Market Definition

The Global Smart Water Purifiers Market encompasses the design, manufacturing, distribution, and after-sale service of internet-connected, sensor-equipped, and digitally intelligent residential, commercial, and institutional water purification devices that integrate advanced filtration and purification technologies with real-time water quality monitoring, automated filter life management, remote diagnostics, mobile application connectivity, and data-driven performance optimisation capabilities that distinguish them from conventional non-connected water purification appliances. Smart water purifiers utilise a combination of purification technologies including reverse osmosis, ultrafiltration, ultraviolet disinfection, activated carbon adsorption, ion exchange softening, and multi-stage composite filter systems, enhanced by embedded sensors that continuously monitor source water turbidity, total dissolved solids, pH, temperature, residual chlorine, heavy metal indicators, and purified water quality parameters, transmitting these measurements to cloud-based analytics platforms and consumer-facing mobile applications that provide real-time water quality visibility, predictive filter replacement alerts, usage pattern analytics, and remote appliance diagnostics accessible to both end users and service providers. The market spans under-sink and countertop residential installations, wall-mounted commercial and institutional units serving offices, schools, hospitals, and hospitality facilities, and drinking water dispensing systems for workplace and public space applications, across purchase, subscription, and rental-with-service delivery models. The technology ecosystem includes the purification hardware device, embedded sensor arrays and microcontrollers, wireless connectivity modules, firmware and edge computing software, cloud data management and analytics platforms, consumer mobile applications, and the replacement filter consumables and service operations that constitute the lifecycle revenue model. Key participants include household appliance manufacturers with water purification product lines, dedicated water purifier specialists, filter technology and membrane developers, consumer electronics companies entering the connected appliance segment, direct-to-consumer subscription water service operators, and the retail, e-commerce, and direct sales channel networks through which smart water purifiers are distributed globally.

Market Insights

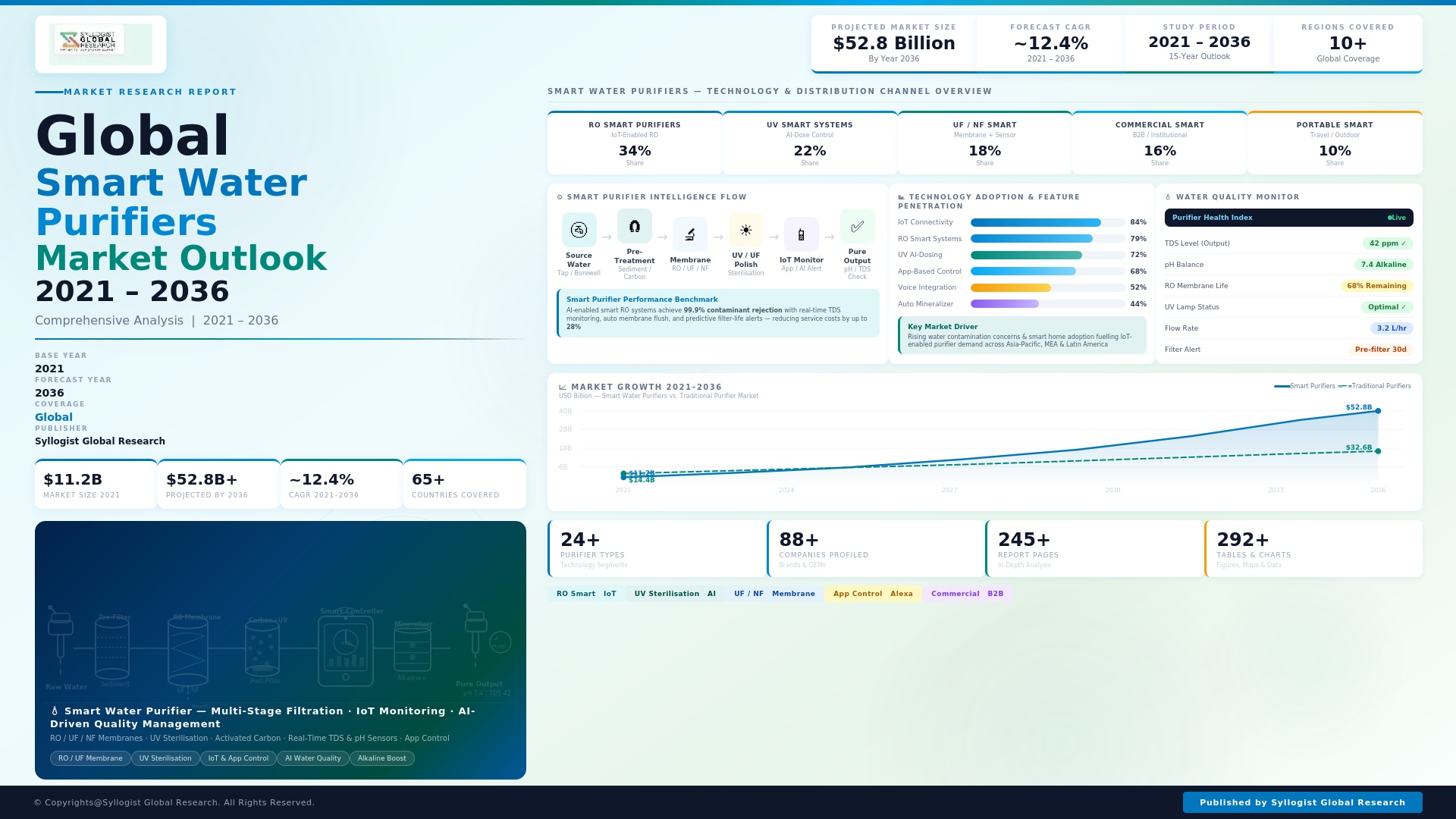

The global smart water purifiers market was valued at approximately USD 5.8 billion in 2025 and is projected to reach USD 16.3 billion by 2034, advancing at a compound annual growth rate of 12.2% over the forecast period from 2027 to 2034, driven by escalating consumer awareness of drinking water contamination risks, the growing adoption of smart home technology ecosystems that increase consumer receptiveness to connected water appliances, rising disposable incomes in rapidly urbanising Asia-Pacific and Middle Eastern markets, and the fundamental shift in water purifier purchasing behaviour from one-time capital equipment acquisition toward subscription and service models whose recurring revenue architecture is reshaping the competitive dynamics and lifetime value economics of the smart water purifier market. The market is experiencing a structural transition from hardware-centric sales models toward platform business models in which the purifier device serves as the primary access point for a recurring service relationship encompassing filter subscription, remote monitoring, quality certification, and water health analytics whose aggregate lifetime revenue substantially exceeds the initial device sale value and creates durable customer retention economics that conventional one-time appliance transactions cannot achieve.

Asia-Pacific dominates the global smart water purifiers market, accounting for approximately 54% of total market revenue in 2025, anchored by China and India whose combined population of approximately 2.8 billion people represents the world’s largest addressable market for residential water purification, with tap water safety concerns, high dissolved solids and heavy metal contamination prevalence in piped water supplies across large proportions of both countries driving strong household purifier adoption across income segments. China’s smart water purifier market reached approximately USD 1.8 billion in 2025, with smart and connected models constituting approximately 43% of total water purifier unit sales in the country as major domestic appliance manufacturers and specialist water treatment brands compete aggressively on connectivity features, water quality sensor capability, and mobile application user experience to differentiate premium-priced smart purifiers in a market where consumer digital sophistication and smart home ecosystem adoption are among the highest globally. India represents the fastest-growing national market within the region at approximately 15.4% annual growth, driven by the government’s Jal Jeevan Mission expanding piped water connections to rural households whose newly connected water supplies frequently carry elevated turbidity, microbiological, and chemical contamination loads that drive immediate residential purifier demand, combined with rising urban middle-class consumer health consciousness and the increasing availability of affordable smart purifier models at price points accessible to a broadening segment of urban Indian households.

The subscription and water-as-a-service delivery model is the most commercially disruptive and rapidly growing business model within the smart water purifier market, advancing at approximately 19.6% annually as consumers and commercial users increasingly prefer the convenience, predictability, and service assurance of monthly subscription plans that bundle device access, automated filter delivery, remote monitoring, and maintenance support into a single recurring payment that eliminates the friction of filter procurement and the uncertainty of do-it-yourself filter change compliance. Smart water purifier operators leveraging IoT connectivity data to predict individual household filter replacement timing based on actual water consumption volume and source water contamination load rather than calendar-based replacement schedules are extending average filter service life by 15% to 28% relative to conservative schedule-based replacement while simultaneously reducing the incidence of degraded purification performance from delayed filter changes that affect consumers managing their own replacement schedules without data guidance. The commercial and institutional segment, encompassing office buildings, hotels, hospitals, schools, and fitness facilities, is growing at approximately 14.3% annually and represents a disproportionately high revenue contribution per unit relative to the residential segment, as multi-person occupancy creates high flow volume requirements that justify premium large-capacity smart purification systems, the operational management value of remote monitoring and automated service scheduling is greatest in facilities where maintenance staff resources are limited, and the water quality liability of serving a large consumer population elevates the business case for certified real-time quality monitoring that smart purifiers provide relative to conventional unmonitored filter systems.

Water quality transparency and real-time contamination reporting capability are emerging as the most powerful consumer purchase decision drivers for smart water purifier premium pricing justification, with the ability of connected purifiers to report current source water quality parameters, purification performance efficiency, and cumulative contaminant removal volumes on consumer smartphone applications creating an evidence-based water safety narrative that resonates strongly with health-conscious consumers in markets where tap water safety uncertainty is a significant quality of life concern. The integration of smart water purifiers with broader smart home ecosystems including voice assistant platforms, home automation hubs, and health monitoring applications is creating cross-platform data integration opportunities that increase the stickiness of smart purifier platform subscriptions within established smart home technology users and are influencing purchasing decisions toward connected purifier brands whose application programming interfaces and data partnership programs align with consumers’ existing smart home platform investments. Per- and polyfluoroalkyl substance contamination awareness, following the United States Environmental Protection Agency’s establishment of maximum contaminant levels for six per- and polyfluoroalkyl substances in drinking water in 2024, is generating a significant new product development cycle in the smart water purifier market as manufacturers develop and certify activated carbon and reverse osmosis filter configurations specifically validated for per- and polyfluoroalkyl substance removal and integrate per- and polyfluoroalkyl substance removal certification claims into smart purifier marketing communication in the North American and European markets where consumer awareness of this contamination category is most acute.

Key Drivers

Rising Drinking Water Contamination Awareness, Heavy Metal and Emerging Contaminant Concerns, and Health-Conscious Consumer Behaviour Driving Premium Smart Purifier Adoption

The global expansion of media coverage, social media discussion, and public health authority communication regarding drinking water contamination risks encompassing lead and arsenic from ageing distribution infrastructure, nitrates and pesticides from agricultural runoff, per- and polyfluoroalkyl substances from industrial and military sources, microplastics from environmental pollution, disinfection byproducts from chlorination, and microbiological pathogens from distribution system failures is creating a sustained and growing consumer demand for verified home water purification solutions that provide measurable, reportable, and trustworthy protection against the specific contaminant categories most relevant to their local water supply context. Smart water purifiers whose embedded sensors and cloud-connected quality reporting capability provide consumers with real-time evidence of purification performance and source water contamination removal are commanding price premiums of 35% to 80% above equivalent non-connected purification systems in markets where consumer health consciousness and digital technology adoption are sufficiently advanced to value verifiable water safety over price minimisation alone. The United States Environmental Protection Agency maximum contaminant level regulations for per- and polyfluoroalkyl substances finalized in 2024 at levels of 4 parts per trillion for perfluorooctanoic acid and perfluorooctane sulfonate individually are generating acute consumer demand for point-of-use water purifiers certified for per- and polyfluoroalkyl substance removal in the approximately 45% of United States public water systems that were estimated to exceed at least one of these maximum contaminant levels before compliance-driven treatment upgrades were completed, providing a major near-term demand catalyst for smart purifiers with certified per- and polyfluoroalkyl substance removal capability in the North American residential market.

Smart Home Ecosystem Proliferation, Consumer IoT Platform Adoption, and Digital Health Monitoring Trends Creating Receptive Technology Adoption Environment for Connected Water Appliances

The global installed base of smart home devices exceeded 1.7 billion units in 2025 and is projected to surpass 3.4 billion units by 2034, creating an expanding population of digitally connected households whose consumers are increasingly accustomed to monitoring, controlling, and optimising home environment parameters through smartphone applications and voice-activated assistants, establishing the behavioural and technological foundations upon which smart water purifier adoption is built and from which connected water appliance purchases arise more naturally than in households without existing smart home platform investment. The integration of smart water purifiers with voice assistant platforms including Amazon Alexa, Google Home, and Apple HomeKit enables hands-free quality status enquiries, filter replacement ordering, and service request initiation that reduce the friction of purifier management and increase the daily interaction frequency between consumers and their purifier platform, reinforcing product satisfaction and reducing subscription cancellation rates by embedding the smart purifier into established daily smart home interaction routines. Consumer adoption of wearable health monitoring devices, nutrition tracking applications, and health data aggregation platforms is creating a population of health-data-engaged consumers whose interest in monitoring all dimensions of their health environment, including the quality of the water they consume, makes them structurally predisposed to adopting smart purifiers whose water quality and consumption data can be integrated with personal health monitoring dashboards, with smart purifier developers actively pursuing data integration partnerships with leading consumer health platforms to position their products within the broader personal health monitoring ecosystem rather than solely within the home appliance category.

Subscription Business Model Innovation, Filter-as-a-Service Convenience, and Direct-to-Consumer Digital Commerce Transforming Smart Purifier Market Economics and Customer Retention

The emergence of subscription-based smart water purifier business models that bundle device hardware, automated filter replenishment, remote performance monitoring, and maintenance services into affordable monthly plans is fundamentally transforming the purchase economics of premium water purification technology by converting what was historically a high-barrier capital equipment decision into a low-upfront-cost recurring service subscription whose monthly cost is comparable to the household expenditure on bottled water that smart purifiers are positioned to replace, dramatically expanding the addressable consumer population beyond the upper-income segments who could justify significant appliance capital expenditure. Subscription smart purifier operators accumulate detailed IoT consumption and quality data across their subscriber bases that enables them to predict individual household filter replacement timing based on measured throughput and contamination loading, reducing average filter material cost per household by 15% to 28% through optimised replacement scheduling while simultaneously achieving higher service satisfaction scores than conventional calendar-based replacement models whose fixed intervals do not reflect actual household consumption patterns or source water quality variation. The direct-to-consumer digital commerce capability of subscription smart purifier operators enables ongoing customer relationship management, personalised water quality reporting, targeted upsell of enhanced service tiers, and community engagement programs whose cumulative customer lifetime value generation substantially exceeds the economics available through conventional retail-sold appliance models, with leading subscription water purifier operators reporting average customer lifetime values of USD 1,800 to USD 3,200 per subscriber compared to USD 350 to USD 600 for equivalent non-subscription appliance transactions, creating a compelling business model differentiation that is driving competitive market entry from appliance manufacturers, consumer electronics brands, and venture-backed direct-to-consumer water service startups.

Key Challenges

High Device Cost and Subscription Price Sensitivity in Developing Market Consumer Segments Limiting Smart Purifier Penetration Beyond Upper-Middle-Income Households

Smart water purifiers incorporating advanced sensor arrays, wireless connectivity modules, cloud platform connectivity, and premium filtration technology carry retail prices of USD 180 to USD 850 for residential under-sink models in the mid-to-premium market segments, with subscription service plans adding monthly fees of USD 15 to USD 45 depending on filter replacement frequency and service tier, creating total annual water purification costs of USD 180 to USD 540 that represent a significant household budget commitment in the price-sensitive emerging market consumer segments of India, Southeast Asia, Africa, and Latin America where the health need for drinking water purification is often greatest but financial capacity to access premium smart purifier technology is most constrained. In India, where household water purifier penetration remains below 20% of total households despite severe drinking water quality challenges across large portions of the country, the pricing of smart connected purifier models positions them predominantly in urban upper-middle and affluent household segments, leaving the mass market of lower-middle-income urban and aspirational rural households served by lower-cost non-connected purifier models or, critically, by no purification at all, limiting the smart purifier market’s public health impact relative to its theoretical addressable market size. Competitive pressure from aggressively priced Chinese-manufactured non-connected purifier models that deliver comparable filtration performance without connectivity features at price points 40% to 60% below equivalent smart models constrains the premium pricing headroom available to smart purifier brands in price-sensitive market segments and requires ongoing product innovation and service value demonstration to maintain consumer justification for the smart connectivity premium.

Data Privacy Concerns, Consumer Trust Barriers to IoT Water Quality Data Sharing, and Cybersecurity Vulnerability of Connected Purifier Platforms

Smart water purifiers that continuously collect household water consumption patterns, usage timing, occupancy indicators, and health-relevant water quality data through cloud-connected platforms are generating increasing consumer privacy concerns as awareness of the behavioural and health inference capability of aggregated household IoT data grows among digital privacy-conscious consumer segments in North America, Europe, and advanced Asia-Pacific markets where privacy regulation and consumer advocacy attention to smart home data practices is most acute. The water quality and consumption data collected by smart purifier cloud platforms reveals sensitive household information including occupancy patterns, daily routines, potential health conditions suggested by drinking water consumption volume changes, and economic indicators reflected in filter replacement patterns, creating data privacy exposure that regulatory frameworks including the European Union General Data Protection Regulation, California Consumer Privacy Act, and equivalent national privacy laws impose data minimisation, consent, and purpose limitation requirements on smart purifier data practices that increase platform compliance complexity and restrict the secondary data monetisation opportunities that some smart purifier business model projections have incorporated. Cybersecurity vulnerabilities in smart purifier internet of things devices, including insecure firmware update mechanisms, unencrypted cloud data transmission, default password vulnerabilities, and insufficient device authentication protocols, expose connected purifier platforms to attack vectors whose exploitation could compromise consumer privacy, enable household occupancy surveillance, or in adversarial scenarios manipulate purifier performance monitoring to generate false quality assurance signals, creating reputational and liability risks for smart purifier brands whose inadequate cybersecurity practices are exposed by security researchers or regulatory investigations.

Filter Technology Complexity, Multi-Contaminant Performance Validation, and Regulatory Certification Burden Increasing Product Development Cost and Market Entry Timelines

Smart water purifiers must simultaneously satisfy the filtration performance requirements for the highly diverse and regionally variable contaminant profiles present in drinking water supplies across global markets, requiring product development programs that validate purification performance against local water quality conditions, emerging contaminant categories, and national drinking water standard frameworks whose specific requirements vary substantially across the United States, European Union, China, India, and other major regulatory jurisdictions, imposing product certification investment and timeline requirements that are disproportionately burdensome for smaller smart purifier developers and new market entrants. The United States National Sanitation Foundation and American National Standards Institute certification program for drinking water treatment units, the European Union Construction Products Regulation framework for materials in contact with drinking water, the Chinese GB drinking water quality standard for water treatment equipment, and the Bureau of Indian Standards certification requirements each impose distinct test protocols, contaminant removal performance thresholds, and materials safety requirements that require separate certification programs whose aggregate cost across major global markets can reach USD 800,000 to USD 2.5 million per product model, creating a significant market entry barrier that favours established appliance manufacturers with existing certification infrastructure and regulatory compliance programs over new entrant smart technology companies seeking to develop connected purifier products. The accelerating pace of emerging contaminant regulation, including the addition of new per- and polyfluoroalkyl substance variants, microplastics, pharmaceutical residues, and disinfection byproducts to national drinking water monitoring frameworks, requires smart purifier manufacturers to continuously invest in filter technology upgrades and performance certification renewal programs whose cost and timeline impose ongoing product development obligations that constrain the pace of smart connectivity and platform feature investment available within finite product development budgets.

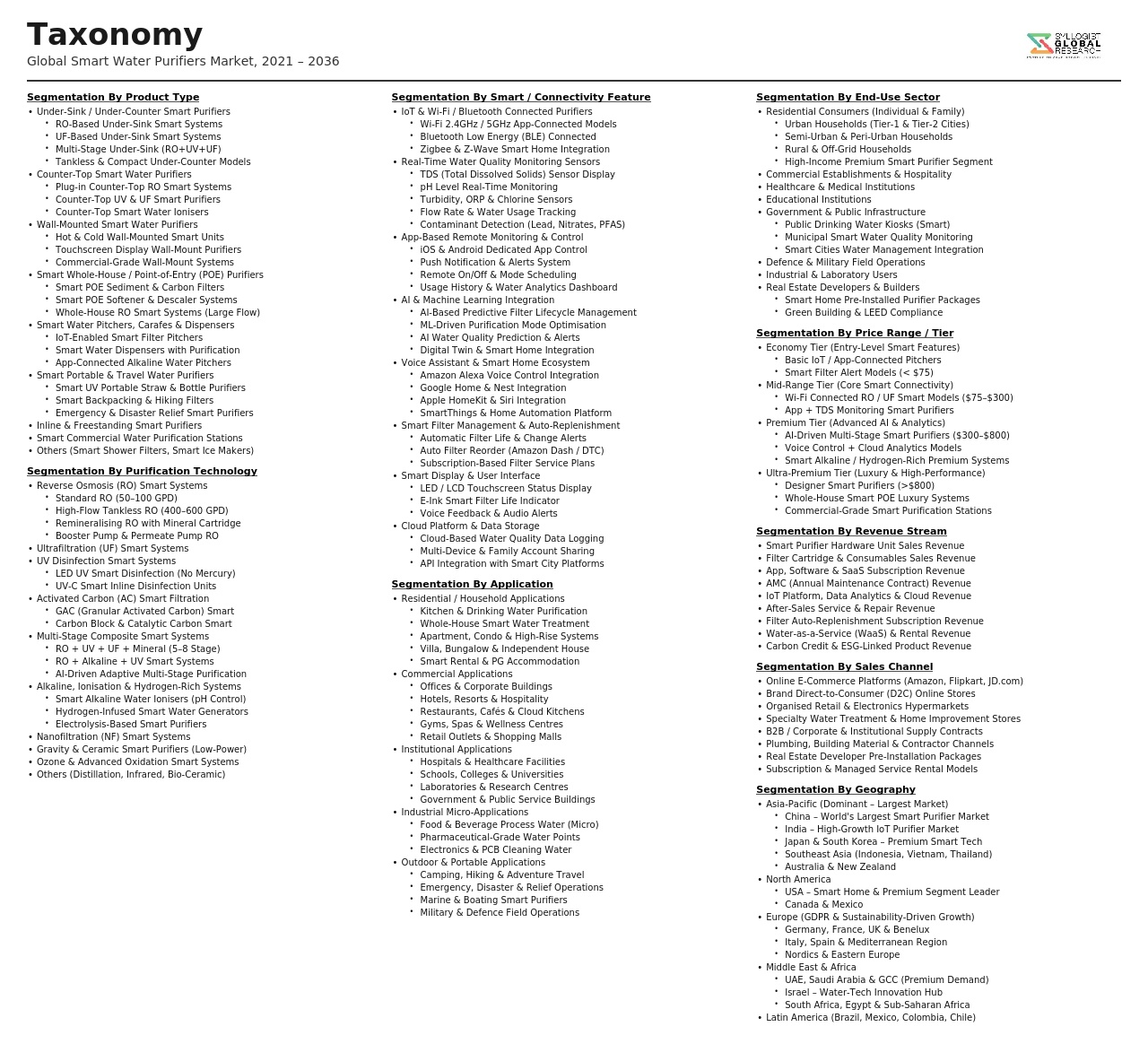

Market Segmentation

- Segmentation By Purification Technology

- Reverse Osmosis (RO) Based Smart Purifiers

- Ultrafiltration (UF) Based Smart Purifiers

- Ultraviolet (UV) Disinfection Smart Purifiers

- Activated Carbon and Adsorption-Based Smart Purifiers

- Multi-Stage Composite (RO Plus UV Plus UF) Smart Purifiers

- Ion Exchange and Water Softening Smart Systems

- Others

- Segmentation By Installation Type

- Under-Sink Residential Smart Purifiers

- Countertop Residential Smart Purifiers

- Wall-Mounted Residential and Light Commercial Purifiers

- Inline Smart Filtration Systems

- Commercial and Institutional Drinking Water Dispensers

- Whole-House Smart Water Filtration Systems

- Others

- Segmentation By Connectivity and Smart Feature

- Wi-Fi and App-Connected Smart Purifiers

- Bluetooth-Connected Smart Purifiers

- Voice Assistant Integrated Purifiers (Alexa, Google, and Siri)

- AI-Enabled Water Quality Analytics Platforms

- Real-Time TDS, pH, and Contaminant Monitoring Purifiers

- Predictive Filter Life and Auto-Replenishment Purifiers

- Segmentation By Business Model

- Outright Purchase and Ownership

- Monthly Subscription with Filter-as-a-Service

- Rental with Maintenance and Replacement Included

- Direct-to-Consumer Digital Commerce Subscription

- B2B Commercial Water-as-a-Service Managed Programs

- Segmentation By End-User Segment

- Residential Households

- Corporate Offices and Workplaces

- Hotels and Hospitality Facilities

- Hospitals and Healthcare Institutions

- Educational Institutions

- Retail and Food Service Establishments

- Fitness and Wellness Centres

- Others

- Segmentation By Contaminant Target

- Heavy Metals (Lead, Arsenic, and Mercury) Removal

- Microbiological Purification (Bacteria, Viruses, and Cysts)

- Total Dissolved Solids and Mineral Reduction

- PFAS and Emerging Organic Contaminant Removal

- Chlorine, Chloramines, and Disinfection Byproduct Reduction

- Nitrates and Agricultural Chemical Removal

- Microplastics Filtration

- Multi-Contaminant Comprehensive Purification

- Segmentation By Sales Channel

- Direct-to-Consumer Digital and E-Commerce

- Specialty Water Treatment Retail

- Consumer Electronics and Home Appliance Retail

- Home Improvement and Hardware Retail

- Professional Installation and Trade Channel

- Direct Sales Force and Dealer Network

- Segmentation By Region

- Asia-Pacific (China, India, South Korea, Japan, and Others)

- North America (United States and Canada)

- Europe (European Union and United Kingdom)

- Middle East and Africa

- Latin America (Brazil, Mexico, and Others)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Smart Water Purifiers Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by purification technology, reverse osmosis, ultrafiltration, ultraviolet, and multi-stage composite, by installation type, residential under-sink, countertop, and commercial, by business model, device purchase and subscription service, and by geography, to enable purifier manufacturers, subscription service operators, filter technology developers, investors, and retail channel partners to identify which product categories, business models, and regional markets will generate the highest absolute revenue and most commercially significant growth momentum across the forecast period?

- How is the subscription and water-as-a-service business model expected to reshape the competitive landscape, customer lifetime value economics, and market share distribution of the smart water purifiers market through 2034, what are the documented customer acquisition cost, monthly churn rate, and lifetime value benchmarks of leading subscription smart purifier operators, which consumer segments and geographic markets are generating the highest subscription adoption rates, and how are established appliance manufacturers and retail-channel-dependent smart purifier brands structurally adapting their business models to compete with direct-to-consumer subscription operators whose recurring revenue architecture and IoT data advantages create compounding competitive differentiation over time?

- What is the projected impact of the United States Environmental Protection Agency per- and polyfluoroalkyl substance maximum contaminant level regulations, the European Union Drinking Water Directive recast, and equivalent national emerging contaminant regulatory frameworks in China, India, and Australia on smart water purifier product development priorities, filter certification investment requirements, and consumer demand trajectory through 2034, which smart purifier technology configurations, activated carbon, reverse osmosis, and combination treatment, are most effectively certified for per- and polyfluoroalkyl substance and emerging contaminant removal, and how are these regulatory developments reshaping market share dynamics between premium smart purifiers with certified contaminant removal capability and lower-cost non-certified alternatives?

- How are smart home ecosystem integration, voice assistant platform connectivity, personal health monitoring data partnerships, and artificial intelligence-driven water quality personalisation features expected to evolve as smart water purifier product differentiators through 2034, which technology platform partnerships and data integration capabilities are generating the highest consumer satisfaction and subscription retention outcomes at currently operating smart purifier platforms, and how are leading smart purifier developers investing in proprietary platform capability versus ecosystem partnership strategies to build durable competitive positions within the connected home and personal health monitoring landscape?

- Who are the leading smart water purifier manufacturers, subscription water service operators, filter technology and membrane developers, and connected appliance platform companies currently defining the competitive landscape of the global smart water purifiers market, and what are their respective product portfolio coverage across purification technologies and smart connectivity capabilities, geographic market presence and distribution channel strategies, subscription business model development and customer lifecycle economics, research and development investment in emerging contaminant filter certification and artificial intelligence-based water quality analytics, and competitive positioning responses to the pricing accessibility, data privacy, and filter certification challenges constraining smart water purifier market penetration across price-sensitive and regulatory-complex market environments globally?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Cybersecurity, Data Privacy & IoT Network Vulnerability Risk in Connected Purifier Ecosystems

- Contaminant Detection Accuracy, Sensor Reliability & Product Performance Liability Risk

- Regulatory Compliance, Drinking Water Safety Certification & Market Access Risk

- Consumer Trust, Health Claim Substantiation & Product Recall Risk

- Supply Chain Disruption, Component Shortage & Filter Media Sourcing Risk

- Regulatory Framework & Standards

- Drinking Water Quality Standards & Point-of-Use Purifier Certification Frameworks (NSF/ANSI, WHO, BIS & Regional Standards)

- IoT Device Security, Consumer Electronics & Smart Home Product Safety Regulations

- Environmental Regulations on Plastic Waste, Filter Cartridge Disposal & Product Take-Back Schemes

- Health Claim Labelling, Advertising Standards & Consumer Protection Regulations for Water Purifiers

- Energy Efficiency, Eco-Design & Smart Appliance Connectivity Standards

- Global Smart Water Purifier Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Product Type

- Smart Reverse Osmosis (RO) Purifiers

- Smart Ultrafiltration (UF) Purifiers

- Smart Activated Carbon & Multi-Stage Filter Purifiers

- Smart UV Disinfection Purifiers

- Smart Gravity-Fed & Non-Electric Purifiers with IoT Monitoring

- Smart Alkaline & Mineral Enhancement Purifiers

- Smart Under-Sink & Countertop Purifier Systems

- Smart Whole-House & Point-of-Entry Purification Systems

- Market Size & Forecast by Technology

- Reverse Osmosis (RO) Membrane Technology

- Ultrafiltration (UF) & Nanofiltration (NF) Membrane Technology

- Ultraviolet (UV) Disinfection Technology

- Activated Carbon & Adsorption Filtration Technology

- Electrodeionisation (EDI) & Ion Exchange Technology

- Multi-Stage Hybrid Filtration Technology

- Real-Time Water Quality Sensing & AI-Driven Filtration Adjustment Technology

- Market Size & Forecast by Connectivity

- Wi-Fi Connected

- Bluetooth Connected

- Zigbee & Z-Wave (Smart Home Protocol) Connected

- Cellular (4G/5G) Connected

- Voice Assistant & Smart Home Ecosystem Integrated (Alexa, Google Home)

- Market Size & Forecast by Smart Feature

- Real-Time Water Quality Monitoring & TDS Display

- Filter Life Monitoring & Auto-Reorder Capability

- Mobile App Control, Remote Diagnostics & Usage Analytics

- AI-Driven Adaptive Filtration & Contaminant-Specific Purification

- Leak Detection & Auto Shut-Off

- Voice Control & Smart Home Integration

- Market Size & Forecast by Application

- Residential (Single-Family Homes & Apartments)

- Commercial (Offices, Hotels, Restaurants & Retail)

- Institutional (Schools, Hospitals & Government Buildings)

- Industrial & Light Manufacturing

- Market Size & Forecast by End-User

- Individual Consumers & Households

- Corporate & Commercial Facility Managers

- Healthcare & Institutional Facility Operators

- Hospitality & Food Service Operators

- Market Size & Forecast by Distribution Channel

- Online Retail (Brand Website, E-Commerce Marketplaces & D2C)

- Offline Retail (Hypermarkets, Electronics & Home Appliance Stores)

- Dealer, Distributor & Franchise Service Network

- Subscription & Filter Replacement Service Model

- B2B Direct Sales & Project Supply Channel

- North America Smart Water Purifier Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Product Type

- By Technology

- By Connectivity

- By Application

- By Distribution Channel

- By End-User

- By Country

- Market Size & Forecast

- Europe Smart Water Purifier Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Product Type

- By Technology

- By Connectivity

- By Application

- By Distribution Channel

- By End-User

- By Country

- Market Size & Forecast

- Asia-Pacific Smart Water Purifier Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Product Type

- By Technology

- By Connectivity

- By Application

- By Distribution Channel

- By End-User

- By Country

- Market Size & Forecast

- Latin America Smart Water Purifier Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Product Type

- By Technology

- By Connectivity

- By Application

- By Distribution Channel

- By End-User

- By Country

- Market Size & Forecast

- Middle East & Africa Smart Water Purifier Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Product Type

- By Technology

- By Connectivity

- By Application

- By Distribution Channel

- By End-User

- By Country

- Market Size & Forecast

- Country-Wise* Smart Water Purifier Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Product Type

- By Technology

- By Connectivity

- By Application

- By Distribution Channel

- By End-User

- By Country

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Smart RO Membrane Technology: Low-Energy Membranes, Permeate Recovery & AI-Driven Pressure Optimisation

- Real-Time Water Quality Sensor Technology: TDS, pH, ORP, Turbidity & Multi-Parameter Detection in Consumer Purifiers

- AI & Machine Learning-Based Adaptive Filtration, Contaminant Profiling & Predictive Maintenance Technology

- IoT Platform, Cloud Connectivity & Mobile App Ecosystem Architecture for Smart Purifiers

- UV-LED & Advanced Disinfection Technology Integration in Smart Point-of-Use Purifiers

- Filter Cartridge Innovation: Long-Life Media, Biodegradable Materials & Subscription-Enabled Smart Cartridge Technology

- Voice Control, Smart Home Integration & Multi-Device Ecosystem Compatibility Technology

- Patent & IP Landscape in Smart Water Purifier Technologies

- Value Chain & Supply Chain Analysis

- Membrane Module, Filter Cartridge & Purification Media Manufacturing Supply Chain

- IoT Sensor, PCB, Connectivity Module & Smart Electronics Component Supply Chain

- Housing, Plastics, Moulded Components & Assembly Manufacturing Supply Chain

- Cloud Platform, Mobile App & Software Development Supply Chain

- Brand Owner, OEM & ODM Manufacturing & Product Development Channel

- Distributor, Dealer, Franchise Service & Retail Channel

- After-Sales Service, Filter Replacement Subscription & Customer Retention Channel

- Pricing Analysis

- Smart Water Purifier Unit Retail Price Analysis by Product Type & Feature Tier

- Filter Cartridge Replacement Cost, Subscription Pricing & Lifetime Consumable Expenditure Analysis

- Installation, Annual Maintenance Contract (AMC) & After-Sales Service Pricing Analysis

- Smart Purifier Subscription & Device-as-a-Service (DaaS) Pricing Model Analysis

- Total Cost of Ownership (TCO) Analysis: Smart vs. Conventional Water Purifier

- Premium vs. Mid-Range vs. Entry-Level Smart Purifier Price Band & Feature Differentiation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Smart Water Purifiers: Carbon Footprint, Plastic Waste, Energy Use & Filter Cartridge Disposal

- Water Efficiency, Wastewater Rejection Reduction & Responsible Water Use in Smart RO Purifier Design

- Biodegradable & Recyclable Filter Cartridge Innovation & Extended Producer Responsibility (EPR) Compliance

- Health Impact, Waterborne Disease Prevention & Safe Drinking Water Access Contribution of Smart Purifiers

- Regulatory-Driven Sustainability, SDG 6 (Clean Water & Sanitation) Alignment & Eco-Label Certification Standards

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type, Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Technology & Geography

- Player Classification

- Established Water Purifier OEMs with Smart Product Lines

- Consumer Electronics & Smart Home Appliance Companies Entering Water Purification

- Pure-Play Smart Water Purifier & Connected Health Appliance Start-ups

- IoT Platform & Software Companies Providing Smart Purifier Ecosystems

- Filter Cartridge & Consumable Subscription Service Providers

- Private Label, ODM & OEM Manufacturers Supplying Smart Purifier Brands

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Smart Water Purifier Products & Technology Portfolio

- Key Retail, E-Commerce & Distribution Partnerships

- Manufacturing Footprint & Production Capacity

- Revenue (Smart Water Purifier Segment) & Units Sold

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Retail Expansion, Funding)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Technology, Connectivity, Application & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output