Global Ferric Chloride Market By Form, By Grade, By Production Method, By Application, By End Use Industry, By Distribution Channel, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Ferric Chloride Market encompasses the production, processing, and commercial distribution of iron(III) chloride in anhydrous solid, hexahydrate crystalline, and aqueous solution forms, manufactured through chlorination of iron or reaction of hydrochloric acid with iron oxide and utilized as a coagulant and flocculant in municipal and industrial water and wastewater treatment, as an etchant in printed circuit board manufacturing, as a catalyst and intermediate in chemical synthesis, and as a reagent in pharmaceuticals, pigments, and specialty chemical production across industrial, municipal, and electronic manufacturing end use markets globally.

Market Insights

The global ferric chloride market is experiencing a period of sustained demand growth across its two primary application pillars of water and wastewater treatment and electronics manufacturing, with each segment driven by distinct structural growth factors that collectively sustain market expansion independently of single-industry demand cyclicality and reinforce the commercial resilience of ferric chloride producers capable of serving both major application channels. The market was valued at approximately USD 1.84 billion in 2025 and is projected to advance at a compound annual growth rate of 5.2% through 2034, as expanding municipal water treatment infrastructure investment across developing economies, progressively tightening industrial wastewater discharge regulations, and the robust growth of printed circuit board production supporting electronics manufacturing for consumer devices, automotive electronics, and industrial IoT applications collectively sustain a multi-vector demand expansion trajectory for ferric chloride across geographically diverse and structurally distinct end use markets.

The water and wastewater treatment segment accounts for the largest and most geographically distributed share of global ferric chloride consumption, as the chemical’s effectiveness as a coagulant for removing suspended solids, phosphorus, heavy metals, and colloidal particles from both potable water and industrial effluent streams at competitive cost relative to alternative coagulants makes it a widely preferred treatment chemical for municipal water utilities, industrial effluent treatment plants, and sludge dewatering applications. Municipal wastewater treatment capacity expansion across Asia-Pacific, the Middle East, and Africa is generating growing ferric chloride procurement volumes as governments invest in wastewater collection and treatment infrastructure to address urban sanitation deficiencies, with phosphorus removal applications in particular benefiting from tightening nutrient discharge standards that require reliable phosphorus precipitation chemistry at treatment plants serving watersheds with eutrophication sensitivity. The printed circuit board etching application maintains its position as the highest unit value ferric chloride consumption segment, reflecting the chemical’s superior copper etching selectivity, controllable etch rate, and extensive installed equipment compatibility across the large global base of PCB manufacturing facilities that have built production processes around ferric chloride etching chemistry over multiple decades of electronics manufacturing development.

Asia-Pacific, led by China, dominates global ferric chloride production and consumption, reflecting the concentration of printed circuit board manufacturing capacity across Chinese, Taiwanese, South Korean, and Malaysian electronics production clusters and the massive scale of municipal and industrial water treatment chemical demand generated by China’s ongoing water infrastructure development and industrial effluent compliance programs. Chinese ferric chloride producers benefit from byproduct supply of ferrous chloride from pickling and surface treatment operations at steel processing facilities that provides advantaged feedstock for ferric chloride production through oxidative chlorination, contributing to production cost competitiveness that supports Chinese ferric chloride export activity serving Asian and global buyers. India is emerging as a significant growth market for ferric chloride, driven by accelerating municipal wastewater treatment investment under national sanitation programs, growing printed circuit board manufacturing capacity supporting domestic electronics assembly, and expanding water treatment chemical consumption from industrial effluent compliance programs across textile, pharmaceutical, and chemical manufacturing sectors.

North America and Europe represent mature but technically sophisticated ferric chloride markets where established municipal water treatment chemical procurement programs, high-specification electronics manufacturing, and stringent industrial wastewater discharge compliance are sustaining stable to modestly growing demand. Regulatory pressure for phosphorus removal from municipal wastewater effluent under nutrient trading and total maximum daily load compliance programs in the United States and nitrogen and phosphorus emission reduction directives in the European Union are generating sustained chemical coagulant procurement demand that includes ferric chloride as a preferred phosphorus precipitation agent. The Middle East and Africa represent the highest proportional growth markets for ferric chloride in the water treatment segment, driven by the scale of desalination pre-treatment chemical consumption and the rapid expansion of municipal wastewater treatment capacity across Gulf Cooperation Council countries, Egypt, Nigeria, and South Africa.

Key Drivers

Global Municipal and Industrial Wastewater Treatment Infrastructure Expansion Creating Sustained Ferric Chloride Coagulant Demand Across Developing Economy Markets

The accelerating investment in municipal wastewater collection and treatment infrastructure across South and Southeast Asia, the Middle East, Africa, and Latin America is generating growing procurement demand for ferric chloride as a coagulant and phosphorus precipitation chemical at newly commissioned and expanded wastewater treatment plants serving urban populations whose wastewater is transitioning from informal disposal into formal treatment systems for the first time. Simultaneously, tightening industrial effluent discharge standards across Chinese, Indian, Southeast Asian, and Latin American manufacturing jurisdictions are compelling industrial operators in textiles, pharmaceuticals, food processing, and chemical manufacturing to invest in effluent treatment infrastructure that consumes ferric chloride for suspended solids removal, heavy metal precipitation, and sludge conditioning applications that improve effluent quality to levels meeting progressively stringent regulatory permit conditions.

Printed Circuit Board Manufacturing Growth Driven by Electronics Demand, Automotive Electrification, and Industrial IoT Expansion Sustaining High-Value Ferric Chloride Etching Chemical Demand

The robust growth of printed circuit board production volumes driven by consumer electronics refresh cycles, automotive electronics content escalation from electric vehicle powertrain and advanced driver assistance system integration, industrial automation and IoT device proliferation, and telecommunications infrastructure expansion including 5G base station deployment is sustaining strong demand for ferric chloride etching solutions at PCB manufacturing facilities across China, Taiwan, South Korea, Malaysia, and Vietnam, where the concentration of global electronics manufacturing creates geographically dense and operationally demanding ferric chloride procurement markets. The trend toward higher circuit density and finer copper trace geometries in advanced PCB designs is simultaneously supporting demand for purified ferric chloride etching solutions with controlled metal impurity levels that deliver consistent etch uniformity across complex multi-layer board configurations.

Phosphorus Removal Regulatory Requirements and Nutrient Discharge Standards Driving Ferric Chloride Adoption in Municipal Wastewater Treatment for Eutrophication Control

Progressively stringent total phosphorus discharge limits imposed on municipal wastewater treatment plants by regulatory agencies in the European Union, United States, Canada, Australia, and increasingly in Asian jurisdictions responding to freshwater lake and coastal water eutrophication concerns are compelling wastewater utilities to implement or expand chemical phosphorus removal programs that rely on iron-based and aluminum-based coagulant addition to precipitate phosphate from treated effluent to compliance levels. Ferric chloride’s high phosphorus precipitation efficiency, the operational simplicity of its dosing and mixing integration with existing treatment plant infrastructure, and its competitive chemical cost relative to aluminum sulfate alternatives in many regional coagulant markets have established it as a widely adopted phosphorus removal reagent whose demand is directly linked to nutrient discharge regulation stringency trajectories in major municipal wastewater markets.

Key Challenges

Ferric Chloride Corrosivity, Handling Hazards, and Storage Infrastructure Requirements Creating Logistics Cost and Safety Compliance Burdens for Producers, Distributors, and End Users

Ferric chloride solution is a highly corrosive material that requires specialized stainless steel, high-density polyethylene, or fiber-reinforced plastic storage and handling equipment throughout the supply chain from production facility to end user application point, imposing capital expenditure and maintenance obligations on producers, distributors, and municipal and industrial customers that add to the total cost of ferric chloride procurement and use relative to less corrosive alternative coagulants. Transportation of ferric chloride solution in bulk tankers classified as hazardous materials under regulatory frameworks governing corrosive liquids requires driver certification, vehicle equipment compliance, emergency response planning, and route restriction compliance that increase logistics cost and delivery lead time complexity for ferric chloride distributors serving geographically dispersed customer bases across large regional territories.

Competition from Alternative Coagulants Including Aluminum Sulfate, Polyaluminum Chloride, and Ferrous Sulfate Constraining Ferric Chloride Market Share Growth in Price-Sensitive Water Treatment Markets

The water and wastewater treatment coagulant market is characterized by competitive substitution among iron-based and aluminum-based coagulant alternatives whose relative economic and technical performance advantages vary by application type, influent water chemistry, regulatory requirement, and regional supply economics, creating ongoing commercial pressure on ferric chloride market share from polyaluminum chloride products that generate lower residual solids volumes, aluminum sulfate that commands lower raw material cost in markets with competitively priced aluminum feedstock, and ferrous sulfate from pickling liquor byproduct streams that provide an extremely low-cost iron coagulant alternative in markets where steel industry byproduct supply is abundant and geographically proximate to treatment facility demand centers.

Raw Material and Energy Cost Volatility in Ferric Chloride Production and Environmental Compliance Costs from Hydrochloric Acid and Chlorine Gas Handling Creating Margin Pressure for Producers

Ferric chloride production through direct chlorination of iron or oxidative dissolution of iron-containing materials in hydrochloric acid is subject to input cost volatility from chlorine and hydrochloric acid market price fluctuations driven by chlor-alkali industry production cycle dynamics, natural gas and electricity cost movements affecting chlor-alkali energy consumption economics, and iron raw material cost variability that collectively affect production cost structures in ways that complicate long-term pricing commitments to municipal utility customers whose procurement is governed by multi-year tender contracts with limited price escalation provisions. Environmental compliance investment for chlorine gas containment, acid mist emission control, and ferric chloride solution spill containment infrastructure adds to production operating costs and requires ongoing capital expenditure to maintain regulatory compliance status.

Market Segmentation

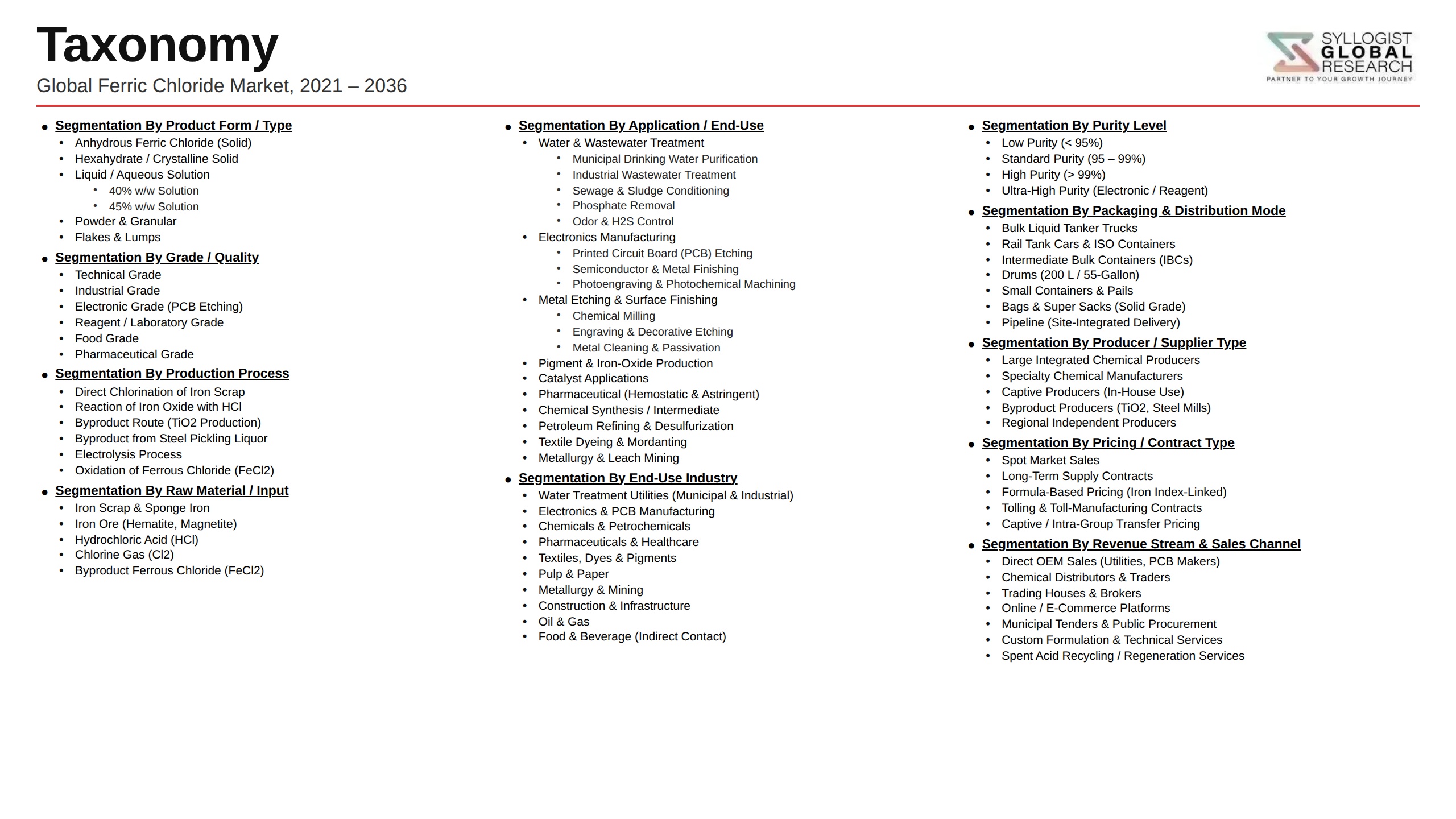

- Segmentation By Form

- Ferric Chloride Aqueous Solution (30-45% Concentration)

- Anhydrous Ferric Chloride Solid

- Ferric Chloride Hexahydrate Crystals

- Others

- Segmentation By Grade

- Technical Grade for Water Treatment

- Electronic Grade for PCB Etching

- Reagent and Laboratory Grade

- Food and Pharmaceutical Grade

- Industrial Grade for Chemical Synthesis

- Segmentation By Production Method

- Chlorination of Iron and Steel Scrap

- Oxidative Dissolution in Hydrochloric Acid

- Byproduct Recovery from Pickling and Surface Treatment Operations

- Electrolytic and Chemical Oxidation of Ferrous Chloride

- Others

- Segmentation By Application

- Municipal Water and Wastewater Coagulation and Flocculation

- Industrial Effluent Treatment and Heavy Metal Removal

- Printed Circuit Board Copper Etching

- Phosphorus Precipitation and Nutrient Removal

- Chemical Synthesis Catalyst and Intermediate

- Sludge Conditioning and Dewatering

- Pigment and Iron Oxide Manufacturing

- Others

- Segmentation By End Use Industry

- Municipal Water Utilities and Wastewater Treatment

- Electronics and Printed Circuit Board Manufacturing

- Chemical and Specialty Chemical Manufacturing

- Textile and Dyeing Industry

- Pharmaceutical and Life Sciences

- Mining and Metals Processing

- Food and Beverage Processing

- Others

- Segmentation By Distribution Channel

- Direct Sales to Large Municipal and Industrial Customers

- Chemical Distributors and Trading Companies

- Bulk Tanker and Drummed Delivery Logistics Providers

- Online Chemical Procurement Platforms

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global ferric chloride market valuation in 2025, projected through 2034, segmented by form, application, and end use industry, enabling ferric chloride producers, chemical distributors, water treatment chemical procurement teams, and electronics manufacturing supply chain managers to identify the highest-growth application segments and most commercially significant demand opportunities across the global market?

- How are municipal wastewater treatment infrastructure expansion programs in Asia-Pacific, the Middle East, and Africa, combined with tightening phosphorus and nutrient discharge standards in North America and Europe, collectively shaping ferric chloride coagulant demand volume trajectories, specification requirements, and preferred supply contract structures for water utility procurement programs through 2034?

- Which printed circuit board manufacturing growth segments, specifically automotive electronics, 5G telecommunications infrastructure, industrial IoT devices, and advanced semiconductor packaging substrates, are generating the highest incremental ferric chloride etching chemical demand, and what circuit density advancement and purity specification trends are shaping product quality and technical service requirements for electronic-grade ferric chloride suppliers?

- How is the competitive landscape structured among global ferric chloride producers, regional chemical manufacturers with byproduct-derived production advantages, and specialty chemical distributors serving municipal and electronic manufacturing markets, and what production cost, product quality, logistics network, and application technical support strategies are enabling leading suppliers to build and maintain commercial positions across diverse geographic markets?

- What competitive threats from polyaluminum chloride, aluminum sulfate, ferrous sulfate byproduct, and emerging organic coagulant alternatives are most significantly constraining ferric chloride market share growth in municipal water treatment, industrial effluent treatment, and sludge dewatering applications, and how are ferric chloride producers differentiating on technical performance, cost-in-use economics, and supply reliability to defend market position?

- How are ferric chloride handling hazard regulations, corrosive material transportation requirements, storage infrastructure compliance obligations, and environmental compliance costs for chlorine and acid emission control affecting the total cost of ferric chloride supply chain operations for producers and distributors, and what logistics network design, packaging format innovation, and handling safety improvement strategies are being pursued to reduce these burden costs?

- Which regional ferric chloride markets, specifically Asia-Pacific, the Middle East and Africa, and Latin America, are expected to generate the highest incremental procurement growth through 2034, and what combinations of wastewater treatment infrastructure investment, electronics manufacturing cluster expansion, industrial effluent compliance program enforcement, and water quality improvement policy initiatives are defining demand growth trajectories and competitive market entry opportunities in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Hydrochloric Acid & Iron Ore Feedstock Price Volatility & Supply Availability Risk

- Corrosive Material Handling, Transportation Safety & Spill Liability Risk

- Environmental Regulation Tightening, Wastewater Iron & Chloride Discharge Limit Risk

- Substitution Risk from Alternative Coagulants: Aluminium Sulphate, PAC & Ferrous Sulphate Competition

- Semiconductor Etchant Market Volatility, Printed Circuit Board Industry Cycle Risk

- Corrosion of Storage & Handling Infrastructure, Asset Damage & Maintenance Cost Risk

- Regulatory Framework & Standards

- REACH, GHS/CLP & Global Hazardous Chemical Classification, Labelling & Safety Data Sheet Standards for Ferric Chloride

- Water Treatment Chemical Standards: NSF/ANSI 60, ACS Reagent Grade & Drinking Water Treatment Coagulant Purity Requirements

- Electronic Chemical Purity Standards: SEMI Standards (C40, C49) & VLSI/ULSI Grade Ferric Chloride Specifications for Semiconductor Use

- DOT 49 CFR, ADR/RID & International Hazardous Materials Transport Regulations for Corrosive Liquid Classification

- Wastewater Discharge Limits, Iron & Chloride Effluent Standards & IPPC/IED Industrial Emission Regulatory Frameworks

- National Chemical Industry Standards: GB Standards (China), IS Standards (India) & Regional Chemical Product Quality Regulations

- Global Ferric Chloride Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes per Annum, MTPA)

- Market Size & Forecast by Form

- Ferric Chloride Solution (Anhydrous-Equivalent 40-45% FeCl3)

- Ferric Chloride Anhydrous (Solid, Granular & Powder)

- Ferric Chloride Hexahydrate (Crystalline Form)

- High-Purity & Electronic Grade Ferric Chloride Solution

- Market Size & Forecast by Production Process

- Chlorination of Iron Powder or Sponge Iron (Direct Chlorination)

- Reaction of Hydrochloric Acid with Iron & Oxidation (HCl-Fe Route)

- By-Product Recovery from Steel Pickling & Hydrochloric Acid Regeneration

- Chlorination of Ferrous Chloride via Chlorine Gas Oxidation

- Dissolution & Purification for High-Purity Electronic Grade Production

- Market Size & Forecast by Purity Grade

- Industrial Grade Ferric Chloride (Standard Purity)

- Technical Grade Ferric Chloride (Water Treatment & PCB)

- Reagent & Analytical Grade Ferric Chloride

- Electronic & Semiconductor Grade Ferric Chloride (Ultra-High Purity)

- Market Size & Forecast by Application

- Municipal Drinking Water Treatment & Clarification

- Industrial Wastewater & Effluent Treatment (Phosphate Removal & Flocculation)

- Printed Circuit Board (PCB) Etching & Copper Chloride Recovery

- Semiconductor Wafer & Microelectronics Etching & Cleaning

- Pigment, Dye & Ink Manufacturing (Iron Oxide Pigment Precursor)

- Chemical Synthesis & Catalyst Applications (Lewis Acid Catalyst)

- Metal Surface Treatment, Pickling & Passivation

- Sludge Conditioning, Dewatering & Biosolids Treatment

- Soil Stabilisation, Civil Engineering & Ground Treatment

- Market Size & Forecast by End-User

- Municipal Water & Wastewater Treatment Utilities

- Printed Circuit Board (PCB) & Electronics Manufacturers

- Semiconductor & Microelectronics Fabricators

- Chemical, Petrochemical & Specialty Chemical Producers

- Industrial & Manufacturing Facilities with Effluent Treatment Requirements

- Metal Processing, Steel & Surface Treatment Companies

- Pigment, Dye & Ink Manufacturers

- Market Size & Forecast by Sales Channel

- Direct Manufacturer Sales to Large Industrial & Utility Customers

- Chemical Distributor & Merchant Wholesaler Network

- Government Tender & Public Utility Procurement Channel

- Electronic Chemical Specialty Distributor Channel

- North America Ferric Chloride Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Form

- By Production Process

- By Purity Grade

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Ferric Chloride Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Form

- By Production Process

- By Purity Grade

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Ferric Chloride Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Form

- By Production Process

- By Purity Grade

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Ferric Chloride Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Form

- By Production Process

- By Purity Grade

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Ferric Chloride Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Form

- By Production Process

- By Purity Grade

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Ferric Chloride Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Form

- By Production Process

- By Purity Grade

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Belgium, Spain, Italy, Poland, China, Japan, South Korea, India, Taiwan, Singapore, Malaysia, Indonesia, Brazil, Argentina, Saudi Arabia, UAE, South Africa, Egypt

- Technology Landscape & Innovation Analysis

- By-Product Ferric Chloride Recovery Technology Deep-Dive: Steel Pickling HCl Regeneration, Iron Chloride Oxidation & Valorisation Economics

- High-Purity Electronic Grade Ferric Chloride Purification Technology: Multi-Stage Filtration, Activated Carbon Treatment & Metal Ion Removal

- Closed-Loop PCB Etching & Copper Recovery Technology: Ferric Chloride Regeneration, Copper Chloride Electrolysis & Waste Minimisation

- Advanced Water Treatment Coagulation Technology: Ferric Chloride Dosing Optimisation, Jar Testing & Real-Time Turbidity Monitoring

- Ferric Chloride Solution Concentration, Spray Drying & Crystallisation Technology for Anhydrous & Hexahydrate Grade Production

- Continuous vs. Batch Production Technology Comparison: Energy Efficiency, Yield & Product Quality for Industrial Grade FeCl3

- Digital Twin, Process Analytical Technology (PAT) & AI-Based Quality Control Technology for Ferric Chloride Manufacturing

- Patent & IP Landscape in Ferric Chloride Production & Purification Technologies

- Value Chain & Supply Chain Analysis

- Iron Ore, Scrap Iron, Iron Powder & Sponge Iron Feedstock Supply Chain

- Hydrochloric Acid (HCl) & Chlorine Gas Raw Material Supply Chain

- By-Product Iron Chloride Stream from Steel Pickling & Chemical Industry Supply Chain

- Ferric Chloride Production, Concentration & Purification Equipment Supply Chain

- Corrosion-Resistant Storage Tank, IBC Container, Isotainer & Road Tanker Logistics Supply Chain

- Chemical Distributor, Bulk Liquid Transporter & Specialty Chemical Logistics Channel

- Water Treatment Chemical Formulator, PCB Chemical Distributor & Electronic Chemical Specialist Channel

- Pricing Analysis

- Ferric Chloride Solution & Anhydrous Price Benchmarking by Grade, Region & Volume (USD/tonne)

- Feedstock Cost Impact: HCl & Iron Raw Material Price Pass-Through & Margin Analysis

- By-Product vs. Dedicated Production Cost Economics & Price Competitiveness Analysis

- Electronic & High-Purity Grade Price Premium vs. Industrial Grade Benchmark Analysis

- Logistics, Bulk vs. Drummed Delivery & Packaging Cost Impact on Delivered Price Analysis

- Price Trend Analysis: HCl Market, Iron Scrap Pricing & Demand Growth Impact on Ferric Chloride Pricing

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Ferric Chloride: Carbon Footprint of Production Routes & Comparison Across Feedstock Types

- By-Product & Waste Recovery as Circular Economy: Steel Mill HCl Regeneration & Iron Chloride Valorisation Environmental Benefit

- PCB Etching Waste Management: Spent Ferric Chloride Disposal, Copper Recovery & Zero-Liquid-Discharge Technology

- Role of Ferric Chloride in Sustainable Water Treatment: Phosphorus Removal, Eutrophication Control & SDG 6 Contribution

- ESG Reporting, Responsible Chemical Sourcing & REACH Compliance for Ferric Chloride Manufacturers & Distributors

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Form, Application & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Form, Application & Geography

- Player Classification

- Integrated Chemical Producers with Ferric Chloride as Primary or Major Product

- By-Product Ferric Chloride Producers (Steel Mills, HCl Producers & Chemical Plants)

- Specialty & High-Purity Electronic Grade Ferric Chloride Producers

- Water Treatment Chemical Formulators & Coagulant Specialists

- Chemical Distributors & Merchant Wholesalers with Ferric Chloride Portfolios

- Competitive Analysis Frameworks

- Market Share Analysis by Form, Application & Region

- Company Profile

- Company Overview & Headquarters

- Ferric Chloride Products, Grade Portfolio & Form Range

- Key Customer Relationships & Reference Applications

- Manufacturing Footprint, Production Capacity & Geographic Coverage

- Revenue (Ferric Chloride Segment) & Annual Volume

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansions, Grade Launches, Certifications)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Production Cost Competitiveness vs. Grade Portfolio Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Form, Purity Grade, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio, Grade Development & Technology Investment Strategy

- Feedstock Sourcing, By-Product Integration & Manufacturing Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Chemical Ecosystem Strategy

- Sustainability, Circular Economy & Waste Recovery Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output