critical enabling technology for achieving the greenhouse sector carbon footprint reductions required to maintain access to sustainability-conscious European retail and foodservice procurement programs.

European Union Horizon Europe Research Funding and National AgriTech Innovation Programs Accelerating Autonomous Greenhouse Technology Commercialization

The European Union’s Horizon Europe research and innovation program has allocated substantial funding across multiple thematic clusters directly supporting the development and commercialization of autonomous greenhouse technologies, including the AgriFood LEIT cluster funding advanced robotics for food production, the Climate, Energy and Mobility cluster supporting energy-autonomous controlled environment agriculture, and the Food, Bioeconomy, Natural Resources, Agriculture and Environment cluster funding precision horticulture digital twin and AI decision engine research, collectively providing the pre-competitive research infrastructure and technology validation evidence base that reduces commercial deployment risk for greenhouse operators evaluating autonomous system investments and for technology developers seeking to advance laboratory and pilot-scale innovations toward commercial product readiness. The Netherlands Enterprise Agency has administered the Greenhouse as Energy Source program and the Kas als Energiebron innovation network through which Dutch greenhouse operators, technology developers, and energy companies have collaboratively developed and field-validated autonomous energy management technologies including aquifer thermal energy storage, geothermal heat integration, and AI-optimized energy system orchestration that are now in commercial deployment across several hundred Dutch greenhouse enterprises. National innovation programs in Belgium through the Flanders Research Institute for Agriculture, Fisheries and Food, in France through INRAE and the Vegetable Industries Technical Institute, and in Spain through the Instituto de Investigacion y Formacion Agraria y Pesquera are each supporting applied autonomous greenhouse research programs that are generating domestically validated technology solutions addressing the specific structural and climatic characteristics of their respective national greenhouse sectors, building the national knowledge bases and demonstration reference sites that support commercial adoption by growers who require proximity-validated evidence of autonomous system performance before committing capital investment.

Key Challenges

High Capital Investment Requirements and Extended Payback Periods Limiting Autonomous System Adoption Among Small and Medium-Scale Greenhouse Operators

The capital cost of deploying fully integrated autonomous greenhouse farming systems, encompassing AI climate management platforms, robotic harvesting systems, autonomous internal logistics infrastructure, and precision sensor networks capable of delivering the continuous crop monitoring data required for autonomous management decision-making, represents an investment threshold of several million euros per hectare of greenhouse production at full autonomous system specification that is commercially accessible only to the largest, most financially sophisticated, and most capital-efficient greenhouse operations in the European horticultural sector, while the vast majority of European greenhouse enterprises operating at scales below 5 hectares face capital access constraints, banking financing limitations, and investment risk tolerance boundaries that effectively exclude them from full autonomous system adoption at current technology pricing levels. The investment payback analysis for robotic harvesting systems, which represent the most capital-intensive individual component of an autonomous greenhouse technology stack with per-robot costs ranging from EUR 150,000 to EUR 400,000 depending on crop type and automation specification, is sensitive to crop throughput performance, operational uptime reliability, and maintenance cost assumptions that remain subject to meaningful uncertainty at current commercial deployment maturity levels, creating financial modeling uncertainty that complicates investment justification processes for growers and their financial advisors who require high confidence in return on investment projections before committing to capital expenditure programs of this scale. The availability of greenhouse-specific autonomous system financing instruments, equipment leasing structures, and technology-as-a-service subscription models that transfer upfront capital cost into operational expenditure payment streams is improving as the commercial ecosystem matures, but remains insufficiently developed to bridge the capital access gap for the large majority of European greenhouse enterprises that cannot self-finance autonomous system investment from operational cash generation.

Technical Complexity of Crop Biological Variability and Greenhouse Environmental Heterogeneity Constraining Autonomous System Reliability and Universal Applicability

The biological variability inherent in living crop systems, encompassing the continuous and non-linear developmental progression of plant growth stages, the dynamic and spatially heterogeneous expression of disease and physiological stress symptoms, the genotype-specific responses of different crop varieties to environmental conditions, and the unpredictable interaction effects between crop physiology, microclimate, and growing media parameters that make greenhouse crop management a domain of genuine complexity resisting full algorithmic codification, represents the fundamental technical challenge confronting autonomous greenhouse system developers seeking to replicate the adaptive judgment of experienced human growers across the full range of conditions encountered in commercial greenhouse production environments. Robotic harvesting systems, despite significant engineering progress, continue to face performance limitations arising from the biological variability of fruit position, orientation, size distribution, and color development within individual plant canopies that creates object detection and manipulation challenges whose resolution requires machine vision systems of substantially greater sophistication than the controlled and consistent manufacturing environments for which industrial robotic systems were originally designed, and whose performance in the variable lighting conditions, foliage occlusion scenarios, and fruit clustering patterns encountered in commercial greenhouse growing lanes falls short of the damage rate and throughput standards required by the most demanding commercial operators. The significant heterogeneity of greenhouse structural designs, climate system architectures, crop varieties, growing system configurations, and operational management cultures across European greenhouse enterprises creates substantial system integration complexity for autonomous technology suppliers seeking to develop commercially scalable solutions that can be reliably deployed across diverse customer environments without extensive and costly site-specific customization that erodes the economics of autonomous system supply and installation.

Grower Knowledge Dependency and the Transition Challenge of Transferring Tacit Horticultural Expertise into Autonomous System Training Datasets

The commercial performance of autonomous greenhouse management systems is fundamentally constrained by the quality, representativeness, and completeness of the training datasets on which their machine learning algorithms are developed and validated, and the acquisition of these datasets requires access to the accumulated tacit horticultural knowledge of experienced commercial growers, whose understanding of crop growth dynamics, early stress indicator recognition, management intervention timing, and variety-specific behavioral characteristics represents decades of experiential learning that has never been systematically codified in the form required to train autonomous decision-making systems. The challenge of knowledge transfer from expert growers to autonomous system developers is compounded by the fact that experienced horticultural knowledge is predominantly embodied, intuitive, and contextual in nature, expressed through manual inspection routines, sensory crop assessment practices, and gestalt pattern recognition capabilities that resist translation into the labeled data formats, quantitative sensor measurements, and explicit decision logic structures required by machine learning model training pipelines. The grower community’s legitimate concern that the development of autonomous systems that replicate their expertise effectively transfers the commercial value of their accumulated knowledge to technology companies without adequate recognition or compensation is creating cultural resistance to the depth of data sharing and operational transparency required for autonomous system training and validation, representing a stakeholder relationship challenge that autonomous greenhouse technology developers must address through equitable data governance arrangements, grower participation in development value creation, and demonstration of genuine performance partnership rather than extractive data acquisition models. The transition period during which greenhouse operations are moving from human-managed to autonomously managed production entails elevated operational risk exposure that requires careful change management, phased implementation planning, and robust technical support infrastructure that many smaller autonomous system developers lack the organizational capacity to provide consistently across expanding commercial deployment bases.

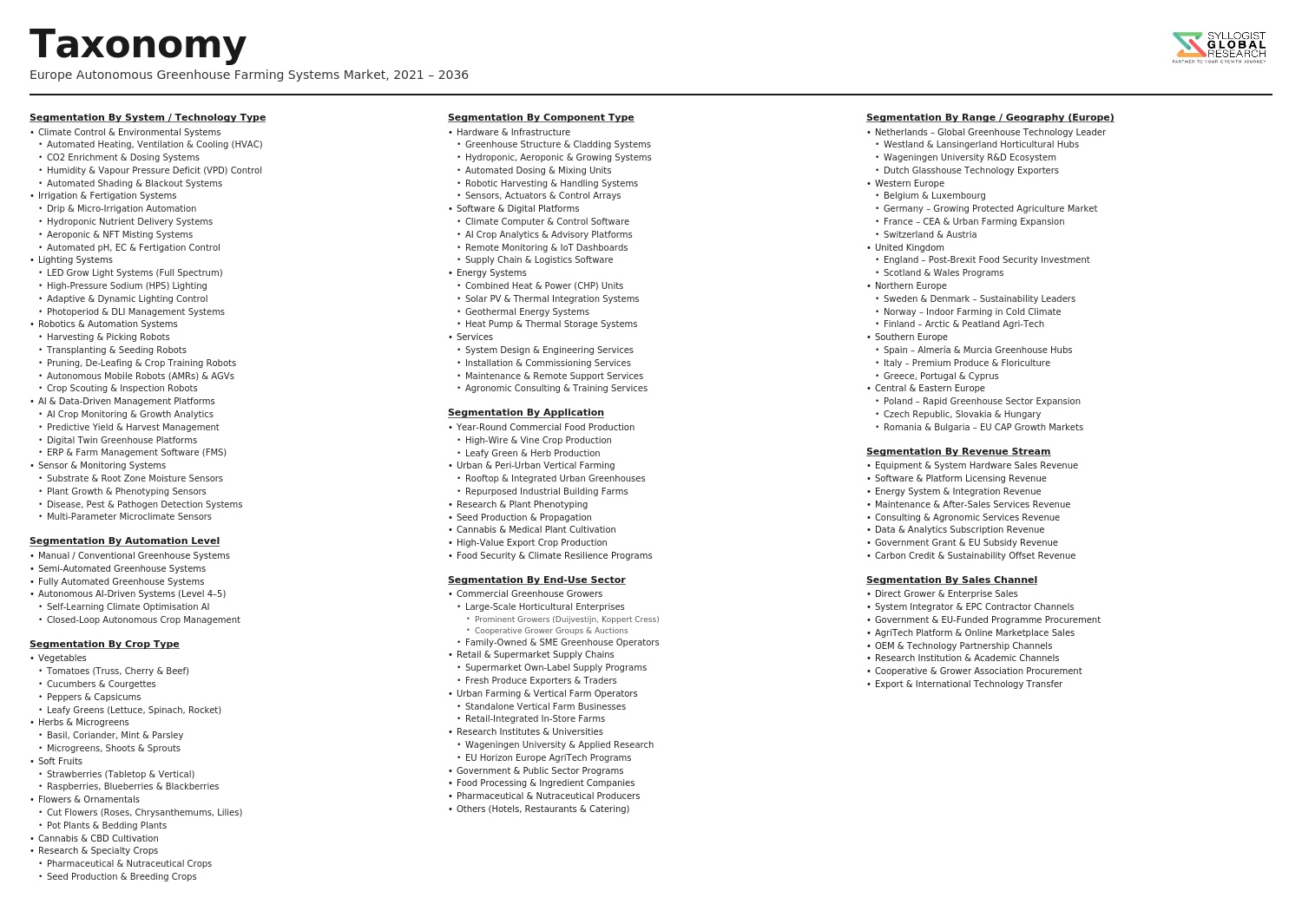

Market Segmentation

Segmentation By System Type

- Autonomous Climate Control and Environmental Management Systems

- AI-Driven Crop Growth and Yield Prediction Platforms

- Robotic Harvesting Systems

- Robotic De-Leafing, Pruning, and Crop Work Systems

- Autonomous Transplanting and Seeding Systems

- Precision Irrigation and Fertigation Automation Systems

- Automated Internal Logistics and Transport Systems (AGVs, Rail-Guided)

- Machine Vision and Autonomous Crop Scouting Systems

- Autonomous Grading, Packing, and Post-Harvest Systems

- Integrated Autonomous Greenhouse Management Software Platforms

- Others

Segmentation By Technology Component

- Robotic Arms, End Effectors, and Manipulation Systems

- Machine Vision and Hyperspectral Imaging Systems

- AI and Machine Learning Software Engines

- IoT Sensor Networks (Climate, Soil, Plant Physiology Sensors)

- Automated Guided Vehicles (AGVs) and Mobile Platforms

- Greenhouse Climate Computers and Actuator Systems

- Digital Twin and Simulation Platforms

- Edge Computing and Real-Time Processing Hardware

- Others

Segmentation By Crop Type

- Tomato

- Cucumber

- Sweet Pepper and Bell Pepper

- Leafy Vegetables and Herbs (Lettuce, Basil, Spinach)

- Strawberry and Soft Fruit

- Cut Flowers and Ornamentals

- Pot Plants and Bedding Plants

- Others

Segmentation By Greenhouse Type

- Venlo-Type Glass Greenhouse

- Polycarbonate Panel Greenhouse

- Plastic Film Tunnel Greenhouse

- Multi-Span Film Greenhouse (Including Almeria-Style)

- Vertical Farming and Indoor Growing Facilities

- Others

Segmentation By Automation Level

- Fully Autonomous (Zero Human Intervention in Production Cycle)

- Highly Automated (Minimal Supervisory Human Role)

- Semi-Automated (Collaborative Human-Robot Operations)

- Decision Support Automation (AI-Assisted Human Management)

- Others

Segmentation By Greenhouse Scale

- Large-Scale Commercial Greenhouses (Above 10 Hectares)

- Medium-Scale Greenhouses (2 to 10 Hectares)

- Small-Scale Greenhouses (Below 2 Hectares)

- Others

Segmentation By End User

- Commercial Horticultural Producers

- Cooperative and Collective Greenhouse Enterprises

- Retail and Food Service Supply Chain Greenhouse Operations

- Research Institutions and Agricultural Universities

- Government-Funded Demonstration and Pilot Facilities

- Others

Segmentation By Country

- Netherlands

- Belgium

- Germany

- Spain

- France

- United Kingdom

- Italy

- Scandinavia (Norway, Sweden, Denmark, Finland)

- Rest of Europe

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the Europe Autonomous Greenhouse Farming Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by system type, technology component, crop type, greenhouse type, automation level, and country, to enable greenhouse technology developers, robotics companies, horticulture investors, and greenhouse operators to identify which autonomous system categories and national markets will generate the highest absolute revenue and most sustained investment demand across the forecast period?

- How is the structural agricultural labor shortage across European greenhouse-producing countries, combined with rising seasonal workforce costs and post-Brexit labor supply disruptions in the United Kingdom, quantifiably reshaping greenhouse operator investment priorities and automation adoption timelines across different greenhouse scale categories and crop types, and what is the projected labor cost avoidance value that commercially available autonomous harvesting, de-leafing, and logistics systems deliver at current performance specifications relative to the manual labor costs they displace at major European greenhouse operations?

- What is the current commercial deployment status, operational performance benchmarks, crop throughput rates, and damage rate achievements of robotic harvesting systems across tomato, cucumber, sweet pepper, and soft fruit applications in European greenhouse environments, which system developers are closest to achieving the performance and reliability thresholds required for full commercial production deployment at scale, and what technology development milestones across machine vision accuracy, end effector design, and canopy navigation capability are required to achieve broad commercial adoption across the European greenhouse sector through 2034?

- How are AI-driven autonomous climate management systems demonstrating quantifiable energy consumption reduction, crop yield improvement, and carbon footprint reduction outcomes at commercial European greenhouse deployments relative to conventionally managed control operations, what is the documented range of energy cost savings achievable through AI autonomous energy optimization at Dutch, Belgian, and Scandinavian greenhouse operations under different energy price and grid structure scenarios, and how are these demonstrated outcomes influencing investment decision timelines among the broader European greenhouse operator community?

- Who are the leading autonomous greenhouse system developers, precision horticulture technology companies, agricultural robotics firms, greenhouse climate computer manufacturers, and integrated systems integrators currently defining the competitive landscape of the Europe autonomous greenhouse farming systems market, and what are their respective technology portfolios, commercial deployment references, R and D investment priorities, partnership structures with greenhouse operators and horticultural cooperatives, financing and business model innovations addressing capital access barriers for smaller growers, and strategic positioning in response to the structural growth opportunity presented by European greenhouse sector labor, energy, and sustainability transition imperatives through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- High Capital Investment, Long Payback Period & Grower Return on Investment Risk

- Technology Complexity, System Integration Failure & Crop Loss Risk from Automation Errors

- Energy Cost Volatility, Grid Reliability & Greenhouse Heating & Lighting Cost Risk in Europe

- Skilled Labour Shortage for System Operation, Maintenance & AI Model Management Risk

- Regulatory Uncertainty, Food Safety Certification & Novel Growing Method Approval Risk Across European Member States

- Regulatory Framework & Standards

- EU Farm to Fork Strategy, Green Deal Agricultural Policy & Sustainable Greenhouse Production Incentive Frameworks

- EU Common Agricultural Policy (CAP) Funding, Rural Development Programme & Horticultural Investment Support Mechanisms

- EU Food Safety & Hygiene Regulations (EC 852/2004), Plant Health Directives & Pesticide Reduction Mandates Relevant to Autonomous Greenhouse Systems

- CE Marking, Machinery Directive, Electrical Equipment Safety & Robotics Standards Applicable to Autonomous Greenhouse Equipment

- GDPR, Agricultural Data Governance, AI Act Compliance & Digital Agriculture Platform Regulatory Requirements in Europe

- Europe Autonomous Greenhouse Farming Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Installed & Greenhouse Area Covered, Hectares)

- Market Size & Forecast by System Type

- Autonomous Climate Control & Environmental Management Systems

- Automated Irrigation & Fertigation Systems

- Autonomous Crop Monitoring & AI-Driven Plant Health Detection Systems

- Robotic Harvesting & Picking Systems

- Autonomous Seeding, Transplanting & Propagation Systems

- Automated Pest, Disease & Integrated Crop Protection Systems

- Autonomous Logistics, Transport & Internal Greenhouse Mobile Robot Systems

- Integrated Greenhouse Management & Autonomous Control Platform Systems

- Autonomous Energy Management & Renewable Integration Systems

- Market Size & Forecast by Component

- Hardware (Sensors, Actuators, Robots, Drones & Mechanical Systems)

- Software & AI Platforms (Greenhouse Management Systems, Digital Twins & Decision Support)

- Connectivity & Communication Infrastructure (IoT Gateways, Edge Computing & 5G)

- Professional Services (System Integration, Installation, Calibration & Training)

- Maintenance, Support & Managed Service Contracts

- Market Size & Forecast by Automation Level

- Fully Autonomous Systems (Closed-Loop AI Control with Minimal Human Intervention)

- Semi-Autonomous Systems (AI-Assisted Decision Making with Human Oversight)

- Partially Automated Systems (Single-Function Automation with Manual Integration)

- Market Size & Forecast by Crop Type

- Tomatoes

- Cucumbers & Peppers

- Lettuce, Leafy Greens & Herbs

- Strawberries & Soft Fruit

- Ornamentals, Cut Flowers & Pot Plants

- Cannabis & Medicinal Plants (Where Legally Permitted)

- Other Vegetable & Specialty Crops

- Market Size & Forecast by Greenhouse Structure Type

- Venlo & Multi-Span Glass Greenhouses

- Plastic Film & Polycarbonate Covered Greenhouses

- Vertical Farming & Indoor Controlled Environment Agriculture (CEA) Facilities

- Hydroponic & Aeroponic Growing Systems

- Aquaponic & Integrated Multi-Trophic Growing Systems

- Market Size & Forecast by Application

- Commercial Horticulture & Large-Scale Protected Crop Production

- Research, Trialling & Seed Production Facilities

- Urban & Peri-Urban Farming & City Rooftop Greenhouses

- Retail & Supermarket In-Store & Near-Store Growing Facilities

- Pharmaceutical, Nutraceutical & Specialty Crop Production

- Market Size & Forecast by End-User

- Large Commercial Greenhouse Growers & Horticultural Cooperatives

- Small & Medium-Scale Greenhouse Farmers

- Agri-Food Companies & Vertically Integrated Retailers

- Research Institutes, Universities & Agricultural Experiment Stations

- Government Bodies & Public Agricultural Development Agencies

- Greenhouse Technology Integrators & Turn-Key Project Developers

- Market Size & Forecast by Sales Channel

- Direct Sales & Turn-Key Project Delivery

- Greenhouse Equipment Dealer & Distributor Network

- Precision Agriculture & Greenhouse Technology Platform Provider

- Government Subsidy, CAP-Funded & Innovation Grant-Assisted Procurement

- Online & Digital Commerce Platform

- Western Europe Autonomous Greenhouse Farming Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Installed & Greenhouse Area Covered, Hectares)

- By System Type

- By Component

- By Crop Type

- By Greenhouse Structure Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Northern Europe Autonomous Greenhouse Farming Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Installed & Greenhouse Area Covered, Hectares)

- By System Type

- By Component

- By Crop Type

- By Greenhouse Structure Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Eastern Europe Autonomous Greenhouse Farming Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Installed & Greenhouse Area Covered, Hectares)

- By System Type

- By Component

- By Crop Type

- By Greenhouse Structure Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Southern Europe Autonomous Greenhouse Farming Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Installed & Greenhouse Area Covered, Hectares)

- By System Type

- By Component

- By Crop Type

- By Greenhouse Structure Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Central Europe Autonomous Greenhouse Farming Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Installed & Greenhouse Area Covered, Hectares)

- By System Type

- By Component

- By Crop Type

- By Greenhouse Structure Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Autonomous Greenhouse Farming Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Installed & Greenhouse Area Covered, Hectares)

- By System Type

- By Component

- By Crop Type

- By Greenhouse Structure Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: Netherlands, Germany, France, United Kingdom, Spain, Italy, Belgium, Poland, Sweden, Denmark, Finland, Norway, Czech Republic, Hungary, Romania, Austria, Switzerland, Portugal, Greece, Ireland

- Technology Landscape & Innovation Analysis

- AI-Driven Climate Control & Multi-Parameter Greenhouse Environment Optimisation Technology Deep-Dive

- Computer Vision, Hyperspectral Imaging & Deep Learning Technology for Autonomous Crop Health & Growth Monitoring

- Robotic Harvesting Technology: End-Effector Design, Soft Robotics & Multi-Crop Adaptability for European Greenhouse Crops

- Automated Fertigation, Substrate Monitoring & Precision Nutrient Delivery Technology for Hydroponic & Soil-Based Systems

- Autonomous Mobile Robot (AMR) Technology for In-Greenhouse Logistics, Crop Transport & Platform Positioning

- Digital Twin, Simulation & Predictive Crop Growth Modelling Technology for Greenhouse Yield Optimisation

- Autonomous Renewable Energy Integration: Solar, Geothermal & Heat Pump Technology for Energy-Neutral Greenhouse Operations

- Patent & IP Landscape in Autonomous Greenhouse Farming Technologies Relevant to Europe

- Value Chain & Supply Chain Analysis

- Sensor, Actuator, Camera & Robotic Component Manufacturing Supply Chain

- Greenhouse Structure, Covering Material & Climate System Manufacturing Supply Chain

- AI Software, Greenhouse Management Platform & Digital Twin Development Supply Chain

- System Integration, Commissioning & Turn-Key Greenhouse Project Delivery Supply Chain

- Greenhouse Equipment Dealer, Distributor & Horticultural Supplier Channel

- Grower, Cooperative & Agri-Food Company Procurement Channel

- Waste, Organic Residue, Substrate & Recycled Water Management Value Chain

- Pricing Analysis

- Autonomous Climate Control & Environmental Management System Capital Cost & TCO Analysis

- Robotic Harvesting & Picking System Capital Cost, Throughput Rate & Payback Period Analysis

- Integrated Greenhouse Automation Platform Licensing, SaaS & Per-Hectare Pricing Model Analysis

- Energy Cost, LED Lighting & Heating System Operating Cost Analysis for Autonomous Greenhouses in Europe

- Turn-Key Autonomous Greenhouse Project Development Cost & Investment Return Analysis

- Total Cost of Autonomous Greenhouse Production per Kilogram of Crop Across System Configurations

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Autonomous Greenhouse Farming Systems: Carbon Footprint, Energy Intensity, Water Use & Material Inputs

- Resource Efficiency Contribution: Water Saving, Fertiliser Reduction, Pesticide Elimination & Land Use Optimisation vs. Open-Field Production

- Autonomous Greenhouse Role in European Food System Resilience, Local Sourcing & Supply Chain Decarbonisation

- Circular Economy in Autonomous Greenhouses: Substrate Reuse, Waste Heat Recovery, CO2 Enrichment & Closed-Loop Water Systems

- Regulatory-Driven Sustainability, SDG 2 (Zero Hunger), SDG 12 (Responsible Consumption) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Crop Type & Country

- Player Classification

- Integrated Autonomous Greenhouse Technology & Turn-Key Solution Providers

- Specialist Greenhouse Climate Control & Environmental Management System Manufacturers

- Robotic Harvesting & Crop Handling Robot Manufacturers

- AI, Computer Vision & Greenhouse Software Platform Providers

- Hydroponic, Vertical Farming & CEA Technology Specialists

- Greenhouse Structure, Covering & Infrastructure Manufacturers with Automation Integration

- Precision Irrigation, Fertigation & Nutrient Management System Providers

- Start-Ups & AgTech Ventures Developing Next-Generation Autonomous Greenhouse Technologies

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Crop Type & Country

- Company Profile

- Company Overview & Headquarters

- Autonomous Greenhouse Products, Systems & Platform Portfolio

- Key Customer Relationships & Reference Greenhouse Installations in Europe

- Manufacturing Footprint & Production Capacity

- Revenue (Autonomous Greenhouse Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Product Launches, Greenhouse Deployments)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Component, Crop Type, End-User & Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output