Market Definition

The India Oilfield Chemicals Market encompasses the formulation, manufacturing, supply, and application of specialty chemical products used across the full lifecycle of oil and gas exploration, drilling, completion, stimulation, production, and enhanced recovery operations conducted by national oil companies, private upstream operators, and service companies active across onshore and offshore hydrocarbon basins in India. Oilfield chemicals are purpose-engineered chemical systems deployed to optimize drilling performance, ensure wellbore integrity, enhance hydrocarbon recovery, manage production-related flow assurance challenges, and protect surface and subsurface equipment from corrosion, scale deposition, bacterial activity, and emulsion formation across the diverse reservoir and formation conditions encountered in Indian upstream operations.

The market encompasses drilling fluid chemicals including water-based and oil-based mud additives such as viscosifiers, fluid loss control agents, shale inhibitors, weighting materials, and lubricants; cementing chemicals including cement accelerators, retarders, extenders, and fluid loss additives used to secure well casings; stimulation chemicals including hydraulic fracturing fluids, acid stimulation systems, diverting agents, and fracture conductivity enhancers; production chemicals including corrosion inhibitors, scale inhibitors, demulsifiers, H2S scavengers, paraffin inhibitors, pour point depressants, biocides, and foam control agents; and enhanced oil recovery chemicals including polymer flooding agents, surfactant systems, and alkali-surfactant-polymer formulations applied to mature fields. Key participants include global specialty chemical companies with dedicated oilfield divisions, domestic Indian chemical manufacturers supplying cost-competitive formulations, oilfield service companies integrating chemical programs within broader production optimization and drilling services, and upstream operators including Oil and Natural Gas Corporation, Oil India Limited, Reliance Industries, Cairn Oil and Gas, and international operators active in Production Sharing Contract and Revenue Sharing Contract acreage whose procurement decisions and field development programs define the demand structure of the Indian oilfield chemicals market.

Market Insights

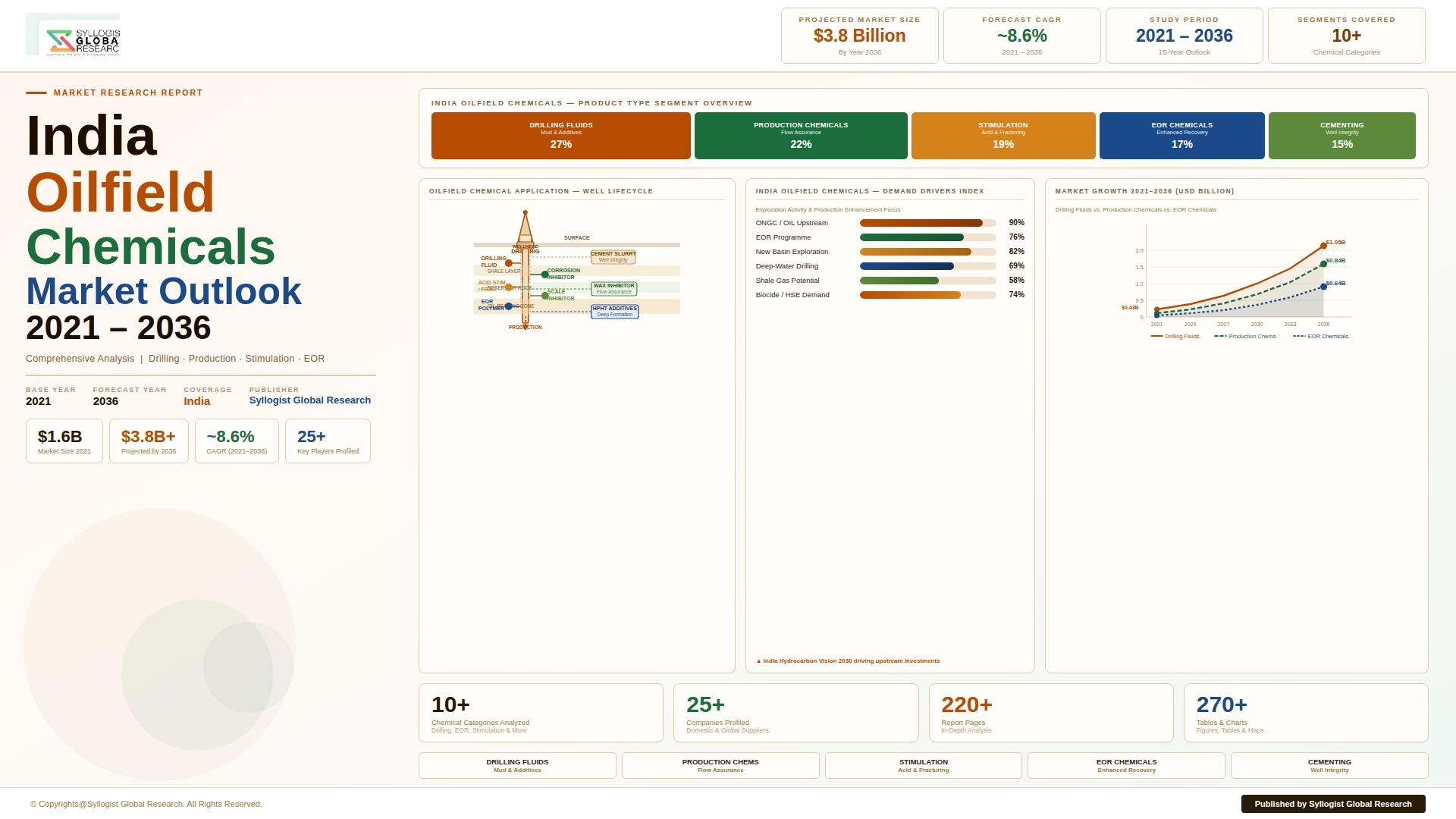

The India oilfield chemicals market is experiencing a structural demand expansion driven by the Indian government’s sustained policy commitment to reducing the country’s crude oil import dependency from its current level of approximately 88% of total consumption, which consumed foreign exchange reserves valued at approximately USD 132 billion in fiscal year 2024-25, by accelerating domestic upstream exploration and production activity through the HELP and OALP licensing rounds, expanding enhanced oil recovery programs at the country’s large portfolio of aging producing fields, and incentivizing deep-water and unconventional resource development that demands technically sophisticated chemical programs unavailable from lower-cost commodity suppliers. The India oilfield chemicals market was valued at approximately USD 1.3 billion in 2025 and is projected to reach USD 2.1 billion by 2034, advancing at a compound annual growth rate of 5.4% over the forecast period from 2027 to 2034, underpinned by growing upstream capital expenditure commitments from ONGC, Oil India, and private operators, the intensifying application of production chemicals to manage decline rates at aging onshore and offshore fields, and the progressive technical sophistication of Indian oilfield chemical procurement frameworks driven by operator awareness of chemical performance differentiation as a reservoir management tool.

Production chemicals constitute the largest and most consistently growing segment of the India oilfield chemicals market, accounting for approximately 41% of total market revenue in 2025, reflecting the structural dominance of production and flow assurance chemistry requirements in a domestic upstream portfolio characterized by a large number of maturing fields with declining reservoir pressure, increasing water cut, and worsening flow assurance challenges including paraffin deposition, asphaltene precipitation, scale formation, and microbiologically induced corrosion that collectively necessitate continuous and technically sophisticated chemical intervention programs to sustain acceptable production rates and equipment integrity. ONGC’s Western Offshore producing assets in the Mumbai High basin, which account for a substantial share of India’s total domestic crude oil production, are operating at reservoir depletion stages where water cut across producing wells has exceeded 70% to 80% in numerous field areas, generating intensive demulsifier, corrosion inhibitor, scale inhibitor, and biocide consumption requirements that are growing in both volume and technical complexity as reservoir conditions deteriorate. The Rajasthan block operated by Cairn Oil and Gas applies one of the most technically comprehensive production chemical programs in the Indian upstream industry, addressing the waxy crude and high pour point characteristics of Rajasthan crude through continuous paraffin inhibitor and pour point depressant injection programs supported by heated pipeline infrastructure, with chemical treatment costs constituting a significant and growing share of total field operating expenditure.

The drilling chemicals segment is positioned for accelerated growth through the forecast period as ONGC, Oil India, and private operators under the Open Acreage Licensing Programme expand exploratory and appraisal drilling activity in frontier basins including the Mahanadi, Andaman, Kerala-Konkan, and Bengal offshore deepwater blocks that demand high-performance water-based and synthetic-based drilling fluid systems capable of maintaining wellbore stability, managing formation pressure, and delivering acceptable rates of penetration in deepwater and technically challenging geological environments where conventional low-cost drilling fluid formulations are inadequate. India’s national ambition to sustain crude oil production above 35 million metric tonnes per year while simultaneously growing natural gas output to meet the government’s target of increasing natural gas share of the primary energy mix from the current 6.3% to 15% by 2030 requires a substantial increase in annual well drilling activity from the approximately 550 to 600 wells drilled annually in recent years, with each additional deepwater or complex horizontal well carrying drilling chemical program values four to eight times greater than comparable onshore vertical well programs. The progressive adoption of horizontal drilling and multi-stage hydraulic fracturing techniques by operators targeting tight gas reservoirs in the Cambay basin, the KG basin tight gas horizons, and the emerging shale and tight oil plays in Damodar Valley and Gondwana basins is creating an entirely new stimulation chemicals demand category within the Indian market that did not exist at meaningful commercial scale a decade ago.

The competitive landscape of the India oilfield chemicals market is undergoing a structural evolution from the historical dominance of global specialty chemical multinationals toward a more balanced competitive architecture in which domestically manufactured oilfield chemical formulations from Indian chemical companies are progressively capturing market share in volume-sensitive production chemical categories where cost competitiveness is a primary procurement criterion, while global leaders retain their position in technically complex drilling fluid systems, deepwater cementing chemistry, and advanced enhanced oil recovery formulations where application engineering expertise and proven field performance track records command procurement preference. The Indian government’s Atmanirbhar Bharat initiative and the production-linked incentive scheme for specialty chemicals are catalyzing investment in domestic oilfield chemical manufacturing capacity, with several mid-sized Indian chemical companies having established dedicated oilfield chemical product lines and field application technical service capabilities that are enabling credible competition against imported formulations in corrosion inhibitor, scale inhibitor, demulsifier, and biocide product categories. The deepwater chemistry segment, addressing the specific challenges of ultra-low temperature hydrate formation, high-pressure scale deposition, and deepwater cementing performance in ONGC’s KG-DWN 98/2 and other deepwater block developments, remains the most technically demanding and highest per-unit-value segment of the Indian oilfield chemicals market, with thermodynamic hydrate inhibitor and low-dosage hydrate inhibitor chemical programs representing some of the highest per-well chemical expenditure commitments in the entire Indian upstream industry.

Key Drivers

Government-Mandated Upstream Exploration Acceleration and OALP Licensing Round Expansion Driving Drilling Activity and Associated Chemical Demand

The Indian government’s strategic imperative to reduce chronic crude oil import dependency and strengthen domestic energy security has translated into a series of concrete policy actions that are directly expanding upstream drilling activity and the associated oilfield chemical demand base, including the award of 144 exploration blocks under nine rounds of the Open Acreage Licensing Programme since 2017, the revision of the Hydrocarbon Exploration and Licensing Policy to introduce revenue sharing contracts that improve exploration economics for private and foreign investors, and the implementation of production-linked incentives for oil and gas production from difficult fields, deepwater blocks, and high-pressure high-temperature reservoirs. ONGC’s approved capital expenditure program for the five-year period through fiscal year 2029-30 totals approximately USD 33 billion, with upstream exploration and production capital expenditure constituting the largest allocation, and the company has committed to drilling over 4,000 wells during this period across onshore and offshore assets, representing a substantial expansion of drilling program scale relative to the preceding five years. Oil India Limited’s ongoing Northeast India asset redevelopment program, targeting enhanced recovery from the mature Assam and Arunachal Pradesh producing fields through infill drilling, workover activity, and waterflood optimization, is generating growing demand for specialized production chemicals, drilling fluid additives, and cementing chemistry across an operational environment characterized by complex formation geology, high bottomhole temperatures, and challenging crude oil viscosity and wax content profiles that require technically differentiated chemical intervention programs.

Maturing Domestic Field Portfolio and Rising Enhanced Oil Recovery Adoption Intensifying Production Chemical Application Requirements

India’s domestic crude oil production profile is dominated by fields that have been in production for multiple decades, with ONGC’s Mumbai High offshore field having produced continuously since 1976 and the onshore Cambay and Assam basin fields representing production histories extending beyond 50 years in many cases, creating a producing asset portfolio characterized by advanced reservoir depletion, structurally high water cut across the majority of producing wells, severe scaling and corrosion challenges in aging production infrastructure, and declining natural reservoir drive energy that collectively necessitate intensifying and increasingly sophisticated chemical treatment programs to sustain commercially viable production rates. The Ministry of Petroleum and Natural Gas has designated enhanced oil recovery as a national priority for maintaining domestic crude oil production volumes, with ONGC implementing polymer flooding projects at Mumbai High North and South fields targeting incremental recovery of approximately 30 to 50 million tonnes of crude oil and requiring substantial polymer chemical procurement commitments, alkaline-surfactant-polymer pilot programs at Viraj and Santhal fields in the Cambay basin, and ongoing thermal EOR applications at heavy oil fields in Gujarat and Rajasthan that each demand specialized chemical formulations with exacting performance specifications. The progressive deterioration of production chemical challenges at aging fields, including the emergence of calcium carbonate and barium sulfate scale deposition in waterflooded reservoirs, the intensification of microbiologically induced corrosion in high water-cut production systems, and the increasing frequency of paraffin deposition incidents in fields where reservoir temperature has declined below crude wax appearance temperature, is driving volume and value growth in scale inhibitor, corrosion inhibitor, biocide, and paraffin management chemical demand that is structurally linked to the advancing age and depletion state of the domestic producing field portfolio.

Deepwater and Frontier Basin Development Programs Creating Demand for High-Performance Specialty Oilfield Chemical Formulations

India’s offshore deepwater and ultra-deepwater hydrocarbon resource base, estimated at potentially significant volumes in the KG basin, Mahanadi deepwater, Andaman offshore, and Kerala-Konkan blocks, represents the frontier development opportunity that is progressively adding technically demanding and high per-well-value oilfield chemical program requirements to the domestic market demand structure as operators advance from exploration and appraisal drilling toward development project sanctioning and production system commissioning. ONGC’s KG-DWN-98/2 deep-water gas and condensate development, representing India’s largest and most technically complex offshore development project, is a landmark demand catalyst for deepwater oilfield chemistry, requiring thermodynamic hydrate inhibitor injection systems consuming monoethylene glycol at rates of several hundred tonnes per day across the subsea production flowline network, low-dosage hydrate inhibitor qualification and application programs, deepwater cementing chemical systems engineered for ultra-low seafloor temperatures and high hydrostatic pressures, and scale inhibitor squeeze programs designed for subsea completion intervals with limited intervention access. Reliance Industries’ deepwater KG-D6 block, producing from the R-Cluster, Satellite Cluster, and MJ field developments at water depths of 1,700 to 3,200 meters, represents a parallel deepwater production chemical demand stream requiring continuous injection of corrosion inhibitors, scale inhibitors, and hydrate management chemicals through subsea umbilical chemical injection systems whose reliability is critical to uninterrupted deepwater production operations, creating premium-specification chemical procurement requirements that favor technically qualified global specialty chemical suppliers with deepwater application engineering expertise and proven field performance references from comparable international deepwater developments.

Key Challenges

Price-Driven Procurement Culture and Tendering Practices of National Oil Companies Constraining Specialty Chemical Value Realization

The procurement frameworks of India’s dominant upstream operators, ONGC and Oil India Limited, which together account for approximately 65% to 70% of total domestic oilfield chemical consumption by volume, are governed by public sector tendering regulations that mandate competitive bidding processes prioritizing lowest-cost compliant bids over total value of ownership assessments, chemical performance differentiation, or long-term production optimization outcomes, creating a structurally challenging commercial environment for specialty chemical suppliers whose premium-formulation products command price premiums that are frequently disqualified in L1-based tender evaluation processes in favor of lower-specification alternatives that may deliver inferior field performance. The dominance of rate contract and annual tender procurement mechanisms in national oil company oilfield chemical purchasing, which commoditize technically differentiated specialty chemical formulations into standardized specification-based line items evaluated primarily on unit price, compresses the commercial realization available to suppliers of technically advanced corrosion inhibitor, scale inhibitor, and production chemical formulations whose performance differentiation is measurable in terms of equipment integrity outcomes and incremental production maintenance rather than upfront chemical unit cost. The limited adoption of performance-based chemical service contracting models, which would align supplier remuneration with demonstrated production enhancement and chemical cost-per-barrel outcomes, means that the commercial incentive for operators to invest in technically superior chemical programs is structurally constrained by procurement policy frameworks that were designed for commodity goods purchasing rather than the outcome-oriented specialty service procurement model that characterizes best-practice oilfield chemical program management in international upstream operations.

Environmental Regulatory Tightening and Produced Water Discharge Standards Increasing Chemical Selection Complexity and Compliance Cost

The progressive strengthening of environmental regulations governing oilfield chemical use, particularly concerning the ecotoxicity, biodegradability, and discharge compliance of production chemicals applied in offshore operations where produced water and chemical residues may enter the marine environment, is increasing the regulatory complexity and qualification cost associated with oilfield chemical product registration, field application approval, and ongoing environmental compliance monitoring across Indian upstream operations governed by the Directorate General of Hydrocarbons and Ministry of Environment, Forest and Climate Change oversight frameworks. Offshore operators including ONGC’s Mumbai High and KG basin assets are subject to produced water discharge regulations that impose limits on oil in water content, chemical oxygen demand, and the concentration of specific oilfield chemical actives in overboard discharge streams, compelling the replacement of historically used corrosion inhibitor and scale inhibitor formulations containing components classified as environmentally hazardous with more expensive but environmentally acceptable alternative chemistries whose field performance equivalence must be demonstrated through comprehensive qualification testing programs before field deployment approval. The lack of a harmonized and clearly defined Indian regulatory framework specifically addressing oilfield chemical environmental classification, offshore discharge limits for chemical actives, and the qualification pathway for environmentally acceptable formulations creates compliance uncertainty for chemical suppliers and operators seeking to navigate the intersection of upstream operational chemistry requirements and environmental protection obligations, adding cost and timeline to product qualification processes and creating inconsistent regulatory interpretation across different offshore operational environments and regulatory jurisdictions within the Indian upstream sector.

Domestic Manufacturing Capability Gaps for Advanced Specialty Chemical Formulations Driving Import Dependency and Supply Chain Vulnerability

While India has developed meaningful domestic manufacturing capability in volume-sensitive oilfield chemical categories including basic corrosion inhibitors, commodity demulsifiers, and standard drilling fluid viscosifiers, the domestic chemical industry lacks the research and development infrastructure, specialty raw material supply chains, and application engineering expertise required to manufacture competitive formulations across the full spectrum of technically sophisticated oilfield chemical categories, creating a structural import dependency for advanced drilling fluid systems, deepwater hydrate inhibitors, high-temperature cementing additives, polymer flooding chemicals, and complex stimulation fluid systems that exposes Indian operators and chemical suppliers to foreign exchange cost volatility, extended procurement lead times, and supply disruption risk in geopolitically sensitive sourcing environments. The specialty raw material inputs for advanced oilfield chemical formulations, including specific acrylamide copolymers for polymer flooding applications, fluorinated surfactants for specialized stimulation systems, and proprietary biopolymer viscosifiers for high-performance drilling fluids, are predominantly manufactured by a small number of global chemical companies outside India, and the absence of domestic production capacity for these critical chemical building blocks creates a supply chain dependency that cannot be rapidly resolved through domestic manufacturing investment given the technical complexity and capital intensity of specialty chemical intermediate production. The Indian government’s production-linked incentive scheme for specialty chemicals, while providing investment incentives for domestic manufacturing capacity expansion, has had limited impact in the technically most demanding oilfield chemical sub-categories where the combination of small addressable market volumes, high formulation complexity, and the incumbent qualification advantages of established global suppliers creates substantial barriers to new domestic entrant viability.

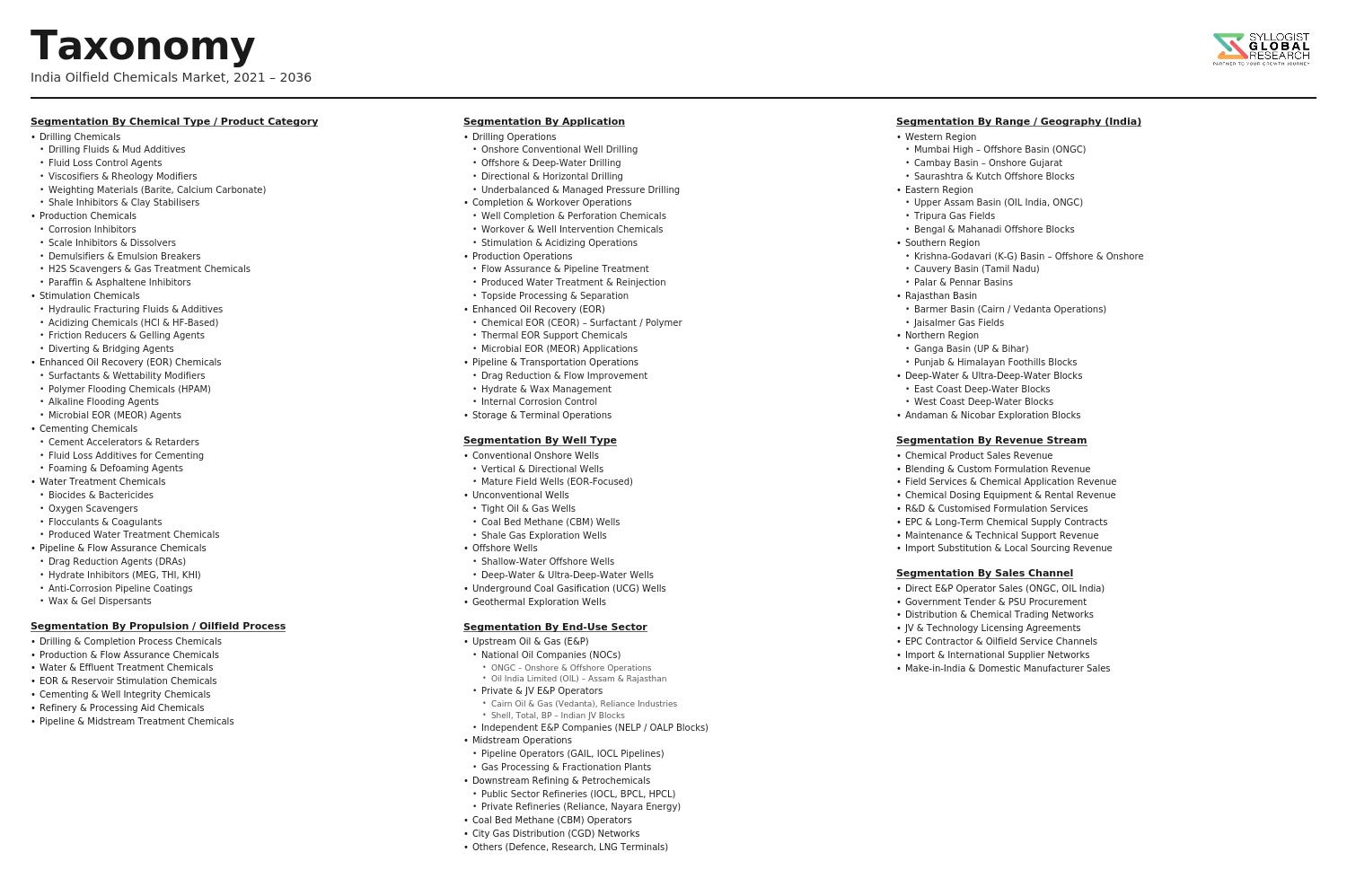

Market Segmentation

- Segmentation By Product Type

- Drilling Fluid Chemicals (Viscosifiers, Fluid Loss Agents, Shale Inhibitors, Lubricants, Weighting Agents)

- Cementing Chemicals (Accelerators, Retarders, Extenders, Fluid Loss Additives, Dispersants)

- Stimulation Chemicals (Hydraulic Fracturing Fluids, Acid Systems, Diverting Agents, Friction Reducers)

- Production Chemicals (Corrosion Inhibitors, Scale Inhibitors, Demulsifiers, Biocides, Paraffin Inhibitors, Pour Point Depressants, H2S Scavengers, Foam Control Agents)

- Enhanced Oil Recovery Chemicals (Polymer Flooding Agents, Surfactants, Alkali-Surfactant-Polymer Systems)

- Water Treatment Chemicals (Flocculants, Coagulants, Oxygen Scavengers, Bactericides)

- Others

- Segmentation By Application

- Drilling and Wellbore Construction

- Well Completion and Workover

- Well Stimulation and Hydraulic Fracturing

- Production and Flow Assurance

- Enhanced Oil Recovery and Improved Recovery

- Pipeline and Surface Facility Treatment

- Produced Water Management

- Others

- Segmentation By Operational Environment

- Onshore Conventional Fields

- Offshore Shallow Water (Up to 400 Meters)

- Offshore Deep Water and Ultra-Deep Water (Above 400 Meters)

- Tight Gas and Unconventional Reservoirs

- Heavy Oil and High-Viscosity Crude Fields

- High Pressure High Temperature (HPHT) Wells

- Others

- Segmentation By End User

- National Oil Companies (ONGC, Oil India Limited)

- Private and Joint Venture Upstream Operators

- Oilfield Service Companies

- Drilling Contractors

- Refinery and Downstream Processing Facilities

- Others

- Segmentation By Basin

- Mumbai Offshore Basin (Western Offshore)

- KG Basin (Onshore and Offshore)

- Cambay Basin (Onshore Gujarat)

- Rajasthan Basin

- Assam and Upper Assam Shelf Basin

- Mahanadi and Bengal Deepwater Basins

- Andaman Offshore and Other Frontier Basins

- Others

- Segmentation By Supply Source

- Domestic Indian Manufacturers

- Imported Specialty Chemical Formulations

- Integrated Oilfield Service Company Supply

- Others

- Segmentation By Region

- Western India (Gujarat, Mumbai Offshore)

- Eastern India (Assam, Arunachal Pradesh, West Bengal)

- Southern India (Andhra Pradesh, Tamil Nadu, KG Basin)

- Rajasthan and Central India

- Offshore (Deep Water and Ultra-Deep Water)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Oilfield Chemicals Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, application, operational environment, and basin, to enable specialty chemical manufacturers, oilfield service companies, upstream operators, and investors to identify which chemical product categories and field application segments will generate the highest absolute revenue and most sustained demand growth across the forecast period?

- How are ONGC and Oil India Limited’s multi-year upstream capital expenditure programs, drilling activity targets, and enhanced oil recovery project commitments expected to translate into incremental oilfield chemical procurement volumes by product category and basin through 2034, and what share of this demand growth is accessible to domestic Indian chemical manufacturers versus global specialty chemical suppliers given the evolving qualification and procurement framework preferences of India’s national oil companies?

- What is the current and projected demand trajectory for deepwater oilfield chemicals specific to ONGC’s KG-DWN-98/2 development and Reliance Industries’ KG-D6 deepwater operations through 2034, covering hydrate inhibitor, deepwater cementing additive, subsea corrosion inhibitor, and scale inhibitor requirement volumes, expenditure values, and the technical performance specifications that define supplier qualification thresholds in deepwater chemical procurement?

- How is the adoption of polymer flooding, alkaline-surfactant-polymer, and other enhanced oil recovery chemical technologies progressing across ONGC’s mature Mumbai High and Cambay basin assets, what are the projected EOR chemical procurement volumes and expenditure values through 2034 at planned and committed EOR project scales, and which polymer and surfactant chemical formulation technologies and suppliers are best positioned to capture the growing Indian EOR chemicals demand opportunity?

- Who are the leading domestic Indian and global specialty oilfield chemical suppliers, integrated oilfield service companies providing chemical programs, and emerging domestic manufacturers currently defining the competitive landscape of the India oilfield chemicals market, and what are their respective product portfolios, manufacturing and supply chain footprints in India, national oil company qualification status, technology development programs for indigenous formulation development, and strategic positioning in response to the Atmanirbhar Bharat policy incentives and production-linked incentive scheme applicable to domestic specialty chemical manufacturing?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil Price Volatility, Upstream Capex Cycle & E&P Spending Risk

- Environmental Regulation, Chemical Toxicity Compliance & HSE Risk

- Raw Material Price Volatility, Import Dependency & Supply Chain Disruption Risk

- Technology Substitution, Green Chemistry & Bio-Based Oilfield Chemical Risk

- Geopolitical, Licensing Round Uncertainty & National Oil Company Procurement Risk

- Regulatory Framework & Standards

- MoPNG Upstream Licensing, NELP & OALP Policy Frameworks Governing Oilfield Chemical Use in India

- CPCB & SPCB Environmental Standards, Effluent Discharge Norms & Hazardous Chemical Handling Regulations

- BIS Standards, DGMS Safety Regulations & Chemical Transportation & Storage Requirements for Oilfield Chemicals

- REACH-Equivalent Indian Chemical Regulation, MSDS Requirements & Restricted Substance Compliance

- Green Chemistry Mandates, Biodegradability Standards & ESG Disclosure Requirements for Oilfield Chemical Suppliers

- India Oilfield Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Chemical Type

- Drilling Fluids & Fluid Additives

- Cementing Chemicals

- Stimulation Chemicals (Hydraulic Fracturing & Acidising Chemicals)

- Production Chemicals

- Enhanced Oil Recovery (EOR) Chemicals

- Water Treatment & Injection Chemicals

- Corrosion & Scale Inhibitors

- Demulsifiers & Defoamers

- Biocides & Microbiological Control Chemicals

- Pipeline & Flow Assurance Chemicals

- Market Size & Forecast by Drilling Fluid Type

- Water-Based Drilling Fluids (WBM)

- Oil-Based Drilling Fluids (OBM)

- Synthetic-Based Drilling Fluids (SBM)

- Pneumatic & Gaseous Drilling Fluids

- Market Size & Forecast by Production Chemical Type

- Scale Inhibitors

- Corrosion Inhibitors

- Asphaltene & Paraffin Inhibitors

- Hydrate Inhibitors (THIs & LDHIs)

- H2S Scavengers

- Oxygen Scavengers

- Emulsion Breakers & Demulsifiers

- Foamers & Defoamers

- Market Size & Forecast by EOR Chemical Type

- Polymer Flooding Chemicals (HPAM & Xanthan Gum)

- Surfactant & Alkaline-Surfactant-Polymer (ASP) Flooding Chemicals

- Microbial Enhanced Oil Recovery (MEOR) Agents

- CO2 & Miscible Flood Additives

- Market Size & Forecast by Application

- Onshore Oilfield Operations

- Offshore Oilfield Operations

- Coal Bed Methane (CBM) & Unconventional Gas Operations

- Tight Oil & Shale Stimulation Operations

- Underground Gas Storage (UGS) Operations

- Market Size & Forecast by Oilfield Operation

- Drilling & Completions

- Well Stimulation & Workover

- Production & Processing

- Enhanced Oil Recovery (EOR)

- Pipeline & Transportation

- Water Injection & Disposal

- Market Size & Forecast by End-User

- National Oil Companies (ONGC, OIL India)

- Private & Joint Venture E&P Operators

- Oilfield Services Companies (OFS)

- Refineries & Downstream Processing Units

- Gas Processing & Transmission Companies

- Market Size & Forecast by Sales Channel

- Direct Supply to E&P Operators & NOCs

- Oilfield Services Company (OFS) Procurement

- Distributors, Stockists & Trading Companies

- Integrated Chemical & Service Contracts

- Western India Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Chemical Type

- By Application

- By Oilfield Operation

- By End-User

- By Basin / State

- By Sales Channel

- Market Size & Forecast

- Eastern India Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Chemical Type

- By Application

- By Oilfield Operation

- By End-User

- By Basin / State

- By Sales Channel

- Market Size & Forecast

- Southern India Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Chemical Type

- By Application

- By Oilfield Operation

- By End-User

- By Basin / State

- By Sales Channel

- Market Size & Forecast

- Northern & Central India Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Chemical Type

- By Application

- By Oilfield Operation

- By End-User

- By Basin / State

- By Sales Channel

- Market Size & Forecast

- Offshore (Arabian Sea & Bay of Bengal) Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Chemical Type

- By Application

- By Oilfield Operation

- By End-User

- By Basin / State

- By Sales Channel

- Market Size & Forecast

- Basin-Wise* Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Chemical Type

- By Application

- By Oilfield Operation

- By End-User

- By Basin / State

- By Sales Channel

- Market Size & Forecast

- *Key Basins & Operating Areas Analyzed: Mumbai Offshore Basin, Cambay Basin, Rajasthan Basin, Krishna Godavari Basin (KG Basin), Cauvery Basin, Assam & Assam-Arakan Basin, Vindhyan Basin, Mahanadi Basin, Andaman & Nicobar Basin

- Technology Landscape & Innovation Analysis

- Advanced Drilling Fluid Additive & High-Performance Fluid System Technology Deep-Dive

- Smart Cementing & Cement Additive Technology for Complex Well Architectures

- Hydraulic Fracturing & Acidising Chemical Technology for Tight & Unconventional Reservoirs

- Enhanced Oil Recovery (EOR) Chemical Flooding Technology for Mature Indian Fields

- Green & Bio-Based Oilfield Chemical Technology: Biodegradable Inhibitors & Bio-Surfactants

- Digital Dosing, Chemical Injection Monitoring & Real-Time Production Chemistry Optimisation Technology

- Flow Assurance & Subsea Chemical Management Technology for Deepwater Operations

- Patent & IP Landscape in Oilfield Chemical Technologies Relevant to India

- Value Chain & Supply Chain Analysis

- Petrochemical & Specialty Chemical Feedstock & Raw Material Supply Chain

- Oilfield Chemical Formulation, Blending & Manufacturing Supply Chain in India

- Packaging, Bulk Storage & Hazardous Chemical Logistics Supply Chain

- Oilfield Chemical Distribution, Stockist & Trading Channel

- Oilfield Services Company (OFS) Procurement & Chemical Application Services

- NOC & E&P Operator Tendering, Vendor Qualification & Procurement Channel

- Waste Chemical Treatment, Neutralisation & Disposal Value Chain

- Pricing Analysis

- Drilling Fluid & Additive Pricing: Water-Based vs. Oil-Based vs. Synthetic-Based System Cost Analysis

- Production Chemical Pricing: Inhibitor, Demulsifier & Biocide Unit Cost & Dosage Rate Analysis

- EOR Chemical Pricing: Polymer, Surfactant & ASP Flood Chemical Cost Analysis

- Stimulation Chemical Pricing: Fracturing Fluid, Acid System & Diverter Cost Analysis

- Import vs. Domestic Manufacturing Cost Comparison & Localisation Premium Analysis

- Total Oilfield Chemical Cost per Barrel of Oil Equivalent (BOE) Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Oilfield Chemicals: Carbon Footprint, Toxicity & Biodegradability Across Chemical Categories

- Green Chemistry Transition: Bio-Based, Biodegradable & Low-Toxicity Oilfield Chemical Alternatives

- Produced Water Treatment, Zero Liquid Discharge (ZLD) & Water Reuse Chemical Solutions

- Environmental Compliance, Spill Risk, Soil Contamination & Remediation Chemical Management

- Regulatory-Driven Sustainability, SDG 6 (Clean Water), SDG 13 (Climate Action) & ESG Disclosure Alignment for Oilfield Chemical Suppliers

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Chemical Type & End-User)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Chemical Type, Application & Basin

- Player Classification

- Global Integrated Oilfield Chemical Majors with India Operations

- Domestic Indian Oilfield Chemical Manufacturers & Formulators

- Specialty Chemical Companies with Oilfield Chemical Divisions

- Oilfield Services Companies Providing Chemical Management Services

- Niche & Application-Specific Oilfield Chemical Specialists

- Chemical Distributors, Stockists & Trading Companies Serving Indian E&P Operators

- Emerging Green Chemistry & Bio-Based Oilfield Chemical Start-Ups

- EPC & Integrated Chemical Injection System Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Chemical Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Oilfield Chemical Products & Solutions Portfolio

- Key Customer Relationships & Reference Field Applications in India

- Manufacturing Footprint & Production Capacity in India

- Revenue (India Oilfield Chemical Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Product Breadth vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Chemical Type, Application, Oilfield Operation, End-User & Basin

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output