Market Definition

The India Gas Pipelines Market encompasses the planning, engineering, procurement, construction, commissioning, operation, maintenance, and regulatory oversight of cross-country natural gas transmission pipelines, city gas distribution networks, liquefied natural gas regasification terminal interconnect pipelines, spur and lateral pipeline connections to industrial consumers, and the associated compression, metering, pressure regulation, and safety infrastructure that collectively form the national gas pipeline grid enabling the transportation of natural gas from domestic production sources, liquefied natural gas import terminals, and cross-border supply points to power generation utilities, industrial facilities, fertilizer plants, compressed natural gas vehicle fueling stations, piped natural gas residential and commercial connections, and city gas distribution networks across India’s geographically vast and supply-demand-imbalanced natural gas consumption landscape. The market encompasses the complete pipeline infrastructure value chain from route survey and environmental impact assessment through right-of-way acquisition, pipe manufacturing and coating, trench excavation and pipe laying, cathodic protection installation, supervisory control and data acquisition system commissioning, hydrostatic testing and pre-commissioning, operational dispatch management, integrity management including inline inspection, corrosion monitoring and pigging programs, and long-term operations and maintenance services that define the commercial relationship between pipeline operators, the Petroleum and Natural Gas Regulatory Board, and the gas shippers and consumers utilizing pipeline infrastructure. Key pipeline infrastructure asset classes in India include the national gas grid trunk pipelines operated by Gas Authority of India Limited, transmission pipelines operated by Indian Oil Corporation, GSPC Gas, and other state and central public sector undertakings, the Jagdishpur-Haldia-Bokaro-Dhamra pipeline being constructed to extend natural gas access to eastern and northeastern India, city gas distribution pipeline networks operated by licensed entities including Indraprastha Gas, Mahanagar Gas, Adani Total Gas, and others across geographical areas authorized by the Petroleum and Natural Gas Regulatory Board, and the regasification terminal interconnect spurs linking India’s liquefied natural gas import terminals at Dahej, Hazira, Dabhol, Ennore, Mundra, and Kochi to the national grid. Key participants include GAIL India, Indian Oil, GSPC, state gas companies, city gas distribution operators, the Petroleum and Natural Gas Regulatory Board, Engineering Procurement and Construction contractors, and pipe manufacturers.

Market Insights

The India gas pipelines market was valued at approximately USD 4.2 billion in 2025 and is projected to reach USD 9.6 billion by 2034, advancing at a compound annual growth rate of 9.6% over the forecast period from 2027 to 2034, driven by the Indian government’s ambitious target of increasing the share of natural gas in the national primary energy mix from approximately 6.7% in 2025 to 15% by 2030 as articulated in the National Gas Grid Vision and reinforced by the Petroleum and Natural Gas Regulatory Board’s accelerated pipeline authorization program, the rapidly expanding city gas distribution network rollout across hundreds of geographical areas, the completion of critical pipeline infrastructure bridging the natural gas supply deficit in eastern and northeastern India, and the progressive integration of new liquefied natural gas import terminal connections into the national grid that is expanding regasification capacity and reducing India’s dependence on domestic gas production whose decline from the KG-D6 basin has created supply-demand imbalances in existing consumption centers. India’s total gas pipeline network length reached approximately 24,600 kilometers of commissioned transmission and distribution pipelines in 2025, with an additional approximately 14,800 kilometers under construction or authorized, reflecting the significant gap relative to the government’s target of a 35,000-kilometer national gas grid that requires sustained capital investment and right-of-way facilitation to achieve within the 2030 policy timeframe. The Petroleum and Natural Gas Regulatory Board had granted city gas distribution authorization to entities in approximately 296 geographical areas covering over 98% of India’s districts by 2025, creating an authorized expansion footprint for compressed natural gas and piped natural gas infrastructure that represents a total capital investment pipeline of approximately USD 18.4 billion over the next decade as licensed city gas distribution entities build out their authorized network coverage and connection base.

The city gas distribution segment represents the most commercially dynamic component of the India gas pipelines market, accounting for approximately 38% of total market revenue in 2025 and growing at approximately 14.2% annually, driven by the combination of policy-mandated rollout obligations imposed by the Petroleum and Natural Gas Regulatory Board on geographical area license holders requiring achievement of minimum compressed natural gas station and piped natural gas connection milestones within defined work program timelines, the economic attractiveness of piped natural gas relative to liquefied petroleum gas, diesel, and petrol at prevailing price differentials, and the growing urban consumer preference for reliable, metered, and safe natural gas supply through permanent pipeline connections that eliminates the handling and storage requirements of cylinder-based liquefied petroleum gas. The compressed natural gas segment within city gas distribution is experiencing particularly strong demand growth as India’s commercial vehicle and bus fleets accelerate compressed natural gas adoption driven by compressed natural gas fuel cost savings of approximately 30% to 45% relative to diesel at prevailing price levels, national clean air action programs requiring conversion of heavy-duty vehicles in polluted cities including Delhi, Mumbai, and Kolkata to compressed natural gas, and state transport undertakings converting bus fleets to compressed natural gas under national clean mobility programs. The piped natural gas residential connection base in India reached approximately 12.4 million connections in 2025 and is projected to expand to approximately 42 million connections by 2034 as the geographical area expansion of city gas distribution licenses progresses from metro and tier-one cities into tier-two, tier-three, and rural areas covered by the ninth and tenth rounds of Petroleum and Natural Gas Regulatory Board geographical area authorization, requiring construction of approximately 1.8 million kilometers of steel and medium-density polyethylene distribution pipelines at a cumulative capital expenditure of approximately USD 12.8 billion through the forecast period.

The national gas grid transmission infrastructure development program, anchored by the government-mandated completion of the Pradhan Mantri Urja Ganga pipeline project and the phased development of the Jagdishpur-Haldia-Bokaro-Dhamra pipeline, the North East Gas Grid connecting the eight northeastern states of India to the national grid, and the proposed Northeast India pipeline that will bring natural gas to some of India’s most energy-deficient states, represents the most strategically significant and capital-intensive investment in the India gas pipelines market, addressing the fundamental connectivity deficiency that has left eastern and northeastern India reliant on petroleum products and coal despite natural gas’s economic and environmental advantages for industrial, domestic, and transport end uses. The Jagdishpur-Haldia-Bokaro-Dhamra pipeline at approximately 3,240 kilometers of trunk and spur lines is connecting the Bhagyanagar Gas, Assam Gas, and Green Gas city gas distribution entities in Uttar Pradesh, Jharkhand, Odisha, and Bihar to national grid supply points, enabling the development of natural gas-based industrial clusters, fertilizer plant feedstock supply, and compressed natural gas and piped natural gas network rollout across states that collectively represent over 400 million people currently without pipeline gas access. GAIL India, which operates approximately 14,800 kilometers of high-pressure gas transmission pipelines representing the backbone of India’s national gas grid and serves as the country’s dominant gas transmission entity, announced a capital expenditure program of approximately USD 3.2 billion for gas pipeline capacity expansion and new pipeline construction through 2026 to 2028, reflecting the scale of infrastructure investment required to keep pace with the growth in gas transmission volumes expected from expanding city gas distribution consumption, new industrial connections, and increasing liquefied natural gas import terminal throughput as India’s gas consumption grows toward the 15% energy mix target.

The liquefied natural gas import terminal and regasification infrastructure integration with the gas pipeline network represents a critical enabler of India’s gas market development, with India’s operational regasification capacity reaching approximately 42.5 million metric tons per annum across terminals at Dahej, Hazira, Dabhol, Ennore, Mundra, Kochi, and Krishnapatnam in 2025, supported by pipeline interconnects feeding regasified liquefied natural gas into the national grid for distribution to power, fertilizer, industrial, and city gas distribution consumers across supply-deficient markets in western, southern, and eastern India. The planned expansion of India’s regasification capacity by approximately 25 million metric tons per annum through new terminals at Chhara, Ennore Phase 2, Jafrabad, Dhamra, and Paradip whose pipeline interconnects require new spur and lateral pipeline infrastructure is creating near-term pipeline construction opportunities valued at approximately USD 1.8 billion that are critical to realizing the increased gas availability that expanded import capacity creates. Pipeline tariff regulation by the Petroleum and Natural Gas Regulatory Board under a cost-of-service framework that determines the allowed return on capital employed for regulated pipeline entities at approximately 12% pre-tax return on regulated asset base is providing investment certainty that encourages pipeline capital expenditure by GAIL, Indian Oil, GSPC, and other regulated transmission and distribution entities while simultaneously creating tariff-setting disputes and rate case proceedings that can delay pipeline construction commencement and investment recovery timelines for pipeline operators challenging Petroleum and Natural Gas Regulatory Board tariff determinations before appellate authorities. The integration of the national gas grid with future hydrogen transport infrastructure is emerging as a strategic long-term planning consideration, with GAIL and the Ministry of Petroleum and Natural Gas exploring the hydrogen blending capacity of existing steel pipeline infrastructure at blend levels of up to 5% to 10% hydrogen by volume that could provide a near-term hydrogen distribution pathway as India’s green hydrogen production capacity scales under the National Green Hydrogen Mission.

Key Drivers

Government Target of 15% Natural Gas Share in Energy Mix, National Gas Grid Vision, and Petroleum and Natural Gas Regulatory Board’s Accelerated Authorization Program Mandating Pipeline Infrastructure Expansion

India’s national energy policy commitment to increasing natural gas’s share in the primary energy mix from approximately 6.7% to 15% by 2030 requires approximately tripling annual natural gas consumption from approximately 60 billion cubic meters to approximately 150 billion cubic meters, a volume increase that can only be achieved through simultaneous expansion of pipeline transmission and city gas distribution infrastructure to connect new consumption centers, new supply sources, and new import terminals within a unified and well-integrated national gas grid, creating a policy-mandated infrastructure investment imperative that is translating into authorized pipeline construction programs, government-facilitated right-of-way acquisition support, and viability gap funding for pipeline projects in economically challenging geographies where regulated tariff recovery alone may not provide sufficient investment incentive. The Petroleum and Natural Gas Regulatory Board’s authorization of city gas distribution entities across 296 geographical areas encompassing the entirety of India’s populated geography and its enforcement of minimum work program obligations requiring compressed natural gas station and piped natural gas connection milestones within contractually defined timelines creates a legally binding investment mandate for city gas distribution entities whose license conditions require capital deployment in pipeline network construction that is independently traceable through quarterly performance reporting to the regulator. The National Gas Grid Vision and the Hydrocarbon Vision 2030 framework articulate specific pipeline length, connection density, and geographical access targets whose implementation is monitored by the Ministry of Petroleum and Natural Gas and the Petroleum and Natural Gas Regulatory Board and whose shortfall generates regulatory intervention, license forfeiture risk, and political pressure that collectively sustain pipeline investment momentum even when short-term gas market economics are unfavorable for private pipeline developers.

Rapidly Expanding Compressed Natural Gas Vehicle Fleet, Clean Air Regulations Mandating Fuel Switching, and Widening CNG-Diesel Price Differential Driving City Gas Distribution Pipeline Investment

India’s compressed natural gas vehicle market is experiencing structural growth driven by the combination of Supreme Court and National Green Tribunal orders mandating compressed natural gas conversion for commercial vehicles, buses, and three-wheelers operating in major cities under the National Clean Air Programme and the Graded Response Action Plan for pollution emergencies, the compelling compressed natural gas-to-diesel price differential of approximately 30% to 45% that creates significant operating cost savings for commercial fleet operators, and the progressive expansion of compressed natural gas fueling infrastructure into new cities and highway corridors under Petroleum and Natural Gas Regulatory Board geographical area expansion that is bringing compressed natural gas fueling access to previously underserved markets. The total compressed natural gas vehicle population in India reached approximately 6.8 million vehicles in 2025 and is projected to grow to approximately 14.2 million by 2034 as original equipment manufacturers including Tata Motors, Ashok Leyland, and Maruti Suzuki expand their factory-fitted compressed natural gas vehicle offerings and state transport undertakings replace aging diesel bus fleets with compressed natural gas vehicles whose lower lifetime fuel and maintenance costs provide government operators with substantial budgetary savings at current compressed natural gas pricing. Each new compressed natural gas station requires steel distribution pipeline connection to the city gas distribution network at capital costs of approximately USD 80,000 to USD 150,000 per station for pipeline spur construction, metering, pressure regulation, and compression equipment, with the projected addition of approximately 8,400 new compressed natural gas stations by 2034 representing a pipeline infrastructure investment component of approximately USD 840 million to USD 1.26 billion that is directly driven by compressed natural gas vehicle fleet growth and is incremental to the residential and industrial piped natural gas connection pipeline investment.

Eastern India Pipeline Connectivity Deficit, Industrial Cluster Development, and Fertilizer Plant Feedstock Requirements Driving Trunk Pipeline Construction in Previously Unserved States

The completion of the Jagdishpur-Haldia-Bokaro-Dhamra pipeline and associated spur lines is unlocking natural gas access in the states of Uttar Pradesh, Jharkhand, Odisha, Bihar, and West Bengal that collectively represent India’s largest concentration of population and industrial activity without pipeline gas connectivity, creating the infrastructure foundation for a substantial wave of new industrial gas demand, city gas distribution rollout, and fertilizer plant construction that will generate sustained gas transmission volume growth through the forecast period. The revival and expansion of fertilizer plants along the Pradhan Mantri Urja Ganga corridor, including the Gorakhpur, Sindri, Barauni, and Talcher urea fertilizer plants whose construction or revamp is predicated on the availability of natural gas pipeline supply, represents a committed anchor demand of approximately 5 to 6 billion cubic meters per year for the eastern pipeline corridor that provides the baseload throughput justifying the pipeline’s capital investment and creating the utilization certainty required for Petroleum and Natural Gas Regulatory Board tariff determination. Industrial corridors including the Amritsar-Kolkata Industrial Corridor, the Eastern Dedicated Freight Corridor industrial nodes, and the National Investment and Manufacturing Zones designated along the eastern pipeline route are developing manufacturing and processing clusters whose natural gas consumption for industrial heating, process steam, and co-generation power requirements will generate incremental pipeline transmission demand estimated at approximately 3.2 billion cubic meters per year in aggregate by 2030, further reinforcing the economic case for eastern pipeline infrastructure investment and sustaining the capital expenditure programs of GAIL, Indian Oil, and the state pipeline entities developing spur and lateral connections to the Pradhan Mantri Urja Ganga trunk pipeline.

Key Challenges

Right-of-Way Acquisition Delays, Land Compensation Disputes, and Multi-Agency Statutory Clearance Requirements Creating Significant Pipeline Construction Timeline and Cost Overrun Risk

The most operationally acute challenge in India’s gas pipeline development is the protracted and legally contested right-of-way acquisition process required to secure access across the private agricultural land, forest land, government land, and urban real estate that long-distance pipeline routes must traverse, with compensation disputes, farmer resistance to perceived inadequate land payment, state government coordination failures, and judicial challenges to acquisition notifications generating average pipeline construction timeline delays of eighteen to thirty-six months beyond original project completion schedules and cost overruns of 15% to 35% above approved project estimates for major trunk pipeline projects. The Jagdishpur-Haldia-Bokaro-Dhamra pipeline, which was originally targeted for completion in 2019, experienced repeated delays attributable to right-of-way and forest clearance challenges across Uttar Pradesh and Jharkhand, illustrating the systemic nature of the right-of-way problem for large diameter, long-distance pipeline projects traversing multiple states with distinct land administration frameworks, compensation assessment methodologies, and political economy considerations that create unpredictable delays at individual pipeline sections. The multi-agency statutory clearance requirement for pipeline projects encompassing environmental impact assessment and forest clearance from the Ministry of Environment, Forest and Climate Change, national highway crossing permissions from the National Highways Authority of India, state industrial area crossing permissions from state pollution control boards and industrial development corporations, and irrigation canal and railway crossing approvals from the respective authorities creates a sequential and often non-coordinated approval gauntlet whose cumulative timeline consistently exceeds the simplified authorization frameworks envisaged in the Petroleum and Natural Gas Regulatory Board’s project development guidelines, requiring pipeline developers to dedicate substantial resources to regulatory liaison and legal management that adds to project overhead costs.

Domestic Natural Gas Price Regulation, Administered Pricing Mechanism Distortions, and Compressed Natural Gas Retail Price Sensitivity Creating Demand Uncertainty for Pipeline Throughput Economics

India’s natural gas pricing framework, which combines a government-administered price for domestically produced gas from legacy blocks regulated under the Administered Price Mechanism and market-determined prices for gas produced from deepwater and difficult terrain blocks alongside imported liquefied natural gas priced at international benchmarks, creates a complex and often opaque pricing environment in which different categories of gas consumers receive supply at materially different prices depending on their classification and the source of gas allocated to them, generating commercial disputes, demand distortions, and investment uncertainty that complicate the throughput projections and tariff recovery assumptions underlying pipeline project financial models. The compressed natural gas retail price, which varies significantly across city gas distribution geographical areas based on the gas procurement cost of individual operators, pipeline tariff levels, operating costs, and permitted marketing margins determined by market competition within the bounded geographical area license, has in several periods reached levels where the compressed natural gas-to-diesel price advantage narrowed to the point of reducing compressed natural gas vehicle conversion incentives for new fleet operators, creating compressed natural gas station utilization uncertainty and complicating the investment case for city gas distribution network expansion in areas where compressed natural gas retail price competitiveness relative to diesel is the primary demand growth driver. The domestic natural gas production decline from the KG-D6 basin of approximately 10 billion cubic meters per year in 2015 to below 3 billion cubic meters per year by 2020 before partial recovery, combined with limited new domestic production additions that are insufficient to meet projected consumption growth, has increased India’s reliance on imported liquefied natural gas at international prices that introduce currency and commodity price volatility into the landed cost of gas supply that is ultimately reflected in end-consumer pricing and demand sensitivity across industrial, power, and city gas distribution consumption categories.

Inadequate Storage Infrastructure, Seasonal Demand Variability, and Grid Balancing Challenges Creating Operational Reliability and Commercial Efficiency Constraints on the National Gas Grid

India’s national gas grid operates without meaningful underground gas storage infrastructure, relying entirely on pipeline linepack and liquefied natural gas terminal send-out flexibility to manage supply-demand imbalances on a daily and seasonal basis, creating a fundamental operational vulnerability in which the grid cannot buffer supply disruptions, accommodate seasonal demand peaks in the compressed natural gas and piped natural gas sectors, or manage the interplay between variable domestic production, liquefied natural gas cargo arrival timing, and fluctuating consumption that characterizes a mature and efficiently operating national gas transmission system. Underground gas storage, which is standard infrastructure in all major gas markets including the United States, European Union, and China where aggregate storage capacity typically equals 10% to 20% of annual gas consumption providing thirty to ninety days of supply security buffer, is conspicuously absent from India’s gas infrastructure portfolio despite multiple government studies and policy discussions spanning over two decades, leaving the national gas grid dependent on just-in-time supply balancing that creates commercial risk for pipeline operators whose transmission agreements require firm capacity delivery commitments and operational stress during supply shortfalls including liquefied natural gas cargo delays, vessel force majeure events, and domestic production disruptions. The operational complexity of managing gas quality specifications across the national grid, where gas supplied from different production sources and liquefied natural gas terminals with varying calorific values, sulfur content, and gas composition must be blended to within Petroleum and Natural Gas Regulatory Board quality standards at interconnection points before delivery to downstream consumers whose equipment is calibrated for specific gas specifications, creates technical challenges and commercial disputes between shippers and pipeline operators that increase transaction costs and reduce the attractiveness of the gas market for new participants seeking transparent and standardized access to pipeline infrastructure.

Market Segmentation

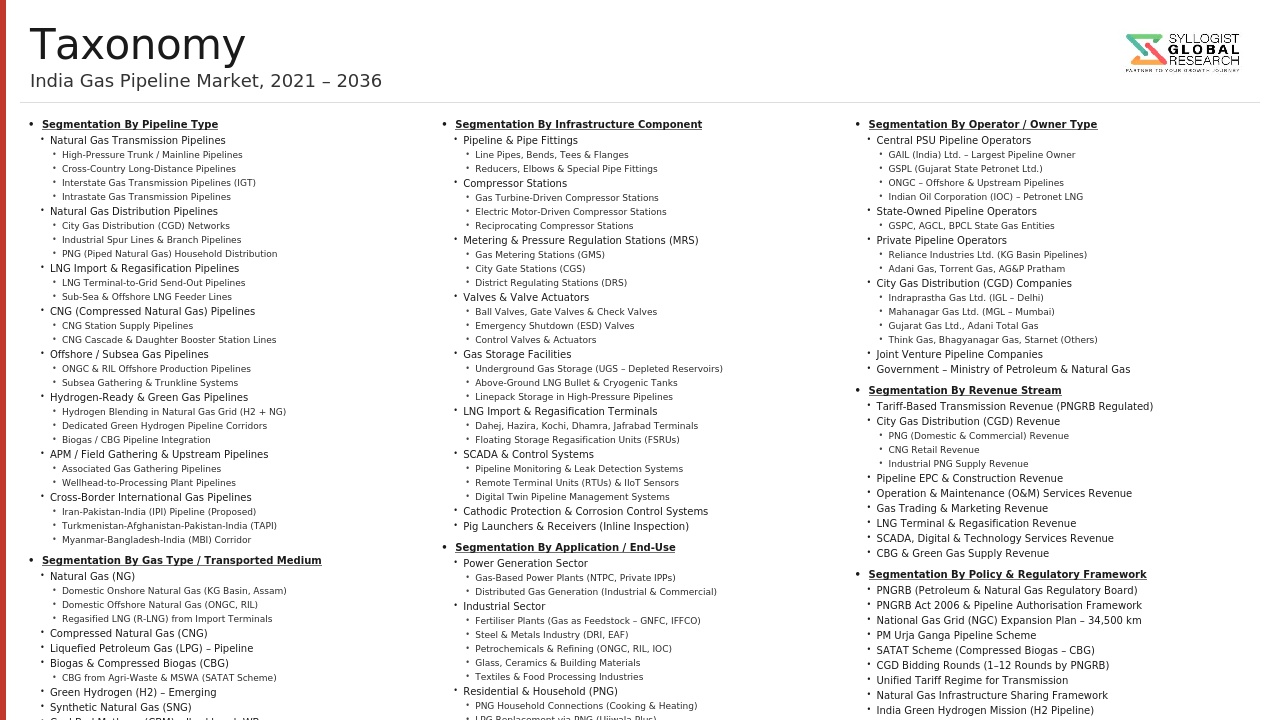

- Segmentation By Pipeline Type

- Cross-Country Transmission Pipelines (High-Pressure Trunk Lines)

- Spur and Lateral Pipelines (Transmission Interconnects)

- City Gas Distribution Steel Distribution Networks

- City Gas Distribution Polyethylene Service Lines

- LNG Terminal Interconnect and Regasification Pipelines

- Offshore Gas Pipeline Connections

- Others

- Segmentation By Diameter

- Large Diameter (Above 600 mm)

- Medium Diameter (300 to 600 mm)

- Small Diameter (Below 300 mm)

- Segmentation By Application

- Power Generation (Gas-Fired Power Plants)

- Fertilizer and Ammonia Production

- Industrial Process and Manufacturing

- Compressed Natural Gas (CNG) Vehicle Fueling

- Piped Natural Gas (PNG) Residential and Commercial

- Petrochemical and Refinery Feedstock

- Steel and Sponge Iron Manufacturing

- Others

- Segmentation By Ownership and Operator Type

- Central Public Sector Undertakings (GAIL, Indian Oil, ONGC)

- State Public Sector Undertakings (GSPC, MPNG, Assam Gas, and Others)

- Private Sector Pipeline Operators

- City Gas Distribution Licensed Entities (Public and Private)

- Joint Venture Pipeline Companies

- Others

- Segmentation By Construction Activity

- New Pipeline Construction and Greenfield Projects

- Pipeline Expansion and Capacity Augmentation

- Spur and Lateral Connection Development

- Pipeline Replacement and Rehabilitation

- Operations, Maintenance, and Integrity Management

- Others

- Segmentation By Region

- North India (Delhi NCR, Uttar Pradesh, Punjab, Rajasthan, and Haryana)

- West India (Gujarat, Maharashtra, and Goa)

- South India (Andhra Pradesh, Telangana, Tamil Nadu, Kerala, and Karnataka)

- East India (West Bengal, Odisha, Jharkhand, and Bihar)

- Northeast India (Assam, Meghalaya, Tripura, and Other Northeastern States)

- Central India (Madhya Pradesh and Chhattisgarh)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Gas Pipelines Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by pipeline type including cross-country transmission, spur and lateral lines, city gas distribution steel and polyethylene networks, and LNG terminal interconnects, by application including power generation, fertilizer production, industrial use, CNG vehicle fueling, and PNG residential and commercial connections, and by operator type including central and state public sector undertakings and private and joint venture entities, to enable pipeline operators, engineering procurement and construction contractors, pipe manufacturers, city gas distribution entities, government policy planners, and infrastructure investors to identify the highest-growth pipeline categories and geographic regions generating the most commercially durable investment demand across the forecast period to 2034?

- What is the current construction status, remaining capital expenditure requirement, authorized capacity, projected commissioning timeline, and anticipated industrial and city gas distribution demand generation of the Jagdishpur-Haldia-Bokaro-Dhamra pipeline, the North East Gas Grid, the Srikakulam-Angul pipeline, and other priority national gas grid expansion projects, and how do the right-of-way acquisition challenges, multi-agency clearance timelines, and viability gap funding requirements of these projects affect their completion schedules and the realization of the gas market development benefits expected in the eastern, northeastern, and southern states whose energy access and industrial development are contingent on pipeline gas connectivity becoming available within policy target timelines?

- What is the Petroleum and Natural Gas Regulatory Board’s current geographical area authorization coverage across the 296 authorized city gas distribution areas, what are the compressed natural gas station and piped natural gas connection work program obligations and compliance performance of major city gas distribution entities including Indraprastha Gas, Mahanagar Gas, Adani Total Gas, Gujarat Gas, and GAIL Gas, and what capital investment programs are these entities executing to meet their Petroleum and Natural Gas Regulatory Board minimum work program milestones, and what are the projected piped natural gas connection additions, compressed natural gas station additions, and annual gas volume growth trajectories by city gas distribution operator and geographic region through 2034 as ninth and tenth round geographical area authorization entities build out their network coverage?

- How is the administered natural gas pricing framework for domestically produced gas, the market-determined pricing for deepwater and difficult terrain block production, and the landed cost variability of imported liquefied natural gas affecting the end-consumer pricing of compressed natural gas and piped natural gas across different city gas distribution geographical areas in India, and what are the projected impacts of Reliance Industries KG-D6 production ramp-up, ONGC deepwater gas production additions, and expected increases in liquefied natural gas import volumes on domestic gas availability, pipeline throughput utilization, and the tariff recovery economics of new pipeline investments whose financial viability depends on achieving minimum throughput levels within defined operating periods?

- What are the government’s plans, technical feasibility studies, proposed locations, storage capacity targets, and investment framework for developing underground natural gas storage infrastructure in India, and how would operational underground gas storage of 3 to 5 billion cubic meters capacity at strategic locations including depleted offshore fields in the western offshore basin, potential aquifer storage sites in Rajasthan and Gujarat, and former producing onshore fields in Assam and Andhra Pradesh address the grid balancing, supply security, and seasonal demand management challenges that currently constrain the operational efficiency of India’s national gas grid, and what regulatory and commercial frameworks under the Petroleum and Natural Gas Regulatory Board would govern underground storage access, injection and withdrawal rights, and tariff determination for future underground gas storage infrastructure?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Zonal & State Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Domestic Gas Supply Availability, Price Pooling & Allocation Policy Risk

- Right-of-Way (RoW) Acquisition, Land Encroachment & Construction Delay Risk

- Regulatory Tariff, PNGRB Order Revision & Pipeline Tariff Dispute Risk

- LNG Import Price Volatility, Global Gas Market Exposure & Regasification Capacity Adequacy Risk

- Pipeline Safety, Third-Party Damage, Corrosion & Operational Integrity Risk

- Regulatory Framework & Standards

- PNGRB (Petroleum & Natural Gas Regulatory Board) Act 2006: Pipeline Authorisation, Tariff Regulation, Open Access Policy, Common Carrier & Contract Carrier Framework for India Natural Gas Transmission

- PNGRB CGD Network Bidding: City Gas Distribution Licence Award Process, Minimum Work Programme (MWP), Geographical Area (GA) Allocation & CGD Network Expansion Policy Under 11th & 12th CGD Bid Rounds

- Gas Pipeline Design, Construction & Safety Standards: ASME B31.8, IS 1239, OISD STD 141 & 214, Petroleum & Natural Gas (Safety in Offshore Operations) Rules & Pipeline Act 1962 Compliance

- Natural Gas Pricing Policy: APM Gas Price, ONGC & Reliance Pricing, HELP (Hydrocarbon Exploration & Licensing Policy), Administered Price Mechanism for CNG & PNG & Gas Marketing Freedom

- India National Gas Grid Vision, PM Urja Ganga Scheme, Gas-Based Economy Target (15% of Energy Mix by 2030) & SATAT (Sustainable Alternative Towards Affordable Transportation) Bio-CNG Policy

- India Gas Pipelines Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Pipeline Length in km & Throughput in MMSCMD)

- Market Size & Forecast by Pipeline Type

- Natural Gas High-Pressure Transmission Pipeline (National Gas Grid Trunk Line)

- Cross-Country Natural Gas Pipeline

- Spur Pipeline & Feeder Line to Industrial Cluster, Power Plant & Fertiliser Complex

- City Gas Distribution (CGD) Steel & HDPE Network: Domestic PNG & Commercial Connections

- CNG Station Supply Pipeline & Compressed Natural Gas Dispensing Network

- LNG Receiving Terminal Connectivity & Regasified LNG (R-LNG) Transmission Pipeline

- LNG Satellite Station & Mini-LNG Terminal Supply Pipeline

- Associated Gas & Upstream Gathering Pipeline (ONGC, OIL & Private Upstream)

- Compressed Biogas (CBG) & Bio-CNG Pipeline under SATAT Scheme

- Market Size & Forecast by Gas Type

- Domestic Natural Gas (APM Gas: ONGC & OIL, Non-APM: Reliance, GSPC & Others)

- Regasified LNG (R-LNG from Dahej, Hazira, Kochi, Ennore & Dhamra LNG Terminals)

- Compressed Natural Gas (CNG) for Transport Sector

- Piped Natural Gas (PNG) for Domestic, Commercial & Industrial Household Supply

- Compressed Biogas (CBG) & Bio-CNG under SATAT Policy Framework

- Hydrogen Blended Natural Gas (Pilot Phase: IGL, GAIL & NTPC Green Hydrogen Blending)

- Market Size & Forecast by Infrastructure Category

- PNGRB-Authorised National Natural Gas Grid (GAIL, GSPL, GIGL, GITL, AGCL & Others)

- State Gas Pipeline Infrastructure (State PSU Networks: MGL, GGL, HPGL, TNGCL)

- City Gas Distribution (CGD) Network (Licensed GA Operators: IGL, MGL, ATGL, GAIL Gas, Gujarat Gas)

- LNG Terminal & Regasification Infrastructure Pipeline Connection

- Captive & Dedicated Pipeline (Fertiliser, Power & Industrial Complex Direct Connection)

- Market Size & Forecast by Pipe Material

- Carbon Steel (API 5L Gr. X52 to X80 for High-Pressure Transmission & CGD Steel Network)

- High-Density Polyethylene (HDPE PE 80 & PE 100 for CGD Last-Mile Distribution)

- Ductile Iron (DI) Pipe for Urban CGD Network in High-Traffic & Dense Localities

- Stainless Steel & Alloy Steel for High-Pressure, High-Temperature & Corrosive Applications

- Market Size & Forecast by End-Use Sector

- Power Generation: Gas-Based Power Plant (CCGT & OCGT) & Captive Power Plant

- Fertiliser & Urea Manufacturing (Major Gas Consumer: IFFCO, NFL, RCF, GNFC)

- Industrial: Steel, Cement, Ceramics, Glass, Textile & Food Processing

- Household Piped Natural Gas (PNG) Domestic Connection

- Transport: CNG for Passenger Vehicle, Auto-Rickshaw, Bus & Commercial Fleet

- Commercial & Institutional: Hotels, Hospitals, Restaurants & Educational Institutions

- Petrochemical & Refinery Feedstock & Fuel

- Market Size & Forecast by Project Type

- Greenfield Transmission Pipeline Project (New Cross-Country & Trunk Line)

- Brownfield Capacity Augmentation & Loop Line Addition

- New CGD Licence Area Rollout (11th, 12th & Future PNGRB CGD Bid Rounds)

- LNG Terminal & Satellite Station Pipeline Integration Project

- Spur Line & Extension to Underserved Industrial & Urban Cluster

- Market Size & Forecast by End-User

- GAIL (India) Ltd. (National Gas Transmission & Marketing)

- Gujarat State Petronet Ltd. (GSPL) & Gujarat Gas Ltd. (State Pipeline & CGD)

- Adani Total Gas Ltd. (ATGL), Indraprastha Gas Ltd. (IGL) & Mahanagar Gas Ltd. (MGL)

- Indian Oil Corporation (IOCL), HPCL & BPCL Pipeline & CGD Subsidiaries

- ONGC, OIL & Upstream Gas Producer Pipeline Users

- Independent Power Producer, Fertiliser Plant & Large Industrial Gas Consumer

- Market Size & Forecast by Sales Channel

- PNGRB Competitive Bid & EPC Turnkey Contract Award

- State PSU Direct Procurement & Government Award

- Joint Venture, Co-Development & Investment Partnership

- Equipment Supply, Material Procurement & O&M Service Contract

- North India Gas Pipelines Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Pipeline Length in km & Throughput in MMSCMD)

- By Pipeline Type

- By Gas Type

- By Infrastructure Category

- By Pipe Material

- By End-Use Sector

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- West India Gas Pipelines Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Pipeline Length in km & Throughput in MMSCMD)

- By Pipeline Type

- By Gas Type

- By Infrastructure Category

- By Pipe Material

- By End-Use Sector

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- South India Gas Pipelines Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Pipeline Length in km & Throughput in MMSCMD)

- By Pipeline Type

- By Gas Type

- By Infrastructure Category

- By Pipe Material

- By End-Use Sector

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- East India Gas Pipelines Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Pipeline Length in km & Throughput in MMSCMD)

- By Pipeline Type

- By Gas Type

- By Infrastructure Category

- By Pipe Material

- By End-Use Sector

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Central India Gas Pipelines Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Pipeline Length in km & Throughput in MMSCMD)

- By Pipeline Type

- By Gas Type

- By Infrastructure Category

- By Pipe Material

- By End-Use Sector

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- State-Wise* India Gas Pipelines Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Pipeline Length in km & Throughput in MMSCMD)

- By Pipeline Type

- By Gas Type

- By Infrastructure Category

- By Pipe Material

- By End-Use Sector

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

*States Analyzed in the Syllogist India Research Portfolio: Gujarat, Maharashtra, Uttar Pradesh, Madhya Pradesh, Rajasthan, Haryana, Punjab, Delhi NCR, Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala, West Bengal, Odisha, Jharkhand, Bihar, Assam, Chhattisgarh, Uttarakhand, Goa

- Technology Landscape & Innovation Analysis

- High-Pressure Natural Gas Transmission Pipeline Design, Coating, Anti-Corrosion & Cathodic Protection Technology Deep-Dive

- City Gas Distribution (CGD) HDPE & Steel Network Design, Pressure Regulation, Metering & District Regulator Station Technology

- SCADA, Telemetry, Pipeline Integrity Management System (PIMS), Real-Time Leak Detection & GIS Mapping Technology

- LNG Receiving Terminal, Cryogenic Storage, Regasification, Satellite LNG & Mini-LNG Station Pipeline Integration Technology

- CNG Compression, Cascade Storage, Dispensing Station & Online CNG (OCNG) Technology for India Transport Sector

- In-Line Inspection (ILI), Smart Pigging, Pipeline Rehabilitation, Repair & Life Extension Technology

- Hydrogen Blending, Green Hydrogen Pipeline Infrastructure & Bio-CNG (CBG) Integration Technology for India Gas Network

- Patent & IP Landscape in Gas Pipeline Technologies Relevant to India

- Value Chain & Supply Chain Analysis

- Gas Supply Chain: Domestic Upstream Production (ONGC, OIL, Reliance), LNG Import Terminal & Spot/Term LNG Procurement

- Line Pipe, Fittings & Valve Manufacturing Supply Chain: India Domestic Mills (Welspun, Jindal SAW, APL Apollo, Ratnamani) & Import Channel

- Compressor, Metering, Pressure Regulation & Instrumentation Equipment Supply Chain

- EPC Contractor & Pipeline Construction Contractor Landscape (KEC, L&T, Megha Engineering, Technipfmc India)

- Gas Transmission, CGD Operator & City Gas Distribution Company Integration

- Gas Marketing, Trading & End-Consumer Supply Distribution

- O&M Service, Integrity Management, Inspection & Pipeline Rehabilitation

- Pricing Analysis

- PNGRB Natural Gas Transmission Tariff: Zone-Based Unified Tariff Structure, Pipeline-Specific Tariff & Open Access Tariff Analysis

- Domestic APM Gas Price (ONGC & OIL) vs. Non-APM Gas Price (RIL KG-D6, GSPC) & Price Pooling Mechanism

- R-LNG (Regasified LNG) Landed Cost Analysis: LNG Import Price, Terminal Use Charge & Transmission Tariff to Delivered City Gate Price

- CNG & PNG Retail Price Build-Up Analysis: Gas Cost, Transmission Tariff, CGD Margin, VAT & Central Excise Impact on End-Consumer Price

- Line Pipe, Fittings & Valve Domestic vs. Import Price Comparison: Steel Pipe (API 5L) & HDPE Pipe Cost Analysis

- CGD Infrastructure Capital Cost & Project Economics: Per-Connection PNG Capital Cost, CNG Station Capex & Payback Period Analysis

- Sustainability & Environmental Analysis

- Natural Gas as Bridge Fuel: GHG Emission Comparison of Gas vs. Coal & Oil in India Power Generation, Industrial & Transport Applications

- CNG & PNG Air Quality Co-Benefit: Particulate Matter (PM2.5, PM10) & NOx Reduction in India Urban Centres from Transport & Household Fuel Switching

- Methane Leak Detection, Fugitive Emission Monitoring & India’s NDC Commitment to Methane Reduction from Gas Pipeline Infrastructure

- SATAT Bio-CNG Programme: Circular Economy, Agricultural Waste Valorisation & Biomethane Contribution to India’s Renewable Energy & Natural Farming Goals

- Green Hydrogen & Hydrogen Blending in India Gas Network: NHTP (National Hydrogen Mission) Pathway, Low-Carbon Gas Grid Transition & PNGRB Hydrogen Pipeline Policy

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Dominated by PSU vs. Emerging Private Sector by Pipeline Type)

- Top 10 Players Market Share by Pipeline Length, Throughput & CGD Connections

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Pipeline Type, End-Use Sector & Geographic Zone

- Player Classification

- National Gas Transmission PSU (GAIL India, GSPL, GIGL, GITL, AGCL)

- City Gas Distribution (CGD) Operator: Listed & Unlisted CGD Companies (IGL, MGL, ATGL, Gujarat Gas, GAIL Gas)

- Integrated Oil & Gas PSU with Pipeline Division (IOCL, HPCL, BPCL, ONGC)

- State Pipeline & Gas PSU (GGCL, MNGL, TNGCL, GSPC, Assam Gas Company)

- Private Sector CGD & Pipeline Operator (Torrent Gas, Adani Total Gas, Think Gas)

- Line Pipe & Material Manufacturer (Welspun Corp, Jindal SAW, APL Apollo, Ratnamani Metals)

- EPC & Pipeline Construction Contractor (L&T, KEC International, Megha Engineering, Spice Energy)

- Compressor, Metering, Valve & Equipment Supplier (Ingersoll Rand, Atlas Copco India, L&T Valves, Forbes Marshall)

- Competitive Analysis Frameworks

- Market Share Analysis by Pipeline Length, Throughput, CGD Connections & Zone

- Company Profile

- Company Overview & Registered Office

- Gas Pipeline & CGD Products, Services & Network Portfolio

- Key Customer Relationships & Off-Take Agreements

- Network Footprint, Pipeline Length (km) & Authorised GA Count

- Revenue (Gas Pipeline & CGD Segment) & EBITDA

- Technology Differentiators & Key Infrastructure Assets

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (New Pipeline Commissioning, CGD Expansion, Regulatory Wins)

- SWOT Analysis

- Strategic Focus Areas & Growth Roadmap

- Competitive Positioning Map (Network Scale vs. Geographic Reach)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Pipeline Type, Gas Type, End-Use Sector, Infrastructure Category & Zone

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Network Expansion & Pipeline Portfolio Investment Strategy

- Operations, Integrity Management & Operational Excellence Strategy

- Geographic Expansion & New CGD Licence Area Entry Strategy

- Customer & End-Use Sector Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Green Hydrogen & Bio-CNG Integration Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)