China Bio-Succinic Acid Market By Production Technology, By Feedstock Type, By Application, By End Use Industry, By Grade, By Distribution Channel, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The China Bio-Succinic Acid Market encompasses the production, processing, and commercial distribution of succinic acid manufactured through microbial fermentation of renewable sugar, agricultural residue, and carbon dioxide feedstocks rather than conventional petrochemical maleic anhydride hydrogenation routes, serving as a bio-based platform chemical for polybutylene succinate bioplastics, polyurethanes, plasticizers, food and beverage acidulants, pharmaceutical intermediates, personal care ingredients, and specialty chemical synthesis applications across Chinese domestic manufacturing and export markets.

Market Insights

The China bio-succinic acid market is positioned at a strategically consequential juncture in its development trajectory, as the convergence of national carbon neutrality policy ambitions, rapidly expanding bioplastics demand from Chinese packaging and consumer goods manufacturers transitioning away from conventional petroleum-derived plastics, and the technological maturation of industrial fermentation production platforms is creating both the regulatory pull and commercial demand foundation for bio-succinic acid to transition from a niche specialty chemical toward a volume-scale platform bio-chemical serving multiple high-growth downstream application chains. The market was valued at approximately USD 186.4 million in 2025 and is projected to advance at a compound annual growth rate of 18.7% through 2034, as China’s strategic commitment to developing domestic bio-based chemical manufacturing capacity, combined with the substantial investment of Chinese fermentation technology developers and chemical producers in bio-succinic acid production scale-up programs, progressively improves domestic production cost competitiveness toward parity with petrochemical succinic acid at commercial production volumes that unlock broad substitution across cost-sensitive industrial application categories.

Polybutylene succinate bioplastics production represents the most strategically significant and commercially expanding downstream application for bio-succinic acid in China, as the rapid growth of domestic polybutylene succinate demand driven by compostable packaging regulations, single-use plastic substitution policies, and the expanding adoption of biodegradable agricultural mulch film under China’s rural plastic pollution reduction programs is creating a durable, policy-supported demand pull for domestic bio-succinic acid supply that directly substitutes for imported bio-succinic acid and petrochemically derived succinic acid currently supplying polybutylene succinate resin producers. China’s position as both the world’s largest polybutylene succinate consumer and a growing producer, supported by active government industrial policy investment in degradable plastics industrial chain development, is establishing a uniquely favorable domestic demand infrastructure for bio-succinic acid market expansion that is unmatched in scale among global bio-succinic acid market development contexts.

The food and pharmaceutical application segments represent distinct high-value bio-succinic acid demand channels in China that command premium pricing relative to industrial polymer applications and provide commercial viability anchoring for bio-succinic acid producers during the market development phase before polybutylene succinate application volumes achieve sufficient scale to support commodity-level bio-succinic acid production economics. Food-grade bio-succinic acid applications in acidity regulation, flavor enhancement, and beverage formulation benefit from growing Chinese consumer preference for naturally sourced food ingredients, and the clean-label positioning advantages of bio-based succinic acid over petrochemically derived alternatives support price premium maintenance in food and nutraceutical ingredient markets. Research and development investment in bio-succinic acid production from carbon dioxide co-fermentation and lignocellulosic agricultural residue feedstocks is attracting Chinese government research funding and industrial company co-investment as strategic technology programs that could simultaneously reduce bio-succinic acid production costs and improve the carbon footprint credentials of Chinese bio-chemical manufacturing relative to both domestic petrochemical alternatives and international bio-succinic acid producers utilizing corn or sugar feedstocks.

Eastern China, encompassing the Yangtze River Delta industrial provinces of Jiangsu, Zhejiang, and Shandong, represents the primary production and consumption geography for bio-succinic acid within China, reflecting the concentration of fermentation biotechnology companies, bioplastics manufacturers, food ingredient producers, and specialty chemical users that collectively constitute the bio-succinic acid value chain in China’s most industrially advanced and biotechnology-investment-intensive regions. Central and southern China are emerging as secondary market development regions, driven by the expansion of biodegradable plastics manufacturing capacity into regions with lower land and utility costs, growing agricultural residue feedstock availability from crop production areas, and provincial government industrial policy programs supporting bio-based chemical manufacturing investment as a strategic industry development priority aligned with national circular bioeconomy policy objectives.

Key Drivers

China’s Single-Use Plastic Restriction Policies and Biodegradable Packaging Mandates Creating Structural Downstream Demand Pull for Polybutylene Succinate and Bio-Succinic Acid

China’s progressively implemented ban on non-degradable single-use plastic bags, straws, food service utensils, and packaging materials under the National Development and Reform Commission plastic pollution control action plan is generating structural demand growth for compostable polybutylene succinate resins and films that require bio-succinic acid as a core monomer input, establishing a regulatory-mandated demand foundation for domestic bio-succinic acid supply that is independent of voluntary sustainability commitments and provides long-term procurement visibility for bio-succinic acid production investment decisions. The extension of compostable plastics requirements to agricultural mulch film replacement programs targeting the massive volume of conventional polyethylene mulch film used in Chinese vegetable and crop production is adding a large additional polybutylene succinate demand channel that further reinforces the bio-succinic acid market growth trajectory.

National Carbon Neutrality Commitments and Bio-Based Chemical Industry Policy Investment Supporting Domestic Bio-Succinic Acid Production Capacity Development and Technology Advancement

China’s dual carbon policy framework targeting peak carbon dioxide emissions before 2030 and carbon neutrality by 2060 is elevating bio-based chemical manufacturing as a strategic industrial development priority within national five-year plans and provincial industrial policy programs, generating direct government support for bio-succinic acid production through research and development grants, demonstration project co-investment, green industry investment fund participation, and preferential financing rates for qualifying bio-based chemical manufacturing capacity. The designation of bio-based chemicals including bio-succinic acid as priority products within the national bioeconomy development strategy is providing industry investment planning certainty and policy support continuity that differentiates China’s bio-succinic acid market development environment from less policy-supported international markets.

Chinese Fermentation Biotechnology Capability and Low-Cost Agricultural Feedstock Availability Creating Competitive Production Economics for Domestic Bio-Succinic Acid Manufacturing

China’s deep industrial fermentation expertise accumulated across pharmaceutical, amino acid, organic acid, and food ingredient production sectors provides a highly relevant technological foundation for bio-succinic acid fermentation process development, as microbial strain engineering, fermentation scale-up optimization, and downstream purification process design capabilities built in adjacent fermentation product industries can be adapted and applied to bio-succinic acid production with lower technology development risk and faster commercialization timelines than equivalent capability building from a greenfield starting point would require. The abundant and competitively priced agricultural feedstocks available in China including corn glucose, cassava starch, sugarcane molasses, and crop residue hydrolysates provide raw material cost advantages for Chinese bio-succinic acid producers relative to international competitors in markets with less favorable renewable carbohydrate feedstock supply economics.

Key Challenges

Bio-Succinic Acid Production Cost Premium Over Petrochemical Succinic Acid Limiting Market Penetration in Cost-Sensitive Industrial Applications Without Sustained Policy Premium Support

Bio-succinic acid produced through microbial fermentation at current Chinese production scales carries manufacturing cost premiums relative to petrochemically derived succinic acid from maleic anhydride hydrogenation that limit market adoption in price-sensitive industrial applications including plasticizers, solvents, and intermediate chemical synthesis where buyers lack financial incentive to pay bio-based premiums without regulatory mandates or voluntary sustainability commitments that specifically reward bio-based content selection. Achieving production cost parity with petrochemical succinic acid requires continued fermentation titer and yield improvement, downstream purification efficiency optimization, and production scale-up to volumes where fixed cost amortization and raw material purchasing scale generate the cost reduction that laboratory and pilot-scale economics project but commercial-scale operations have not yet uniformly demonstrated in the Chinese production context.

Fermentation Feedstock Price Volatility and Agricultural Raw Material Supply Security Creating Input Cost Uncertainty for Bio-Succinic Acid Production Economics

Bio-succinic acid production economics are significantly influenced by the cost and availability of fermentable sugar feedstocks including corn starch glucose syrup, cassava starch, and sugarcane molasses whose prices are subject to agricultural commodity market volatility driven by weather conditions, crop disease, energy cost impacts on agricultural production, and government price support policy changes that can materially alter the variable production cost economics of bio-succinic acid fermentation within production cost planning periods. The competition between bio-succinic acid production and food processing, animal feed, and bioethanol fermentation for glucose and starch feedstock supplies during periods of agricultural commodity supply tightness creates additional feedstock sourcing risk for bio-succinic acid producers whose production cost models are calibrated to long-term average agricultural commodity price levels rather than peak price scenarios.

Downstream Application Market Development Pace and Polybutylene Succinate Value Chain Maturity Constraining Near-Term Bio-Succinic Acid Demand Realization Against Installed Production Capacity

The development of large-scale bio-succinic acid consumption in China is contingent on the concurrent maturation of downstream polybutylene succinate resin production capacity, compostable packaging processing infrastructure, biodegradable agricultural film manufacturing scale, and consumer and industrial market acceptance of bio-based packaging formats as functionally adequate and commercially available substitutes for conventional plastic alternatives, creating market development dependencies whose pace is not fully within the control of bio-succinic acid producers and may lag behind production capacity investment timelines in ways that generate oversupply conditions and pricing pressure in the near-to-medium term market development phase. Building brand owner and consumer acceptance of bio-based packaging properties including differences in moisture barrier performance, heat resistance, and mechanical properties relative to conventional plastics requires end-use application development investment that extends beyond bio-succinic acid producer capabilities into the downstream packaging design and materials testing ecosystem.

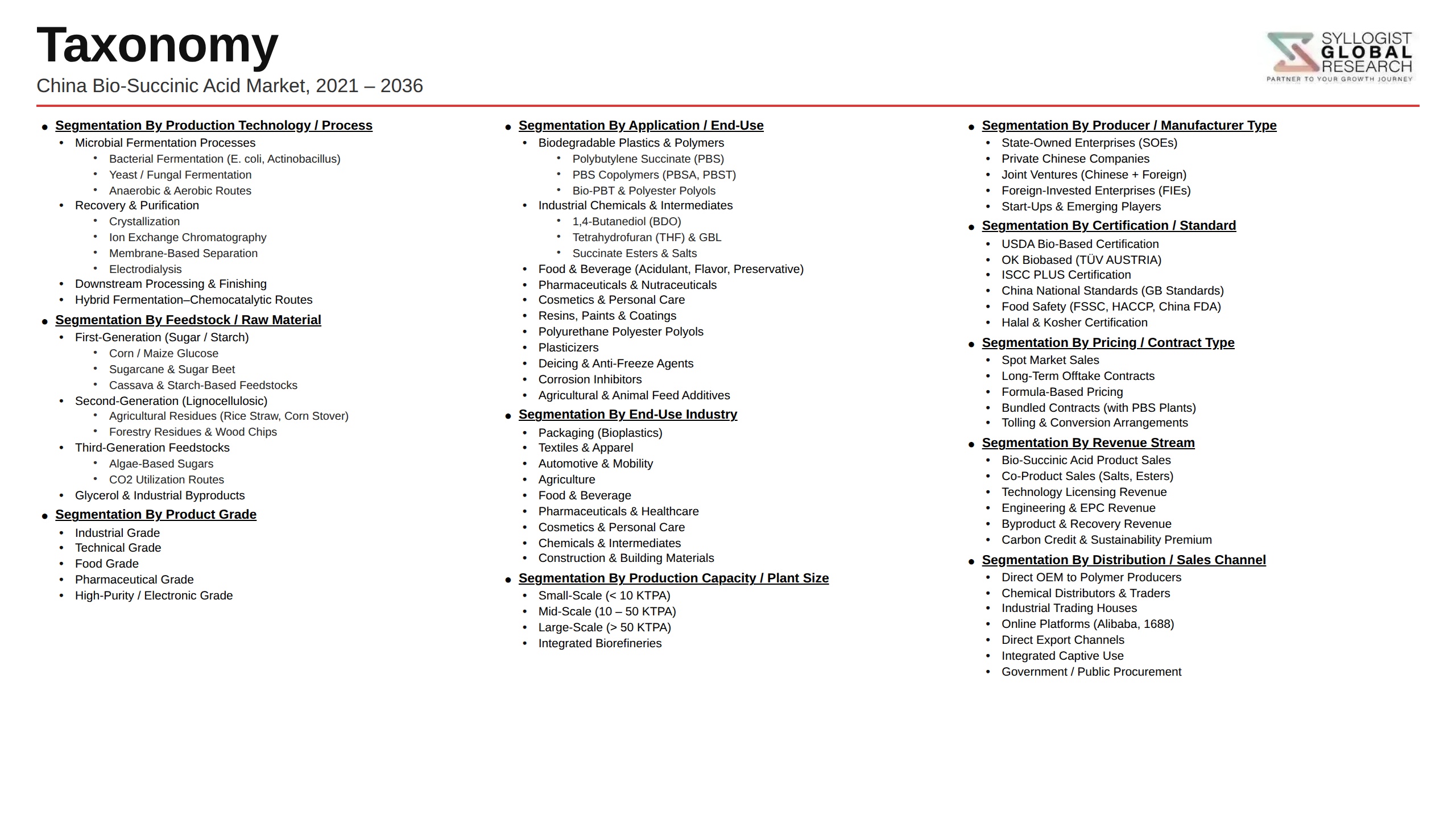

Market Segmentation

- Segmentation By Production Technology

- Aerobic Fermentation with Glucose Feedstock

- Anaerobic Fermentation with Carbon Dioxide Co-Fixation

- Lignocellulosic Biomass Hydrolysate Fermentation

- Engineered E. coli and Corynebacterium Fermentation Platforms

- Yeast-Based Fermentation Systems

- Others

- Segmentation By Feedstock Type

- Corn Starch and Glucose Syrup

- Cassava Starch and Tapioca

- Sugarcane Molasses and Bagasse

- Agricultural Residue and Lignocellulosic Biomass

- Carbon Dioxide and Renewable Gas Feedstocks

- Others

- Segmentation By Application

- Polybutylene Succinate and Bioplastics Production

- Polyurethane and Resin Synthesis

- Plasticizers and Lubricant Additives

- Food and Beverage Acidulant and Flavor Ingredient

- Pharmaceutical Intermediates and Active Ingredients

- Personal Care and Cosmetics Ingredients

- Specialty Chemical Synthesis and Solvents

- Others

- Segmentation By End Use Industry

- Bioplastics and Packaging Manufacturing

- Food and Beverage Processing

- Pharmaceutical and Nutraceutical Manufacturing

- Personal Care and Cosmetics

- Agricultural Chemicals and Crop Protection

- Coatings, Adhesives, and Sealants

- Others

- Segmentation By Grade

- Industrial Grade Bio-Succinic Acid

- Food Grade Bio-Succinic Acid

- Pharmaceutical Grade Bio-Succinic Acid

- Technical and Reagent Grade Bio-Succinic Acid

- Segmentation By Distribution Channel

- Direct Sales to Industrial and Polymer Manufacturers

- Specialty Chemical Distributors and Traders

- Food Ingredient and Pharmaceutical Raw Material Suppliers

- Export and International Trade Channels

- Others

- Segmentation By Region

- East China (Jiangsu, Zhejiang, Shandong, Shanghai)

- Central China (Henan, Hubei, Hunan)

- South China (Guangdong, Guangxi, Fujian)

- North China (Beijing, Tianjin, Hebei)

- Northeast and Western China

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total China bio-succinic acid market valuation in 2025, projected through 2034, segmented by production technology, application, and end use industry, enabling bio-succinic acid producers, fermentation technology developers, downstream polymer manufacturers, and investors to identify the highest-growth application segments and most commercially significant production investment opportunities within the Chinese bio-succinic acid market?

- How are China’s single-use plastic ban implementation, compostable packaging regulatory mandates, and biodegradable agricultural mulch film replacement programs creating quantifiable downstream polybutylene succinate demand growth that translates into bio-succinic acid procurement volumes, and what implementation timelines, geographic enforcement patterns, and policy expansion trajectories are most materially shaping the bio-succinic acid demand outlook through 2034?

- Which fermentation production technology platforms, specifically engineered E. coli glucose fermentation, anaerobic carbon dioxide co-fixation routes, and lignocellulosic biomass hydrolysate fermentation systems, are demonstrating the most commercially competitive production cost trajectories in China, and what titer, yield, and purification efficiency milestones must be achieved to reach cost parity with petrochemical succinic acid at commercial production scales?

- How is the competitive landscape structured among Chinese domestic bio-succinic acid producers, international bio-succinic acid suppliers, and petrochemical succinic acid manufacturers competing for Chinese market share across polymer, food, pharmaceutical, and specialty chemical application segments, and what technology licensing, production scale, product quality differentiation, and customer partnership strategies are shaping competitive positioning?

- What government policy support mechanisms, including national bioeconomy strategy designation, green industry investment fund participation, research and development co-investment programs, and preferential financing rates for bio-based chemical capacity, are most significantly accelerating bio-succinic acid production investment in China, and how are provincial industrial policy programs in key production regions complementing national policy frameworks?

- How are food-grade and pharmaceutical-grade bio-succinic acid applications in Chinese food ingredient, nutraceutical, and pharmaceutical manufacturing providing premium pricing and early commercial viability support for Chinese bio-succinic acid producers during the market development phase, and what regulatory certification requirements, quality specifications, and customer qualification processes govern market entry in these higher-value segments?

- What downstream polybutylene succinate value chain maturity constraints, compostable packaging processing infrastructure development timelines, consumer and brand owner acceptance challenges, and competitive pressures from imported bio-succinic acid are most significantly affecting the pace at which Chinese bio-succinic acid production investment translates into commercial-scale market demand realization and financially sustainable production operations through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Feedstock Price Volatility: Glucose, Corn Starch & Agricultural Raw Material Cost Fluctuation Risk

- Fermentation Yield, Process Stability & Scale-Up from Pilot to Industrial Production Risk

- Price Competition from Petroleum-Derived Succinic Acid & Alternative Bio-Based Diacids Risk

- Downstream Market Adoption Barrier & Customer Qualification Timeline Risk

- Regulatory Approval, Food & Medical Grade Certification & Product Compliance Risk

- Export Market Access, International Trade Policy & Bio-Based Product Certification Recognition Risk

- Regulatory Framework & Standards

- National Development & Reform Commission (NDRC) Bio-Economy Policy, 14th Five-Year Plan & Bio-Based Chemical Industry Development Standards

- Ministry of Industry & Information Technology (MIIT) Bio-Manufacturing Industry Development Guidelines & Green Chemical Standards

- GB Standards, Chinese Pharmacopoeia & National Food Safety Standards for Succinic Acid in Food, Feed & Pharmaceutical Applications

- China Environmental Protection Standards, Bio-Fermentation Wastewater Discharge & Carbon Emission Trading Scheme (ETS) Compliance

- Bio-Based Product Certification, CNAS Laboratory Accreditation & ISO 16620 Bio-Based Content Standards for China Market

- Export Compliance: EU REACH, FDA Food Additive Status, Kosher/Halal Certification & International Bio-Based Chemical Trade Standards

- China Bio-Succinic Acid Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Tonnes per Annum, TPA)

- Market Size & Forecast by Production Process

- Bacterial Fermentation (E. coli, Basfia succiniciproducens & Actinobacillus succinogenes)

- Yeast Fermentation (Saccharomyces cerevisiae & Yarrowia lipolytica)

- Fungal & Filamentous Fungi Fermentation Routes

- Electrochemical CO2 Reduction & Electrosynthesis Routes

- Hybrid Biological-Chemical Catalytic Process Routes

- Market Size & Forecast by Feedstock

- Corn Starch, Glucose Syrup & Dextrose-Based Feedstock

- Cassava, Sweet Potato & Starch Crop-Based Feedstock

- Lignocellulosic Biomass & Agricultural Residue-Based Feedstock

- CO2 & Waste Carbon Feedstock (Coupled with Renewable Energy)

- Waste Glycerol & Industrial By-Product Feedstock

- Market Size & Forecast by Purity Grade

- Industrial Grade Bio-Succinic Acid

- Food Grade Bio-Succinic Acid

- Pharmaceutical Grade Bio-Succinic Acid

- Electronic & Specialty Chemical Grade Bio-Succinic Acid

- Market Size & Forecast by Derivative & Downstream Application

- 1,4-Butanediol (BDO) & Polybutylene Succinate (PBS) Biodegradable Plastic

- Polyester Polyols & Polyurethane Synthesis

- N-Methyl-2-Pyrrolidone (NMP) & Solvent Applications

- Succinic Anhydride & Specialty Chemical Synthesis

- Food Additive, Flavour Enhancer & Acidulant Applications

- Pharmaceutical Excipient, Drug Salt Formation & Active Ingredient Applications

- Personal Care, Cosmetic & Skin Care Formulation Applications

- Agricultural Chemical & Crop Protection Formulation Applications

- Coatings, Adhesives, Sealants & Specialty Resin Applications

- Market Size & Forecast by End-User Industry

- Biodegradable Plastics & Bio-Based Polymer Industry

- Food, Feed & Flavour Industry

- Pharmaceutical & Health Supplement Industry

- Chemical, Petrochemical & Specialty Chemical Industry

- Personal Care & Cosmetics Industry

- Agriculture & Agrochemical Industry

- Coating, Adhesive & Construction Materials Industry

- Market Size & Forecast by Sales Channel

- Direct Producer-to-Industrial Buyer Sales Channel

- Chemical Distributor & Trading Company Channel

- Export & International Trading Channel

- E-Commerce & Digital B2B Platform Channel

- East China Bio-Succinic Acid Market Outlook

- Market Size & Forecast

- By Value

- By Volume (TPA)

- By Production Process

- By Feedstock

- By Purity Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Province

- By Sales Channel

- Market Size & Forecast

- North China Bio-Succinic Acid Market Outlook

- Market Size & Forecast

- By Value

- By Volume (TPA)

- By Production Process

- By Feedstock

- By Purity Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Province

- By Sales Channel

- Market Size & Forecast

- Central & South China Bio-Succinic Acid Market Outlook

- Market Size & Forecast

- By Value

- By Volume (TPA)

- By Production Process

- By Feedstock

- By Purity Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Province

- By Sales Channel

- Market Size & Forecast

- Northeast China Bio-Succinic Acid Market Outlook

- Market Size & Forecast

- By Value

- By Volume (TPA)

- By Production Process

- By Feedstock

- By Purity Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Province

- By Sales Channel

- Market Size & Forecast

- Southwest China Bio-Succinic Acid Market Outlook

- Market Size & Forecast

- By Value

- By Volume (TPA)

- By Production Process

- By Feedstock

- By Purity Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Province

- By Sales Channel

- Market Size & Forecast

- Province-Wise* China Bio-Succinic Acid Market Outlook

- Market Size & Forecast

- By Value

- By Volume (TPA)

- By Production Process

- By Feedstock

- By Purity Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Province

- By Sales Channel

- Market Size & Forecast

- *Provinces & Municipalities Analyzed in the Syllogist China Research Portfolio: Shandong, Jiangsu, Zhejiang, Shanghai, Guangdong, Fujian, Hebei, Henan, Anhui, Hubei, Hunan, Liaoning, Jilin, Sichuan, Chongqing, Inner Mongolia, Xinjiang

- Technology Landscape & Innovation Analysis

- Anaerobic Fermentation Technology Deep-Dive: Metabolic Engineering of E. coli, Glucose Utilisation Efficiency & CO2 Fixation Advances

- Yeast-Based Fermentation Technology: Acid-Tolerant Strain Development, Downstream Simplification & Cost-Reduction Pathway

- Downstream Purification Technology: Crystallisation, Reactive Extraction, Electrodialysis & Membrane Separation for High-Purity BSA

- PBS & Biodegradable Polyester Technology: Succinic Acid-Based Polycondensation, Chain Extension & Property Enhancement

- Electrochemical CO2-to-Succinic Acid Conversion Technology: Catalyst Design, Cell Architecture & Scale-Up in Chinese Research Institutes

- Lignocellulosic Biomass Pretreatment, Hydrolysis & Fermentation Technology for Second-Generation Bio-Succinic Acid Production

- AI & Synthetic Biology-Driven Strain Engineering, Fermentation Optimisation & Process Digital Twin Technology

- Patent & IP Landscape in Bio-Succinic Acid Technologies in China

- Value Chain & Supply Chain Analysis

- Corn, Cassava & Starch Crop Agricultural Feedstock Procurement & Price Dynamics Supply Chain

- Glucose Syrup, Dextrose & Hydrolysate Processing & Supply to Bio-Fermentation Facilities

- Bioreactor, Fermentation Equipment & Downstream Processing Equipment Manufacturing Supply Chain

- Fermentation Microorganism, Culture Media, Enzyme & Process Chemical Supply Chain

- Bio-Succinic Acid Purification, Crystallisation, Drying, Packaging & Logistics Supply Chain

- PBS & Derivative Converter, Downstream Chemical & Polymer Manufacturer Channel

- Domestic Chemical Distributor, Export Trading Company & International Market Channel

- Pricing Analysis

- China Bio-Succinic Acid Spot & Contract Price Analysis by Grade & Volume (RMB/tonne & USD/tonne)

- Bio-Based vs. Petroleum-Derived Succinic Acid Price Parity & Cost Competitiveness Analysis

- Production Cost Breakdown Analysis: Feedstock, Energy, Labour, Depreciation & By-Product Credit

- PBS & Bio-Succinic Acid Derivative Price Premium vs. Conventional Polymer & Chemical Benchmarks

- Export Price & FOB China Price Analysis vs. Global Market Benchmarks

- Price Trend Analysis: Corn Feedstock Price Impact, Scale Economy & Technology Cost Reduction Roadmap

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of China Bio-Succinic Acid: Carbon Footprint, Feedstock GHG Impact & Comparison with Petroleum Route

- CO2 Fixation & Net Carbon Contribution: Role of Anaerobic Fermentation in Carbon Capture & Utilisation (CCU)

- PBS Biodegradability, Compostability & China National Standard GB/T 19811 & GB/T 28018 Compliance

- China Dual Carbon Goals (Carbon Peak by 2030, Carbon Neutrality by 2060) & Bio-Succinic Acid Contribution to Bio-Economy

- Wastewater Treatment, Fermentation By-Product Management & Environmental Compliance for Bio-Succinic Acid Facilities

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Production Process & Region)

- Top 10 Players Market Share in China

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Process Technology, Application & Region

- Player Classification

- Dedicated Domestic Bio-Succinic Acid Producers & Biotechnology Companies

- State-Owned Chemical & Petrochemical Enterprises Developing Bio-Based Routes

- University Spin-Offs, Research Institute-Backed Bio-Manufacturing Startups

- Multinational Bio-Based Chemical Companies with China Production or Import Operations

- Downstream PBS & Biodegradable Polymer Producers with Backward Integration

- Competitive Analysis Frameworks

- Market Share Analysis by Production Process, Application & Region

- Company Profile

- Company Overview & China Headquarters

- Bio-Succinic Acid Products, Production Process & Grade Portfolio

- Key Customer Relationships & Downstream Application Coverage

- China Production Capacity, Plant Location & Utilisation Rate

- Revenue (Bio-Succinic Acid Segment) & Funding/Investment Background

- Technology Differentiators, Proprietary Strains & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansions, Grade Launches, Certification Approvals)

- SWOT Analysis

- Strategic Focus Areas & China Market Roadmap

- Competitive Positioning Map (Production Cost Competitiveness vs. Product Grade Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Production Process, Derivative, Application, End-User & Region

- White Space Opportunity Analysis

- Strategic Recommendations

- Production Process, Strain Development & Technology Investment Strategy for China

- Capacity Expansion, Feedstock Diversification & Manufacturing Excellence Strategy

- Regional Expansion & China Province-Level Market Penetration Strategy

- Downstream Customer, Application Development & End-User Engagement Strategy

- Export Market Entry, International Certification & Global Sales Strategy

- Government Policy Alignment, Subsidy Capture & Dual Carbon Goal Positioning Strategy

- Sustainability, LCA Communication & Green Chemistry Positioning Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output