Market Definition

The Global Gas-to-Liquids Technologies Market encompasses the process engineering, catalyst development, proprietary technology licensing, equipment manufacturing, plant construction, and commercial operation of conversion systems that transform natural gas, associated gas, stranded gas, biogas, synthetic gas derived from biomass or waste gasification, and in an emerging subset of the market, synthesis gas produced from green hydrogen and captured carbon dioxide, into liquid hydrocarbon products including synthetic diesel, naphtha, kerosene, jet fuel, lubricant base oils, waxes, and liquid petroleum chemicals through a sequence of chemical conversion steps. The primary conversion pathway within gas-to-liquids technology involves the partial oxidation or steam reforming of methane-rich feedstock gas into synthesis gas comprising hydrogen and carbon monoxide, followed by Fischer-Tropsch synthesis over iron or cobalt catalysts at controlled temperature and pressure conditions to polymerize the synthesis gas into a distribution of hydrocarbon chains, and subsequent hydrocracking and isomerization to upgrade the Fischer-Tropsch wax and raw syncrude into finished liquid fuel and chemical product specifications. The market additionally encompasses the methanol-to-gasoline and methanol-to-olefins conversion pathway in which synthesis gas is first converted to methanol and subsequently converted to transportation fuels or petrochemical feedstocks using zeolite catalysts, the compact and modular gas-to-liquids technologies designed for monetization of stranded gas resources, associated gas flaring elimination, and remote location liquid fuel production at scales from below 1,000 barrels per day to several thousand barrels per day that are technically and economically distinct from large-scale Fischer-Tropsch facilities of 100,000 barrels per day or more. The market is increasingly intersecting with the power-to-liquids and e-fuels technology space in which green hydrogen electrolysis and direct air capture or point-source carbon dioxide capture generate a synthetic equivalent feedstock for Fischer-Tropsch or methanol synthesis using renewable energy, creating a pathway for carbon-neutral synthetic fuels production that builds on conventional gas-to-liquids process technology. Key participants include technology licensors, engineering procurement and construction contractors, catalyst manufacturers, national oil companies, independent gas producers, specialty chemical companies, and aviation and maritime operators seeking low-carbon synthetic fuel supply.

Market Insights

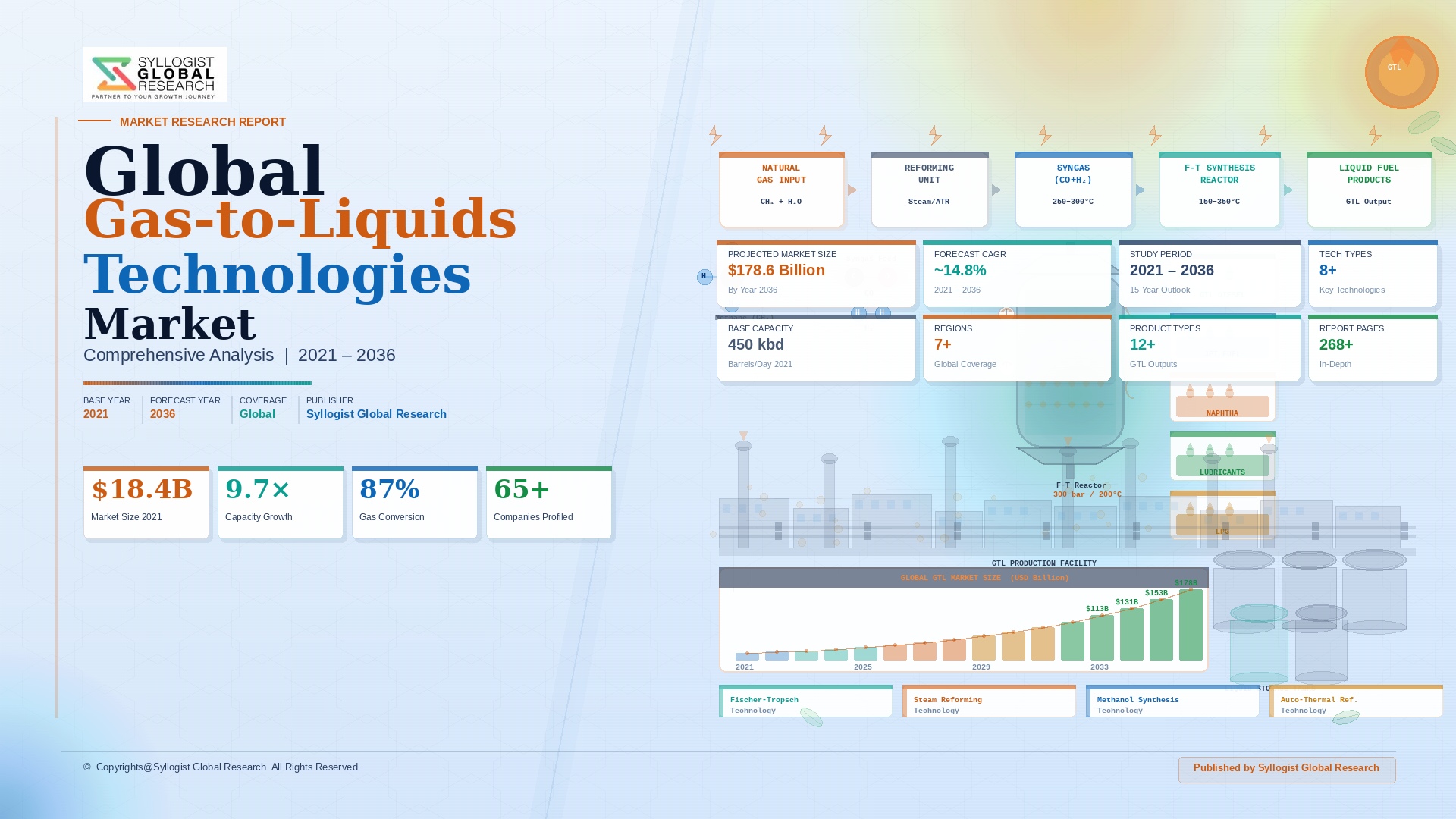

The global gas-to-liquids technologies market was valued at approximately USD 12.4 billion in 2025 and is projected to reach USD 24.8 billion by 2034, advancing at a compound annual growth rate of 8.0% over the forecast period from 2027 to 2034, driven by the growing imperative to monetize stranded natural gas reserves that lack pipeline or liquefied natural gas export infrastructure access, the accelerating regulatory pressure to eliminate associated gas flaring at oil production sites globally, the strategic interest of gas-rich nations in developing downstream liquid fuel and chemical production industries that capture more value from their hydrocarbon resource endowments, and the nascent but structurally significant convergence of gas-to-liquids process technology with the power-to-liquids synthetic fuel production pathway that is attracting investment from aviation, shipping, and heavy transport operators seeking carbon-neutral synthetic hydrocarbon fuel supply. Global stranded natural gas reserves available for in-situ monetization through gas-to-liquids conversion are estimated at approximately 2,800 trillion cubic feet across sub-Saharan Africa, the Middle East, Southeast Asia, Central Asia, and remote North American basins whose distance from existing pipeline infrastructure, insufficient volume for standalone liquefied natural gas liquefaction economics, or flaring regulatory compliance requirements make gas-to-liquids an economically and strategically attractive monetization alternative that generates liquid products with established transportation logistics, established commodity markets, and premium pricing relative to wellhead natural gas values in stranded location contexts. The total installed gas-to-liquids conversion capacity globally reached approximately 560,000 barrels of liquid product per day in 2025, concentrated in the mega-scale Fischer-Tropsch facilities operated by Shell at Pearl in Qatar at 140,000 barrels per day, Sasol at Oryx and Escravos with aggregate capacity of approximately 62,000 barrels per day, and PetroSA at its Mossel Bay plant in South Africa, with these large-scale facilities collectively accounting for approximately 68% of total installed global capacity and demonstrating the commercial viability of Fischer-Tropsch technology at industrial scale over multiple decades of continuous operation.

The modular and small-scale gas-to-liquids technology segment, targeting associated gas monetization at oil production sites, remote stranded gas fields, and biogas upgrading applications at scales of 500 to 10,000 barrels per day, is the most commercially dynamic growth segment within the global market, growing at approximately 14.8% annually in 2025 as regulatory enforcement of flaring reduction obligations, economic incentive structures for associated gas monetization in Nigeria, Russia, Iraq, Angola, and the United States Permian Basin, and the development of compact Fischer-Tropsch reactor designs that achieve economically viable conversion efficiency at small scale collectively create demand for deployable gas-to-liquids solutions that can be installed at wellsite or gathering system locations without the pipeline infrastructure required for conventional gas monetization. The World Bank’s Global Gas Flaring Reduction Partnership has documented continued flaring of approximately 144 billion cubic meters of associated gas globally in 2024, equivalent to the combined annual gas consumption of Sub-Saharan Africa and Central America, representing a wasted energy resource of approximately USD 25 billion in natural gas value at typical field-gate pricing and a source of approximately 400 million metric tons of carbon dioxide equivalent annually that is progressively being targeted by national regulations including the United States Bureau of Land Management zero routine flaring rule for federal and tribal lands, Nigeria’s flaring prohibition enforcement program, and Iraq’s gas utilization program, each of which creates a regulatory compliance driver for associated gas monetization through gas-to-liquids technology deployment at production sites where the gas volumes are insufficient for pipeline gathering or liquefied natural gas economics. Technology providers including Velocys, SGP BioEnergy, INFRA Technology, and Greyrock Energy have developed second-generation modular Fischer-Tropsch systems with improved catalyst life, thermal management, and process intensification that are achieving commercial demonstration milestones necessary for full-scale deployment across oil field associated gas monetization programs in the United States, Nigeria, and the Middle East.

The intersection of conventional gas-to-liquids Fischer-Tropsch process technology with the emerging power-to-liquids synthetic fuel production pathway represents the most strategically significant long-term market development within the gas-to-liquids industry, as aviation, shipping, and heavy transport operators facing mandatory decarbonization obligations under regulatory frameworks including the European Union Sustainable Aviation Fuel mandate requiring 2% sustainable aviation fuel blend by 2025 escalating to 70% by 2050, the International Maritime Organization’s greenhouse gas strategy targeting net-zero shipping emissions by 2050, and the International Civil Aviation Organization’s Carbon Offsetting and Reduction Scheme for International Aviation are driving investment in power-to-liquids facilities that produce carbon-neutral synthetic jet fuel, marine diesel, and other liquid hydrocarbons through Fischer-Tropsch synthesis of hydrogen from electrolysis and carbon dioxide from direct air capture or point-source capture. The lifecycle carbon intensity of power-to-liquids synthetic fuels approaches zero or below zero when produced from renewable electricity and direct air capture carbon dioxide, compared to approximately 75 to 90 grams of carbon dioxide equivalent per megajoule for conventional fossil jet fuel, making power-to-liquids the only liquid fuel pathway capable of delivering genuine lifecycle carbon neutrality for long-haul aviation where battery electrification is technically infeasible and hydrogen combustion faces infrastructure and safety adoption barriers. Norsk e-Fuel, HIF Global, Twelve, and Carbon Engineering-backed facilities are advancing power-to-liquids commercial demonstration programs in Norway, Chile, Germany, and Canada whose production cost trajectories from approximately USD 8 to USD 12 per liter in 2025 toward projected USD 2 to USD 3 per liter by the mid-2030s as electrolyzer costs, renewable electricity prices, and direct air capture costs decline simultaneously represent the economic threshold at which power-to-liquids sustainable aviation fuel achieves commercial blending economics without mandate-driven price support.

The gas-to-chemicals pathway within the broader gas-to-liquids technology market, which routes synthesis gas and Fischer-Tropsch products toward high-value specialty chemical and lubricant base oil production rather than transportation fuel blending, is generating premium economics that improve the financial viability of gas-to-liquids projects in contexts where transportation fuel commodity pricing alone provides insufficient return on the substantial capital investment required for gas-to-liquids plant construction. Fischer-Tropsch wax, which is the heaviest product fraction from cobalt-catalyzed Fischer-Tropsch synthesis at approximately 200 to 220 degrees Celsius, commands prices of approximately USD 1,400 to USD 2,200 per metric ton for high-purity grades used in specialty applications including food-contact packaging coatings, cosmetics, candle manufacturing, and hot-melt adhesive formulation, substantially above the equivalent energy-basis value of the wax when upgraded to diesel, creating a product slate optimization incentive for gas-to-liquids operators to maximize wax yield and minimize hydrocracking severity. The gas-to-olefins pathway through methanol intermediate production and methanol-to-olefins zeolite conversion is attracting particular investment interest in China, where coal-to-methanol and gas-to-methanol plants feeding methanol-to-olefins facilities have created a substantial domestic synthetic olefin production industry whose economics are competitive with naphtha cracking at Chinese coal and gas pricing, providing a template for gas-to-liquids technology deployment in the Middle East, Central Asia, and North Africa where stranded gas monetization through methanol and olefin production into the Asian petrochemical market represents a commercially attractive development opportunity for national gas producers seeking to diversify energy export revenues toward higher-value chemical commodities.

Key Drivers

Global Associated Gas Flaring Reduction Regulations and Stranded Gas Monetization Imperatives Creating Structural Demand for Modular Gas-to-Liquids Deployment at Oil Production Sites

The converging regulatory, economic, and reputational pressure on oil-producing nations and companies to eliminate routine associated gas flaring is creating a substantial and growing demand for modular gas-to-liquids technology as the technically feasible and economically viable alternative to flaring at production sites where associated gas volumes are insufficient for conventional monetization through pipeline gathering or liquefied natural gas processing, establishing a well-defined and large addressable market for compact Fischer-Tropsch technology providers capable of delivering deployable, field-installable, and operationally reliable conversion systems. The World Bank Zero Routine Flaring initiative, which has been endorsed by over 80 governments and oil companies committing to eliminate routine associated gas flaring by 2030, combined with the United States Bureau of Land Management’s zero routine flaring rule effective 2025 for federal and tribal lands that imposes financial penalties for non-compliance, Nigeria’s revised Flare Gas Prevention of Waste and Pollution Regulations prescribing a USD 2.00 per thousand standard cubic feet flaring penalty, and Iraq’s gas utilization program targets collectively create a regulatory compliance cost for flaring that progressively erodes the economics of continued flaring relative to gas monetization investment in major producing nations. The Permian Basin of Texas and New Mexico alone flared approximately 590 million cubic feet per day of associated gas in 2025 from wells without sufficient pipeline takeaway capacity, representing an annual wasted gas value of approximately USD 430 million at prevailing regional natural gas prices and a direct financial case for gas-to-liquids deployment at gathering system hubs serving clustered production areas where aggregate volumes justify modular plant investment at payback periods of four to six years based on synthetic diesel and naphtha sales revenue at current product prices.

Aviation and Maritime Decarbonization Mandates Driving Demand for Fischer-Tropsch-Derived Synthetic Sustainable Fuels and Power-to-Liquids Technology Investment

The regulatory mandated transition of the aviation and maritime industries toward low-carbon fuels under binding blending obligation frameworks, carbon offset requirements, and emissions intensity reduction targets is creating a structurally growing and long-term demand stream for Fischer-Tropsch-derived synthetic sustainable aviation fuel and synthetic marine diesel that represents the most commercially significant new market opportunity for gas-to-liquids and power-to-liquids technology providers, positioning process technology licensors, engineering firms, and project developers with Fischer-Tropsch expertise as critical enablers of aviation and shipping decarbonization strategies that have no technically equivalent alternatives for long-haul high-energy-density applications. The European Union Sustainable Aviation Fuel regulation mandates increasing synthetic aviation fuel blending ratios from 1.2% in 2030 escalating to 35% by 2040 and 70% by 2050 of total aviation fuel supply at EU airports, with power-to-liquids pathways using green hydrogen and captured carbon dioxide specifically incentivized through separate sub-targets of 0.7% by 2030 and 10% by 2040, creating contractual off-take demand that project developers can use to secure financing for first-of-kind commercial power-to-liquids facilities. The International Maritime Organization’s 2023 revised greenhouse gas strategy targeting a 20% to 30% greenhouse gas reduction by 2030, 70% to 80% by 2040, and net zero by 2050 relative to 2008 levels, combined with the European Union FuelEU Maritime regulation requiring a 2% reduction in the greenhouse gas intensity of maritime fuels by 2025 escalating to 80% by 2050, is driving shipping company investment in synthetic marine fuel supply chain development and generating contracted fuel offtake demand for power-to-liquids and biomass-to-liquids Fischer-Tropsch projects whose long-term supply agreements provide the revenue certainty required for USD 500 million to USD 2 billion commercial facility financing.

Gas-Rich Nations Pursuing Downstream Value Addition Strategies and Energy Diversification Programs Investing in Gas-to-Liquids as a Petrochemical and Fuel Production Platform

National energy strategies across the Middle East, Central Asia, Sub-Saharan Africa, and Southeast Asia that prioritize transformation of exported raw natural gas into higher-value liquid hydrocarbons, petrochemicals, and specialty chemicals as a domestic industrial development, employment creation, and export revenue diversification objective are sustaining strategic investment in gas-to-liquids technology at scales that extend beyond what pure commercial return analysis would justify, reflecting the full socioeconomic benefit calculus of downstream hydrocarbon processing investment for resource-rich developing economies. Qatar, whose Pearl gas-to-liquids plant operated by Shell at 140,000 barrels per day represents the world’s largest gas-to-liquids facility and has demonstrated commercially viable operations over more than a decade of production, continues to evaluate expanded gas-to-liquids capacity as part of its North Field expansion program as a pathway for converting incremental natural gas production into premium synthetic fuels and base oils that command higher revenues than liquefied natural gas export prices in oversupplied global gas markets. Saudi Arabia’s Vision 2030 industrial diversification program, Nigeria’s gas utilization and industrialization strategy targeting domestic gas processing infrastructure, Mozambique’s ambition to develop domestic value-added gas processing alongside its emerging liquefied natural gas export industry, and Turkmenistan’s gas-to-liquids investments at its Kiyanly polymer plant complex collectively illustrate the breadth of national strategic commitment to downstream gas processing investment across gas-rich developing nations that is creating a sustained and geographically diverse project pipeline for gas-to-liquids technology licensors, engineering procurement and construction firms, and catalyst suppliers through the forecast period.

Key Challenges

High Capital Intensity of Gas-to-Liquids Plants, Sensitivity to Natural Gas Feedstock and Liquid Product Price Differentials, and Long Payback Periods Creating Investment Hesitancy

Large-scale gas-to-liquids facilities are among the most capital-intensive hydrocarbon processing projects in the energy industry, with the capital cost of a world-scale Fischer-Tropsch plant of 100,000 barrels per day capacity typically ranging from USD 15 billion to USD 25 billion depending on location, feedstock infrastructure requirements, product slate configuration, and technology selection, generating per-barrel capital expenditure of approximately USD 150,000 to USD 250,000 that requires sustained high liquid product prices and low feedstock gas costs to generate acceptable returns on capital employed over the fifteen-to-twenty-year investment horizon of a gas-to-liquids project. The economics of gas-to-liquids conversion are fundamentally driven by the spread between the value of natural gas feedstock at the project location and the prevailing market price of the liquid products produced, with the fuel spread between stranded gas cost of approximately USD 0.50 to USD 2.00 per million British thermal units and synthetic diesel market prices of USD 20 to USD 25 per million British thermal units typically providing viable conversion economics, but the spread compressing significantly when oil prices decline below USD 60 per barrel, as occurred during the 2015 to 2016 and 2020 commodity downturns that severely impacted the financial performance of operating gas-to-liquids facilities and contributed to the cancellation of multiple planned large-scale projects including Sasol’s Lake Charles facility in Louisiana. The capital cost premium of modular small-scale gas-to-liquids systems relative to large-scale facilities on a per-barrel-of-capacity basis is substantial, with compact Fischer-Tropsch systems of 500 to 2,000 barrels per day carrying capital costs of USD 50,000 to USD 120,000 per barrel per day of capacity, requiring careful project economics analysis to ensure viability within the constraints of the associated gas volumes and product logistics available at individual field locations.

Fischer-Tropsch Catalyst Deactivation, Process Complexity, and Operational Reliability Challenges at Commercial Scale Increasing Operating Cost and Technology Risk

The technical operation of commercial gas-to-liquids facilities presents persistent challenges arising from the sensitivity of Fischer-Tropsch catalysts to feedstock impurities, the complexity of managing thermal gradients and heat removal across large-scale multi-tubular or slurry-phase reactor configurations, and the requirement for continuous catalyst management including in-situ regeneration, periodic replacement, and performance optimization that collectively create operating cost burdens and reliability risks that are more demanding than conventional refinery or petrochemical operations with which gas-to-liquids plant operators must compete for skilled process engineering talent. Cobalt-based Fischer-Tropsch catalysts, which are preferred for natural gas feedstock applications due to their high selectivity for long-chain paraffin products and low water-gas shift activity that maximizes liquid hydrocarbon yield from hydrogen-rich synthesis gas, are susceptible to deactivation through sulfur poisoning at parts per billion levels of hydrogen sulfide in the synthesis gas feed, sintering of cobalt crystallites at elevated reactor temperatures, carbon deposition through Boudouard reaction side reactions, and oxidation of metallic cobalt by product water at low hydrogen partial pressure conditions, requiring stringent synthesis gas purification upstream of Fischer-Tropsch reactors and precise temperature management within reactor beds to maintain catalyst activity over the multi-year operational periods expected in commercial production economics. The heat management challenge in Fischer-Tropsch synthesis is particularly demanding given the highly exothermic nature of the polymerization reactions generating approximately 170 kilojoules per mole of carbon monoxide converted, requiring reactor designs with intensive cooling infrastructure whose engineering and operational complexity has historically contributed to cost overruns and production reliability issues at large-scale commercial Fischer-Tropsch plants including the Sasol Oryx Qatar plant and the Pearl GTL facility during their respective ramp-up phases.

Energy Transition Headwinds, Net-Zero Commitments, and Long-Term Fossil Fuel Demand Uncertainty Creating Strategic Investment Hesitancy for Conventional Gas-to-Liquids Capacity Expansion

The long-term investment case for new conventional gas-to-liquids capacity producing fossil-derived synthetic fuels is structurally challenged by the accelerating global energy transition toward electrification of transportation, industrial processes, and heating that is projected to reduce global liquid hydrocarbon fuel demand over the multi-decade investment horizon of a gas-to-liquids project, creating demand uncertainty that increases the revenue risk of long-lived fixed capital investments in fossil liquid fuel production at precisely the time when the economics of individual projects may appear favorable based on near-term gas and oil price fundamentals. International oil company capital allocation frameworks increasingly subject new hydrocarbon processing investments to climate scenario stress testing under International Energy Agency Net Zero Emissions by 2050 and Stated Policies Scenario demand trajectories, with gas-to-liquids projects whose economics depend on sustained transportation fuel demand through the late 2030s and 2040s facing material stranded asset risk under accelerated electrification scenarios that is creating board-level hesitancy to approve large capital commitments for projects that generate returns predominantly in the later years of their operating life when demand uncertainty is greatest. The climate commitment alignment requirements of institutional investors, green bond market eligibility standards, and sustainability-linked lending facility conditions are creating financing access constraints for conventional gas-to-liquids projects that depend on continued fossil fuel demand, as lenders and investors increasingly require climate scenario analysis, Paris Agreement alignment assessments, and transition risk documentation that conventional gas-to-liquids projects struggle to satisfy, shifting the financing environment in favor of the power-to-liquids and biogas-to-liquids variants that can demonstrate a credible carbon neutrality pathway but whose current higher production costs require policy support to achieve commercial viability.

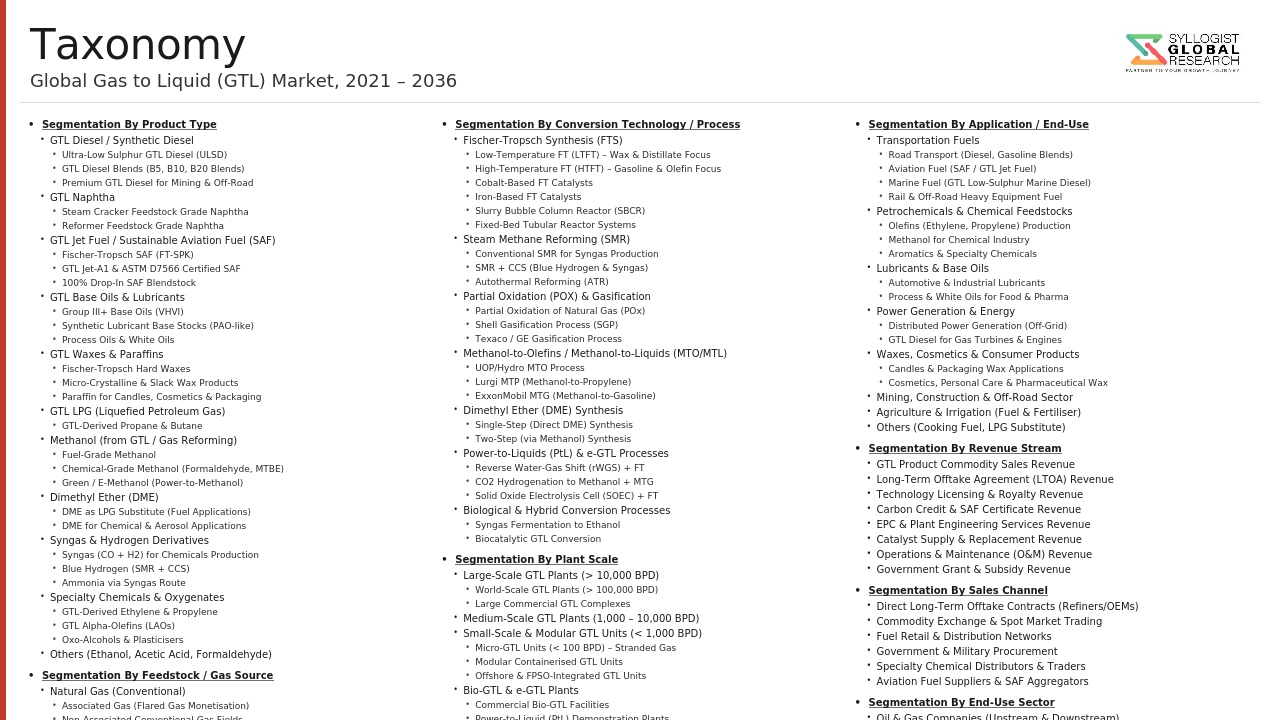

Market Segmentation

- Segmentation By Conversion Technology

- Fischer-Tropsch Synthesis (Cobalt-Catalyzed, Iron-Catalyzed)

- Methanol Synthesis and Methanol-to-Gasoline (MTG)

- Methanol-to-Olefins (MTO) and Methanol-to-Propylene (MTP)

- Dimethyl Ether (DME) Synthesis

- Power-to-Liquids and e-Fuels (Fischer-Tropsch via Green Hydrogen and CO2)

- Compact and Modular Gas-to-Liquids Systems

- Others

- Segmentation By Feedstock

- Conventional Pipeline Natural Gas

- Associated Gas and Stranded Gas

- Liquefied Natural Gas (Regasified)

- Biogas and Landfill Gas

- Synthetic Gas from Biomass or Waste Gasification

- Green Hydrogen and Captured Carbon Dioxide (Power-to-Liquids)

- Shale and Tight Gas

- Others

- Segmentation By Plant Scale

- Micro and Small Scale (Below 1,000 Barrels per Day)

- Modular Scale (1,000 to 10,000 Barrels per Day)

- Medium Scale (10,000 to 50,000 Barrels per Day)

- Large and World Scale (Above 50,000 Barrels per Day)

- Segmentation By Product

- Synthetic Diesel and Gasoil

- Synthetic Naphtha and Gasoline

- Synthetic Jet Fuel and Sustainable Aviation Fuel (SAF)

- Fischer-Tropsch Waxes and Specialty Waxes

- Lubricant Base Oils (Group III and Group IV)

- Olefins (Ethylene, Propylene) and Petrochemicals

- Methanol and Dimethyl Ether

- Others

- Segmentation By Application

- Transportation Fuel (Road, Aviation, and Marine)

- Petrochemical Feedstock

- Specialty Chemicals and Wax Applications

- Lubricant and Base Oil Production

- Power Generation

- Associated Gas Monetization and Flaring Reduction

- Others

- Segmentation By End-Use Industry

- Oil and Gas Producers (Upstream and Midstream)

- Petroleum Refiners and Petrochemical Producers

- Aviation Companies and Fuel Suppliers

- Shipping and Maritime Operators

- Specialty Chemical and Wax Manufacturers

- National Oil Companies

- Synthetic Fuel and E-Fuel Developers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Gas-to-Liquids Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by conversion technology including Fischer-Tropsch synthesis, methanol-to-gasoline, methanol-to-olefins, dimethyl ether, and power-to-liquids, by plant scale including micro and modular systems, medium-scale, and world-scale facilities, and by product including synthetic diesel, naphtha, jet fuel and sustainable aviation fuel, waxes, lubricant base oils, and olefins, to enable technology licensors, engineering procurement and construction contractors, catalyst manufacturers, national oil companies, independent gas producers, aviation fuel buyers, and capital market investors to identify the highest-growth technology and application combinations generating the most commercially attractive demand trajectories across the forecast period to 2034?

- What is the global scale of the associated gas flaring problem quantified by volume, location, economic value of wasted gas, and greenhouse gas emissions, how are regulatory frameworks including the United States Bureau of Land Management zero routine flaring rule, Nigeria’s flaring penalty regulations, Iraq’s gas utilization program, and the World Bank Zero Routine Flaring initiative collectively creating compliance-driven demand for modular gas-to-liquids deployment at oil production sites, and which oil-producing regions and individual production basins including the Permian Basin, Nigerian onshore fields, Iraqi southern gas fields, and Central Asian associated gas sources represent the most commercially concentrated near-term project opportunities for modular Fischer-Tropsch technology providers in terms of aggregate flared gas volumes, regulatory timeline urgency, and favorable product logistics for synthetic diesel and naphtha sales?

- What is the current production cost structure, electrolyzer capital cost and green electricity pricing dependency, carbon dioxide capture cost contribution, full lifecycle carbon intensity, and projected cost reduction trajectory through 2034 for power-to-liquids synthetic aviation fuel production at leading commercial demonstration projects operated by Norsk e-Fuel, HIF Global, Twelve, and others in Norway, Chile, Germany, and Canada, and at what production cost threshold and projected year does power-to-liquids sustainable aviation fuel achieve commercial blending economics without mandate-driven price support, and how are aviation fuel offtake agreements structured between airlines, fuel suppliers, and power-to-liquids project developers to provide the long-term revenue certainty required for USD 500 million to USD 2 billion commercial facility project financing?

- What are the specific catalyst deactivation mechanisms, reactor thermal management challenges, synthesis gas purification requirements, catalyst replacement cost, and maintenance cycle economics of cobalt-catalyzed Fischer-Tropsch technology at commercial scale based on operational data from Shell Pearl GTL and Sasol Oryx and Escravos plants, and how are second-generation modular Fischer-Tropsch technology developers including Velocys, INFRA Technology, and Greyrock Energy addressing these operational challenges through improved catalyst formulation, process intensification, heat management design, and automated process control innovations in their compact reactor systems targeting the associated gas monetization market at 500 to 5,000 barrels per day scales?

- How are gas-rich nations including Qatar, Saudi Arabia, Nigeria, Mozambique, Turkmenistan, and Indonesia incorporating gas-to-liquids technology investment within their broader national energy strategy, downstream industrial diversification, and export revenue optimization programs, what is the project pipeline value, technology selection rationale, financing structure, and state versus private capital allocation across announced and planned gas-to-liquids projects in each country, and how are long-term liquid product price scenarios, natural gas reserve depletion timelines, competing liquefied natural gas export capacity development, and climate policy alignment requirements collectively influencing the financial attractiveness and strategic prioritization of gas-to-liquids investment relative to alternative gas monetization pathways across these resource-rich geographies through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Feedstock Price Volatility & Natural Gas Supply Security Risk

- Technology Scale-Up, Catalyst Deactivation & Process Yield Risk

- Regulatory, Carbon Pricing & Fossil Fuel Phase-Down Policy Risk

- Capital Intensity, Project Finance & Construction Cost Overrun Risk

- Liquid Fuel Price Competition, Market Demand & Commodity Substitution Risk

- Regulatory Framework & Standards

- Fuel Quality & Product Specification Standards: EU Fuel Quality Directive, ASTM D975 (Diesel), ASTM D1655 & DEF STAN 91-091 (Jet Fuel), IMO Bunker Fuel & CORSIA SAF Specification

- Carbon Pricing, ETS & Low-Carbon Fuel Standard (LCFS) Regulatory Frameworks Impacting GTL Economics: EU ETS, California LCFS, UK ETS & Emerging National Carbon Taxes

- Sustainable Aviation Fuel (SAF) Policy & Mandate: EU ReFuelEU Aviation, US SAF Grand Challenge, CORSIA Eligible Fuels & ICAO SAF Pathway Certification

- Environmental Permitting, Air Quality, Greenhouse Gas Emission Reporting & Industrial Emission Directive Compliance for GTL Plant Siting & Operation

- Associated Gas Flaring Regulation & Stranded Gas Monetisation Policy: World Bank Zero Routine Flaring Initiative, National Flaring Reduction Mandates & Gas-to-Liquids Incentive Frameworks

- Global Gas-to-Liquids Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Barrels per Day of Liquid Product Capacity)

- Market Size & Forecast by Technology Type

- Low-Temperature Fischer-Tropsch Synthesis (LTFT): Cobalt-Catalysed, Waxy Product Selective

- High-Temperature Fischer-Tropsch Synthesis (HTFT): Iron-Catalysed, Olefin & Gasoline Selective

- Methanol Synthesis & Methanol-to-Liquids (MTL) Platform Technology

- Methanol-to-Olefins (MTO) & Methanol-to-Propylene (MTP) Process Technology

- Methanol-to-Gasoline (MTG) Process Technology

- Dimethyl Ether (DME) Synthesis & DME-to-Olefins Technology

- Power-to-Liquids (PtL) & e-Fuels: Green Hydrogen + Captured CO2 + Fischer-Tropsch Pathway

- Direct Methane Conversion: Oxidative Coupling of Methane (OCM) & Partial Oxidation

- Biomass-to-Liquids (BtL) via Gasification + Fischer-Tropsch (Bio-GTL)

- Market Size & Forecast by Process Stage

- Syngas Generation: Steam Methane Reforming (SMR), Partial Oxidation (POX) & Autothermal Reforming (ATR)

- Syngas Conditioning & Purification: CO2 Removal, Sulphur Removal, Water-Gas Shift & H2/CO Ratio Adjustment

- Catalytic Conversion Reactor System: FTS, Methanol, DME & OCM Reactor Technology

- Product Upgrading & Refining: Hydrocracking, Hydrotreating & Isomerisation

- Product Separation, Fractionation & Storage

- Utilities, Waste Heat Recovery, CO2 Capture Integration & Offsite Infrastructure

- Market Size & Forecast by Feedstock

- Conventional Pipeline Natural Gas

- Associated Gas & Stranded Flare Gas

- Shale Gas & Tight Gas

- Coal Bed Methane (CBM) & Landfill Gas

- Biogas & Renewable Natural Gas (RNG)

- Biomass-Derived Syngas via Gasification

- Green Hydrogen plus Captured or Biogenic CO2 (Power-to-Liquids Feedstock)

- Market Size & Forecast by Output Product

- Synthetic Ultra-Clean Diesel & Gasoil (FTS Diesel, Cetane 70 Plus)

- Sustainable Aviation Fuel (SAF) & Synthetic Kerosene (SPK, ATJ, FT-SPK)

- Synthetic Naphtha & Gasoline

- Methanol (Fuel Grade & Chemical Grade)

- Dimethyl Ether (DME): LPG Substitute & Diesel Blend Component

- Olefins: Ethylene & Propylene from MTO/MTP Routes

- Fischer-Tropsch Wax, Paraffin & Specialty Lubricant Base Oil

- Liquefied Petroleum Gas (LPG) & Light Hydrocarbon Fractions

- Market Size & Forecast by Plant Scale

- Large World-Scale GTL Complex (Above 10,000 bpd Liquid Product)

- Medium-Scale GTL Plant (1,000 to 10,000 bpd)

- Small-Scale & Modular GTL Unit (100 to 1,000 bpd)

- Micro & Distributed GTL Unit (Below 100 bpd, Flare Gas & Remote Site)

- Market Size & Forecast by Application

- Transportation Fuel (Road Diesel, Aviation Fuel & Marine Fuel)

- Petrochemical & Chemical Feedstock (Olefins, Methanol & Wax)

- Power Generation & Industrial Fuel

- Stranded & Associated Gas Monetisation (Flare Reduction & Remote Asset Value Recovery)

- e-Fuels & Sustainable Fuel for Net Zero & Decarbonisation Pathways

- Market Size & Forecast by End-User

- National Oil Company (NOC) & State Energy Enterprise

- International Oil Company (IOC) & Independent E&P Operator

- Independent GTL Technology Licensor & Project Developer

- Refinery, Petrochemical & Chemical Complex Operator

- Biofuel, SAF & Renewable Fuel Producer

- Government, Strategic Reserve Programme & National Fuel Security Authority

- Market Size & Forecast by Sales Channel

- Technology Licence, Catalyst Supply & Process Design Package (Licensor Channel)

- EPC Turnkey & EPCM Contract (Engineering, Procurement & Construction)

- Joint Venture, Equity Co-Investment & Co-Development Agreement

- Modular GTL Equipment Supply, Lease & Service Agreement

- North America Gas-to-Liquids Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Barrels per Day of Liquid Product Capacity)

- By Technology Type

- By Process Stage

- By Feedstock

- By Output Product

- By Plant Scale

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Gas-to-Liquids Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Barrels per Day of Liquid Product Capacity)

- By Technology Type

- By Process Stage

- By Feedstock

- By Output Product

- By Plant Scale

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Gas-to-Liquids Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Barrels per Day of Liquid Product Capacity)

- By Technology Type

- By Process Stage

- By Feedstock

- By Output Product

- By Plant Scale

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Gas-to-Liquids Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Barrels per Day of Liquid Product Capacity)

- By Technology Type

- By Process Stage

- By Feedstock

- By Output Product

- By Plant Scale

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Gas-to-Liquids Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Barrels per Day of Liquid Product Capacity)

- By Technology Type

- By Process Stage

- By Feedstock

- By Output Product

- By Plant Scale

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Gas-to-Liquids Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Barrels per Day of Liquid Product Capacity)

- By Technology Type

- By Process Stage

- By Feedstock

- By Output Product

- By Plant Scale

- By Application

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Qatar, Saudi Arabia, UAE, Nigeria, South Africa, Mozambique, Russia, Norway, Germany, France, Netherlands, United Kingdom, China, Japan, South Korea, India, Australia, Brazil, Malaysia, Indonesia, Kazakhstan

- Technology Landscape & Innovation Analysis

- Fischer-Tropsch Synthesis (FTS) Reactor, Catalyst & Product Selectivity Technology Deep-Dive

- Syngas Generation Technology: SMR, POX, ATR, Combined Reforming & Compact Reforming for GTL Applications

- Methanol Synthesis, MTO, MTG & MTP Process Technology: Reactor Design, Catalyst Selection & Product Yield Optimisation

- Small-Scale & Modular GTL Technology for Stranded Gas, Associated Gas Flare Reduction & Remote Monetisation

- Power-to-Liquids (PtL) & e-Fuels: Electrolytic Green Hydrogen plus CO2 Capture plus Fischer-Tropsch Integration Technology

- Product Upgrading, Hydrocracking, Hydrotreating & SAF Pathway Certification Technology

- Process Simulation, AI-Based Catalyst Optimisation, Digital Twin & Advanced Process Control Technology for GTL Plants

- Patent & IP Landscape in Gas-to-Liquids Technologies

- Value Chain & Supply Chain Analysis

- Feedstock Supply Chain: Natural Gas Supply Agreement, Pipeline Access, Associated Gas Offtake & Flare Gas Capture Infrastructure

- Catalyst Manufacturing & Supply Chain: FTS Cobalt & Iron Catalyst, Methanol Catalyst & Reforming Catalyst Producer Landscape

- Process Equipment & Reactor Manufacturer Supply Chain: Syngas Reformer, FTS Reactor, Heat Exchanger & Separation Column

- Technology Licensor, Process Design Package Provider & EPC Contractor Landscape

- GTL Plant Operator, NOC & IOC Integration & Project Development Channel

- Product Offtake, Logistics, Blending & End-Market Distribution

- Waste, Tail Gas Utilisation, CO2 Management & Circular Carbon Strategy

- Pricing Analysis

- GTL Synthetic Diesel & Naphtha Breakeven Price vs. Conventional Crude-Derived Fuel at Varying Gas Feedstock Cost

- GTL Sustainable Aviation Fuel (SAF) Production Cost vs. Fossil Jet Fuel & Bio-SAF Benchmark

- Methanol & Olefin Production Cost from GTL Route vs. Naphtha Cracking & Conventional Methanol Plant Benchmark

- Small-Scale & Modular GTL Capital Cost per bpd vs. Large World-Scale GTL Complex: Economies of Scale Analysis

- Power-to-Liquids (PtL) e-Fuel Production Cost Analysis: Electrolyser, Green Hydrogen, CO2 Capture & FTS Cost Trajectory to 2035

- Technology Licence Fee, Catalyst Replacement Cost & Total Plant Operating Cost Structure Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of GTL Fuel vs. Conventional Petroleum Fuel: Well-to-Wheel GHG Intensity Comparison by Feedstock & Technology Route

- CO2 Emissions Profile of GTL Process: Scope 1 Plant Emission, CCUS Integration Potential & Net Carbon Intensity Reduction Pathway

- Associated Gas Flare Reduction & Methane Emission Abatement Co-Benefit of Small-Scale & Modular GTL Deployment

- Power-to-Liquids (PtL) Net Zero Potential: Green Hydrogen Sourcing, Biogenic CO2 Utilisation & Lifecycle Carbon Neutrality Assessment

- Regulatory-Driven Sustainability: CORSIA SAF Lifecycle Emissions Threshold, EU ReFuelEU Mandate, LCFS Credit Value & Carbon Border Adjustment Mechanism Impact on GTL Product Competitiveness

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Concentrated by Technology Type & Plant Scale)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Type, Output Product & Geography

- Player Classification

- Global Integrated GTL Technology Licensor & Process Design Package Provider

- National Oil Company (NOC) & State Energy Enterprise Operating World-Scale GTL Assets

- International Oil Company (IOC) GTL Operator & Technology Co-Developer

- Independent Modular & Small-Scale GTL Technology Developer & Equipment Provider

- FTS Catalyst Manufacturer & Speciality Catalyst Developer

- Methanol, DME & Methanol-to-Olefins Technology Licensor

- Power-to-Liquids (PtL) & e-Fuels Technology Developer & Project Developer

- EPC Contractor & Process Systems Integrator Specialising in GTL & Syngas Plant

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Output Product & Region

- Company Profile

- Company Overview & Headquarters

- GTL Technology Products, Licence Portfolio & Process Design Package

- Key Customer Relationships & Reference Plant Installations

- Manufacturing Footprint & Installed GTL Capacity

- Revenue (GTL Technology & Catalyst Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Plant Start-Ups, Licence Awards, Technology Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Type, Feedstock, Output Product, Plant Scale & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Market Development Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Carbon Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)