Market Definition

The Global Renewable Energy-Powered Desalination Market encompasses the engineering, procurement, construction, commissioning, and operation of water treatment systems that remove dissolved salts, minerals, and contaminants from seawater, brackish groundwater, and impaired water sources through thermally or pressure-driven separation processes powered entirely or substantially by solar photovoltaic, wind, concentrated solar power, wave energy, geothermal, or hybrid renewable energy sources, eliminating or substantially reducing the dependence on fossil fuel-derived electricity and heat that has historically constrained the sustainability credentials and geographic deployability of conventional desalination infrastructure. The market encompasses the complete project and technology portfolio spanning small-scale off-grid solar-powered reverse osmosis systems of below 100 cubic meters per day capacity serving remote communities, islands, and humanitarian applications through medium-scale wind and solar hybrid reverse osmosis installations of 100 to 10,000 cubic meters per day serving coastal towns, industrial facilities, and agricultural users, to large-scale utility-grade seawater reverse osmosis plants of above 100,000 cubic meters per day capacity procuring renewable electricity through dedicated power purchase agreements, captive generation assets, or grid renewable energy procurement frameworks. The primary desalination technologies integrated with renewable energy systems include reverse osmosis membrane separation, which accounts for the dominant share of new installed capacity globally due to its electrical energy compatibility with variable renewable power sources and its continuously improving specific energy consumption performance now achievable below 2.0 kilowatt-hours per cubic meter at full energy recovery; multi-effect distillation thermal desalination using concentrated solar power or waste heat; membrane distillation using low-grade solar thermal energy; electrodialysis reversal systems suited for brackish water desalination powered by solar photovoltaic; and forward osmosis systems at developmental commercial stage. Key participants include desalination technology licensors and equipment suppliers, engineering procurement and construction contractors, renewable energy developers, project finance providers, water utility offtakers, national water authorities, and technology development organizations advancing next-generation membrane and energy recovery innovations.

Market Insights

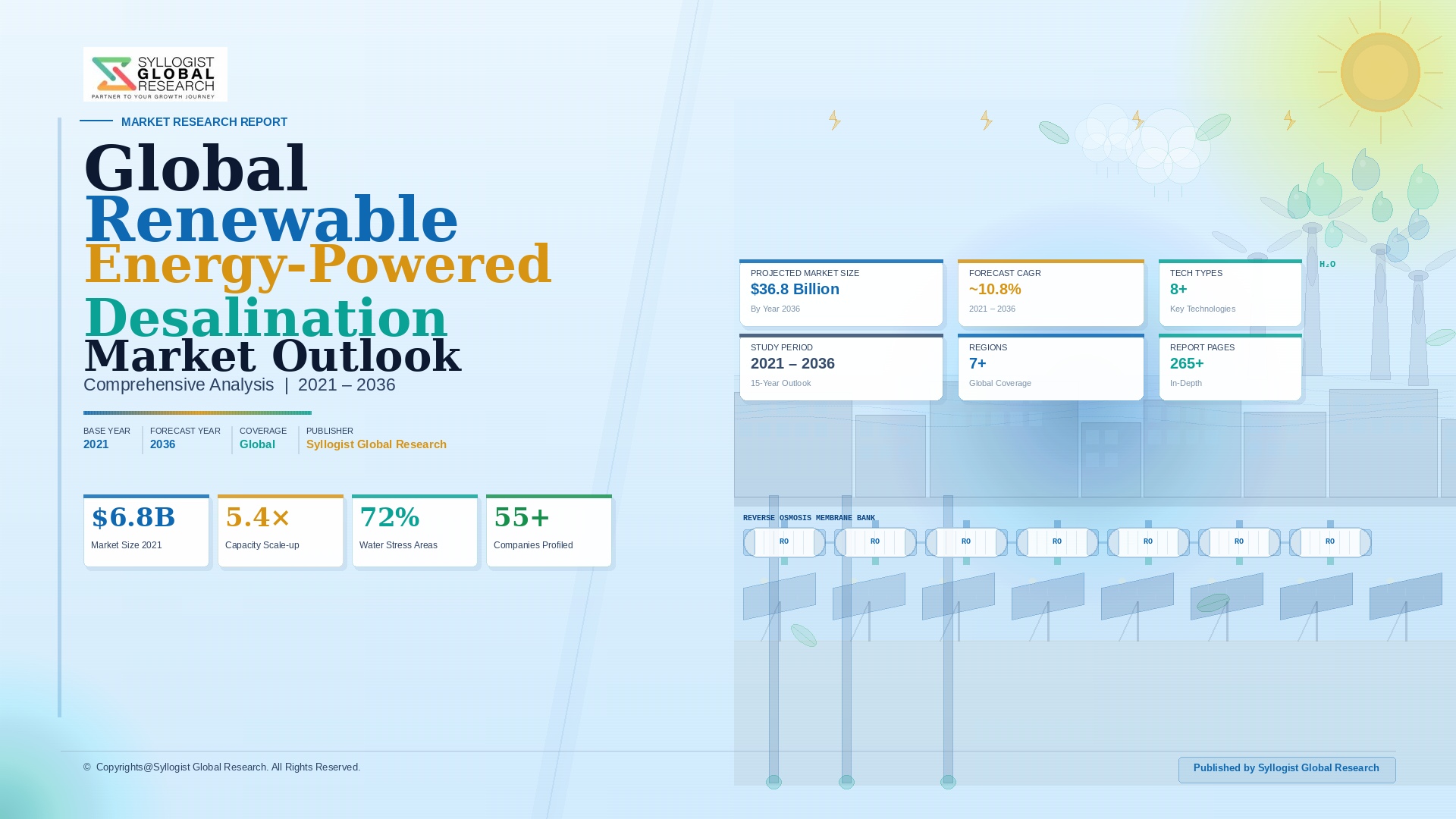

The global renewable energy-powered desalination market was valued at approximately USD 4.2 billion in 2025 and is projected to reach USD 14.8 billion by 2034, advancing at a compound annual growth rate of 15.1% over the forecast period from 2027 to 2034, driven by the simultaneous structural deterioration of freshwater availability across water-stressed geographies in the Middle East, North Africa, South Asia, Southern Europe, Sub-Saharan Africa, and coastal Australia, the dramatic decline in renewable energy generation costs that has fundamentally transformed the economic case for clean desalination, and the growing policy alignment between national water security strategies and net-zero energy transition commitments that makes renewable-powered desalination the preferred technology solution for closing the widening gap between freshwater demand and conventionally available supply. Global installed desalination capacity reached approximately 114 million cubic meters per day in 2025, of which renewable energy-powered installations accounted for approximately 8.4% by production volume, a share projected to grow to approximately 31.6% by 2034 as new capacity additions across the Middle East, North Africa, Asia-Pacific, and Latin America are increasingly configured with dedicated renewable power supply rather than the fossil fuel-based electricity that continues to dominate the existing installed base. The economics of solar-powered reverse osmosis desalination have undergone a transformative improvement over the past decade, with the levelized cost of desalinated water from solar photovoltaic-powered seawater reverse osmosis systems declining from approximately USD 1.80 to USD 2.40 per cubic meter in 2015 to approximately USD 0.52 to USD 0.78 per cubic meter at large-scale plants in high-irradiance locations in 2025, a cost reduction trajectory driven by the near-continuous decline in solar photovoltaic module and inverter costs, improvements in reverse osmosis membrane performance and energy recovery device efficiency, and the accumulation of operational experience in optimizing variable-power-input desalination plant design and control systems.

The Middle East and North Africa region constitutes the dominant geographic market for renewable energy-powered desalination, accounting for approximately 46% of global market revenue in 2025, anchored by the extraordinarily ambitious desalination capacity expansion programs of Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, Bahrain, Oman, Egypt, and Morocco whose combination of world-class solar and wind resources, severe freshwater scarcity, rapidly growing municipal and industrial water demand, and government-mandated transition away from oil and gas-fired desalination power supply creates the most commercially concentrated and capital-intensive deployment environment for renewable desalination globally. Saudi Arabia’s National Water Company has committed to achieving 30% renewable energy powering of its desalination capacity by 2030 as part of the Kingdom’s Vision 2030 energy transition framework, with NEOM’s water supply infrastructure incorporating the world’s largest planned renewable energy-powered desalination complex at approximately 500,000 cubic meters per day capacity powered entirely by dedicated wind and solar generation, representing a flagship project that demonstrates the commercial and technical feasibility of gigawatt-scale renewable desalination at unprecedented project scale. The United Arab Emirates has commissioned the Al Taweelah desalination plant in Abu Dhabi at a capacity of approximately 909,200 cubic meters per day, developed under a public-private partnership framework with a committed trajectory toward renewable power integration, while the Hassyan seawater reverse osmosis plant in Dubai at approximately 818,000 cubic meters per day represents one of the largest reverse osmosis facilities globally, with both projects establishing benchmark reference points for large-scale seawater reverse osmosis economics and renewable integration pathways applicable across the Gulf Cooperation Council desalination sector. The Ouarzazate integrated solar and desalination complex in Morocco and the DEWA-affiliated renewable desalination programs in Dubai collectively illustrate the regional momentum toward solar-powered water production that is reshaping infrastructure investment patterns across North Africa and the Arabian Peninsula through the forecast period.

The reverse osmosis technology platform represents the overwhelmingly dominant desalination technology integrated with renewable energy systems, accounting for approximately 79% of renewable desalination installed capacity additions globally in 2025, reflecting reverse osmosis electricity compatibility with variable renewable power generation, the technology’s continuous specific energy consumption improvement from above 10 kilowatt-hours per cubic meter in 1980 to below 2.0 kilowatt-hours per cubic meter at world-class facilities in 2025 through advances in high-efficiency membrane elements, pressure center and isobaric energy recovery devices, and high-pressure pump design, and the technology’s modular scalability that enables deployment across the full capacity range from below one cubic meter per day for individual household applications through to mega-plant installations exceeding 500,000 cubic meters per day. The emergence of battery energy storage systems as an enabling component of off-grid and grid-independent renewable desalination configurations is progressively resolving the historically problematic operational incompatibility between the variable and intermittent power output of solar photovoltaic and wind generation and the requirement for stable continuous power input to maintain reverse osmosis membrane performance, reduce fouling accumulation, and optimize water recovery ratios, with lithium-ion battery storage integrated within solar reverse osmosis systems enabling continuous 24-hour operation on renewable power at island and remote community installations where the alternative is either diesel backup generation or operational shut-down during low-irradiance periods that compromises daily water production reliability. Concentrated solar power with integrated thermal storage is emerging as a commercially attractive renewable energy platform for thermal desalination applications including multi-effect distillation and membrane distillation in regions combining high direct normal irradiance with requirements for reliable 24-hour water production unaffected by solar variability, with the NOOR complex in Morocco and emerging concentrated solar power projects in Saudi Arabia, Oman, and the United Arab Emirates demonstrating the commercial viability of dispatchable solar thermal power for continuous desalination plant operation.

The small and medium-scale off-grid and decentralized renewable desalination segment is emerging as the fastest-growing sub-market within the global renewable energy-powered desalination landscape, driven by the acute freshwater access crisis affecting approximately 2.2 billion people globally who lack access to safely managed drinking water, the proliferation of low-cost solar photovoltaic technology reaching remote and island communities at price points enabling economically viable small-scale desalination deployment, and the recognition by development finance institutions, humanitarian organizations, and national governments that distributed solar-powered desalination represents a faster, more resilient, and more cost-effective water security solution for remote coastal, island, and arid rural communities than the conventional approach of extending centralized water supply infrastructure across challenging terrain at prohibitive capital cost. Solar-powered containerized reverse osmosis systems of 50 to 500 cubic meters per day capacity are being deployed across Pacific island nations, Caribbean islands, remote coastal communities in Sub-Saharan Africa, and arid inland regions of India, Chile, and Peru at capital costs declining toward USD 800 to USD 1,400 per cubic meter per day of installed capacity, with the modular container format enabling sea freight delivery, rapid on-site commissioning without specialized civil works, and future capacity expansion through additional module addition without plant redesign. The intersection of climate finance, development assistance funding, and blended finance instruments from multilateral development banks including the World Bank, Asian Development Bank, African Development Bank, and the Green Climate Fund is mobilizing concessional capital for renewable desalination deployment in least developed countries and small island developing states that lack the sovereign credit quality and project scale required to attract commercial project finance on standalone bankability assessments, creating a publicly subsidized demand base for small and medium-scale renewable desalination technology deployment that complements the commercially self-sustaining large utility-scale segment.

Key Drivers

Precipitous Decline in Solar Photovoltaic and Wind Energy Generation Costs Reaching Grid Parity and Enabling Economically Competitive Renewable-Powered Desalination Across Water-Stressed Geographies

The sustained and accelerating reduction in the levelized cost of electricity from solar photovoltaic and wind energy generation over the past decade has fundamentally transformed the economic case for renewable-powered desalination from an environmentally motivated premium solution requiring subsidy support into an increasingly cost-competitive and commercially self-sustaining water production pathway that in high-irradiance and high-wind-resource locations can produce desalinated water at costs below conventional fossil fuel-powered alternatives when the full energy cost differential is accounted for within project levelized cost analysis. Solar photovoltaic electricity generation costs have declined from approximately USD 0.28 per kilowatt-hour in 2015 to approximately USD 0.033 per kilowatt-hour at record competitive tender results in 2025 in high-irradiance markets including Saudi Arabia, UAE, Chile, and India, enabling the procurement of clean electricity for large-scale seawater reverse osmosis at energy input costs that are below the fuel cost component alone of oil and gas-fired power generation used for conventional desalination, fundamentally inverting the cost economics that made renewable desalination more expensive than fossil-powered alternatives throughout the preceding two decades. The combination of low solar electricity cost and the specific energy consumption of advanced seawater reverse osmosis systems below 2.0 kilowatt-hours per cubic meter enables levelized water production costs at large-scale renewable desalination plants in optimal locations below USD 0.55 per cubic meter, a cost level that is competitive with conventional desalination in all but the lowest-cost gas-fired power markets and substantially below the cost of water trucking, emergency water supply, or conventional surface water treatment in water-scarce regions dependent on diminishing groundwater and declining precipitation that represent the true alternative water supply cost basis for renewable desalination investment appraisal in most water-stressed markets.

Acute and Worsening Global Freshwater Scarcity, Groundwater Depletion, and Climate Change-Driven Reduction in Surface Water Availability Expanding the Addressable Market for Desalinated Water Supply

The structural intensification of global freshwater scarcity driven by population growth concentrating in coastal and arid urban centers, agricultural expansion increasing irrigation demand from already over-extracted groundwater aquifers, industrial water consumption growing with economic development, and climate change reducing precipitation reliability and accelerating glacier retreat that feeds historically dependable river systems, is expanding the geographic scope and urgency of desalination as the primary climate-resilient water supply augmentation solution for an increasing number of national and regional water security strategies that recognize conventional freshwater sources as insufficient to sustainably meet projected demand trajectories within the forecast period. Approximately 4.0 billion people currently experience severe water scarcity for at least one month per year, a figure projected to increase to 5.7 billion by 2050 under climate change scenarios, while groundwater aquifer depletion in major agricultural regions including the Arabian aquifer system, the Central Valley of California, the North China Plain, and the Indo-Gangetic Plain is reducing available groundwater volumes at rates that cannot be replenished within human planning horizons, making seawater and brackish water desalination the only technically reliable and climate-independent water supply augmentation pathway for coastal populations in these regions. The progressive alignment of national water security strategies with renewable energy transition commitments in water-stressed nations including Saudi Arabia, Israel, Chile, India, Spain, Morocco, and Australia is institutionalizing renewable-powered desalination as the preferred policy response to freshwater scarcity, with government water master plans, national determined contributions to the Paris Agreement, and sustainable development goal implementation programs collectively creating durable policy demand pull for renewable desalination capacity investment that extends across electoral cycles and commodity price fluctuations.

Net-Zero Energy Transition Mandates, Carbon Pricing Mechanisms, and Sustainability-Linked Project Finance Requirements Driving Decarbonization of Existing Desalination Infrastructure

The global net-zero energy transition imperative is creating a powerful retrofitting and repowering demand stream within the renewable desalination market as the substantial existing base of fossil fuel-powered desalination infrastructure, estimated at over 100 million cubic meters per day of installed capacity globally consuming approximately 75 to 100 billion kilowatt-hours of electricity and thermal energy annually derived predominantly from natural gas and oil, faces mounting decarbonization pressure from national carbon pricing frameworks, corporate net-zero commitments by water utility operators, sustainability-linked project finance covenants, and the growing reputational and regulatory risk associated with operating carbon-intensive water infrastructure in an era of mandatory climate-related financial disclosure and social license scrutiny. The Gulf Cooperation Council desalination sector, which operates the world’s largest concentration of thermal and reverse osmosis desalination capacity consuming approximately 22 billion kilowatt-hours of electricity and generating approximately 15 million metric tons of carbon dioxide annually, is the highest-priority target for renewable energy retrofitting investment, with Saudi Arabia, UAE, Qatar, and Kuwait each having announced national decarbonization programs for their desalination sectors supported by sovereign wealth fund investment, development bank financing, and public-private partnership frameworks that are mobilizing renewable power generation and grid integration capital specifically for desalination sector decarbonization. Sustainability-linked loan facilities and green bond issuances by water utilities and desalination project developers that embed renewable energy integration milestones within financial covenant structures are creating direct financial incentives for accelerating the transition of desalination plant power supply from fossil to renewable sources, with the cost of capital differential between sustainability-linked and conventional debt reaching 15 to 40 basis points in favorable market conditions, providing a financially material incentive for utilities to advance renewable integration timelines beyond what regulatory obligation alone would mandate.

Key Challenges

Intermittency and Variability of Renewable Energy Sources Creating Operational Reliability, Membrane Performance, and Water Production Consistency Challenges for Desalination Plants

The fundamental technical incompatibility between the variable and intermittent power output profiles of solar photovoltaic and wind generation and the operational requirements of reverse osmosis membrane systems for stable pressure, consistent flow rates, and continuous operation to maintain optimal membrane performance, minimize biological and scaling fouling accumulation, and achieve reliable daily water production volumes represents the central engineering challenge governing the design, capital cost, and operational economics of renewable-powered desalination installations across all scales of deployment. Reverse osmosis membranes subjected to frequent start-stop cycling, pressure fluctuation, and flow variability experience accelerated membrane compaction, elevated concentration polarization at the membrane surface during low-flow periods, and increased biological fouling risk during shut-down intervals when residual feedwater within the pressure vessel system provides a growth medium for microorganism colonization, collectively degrading membrane performance, reducing water recovery ratios, and shortening membrane replacement intervals relative to continuously operated fossil-powered plants in ways that increase operating cost and reduce water production reliability. The capital cost of integrating battery energy storage systems of sufficient capacity to buffer solar photovoltaic generation variability and enable continuous reverse osmosis operation through nighttime and low-irradiance periods adds approximately USD 0.12 to USD 0.28 per cubic meter of water produced to the levelized cost of off-grid solar desalination systems depending on storage duration requirement, battery technology, and system scale, representing a significant cost increment that narrows the competitive advantage of renewable desalination over grid-connected alternatives in locations where grid electricity is available at reasonable cost and partially erodes the levelized cost of water improvements achievable through low-cost solar electricity procurement alone.

High Capital Investment Requirements, Long Project Development Timelines, and Complex Multi-Party Contractual Structures Creating Financing and Execution Barriers for Renewable Desalination Projects

Large-scale renewable energy-powered desalination projects require the simultaneous development, financing, and contractual integration of two capital-intensive infrastructure assets, a renewable energy generation facility and a desalination plant, whose combined capital investment, technology risk profiles, permitting timelines, and bankability requirements create project development complexity substantially exceeding that of either asset developed independently, with total project capital expenditure for a large-scale solar-powered seawater reverse osmosis plant of 200,000 cubic meters per day capacity including dedicated solar photovoltaic generation, battery storage, reverse osmosis process trains, brine outfall infrastructure, and water transmission connection typically ranging from USD 400 million to USD 700 million depending on site conditions, water source salinity, and storage configuration, requiring multi-source project finance structures combining commercial bank debt, development bank concessional lending, export credit agency support, and equity from specialized infrastructure funds that take 24 to 48 months to assemble and execute. Permitting and environmental impact assessment processes for coastal desalination facilities incorporating large seawater intake and brine outfall structures require multi-agency regulatory approvals addressing coastal zone management, marine ecosystem impact, brine dispersion modeling, impingement and entrainment assessment for marine organism protection, and desalination plant noise, visual, and land use impact assessments that collectively extend project development timelines by three to seven years from concept to construction commencement in most jurisdictions, creating long pre-revenue development cost periods and regulatory approval risk that discourages smaller developers and increases the market concentration of large integrated infrastructure companies with balance sheet capacity to sustain extended pre-construction development programs. The absence of standardized offtake agreement structures, water tariff regulatory frameworks, and bankable contractual templates for renewable desalination projects across many emerging market geographies further increases legal and commercial structuring cost and timeline for projects targeting water-scarce developing country markets.

Concentrated Brine Discharge Environmental Impacts, Coastal Ecosystem Sensitivity, and Marine Permitting Complexity Constraining Suitable Site Availability for Seawater Desalination Expansion

Seawater reverse osmosis desalination produces a concentrated brine reject stream typically at approximately twice the salinity of the source seawater that must be discharged to the marine environment, and despite advances in brine dilution, diffuser design, and offshore discharge engineering that reduce near-field concentration elevation above ambient seawater baseline, the cumulative environmental impact of large-scale brine discharge on benthic marine ecosystems, seagrass meadows, coral reef communities, and coastal fisheries habitats in shallow or semi-enclosed coastal water bodies represents a significant ecological concern that is increasingly scrutinized by marine regulatory authorities and environmental advocacy organizations and is progressively constraining the permissible siting, discharge volume, and operating conditions of coastal desalination facilities in environmentally sensitive locations. The Mediterranean Sea, Persian Gulf, Red Sea, and enclosed coastal embayments in Australia, California, and Southeast Asia where large concentrations of desalination capacity are proposed or operating are particularly vulnerable to cumulative brine salinity elevation given their limited water exchange with open ocean systems, with scientific studies documenting measurable salinity anomalies in the Persian Gulf attributable to aggregate brine discharge from the region’s concentrated desalination capacity, raising concerns about long-term ecosystem impacts at the scale of basin-wide water quality that are prompting regional regulatory review of total brine discharge loading. Brine valorization and zero liquid discharge technologies that recover additional minerals, salts, and chemicals from brine concentrate streams before disposal, including lithium recovery from desalination brine that is attracting growing commercial interest given lithium’s critical mineral designation, have the potential to reduce net brine volumes and improve the environmental and economic sustainability of large-scale desalination operations, but remain at early commercial development stages with process economics that have not yet demonstrated competitiveness at the brine concentrations and volumes characteristic of seawater reverse osmosis operations at current commodity prices.

Market Segmentation

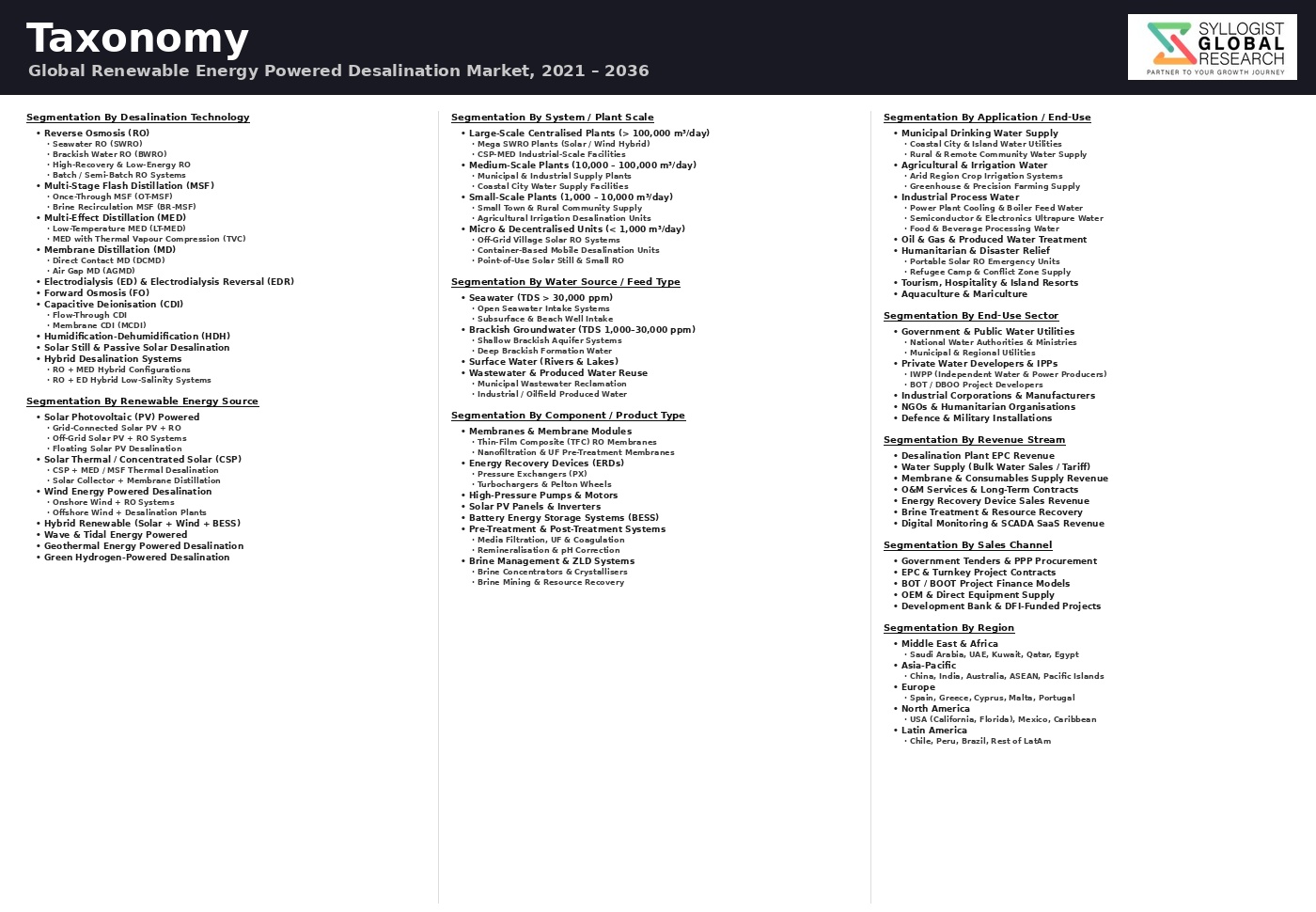

- Segmentation By Desalination Technology

- Reverse Osmosis (Seawater Reverse Osmosis and Brackish Water Reverse Osmosis)

- Multi-Effect Distillation

- Multi-Stage Flash Distillation

- Membrane Distillation

- Electrodialysis and Electrodialysis Reversal

- Forward Osmosis

- Hybrid Desalination Systems (Thermal and Membrane Combined)

- Others

- Segmentation By Renewable Energy Source

- Solar Photovoltaic

- Wind Energy (Onshore and Offshore)

- Concentrated Solar Power with Thermal Storage

- Solar Photovoltaic and Wind Hybrid

- Solar Photovoltaic with Battery Energy Storage

- Wave and Tidal Energy

- Geothermal Energy

- Others (Green Hydrogen-Powered, Biomass, and Multi-Source Hybrid)

- Segmentation By Plant Capacity

- Small Scale (Below 100 Cubic Meters per Day)

- Medium Scale (100 to 10,000 Cubic Meters per Day)

- Large Scale (10,000 to 100,000 Cubic Meters per Day)

- Mega Scale (Above 100,000 Cubic Meters per Day)

- Segmentation By Water Source

- Seawater

- Brackish Groundwater

- Wastewater and Treated Effluent (Indirect Potable Reuse)

- River and Surface Water with High Salinity

- Others

- Segmentation By Grid Connectivity

- Off-Grid Standalone Renewable Desalination Systems

- Grid-Connected with Dedicated Renewable Power Purchase Agreement

- Grid-Connected with Captive On-Site Renewable Generation

- Hybrid Grid and Renewable with Fossil Fuel Backup

- Others

- Segmentation By End-Use Application

- Municipal and Urban Drinking Water Supply

- Agricultural and Irrigation Water Supply

- Industrial Process Water (Oil and Gas, Mining, Power, and Manufacturing)

- Tourism and Hospitality Water Supply

- Remote Community and Island Water Supply

- Humanitarian and Emergency Water Supply

- Others

- Segmentation By Project Delivery Model

- Build-Own-Operate and Build-Own-Operate-Transfer

- Public-Private Partnership and Design-Build-Finance-Operate

- Engineering-Procurement-Construction (Turnkey)

- Equipment Supply and Technology Licensing

- Operations and Maintenance Service Contracts

- Others

- Segmentation By Region

- Middle East and North Africa

- Asia-Pacific

- Europe

- North America

- Sub-Saharan Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Renewable Energy-Powered Desalination Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by desalination technology including reverse osmosis, multi-effect distillation, membrane distillation, and electrodialysis, by renewable energy source including solar photovoltaic, wind, concentrated solar power, and hybrid configurations, by plant capacity including small off-grid, medium, large, and mega-scale installations, and by end-use application including municipal water supply, agricultural irrigation, industrial process water, and remote community water supply, to enable desalination technology suppliers, renewable energy developers, project finance institutions, water utility operators, national water authorities, and infrastructure investors to identify the highest-growth technology and application combinations generating the most commercially durable demand across the forecast period to 2034?

- How has the levelized cost of water produced through solar photovoltaic-powered seawater reverse osmosis evolved from approximately USD 1.80 to USD 2.40 per cubic meter in 2015 to approximately USD 0.52 to USD 0.78 per cubic meter in 2025 at large-scale plants in optimal irradiance locations, and what is the projected cost reduction trajectory through 2034 as solar electricity costs continue declining, reverse osmosis membrane performance improves, energy recovery device efficiency advances, and battery storage costs decrease, and under what combinations of solar irradiance level, plant scale, feedwater salinity, grid connectivity, and battery storage configuration does renewable desalination achieve full levelized cost parity with fossil fuel-powered desalination and with alternative water supply solutions including groundwater extraction, wastewater reuse, and long-distance water transfer across the major water-stressed geographic markets?

- What are the national water security strategies, desalination capacity expansion programs, renewable energy integration commitments, project pipeline details, and technology procurement preferences of the largest renewable desalination market developers across Saudi Arabia, the United Arab Emirates, Israel, Australia, Chile, India, Spain, Morocco, and the United States, and how are major engineering procurement and construction contractors, technology licensors, and integrated water and energy companies including ACCIONA Agua, SUEZ, Veolia Water Technologies, IDE Technologies, Doosan Enerbility, ACWA Power, and Abengoa positioning their renewable desalination technology offerings, project development capabilities, and long-term service and operations capabilities to capture market share across utility-scale, industrial, and decentralized application segments in these priority markets through 2034?

- How are the operational challenges of integrating variable solar photovoltaic and wind power generation with reverse osmosis membrane systems being addressed through battery energy storage buffer systems, variable frequency drive pressure pump control, smart plant automation and predictive control algorithms, and hybrid renewable and grid connection architectures, and what are the quantified impacts of different levels of renewable energy integration on reverse osmosis membrane lifetime, water recovery ratio, specific energy consumption, and levelized water production cost at commercial-scale operating plants, and which operational strategies and control system approaches are demonstrating the best outcomes in reconciling renewable energy variability with the membrane performance stability requirements of continuous desalination operations?

- What are the environmental impact assessment requirements, brine discharge permitting frameworks, coastal zone management restrictions, and marine ecosystem protection obligations applicable to seawater desalination facility development across major coastal markets including the Mediterranean Sea countries, Gulf Cooperation Council nations, Australia, the United States Pacific Coast, and India, and how are emerging brine valorization technologies for lithium, magnesium, and other mineral recovery from desalination concentrate streams evolving toward commercial viability in ways that could reduce net brine discharge volumes, generate additional revenue streams from mineral co-production, and improve the environmental and financial sustainability profile of large-scale renewable desalination operations through the forecast period to 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Renewable Energy Intermittency & Water Production Reliability Risk

- Technology Integration, Scaling & Performance Risk

- Regulatory, Permitting & Water Rights Risk

- Market, Financing & Project Development Risk

- Environmental, Brine Disposal & Marine Ecosystem Risk

- Regulatory Framework & Standards

- National Water Security, Desalination Licensing & Water Quality Standards

- Renewable Energy Policy, Feed-in Tariff, Auction & Grid Connection Frameworks for Desalination

- Brine & Concentrate Discharge Regulations, Marine Environmental Protection & Zero Liquid Discharge Standards

- Drinking Water Quality Standards (WHO Guidelines, EU Directive, US EPA) for Desalinated Water Supply

- International Finance, Green Bond, Climate Fund & PPP Procurement Standards for RE-Desalination Projects

- Global Renewable Energy-Powered Desalination Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Cubic Metres per Day of Installed Capacity)

- Market Size & Forecast by Desalination Technology

- Reverse Osmosis (RO): Seawater (SWRO) & Brackish Water (BWRO)

- Multi-Stage Flash (MSF) Distillation

- Multi-Effect Distillation (MED) & MED-Thermal Vapour Compression (MED-TVC)

- Electrodialysis (ED) & Electrodialysis Reversal (EDR)

- Membrane Distillation (MD)

- Forward Osmosis (FO)

- Capacitive Deionisation (CDI) & Electrochemical Desalination

- Humidification-Dehumidification (HDH) & Solar Still Systems

- Market Size & Forecast by Renewable Energy Source

- Solar Photovoltaic (PV) Powered Desalination

- Wind Energy Powered Desalination (Onshore & Offshore Wind)

- Solar Thermal & Concentrated Solar Power (CSP) Powered Desalination

- Hybrid Solar PV + Wind Powered Desalination

- Geothermal Energy Powered Desalination

- Wave & Tidal Energy Powered Desalination

- Green Hydrogen-Powered Desalination (Fuel Cell & Electrolysis-Integrated)

- Market Size & Forecast by System Size / Capacity

- Small-Scale & Decentralised Systems (Up to 100 m3/day: Remote, Rural & Island Applications)

- Medium-Scale Systems (100 to 10,000 m3/day: Small Municipality & Industrial)

- Large-Scale Systems (10,000 to 100,000 m3/day: Municipal & Industrial)

- Mega-Scale Systems (Above 100,000 m3/day: National Water Security Infrastructure)

- Market Size & Forecast by Feed Water Source

- Seawater Desalination (Open Sea Intake & Subsurface Intake)

- Brackish Water Desalination (Groundwater, Inland Saline Aquifer & Estuary)

- Wastewater Reclamation & Reuse (Tertiary Treatment & Advanced Purification)

- Agricultural & Industrial Process Water Reuse & Brine Recovery

- Market Size & Forecast by Component

- Membranes & Membrane Elements (RO, NF, UF & MF Membranes)

- High-Pressure Pumps, Energy Recovery Devices (ERD) & Pressure Exchangers

- Pre-Treatment Systems (Media Filtration, UF Pre-Treatment, Chemical Dosing)

- Post-Treatment & Remineralisation Systems

- Renewable Energy Equipment (Solar PV Panels, Wind Turbines, Inverters & BESS)

- Control Systems, SCADA, Digital Monitoring & Automation Platforms

- Brine Management, Concentrate Treatment & Zero Liquid Discharge (ZLD) Systems

- Market Size & Forecast by End-Use Application

- Municipal & Public Water Supply

- Industrial Process Water (Power Generation, Mining, Oil & Gas, Chemicals)

- Agricultural Irrigation Water Supply

- Emergency, Humanitarian & Disaster Relief Water Supply

- Off-Grid, Remote Community & Island Water Supply

- Water Reuse & Circular Water Economy Applications

- Market Size & Forecast by End-User

- Government & Municipal Water Authorities

- Independent Water & Power Producers (IWPPs) & Project Developers

- Industrial & Mining Operators

- Agricultural Cooperative & Irrigation Scheme Operators

- Humanitarian & NGO Organisations

- Market Size & Forecast by Sales Channel

- EPC / Turnkey Project Contract (Engineering, Procurement & Construction)

- Build-Operate-Transfer (BOT), PPP & Concession Contract

- Water-as-a-Service (WaaS) & Design-Build-Operate (DBO) Contract

- Direct Equipment Supply & System Integration Channel

- North America Renewable Energy-Powered Desalination Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres per Day of Installed Capacity)

- By Desalination Technology

- By Renewable Energy Source

- By System Size / Capacity

- By Feed Water Source

- By Component

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Renewable Energy-Powered Desalination Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres per Day of Installed Capacity)

- By Desalination Technology

- By Renewable Energy Source

- By System Size / Capacity

- By Feed Water Source

- By Component

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Renewable Energy-Powered Desalination Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres per Day of Installed Capacity)

- By Desalination Technology

- By Renewable Energy Source

- By System Size / Capacity

- By Feed Water Source

- By Component

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Renewable Energy-Powered Desalination Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres per Day of Installed Capacity)

- By Desalination Technology

- By Renewable Energy Source

- By System Size / Capacity

- By Feed Water Source

- By Component

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Renewable Energy-Powered Desalination Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres per Day of Installed Capacity)

- By Desalination Technology

- By Renewable Energy Source

- By System Size / Capacity

- By Feed Water Source

- By Component

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Renewable Energy-Powered Desalination Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Cubic Metres per Day of Installed Capacity)

- By Desalination Technology

- By Renewable Energy Source

- By System Size / Capacity

- By Feed Water Source

- By Component

- By End-Use Application

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Mexico, Spain, Italy, Portugal, Greece, Israel, Cyprus, Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain, Jordan, Egypt, Morocco, Algeria, Tunisia, Libya, India, China, Australia, Chile

- Technology Landscape & Innovation Analysis

- Solar PV-Powered Reverse Osmosis (PV-RO) Technology Deep-Dive

- Direct-Coupled PV-RO System Design: DC Pump Drive, Variable Flow Operation & Battery-Free Architecture for Off-Grid Brackish & Seawater Applications

- Grid-Connected & Hybrid PV-BESS-RO System Configuration: Inverter Selection, Battery Sizing, Energy Management Controller Design & Grid Interconnection for 24/7 Production

- Energy Recovery Device (ERD) Integration in Solar RO Systems: Pressure Exchanger, Turbocharger & Work Exchanger Selection for High-Recovery & Variable-Flow Operation

- Membrane Selection & Fouling Management for PV-RO: High-Flux Low-Energy RO Membrane Performance, Antiscalant Dosing Control & Intermittent Operation Membrane Protection Strategy

- Autonomous Control & Remote Monitoring for Off-Grid PV-RO Systems: PLC-Based Sequencing, IoT Sensor Integration, Remote SCADA & Predictive Maintenance Algorithms

- Wind Energy-Powered Desalination Technology

- CSP & Solar Thermal-Powered MED & MSF Desalination Technology

- Advanced Reverse Osmosis Membrane, Module & Energy Recovery Technology

- Emerging Desalination Technologies (Membrane Distillation, Forward Osmosis, CDI & HDH)

- Brine Management, Zero Liquid Discharge (ZLD) & Mineral Recovery Technology

- Digital Twin, AI Optimisation & Autonomous Operation Technology for RE-Desalination Plants

- Patent & IP Landscape in Renewable Energy-Powered Desalination

- Solar PV-Powered Reverse Osmosis (PV-RO) Technology Deep-Dive

- Value Chain & Supply Chain Analysis

- Membrane, High-Pressure Pump & Energy Recovery Device Manufacturing Supply Chain

- Renewable Energy Equipment (Solar PV, Wind Turbine, BESS & Inverter) Supply Chain

- Pre-Treatment Chemical, Antiscalant & Coagulant Supply Chain

- EPC Contractor, System Integrator & Project Developer Landscape

- Water Authority, Utility & Industrial End-User Procurement & Offtake Channel

- Operations & Maintenance (O&M), Performance Contract & WaaS Service Channel

- Brine Disposal, Mineral Recovery, Waste Treatment & Circular Water Economy

- Pricing Analysis

- Solar PV-Powered SWRO Levelised Cost of Water (LCOW) Analysis

- Wind-Powered Desalination LCOW Analysis

- CSP & Solar Thermal MED / MSF Desalination Cost Analysis

- Small-Scale & Off-Grid RE-Desalination System Capital & Operating Cost Analysis

- EPC Contract, BOT & WaaS Tariff Pricing Analysis by Region & Project Type

- RE-Desalination vs. Conventional Fossil-Powered Desalination LCOW Benchmark Comparison

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Renewable Energy-Powered vs. Conventional Fossil-Fuelled Desalination

- Carbon Footprint, GHG Emission Reduction & Net Zero Contribution of RE-Desalination

- Brine & Concentrate Disposal, Marine Ecosystem Impact & Coastal Environmental Management

- Water-Energy-Food Nexus: RE-Desalination Contribution to Climate Resilience & Water Security

- Regulatory-Driven Sustainability, Green Finance Eligibility & SDG 6 (Clean Water) Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Desalination Technology, RE Source & Geography

- Player Classification

- Integrated Water & Desalination Technology Companies with RE Capability

- Specialist Reverse Osmosis Membrane & System Manufacturers

- Thermal Desalination (MSF & MED) Technology & EPC Providers

- Renewable Energy Companies Integrating Desalination into Water Projects

- Independent Water & Power Producers (IWPPs) & Project Developers

- Emerging Technology Providers (Membrane Distillation, FO, CDI & HDH)

- Digital, AI & Remote Monitoring Platform Providers for Desalination

- EPC Contractors, System Integrators & O&M Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Desalination Technology, RE Source & Region

- Company Profile

- Company Overview & Headquarters

- RE-Desalination Products, Technology Portfolio & Project References

- Key Customer Relationships & Offtake Agreements

- Manufacturing Footprint & Production Capacity

- Revenue (Desalination Segment) & Project Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Desalination Technology, RE Source, System Capacity, Application & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)