Global PET Resin Market By Grade, By Application, By End Use Industry, By Production Process, By Recycled Content, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global PET Resin Market encompasses the production, processing, and commercial distribution of polyethylene terephthalate thermoplastic polyester resin manufactured through the polycondensation of purified terephthalic acid and monoethylene glycol, available in bottle-grade, fiber-grade, film-grade, and specialty formulations, serving packaging, textile fiber, engineering film, and technical end use applications across beverage, food, personal care, pharmaceutical, consumer goods, automotive, and industrial markets globally, including both virgin PET resin and resin incorporating chemically or mechanically recycled polyester content.

Market Insights

The global PET resin market is navigating a complex commercial environment that simultaneously presents structural long-term demand growth from developing economy packaging and consumer goods expansion, increasing regulatory and brand owner pressure to incorporate recycled content that is reshaping supply chain economics, and persistent capacity surplus conditions in certain regional markets that are compressing commodity grade margins and intensifying competitive dynamics among the largest integrated PTA-PET producers. The market was valued at approximately USD 72.4 billion in 2025 and is projected to grow at a compound annual growth rate of 4.6% through 2034, as sustained growth in beverage and water bottle packaging consumption across Asia, Africa, and the Middle East, expanding food and household product PET packaging adoption, and growing recycled PET content demand from brand owner sustainability commitments collectively maintain positive volume growth trajectory despite the packaging sustainability policy headwinds affecting PET bottle volumes in European and certain North American markets.

Bottle-grade PET resin retains its position as the largest volume application segment globally, underpinned by PET’s unmatched combination of clarity, lightweight structure, barrier properties for carbonated beverage carbon dioxide retention, recyclability through well-established mechanical recycling infrastructure, and competitive production economics that collectively sustain PET’s dominant position in single-serve and multi-serve beverage packaging formats against competitive challenges from aluminum cans, glass bottles, and emerging alternative packaging materials. The per capita PET bottle consumption growth trajectory in South and Southeast Asia, sub-Saharan Africa, and the Middle East remains strongly positive, driven by rising bottled water consumption associated with income growth and urban water quality concerns, expanding ready-to-drink beverage market development, and the progressive displacement of refillable glass bottle formats by PET packaging in markets transitioning toward modern retail-compatible one-way packaging formats. Textile fiber represents the second largest PET resin application by volume, with polyester staple fiber and filament yarn production in China and broader Asia-Pacific consuming the largest absolute volume of fiber-grade PET resin, driven by apparel, home textile, technical textile, and nonwoven fabric demand growth across global markets.

The recycled PET segment is undergoing the most structurally significant commercial transformation within the global PET resin market, as mandatory recycled content legislation, brand owner voluntary targets, and extended producer responsibility frameworks across the European Union, United Kingdom, and a growing number of additional jurisdictions create regulated demand for food-contact-approved recycled PET content in bottle and food packaging applications that is generating investment in both mechanical recycling collection and sorting infrastructure expansion and chemical recycling depolymerization technologies capable of producing food-grade recycled PET meeting the purity specifications of beverage packaging regulatory frameworks. The economics of recycled PET supply are currently challenged by the price premium of certified food-grade recycled PET relative to virgin resin at current oil-derived raw material prices, creating a structural economic gap that mandatory content regulations and recycled content certificate market development are progressively bridging through compliance-driven demand that is independent of relative price economics between virgin and recycled resin. Specialty PET grades including high intrinsic viscosity PET for engineering film, heat-set bottle grades for hot-fill beverage applications, oxygen barrier nanocomposite PET for juice and beer packaging, and copolymer glycol-modified PET for premium rigid packaging are generating growing revenue streams for technically differentiated producers able to command specialty grade premiums above commodity bottle resin benchmark pricing.

Asia-Pacific, led by China, dominates global PET resin production capacity and consumption, reflecting the concentration of integrated PTA-PET manufacturing complexes across China, India, South Korea, Taiwan, and Indonesia that collectively account for the majority of globally installed PET resin production capacity. China’s domestic PET resin production, while primarily serving its own large domestic packaging and fiber markets, also generates export volumes that flow to regional and international markets during periods of domestic demand softness or inventory accumulation, influencing global benchmark pricing and creating competitive pressure for non-Chinese producers. India is the fastest-growing major national PET resin market, driven by rising bottled water and carbonated soft drink consumption, expanding packaged food adoption, and growing pharmaceutical and personal care PET container usage among India’s expanding middle-class consumer population. North America and Europe are mature PET markets where bottle recycling rate improvement, mandatory recycled content compliance investment, and premium specialty grade development represent the primary market development drivers against a backdrop of flat to modestly declining per capita virgin PET packaging consumption.

Key Drivers

Developing Economy Beverage, Bottled Water, and Packaged Food Consumption Growth Sustaining Structural PET Resin Volume Demand Expansion Across Asia, Africa, and Latin America

Rising per capita incomes, urbanization, and the expansion of modern retail distribution across South and Southeast Asia, sub-Saharan Africa, the Middle East, and Latin America are driving robust and durable growth in bottled water, carbonated beverages, ready-to-drink tea and juice, and packaged food product consumption, all of which extensively utilize PET bottle, jar, and tray packaging formats that sustain growing virgin PET resin demand independent of the sustainability-driven demand moderation visible in established European and North American PET markets. The absence of viable alternative packaging materials at competitive cost and performance levels for high-volume still and carbonated beverage packaging in these high-growth markets ensures that PET volume growth momentum in developing economy consumer markets substantially outpaces the demand erosion from sustainability substitution in mature markets.

Mandatory Recycled Content Legislation and Brand Owner Sustainability Commitments Creating Regulated Demand Pull for Food-Grade Recycled PET Supply Across European and Global Packaging Markets

The European Union Single Use Plastics Directive mandate requiring a minimum twenty-five percent recycled plastic content in PET beverage bottles from 2025 and thirty percent from 2030, complemented by national packaging recycled content taxes, extended producer responsibility financial incentives for recycled content inclusion, and voluntary brand owner commitments from major beverage and consumer goods corporations to incorporate recycled PET content across their packaging portfolios, is creating a compliance-driven demand base for food-grade recycled PET that is generating sustained capital investment in collection infrastructure, sorting technology, mechanical recycling capacity, and chemical recycling depolymerization plants that collectively expand recycled PET supply at rates aligned with growing regulatory content requirements.

PET Packaging Lightweighting Innovation and Material Efficiency Improvement Extending Per-Unit Resin Competitiveness While Expanding Addressable Packaging Application Coverage

Continuous innovation in PET bottle preform design, blow molding process optimization, and resin molecular weight distribution engineering is enabling progressive reduction in bottle wall thickness and per-container resin weight without compromising performance specifications for pressure retention, drop impact resistance, and barrier properties, improving the competitive cost economics of PET packaging relative to alternative materials and sustaining PET’s commercial viability against sustainability-motivated material substitution challenges by demonstrating measurable material use reduction progress that satisfies brand owner and regulatory sustainability performance expectations. Advances in specialty PET barrier technologies including oxygen scavenger incorporation, passive barrier copolymer formulation, and active barrier coatings are simultaneously expanding PET’s addressable packaging application coverage into sensitive food, juice, beer, and pharmaceutical packaging formats previously requiring more expensive multilayer packaging solutions.

Key Challenges

Chronic Global PET Resin Capacity Surplus and Commodity Grade Margin Compression Creating Challenging Return on Capital Conditions for Commodity Bottle Resin Producers

The global PET resin production capacity base, built out through successive investment cycles driven by demand growth expectations and national self-sufficiency objectives in major producing economies, has periodically generated structural excess capacity conditions that compress commodity bottle grade PET resin margins below the levels required to justify new investment and challenge the financial viability of high-cost legacy production assets unable to achieve the operating cost efficiency of modern large-scale integrated PTA-PET complexes. Chinese PET capacity expansion in particular has created export surplus conditions that depress benchmark pricing in regional Asian and global spot markets during periods of domestic demand softness, creating persistent margin pressure for non-Chinese commodity PET producers whose production cost positions are less competitive than integrated Chinese complexes with access to captive PTA supply.

Single-Use Plastic Regulation, Packaging Sustainability Policy Pressure, and Material Substitution Risk Constraining Bottle-Grade PET Demand Growth in Key Developed Market Economies

Extended producer responsibility legislation, deposit return scheme implementation that affects PET bottle format economics, packaging minimization regulations, and the active pursuit of reusable packaging alternatives by brand owners responding to consumer and regulatory sustainability pressure are collectively moderating virgin bottle-grade PET demand growth in European and progressively other developed market packaging economies, creating strategic market development uncertainty for PET resin producers whose long-term capacity investment assumptions were predicated on continued per capita bottle consumption growth trajectories that sustainability policy frameworks are interrupting. The proliferation of regulatory approaches across national and subnational jurisdictions creates compliance complexity for multinational packaging operators managing PET material specifications and recycled content compliance across multiple market requirements simultaneously.

Recycled PET Cost Premium, Food-Grade Certification Complexity, and Chemical Recycling Scale-Up Challenges Limiting the Pace of Recycled Content Integration in PET Packaging Supply Chains

Certified food-contact-approved recycled PET currently commands a significant price premium over virgin PET resin at prevailing petrochemical raw material prices, creating a structural cost increase for packaging producers incorporating mandatory or voluntary recycled content at specifications required for food and beverage contact regulatory clearance that compresses converter margins and limits the financial incentive for recycled content integration beyond minimum regulatory compliance requirements. The rigorous food safety assessment process required for novel recycled PET sources and chemical recycling-derived PET under European Food Safety Authority and other regulatory agency frameworks extends qualification timelines and adds regulatory development cost that constrains the pace at which new recycling technologies and supply sources can contribute to meeting growing recycled content demand obligations.

Market Segmentation

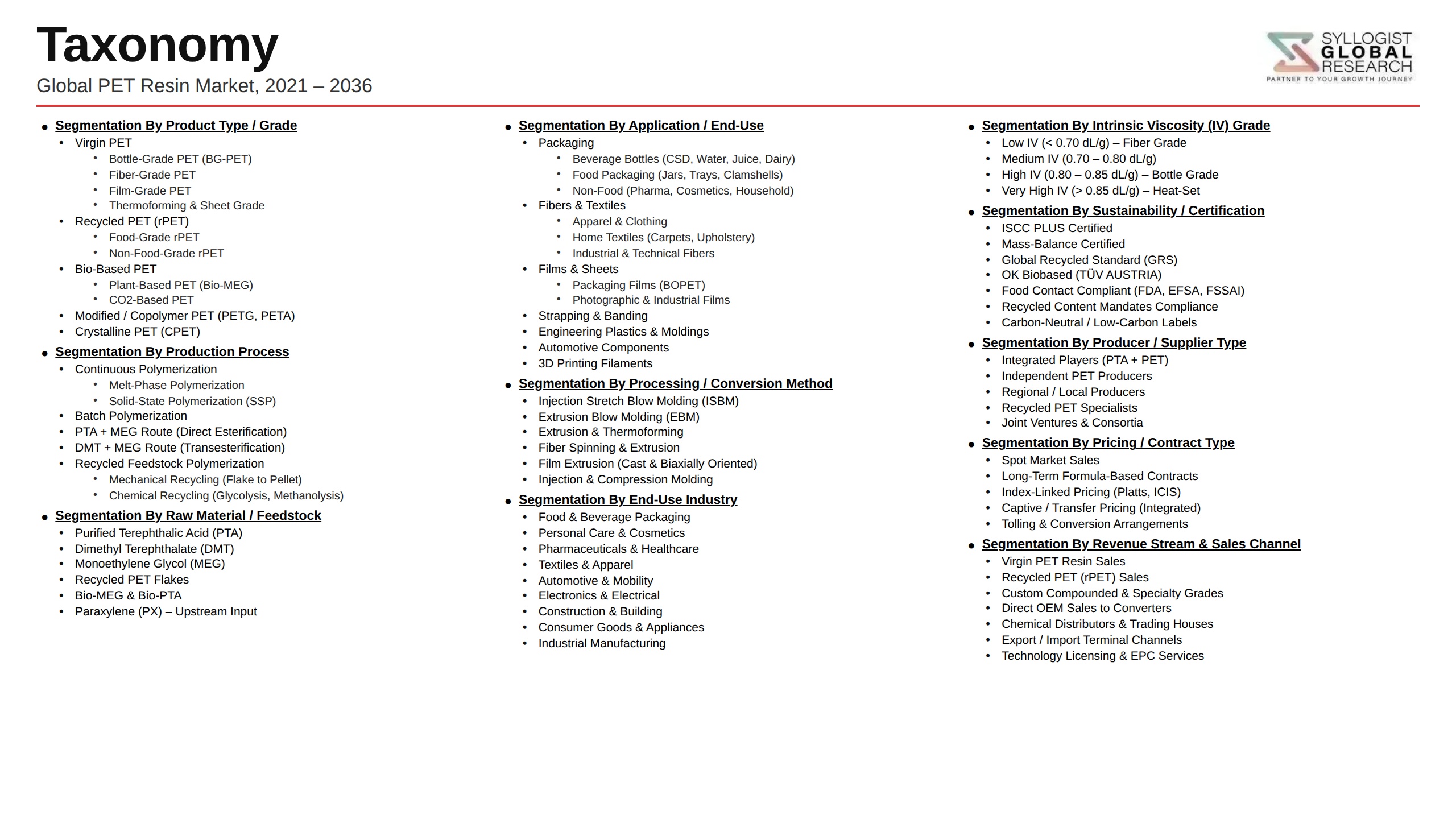

- Segmentation By Grade

- Bottle-Grade PET Resin

- Fiber-Grade PET Resin

- Film-Grade PET Resin

- Engineering and Specialty Grade PET

- Food Packaging and Hot-Fill Grade PET

- Others

- Segmentation By Application

- Beverage Bottles (Water, CSD, Juice, Ready-to-Drink)

- Food Packaging (Trays, Jars, and Containers)

- Polyester Fiber and Yarn

- Biaxially Oriented PET Film

- Pharmaceutical and Personal Care Packaging

- Automotive and Technical Components

- Others

- Segmentation By End Use Industry

- Beverages and Bottled Water

- Food Processing and Packaging

- Textile and Apparel

- Pharmaceutical and Healthcare

- Personal Care and Household Products

- Electrical and Electronics

- Automotive and Transportation

- Others

- Segmentation By Production Process

- Continuous Polymerization (CP) Process

- Batch and Semi-Batch Polycondensation

- Solid-State Polymerization for High IV Grades

- Integrated PTA-to-PET Complex Production

- Segmentation By Recycled Content

- Virgin PET Resin (0% Recycled Content)

- Partially Recycled PET (Below 30% rPET Content)

- High Recycled Content PET (30% to 70% rPET)

- Fully Recycled and Closed-Loop rPET Resin

- Chemically Recycled and Depolymerized PET

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global PET resin market valuation in 2025, projected through 2034, segmented by grade, application, and end use industry, enabling PET resin producers, packaging converters, and chemical investors to identify the highest-growth product categories, most commercially significant regional demand expansion opportunities, and most strategically important recycled content integration trends across the global PET value chain?

- How are European Union recycled content mandates, national packaging taxes, extended producer responsibility frameworks, and major brand owner voluntary recycled PET commitments collectively creating food-grade recycled PET supply and demand economics, and what mechanical recycling capacity expansion, chemical recycling technology scale-up investment, and certification program developments are required to fulfill growing mandatory content obligations through 2034?

- Which developing economy PET consumption markets, specifically India, Southeast Asia, sub-Saharan Africa, and the Middle East, are expected to generate the highest absolute volume demand growth through 2034, and what combinations of bottled water consumption per capita growth, packaged food adoption, pharmaceutical packaging expansion, and modern retail penetration are driving PET bottle and container demand trajectories in these high-growth regional markets?

- How is the competitive landscape structured among global integrated PTA-PET producers, regional commodity PET resin manufacturers, and specialty grade PET developers, and what production scale advantages, PTA feedstock integration economics, specialty grade premiums, recycled content supply chain positioning, and geographic market proximity strategies are enabling leading PET producers to sustain competitive returns in an environment of persistent capacity surplus pressure?

- What single-use plastic regulation trajectories, deposit return scheme implementations, reusable packaging mandates, and material substitution competitive threats from aluminum, glass, and alternative packaging formats are most significantly affecting bottle-grade PET demand trajectories in European, North American, and progressively other developed market packaging economies, and how are PET industry participants responding through recycled content integration, lightweighting innovation, and packaging format diversification?

- How are chemical recycling depolymerization technologies including glycolysis, methanolysis, and hydrolysis-based PET depolymerization progressing toward commercial scale, food-contact regulatory approval, and cost-competitive operation relative to mechanical recycling and virgin production, and what investment timelines, capacity scale milestones, and regulatory framework developments are required for chemical recycling to contribute meaningfully to global recycled PET supply through 2034?

- What specialty PET grade innovation in oxygen barrier properties, high-temperature hot-fill performance, UV protection, lightweighting, and mono-material recyclable packaging designs is expanding PET’s addressable application coverage into premium food, juice, beer, pharmaceutical, and personal care packaging formats, and how are these specialty grade developments enabling PET producers to capture value-added margin opportunities beyond commodity bottle resin benchmark pricing dynamics?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- PTA & MEG Feedstock Price Volatility & Polymerisation Margin Compression Risk

- Capacity Oversupply, New Capacity Wave & Prolonged Margin Downturn Risk

- Plastics Regulation, Single-Use PET Bottle Ban & Extended Producer Responsibility (EPR) Demand Erosion Risk

- Substitution Risk from Aluminium, Glass, Multilayer Pouches & Other Packaging Formats

- rPET Mandates, Recycled Content Obligations & Feedstock Competition Risk for Virgin PET

- Geopolitical Trade Disruption, Anti-Dumping Duties & Market Access Risk

- Regulatory Framework & Standards

- EU Packaging & Packaging Waste Regulation (PPWR), 25% rPET Mandatory Content by 2025 & 30% by 2030 for Beverage Bottles

- FDA 21 CFR 177.1630, EU Regulation 10/2011 & Global Food Contact PET Safety & Migration Standards

- Extended Producer Responsibility (EPR) Schemes, Deposit Return Systems (DRS) & PET Bottle Collection Regulatory Frameworks

- ISO 15270, EN 15343 & Recycled PET Quality, Traceability & Food-Grade Recyclate Standards

- UN Global Plastics Treaty, National Single-Use Plastics Bans & PET Beverage Container Regulatory Frameworks by Jurisdiction

- REACH, RoHS & Restricted Substance Standards for PET Resin Additives, Colorants & Stabilisers

- Global PET Resin Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes per Annum, MTPA)

- Market Size & Forecast by PET Type

- Bottle-Grade PET Resin (Homopolymer & Copolymer)

- Fibre-Grade PET Resin (Standard & High-Tenacity)

- Film-Grade PET Resin (BOPET & Technical Film Grade)

- Engineering-Grade PET Resin (Filled, Reinforced & Specialty)

- Recycled PET (rPET) Resin (Mechanical & Chemical Recycle)

- Bio-Based PET Resin (Partially Bio-Based & Fully Bio-Based)

- Market Size & Forecast by Production Process

- Continuous Polycondensation (CP) Process

- Batch Polycondensation Process

- Solid-State Polymerisation (SSP) for High-IV Bottle-Grade PET

- PTA Direct Esterification Route

- DMT Transesterification Route

- Chemical Recycling: Glycolysis, Methanolysis & Hydrolysis for rPET Production

- Market Size & Forecast by Feedstock

- Purified Terephthalic Acid (PTA) Feedstock

- Monoethylene Glycol (MEG) Feedstock

- Dimethyl Terephthalate (DMT) Feedstock

- Isophthalic Acid (IPA) & Diethylene Glycol (DEG) Comonomer Feedstock

- Post-Consumer PET Flake & Pellet Recycled Feedstock

- Market Size & Forecast by Intrinsic Viscosity (IV)

- Low IV PET Resin (Below 0.60 dl/g – Fibre & Staple Grade)

- Medium IV PET Resin (0.60 to 0.75 dl/g – Film & Sheet Grade)

- High IV PET Resin (0.76 to 0.84 dl/g – Standard Bottle Grade)

- Very High IV PET Resin (Above 0.84 dl/g – Hot-Fill & High-Performance Bottle Grade)

- Market Size & Forecast by Application

- Beverage Bottles (CSD, Water, Juice, Beer & Hot-Fill)

- Food & Edible Oil Containers & Trays

- Non-Food Containers (Personal Care, Household Chemical & Pharmaceutical)

- Polyester Textile Fibre & Apparel

- Industrial & Technical Polyester Fibre (Non-Woven, Filling & Geotextile)

- Biaxially-Oriented PET (BOPET) Film for Packaging, Electronics & Solar

- Engineering & Injection Moulded PET Components

- Strapping, Monofilament & Technical Applications

- Market Size & Forecast by End-User Industry

- Beverage & Bottled Water Industry

- Food Packaging & Food Processing Industry

- Textile, Apparel & Fashion Industry

- Personal Care, Pharmaceutical & Household Products Packaging Industry

- Electronics, Electrical & Solar Panel Industry

- Automotive & Engineering Plastics Industry

- Market Size & Forecast by Sales Channel

- Direct Producer-to-Converter Bilateral Contract Channel

- Commodity Trader, Broker & Spot Market Channel

- Distributor & Regional Merchant Channel

- Online & Digital B2B Procurement Platform Channel

- North America PET Resin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By PET Type

- By Production Process

- By Feedstock

- By Intrinsic Viscosity (IV)

- By Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe PET Resin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By PET Type

- By Production Process

- By Feedstock

- By Intrinsic Viscosity (IV)

- By Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific PET Resin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By PET Type

- By Production Process

- By Feedstock

- By Intrinsic Viscosity (IV)

- By Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America PET Resin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By PET Type

- By Production Process

- By Feedstock

- By Intrinsic Viscosity (IV)

- By Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa PET Resin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By PET Type

- By Production Process

- By Feedstock

- By Intrinsic Viscosity (IV)

- By Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* PET Resin Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By PET Type

- By Production Process

- By Feedstock

- By Intrinsic Viscosity (IV)

- By Application

- By End-User Industry

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Poland, China, Japan, South Korea, India, Indonesia, Thailand, Taiwan, Malaysia, Brazil, Argentina, Saudi Arabia, UAE, Iran, Egypt, South Africa, Turkey

- Technology Landscape & Innovation Analysis

- Continuous Polycondensation (CP) & SSP Technology Deep-Dive: IV Control, Acetaldehyde Reduction, Colour Quality & Energy Efficiency

- Chemical Recycling of PET Technology: Glycolysis, Methanolysis, Hydrolysis & Enzymatic (Carbios PETase) Process Comparison

- Mechanical rPET Technology: Post-Consumer Flake Processing, Super-Clean Recycling & Food-Grade rPET Production

- Bio-Based PET Technology: Bio-MEG from Sugarcane Ethanol, Bio-PTA from Bio-p-Xylene & Fully Circular Bio-PET Roadmap

- Barrier & Multi-Layer PET Technology: Oxygen Scavenger, Passive Barrier (MXD6, EVOH) & Monolayer High-Barrier PET Innovation

- Coloured, Opaque & Specialty PET: Lightweighting, Functional Additive Masterbatch & Value-Added Bottle-Grade Development

- Digital Twin, APC & AI-Based PET Polymerisation Reactor Optimisation & Quality Assurance Technology

- Patent & IP Landscape in PET Resin Production, Recycling & Bio-Based Technologies

- Value Chain & Supply Chain Analysis

- PTA Feedstock: Paraxylene Oxidation, PTA Plant & Supply Chain

- MEG Feedstock: Ethylene Oxide Hydration, Coal-to-MEG & Bio-MEG Supply Chain

- Catalyst, Stabiliser, Pigment & Additive Masterbatch Supply Chain for PET Polymerisation

- PET Resin Pellet Production, Packaging, Bulk Handling & Logistics Supply Chain

- Post-Consumer PET Bottle Collection, Sorting, Washing & Flake Production Supply Chain

- PET Converter: Preform Injection Moulder, Blow Moulder, Film Extruder & Fibre Spinner Supply Chain

- Brand Owner, Retailer, Beverage Company & Recycler Channel

- Pricing Analysis

- Global PET Resin Benchmark Price Analysis: FOB Asia, CFR Europe & US Domestic Price Benchmarking

- PTA & MEG Feedstock Cost, Polymerisation Margin & PET Resin Conversion Cost Analysis

- Bottle-Grade vs. Fibre-Grade vs. Film-Grade PET Price Differential Analysis

- Virgin PET vs. rPET Price Spread & Recycled Content Premium/Discount Analysis

- Bio-Based PET Price Premium vs. Conventional PET Benchmark Analysis

- Regional PET Price Differential: Asia-Pacific vs. Europe vs. Americas & Trade Flow Arbitrage Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of PET Resin: Carbon Footprint, Energy Intensity & End-of-Life Impact by Grade & Application

- PET Recyclability, Mono-Material Design & Closed-Loop Mechanical Recycling Performance

- Chemical Recycling of PET: Technology Readiness, GHG Balance & Contribution to Circular Economy

- rPET Mandates, Deposit Return Systems (DRS) & Collection Infrastructure Impact on Virgin vs. Recycled PET Demand

- Bio-Based PET: Sugarcane MEG Lifecycle GHG Advantage, Bio-PTA Development & Path to Fully Circular Bio-PET

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by PET Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by PET Type, Application & Geography

- Player Classification

- Integrated PTA-MEG-PET Complex Operators

- Standalone PET Resin Producers Purchasing PTA & MEG

- Recycled PET (rPET) Producers: Mechanical & Chemical Recyclers

- Specialty & Engineering PET & Copolymer Producers

- Bio-Based PET & Sustainable Polymer Producers

- Competitive Analysis Frameworks

- Market Share Analysis by PET Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- PET Resin Products, Grade Portfolio & Technology Platform

- Key Customer Relationships & Offtake Agreements

- Manufacturing Footprint, PET Production Capacity (MTPA) & Plant Locations

- Revenue (PET Resin Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansions, rPET Integration, Sustainability Initiatives)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Feedstock Integration vs. Sustainability Portfolio Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By PET Type, Application, End-User Industry & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio, Grade Development & Technology Investment Strategy

- Capacity Expansion, Feedstock Integration & Manufacturing Excellence Strategy

- Geographic Expansion & New Market Penetration Strategy

- Customer, Converter & Brand Owner Engagement Strategy

- Partnership, M&A & Petrochemical Ecosystem Strategy

- Sustainability, rPET Integration & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output