Market Definition

The Global Zero Liquid Discharge Systems Market encompasses the engineering, manufacturing, integration, deployment, and lifecycle service of industrial water treatment systems that eliminate all liquid wastewater discharge from industrial facilities by concentrating dissolved solids, recovering treated water for process reuse, and converting residual brines and contaminants into solid or semi-solid waste streams suitable for controlled disposal or resource recovery, thereby achieving complete closure of the facility water cycle with no liquid effluent released to surface water bodies, groundwater systems, or municipal sewer networks. Zero liquid discharge systems are applied across a broad spectrum of water-intensive industrial sectors including power generation, semiconductor and electronics manufacturing, pharmaceutical production, textile and dyeing operations, chemical and petrochemical manufacturing, mining and mineral processing, food and beverage production, oil and gas produced water management, flue gas desulphurisation, and fertilizer manufacturing, where increasingly stringent wastewater discharge regulations, freshwater scarcity in water-stressed operating locations, the presence of hazardous or high-value dissolved constituents in process effluent, and corporate water stewardship commitments collectively motivate the capital-intensive investment in complete liquid discharge elimination. The technology architecture of a zero liquid discharge system typically comprises multiple integrated treatment stages including preliminary wastewater equalization and pre-treatment, physicochemical treatment for suspended solids and organic removal, high-recovery reverse osmosis or nanofiltration concentration, brine concentration through thermal evaporation using mechanical vapour recompression or multiple-effect evaporation technology, and final crystallisation through evaporative crystallisers or spray dryers that convert concentrated brine to dry solid residue. The market value chain extends from membrane technology developers, thermal evaporation equipment manufacturers, crystallisation system specialists, and process chemical suppliers through engineering procurement and construction contractors who design and commission complete zero liquid discharge systems, to the industrial water operators and third-party water management service providers whose operational management of deployed systems defines long-term performance and reliability. Key participants include thermal evaporation and crystallisation equipment manufacturers, membrane system integrators, engineering design firms, specialty chemical suppliers, and industrial facility operators across water-constrained and regulatory-sensitive manufacturing geographies globally.

Market Insights

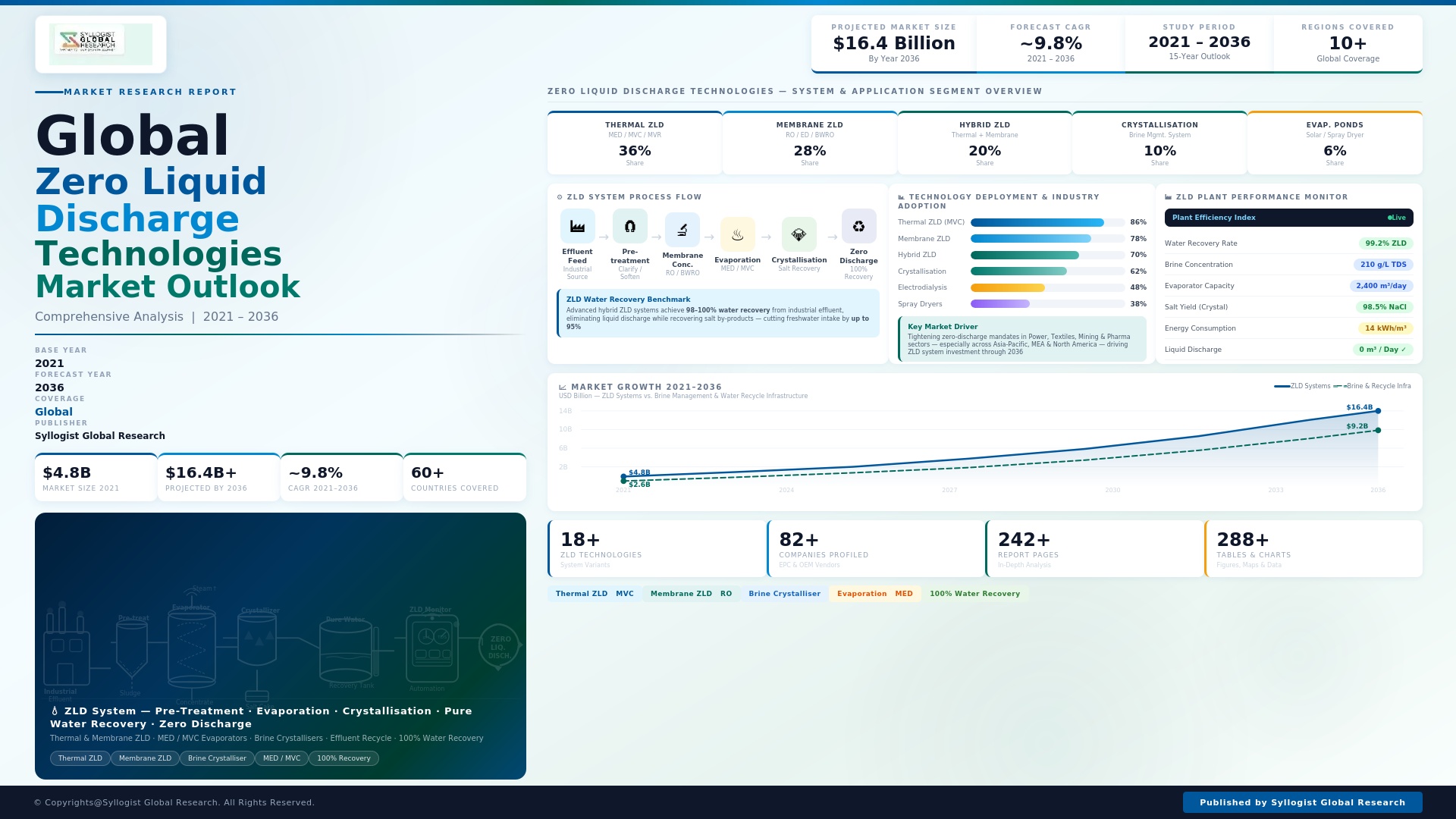

The global zero liquid discharge systems market was valued at approximately USD 7.4 billion in 2025 and is projected to reach USD 17.9 billion by 2034, advancing at a compound annual growth rate of 10.2% over the forecast period from 2027 to 2034, driven by the escalating intensity of wastewater discharge regulatory enforcement across Asia-Pacific, North America, and Europe, the expanding geographic reach of freshwater scarcity into previously water-secure industrial manufacturing regions, and the growing proportion of industrial facility operators whose environmental liability management and corporate sustainability commitments require verifiable zero liquid effluent performance rather than the discharge permit compliance that conventional wastewater treatment systems provide. The market is transitioning from a niche regulatory compliance solution deployed primarily at facilities with no technically viable discharge pathway toward a mainstream industrial water management strategy adopted by a broadening range of industries seeking to simultaneously address water scarcity risk, regulatory exposure, and water recovery economics across manufacturing operations in water-constrained geographies from the Middle East and India to the southwestern United States and northern China.

The power generation sector represents the largest single end-use market for zero liquid discharge systems by installed capacity, accounting for approximately 31% of global market revenue in 2025, driven by the regulatory requirements of the United States Environmental Protection Agency Effluent Limitation Guidelines for steam electric power plants that mandate zero discharge of flue gas desulphurisation wastewater, bottom ash transport water, and fly ash transport water from coal-fired power plants, compelling the installation of evaporative crystallisation-based zero liquid discharge systems at hundreds of affected facilities across the United States through the 2025 to 2030 compliance schedule. The semiconductor and electronics manufacturing segment is the fastest-growing end-use sector within the zero liquid discharge market, advancing at approximately 13.6% annually, driven by the ultra-pure water consumption intensity of chip fabrication operations, the presence of high-concentration per- and polyfluoroalkyl substances, ammonia, acids, and solvents in semiconductor wastewater streams that preclude conventional treatment and discharge, and the geographic concentration of new semiconductor fab construction programs in water-stressed states including Arizona, Texas, and Ohio in the United States and in Taiwan, South Korea, and Japan where water availability constraints and regulatory standards combine to mandate comprehensive water recycling including zero liquid discharge at new fabrication facility designs. Pharmaceutical and life sciences manufacturing facilities represent a growing zero liquid discharge application segment, advancing at approximately 11.8% annually, as the combination of pharmaceutical active ingredient residuals, solvents, and process chemicals in manufacturing effluent that are subject to progressively tighter discharge concentration limits and the water security requirements of facilities whose production continuity is critical to supply chain reliability are driving investment in complete water cycle closure.

Asia-Pacific dominates the global zero liquid discharge systems market, accounting for approximately 47% of total market revenue in 2025, driven by the concentration of water-intensive textile, chemical, pharmaceutical, and power generation industries in India and China where regulatory enforcement of wastewater discharge standards has intensified substantially since 2015, the acute freshwater scarcity affecting large proportions of both countries’ industrial manufacturing geographies, and the rapid expansion of semiconductor and electronics manufacturing capacity across Taiwan, South Korea, Japan, and the emerging chip fabrication clusters of India and Vietnam. India’s zero liquid discharge mandate, which requires zero liquid discharge compliance from textile dyeing and finishing units, pharmaceutical manufacturing facilities, and other specified industries in environmentally sensitive areas under the Central Pollution Control Board notification framework, has generated one of the largest concentrated national markets for zero liquid discharge system deployment globally, with an estimated 4,200 zero liquid discharge systems installed at Indian industrial facilities as of 2025 across textile clusters in Gujarat, Rajasthan, Tamil Nadu, and Maharashtra and pharmaceutical manufacturing zones in Hyderabad, Ahmedabad, and Baddi. China’s zero liquid discharge market is expanding rapidly under the ultra-low emission standards and water pollutant discharge standards enforced by the Ministry of Ecology and Environment since 2018, with coal-fired power plants, chemical manufacturing parks, and textile production clusters in water-scarce northern and northwestern provinces investing in evaporative concentration and crystallisation systems to achieve zero liquid discharge compliance mandated under provincial environmental protection regulations.

The technology architecture of zero liquid discharge systems is evolving toward hybrid configurations that reduce energy consumption and capital cost relative to conventional all-thermal zero liquid discharge designs by maximising recovery in the low-energy membrane concentration stages before thermal evaporation and crystallisation treat the residual high-salinity brine concentrate, with best-practice hybrid membrane-thermal zero liquid discharge systems achieving water recovery rates of 95% to 98% compared to 70% to 85% for high-recovery reverse osmosis alone, at specific energy consumption of 20 to 35 kilowatt hours per cubic metre of distillate produced compared to 50 to 80 kilowatt hours per cubic metre for all-thermal evaporative crystallisation designs, generating a compelling lifecycle cost improvement that is broadening the economic accessibility of zero liquid discharge across industrial sectors where all-thermal system operating costs were previously prohibitive. Brine valorisation and resource recovery from zero liquid discharge solid residues is emerging as a commercially significant dimension of the market, with the recovery of lithium, sodium sulphate, sodium chloride, calcium carbonate, and other dissolved mineral constituents from industrial brine streams through selective precipitation and crystallisation sequences generating marketable mineral co-products that offset zero liquid discharge operating costs and in some cases generate positive net revenue from what was previously a waste treatment cost centre. The integration of artificial intelligence process optimisation, digital twin simulation, and real-time water quality monitoring into zero liquid discharge system control architectures is delivering documented reductions in energy consumption of 10% to 18% and chemical dosing costs of 14% to 24% at optimised installations relative to conventionally controlled systems, improving the operating economics of zero liquid discharge and accelerating the payback period of capital-intensive system investments that have historically been among the most challenging industrial water treatment projects to justify on pure economics absent regulatory mandate.

Key Drivers

Accelerating Industrial Wastewater Discharge Regulation Enforcement and Zero Discharge Mandates Creating Non-Negotiable Compliance Investment Demand Across Multiple Industrial Sectors

The progressive tightening and enforcement of industrial wastewater discharge standards across the United States, European Union, China, India, and an expanding group of emerging market economies is creating regulatory compliance-driven zero liquid discharge investment demand that is largely independent of water economics and represents a non-discretionary capital expenditure obligation for affected industries whose discharge permits are being ratcheted toward zero-discharge levels at regulatory review cycles of three to five years. The United States Environmental Protection Agency Effluent Limitation Guidelines for steam electric power generation, finalized with compliance dates extending from 2025 through 2029 depending on plant capacity and technology selection, mandate zero discharge of flue gas desulphurisation wastewater and bottom ash transport water at coal-fired power plants above specified capacity thresholds, representing the single largest regulatory compliance driver for zero liquid discharge system installation in the North American market and generating an estimated USD 1.8 billion in zero liquid discharge equipment procurement demand across the affected fleet. India’s Central Pollution Control Board notifications requiring zero liquid discharge compliance at textile processing units, pharmaceutical formulation facilities, and distilleries in designated highly polluted areas have been progressively extended since 2016 to cover larger facility populations and additional industrial categories, with non-compliant facilities subject to closure orders whose enforcement has been strengthened since 2019, creating an urgency-driven procurement dynamic that has elevated India to among the world’s largest national markets for industrial zero liquid discharge system installation on a unit count basis.

Intensifying Freshwater Scarcity in Industrial Manufacturing Regions Compelling Water Recovery Economics That Make Zero Liquid Discharge Financially Competitive With Conventional Treatment

The convergence of groundwater depletion, surface water allocation constraints, and climate-driven precipitation variability across major industrial manufacturing regions including northwestern India, northern China, the southwestern United States, the Middle East, and northern Mexico is creating water supply security risks at industrial facilities whose production continuity depends on reliable freshwater access, compelling water-intensive manufacturers to invest in zero liquid discharge systems that recover 95% to 99% of process water for reuse and effectively decouple facility water consumption from external freshwater abstraction that is becoming increasingly constrained and costly. Water tariff escalation in water-scarce regions is improving the operating economics of zero liquid discharge systems by increasing the avoided cost value of the treated water recovered, with industrial freshwater tariffs in water-stressed Indian cities including Chennai, Ahmedabad, and Bangalore reaching USD 2.5 to USD 4.8 per cubic metre for industrial users in 2025, levels at which the water recovery economics of zero liquid discharge systems generate payback periods of four to seven years even at the elevated capital and energy costs of thermal concentration technology, creating a commercially self-justifying investment case in addition to the regulatory compliance driver. Semiconductor fabrication facilities whose ultra-pure water consumption ranges from 2 million to 8 million gallons per day at large-scale fabs are experiencing acute water supply access constraints at sites in Arizona, Israel, and Taiwan where groundwater and surface water availability is insufficient to sustain planned facility expansions without on-site water recycling and zero liquid discharge to maximise recovery from all process wastewater streams, creating a technology investment imperative whose urgency is elevated by the multi-billion dollar capital investments in fab construction that cannot be protected without assured water supply continuity.

Corporate Water Stewardship Commitments, ESG Reporting Obligations, and Investor Scrutiny of Industrial Water Risk Driving Voluntary Zero Liquid Discharge Adoption Beyond Regulatory Mandate

The mainstreaming of corporate water stewardship frameworks including the CDP Water Security questionnaire, the Science Based Targets Network freshwater targets, the Alliance for Water Stewardship standard, and the water-related financial risk disclosure frameworks incorporated into investor environmental, social, and governance assessment criteria is compelling a growing proportion of multinational manufacturing companies to implement zero liquid discharge programs at facilities in water-stressed locations as a demonstrable expression of water responsibility that supports corporate water stewardship certification, sustainability reporting, and supply chain due diligence compliance requirements. Consumer goods brand owners and retail customers of water-intensive supplier industries including textile and apparel manufacturing, food ingredient processing, and electronics assembly are implementing supply chain sustainability requirements that include verified zero liquid discharge compliance as a qualification criterion for preferred supplier status in an expanding number of corporate procurement programs, creating market pull demand for zero liquid discharge system investment at supplier facilities whose commercial relationships with these brands are contingent on water stewardship performance verification. The financial sector’s growing integration of water risk into credit analysis, insurance underwriting, and equity valuation frameworks for water-intensive industries is creating a capital cost differentiation between facilities with zero liquid discharge certification and those with conventional discharge-dependent water management systems, with water-resilient facilities in water-stressed regions commanding lower risk premiums in project financing, lower environmental liability insurance costs, and higher equity valuations that provide a financially quantifiable incentive for zero liquid discharge investment beyond the regulatory compliance and operational water security motivations that have historically driven adoption.

Key Challenges

Prohibitive Capital Cost and High Specific Energy Consumption of Thermal Evaporation and Crystallisation Systems Constraining Market Accessibility for Smaller Industrial Operators

The capital cost of a complete zero liquid discharge system incorporating high-recovery reverse osmosis, mechanical vapour recompression evaporation, and evaporative crystallisation stages typically ranges from USD 3 million to USD 45 million depending on system capacity, feedwater chemistry, and recovery requirement, with the thermal evaporation and crystallisation components alone accounting for 55% to 70% of total installed system cost and representing a capital expenditure barrier that is frequently prohibitive for small and medium-sized industrial facilities whose financial capacity and return on investment thresholds cannot accommodate the capital intensity of complete zero liquid discharge implementation. The specific energy consumption of thermal zero liquid discharge systems, ranging from 50 to 80 kilowatt hours per cubic metre of wastewater processed through evaporation and crystallisation stages, imposes operating costs of USD 4 to USD 8 per cubic metre of wastewater treated at average industrial electricity tariffs, generating annual operating cost burdens of USD 400,000 to USD 3 million per year at medium-scale industrial facilities that create ongoing profitability pressure and require careful operational management to remain within the economic parameters of zero liquid discharge project financial models approved at investment committee. The high capital and operating cost profile of zero liquid discharge systems creates a significant economic gap between the regulatory compliance obligation that mandates zero liquid discharge at affected facilities and the financial capacity of the small and medium industrial enterprises that constitute the majority of regulated facility populations in India, China, and Southeast Asia, requiring government-subsidised financing schemes, shared infrastructure models, and centralized zero liquid discharge treatment facility development by industrial park operators to make compliance economically achievable for the full range of affected industrial operators.

Solid Residue Disposal Complexity, Hazardous Waste Classification of Crystallised Salts, and Brine Valorisation Market Development Constraints Limiting System Economics

Zero liquid discharge systems achieve the objective of eliminating liquid wastewater discharge by converting dissolved contaminants and mineral salts into solid crystallised residues whose disposal or valorisation represents a distinct and often underestimated challenge in zero liquid discharge project planning, with the composition, volume, regulatory classification, and disposal economics of solid residues varying materially across different industrial wastewater chemistries in ways that can fundamentally determine the overall economics and operational sustainability of a zero liquid discharge program. Industrial zero liquid discharge crystalliser salts from textile, chemical, and pharmaceutical wastewater streams frequently contain mixed sodium sulphate, sodium chloride, and calcium sulphate fractions whose combined composition prevents cost-effective valorisation as a single commercial salt product, requiring either hazardous waste landfill disposal at costs of USD 80 to USD 350 per metric ton depending on jurisdiction and waste classification, or investment in additional selective crystallisation stages that separate mixed salt fractions into marketable pure salt products but add 20% to 35% to system capital cost. The regulatory classification of zero liquid discharge crystallised solid residues as hazardous waste under the Resource Conservation and Recovery Act in the United States, the Hazardous Waste Management Rules in India, and equivalent frameworks in other jurisdictions imposes manifesting, transportation, storage, and disposal obligations that add compliance management burden and ongoing liability exposure to zero liquid discharge facility operations, with the potential for regulatory reclassification of currently non-hazardous crystallised residues as analytical detection capabilities for trace contaminants improve creating a long-term disposal liability uncertainty that complicates zero liquid discharge system lifecycle cost modelling.

Scaling, Fouling, and Corrosion Management in High-Salinity Evaporation Systems Requiring Specialty Materials and Continuous Chemical Treatment Investment

The operation of zero liquid discharge evaporation and crystallisation systems in contact with high-salinity, multi-component brine streams containing calcium sulphate, silica, calcium carbonate, and other sparingly soluble species whose combined concentration significantly exceeds solubility limits in the concentration range targeted by evaporation systems creates persistent scaling, fouling, and corrosion management challenges that require continuous antiscalant chemical dosing, acid treatment, and periodic mechanical cleaning programs whose cost and complexity are frequently underestimated in zero liquid discharge project feasibility assessments. Heat exchanger surface scaling in mechanical vapour recompression evaporators treating high-sulphate or high-silica brine streams reduces heat transfer coefficients by 15% to 40% during operating cycles between cleaning interventions, increasing steam consumption and reducing system throughput capacity in proportion to the scaling severity, with cleaning chemical and downtime costs at severely scaling installations adding USD 0.30 to USD 0.85 per cubic metre to evaporation system operating costs over annual operating cycles. The requirement for titanium, duplex stainless steel, high-alloy nickel, or fibre-reinforced polymer construction materials in evaporation system components contacting high-chloride, high-temperature brine streams whose corrosivity exceeds the tolerance of standard stainless steel alloys increases zero liquid discharge system capital cost by 20% to 40% relative to equivalent systems treating lower-salinity wastewater streams, and requires specialty fabrication expertise and extended delivery lead times for critical evaporator components that add risk to zero liquid discharge project construction schedules and increase the replacement cost of worn or corroded components during system lifecycle operation.

Market Segmentation

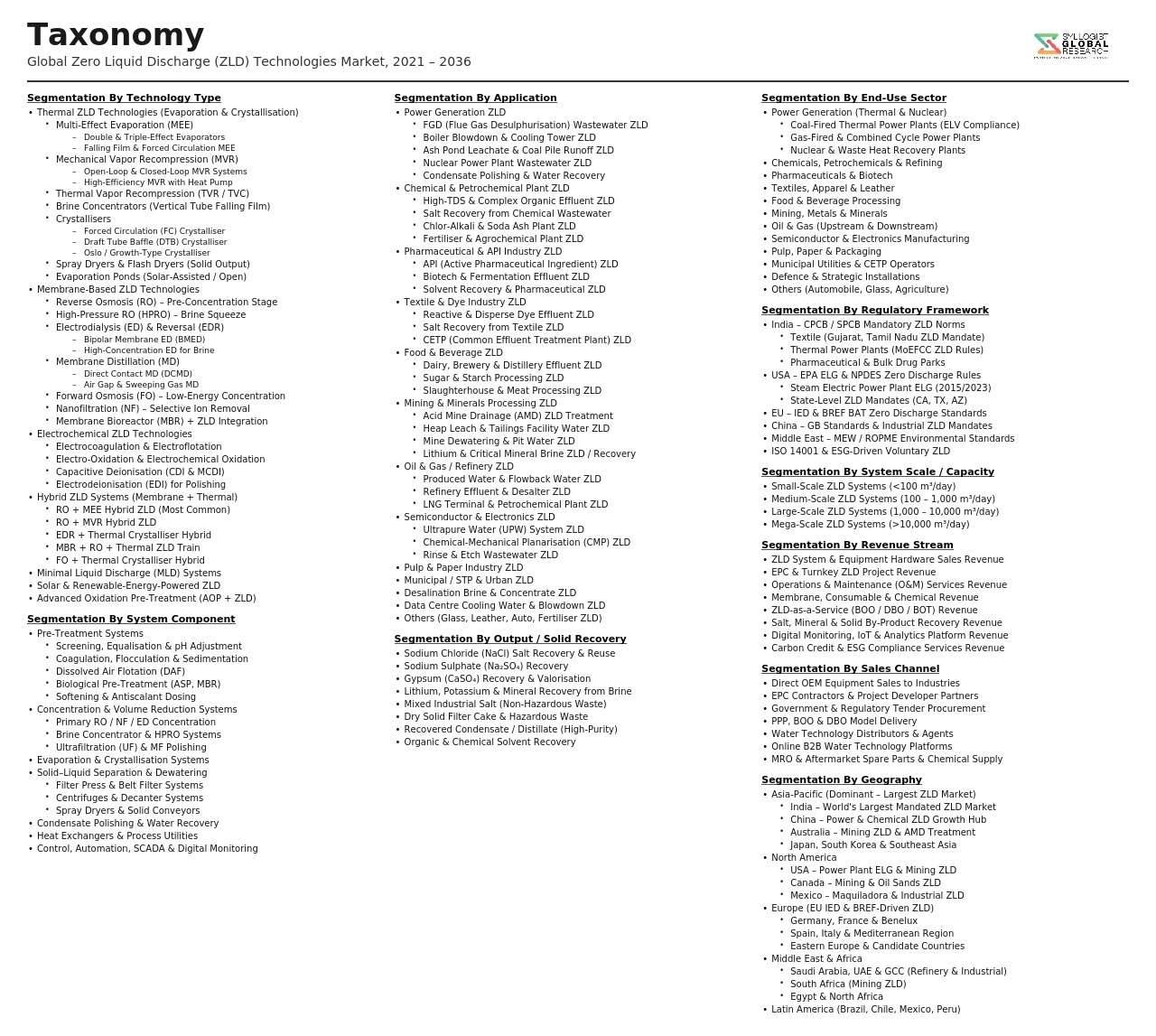

- Segmentation By Technology Type

- High-Recovery Reverse Osmosis (HRRO) and Nanofiltration Concentration

- Mechanical Vapour Recompression (MVR) Evaporation

- Multiple-Effect Evaporation (MEE) Systems

- Evaporative Crystallisation Systems

- Spray Dryers and Spray Evaporation Systems

- Membrane Distillation

- Forward Osmosis and Osmotically Assisted Reverse Osmosis

- Electrochemical Brine Concentration Systems

- Selective Crystallisation and Salt Recovery Systems

- Hybrid Membrane-Thermal ZLD Systems

- Others

- Segmentation By End-Use Industry

- Power Generation (Coal-Fired and Gas-Fired Plants)

- Semiconductor and Electronics Manufacturing

- Pharmaceutical and Life Sciences Manufacturing

- Textile Dyeing and Finishing

- Chemical and Petrochemical Manufacturing

- Mining and Mineral Processing

- Oil and Gas and Produced Water Management

- Food and Beverage Processing

- Fertilizer and Agrochemical Manufacturing

- Flue Gas Desulphurisation (FGD) Wastewater Treatment

- Others

- Segmentation By Wastewater Source

- Flue Gas Desulphurisation Wastewater

- Cooling Tower Blowdown

- Reverse Osmosis Reject and Concentrate Streams

- Industrial Process Effluent

- Produced Water from Oil and Gas Operations

- Mining Process and Tailings Water

- Pharmaceutical and Chemical Manufacturing Effluent

- Textile Dyehouse Effluent

- Others

- Segmentation By System Capacity

- Large-Scale Systems (Above 5,000 cubic metres per day)

- Medium-Scale Systems (500 to 5,000 cubic metres per day)

- Small-Scale and Modular Systems (Below 500 cubic metres per day)

- Segmentation By Deployment Driver

- Regulatory Compliance and Mandatory Zero Discharge Requirement

- Freshwater Scarcity and Water Recovery Economics

- Corporate Water Stewardship and ESG Commitment

- Hazardous Constituent Containment and Environmental Liability Management

- Resource and Mineral Recovery from Brine

- Segmentation By System Component

- Pre-Treatment and Equalization Systems

- Membrane Concentration Equipment and Modules

- Thermal Evaporation and Heat Exchange Equipment

- Crystallisation and Solids Separation Equipment

- Specialty Anti-Scalant and Process Chemicals

- Process Instrumentation, Sensors, and Analysers

- Control Systems and Digital Optimisation Platforms

- Engineering Design and Commissioning Services

- Operations and Maintenance Services

- Segmentation By Delivery Model

- Engineer-Procure-Construct (EPC) Turnkey System Delivery

- Design-Build-Operate (DBO) with Performance Guarantees

- Water-as-a-Service and Managed ZLD Operations

- Modular and Packaged System Supply

- Centralised Common Effluent ZLD Treatment for Industrial Parks

- Segmentation By Region

- North America (United States and Canada)

- Europe (European Union and United Kingdom)

- Asia-Pacific (China, India, Taiwan, South Korea, and Others)

- Middle East and North Africa

- Latin America (Mexico, Brazil, and Others)

- Sub-Saharan Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Zero Liquid Discharge Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type, membrane concentration, mechanical vapour recompression evaporation, multiple-effect evaporation, and evaporative crystallisation, by end-use industry, power generation, semiconductor, textile, pharmaceutical, and chemical sectors, and by geography, to enable system manufacturers, engineering contractors, industrial water managers, and investors to identify which technology segments and industrial end-use markets will generate the highest absolute revenue and most commercially significant adoption momentum across the forecast period?

- How is the regulatory landscape governing industrial wastewater discharge and zero liquid discharge compliance obligations expected to evolve across the United States, European Union, China, India, and Southeast Asia through 2034, which industrial sectors and geographic markets are subject to the most imminent and commercially significant mandatory zero liquid discharge compliance timelines, what are the estimated total capital expenditure requirements for regulatory compliance-driven zero liquid discharge installation across the affected power generation, textile, and pharmaceutical facility populations in each major jurisdiction, and how are enforcement mechanisms and penalty frameworks evolving to accelerate compliance timelines?

- What is the projected commercial trajectory of hybrid membrane-thermal zero liquid discharge system architectures through 2034 relative to all-thermal evaporative crystallisation designs, at what water recovery rate and specific energy consumption benchmarks are best-practice hybrid zero liquid discharge systems operating at currently commissioned reference facilities, which industrial wastewater chemistry profiles are most and least suited to hybrid membrane-thermal approaches, and how are advances in high-pressure reverse osmosis membrane performance, osmotically assisted reverse osmosis, and forward osmosis membrane technology expected to extend membrane concentration boundaries and reduce the thermal evaporation load in next-generation zero liquid discharge system designs?

- How are brine valorisation technologies and resource recovery programs transforming the economics and waste management profile of zero liquid discharge systems through 2034, which dissolved mineral constituents including lithium, sodium sulphate, sodium chloride, and calcium carbonate are generating the most commercially viable recovery opportunities from industrial zero liquid discharge brine streams, what selective crystallisation and precipitation technology investments are required to convert mixed salt residues into marketable pure mineral products, and how are lithium recovery programs from geothermal brine, mining process water, and battery manufacturing wastewater zero liquid discharge systems emerging as a commercially significant sub-market within the broader zero liquid discharge industry?

- Who are the leading zero liquid discharge system manufacturers, thermal evaporation and crystallisation equipment suppliers, high-recovery membrane system integrators, and engineering procurement and construction contractors currently defining the competitive landscape of the global zero liquid discharge market, and what are their respective technology portfolio coverage across membrane, thermal, and hybrid system architectures, reference project track records by industry sector and system capacity, research and development investment in energy reduction and brine valorisation technology, service and operations management capability for long-term system performance assurance, and strategic competitive positioning responses to the capital cost, solid residue disposal, and scaling management challenges that constrain zero liquid discharge system accessibility and economics across small and medium industrial operator segments globally?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- High Capital Expenditure, Long Payback Period & Project Financing Risk

- Energy Intensity, Operating Cost Escalation & Utility Availability Risk

- Brine Scaling, Fouling, Corrosion & System Reliability Risk

- Solid Waste & Salt Cake Disposal, Regulatory Compliance & Liability Risk

- Regulatory Tightening, Discharge Standard Changes & Permit Uncertainty Risk

- Regulatory Framework & Standards

- Industrial Effluent Discharge & Zero Liquid Discharge Mandate Regulations by Jurisdiction

- Water Scarcity, Water Allocation & Industrial Water Recycling Policy Frameworks

- Hazardous Waste, Solid Residue & Salt Cake Disposal Regulations Applicable to ZLD Systems

- Energy Efficiency, Thermal Process Emissions & Environmental Permit Requirements for ZLD Installations

- Green Finance, ESG Disclosure & Sustainable Industrial Water Management Standards

- Global Zero Liquid Discharge (ZLD) Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Installed Capacity, m3/day)

- Market Size & Forecast by System Type

- Conventional Thermal ZLD Systems

- Hybrid ZLD Systems (Membrane-Thermal Combination)

- Membrane-Based ZLD Systems (High-Recovery RO & Electrodialysis)

- Minimal Liquid Discharge (MLD) Systems

- Market Size & Forecast by Technology

- Evaporator & Crystalliser (Mechanical Vapour Recompression, Multi-Effect Evaporation)

- Reverse Osmosis (RO) & High-Recovery Reverse Osmosis (HRRO)

- Electrodialysis (ED) & Electrodialysis Reversal (EDR)

- Brine Concentrator & Spray Dryer Systems

- Forward Osmosis & Membrane Distillation

- Ultrafiltration (UF) & Nanofiltration (NF) Pre-Treatment Systems

- Solar Evaporation & Emerging Low-Energy ZLD Technologies

- Market Size & Forecast by Component

- Evaporators & Crystallisers

- Membrane Modules & Filtration Units

- Heat Exchangers & Energy Recovery Devices

- Pumps, Compressors & Blowers

- Instrumentation, Controls & SCADA Systems

- Chemical Dosing & Pre-Treatment Systems

- Services (Engineering, Installation, O&M & Aftermarket)

- Market Size & Forecast by End-User Industry

- Power Generation (Coal, Gas & Nuclear Power Plants)

- Chemicals & Petrochemicals

- Textiles & Dyeing

- Pharmaceuticals & Biotechnology

- Food & Beverage Processing

- Mining & Minerals Processing

- Oil & Gas Refining & Upstream Operations

- Pulp & Paper Manufacturing

- Steel, Metals & Metal Finishing

- Semiconductor & Electronics Manufacturing

- Market Size & Forecast by Application

- Industrial Effluent Treatment & Discharge Elimination

- Produced Water Treatment & Reuse in Oil & Gas

- Flue Gas Desulphurisation (FGD) Wastewater Treatment in Power Plants

- Cooling Tower Blowdown Recycling

- Boiler Feed Water Recovery & Reuse

- Salt & By-Product Recovery from Industrial Effluent

- Market Size & Forecast by Project Scale

- Large-Scale Industrial ZLD Plants (Above 5,000 m3/day)

- Medium-Scale Industrial ZLD Plants (500 to 5,000 m3/day)

- Small-Scale & Modular ZLD Systems (Below 500 m3/day)

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Project Contract (Engineering, Procurement & Construction)

- Equipment Supply & System Integration

- Build-Operate-Transfer (BOT) & Design-Build-Operate (DBO) Contract

- Operations & Maintenance (O&M) Service & Performance Contract

- North America Zero Liquid Discharge (ZLD) Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, m3/day)

- By System Type

- By Technology

- By End-User Industry

- By Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Europe Zero Liquid Discharge (ZLD) Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, m3/day)

- By System Type

- By Technology

- By End-User Industry

- By Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Asia-Pacific Zero Liquid Discharge (ZLD) Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, m3/day)

- By System Type

- By Technology

- By End-User Industry

- By Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Latin America Zero Liquid Discharge (ZLD) Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, m3/day)

- By System Type

- By Technology

- By End-User Industry

- By Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Middle East & Africa Zero Liquid Discharge (ZLD) Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, m3/day)

- By System Type

- By Technology

- By End-User Industry

- By Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Country-Wise* Zero Liquid Discharge (ZLD) Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, m3/day)

- By System Type

- By Technology

- By End-User Industry

- By Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Mechanical Vapour Recompression (MVR) & Multi-Effect Evaporation (MEE) Technology Deep-Dive

- High-Recovery Reverse Osmosis (HRRO) & Electrodialysis Reversal (EDR) Technology for ZLD Pre-Concentration

- Crystalliser Technology: Forced Circulation, Draft Tube Baffle & Fluidised Bed Crystallisation

- Forward Osmosis & Membrane Distillation as Emerging Low-Energy ZLD Concentration Technologies

- Solar-Assisted & Waste Heat-Driven ZLD Technology for Energy Cost Reduction

- Salt & By-Product Recovery, Valorisation & Circular Economy Integration in ZLD Systems

- Digital Twin, AI-Driven Process Optimisation & Remote Monitoring Technology for ZLD Plants

- Patent & IP Landscape in Zero Liquid Discharge Technologies

- Value Chain & Supply Chain Analysis

- Evaporator, Crystalliser & Thermal Process Equipment Manufacturing Supply Chain

- Membrane Module, Filtration Element & Ion Exchange Media Manufacturing Supply Chain

- Heat Exchanger, Energy Recovery Device & Mechanical Equipment Supply Chain

- Chemical Reagent, Scale Inhibitor, Antiscalant & Pre-Treatment Chemical Supply Chain

- Instrumentation, Sensors & SCADA Control Systems Supply Chain

- EPC Contractor, Process Licensor & System Integrator Procurement Landscape

- Industrial End-User Procurement, O&M & Long-Term Service Channel

- Pricing Analysis

- Conventional Thermal ZLD System Capital Cost & Total Cost of Ownership (TCO) Analysis

- Hybrid ZLD System Capital Cost Comparison: Membrane-Thermal vs. Fully Thermal Routes

- Evaporator & Crystalliser Equipment Unit Pricing & Installation Cost Analysis

- Energy Cost Analysis: MVR vs. MEE vs. Membrane-Based ZLD System Operating Expenditure

- ZLD Project Finance, Tariff Structure & Revenue Model Analysis

- Levelised Cost of ZLD Treatment (LCT) Benchmarking Across Technology Routes & Industry Segments

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of ZLD Systems: Carbon Footprint, Energy Intensity & Chemical Consumption Across Technology Routes

- Water Conservation & Freshwater Withdrawal Reduction Contribution of ZLD Adoption

- Salt & By-Product Recovery, Waste Valorisation & Circular Economy Co-Benefits of ZLD Systems

- Solid Residue, Salt Cake Disposal & Long-Term Environmental Liability Assessment

- Regulatory-Driven Sustainability, SDG 6 (Clean Water) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type, Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Technology & Geography

- Player Classification

- Integrated Water & Wastewater Technology Companies with Full ZLD Portfolios

- Specialist Thermal Evaporation & Crystallisation Technology Providers

- Membrane Technology & High-Recovery RO System Manufacturers

- Electrodialysis & Ion Exchange Technology Specialists

- EPC Contractors & Process Licensors Specialising in ZLD Projects

- Modular & Packaged ZLD System Providers

- Operations & Maintenance Service Providers for Industrial ZLD Plants

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- ZLD Products, Technology Portfolio & Process Licensing Capabilities

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (ZLD Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Technology, Component, End-User Industry & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output