Market Definition

The Global Petrochemical Recycling Technologies Market encompasses the development, engineering, commercialization, and deployment of advanced process technologies that chemically, thermally, or catalytically convert end-of-life plastic waste, mixed polymer streams, rubber, synthetic textile fibers, and other petrochemical-derived materials back into hydrocarbon feedstocks, monomers, chemical intermediates, fuels, waxes, and synthesis gas that can be reintroduced into petrochemical manufacturing value chains as substitutes for virgin fossil fuel-derived feedstocks, thereby closing the material loop of the global petrochemical industry and reducing its dependence on primary hydrocarbon extraction as a raw material source. Petrochemical recycling technologies are distinguished from conventional mechanical recycling by their ability to process contaminated, mixed, and multi-layer plastic waste streams that cannot be economically recovered through physical sorting and remelting processes, and to produce recycled outputs with chemical equivalence to virgin petrochemical feedstocks that are acceptable as drop-in replacements across the full range of polymer production, refining, and chemical synthesis applications without performance compromise.

The market encompasses pyrolysis technologies that thermally decompose plastic waste into pyrolysis oil, gas, and char fractions through high-temperature treatment in oxygen-deficient environments; catalytic cracking and hydrocracking systems applying zeolitic or acid catalysts to accelerate and direct plastic depolymerization toward targeted product slates; gasification technologies converting mixed plastic and rubber waste into syngas streams for chemical synthesis or energy recovery applications; depolymerization technologies including glycolysis, methanolysis, hydrolysis, and aminolysis that chemically break condensation polymer chains into constituent monomers for repolymerization into virgin-equivalent recycled resins; solvent-based purification and dissolution technologies that selectively dissolve and reprecipitate target polymers from mixed waste streams; and enzymatic and biological catalysis technologies at early commercial development stages targeting specific polymer degradation pathways. Key participants include chemical and energy technology licensors, engineering procurement and construction companies, petrochemical producers integrating recycled feedstock into existing cracker and polymer plant operations, independent advanced recycling plant developers, waste management companies providing sorted plastic feedstock supply, and regulatory bodies whose extended producer responsibility frameworks and recycled content mandates define the policy-driven demand foundation of the global petrochemical recycling technologies market.

Market Insights

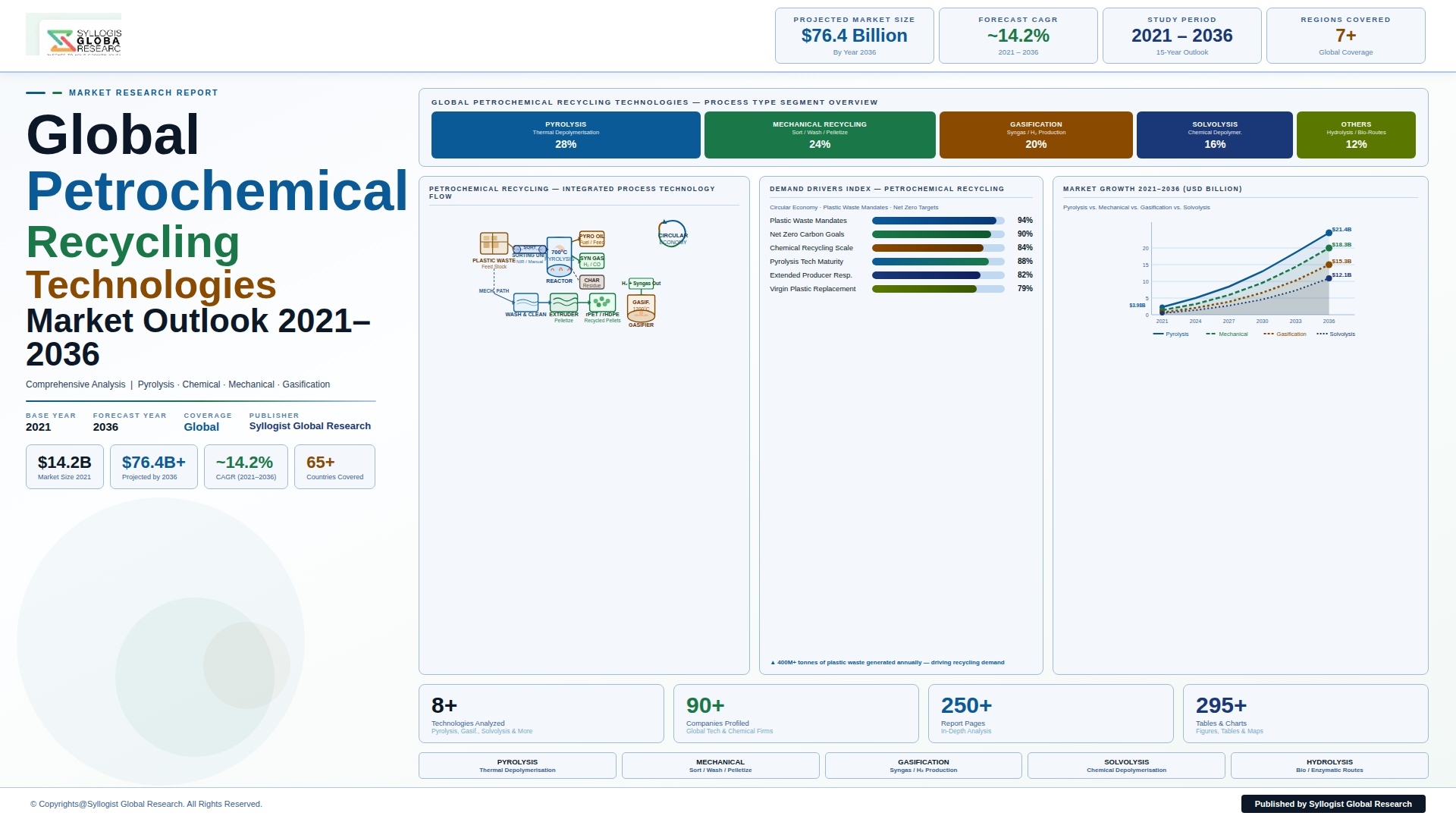

The global petrochemical recycling technologies market is experiencing an unprecedented commercial mobilization driven by the simultaneous convergence of binding regulatory mandates for recycled plastic content in consumer goods and packaging, the strategic commitment of major petrochemical producers to circular economy feedstock integration, escalating brand owner sustainability obligations under extended producer responsibility frameworks, and the maturing technology readiness of pyrolysis, depolymerization, and solvent-based recycling platforms that are transitioning from demonstration-scale pilot operations to commercially operational plants capable of processing tens of thousands of tonnes of plastic waste annually. The global petrochemical recycling technologies market was valued at approximately USD 5.4 billion in 2025 and is projected to reach USD 18.7 billion by 2034, advancing at a compound annual growth rate of 14.8% over the forecast period from 2027 to 2034, driven by the accelerating deployment of commercial-scale pyrolysis and chemical depolymerization capacity across Europe, North America, and Asia-Pacific, the integration of recycled petrochemical feedstocks into the cracker and polymer production systems of BASF, LyondellBasell, Ineos, Sabic, and other major chemical producers, and the premium commercial value commanded by certified chemically recycled polymer resins in food contact, pharmaceutical packaging, and high-value consumer goods applications where mechanical recycling cannot deliver the required material quality and regulatory compliance credentials.

Pyrolysis technology constitutes the most commercially advanced and widely deployed segment within the global petrochemical recycling technologies market, accounting for approximately 52% of total installed advanced recycling capacity by feedstock throughput volume in 2025, driven by pyrolysis technology’s relative process maturity, feedstock flexibility in accepting mixed and contaminated polyolefin waste streams including polyethylene, polypropylene, and polystyrene fractions that constitute the largest volume plastic waste categories, and the commercial viability of pyrolysis oil as a steam cracker feedstock substitute commanding prices linked to naphtha market benchmarks whose value has been sufficiently attractive to underpin commercial plant investment across multiple technology developer and petrochemical producer partnership structures. Plastic Energy, Neste, Quantafuel, Wastefront, and Recycling Technologies have each commissioned or advanced commercial pyrolysis plants in Europe with individual processing capacities ranging from 10,000 to 80,000 tonnes per year of plastic waste input, while SABIC’s Trucircle and LyondellBasell’s MoReTec programs represent major petrochemical producer-led pyrolysis integration initiatives that are progressively incorporating pyrolysis oil into their existing steam cracker feedstock slates under mass balance attribution methodologies certified by independent third-party auditors. The challenge of pyrolysis oil quality consistency, specifically the management of chlorine content from PVC contamination, nitrogen and sulfur impurities from non-polyolefin waste fractions, and the presence of polyaromatic hydrocarbons and other cracker-incompatible compounds in pyrolysis oil produced from poorly sorted feedstock streams, has driven substantial technology development investment in feedstock pre-treatment, catalytic upgrading, and hydrotreatment systems that improve pyrolysis oil acceptance specifications at petrochemical steam crackers and refinery units.

Chemical depolymerization technologies targeting condensation polymers including PET, nylon, and polycarbonate represent the segment with the most direct and highest-value circular economy proposition within the petrochemical recycling technology landscape, as the monomer recovery outputs of glycolysis, methanolysis, and hydrolysis processes can be purified to virgin-equivalent quality specifications and directly repolymerized into certified recycled PET, recycled nylon, and recycled polycarbonate resins whose material properties are indistinguishable from virgin polymer, enabling food contact approval, pharmaceutical packaging certification, and premium consumer goods application without the property degradation inherent in mechanical recycling pathways. The global PET chemical recycling capacity is expanding rapidly, with major investments from Eastman Chemical’s molecular recycling facility in Kingsport Tennessee targeting 110,000 tonnes per year of PET waste processing through methanolysis, Loop Industries’ depolymerization platform, and Carbios’s enzymatic PET depolymerization technology licensed to a consortium of L’Oreal, Nestle, PepsiCo, and Suntory at a commercial flagship plant in Longlaville France, collectively representing over USD 2.1 billion of announced investment in PET chemical recycling capacity as of 2025. The nylon depolymerization segment, targeting post-consumer nylon carpet, fishing nets, and industrial nylon waste through aminolysis and hydrolysis pathways that recover caprolactam or adipic acid and hexamethylenediamine monomers for polyamide resin remanufacturing, is experiencing growing commercial investment from Aquafil through its ECONYL regenerated nylon program and from DSM-Firmenich’s advanced recycling partnerships with automotive and textile sector customers committed to recycled nylon content in their product formulations.

The regulatory and corporate sustainability framework governing the global petrochemical recycling technologies market has become the dominant near-term commercial demand driver, with the European Union’s Single Use Plastics Directive, Packaging and Packaging Waste Regulation revision mandating minimum 30% recycled content in plastic packaging by 2030 and 65% by 2040, and the EU Taxonomy Regulation’s criteria for environmentally sustainable circular economy activities together creating a policy architecture that makes chemically recycled polymer procurement commercially rational for European brand owners and packaging converters even at current price premiums of 20% to 80% above virgin polymer benchmark prices. The extension of recycled content mandates to food contact materials, medical device packaging, and automotive interior applications across the European Union and increasingly across US state-level extended producer responsibility legislation in California, Maine, Oregon, and Colorado is progressively expanding the total addressable market for certified chemically recycled polymer resins beyond the discretionary sustainability procurement segment into regulatory compliance-driven demand that carries lower price sensitivity and longer supply contract duration, providing the demand visibility required to underpin petrochemical recycling plant capital investment decisions at the commercial scale required to achieve cost competitiveness with virgin petrochemical feedstock economics. Asia-Pacific, led by Japan’s recycled plastic content mandates, South Korea’s resource recycling promotion laws, and China’s National Sword policy-driven domestic plastic waste processing imperative, represents the fastest-growing regional market for petrochemical recycling technology investment at approximately 16.2% annually, with several hundred million USD of announced capacity investment from chemical producers, waste management enterprises, and technology developers across the region.

Key Drivers

Binding Regulatory Mandates for Recycled Plastic Content and Extended Producer Responsibility Frameworks Creating Policy-Underwritten Demand for Chemically Recycled Polymers

The global legislative transition from voluntary corporate sustainability commitments toward legally binding recycled content requirements, plastic waste reduction mandates, and extended producer responsibility obligations is creating a structurally durable and commercially quantifiable demand foundation for chemically recycled polymer products that does not depend on voluntary premium purchasing decisions by sustainability-motivated brand owners but rather on the regulatory compliance imperatives of consumer goods manufacturers, packaging converters, and material producers who face financial penalties, market access restrictions, and reputational consequences for non-compliance with mandated recycled content thresholds. The European Union’s Packaging and Packaging Waste Regulation, which introduces mandatory minimum recycled content thresholds of 30% for plastic contact-sensitive packaging by 2030 and 65% by 2040 across all plastic packaging categories, creates a demand signal for certified recycled polymer volumes that substantially exceeds current global advanced recycling capacity and requires multi-year capacity investment ramp-up by technology developers and petrochemical producers to satisfy, providing the demand certainty needed to underpin large-scale capital commitment to commercial pyrolysis, depolymerization, and solvent-based recycling facilities. The United Nations Global Plastics Treaty negotiations, advancing toward an internationally binding agreement on plastic pollution reduction, virgin plastic production limits, and extended producer responsibility standards applicable across signatory nations, represent a further regulatory demand catalyst that if adopted in meaningful form would extend recycled content obligation frameworks beyond the European regulatory jurisdiction into global consumer goods and packaging supply chains, multiplying the total addressable market for petrochemical recycling technology deployment across both developed and developing economy manufacturing regions through the forecast period.

Strategic Integration Commitments by Major Petrochemical Producers Deploying Recycled Feedstocks Into Existing Cracker and Polymer Plant Infrastructures

The strategic decision by the world’s major petrochemical producers, including BASF, LyondellBasell, SABIC, Ineos, Covestro, Eastman, Dow, and ExxonMobil Chemical, to integrate chemically recycled feedstocks into their existing steam cracker, polymer production, and specialty chemical manufacturing infrastructure represents a transformative commercial development for the petrochemical recycling technologies market, as these organizations bring the capital scale, technology development capability, supply chain integration expertise, and customer credentialing capacity required to deploy advanced recycling at the industrial volumes needed to achieve cost competitiveness with virgin petrochemical alternatives and to deliver certified recycled polymer resins to consumer goods brand owner customers at the quality, consistency, and quantity scale that mass market adoption requires. The mass balance attribution framework, which allows petrochemical producers to allocate the circular carbon content of chemically recycled feedstock inputs proportionally across their polymer production output through certified chain-of-custody accounting systems audited by ISCC PLUS, REDcert2, and equivalent certification bodies, has been critical in enabling the integration of recycled feedstocks into existing continuous production processes without requiring dedicated segregated production lines, dramatically reducing the capital and operational cost barrier to recycled feedstock integration at commercial petrochemical scale. The announced capital expenditure commitments of major petrochemical producers toward advanced recycling capacity, including BASF’s ChemCycling program, LyondellBasell’s MoReTec pyrolysis technology commercialization, Eastman’s USD 1 billion molecular recycling complex, and ExxonMobil’s advanced recycling facility in Baytown Texas processing 30,000 tonnes per year of plastic waste, collectively represent a manufacturing infrastructure investment wave that is structurally anchoring the commercial development trajectory of the petrochemical recycling technologies market for the decade ahead.

Consumer Brand Owner Sustainability Commitments and Circular Economy Packaging Targets Driving Premium Recycled Polymer Procurement Across Consumer Goods Value Chains

The binding public commitments of the world’s largest consumer goods manufacturers, food and beverage companies, personal care product producers, and retail operators to achieve specific recycled plastic content targets in their packaging portfolios by defined near-term deadlines are creating a confirmed and commercially significant demand pipeline for certified chemically recycled polymer resins that provides revenue visibility to advanced recycling plant operators and justifies the supply agreements and offtake contract structures needed to underpin project finance for commercial-scale facility construction. Unilever’s commitment to 25% recycled plastic content across all plastic packaging by 2025, Nestle’s target of 50% recycled materials in packaging by 2025, PepsiCo’s 50% recycled content in primary plastic packaging by 2030, and Procter and Gamble’s 50% post-consumer recycled plastic in packaging by 2030 collectively represent demand commitments from four consumer goods organizations alone whose annual plastic packaging consumption exceeds several million tonnes, creating a structural demand overhang for certified recycled polymer supply that current global advanced recycling capacity cannot satisfy and that is directly incentivizing the accelerated capital deployment into commercial pyrolysis and depolymerization plants needed to close the supply gap. The food contact approval pathway for chemically recycled polyolefins and PET through regulatory dossier submissions to the European Food Safety Authority and the United States Food and Drug Administration, which enables certified pyrolysis-derived recycled polyethylene and chemically recycled PET to be used in direct food contact packaging applications, is the critical regulatory enabler for brand owner premium procurement, as food and beverage packaging represents the highest-value and highest-volume plastic packaging segment whose conversion to recycled content materials would generate the largest incremental demand signal for advanced recycling technology capacity deployment.

Key Challenges

Plastic Waste Feedstock Quality, Sorting Infrastructure Inadequacy, and Contamination Constraining Advanced Recycling Plant Throughput and Economics

The commercial viability of petrochemical recycling technology plants is critically dependent on the consistent supply of adequately sorted, contaminated, and compositionally defined plastic waste feedstock streams whose quality characteristics directly determine plant operational efficiency, product yield, output quality, and cracker or polymer plant acceptance specifications, yet the current state of global plastic waste collection, sorting, and pre-treatment infrastructure is fundamentally inadequate to supply the volumes of clean, composition-defined polyolefin, PET, and nylon waste streams required by commercial advanced recycling facilities operating at the throughput scales needed to achieve economic unit cost targets. The contamination of plastic waste streams with PVC, which releases corrosive hydrogen chloride during pyrolysis and creates chlorine contamination in pyrolysis oil that exceeds steam cracker feedstock acceptance limits, with food organic residues that increase oxygen content and acidity of pyrolysis outputs, and with non-plastic materials including glass, metals, and paper that reduce effective plastic throughput per unit of plant operating cost, is the primary operational challenge confronting commercial pyrolysis plant operators whose feedstock procurement must navigate the variable quality of material recovery facility outputs whose composition changes seasonally and geographically with municipal waste collection system characteristics. The investment required to establish dedicated plastic waste pre-treatment facilities capable of shredding, washing, drying, and composition-sorting mixed plastic waste to the quality specifications required by commercial advanced recycling plants represents a capital and operational cost addition of USD 15 to USD 45 per tonne of processed plastic that substantially affects plant economics, and whose financing and development is typically treated as a separate supply chain investment outside the primary advanced recycling facility scope, creating a coordination and investment responsibility gap between waste management infrastructure developers and advanced recycling technology operators that slows the establishment of integrated feedstock-to-recycled-product value chains.

High Capital Cost and Technological Scale-Up Risk of Commercial Advanced Recycling Plants Creating Investment Hesitancy and Project Finance Complexity

The transition of petrochemical recycling technologies from pilot and demonstration scale to commercial production scale involves substantial technology scale-up risk, capital cost uncertainty, and operational performance verification challenges that have contributed to project delays, cost overruns, and in several cases commercial plant cancellations or restructurings among early-mover advanced recycling developers who have encountered unexpected engineering, feedstock, and product quality challenges during the scaling process that were not apparent at pilot plant operating conditions. The capital cost of a commercial-scale pyrolysis plant processing 30,000 to 50,000 tonnes per year of plastic waste input, including feedstock pre-treatment, pyrolysis reaction system, condensation and product separation infrastructure, product upgrading and quality assurance systems, and utility and safety infrastructure, ranges from USD 80 million to USD 200 million depending on technology provider, site conditions, and product quality specification requirements, representing a capital intensity that requires multi-year offtake agreements, strategic corporate partnerships, government grant co-financing, or development finance institution participation to achieve bankable project finance structures acceptable to commercial lenders. The current economics of most pyrolysis and depolymerization technologies remain marginal or dependent on premium recycled content market pricing to achieve acceptable investment returns at current plastic waste feedstock procurement costs and recycled oil or monomer market prices, creating a commercial vulnerability to oil price downturns that reduce the benchmark value of pyrolysis oil relative to virgin naphtha and to market price convergence between virgin and recycled polymer resins as recycled supply volumes grow, requiring continuous technology cost reduction and operational efficiency improvement to maintain commercial viability through the forecast period.

Lifecycle Carbon Accounting Complexity and Regulatory Uncertainty Over Mass Balance Attribution Methodologies Affecting Recycled Content Certification Credibility

The credibility of chemically recycled polymer products as genuine circular economy materials contributing to corporate sustainability targets and regulatory recycled content compliance depends fundamentally on the robustness, consistency, and independent verifiability of the lifecycle carbon accounting methodologies and mass balance attribution frameworks used to track and certify recycled feedstock input allocation across petrochemical production systems, and the current landscape of competing and partially incompatible certification standards, mass balance calculation methodologies, and auditing frameworks is creating market confusion, certification credibility concerns, and regulatory interpretation divergence that are complicating brand owner procurement decisions and undermining the commercial premium that recycled content products command relative to conventional virgin polymer alternatives. The mass balance attribution methodology, which allows the circular carbon content of a recycled feedstock input to a petrochemical cracker processing thousands of tonnes per day of mixed feedstocks to be allocated to a specific polymer product output on a proportional accounting basis, represents a pragmatic commercial necessity for integrating recycled feedstocks into continuous large-scale chemical production processes, but its acceptance by national regulators as a valid method of demonstrating recycled content compliance under specific product regulations including EU food contact legislation, national packaging recycled content mandates, and corporate sustainability reporting standards remains inconsistent and subject to ongoing regulatory interpretation disputes that create compliance uncertainty for brand owners relying on mass balance certified recycled polymer procurement to meet their regulatory and public commitment obligations. The development of a harmonized international standard for petrochemical recycling mass balance accounting, reconciling the methodological divergences between ISCC PLUS, REDcert2, RSB, and national certification schemes, is a prerequisite for the global scaling of advanced recycling as a credible and commercially reliable circular economy solution but remains a work in progress through the forecast period.

Market Segmentation

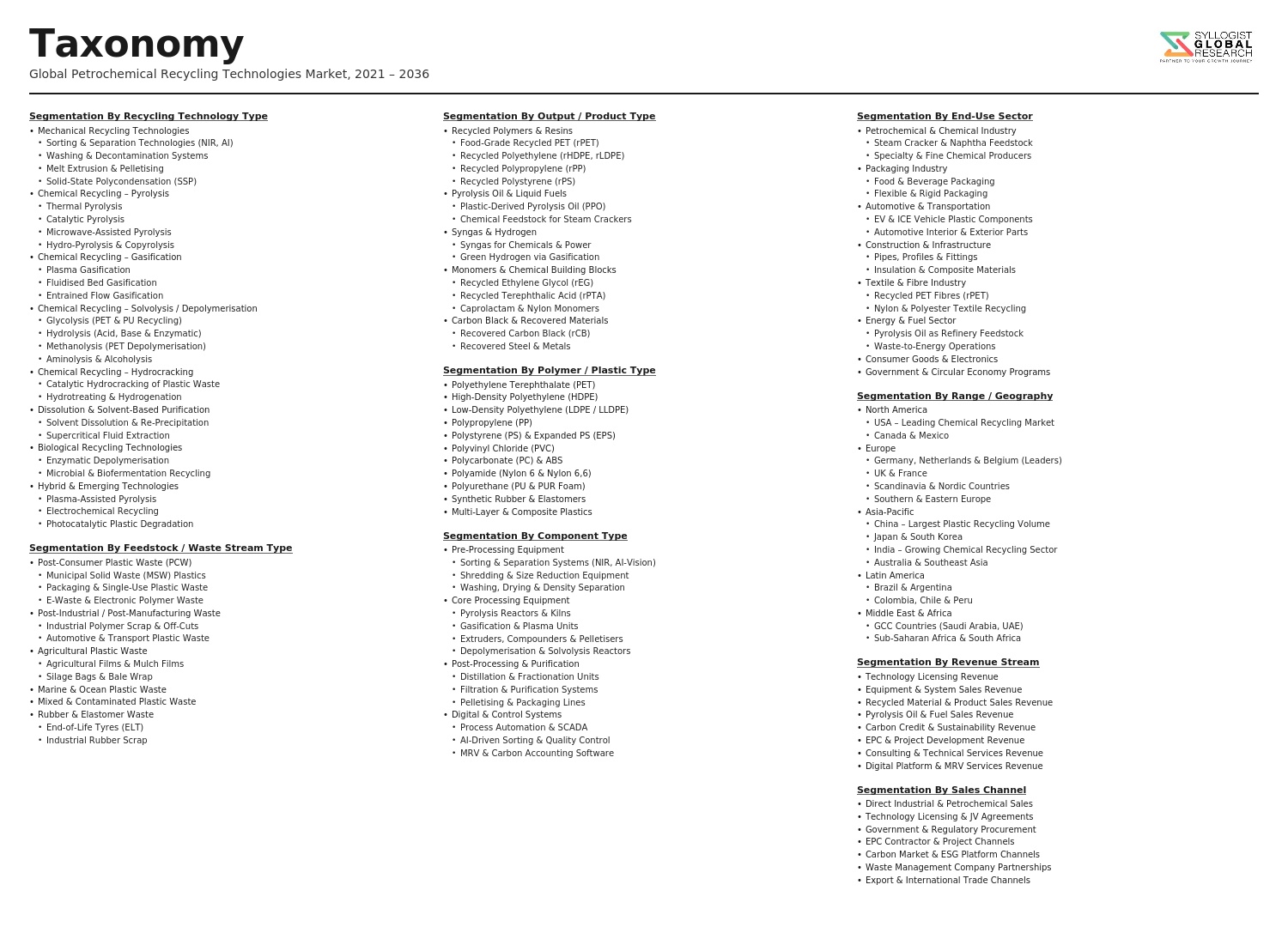

- Segmentation By Technology Type

- Pyrolysis (Thermal and Catalytic)

- Gasification and Partial Oxidation

- Hydrocracking and Hydrothermal Liquefaction

- Glycolysis, Methanolysis, and Hydrolysis (Chemical Depolymerization)

- Solvent-Based Dissolution and Purification Technologies

- Enzymatic and Biological Depolymerization Technologies

- Plasma-Based and Microwave-Assisted Pyrolysis

- Others

- Segmentation By Feedstock Type

- Polyolefins (Polyethylene and Polypropylene)

- Polyethylene Terephthalate (PET)

- Polystyrene and Expanded Polystyrene

- Polyamide and Nylon Waste

- Mixed and Contaminated Plastic Waste Streams

- Multi-Layer and Flexible Packaging Waste

- End-of-Life Tires and Rubber Waste

- Synthetic Textile Fiber Waste

- Others

- Segmentation By Output Product

- Pyrolysis Oil and Recycled Naphtha (Cracker Feedstock)

- Recycled Monomers (Ethylene Glycol, Caprolactam, Styrene, TPA)

- Synthesis Gas (Syngas) for Chemical or Energy Applications

- Recycled Waxes and Specialty Hydrocarbon Fractions

- Recycled Polymer Resins (Certified Circular Grade)

- Carbon Black and Recovered Carbon Char

- Hydrogen from Plastic Waste Gasification

- Others

- Segmentation By Application

- Packaging (Flexible, Rigid, Food Contact, Pharmaceutical)

- Automotive and Transportation Components

- Textiles and Apparel

- Consumer Electronics and Electrical Equipment

- Construction and Building Materials

- Agricultural Films and Inputs

- Industrial and Chemical Feedstock Supply

- Others

- Segmentation By End User

- Petrochemical Producers and Steam Cracker Operators

- Polymer Resin Manufacturers

- Consumer Goods Brand Owners and Packaging Converters

- Fuel Blenders and Refinery Operators

- Specialty Chemical Manufacturers

- Waste Management and Advanced Recycling Plant Operators

- Others

- Segmentation By Plant Scale

- Pilot and Demonstration Scale (Below 5,000 Tonnes Per Year)

- Small Commercial Scale (5,000 to 20,000 Tonnes Per Year)

- Medium Commercial Scale (20,000 to 50,000 Tonnes Per Year)

- Large Commercial Scale (Above 50,000 Tonnes Per Year)

- Others

- Segmentation By Business Model

- Technology Licensor Model (Process Technology Sale and Licensing)

- Build-Own-Operate (Independent Advanced Recycling Plant)

- Integrated Petrochemical Producer Model

- Joint Venture and Strategic Partnership Model

- Waste Management Company-Led Integration Model

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Petrochemical Recycling Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type, feedstock category, output product, application, and region, to enable technology licensors, petrochemical producers, advanced recycling plant developers, waste management companies, and investors to identify which recycling technology segments and geographic markets will generate the highest absolute revenue and the most commercially durable demand growth across the forecast period?

- How is the global installed and announced commercial advanced recycling capacity distributed across pyrolysis, chemical depolymerization, and solvent-based technology platforms by geography and operator type as of 2025, what is the projected capacity addition timeline and cumulative throughput volume available from announced projects through 2034, and how does the projected recycled feedstock supply from commercial advanced recycling capacity compare to the demand implied by brand owner and regulatory recycled content obligations across European and North American packaging markets?

- What is the current and projected commercial viability of pyrolysis oil, chemically recycled PET monomers, and recycled polyolefin resins relative to virgin naphtha, virgin PTA and MEG, and virgin HDPE and PP price benchmarks under different oil price scenarios, carbon price environments, and recycled content premium assumptions, and what technology cost reduction, operational efficiency improvement, and feedstock procurement optimization pathways are available to advanced recycling plant operators to achieve cost competitiveness with virgin petrochemical alternatives through the forecast period?

- How are the competing mass balance attribution methodologies and certification frameworks including ISCC PLUS, REDcert2, and RSB governing the allocation of circular feedstock content across petrochemical production systems being evaluated by regulatory authorities in the European Union, United States, Japan, and South Korea for compliance with national recycled content mandates, food contact material regulations, and corporate sustainability reporting standards, and what harmonization initiatives are underway to resolve the methodological divergences that are creating certification credibility and regulatory acceptance uncertainty for brand owners and advanced recycling plant operators?

- Who are the leading petrochemical recycling technology licensors, integrated petrochemical producer advanced recycling programs, independent commercial plant operators, and strategic partnership consortia currently defining the competitive landscape of the global petrochemical recycling technologies market, and what are their respective technology platforms, commercial plant portfolios and announced capacity expansion pipelines, feedstock procurement and offtake agreement structures, certification and chain-of-custody frameworks, customer base across packaging brand owners and polymer converters, and strategic responses to the accelerating regulatory and corporate sustainability demand signals shaping advanced recycling market growth through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Plastic Waste Feedstock Quality, Contamination & Inconsistent Collection Infrastructure Risk

- High Capital Investment, Technology Immaturity & Commercial Scale-Up Failure Risk for Chemical Recycling

- Virgin Polymer Price Competition, Oil Price Linkage & Recycled Output Price Realisation Risk

- Regulatory Fragmentation, Recycled Content Certification, Mass Balance Accounting & Cross-Border Waste Shipment Risk

- Public Acceptance, Greenwashing Perception & Brand Owner Offtake Commitment Risk for Recycled Petrochemicals

- Regulatory Framework & Standards

- EU Packaging & Packaging Waste Regulation (PPWR), Recycled Content Mandates & Chemical Recycling Recognition Frameworks

- EU Taxonomy for Sustainable Finance, Green Bond Standards & ESG Eligibility Criteria for Petrochemical Recycling Investments

- US EPA Recycling Infrastructure & Market Development Policy, PLASTICS Act & State-Level Extended Producer Responsibility (EPR) Frameworks

- ISCC PLUS, REDcert2 & Other Mass Balance Certification & Chain of Custody Standards for Chemically Recycled Polymers

- Basel Convention Amendments, Cross-Border Plastic Waste Trade Regulations & National Plastic Waste Management Frameworks

- Global Petrochemical Recycling Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes of Plastic Waste Processed)

- Market Size & Forecast by Technology Type

- Mechanical Recycling Technologies

- Pyrolysis & Thermal Cracking Technologies

- Gasification & Plasma Gasification Technologies

- Solvent-Based Dissolution & Purification Technologies

- Depolymerisation & Glycolysis Technologies

- Hydrothermal & Supercritical Water Processing Technologies

- Enzymatic & Biological Depolymerisation Technologies

- Integrated Hybrid & Multi-Stage Recycling Technology Platforms

- Market Size & Forecast by Recycling Process

- Mechanical Recycling (Sorting, Washing, Grinding & Recompounding)

- Chemical Recycling: Pyrolysis to Pyrolysis Oil & Naphtha

- Chemical Recycling: Gasification to Syngas & Hydrogen

- Chemical Recycling: Dissolution & Polymer Purification

- Chemical Recycling: Depolymerisation to Monomers (PET Glycolysis, PS Depolymerisation & PA Methanolysis)

- Feedstock Recycling via Integration into Steam Crackers & Refineries

- Market Size & Forecast by Feedstock Plastic Type

- Polyethylene Terephthalate (PET)

- Polyethylene (PE: HDPE, LDPE & LLDPE)

- Polypropylene (PP)

- Polystyrene (PS) & Expanded Polystyrene (EPS)

- Polyvinyl Chloride (PVC)

- Polyamide (PA / Nylon)

- Polycarbonate (PC) & Engineering Plastics

- Mixed & Contaminated Plastic Waste Streams

- Multilayer, Flexible & Hard-to-Recycle Packaging

- Market Size & Forecast by Output Product

- Recycled Polymers & Resins (rPET, rPP, rPE & rPS)

- Pyrolysis Oil & Recycled Naphtha (Feedstock for Steam Crackers)

- Syngas, Hydrogen & Fuel Gas

- Recycled Monomers (PTA, MEG, Styrene, Caprolactam & Others)

- Recycled Chemicals & Solvents

- Carbon Black & Solid Char Residues

- Market Size & Forecast by Plant Scale

- Small-Scale & Decentralised Recycling Units (Below 20,000 Tonnes per Annum)

- Medium-Scale Commercial Plants (20,000 to 100,000 Tonnes per Annum)

- Large-Scale Industrial Facilities (Above 100,000 Tonnes per Annum)

- Market Size & Forecast by End-Use Industry

- Packaging & Consumer Goods

- Automotive & Transportation

- Textiles & Fibres

- Construction & Building Materials

- Electrical & Electronics

- Healthcare & Medical Devices

- Petrochemical & Chemical Industry Feedstock

- Market Size & Forecast by End-User

- Integrated Oil, Gas & Petrochemical Companies

- Dedicated Chemical Recycling Technology Companies

- Waste Management & Materials Recovery Companies

- Packaging & Consumer Goods Manufacturers

- Retailers & Brand Owners with Recycled Content Commitments

- Government Bodies & Municipal Waste Authorities

- Market Size & Forecast by Sales Channel

- Technology Licensing & Royalty Agreement

- Turn-Key Plant Engineering, Procurement & Construction (EPC) Contract

- Offtake Agreement & Long-Term Recycled Output Supply Contract

- Joint Venture & Co-Investment Partnership

- Recycled Material Direct Sale & Spot Market

- North America Petrochemical Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Plastic Waste Processed)

- By Technology Type

- By Recycling Process

- By Feedstock Plastic Type

- By Output Product

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Petrochemical Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Plastic Waste Processed)

- By Technology Type

- By Recycling Process

- By Feedstock Plastic Type

- By Output Product

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Petrochemical Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Plastic Waste Processed)

- By Technology Type

- By Recycling Process

- By Feedstock Plastic Type

- By Output Product

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Petrochemical Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Plastic Waste Processed)

- By Technology Type

- By Recycling Process

- By Feedstock Plastic Type

- By Output Product

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Petrochemical Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Plastic Waste Processed)

- By Technology Type

- By Recycling Process

- By Feedstock Plastic Type

- By Output Product

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Petrochemical Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Plastic Waste Processed)

- By Technology Type

- By Recycling Process

- By Feedstock Plastic Type

- By Output Product

- By End-Use Industry

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Advanced Pyrolysis Technology Deep-Dive: Catalytic, Thermal & Microwave Pyrolysis Reactor Design, Yield Optimisation & Oil Quality

- Gasification & Plasma Gasification Technology: Syngas Composition, Tar Removal & Hydrogen Co-Production for Plastic Waste Streams

- Solvent-Based Dissolution Technology: Solvent Selection, Polymer Purity, Solvent Recovery & Scalability for PP, PE & PS Purification

- Catalytic Depolymerisation Technology: PET Glycolysis, Methanolysis, Hydrolysis & PS Depolymerisation to Virgin-Quality Monomers

- Enzymatic & Biological Depolymerisation Technology: PETase, Cutinase & Engineered Enzyme Performance for PET & Polyester Recycling

- Steam Cracker & Refinery Integration Technology: Co-Processing Pyrolysis Oil & Recycled Naphtha in Existing Petrochemical Assets

- AI-Driven Feedstock Sorting, Hyperspectral Imaging & Automated Waste Stream Characterisation Technology

- Patent & IP Landscape in Petrochemical Recycling Technologies

- Value Chain & Supply Chain Analysis

- Post-Consumer & Post-Industrial Plastic Waste Collection, Sorting & Pre-Treatment Supply Chain

- Recycling Technology Equipment, Reactor & Process Plant Manufacturing Supply Chain

- Catalyst, Solvent, Chemical Reagent & Consumable Supply Chain for Chemical Recycling

- Recycled Output Product Purification, Quality Certification & Storage Supply Chain

- Offtake Partner, Petrochemical Reintegration & Recycled Polymer Sales Channel

- Brand Owner, Retailer & Consumer Goods Manufacturer Recycled Content Procurement Channel

- Residue, Char, Ash & By-Product Valorisation & Waste Disposal Value Chain

- Pricing Analysis

- Mechanical Recycling Cost Structure: Collection, Sorting, Processing & Output Price Analysis by Polymer Type

- Pyrolysis Plant Capital Cost, Operating Cost & Pyrolysis Oil Price Benchmarking vs. Virgin Naphtha

- Chemical Depolymerisation Plant Economics: CapEx, OpEx, Monomer Yield & Price Realisation vs. Virgin Monomer

- Recycled Polymer (rPET, rPP & rPE) Price Premium vs. Virgin Resin & Price-Parity Trajectory Analysis

- Technology Licensing Fee, Royalty Structure & Turn-Key EPC Project Cost Analysis

- Total Levelised Cost of Recycling (LCoR) per Tonne of Plastic Waste Processed Across Technology Routes

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Petrochemical Recycling Technologies: Carbon Footprint, Energy Intensity & GHG Savings vs. Landfill & Incineration

- Chemical vs. Mechanical Recycling Environmental Trade-Offs: Carbon Footprint, Water Use & Chemical Input Comparison

- Contribution to Circular Economy, Plastic Waste Reduction & Virgin Feedstock Displacement in Global Petrochemical Supply Chains

- Mass Balance, Recycled Content Traceability & Chain of Custody: ISCC PLUS & REDcert2 Certification Environmental Integrity

- Regulatory-Driven Sustainability, SDG 12 (Responsible Consumption), SDG 13 (Climate Action) & SDG 14 (Life Below Water) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Type, Feedstock Plastic & Region

- Player Classification

- Integrated Oil, Gas & Petrochemical Majors Developing Chemical Recycling Capabilities

- Dedicated Chemical Recycling Technology Developers & Licensors

- Advanced Pyrolysis Technology Companies

- Depolymerisation & Monomer Recovery Technology Specialists

- Solvent-Based Dissolution & Polymer Purification Technology Companies

- Mechanical Recycling Technology & Equipment Manufacturers

- Waste Management Companies Transitioning to Advanced Recycling

- Start-Ups & Deep Tech Ventures in Enzymatic & Biological Recycling

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Feedstock Plastic & Region

- Company Profile

- Company Overview & Headquarters

- Petrochemical Recycling Technology Products, Processes & Platform Portfolio

- Key Customer Relationships, Offtake Partners & Reference Plant Installations

- Plant Capacity, Processing Throughput & Geographic Footprint

- Revenue (Petrochemical Recycling Segment) & Project Pipeline

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Plant Commissioning, Technology Milestones, Offtake Agreements)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Maturity vs. Commercial Scale)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Type, Recycling Process, Feedstock Plastic, Output Product, End-Use Industry & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output