Market Definition

The Global Refinery-to-Chemicals Technologies Market encompasses the process technologies, catalysts, engineering solutions, proprietary conversion systems, and integrated facility configurations that enable petroleum refineries to maximize the conversion of crude oil and refinery intermediate streams directly into petrochemical feedstocks and chemical building blocks, replacing or substantially reducing the production of transportation fuels including gasoline, diesel, jet fuel, and fuel oil whose long-term demand is projected to decline under accelerating energy transition scenarios, with high-value petrochemical products including ethylene, propylene, butadiene, aromatics such as benzene, toluene, and xylenes, and specialty chemical precursors whose demand growth trajectory is structurally supported by polymer consumption expansion in developing economies. Refinery-to-chemicals integration spans a spectrum of conversion approaches from high-severity fluid catalytic cracking configurations modified to maximize olefin yield at the expense of gasoline production, to dedicated crude oil steam cracking that bypasses conventional refinery operations entirely to feed crude or atmospheric residue directly to steam cracker furnaces, to deep hydrocracking of vacuum gas oil and atmospheric residue into naphtha and lighter fractions suitable for steam cracker feedstock, to pyrolysis oil and mixed plastic waste co-processing in existing refinery units that produces recycled chemical intermediates. The market encompasses technology licensing by petroleum process technology developers, catalyst supply by chemical catalyst manufacturers, engineering design and project execution by refinery and petrochemical engineering companies, and the capital investment programs of integrated oil and petrochemical companies executing refinery conversion and integration projects. Key technology configurations within the market include crude oil to chemicals direct conversion, maximum propylene fluid catalytic cracking, steam cracker integration with hydroprocessed refinery intermediate feeds, toluene and mixed xylene extraction and conversion to paraxylene, residue upgrading and deep conversion for chemical feedstock generation, and advanced hydroprocessing configurations that produce maximum naphtha yield for downstream steam cracker operation. Key participants include process technology licensors, catalyst manufacturers, engineering procurement and construction contractors, integrated oil and chemical companies, national oil companies, and refinery operators implementing chemical integration strategies.

Market Insights

The global refinery-to-chemicals technologies market was valued at approximately USD 8.4 billion in 2025 and is projected to reach USD 19.8 billion by 2034, advancing at a compound annual growth rate of 10.0% over the forecast period from 2027 to 2034, driven by the strategic imperative of oil and gas companies and national oil companies to transform their refining asset bases from fuel-oriented configurations that face structural margin erosion from transportation electrification and energy efficiency improvement toward chemically integrated facilities whose petrochemical product output growth trajectory aligns with polymer demand expansion in the developing world, the demonstrated economics of crude oil to chemicals conversion at integrated facilities achieving chemical yields of 40% to 80% of crude oil mass input compared to approximately 5% to 15% for conventionally configured refineries, and the significant capital investment programs announced by Saudi Aramco, Sinopec, ADNOC, Reliance Industries, ExxonMobil, and BASF in integrated refinery and petrochemical complexes whose combined announced investment exceeds USD 180 billion through 2030. The Saudi Aramco and SABIC integrated refinery-to-chemicals program, which includes the USD 20 billion Amiral petrochemical complex at Jubail Industrial City incorporating high-severity fluid catalytic cracking and steam cracker integration to maximize ethylene and propylene yield from Arabian Light crude oil processing, and the Crude Oil to Chemicals project being developed in partnership with international technology licensors targeting 70% to 80% chemicals yield from crude oil input, exemplifies the scale and strategic commitment of national oil company refinery transformation programs that are the primary driver of refinery-to-chemicals technology investment globally. China’s refinery sector, operating approximately 900 million metric tons per year of crude distillation capacity against declining domestic transportation fuel demand growth, is simultaneously the world’s largest and most urgently motivated market for refinery-to-chemicals technology deployment as Chinese refinery operators face stranded asset risk from declining gasoline and diesel demand and are investing in maximum olefin fluid catalytic cracking, propane dehydrogenation integration, and steam cracker connectivity to redirect crude oil processing capacity toward polyethylene, polypropylene, and aromatics production.

The crude oil to chemicals direct conversion technology segment, which represents the most technically ambitious and commercially transformative category within the refinery-to-chemicals market, has advanced from conceptual engineering through pilot plant demonstration to initial commercial scale deployment over the past decade, with the COTC pathway developed by Saudi Aramco in collaboration with process technology licensors achieving commercially validated chemical yields approaching 70% to 80% of crude oil input mass by routing crude oil atmospheric and vacuum distillation cuts through intensive hydroprocessing, catalytic cracking at maximized severity conditions, and integration with dedicated steam crackers for naphtha, light gases, and cracked fractions, bypassing the conventional fuel blending pool and eliminating the production of road transportation fuels and bunker fuel that represent approximately 85% of the output product slate of a conventionally configured crude oil refinery. The Saudi Aramco-Total Energies Amiral complex at Jubail, with USD 11 billion of committed petrochemical investment scheduled for commissioning in 2026, and the Saudi Aramco partnership with Sinopec for a refinery-to-chemicals complex in Fujian Province, China, represent the first major commercial-scale deployments of the crude oil to chemicals philosophy at billion-dollar investment scale, providing demonstration projects whose operational performance, achieved chemical yield percentages, and capital and operating cost actualization will define the commercial investment case for subsequent crude oil to chemicals capacity expansions by other national oil companies and integrated energy companies evaluating their refinery portfolio strategic transformation options. The capital cost of retrofitting an existing conventional refinery for maximum chemicals output through the installation of high-severity catalytic cracking units, hydroprocessing capacity additions, steam cracker connections, and aromatics extraction units is estimated at USD 600 to USD 1,200 per ton per day of crude oil processing capacity depending on existing configuration and target chemical yield, with a 400,000 barrel per day refinery requiring USD 3.5 to USD 7.0 billion of capital investment for full chemicals integration at 70% chemical yield, a substantial investment whose internal rate of return depends critically on the differential between petrochemical product margins and fuel product margins that is the fundamental economic driver of refinery-to-chemicals conversion.

The maximum propylene and olefins fluid catalytic cracking segment, which involves the modification or replacement of conventional gasoline-maximizing fluid catalytic cracker units with high-severity catalytic cracking configurations operating at higher cracking temperatures, lower hydrocarbon partial pressures, shorter contact times, and with specialized zeolite catalyst formulations that maximize propylene and light olefin production at the expense of gasoline yield, represents the most immediately commercially deployable technology pathway for existing refinery operators seeking to increase chemical output without the full capital commitment of crude oil to chemicals greenfield investment. High-severity fluid catalytic cracking operations using maximum propylene catalysts including ZSM-5 additive-rich catalyst systems can achieve propylene yields of 15% to 22% of fluid catalytic cracker feed weight compared to approximately 5% to 8% for conventional gasoline-maximizing operation, with the incremental propylene produced available for polypropylene or acrylonitrile production at values substantially above the gasoline blending value it displaces, providing a compelling economics case in refinery markets where polypropylene margins are strong and gasoline blending economics are weak from overcapacity or biofuel blend mandate displacement. The aromatics extraction and conversion segment, targeting the recovery of benzene, toluene, and mixed xylenes from catalytic reformate and pyrolysis gasoline fractions for separation and conversion to purified paraxylene through adsorptive separation or crystallization processes, is experiencing growing investment driven by the structural growth in paraxylene demand for purified terephthalic acid production and polyethylene terephthalate fiber, film, and bottle resin whose end-use consumption in textile, packaging, and beverage applications in Asia-Pacific, particularly in China, India, and Southeast Asia, is growing at approximately 5.8% annually and sustaining paraxylene capacity investment at refinery and petrochemical complex sites with access to reformate or pyrolysis gasoline aromatic feedstock streams.

The integration of plastic waste chemical recycling within refinery-to-chemicals technology portfolios represents an emerging and commercially significant development that is both expanding the scope of the market and providing petroleum refineries with a sustainability narrative and circular economy revenue stream that supports regulatory and social license maintenance for refinery operations in jurisdictions implementing extended producer responsibility and plastic waste reduction frameworks. Plastic pyrolysis oil, produced through the thermal depolymerization of mixed post-consumer polyolefin waste at temperatures of 400 to 500 degrees Celsius, generates a mixed hydrocarbon oil product whose composition closely resembles light vacuum gas oil and whose integration into conventional refinery hydroprocessing, fluid catalytic cracking, or steam cracker operations produces certified recycled content chemical intermediates traceable through mass balance chain of custody to the polymer feedstocks from which the original plastics were manufactured. Major integrated refinery and chemical companies including LyondellBasell, Sabic, ExxonMobil, and Dow have announced pyrolysis oil co-processing programs with planned processing volumes of 50,000 to 200,000 metric tons per year of plastic waste feedstock at individual refinery sites, with the European Union Packaging and Packaging Waste Regulation’s mandatory recycled content requirements for plastic packaging creating a certified recycled polymer demand stream that justifies the premium input cost of pyrolysis oil relative to virgin fossil feedstock at the chemical value of the recycled content certification it enables. The competitive landscape of the refinery-to-chemicals technology licensing market is concentrated among a small number of major process technology companies including Lummus Technology, Honeywell UOP, Axens, Shell Catalysts and Technologies, and KBR whose proprietary catalytic cracking, hydroprocessing, steam cracking, aromatics, and paraxylene separation technology portfolios collectively define the technical options available to refinery operators implementing chemicals integration strategies, with technology selection decisions involving multi-year licensing relationships and catalyst supply agreements that create long-term commercial dependencies between technology licensors and operating companies.

Key Drivers

Structural Decline in Transportation Fuel Demand from Vehicle Electrification and Efficiency Improvement Compelling Refiners to Redirect Crude Oil Processing Capacity Toward Petrochemical Production

The accelerating electrification of passenger and commercial vehicle fleets, combined with the progressive improvement in combustion engine fuel efficiency under regulatory corporate average fuel economy and fleet emissions standards, is creating a structural and increasingly quantifiable decline trajectory for gasoline and diesel demand across major consuming markets that is compelling petroleum refiners to confront a fundamental business model transformation challenge, as the transportation fuel revenues that have historically supported the economics of crude oil refining operations progressively erode under scenario projections that show OECD gasoline demand declining by approximately 40% between 2025 and 2040 under stated policies scenarios and diesel demand falling even more sharply as commercial vehicle electrification and natural gas substitution accelerate. The International Energy Agency’s Stated Policies Scenario projects global road transportation fuel demand peaking in the late 2020s and declining at approximately 1.5% to 2.5% per year through 2040, while petrochemical feedstock demand from refineries grows at approximately 3.5% to 4.5% per year driven by polymer consumption expansion in developing economies, creating a directional demand divergence between fuel and chemical products that makes the economics of refinery-to-chemicals conversion increasingly compelling as each year of fuel demand decline simultaneously reduces the revenue earned on conventional fuel-oriented production and increases the value of chemical yield maximization investments. For national oil companies including Saudi Aramco, ADNOC, Kuwait Petroleum, and Qatar Energy whose revenue sustainability depends on maximizing crude oil value in a transitioning energy economy, refinery-to-chemicals transformation represents not merely an operational optimization but an existential strategic imperative to maintain the economic value of their crude oil reserves across a multi-decade period in which transportation fuel demand declines but petrochemical feedstock demand grows.

Polymer Demand Growth in Developing Economies, Proximity to Petrochemical Feedstock Supply, and Higher Margin Realization of Chemical Products Over Fuel Blendstocks Justifying Conversion Capital Investment

The structural economic case for refinery-to-chemicals conversion is grounded in the significant and persistent value differential between petrochemical products including ethylene, propylene, paraxylene, and benzene and the fuel blendstocks including gasoline, diesel, and fuel oil that they replace in the refinery output slate, with ethylene typically valued at USD 600 to USD 900 per metric ton above the calorific equivalent value of naphtha as gasoline blendstock and paraxylene commanding USD 400 to USD 700 per metric ton premium over reformate as gasoline blendstock, creating a margin improvement of approximately USD 80 to USD 150 per barrel of crude oil processed when refinery output is successfully redirected from fuels to chemicals. The proximity of major crude oil producing regions including the Middle East and North Africa to the high-growth polymer and chemical consuming markets of Asia, South Asia, and East Africa provides an additional logistics and supply chain advantage to refinery-to-chemicals projects in these regions whose delivered chemical product cost competitiveness against Asian domestic production is enhanced by proximity to consumption, creating an investment environment where Middle Eastern and North African integrated refinery-to-chemicals facilities can access growing Asian polymer demand at competitive delivered economics. Refinery operators who successfully complete chemicals integration maintain a competitive advantage in product diversification that reduces their vulnerability to individual commodity cycle downturns, as the chemical product output from refinery-to-chemicals complexes participates in the polymer and specialty chemical margin cycles rather than the transportation fuel margin cycle, providing portfolio diversification that smooths overall facility EBITDA through petrochemical and fuel market cycles that have historically been imperfectly correlated and providing margin stability superior to single-cycle fuel-only refinery operations.

National Energy Security Strategies, Domestic Chemical Industry Development Goals, and Industrial Diversification Programs Mobilizing State Capital for Integrated Refinery-to-Chemicals Investment

National energy and industrial policy frameworks in China, India, Saudi Arabia, the United Arab Emirates, Iran, Kuwait, Indonesia, and Malaysia are explicitly incorporating refinery-to-chemicals integration as a strategic objective within their domestic petrochemical industry development programs, allocating state capital, providing feedstock subsidy support, and offering technology collaboration frameworks that mobilize investment at scales and risk tolerance levels not achievable through commercial investment criteria alone, creating a policy-supported investment pipeline that sustains refinery-to-chemicals technology demand independent of the short-term petrochemical commodity cycle. China’s 14th Five-Year Plan for the petroleum and chemical industry explicitly targets increasing chemical yield from Chinese refinery operations, with the National Development and Reform Commission approving multiple large-scale integrated refinery-petrochemical complex projects including the Yulong Petrochemical complex in Shandong at 40 million metric tons per year crude capacity with integrated olefins and aromatics production, and the Gulei Petrochemical complex in Fujian, collectively representing over USD 60 billion of state-guided investment in refinery-to-chemicals capacity that is simultaneously addressing China’s chemical self-sufficiency objective and creating a new generation of technically advanced integrated facilities. India’s ambition to achieve chemical industry revenues of USD 300 billion by 2025 and USD 1 trillion by 2040 under the national chemicals and petrochemicals policy framework is driving Reliance Industries, Indian Oil Corporation, and HPCL-Mittal Energy to pursue refinery integration upgrades that maximize petrochemical yield from their combined crude oil processing capacity of approximately 260 million metric tons per year, with Reliance Industries’ Jamnagar complex already achieving chemical integration at a level that generates approximately 40% of refinery throughput value from chemicals while maintaining full crude flexibility and transportation fuel capability.

Key Challenges

Extremely High Capital Investment Requirements, Long Project Execution Timelines, and Complex Multi-Technology Integration Risks Creating Financial and Execution Barriers for Refinery-to-Chemicals Conversion

The capital investment required to transform a conventionally configured petroleum refinery into a highly integrated chemicals complex through the installation of high-severity catalytic cracking units, hydroprocessing capacity additions, steam cracker units, aromatics extraction and paraxylene separation systems, olefin recovery and fractionation trains, and the associated utilities, storage, and infrastructure upgrades represents among the largest and most complex industrial capital projects in the energy and chemicals sector, with full-scale crude oil to chemicals conversion projects at 200,000 to 400,000 barrel per day processing scale requiring total capital expenditure of USD 5 to USD 20 billion depending on greenfield versus brownfield configuration, target chemical yield, and product slate complexity, making refinery-to-chemicals projects among the most capital-intensive industrial investments globally whose financial returns depend on sustained favorable petrochemical margin cycles over twenty to thirty-year project lives. The technical complexity of integrating multiple heterogeneous process units including hydroprocessing, catalytic cracking, steam cracking, aromatics separation, and olefin fractionation within a single operationally interconnected facility creates significant engineering interface risk, with inter-unit dependency meaning that the mechanical reliability and throughput performance of each unit directly affects the production rates and product quality of downstream units in ways that are difficult to fully model and validate before actual combined operation, generating start-up commissioning challenges and extended ramp-up periods that delay commercial production achievement and revenue realization relative to project schedules. Cost overrun risk on large integrated refinery-to-chemicals projects is systemic in the industry, with major projects including the Saudi Aramco Amiral complex, the Yulong Petrochemical project, and various Middle Eastern integrated complexes all experiencing capital cost increases of 20% to 40% above original approved estimates driven by engineering scope growth, construction labor inflation, equipment delivery delays, and pandemic-related supply chain disruptions that have collectively made large refinery-to-chemicals projects among the most challenging capital allocation decisions for corporate investment committees.

Petrochemical Product Oversupply Risk, Timing of Chemicals Margin Cycle Entry, and Competition from Dedicated Petrochemical Capacity Creating Revenue Uncertainty for New Refinery-to-Chemicals Capacity

The refinery-to-chemicals technology investment pipeline of the 2020s is occurring against a backdrop of significant petrochemical product oversupply in ethylene, polyethylene, propylene, polypropylene, and paraxylene created by the concurrent large-scale capacity additions of the 2020 to 2026 period in China, the United States, and the Middle East, creating a risk that new refinery-to-chemicals capacity completing construction and beginning product sales between 2026 and 2030 will enter markets characterized by compressed derivative margins and high competitive intensity that reduce the financial returns achievable in the early commercial production years that are most critical for project economics and capital recovery. Refinery-to-chemicals projects face competition not only from standalone petrochemical cracker and derivative units whose capital structure is lighter and whose product slate flexibility is greater than integrated facilities designed around specific crude oil processing configurations, but also from the rapidly expanding methanol-to-olefins and coal-to-olefins capacity in China whose coal and methanol feedstock cost independence from crude oil pricing creates a competitive floor price in Asian olefin markets that integrated crude oil to chemicals facilities must compete against regardless of their crude oil feedstock cost position. The chemical yield achieved by refinery-to-chemicals conversion is highly sensitive to crude oil feed quality, with high-sulfur heavy crude oils requiring substantially more intensive hydroprocessing to achieve the naphtha yield and quality suitable for steam cracker operation, and the processing cost and hydrogen consumption for high-sulfur residue upgrading consuming a significant portion of the chemical value improvement that lighter sweet crude processing could achieve, creating a feedstock quality dependency that constrains the economic attractiveness of refinery-to-chemicals conversion at refineries whose crude slate includes large proportions of heavy sour crudes.

Hydrogen Supply Intensity, Water Consumption, and Carbon Emissions Profile of Hydroprocessing-Intensive Refinery-to-Chemicals Configurations Complicating Sustainability and Regulatory Compliance

Refinery-to-chemicals conversion through intensive hydroprocessing routes, which represent the primary pathway for achieving high chemical yields from heavy and sour crude oil feedstocks, require extraordinarily large quantities of hydrogen to hydrodesulfurize, hydrocrack, and upgrade residual and intermediate refinery streams to the quality and yield profile required for steam cracker feed or aromatics extraction, with a crude oil to chemicals complex processing 400,000 barrels per day at 70% chemical yield potentially requiring 500,000 to 800,000 metric tons per year of hydrogen, equivalent to the hydrogen consumption of a major ammonia fertilizer complex, whose production from natural gas steam methane reforming generates approximately 8 to 10 metric tons of carbon dioxide per metric ton of hydrogen produced and represents a substantial greenhouse gas emissions burden that complicates regulatory compliance and sustainability reporting for integrated facility operators in carbon-priced jurisdictions. The carbon dioxide emissions intensity of hydroprocessing-intensive crude oil to chemicals facilities is substantially higher per ton of chemical product produced than equivalent steam cracker-based olefin production from natural gas liquids feedstock, creating a carbon cost disadvantage for crude oil to chemicals operators in jurisdictions with carbon pricing mechanisms including the European Union Emissions Trading System, UK ETS, and emerging Asian carbon markets whose progressive tightening will increase the relative cost competitiveness of low-carbon feedstock-based chemical production relative to crude oil to chemicals pathways that depend on high-emission hydrogen production from fossil natural gas. The water consumption intensity of integrated refinery-to-chemicals complexes whose cooling water, steam generation, hydroprocessing quench water, and process water requirements can reach 5 to 10 metric tons of water per metric ton of chemical product creates siting constraints and regulatory compliance obligations in water-stressed locations including the Middle East, China’s northern provinces, and India’s arid and semi-arid regions where major refinery-to-chemicals projects are planned, requiring significant desalination or water recycling infrastructure investment that adds to total project capital and operating cost.

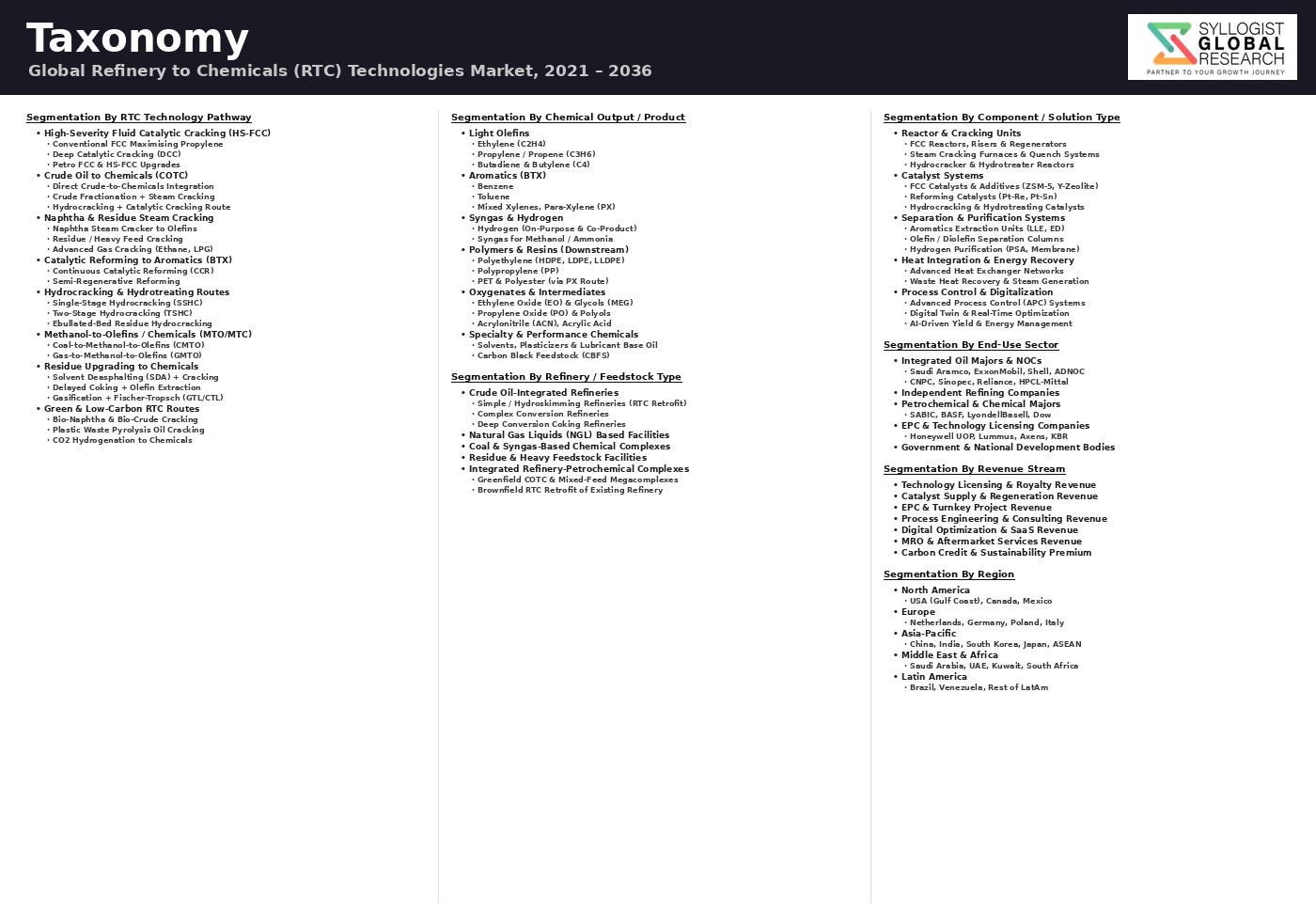

Market Segmentation

- Segmentation By Technology Pathway

- Crude Oil to Chemicals (COTC) Direct Conversion

- High-Severity and Maximum Propylene Fluid Catalytic Cracking (FCC)

- Steam Cracker Integration with Hydroprocessed Refinery Intermediates

- Deep Hydrocracking and Residue Upgrading for Chemical Feedstock

- Aromatics Extraction, Toluene Conversion, and Paraxylene Separation

- Naphtha Reforming and Dehydrogenation Integration

- Pyrolysis Oil and Plastic Waste Co-Processing

- Others

- Segmentation By Feedstock

- Crude Oil (Light Sweet, Medium Sour, and Heavy Crude)

- Atmospheric Residue and Vacuum Gas Oil

- Naphtha and Condensate

- Liquefied Petroleum Gas and Natural Gas Liquids

- Pyrolysis Oil from Plastic Waste

- Hydrocrackate and Hydrotreated Intermediates

- Others

- Segmentation By Target Chemical Product

- Ethylene and Derivatives

- Propylene and Polypropylene

- Benzene, Toluene, and Xylenes (BTX)

- Paraxylene and Purified Terephthalic Acid (PTA)

- Butadiene and C4 Olefins

- Cyclohexane and Specialty Aromatics

- Hydrogen and Synthesis Gas

- Others

- Segmentation By Project Type

- Greenfield Integrated Refinery-Petrochemical Complex

- Brownfield Refinery Conversion and Chemicals Integration Retrofit

- Refinery Petrochemical Interconnection and Feed Optimization

- Standalone Chemicals Integration Unit Addition

- Others

- Segmentation By Technology Provider

- Process Technology Licensing

- Catalyst Supply and Management

- Engineering, Procurement, and Construction (EPC)

- Digital and Process Optimization Software

- Others

- Segmentation By End User

- Integrated Oil and Chemical Companies

- National Oil Companies (NOCs)

- Independent Petroleum Refiners

- Petrochemical Companies Integrating Upstream

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Refinery-to-Chemicals Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology pathway including crude oil to chemicals direct conversion, high-severity fluid catalytic cracking, steam cracker integration with hydroprocessed intermediates, deep hydrocracking, aromatics extraction and paraxylene separation, and pyrolysis oil co-processing, by target chemical product including ethylene, propylene, paraxylene, benzene and toluene, and butadiene, and by project type including greenfield integrated complexes and brownfield conversion retrofits, to enable technology licensors, catalyst manufacturers, engineering companies, integrated oil and chemical companies, national oil companies, and capital market investors to identify the highest-value technology pathways and geographic markets generating the strongest investment demand through 2034?

- What is the operational performance, achieved chemical yield percentage, actual capital cost versus original estimate, commissioning timeline actualization, and commercial product margin realization of the landmark crude oil to chemicals and high-severity refinery-to-chemicals projects commissioned or under construction including the Saudi Aramco and TotalEnergies Amiral complex at Jubail, the Saudi Aramco and Sinopec Fujian refinery-to-chemicals project, the Yulong Petrochemical complex in Shandong, and the Gulei Petrochemical complex in Fujian, and what operational learnings and capital cost benchmarks from these first-of-kind commercial-scale projects are informing the investment decisions and technology selection of subsequent refinery-to-chemicals capacity additions by other national oil companies and integrated energy companies evaluating similar transformation strategies?

- How are the structural drivers of refinery-to-chemicals conversion including transportation fuel demand decline projections, fuel to chemical margin differential economics, polymer consumption growth in developing markets, and crude oil reserve monetization imperatives affecting the capital investment sanctioning decisions of the major national oil companies including Saudi Aramco, ADNOC, Kuwait Petroleum, Qatar Energy, Sinopec, PetroChina, Reliance Industries, and Indian Oil Corporation, and what specific investment volumes, technology selections, project timelines, product slate targets, and market positioning strategies characterize the refinery-to-chemicals programs of each of these major operators whose collective investment will define the majority of global refinery-to-chemicals capacity additions through 2034?

- What are the hydrogen consumption intensity, carbon dioxide emissions per ton of chemical product, water consumption, and total carbon footprint profile of hydroprocessing-intensive crude oil to chemicals configurations compared to naphtha-based steam cracking, ethane-based steam cracking, and methanol-to-olefins alternative chemical production pathways, and how are carbon pricing mechanisms including the EU ETS and emerging Asian carbon markets affecting the competitive cost position of crude oil to chemicals facilities operating in or exporting to carbon-priced markets, and what low-carbon hydrogen supply strategies including green hydrogen, blue hydrogen, and hydrogen import are refinery-to-chemicals operators evaluating to reduce the greenhouse gas intensity of their hydroprocessing hydrogen requirements within acceptable capital investment and operating cost parameters?

- How is the integration of plastic waste pyrolysis oil co-processing within refinery-to-chemicals technology configurations advancing from pilot-scale demonstrations toward commercial-scale deployment, what are the technical specifications, processing yield, hydroprocessing catalyst compatibility, and certified recycled content chain of custody requirements for pyrolysis oil integration at major refinery-to-chemicals facilities operated by LyondellBasell, Sabic, ExxonMobil, and Dow, and what volumes of post-consumer plastic waste feedstock can realistically be processed through refinery-to-chemicals pyrolysis oil co-processing pathways by 2034 as a contribution to the mandatory recycled content requirements of the European Union Packaging and Packaging Waste Regulation and equivalent circular economy mandates in other major markets?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil Price Volatility & Feedstock Cost Risk Affecting RTC Project Economics & Investment Return

- Peak Oil Demand, Energy Transition & Long-Term Fuel Demand Decline Risk Accelerating Refinery-to-Chemicals Conversion Need

- Technology Scale-Up, Catalyst Performance & Process Integration Complexity Risk in First-of-a-Kind RTC Projects

- Capital Intensity, EPC Cost Overrun & Project Financing Risk for Large Greenfield RTC Complex

- Petrochemical Overcapacity, Chemical Commodity Price Cyclicality & End-Market Demand Risk

- Regulatory Framework & Standards

- Refinery Environmental Permitting, Industrial Emission Directive (IED), Best Available Technique (BAT) Reference Document & Air Quality Regulation for Integrated Refinery-Petrochemical Complex

- Carbon Pricing, ETS & Low-Carbon Fuel Standard Regulation Impacting RTC Project Investment Economics: EU ETS, CBAM, UK ETS & National Carbon Tax on Refinery & Petrochemical Operations

- Petrochemical Product Registration & REACH Compliance: Chemical Safety Data, Downstream Use Registration & Hazardous Substance Management for RTC Output Streams

- Refinery Process Safety, OSHA PSM (Process Safety Management) & ATEX Equipment Standards for High-Pressure Cracking, Hydroprocessing & Aromatic Extraction Units

- National Petrochemical Industrial Policy, Special Economic Zone (SEZ) Incentive & Foreign Investment Framework: Saudi Vision 2030 Petchem Localisation, China Petrochemical Park Policy, India Petroleum, Chemicals & Petrochemicals Investment Region (PCPIR)

- Global Refinery-to-Chemicals (RTC) Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes of Chemical Output & Barrels per Day Converted)

- Market Size & Forecast by Technology Type

- Crude-to-Chemicals (CtC) Direct Conversion (Thermal, Catalytic & Combined Route)

- Naphtha Steam Cracking Integration with Refinery Complex

- Ethane & LPG Steam Cracking (Refinery Off-Gas & Associated Gas Based)

- High-Severity & Maximum Propylene Fluid Catalytic Cracking (HS-FCC & Max-Propylene FCC)

- Catalytic Reforming & Continuous Catalytic Reforming (CCR) for BTX Aromatics Production

- Aromatic Complex: Paraxylene (PX), Benzene Extraction & Xylene Isomerisation Technology

- Hydrocracking & Deep Hydroprocessing for Maximum Naphtha & Chemical Feedstock Yield

- Residue Upgrading to Chemicals: Resid FCC, Residue Hydrocracking & Gasification-to-Chemicals

- On-Purpose Propylene Technologies: Propane Dehydrogenation (PDH), Metathesis & Olefin Cracking

- Integrated Refinery-Petrochemical Complex (IPC) incorporating Full-Conversion Configuration

- Market Size & Forecast by Chemical Output

- Ethylene & Ethylene Derivatives (Polyethylene, Ethylene Oxide, EDC/VCM)

- Propylene & Propylene Derivatives (Polypropylene, Acrylonitrile, Propylene Oxide)

- Mixed C4 Fraction & Butadiene

- BTX Aromatics: Benzene, Toluene & Xylene (including Paraxylene for PTA/PET)

- Methanol & Methanol Derivatives (Formaldehyde, MTBE, Acetic Acid)

- Synthesis Gas & Hydrogen (By-Product & On-Purpose Production)

- Specialty Chemicals, Intermediates & Solvents

- Market Size & Forecast by Process Stage

- Feed Pre-Treatment: Desalting, Desulphurisation & Contaminant Removal

- Atmospheric & Vacuum Distillation Unit (ADU & VDU)

- Conversion & Cracking (FCC, Hydrocracker & Coker)

- Hydroprocessing (HDS, HDN & Hydrodeoxygenation)

- Reforming, Isomerisation & Aromatisation Unit

- Olefin & Aromatic Separation, Extraction & Fractionation

- Utilities, Heat Integration, Hydrogen Management & Energy Recovery

- Market Size & Forecast by Feedstock

- Light & Medium Crude Oil

- Heavy & Extra-Heavy Crude Oil & Bitumen

- Straight-Run & Hydrocracked Naphtha

- Vacuum Gas Oil (VGO) & Atmospheric Gas Oil

- Atmospheric & Vacuum Residue

- Ethane, LPG & Natural Gas Liquids (NGL)

- Recycled Plastics & Waste Pyrolysis Oil (Circular Feedstock)

- Market Size & Forecast by Project Type

- Greenfield Integrated Refinery-Petrochemical Complex (IPC) New Build

- Brownfield Refinery Conversion & Chemicals Yield Maximisation Upgrade

- Standalone Petrochemical Unit Addition to Existing Refinery

- Refinery Repurposing & Fuel-to-Chemicals Re-Configuration

- Market Size & Forecast by End-Use Chemical Market

- Polymers & Plastics (Polyethylene, Polypropylene, PTA & PET)

- Synthetic Fibres (Polyester, Nylon & Acrylic)

- Fertilisers, Methanol & Agricultural Chemicals

- Solvents, Coatings, Adhesives & Resins

- Specialty Chemicals & Pharmaceutical Intermediates

- Market Size & Forecast by End-User

- National Oil Company (NOC) & State Petrochemical Enterprise

- International Oil Company (IOC) with Integrated Chemicals Division

- Independent Petrochemical & Chemical Company

- Integrated Downstream Complex Operator (Refining + Chemicals + Polymers)

- Government & Sovereign Industrial Development Corporation

- Market Size & Forecast by Sales Channel

- Technology Licence & Process Design Package (Technology Licensor)

- EPC & EPCM Turnkey Contract (Engineering, Procurement & Construction)

- Joint Venture, Co-Development & Equity Participation Agreement

- Catalyst Supply, Equipment & Long-Term Service Agreement

- North America Refinery-to-Chemicals (RTC) Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Chemical Output)

- By Technology Type

- By Chemical Output

- By Process Stage

- By Feedstock

- By Project Type

- By End-Use Chemical Market

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Refinery-to-Chemicals (RTC) Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Chemical Output)

- By Technology Type

- By Chemical Output

- By Process Stage

- By Feedstock

- By Project Type

- By End-Use Chemical Market

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Refinery-to-Chemicals (RTC) Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Chemical Output)

- By Technology Type

- By Chemical Output

- By Process Stage

- By Feedstock

- By Project Type

- By End-Use Chemical Market

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Refinery-to-Chemicals (RTC) Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Chemical Output)

- By Technology Type

- By Chemical Output

- By Process Stage

- By Feedstock

- By Project Type

- By End-Use Chemical Market

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Refinery-to-Chemicals (RTC) Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Chemical Output)

- By Technology Type

- By Chemical Output

- By Process Stage

- By Feedstock

- By Project Type

- By End-Use Chemical Market

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Refinery-to-Chemicals (RTC) Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of Chemical Output)

- By Technology Type

- By Chemical Output

- By Process Stage

- By Feedstock

- By Project Type

- By End-Use Chemical Market

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, Netherlands, Belgium, Italy, United Kingdom, Russia, China, Japan, South Korea, India, Singapore, Malaysia, Indonesia, Saudi Arabia, UAE, Kuwait, Qatar, Brazil, Mexico, South Africa

- Technology Landscape & Innovation Analysis

- Crude-to-Chemicals (CtC) Direct Conversion Technology Deep-Dive: TC2C (SABIC/ExxonMobil), HS-FCC (Saudi Aramco/JX) & Advanced Thermal Catalytic Route Comparison

- Steam Cracking Technology: Naphtha, Ethane & Mixed Feed Cracker Design, Furnace Configuration & Integration Optimisation with Refinery Complex

- High-Severity FCC & Maximum Propylene FCC Technology: Reactor Design, Catalyst Selection, Riser Modification & C3 Yield Maximisation

- Aromatic Complex Technology: Continuous Catalytic Reforming (CCR), Selective Toluene Disproportionation (STDP), Paraxylene Adsorptive Separation (Parex) & Xylene Isomerisation

- Residue Upgrading to Chemicals: Resid Hydrocracking, Ebullated Bed, Slurry Phase Hydrocracking & Heavy Residue Gasification-to-Chemicals Technology

- On-Purpose Propylene Production: Propane Dehydrogenation (PDH) Catofin & Oleflex Technology, Metathesis & Olefin Cracking Unit (OCU)

- Process Integration, Heat Network, Hydrogen Pinch, Digital Twin & AI-Based Yield Optimisation Technology for RTC Complex

- Patent & IP Landscape in Refinery-to-Chemicals Technologies

- Value Chain & Supply Chain Analysis

- Crude Oil & Feedstock Supply Chain: NOC Production, Spot & Term Crude Procurement, Pipeline & Tanker Logistics

- Catalyst Manufacturing & Supply Chain: FCC Catalyst, Hydroprocessing Catalyst, Reforming Catalyst & Cracking Catalyst Supplier Landscape

- Process Equipment Supply Chain: Reactor, Column, Furnace, Compressor, Heat Exchanger & Rotating Equipment Manufacturer

- Technology Licensor, Process Design Package Provider & EPC Contractor Landscape

- RTC Complex Operator, NOC & IOC Integration & Project Development Channel

- Chemical Product Offtake, Storage, Logistics & Downstream Polymer & Chemical Marketing

- Catalyst Regeneration, Spent Catalyst Management, Waste Stream Treatment & Circular Feedstock Integration

- Pricing Analysis

- RTC Technology Licence Fee, Royalty & Process Design Package Cost Analysis by Technology Type & Capacity

- EPC & EPCM Project Cost Benchmarking for Greenfield IPC & Brownfield Conversion: USD per Tonne of Ethylene Equivalent Capacity

- Feedstock-to-Chemical Margin Analysis: Crude, Naphtha & Ethane Spread vs. Ethylene, Propylene, BTX & Polymer Price

- Catalyst Cost Analysis: FCC Catalyst, Hydroprocessing Catalyst & Reforming Catalyst Annual Consumption & Replacement Cost per Unit Output

- Operating Cost Comparison: RTC Integrated Complex vs. Standalone Cracker & Standalone Refinery Economics by Region & Feedstock

- Carbon Cost & CBAM Impact: RTC Complex CO2 Emission Intensity, EU ETS Allowance Cost & Carbon Border Adjustment Mechanism Financial Exposure for Chemical Exports

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of RTC Route vs. Conventional Refinery plus Standalone Cracker: CO2 Intensity, Energy Consumption & Water Use Comparison

- Carbon Capture & CCUS Integration Potential for RTC Complex: Refinery & Cracker Flue Gas CO2 Capture, H2 Production & Blue Hydrogen Integration

- Circular Economy & Waste Plastics Integration: Pyrolysis Oil & Chemical Recycling Feedstock Co-Processing in RTC Complex for Circular Polymer Production

- Hydrogen Economy Role of RTC: Grey, Blue & Green Hydrogen Production, Integration & Supply to Chemical & Refinery Processes

- Regulatory-Driven Sustainability: EU IED BAT Compliance, REACH Chemical Registration, Carbon Pricing Exposure & ESG Disclosure Reporting for Integrated Refinery-Petrochemical Operator

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Concentrated Technology Licensor Segment vs. Fragmented Operator Segment)

- Top 10 Players Market Share by Licence Awards, Installed Capacity & Technology Portfolio Breadth

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Type, Chemical Output & Geography

- Player Classification

- Global Integrated Technology Licensor & Process Design Package Provider (Full RTC Portfolio)

- Specialist Cracking Technology Licensor (Steam Cracking & FCC)

- Aromatic Complex & Paraxylene Technology Licensor

- Residue Upgrading & Hydrocracking Technology Licensor

- Catalyst Manufacturer for RTC Process Units (FCC, Hydroprocessing & Reforming)

- National Oil Company (NOC) with Proprietary RTC Technology Development

- EPC Contractor & Process Systems Integrator for Refinery-Petrochemical Complex

- Emerging Digital, AI & Process Optimisation Platform Provider for RTC Operations

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Chemical Output & Region

- Company Profile

- Company Overview & Headquarters

- RTC Technology Products, Licence Portfolio & Process Design Package

- Key Customer Relationships & Reference Plant Installations

- Manufacturing Footprint & Installed RTC Capacity Under Licence

- Revenue (RTC Technology & Catalyst Segment) & Backlog

- Technology Differentiators & IP Portfolio

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Licence Awards, Plant Start-Ups, Technology Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Breadth vs. Licence Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Type, Chemical Output, Feedstock, Project Type & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Technology Portfolio & R&D Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Market Development Strategy

- Customer & Operator Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Circular Feedstock & Decarbonisation Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)