Global Cumene Market By Production Process, By Application, By End Use Industry, By Grade, By Distribution Channel, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Cumene Market encompasses the production, processing, and commercial supply of isopropylbenzene, commonly known as cumene, manufactured through the Friedel-Crafts alkylation of benzene with propylene over zeolite or phosphoric acid catalysts, serving primarily as an intermediate feedstock for the cumene hydroperoxide process producing phenol and acetone co-products, and secondarily as a specialty solvent, high-octane gasoline blendstock, and chemical intermediate for alpha-methylstyrene, acetophenone, and diisopropylbenzene synthesis across petrochemical, chemical, and refining industries globally.

Market Insights

The global cumene market is fundamentally characterized by its captive feedstock role within the integrated phenol-acetone production value chain, a structural relationship that makes cumene market dynamics inseparable from the demand trajectory of phenol and acetone, the two co-products generated in near-fixed stoichiometric ratio through cumene hydroperoxide oxidation and cleavage, and whose simultaneous demand balance management represents the central commercial challenge for cumene-to-phenol process operators globally. The market was valued at approximately USD 18.4 billion in 2025 and is projected to grow at a compound annual growth rate of 4.1% through 2034, as growing downstream phenol derivative consumption in bisphenol A, polycarbonate, epoxy resins, caprolactam, and phenolic resins across construction, automotive, electronics, and consumer goods industries drives cumene production capacity expansion, while the simultaneous management of acetone co-product demand balance from solvents, methyl methacrylate, and bisphenol A synthesis applications determines the overall commercial viability of cumene-phenol process economics.

Bisphenol A production represents the largest single downstream consumption driver for phenol from the cumene oxidation chain, and the growth trajectory of bisphenol A demand from polycarbonate and epoxy resin manufacturing constitutes the primary commercial justification for new cumene production capacity investment globally. Polycarbonate consumption in automotive glazing, optical disc, electrical and electronic equipment housings, and construction sheet applications is sustaining bisphenol A and phenol demand growth across Asia-Pacific manufacturing markets, with Chinese polycarbonate production capacity expansion particularly significant as China pursues domestic supply self-sufficiency in engineering polymer resins that have historically been imported from Japanese, South Korean, and European producers with established integrated cumene-phenol-bisphenol A-polycarbonate value chains. Epoxy resin production for wind turbine blade composite manufacturing, electronics laminate substrate, automotive adhesive, and infrastructure protective coating applications is providing an additional durable demand vector for bisphenol A and phenol that reinforces the growth case for cumene production capacity investment beyond polycarbonate market dynamics alone.

The zeolite catalyst-based cumene alkylation process has comprehensively displaced legacy phosphoric acid on kieselguhr catalyst technology in most recently constructed and retrofitted cumene production units, delivering superior cumene selectivity, reduced polyalkylbenzene byproduct formation, elimination of acid waste disposal requirements, and improved catalyst regenerability that collectively lower production cost and environmental compliance burden relative to solid phosphoric acid process operation. The integration of cumene production with co-located benzene and propylene supply from naphtha crackers or fluid catalytic cracking operations in refinery-petrochemical complexes provides advantaged feedstock logistics and competitive cost positions for integrated producers relative to standalone cumene manufacturers dependent on merchant benzene and propylene procurement at market prices subject to supply-demand cycle volatility. Process innovation targeting improved meta-diisopropylbenzene and para-diisopropylbenzene transalkylation integration with cumene alkylation is enabling producers to improve cumene yield from benzene feedstock utilization and reduce the undesirable di- and tri-isopropylbenzene byproduct streams that erode feedstock efficiency in alkylation process operations.

Asia-Pacific, led by China, dominates the global cumene market in both production capacity and consumption, reflecting the massive scale of Chinese and broader Asian phenol, bisphenol A, polycarbonate, and epoxy resin manufacturing industries that collectively consume the largest share of globally produced cumene. China’s strategic investment in domestic cumene production capacity, driven by the national priority of achieving self-sufficiency in key petrochemical intermediates and reducing import dependency for phenol and downstream derivatives, has generated substantial capacity additions that are reshaping Asian and global cumene trade flows and competitive economics. North America and Europe represent mature cumene production markets with established refinery-integrated production positions and stable downstream phenol and acetone demand from well-developed derivative manufacturing industries, while the Middle East is developing as an emerging cumene export production hub leveraging low-cost propylene and benzene feedstock advantages from integrated refinery petrochemical complex operations.

Key Drivers

Bisphenol A and Polycarbonate Demand Growth from Automotive, Electronics, and Construction Applications Driving Phenol and Cumene Production Capacity Expansion Globally

The structural growth of bisphenol A consumption for polycarbonate resin production serving automotive glazing lightweighting, consumer electronics housing, optical lens, and construction sheet applications across expanding Asian manufacturing markets is the primary demand driver sustaining cumene production investment, as the stoichiometric relationship between cumene, phenol, and bisphenol A in the integrated production chain means that every unit of polycarbonate capacity expansion requires a corresponding expansion of cumene processing through the cumene hydroperoxide oxidation pathway. Chinese domestic polycarbonate capacity expansion programs reducing import dependency, combined with growing epoxy resin consumption from wind energy composite and electronics applications, are collectively providing sustained long-term downstream pull for phenol and consequently cumene production investment across Asian and globally integrated petrochemical complexes.

Integrated Refinery-Petrochemical Complex Development Providing Advantaged Benzene and Propylene Feedstock Economics That Support Competitive Cumene Production Cost Positions

The strategic development of deeply integrated refinery-petrochemical complexes in China, the Middle East, and India that maximize chemical yield from crude oil processing while co-producing benzene from catalytic reformate and propylene from fluid catalytic cracking operations provides co-located cumene alkylation plants with feedstock cost advantages through captive internal transfer pricing of benzene and propylene that avoids merchant market price volatility exposure and logistics cost premiums applicable to standalone cumene producers purchasing feedstocks from external suppliers. The integration of cumene production within these large complexes also enables shared infrastructure, utilities, and logistics cost amortization that improve overall production cost competitiveness relative to independently operated alkylation plants whose fixed cost structures cannot achieve equivalent per-unit efficiency at similar production scales.

Caprolactam and Nylon-6 Demand Growth from Automotive Lightweighting and Textile Applications Supporting Phenol Derivatives Demand Chain That Underpins Cumene Market Expansion

Phenol serves as the entry point for multiple high-growth chemical derivative chains beyond bisphenol A, with cyclohexanone and cyclohexanol produced from phenol hydrogenation serving as key intermediates for caprolactam production used in nylon-6 fiber and engineering resin manufacturing for automotive structural components, tire cord reinforcement, textile apparel, and industrial filtration applications whose aggregate consumption growth provides additional durable demand support for the phenol and cumene production chain that reduces dependence on bisphenol A and polycarbonate market cycles alone. Phenolic resin production for automotive brake pads, abrasive bonding agents, wood composite adhesives, and electrical insulation laminates provides a further established and structurally stable phenol consumption channel that contributes cumene demand underpinning across multiple industrial end use categories.

Key Challenges

Acetone Co-Product Demand Imbalance Risk and the Structural Challenge of Managing Stoichiometrically Linked Phenol and Acetone Production Economics in Volatile Derivative Markets

The cumene hydroperoxide process produces phenol and acetone in a near-fixed molar ratio of approximately one to one by mass, creating a structural co-product marketing challenge for cumene-to-phenol producers who must simultaneously find commercially acceptable demand for both products regardless of the relative demand trajectories of phenol and acetone derivative markets in any given period. When acetone demand weakens relative to phenol demand growth, acetone prices decline, reducing the effective economic credit available to cumene process economics for acetone co-product sales and potentially requiring producers to accept below-cost acetone pricing to maintain production rates driven by phenol demand obligations, creating margin compression that cannot be avoided without reducing cumene throughput below phenol contract supply commitments.

Bisphenol A Regulatory Scrutiny and Potential Demand Substitution Under Endocrine Disruptor Concerns Creating Long-Term Demand Uncertainty for the Primary Phenol Derivative Market

Bisphenol A, the largest single end use application for phenol from the cumene chain, has been subject to growing regulatory scrutiny in the European Union, United States, Canada, and other markets under concerns about its endocrine disrupting properties at low exposure levels, resulting in restrictions on bisphenol A use in food contact materials, infant feeding products, and certain consumer goods that have moderated polycarbonate demand in regulated applications and incentivized material substitution development by downstream plastic producers seeking to develop bisphenol A-free polycarbonate alternatives. The longer-term trajectory of bisphenol A regulatory restriction expansion across additional product categories and jurisdictions introduces structural demand uncertainty into the primary phenol application market that creates investment planning risk for cumene production capacity expansion decisions predicated on multi-decade bisphenol A demand growth assumptions.

Benzene and Propylene Feedstock Price Volatility and Supply Chain Exposure Creating Production Cost Uncertainty for Merchant Cumene Producers Without Integrated Feedstock Supply

Cumene production economics for merchant producers without integrated benzene and propylene supply are directly exposed to the price volatility of both aromatic and olefin feedstock markets, whose prices are governed by different supply-demand dynamics including naphtha cracker run rates and pyrolysis gasoline production for benzene supply and refinery fluid catalytic cracker operations and propane dehydrogenation capacity for propylene supply, creating a production cost sensitivity to the relative movements of two feedstocks whose price relationship can shift unpredictably with petrochemical supply cycle dynamics. Periods of simultaneous benzene and propylene price elevation resulting from concurrent aromatics market tightness and propylene supply constraints create particular margin compression risk for standalone cumene producers unable to hedge feedstock exposure through integrated captive supply arrangements.

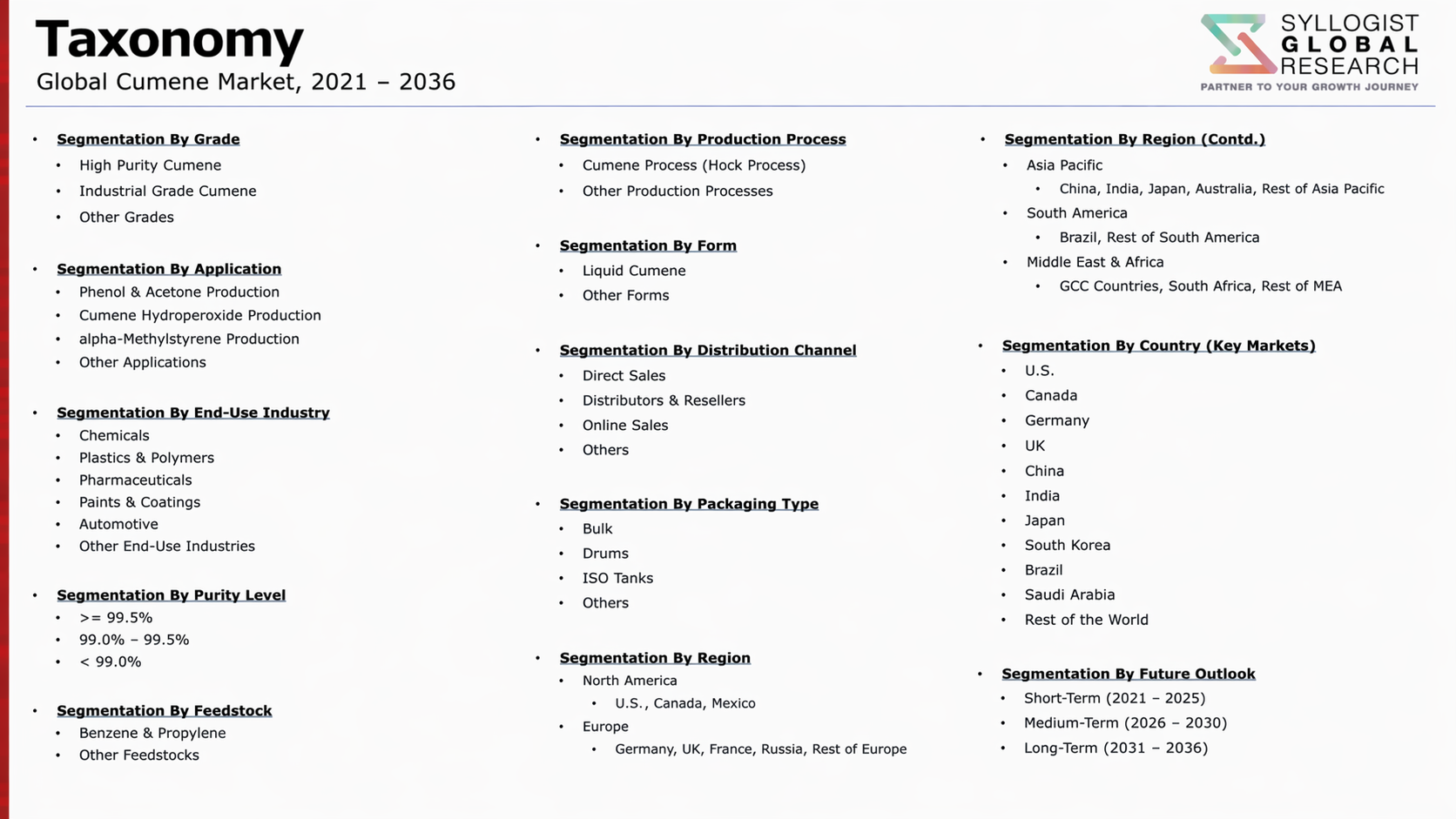

Market Segmentation

- Segmentation By Production Process

- Zeolite Catalyst Alkylation (UOP, Dow-Kellogg, and EBMax Processes)

- Solid Phosphoric Acid Catalyst Alkylation

- AlCl3 Friedel-Crafts Alkylation

- Others

- Segmentation By Application

- Phenol and Acetone Production via Cumene Hydroperoxide Oxidation

- Alpha-Methylstyrene Production

- Diisopropylbenzene and Specialty Aromatic Synthesis

- High-Octane Gasoline Blendstock

- Industrial Solvent Applications

- Acetophenone and Fine Chemical Synthesis

- Others

- Segmentation By End Use Industry

- Polycarbonate and Bisphenol A Manufacturing

- Epoxy Resin and Curing Agent Production

- Caprolactam and Nylon-6 Manufacturing

- Phenolic Resins and Adhesives

- Acetone Derivatives and Solvents

- Pharmaceutical and Fine Chemicals

- Refining and Petrochemical Processing

- Others

- Segmentation By Grade

- Commercial Grade Cumene (99%+ Purity)

- High-Purity Cumene for Specialty Applications

- Technical Grade Cumene for Fuel Blending

- Segmentation By Distribution Channel

- Captive Integrated Production and Internal Transfer

- Long-Term Supply Contracts with Derivative Producers

- Spot Market and Commodity Chemical Trading

- Chemical Distributors and Brokers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global cumene market valuation in 2025, projected through 2034, segmented by production process, application, and end use industry, enabling cumene producers, phenol and bisphenol A manufacturers, and petrochemical investors to identify the highest-growth downstream demand drivers and most strategically significant production capacity investment opportunities across the integrated cumene value chain?

- How are bisphenol A demand growth trajectories for polycarbonate and epoxy resin manufacturing in China and broader Asia-Pacific, combined with caprolactam and phenolic resin consumption expansion, collectively shaping the long-term phenol and cumene production capacity investment case, and what downstream application growth rates and geographic demand distribution shifts are most materially influencing cumene market outlook through 2034?

- How are integrated refinery-petrochemical complex developments in China, the Middle East, and India reshaping the competitive economics and production geography of global cumene supply, and what captive benzene and propylene feedstock cost advantages, shared infrastructure efficiency benefits, and export market positioning strategies are enabling these integrated producers to compete against established North American and European cumene suppliers?

- How is the cumene hydroperoxide process acetone co-product demand imbalance challenge being managed by leading phenol producers across different regional markets, and what acetone derivative growth in methyl methacrylate, bisphenol A synthesis, acetone cyanohydrin, and solvent applications is determining the co-product value contribution to cumene-phenol process economics under varying market conditions through 2034?

- What bisphenol A regulatory restriction trajectories in food contact, consumer goods, and healthcare applications across the European Union, North America, and Asia-Pacific are most significantly creating polycarbonate demand uncertainty, and how are cumene and phenol producers incorporating bisphenol A regulatory risk into long-term capacity investment planning, derivative market diversification strategies, and downstream application development programs?

- How is the competitive landscape structured among global integrated cumene-phenol-bisphenol A producers, merchant cumene suppliers, and regional phenol derivative manufacturers, and what backward integration strategies, zeolite alkylation technology licensing, production scale economies, and long-term feedstock supply security arrangements are enabling leading players to sustain competitive cost positions and customer supply relationship stability?

- Which regional cumene markets, specifically Asia-Pacific, the Middle East, and North America, are expected to generate the most significant production capacity additions and demand growth through 2034, and what combinations of domestic phenol and derivative self-sufficiency policy ambitions, integrated complex investment programs, import substitution dynamics, and downstream polycarbonate and epoxy resin manufacturing expansions are defining production investment and trade flow trajectories?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Benzene & Propylene Feedstock Price Volatility & Alkylation Margin Compression Risk

- Phenol & Acetone Demand Cyclicality, Capacity Overhang & Downstream Margin Squeeze Risk

- Cumene Hydroperoxide (CHP) Explosion Hazard, Process Safety & Regulatory Liability Risk

- Geopolitical Trade Disruption, Benzene Supply Route Risk & Tariff Escalation Risk

- Energy Transition, Long-Term Bisphenol A (BPA) & Polycarbonate Demand Erosion Risk

- Technology Substitution: Alternative Phenol & Acetone Production Routes & Bio-Based Cumene Risk

- Regulatory Framework & Standards

- REACH, TSCA & Global Chemical Registration, Evaluation & Authorisation Standards for Cumene

- IARC Group 2B Classification, Occupational Exposure Limits (OEL) & Cumene Carcinogenicity Regulatory Standards

- Seveso III, OSHA PSM & Process Hazard Analysis (PHA) Standards for Cumene Hydroperoxide (CHP) Handling Facilities

- VOC Emission Standards, Benzene Fugitive Emission Control & Air Quality Regulatory Frameworks for Cumene Plants

- EU Bisphenol A (BPA) Restrictions, Food Contact Material Standards & Downstream Demand Regulatory Impact

- Fuel Blending Standards: EN 228, ASTM D4814 & Octane Blending Regulatory Frameworks for Gasoline-Grade Cumene

- Global Cumene Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes per Annum, MTPA)

- Market Size & Forecast by Production Process

- Zeolite-Based Solid Acid Alkylation (UOP Q-Max, Lummus EBMax & CDCumene Process)

- Phosphoric Acid on Kieselguhr (SPA) Solid Phosphoric Acid Cumene Process

- AlCl3 & Lewis Acid Catalysed Friedel-Crafts Alkylation Process

- Transalkylation of Di-Isopropylbenzene (DIPB) & Heavy Alkylate Recycle Route

- Market Size & Forecast by Feedstock

- Refinery-Grade Benzene & High-Purity Benzene Feedstock

- Polymer-Grade Propylene & Refinery-Grade Propylene Feedstock

- Crude Propylene & Propane Dehydrogenation (PDH)-Derived Propylene Feedstock

- Market Size & Forecast by Grade

- Chemical Grade Cumene (Phenol-Grade, High Purity for CHP Oxidation)

- Fuel & Gasoline Blending Grade Cumene

- Solvent & Industrial Grade Cumene

- Market Size & Forecast by Derivative & Downstream Application

- Phenol via Cumene-Phenol (Hock) Process

- Acetone via Cumene-Phenol (Hock) Process Co-Production

- Alpha-Methylstyrene (AMS) from Cumene Oxidation By-Product

- Cumene Hydroperoxide (CHP) as Propylene Oxide & Other Co-Product Route

- Gasoline Octane Blending (High Octane Blend Component)

- Solvent, Thinner & Industrial Chemical Applications

- Market Size & Forecast by End-User Industry

- Phenol-Formaldehyde Resin, Phenolic Laminate & Adhesive Industry

- Bisphenol A (BPA) & Polycarbonate (PC) Resin Industry

- Epoxy Resin & Epichlorohydrin Industry

- Caprolactam & Nylon 6 Fibre Industry

- Acetone Solvent & Methyl Methacrylate (MMA) Industry

- Fuel Blending & Petroleum Refining Industry

- Specialty Chemical, Pharmaceutical & Fragrance Industry

- Market Size & Forecast by Sales Channel

- Integrated Producer Self-Supply & Intra-Company Transfer Channel

- Long-Term Bilateral Contract & Offtake Agreement Channel

- Spot & Short-Term Trading Channel

- Commodity Trader, Broker & Chemical Distributor Channel

- North America Cumene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Cumene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Cumene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Cumene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Cumene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Cumene Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Production Process

- By Feedstock

- By Grade

- By Derivative & Downstream Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Belgium, Spain, Italy, Poland, China, Japan, South Korea, India, Singapore, Thailand, Taiwan, Malaysia, Iran, Saudi Arabia, UAE, Kuwait, Qatar, South Africa, Brazil

- Technology Landscape & Innovation Analysis

- Zeolite Alkylation Technology Deep-Dive: UOP Q-Max Beta Zeolite, MCM-22 Catalyst, Selectivity & Yield vs. SPA Process Comparison

- Transalkylation Technology: DIPB & Heavy Alkylate Recycle, Separate Transalkylation Reactor Design & Cumene Selectivity Optimisation

- Cumene Hydroperoxide (CHP) Oxidation & Cleavage Technology: Reactor Design, Safety Systems & Selectivity for Phenol-Acetone Production

- Propylene Supply Flexibility Technology: On-Purpose PDH Integration, Refinery-Grade vs. Polymer-Grade Propylene Feed Qualification

- Bio-Cumene & Bio-Phenol Pathway Technology: p-Cymene Bioconversion, Bio-Isopropylbenzene Routes & Circular Feedstock Development

- Alpha-Methylstyrene (AMS) Recovery & Purification Technology: Hydrogenation vs. Recovery Options & Value Chain Optimisation

- Digital Twin, APC & AI-Based Process Optimisation Technology for Cumene Alkylation & Phenol Plant Operations

- Patent & IP Landscape in Cumene Production & Processing Technologies

- Value Chain & Supply Chain Analysis

- Benzene Feedstock: Naphtha Reformate, Pygas Extraction & Hydrodealkylation Supply Chain

- Propylene Feedstock: Steam Cracker, FCC, PDH & Refinery-Grade Propylene Supply Chain

- Zeolite Catalyst, SPA Catalyst & Process Chemical Supply Chain for Cumene Alkylation

- Cumene Storage, Blending, Terminal Logistics & Marine Transportation Supply Chain

- Integrated Cumene-Phenol-Acetone Complex Design & Plant Engineering Supply Chain

- Phenol, Acetone & AMS Downstream Derivative Manufacturing Supply Chain

- Commodity Trader, Chemical Distributor & Industrial Offtaker Channel

- Pricing Analysis

- Global Cumene Benchmark Price Analysis: FOB Korea, CFR China & FD NWE Price Benchmarking

- Benzene-to-Cumene & Propylene-to-Cumene Alkylation Margin Analysis

- Cumene-to-Phenol & Cumene-to-Acetone Conversion Margin & Net Back Value Analysis

- Cumene vs. Gasoline Blending Value Parity & Opportunity Cost Analysis

- Regional Cumene Price Differential Analysis: Asia-Pacific vs. Europe vs. US Gulf Coast

- Price Cycle Analysis: Historical Cumene Margin Cycles, Benzene Availability & Phenol Demand Impact

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Cumene & Cumene-Phenol-Acetone Chain: Carbon Footprint, Energy Intensity & GHG Emissions

- Process Safety & Risk Management: CHP Explosion Hazard, HAZOP & Inherently Safer Design for Cumene Oxidation

- EU BPA Regulation, Endocrine Disruptor Classification & Long-Term Impact on Bisphenol A Demand from Cumene

- Decarbonisation of Cumene-Phenol Production: Green Hydrogen, Electrification & CCS Integration Pathways

- Bio-Based Cumene & Circular Phenol: Biomass-Derived Feedstock, Bio-Content Certification & ESG Value Proposition

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Region)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Production Process, Geography & Value Chain Integration

- Player Classification

- Integrated Refinery-Petrochemical Majors with Cumene & Phenol Complex Operations

- Dedicated Cumene & Phenol-Acetone Plant Operators

- State-Owned & National Oil Company Cumene Producers

- Independent Cumene Merchants, Traders & Blending Companies

- Technology Licensors (UOP, Lummus, CDTECH & Exxon) Providing Cumene Process Technology

- Competitive Analysis Frameworks

- Market Share Analysis by Region & Value Chain Integration

- Company Profile

- Company Overview & Headquarters

- Cumene & Cumene-Derived Products Portfolio & Production Process

- Key Customer Relationships & Offtake Agreements

- Manufacturing Footprint, Cumene Capacity (MTPA) & Plant Locations

- Revenue (Cumene & Phenol-Acetone Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansions, Technology Upgrades, Market Moves)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Feedstock Integration Depth vs. Derivative Value Chain Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Production Process, Derivative, End-User Industry & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Production Process, Catalyst Technology & Yield Optimisation Strategy

- Feedstock Flexibility, Integration & Procurement Strategy

- Geographic Expansion & Market Penetration Strategy

- Downstream Derivative, Customer & Offtake Partner Engagement Strategy

- Partnership, M&A & Petrochemical Ecosystem Strategy

- Sustainability, Decarbonisation & Bio-Based Transition Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output