Market Definition

The Global Water Reuse and Recycling Technologies Market encompasses the engineering, manufacturing, deployment, operation, and maintenance of treatment systems, process equipment, membranes, chemicals, sensors, and digital management platforms that enable the collection, purification, and beneficial reuse of municipal wastewater, industrial process water, agricultural drainage, stormwater, and produced water streams that would otherwise be discharged or lost to the environment. Water reuse encompasses the treatment of wastewater effluent to standards sufficient for non-potable applications including agricultural and landscape irrigation, industrial cooling and process water supply, groundwater recharge, environmental flow augmentation, and potable reuse applications ranging from indirect potable reuse through managed aquifer recharge and reservoir augmentation to direct potable reuse systems that treat reclaimed water to drinking water quality standards for direct introduction into potable water distribution networks. The market spans the complete technology value chain from preliminary and primary treatment systems through secondary biological treatment, tertiary treatment including filtration and disinfection, advanced treatment comprising membrane filtration, reverse osmosis, advanced oxidation, and ion exchange processes, and the monitoring, control, and digital management systems that ensure treated water quality compliance across all intended reuse applications. Technologies encompassed include membrane bioreactors, ultrafiltration and microfiltration systems, reverse osmosis systems, ultraviolet and ozone disinfection equipment, electrochemical treatment systems, biological nutrient removal systems, constructed wetlands and nature-based treatment systems, advanced oxidation process equipment, ion exchange and adsorption systems, and the supervisory control and data acquisition, remote monitoring, and artificial intelligence-based process optimisation platforms that manage multi-stage reuse treatment trains. Key participants include water treatment equipment manufacturers, membrane technology developers, specialty chemical suppliers, engineering procurement and construction contractors, water utility operators, industrial water management companies, digital water technology providers, and the municipal and industrial water users whose water scarcity exposure, regulatory compliance obligations, and operational water efficiency imperatives define the demand structure of the global water reuse and recycling technologies market.

Market Insights

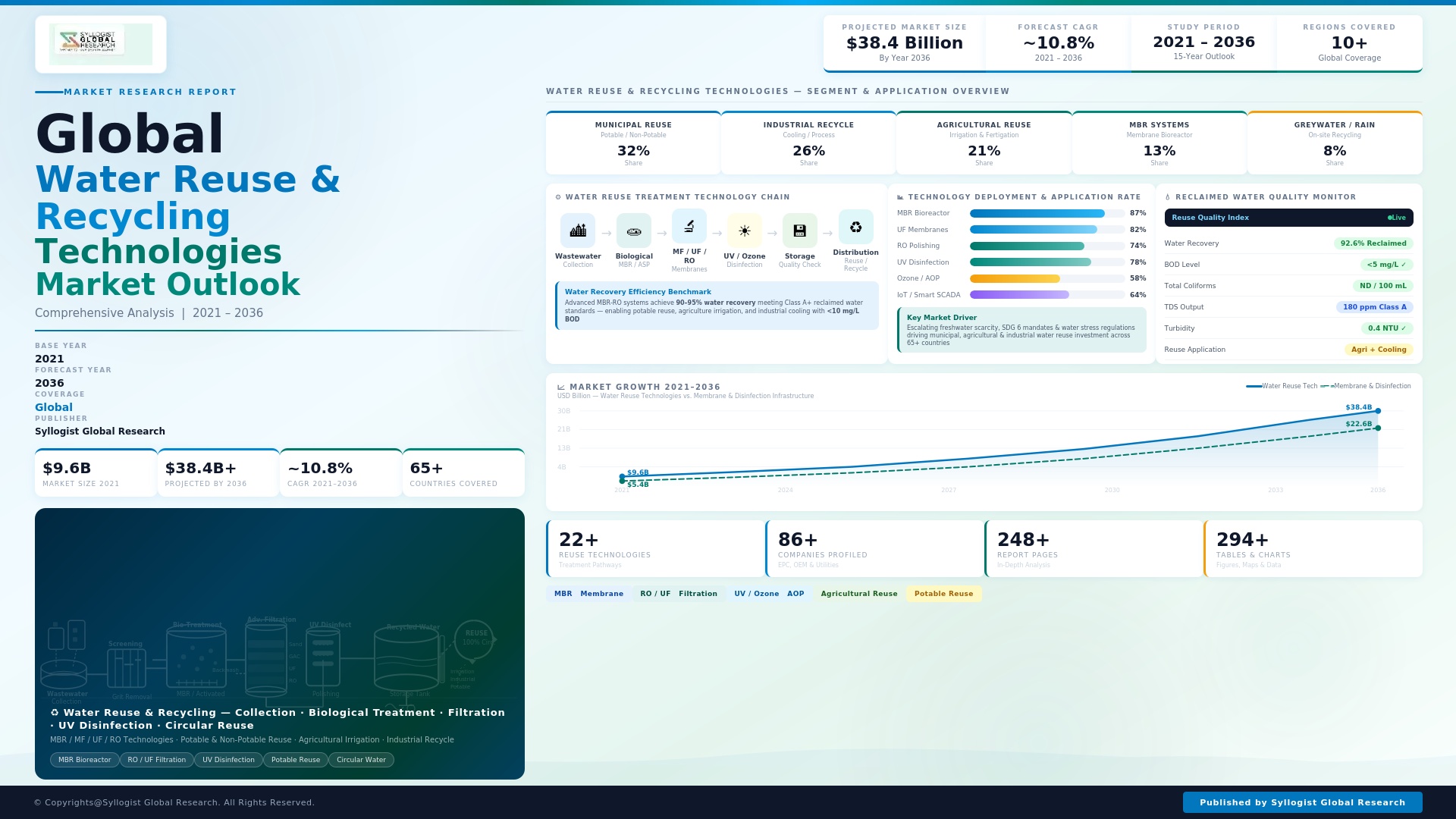

The global water reuse and recycling technologies market was valued at approximately USD 18.7 billion in 2025 and is projected to reach USD 36.4 billion by 2034, advancing at a compound annual growth rate of 7.6% over the forecast period from 2027 to 2034, driven by the accelerating convergence of physical water scarcity across major agricultural, industrial, and urban water-consuming regions, progressively more stringent wastewater discharge and water quality regulations globally, and the increasing economic competitiveness of advanced water recycling technologies whose capital and operating costs have declined materially as membrane and digital technology scale economies have improved. Approximately 2.3 billion people globally live in water-stressed countries as of 2025, and the proportion of the world’s population experiencing severe water scarcity for at least one month per year has reached approximately 3.6 billion, establishing a structural and growing demand foundation for water reuse infrastructure investment that is increasingly treated as a critical component of national water security strategy in arid and semi-arid regions including the Middle East, North Africa, Southern Europe, western United States, India, and Australia.

Municipal wastewater reclamation and potable reuse represent the fastest-evolving and most strategically significant application segments within the global water reuse market, with the number of advanced water recycling facilities producing reclaimed water for indirect or direct potable reuse applications growing at approximately 9.4% annually as water utilities in water-scarce regions exhaust conventional supply augmentation options and turn to purified recycled water as the only drought-proof locally available water resource capable of closing the gap between projected supply and demand at urban water system planning horizons extending to 2050. Singapore’s NEWater program, which supplies approximately 40% of the country’s water demand from reclaimed water produced by a system of membrane bioreactor, microfiltration, reverse osmosis, and ultraviolet disinfection treatment trains, represents the global benchmark for advanced water reclamation at national scale and has served as the technical and institutional reference model for advanced water reuse programs being implemented in Israel, Australia, Namibia, the United States, and an expanding group of Middle Eastern nations. Industrial water recycling is simultaneously generating substantial technology deployment demand across semiconductor manufacturing, power generation, food and beverage processing, pharmaceutical manufacturing, mining, and oil and gas production sectors where zero liquid discharge systems, high-recovery reverse osmosis, and closed-loop cooling water recycling programs are being implemented to reduce freshwater abstraction, achieve wastewater discharge permit compliance, and manage the operational risk of water supply interruption at production facilities located in water-constrained regions.

The Middle East and North Africa region represents the world’s most water-stressed geography and the most advanced national policy environment for mandated water reuse, with Israel reusing approximately 90% of its treated municipal wastewater for agricultural irrigation, making it the global leader in municipal water reuse intensity by proportion of treated effluent reused, while Saudi Arabia, the United Arab Emirates, Kuwait, and Qatar are operating large-scale water reclamation programs and have established regulatory frameworks requiring progressive increases in the proportion of treated wastewater reused rather than discharged. The region’s water reuse technology investment is driven by the combination of virtually zero natural freshwater replenishment from rainfall in Gulf Cooperation Council states, rapidly growing urban and industrial water demand, and the strategic imperative to reduce the proportion of desalinated water in national water supply portfolios by substituting reclaimed water for non-potable applications including landscape irrigation, industrial cooling, and construction water supply, freeing desalination capacity for potable supply. Asia-Pacific is the fastest-growing regional market for water reuse technology by absolute investment volume, with China having invested approximately USD 4.8 billion in water reclamation infrastructure between 2021 and 2025 under successive Five Year Plan targets for urban wastewater reuse rate improvement, and India implementing national water recycling programs under the National Water Mission and Smart Cities Mission that are generating substantial membrane bioreactor, tertiary treatment, and reclaimed water distribution network procurement across metropolitan wastewater utilities.

Digital water technology integration is transforming the operational economics and reliability assurance of water reuse systems, with artificial intelligence-based process optimisation platforms, real-time online water quality monitoring systems, predictive membrane fouling management algorithms, and digital twin-based treatment plant simulation tools collectively reducing the energy consumption, chemical dosing costs, and membrane replacement frequency of advanced water reuse systems in ways that are materially improving the lifecycle economics of water recycling investment relative to the operating cost benchmarks established by first-generation advanced treatment facilities. Energy consumption represents approximately 30% to 50% of the operating cost of advanced water reuse systems incorporating reverse osmosis treatment, with energy recovery devices and artificial intelligence-based pump and pressure management systems reducing the specific energy consumption of reverse osmosis water reclamation systems from historical benchmarks of 1.2 to 1.8 kilowatt hours per cubic metre toward 0.8 to 1.1 kilowatt hours per cubic metre at best-practice facilities, generating operating cost savings that are accelerating the payback period and improving the lifecycle cost competitiveness of advanced water reuse systems relative to alternative water supply options including desalination and interbasin transfer. Nature-based water treatment solutions including constructed wetlands, soil aquifer treatment, riverbank filtration, and managed aquifer recharge systems are gaining commercial momentum as complementary and cost-effective components of integrated water reuse schemes, particularly for agricultural and environmental reuse applications where treatment costs are constrained by the low economic value of the end use, with the global constructed wetland water treatment market growing at approximately 8.9% annually as developing nation water utilities and agricultural sector reuse programs adopt low-energy biological treatment approaches that deliver acceptable water quality at substantially lower capital and operating costs than energy-intensive membrane-based treatment alternatives.

Key Drivers

Escalating Physical Water Scarcity, Aquifer Depletion, and Climate-Driven Drought Frequency Creating Structural and Urgent Demand for Water Reuse Infrastructure

The convergence of population growth, urbanisation, agricultural intensification, and climate change-driven precipitation pattern disruption is creating a structural water supply deficit across an expanding proportion of the global population whose severity and geographic reach are compelling governments, water utilities, and industrial water users to invest in water reuse infrastructure as a fundamental water security measure rather than a supplementary supply source of last resort. Groundwater aquifers supplying approximately 2 billion people globally are being depleted at rates that exceed natural recharge, with the Central Valley aquifer in California, the High Plains Ogallala aquifer in the central United States, the North China Plain aquifer, and the Indo-Gangetic aquifer in South Asia all experiencing unsustainable extraction rates that are progressively reducing the reliable yield available to agricultural and municipal users dependent on these systems. The frequency and severity of multi-year droughts affecting previously water-secure regions including southern Europe, southeastern Australia, South Africa, and the American Southwest are demonstrating that historical surface water supply reliability assumptions embedded in water infrastructure planning are no longer valid under contemporary climate conditions, compelling water planners to invest in drought-independent supply sources of which advanced water recycling is the most locally available, energy-efficient, and volumetrically reliable option for most water-stressed urban and agricultural regions. Global municipal water demand is projected to increase by approximately 55% between 2025 and 2050 driven by urban population growth and rising per-capita service levels in developing nations, creating a supply gap whose closure through water reuse is estimated to require cumulative global investment in water reclamation infrastructure of approximately USD 480 billion through 2040 under conservative scenario projections.

Tightening Wastewater Discharge Regulations, Nutrient Pollution Controls, and Industrial Zero Liquid Discharge Requirements Compelling Treatment Upgrade Investment

Regulatory escalation in wastewater discharge standards across the European Union, United States, China, India, and other major economies is compelling municipal wastewater utilities and industrial water users to invest in advanced treatment upgrades whose technology specifications are increasingly compatible with water reuse applications, creating a dual compliance and resource recovery justification for water recycling technology investment that improves the business case economics relative to treatment upgrades designed purely for discharge compliance without beneficial reuse of the treated effluent. The European Union Urban Wastewater Treatment Directive recast, adopted in 2024 and requiring implementation by member states through 2033, establishes new nutrient removal, micropollutant elimination, and energy recovery requirements for wastewater treatment plants serving populations above 10,000 persons equivalent that will require advanced tertiary treatment installations at hundreds of facilities across Europe, with the technical specifications of the required tertiary treatment systems creating treated effluent quality that is directly compatible with non-potable reuse applications including agricultural irrigation and groundwater recharge. Industrial zero liquid discharge requirements, driven by the combination of freshwater scarcity in water-constrained manufacturing regions, wastewater discharge permit restrictions in environmentally sensitive receiving water bodies, and the increasing economic value of water recovery from high-concentration industrial effluent streams, are generating investment in high-recovery reverse osmosis, brine concentration, and evaporative crystallisation systems that eliminate wastewater discharge while recovering water for process reuse, with the zero liquid discharge system market growing at approximately 10.2% annually as semiconductor, pharmaceutical, textile, and mining industry operators implement closed-loop water management programs.

Declining Advanced Treatment Technology Costs, Membrane Performance Improvement, and Digital Water Management Maturation Improving Water Reuse Economic Competitiveness

The progressive decline in capital and operating costs of membrane filtration and reverse osmosis technology, driven by manufacturing scale economies, polymer chemistry innovation, and energy recovery device improvement, combined with the maturation of digital water management platforms that optimise treatment process performance in real time, is systematically improving the lifecycle cost competitiveness of advanced water reuse systems relative to conventional water supply alternatives across a widening range of geographic and application contexts. Reverse osmosis membrane element costs have declined by approximately 65% since 2000 in real terms, while membrane flux performance has improved by approximately 40% over the same period, collectively reducing the capital cost of membrane-based water recycling systems by approximately 35% to 45% relative to first-generation installations and enabling advanced water reuse to achieve cost competitiveness with desalination in most coastal water-stressed regions and with long-distance water transfer infrastructure in an expanding range of inland applications. The deployment of artificial intelligence and machine learning optimisation systems across advanced water reuse facilities is generating documented reductions in energy consumption of 8% to 18%, chemical dosing costs of 12% to 22%, and unplanned membrane replacement events of 25% to 35% relative to conventionally operated treatment facilities, improving operating cost economics and system reliability in ways that materially strengthen the investment case for water reuse infrastructure deployment across municipal and industrial water management programs globally.

Key Challenges

Public Perception Barriers, Regulatory Acceptance Complexity, and Potable Reuse Social Licence Constraints Limiting Advanced Water Recycling Program Deployment

The implementation of advanced municipal water reuse programs, particularly those involving indirect or direct potable reuse applications where reclaimed water re-enters drinking water supply systems, faces persistent public acceptance challenges rooted in psychological aversion to the concept of consuming treated wastewater regardless of the demonstrably superior water quality of advanced purified recycled water relative to conventionally treated drinking water supplies in most utility systems. The colloquial characterisation of potable water reuse as toilet-to-tap, which misrepresents the multi-barrier advanced treatment processes and extensive water quality monitoring systems that govern modern water recycling programs, has been used effectively by opponents of water reuse schemes in public consultation processes across the United States, Australia, and Europe to generate community opposition that has delayed or cancelled economically justified and technically sound water recycling projects in several water-stressed jurisdictions. Regulatory frameworks governing potable reuse remain inconsistent across jurisdictions, with some states and nations having established clear water quality criteria, treatment specification requirements, and public health monitoring frameworks for indirect and direct potable reuse while others maintain regulatory gaps or prohibitions that prevent water utilities from implementing advanced recycling programs whose technical safety has been established by decades of operating experience at reference facilities globally, creating a fragmented regulatory landscape that increases project development cost and risk and requires water utilities to invest substantially in regulatory engagement and public consultation processes whose duration and outcome are uncertain.

Energy Intensity of Advanced Treatment Processes, Carbon Footprint Concerns, and Operational Cost Barriers to Water Reuse System Deployment in Cost-Sensitive Markets

Advanced water reuse systems incorporating reverse osmosis treatment are energy-intensive relative to conventional water treatment processes, with the specific energy consumption of membrane-based water recycling systems ranging from 0.8 to 2.5 kilowatt hours per cubic metre of reclaimed water produced depending on feedwater quality, recovery ratio, and system design, creating operational cost and carbon footprint challenges in contexts where electricity costs are high, carbon pricing mechanisms apply, or energy reliability is limited, constraining the economic competitiveness of advanced water reuse relative to lower-energy conventional treatment and direct discharge options in jurisdictions where freshwater scarcity costs are not fully reflected in water pricing structures. In developing nation urban water utilities where tariff revenue is insufficient to recover the full operating cost of existing conventional wastewater treatment infrastructure, the incremental energy and chemical costs associated with advanced treatment upgrade for water reuse represent an affordability barrier whose financing requires external grant funding, concessional loan support from multilateral development banks, or private sector partnership models that introduce transaction cost and complexity into project development that are not required for simpler conventional treatment infrastructure investment. The carbon footprint of energy-intensive water recycling operations is becoming an increasingly prominent consideration for water utilities and industrial water users with corporate climate commitments and scope two greenhouse gas emission reduction targets, requiring investment in renewable energy supply, energy recovery optimisation, and low-energy treatment alternatives including biological treatment, constructed wetlands, and solar-driven desalination that may not always achieve the water quality specifications required for intended reuse applications.

Emerging Contaminant Complexity, Micropollutant Removal Requirements, and Evolving Analytical Detection Capability Increasing Treatment System Specification Demands

The increasing analytical detection capability for trace chemical contaminants in water at concentration levels below one microgram per litre, combined with growing scientific understanding of the potential chronic health effects of low-concentration exposure to pharmaceuticals, endocrine-disrupting compounds, per- and polyfluoroalkyl substances, microplastics, and disinfection by-products in recycled water, is continuously expanding the list of contaminants of concern that water reuse treatment systems must demonstrably remove to concentrations below health-based guideline values, driving treatment system specification requirements toward increasingly complex multi-barrier advanced treatment trains whose capital and operating costs exceed those of the simpler treatment configurations that were technically adequate under earlier, less comprehensive water quality frameworks. Per- and polyfluoroalkyl substances have emerged as a particularly significant water reuse treatment challenge since 2020, as the extremely high chemical stability of these compounds renders them resistant to conventional biological and chemical treatment processes, requiring the addition of activated carbon adsorption, ion exchange, or advanced oxidation treatment stages to existing water recycling facilities at capital costs that can range from USD 8 million to USD 45 million per facility depending on facility scale and feedwater per- and polyfluoroalkyl substance concentrations, while the evolving regulatory status of per- and polyfluoroalkyl substance maximum contaminant levels in drinking water creates ongoing uncertainty about the treatment performance standards that water reuse systems must achieve. The continuous evolution of contaminant monitoring requirements and treatment performance standards for advanced water reuse applications requires water recycling facility operators to maintain adaptive management programs and capital reinvestment reserves for treatment process upgrades whose timing and cost are difficult to predict with the certainty required for long-term infrastructure financing planning.

Market Segmentation

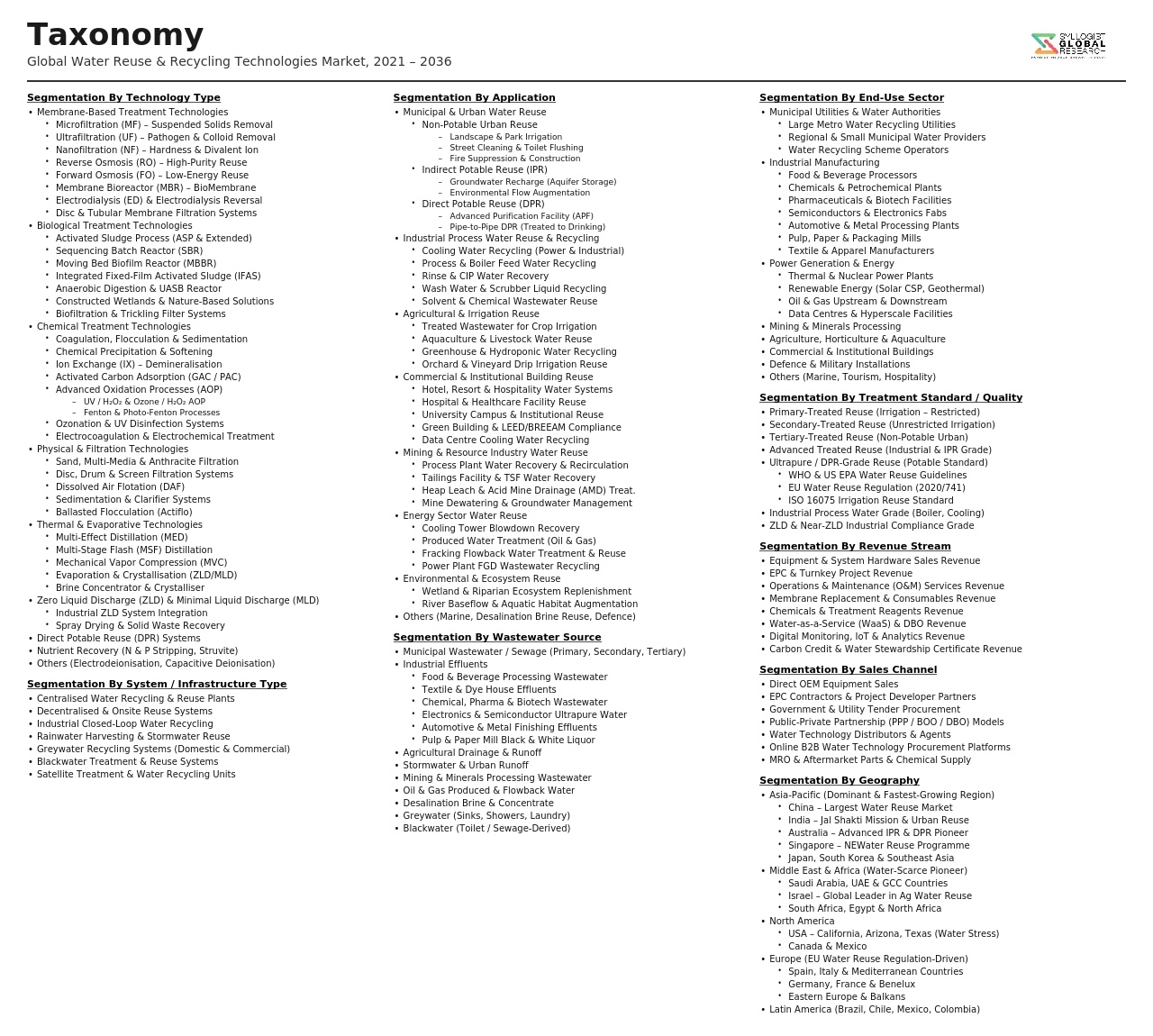

- Segmentation By Technology Type

- Membrane Bioreactor (MBR) Systems

- Ultrafiltration and Microfiltration Systems

- Reverse Osmosis and Nanofiltration Systems

- Advanced Oxidation Process (AOP) Systems (UV, Ozone, and Hydroxyl Radical)

- Ultraviolet Disinfection Systems

- Electrochemical Treatment and Electrodialysis Systems

- Ion Exchange and Adsorption Systems

- Biological Nutrient Removal and Enhanced Biological Treatment

- Constructed Wetlands and Nature-Based Treatment Systems

- Zero Liquid Discharge and Brine Concentration Systems

- Digital Water Management and AI Optimisation Platforms

- Others

- Segmentation By Application

- Municipal Non-Potable Reuse (Irrigation and Industrial Supply)

- Indirect Potable Reuse (Managed Aquifer Recharge and Reservoir Augmentation)

- Direct Potable Reuse (Treatment Train to Distribution Network)

- Agricultural and Landscape Irrigation

- Industrial Process Water Recycling

- Industrial Cooling Water Recycling

- Groundwater Recharge and Aquifer Storage

- Environmental and Ecological Flow Augmentation

- Stormwater Harvesting and Treatment

- Others

- Segmentation By End-Use Sector

- Municipal Water and Wastewater Utilities

- Semiconductor and Electronics Manufacturing

- Power Generation (Thermal and Nuclear Cooling)

- Food and Beverage Processing

- Pharmaceutical and Life Sciences Manufacturing

- Mining and Mineral Processing

- Oil and Gas and Produced Water Treatment

- Textile and Apparel Manufacturing

- Agriculture and Horticulture

- Others

- Segmentation By Treatment Stage

- Secondary Biological Treatment

- Tertiary Filtration and Disinfection

- Advanced Treatment (Membrane and AOP)

- Concentrate and Brine Management

- Post-Treatment Stabilisation and Remineralisation

- Monitoring, Control, and Quality Assurance Systems

- Segmentation By System Scale

- Large Municipal Systems (Above 50,000 cubic metres per day)

- Medium Municipal and Industrial Systems (5,000 to 50,000 cubic metres per day)

- Small and Decentralised Systems (Below 5,000 cubic metres per day)

- Building-Scale and Onsite Greywater and Rainwater Recycling Systems

- Segmentation By Deployment Model

- Engineer-Procure-Construct (EPC) Project Delivery

- Design-Build-Operate Concession

- Public-Private Partnership and BOOT Models

- Water-as-a-Service and Managed Operations

- Modular and Packaged System Supply

- Segmentation By Component

- Equipment and Systems Hardware

- Membranes and Filter Media

- Specialty Chemicals (Antiscalants, Coagulants, and Disinfectants)

- Instrumentation, Sensors, and Analysers

- Digital Software and Control Platforms

- Engineering and Professional Services

- Operations and Maintenance Services

- Segmentation By Region

- North America (United States and Canada)

- Europe (European Union, United Kingdom, and Others)

- Asia-Pacific (China, India, Australia, Singapore, and Others)

- Middle East and North Africa (Israel, Saudi Arabia, UAE, and Others)

- Latin America (Chile, Brazil, Mexico, and Others)

- Sub-Saharan Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Water Reuse and Recycling Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type, membrane systems, advanced oxidation, biological treatment, digital management, and nature-based solutions, by application, municipal potable and non-potable reuse, industrial water recycling, and agricultural reuse, and by geography, to enable water technology manufacturers, engineering contractors, utilities, and investors to identify which technology segments and regional markets will generate the highest absolute revenue and most commercially significant adoption momentum across the forecast period?

- How is the regulatory and policy landscape governing potable and non-potable water reuse expected to evolve across the European Union, United States, Middle East, China, India, and Australia through 2034, which jurisdictions are implementing the most commercially enabling water reuse regulatory frameworks, what are the projected treatment specification requirements and water quality criteria that advanced water recycling systems must satisfy under next-generation reuse standards, and how are tightening micropollutant removal requirements for per- and polyfluoroalkyl substances, pharmaceuticals, and endocrine-disrupting compounds reshaping treatment technology selection and capital investment requirements at water reuse facilities globally?

- What is the projected growth trajectory and competitive landscape of industrial zero liquid discharge systems and high-recovery industrial water recycling technology through 2034, which industrial sectors, semiconductor, pharmaceutical, mining, textile, and power generation, are generating the most significant near-term deployment demand, what are the documented water recovery rates, energy consumption benchmarks, and total cost of ownership profiles of best-practice industrial water recycling installations, and which technology platforms are best positioned to serve the growing market for closed-loop industrial water management in water-constrained manufacturing regions across Asia-Pacific, the Middle East, and North America?

- How are digital water management platforms, artificial intelligence process optimisation, real-time online water quality monitoring, and predictive maintenance systems reshaping the operational economics and reliability performance of advanced water reuse facilities, what are the quantified energy, chemical, and maintenance cost reductions being documented at water recycling facilities implementing digital management upgrades, and which water technology vendors and digital platform providers are establishing the most commercially significant competitive positions in the integrated digital water reuse management market through 2034?

- Who are the leading water treatment equipment manufacturers, membrane technology developers, engineering procurement and construction contractors, specialty chemical suppliers, and digital water technology providers currently defining the competitive landscape of the global water reuse and recycling technologies market, and what are their respective product portfolio breadth across treatment technology categories and application segments, reference project track records in municipal potable reuse, industrial zero liquid discharge, and agricultural water recycling, research and development investment in next-generation membrane materials and low-energy treatment processes, partnership and ecosystem development strategies, and competitive positioning responses to the public acceptance, energy intensity, and emerging contaminant challenges constraining water reuse program adoption globally?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Water Quality, Contaminant Variability & Public Health Compliance Risk

- Regulatory Fragmentation, Permit Complexity & Cross-Jurisdictional Approval Risk

- Technology Performance, Membrane Fouling & Process Reliability Risk

- Public Perception, Social Acceptance & Behavioural Resistance Risk

- Financing, Tariff Viability & Long-Term Project Bankability Risk

- Regulatory Framework & Standards

- National & Regional Water Reuse Regulations, Quality Standards & Permitting Frameworks

- WHO, ISO 16075 & International Guidelines for Agricultural & Urban Water Reuse

- Industrial Effluent Discharge, Zero Liquid Discharge (ZLD) & Water Recycling Compliance Requirements

- Potable Reuse Regulations, Direct & Indirect Potable Reuse Approval Frameworks

- Green Finance, Water Stewardship, ESG Disclosure & Sustainable Water Infrastructure Standards

- Global Water Reuse & Recycling Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million m3/day Treated & Reused)

- Market Size & Forecast by Technology

- Membrane Bioreactor (MBR) Technology

- Reverse Osmosis (RO) & Nanofiltration (NF) Technology

- Ultrafiltration (UF) & Microfiltration (MF) Technology

- Advanced Oxidation Processes (AOP) Technology

- Biological Treatment & Activated Sludge Systems

- Constructed Wetlands & Nature-Based Treatment Technology

- Electrochemical & Electrodialysis Treatment Technology

- UV Disinfection, Ozonation & Chlorination Technology

- Zero Liquid Discharge (ZLD) & Minimal Liquid Discharge (MLD) Systems

- Market Size & Forecast by Treatment Process

- Primary Treatment

- Secondary Treatment

- Tertiary & Advanced Treatment

- Disinfection & Polishing

- Market Size & Forecast by Reuse Application

- Agricultural Irrigation & Crop Production

- Industrial Process Water & Cooling Water Recycling

- Municipal Non-Potable Reuse (Landscaping, Toilet Flushing & Street Cleaning)

- Indirect Potable Reuse (Groundwater Recharge & Reservoir Augmentation)

- Direct Potable Reuse

- Environmental Flow Restoration & Wetland Recharge

- Mining & Oil and Gas Process Water Recycling

- Market Size & Forecast by End-User

- Municipal Water & Wastewater Utilities

- Industrial Manufacturers (Food & Beverage, Chemicals, Pulp & Paper)

- Power Generation & Energy Sector

- Mining, Oil & Gas Operators

- Agricultural Cooperatives & Irrigation Scheme Operators

- Government Agencies & National Water Authorities

- Market Size & Forecast by Project Scale

- Large-Scale Municipal & Regional Water Recycling Plants (Above 100,000 m3/day)

- Medium-Scale Industrial & Municipal Projects (10,000 to 100,000 m3/day)

- Small-Scale Decentralised & On-Site Recycling Systems (Below 10,000 m3/day)

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Project Contract (Engineering, Procurement & Construction)

- Public-Private Partnership (PPP), BOT & Concession Contract

- Direct Equipment & Membrane Technology Supply with System Integration

- Operations & Maintenance (O&M) Service & Performance Contract

- North America Water Reuse & Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million m3/day Treated & Reused)

- By Technology

- By Treatment Process

- By Reuse Application

- By End-User

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Europe Water Reuse & Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million m3/day Treated & Reused)

- By Technology

- By Treatment Process

- By Reuse Application

- By End-User

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Asia-Pacific Water Reuse & Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million m3/day Treated & Reused)

- By Technology

- By Treatment Process

- By Reuse Application

- By End-User

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Latin America Water Reuse & Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million m3/day Treated & Reused)

- By Technology

- By Treatment Process

- By Reuse Application

- By End-User

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Middle East & Africa Water Reuse & Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million m3/day Treated & Reused)

- By Technology

- By Treatment Process

- By Reuse Application

- By End-User

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Country-Wise* Water Reuse & Recycling Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million m3/day Treated & Reused)

- By Technology

- By Treatment Process

- By Reuse Application

- By End-User

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Membrane Bioreactor (MBR) Technology Deep-Dive: Configuration, Performance & Next-Generation Developments

- Reverse Osmosis & Nanofiltration Technology for Water Reuse: Energy Recovery, Fouling Control & Advanced Membrane Materials

- Advanced Oxidation Processes (AOP) & Contaminant of Emerging Concern (CEC) Removal Technology

- Zero Liquid Discharge (ZLD) & Brine Management Technology for Industrial Water Recycling

- Nature-Based Solutions, Constructed Wetlands & Hybrid Treatment Technology for Decentralised Reuse

- Digital Twin, AI-Driven Process Optimisation & SCADA Integration for Water Reuse Plants

- Potable Reuse Treatment Train Technology: Multi-Barrier Approach & Fit-for-Purpose Water Quality

- Patent & IP Landscape in Water Reuse & Recycling Technologies

- Value Chain & Supply Chain Analysis

- Membrane Module, Filtration Element & Separation Media Manufacturing Supply Chain

- Process Equipment (Pumps, Blowers, UV Systems & Chemical Dosing) Supply Chain

- Chemical Reagent, Coagulant, Flocculant & Disinfection Chemical Supply Chain

- Instrumentation, Sensors, SCADA & Digital Control Systems Supply Chain

- EPC Contractor, Project Developer & System Integrator Procurement Landscape

- Utility Operator, Government Authority & Offtake Partner Channel

- Residuals Management, Biosolids Valorisation & Brine Disposal Channel

- Pricing Analysis

- MBR Plant Capital Cost, OPEX & Levelised Cost of Water (LCOW) Analysis

- RO & Advanced Treatment System Capital & Energy Cost Analysis for Reuse Applications

- ZLD System Capital Cost, Evaporator & Crystalliser Pricing Analysis

- Membrane Replacement, Cleaning Chemical & Consumable Lifecycle Cost Analysis

- Water Reuse Project Finance, PPP Tariff & Revenue Structure Analysis

- Total Water Reuse Project Economics: LCOW Benchmarking Across Technology Routes & Reuse Applications

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Water Reuse & Recycling Technologies: Carbon Footprint, Energy Intensity & Chemical Consumption

- Water Circularity, Resource Recovery & Contribution to Freshwater Demand Reduction

- Nutrient Recovery, Biogas Generation & Circular Economy Co-Benefits of Advanced Wastewater Reuse

- Environmental Compliance, Receiving Water Body Protection & Ecosystem Impact of Water Reuse Schemes

- Regulatory-Driven Sustainability, SDG 6 (Clean Water & Sanitation) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology, Application & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology, Application & Geography

- Player Classification

- Integrated Water Technology & Treatment System Companies

- Specialist Membrane Technology & Module Manufacturers

- Advanced Oxidation, Disinfection & Chemical Treatment Technology Providers

- ZLD & Brine Management Technology Specialists

- Digital & Process Automation Platform Providers for Water Reuse

- EPC Contractors & Project Developers Specialising in Water Reuse Infrastructure

- Water Utility Operators & Concession Holders Running Reuse Schemes

- Competitive Analysis Frameworks

- Market Share Analysis by Technology, Application & Region

- Company Profile

- Company Overview & Headquarters

- Water Reuse & Recycling Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Water Reuse Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology, Treatment Process, Reuse Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output