Market Definition

Industrial valves are engineered flow-control devices designed to start/stop, throttle, divert, regulate, or protect the movement of liquids, gases, steam, and slurries across process and utility systems. Unlike commodity piping components, valves are application-critical safety and reliability assets, often a small fraction of total plant CapEx, but disproportionately responsible for uptime, product quality, emissions compliance, and process safety.

The market spans isolation valves (ball, gate, butterfly, plug), control valves (globe/rotary control), non-return valves (check types), and pressure protection valves (safety/relief). Performance and selection are defined by service duty (clean fluids vs corrosive vs abrasive slurry), pressure/temperature class, size, end connection standards (ASME/EN/ISO), material of construction (cast iron to duplex/nickel alloys), and automation layer (manual to actuated valves with smart positioners and diagnostics).

Industrial valves sit at the intersection of mechanical integrity + metallurgy + sealing technology + automation. In modern plants, valves increasingly function as “control and compliance nodes” that manage not only flow, but also fugitive emissions, safety instrumented functions (SIF), and predictive maintenance data.

Market Insights

The global industrial valves market is structurally shifting from a volume-led hardware business toward a value-led reliability and compliance market. While standard valves remain largely specification-driven and price competitive, growth and margin expansion are increasingly concentrated in engineered and severe-service applications, where downtime costs, safety exposure, and emissions risk drive customers toward proven designs, certified performance, and strong aftermarket support.

Demand is shaped by two distinct engines: project CapEx (new builds/expansions) and aftermarket MRO (replacement, spares, shutdown/turnarounds). In most mature industrial economies, MRO forms the stable base of demand; in fast-industrializing regions, project cycles and EPC procurement drive volatility. Competitive advantage is increasingly defined by low-emission sealing performance, lead-time assurance (for forgings/castings), actuation & controls integration, and service network depth, not just the valve body itself.

As plants digitize, valves are evolving from passive mechanical components into instrumented assets, enabled by smart positioners, partial-stroke testing, and condition monitoring that reduce unplanned shutdowns and improve compliance reporting.

Key Drivers

Energy Transition + Refining/Petrochemical Complexity

Refining and petrochemical assets are being upgraded for higher complexity feeds, tighter safety standards, hydrogen service, and efficiency retrofits. This increases demand for high-integrity isolation, fire-safe valves, high-performance control valves, and alloy upgrades in critical circuits where leakage, failure, or cavitation creates high risk.

Fugitive Emissions Regulations and ESG Compliance

Tightening requirements around VOC leakage and methane emissions are pushing adoption of low-emission packing, certified valve/packing systems, and LDAR-driven replacements. Valves become a direct lever for “measurable compliance,” accelerating replacement cycles in hydrocarbons, chemicals, and certain high-value industrial clusters.

Expansion and Rehabilitation of Water & Wastewater Infrastructure

Municipal and industrial water projects drive high-volume demand for butterfly, gate, check, and air valves, while industrial water reuse/ZLD increases needs for corrosion-resistant materials and reliable actuation. Rehabilitation programs also create sustained MRO pull for large installed bases.

Automation, Remote Operations, and Reliability Engineering

Plants are investing in automated valves, smart positioners, and diagnostics to reduce manual intervention, improve control stability, and avoid unplanned outages. This supports higher value share for actuated packages, SIL/ESD solutions, and control valve upgrades.

Mining, Slurry Handling, and Materials Processing Growth

Mining/metals and certain process industries require valves that can survive abrasive slurries, erosion, and scaling, driving demand for knife gate, pinch, lined valves, and hardened trims, typically higher ASP and more engineered content.

Key Challenges

Lead-Time and Capacity Constraints in Castings/Forgings and Special Alloys

Valve delivery schedules are often dictated by upstream supply availability, forgings, castings, machining slots, and special alloy procurement. Constraints are most visible in large sizes, high pressure classes, and duplex/nickel alloy valves, creating risk for EPC schedules and pushing buyers to dual-source strategies.

Pricing Volatility in Metals and Sealing Materials

Cost structures are sensitive to carbon steel/stainless/duplex/nickel alloys, as well as elastomers and packing materials (PTFE, graphite, FKM/FFKM). Volatility can compress margins in fixed-price project contracts, especially when specifications are locked early but deliveries occur much later.

Qualification Barriers and Vendor Approval Cycles

End users often require extensive qualification (vendor registration, MTC traceability, FAT/SAT, fire-safe and fugitive emissions certifications). For new entrants, the biggest barrier isn’t design, it’s approval time, references, and proven field performance.

Counterfeit / Substandard Supply Risk in Fragmented Channels

In some markets, parallel supply and weak traceability introduce risks around material authenticity, pressure class compliance, and test certification integrity, pushing critical end users toward trusted OEMs and authorized service ecosystems.

Severe-Service Performance Risk (Cavitation, Erosion, Cycling, Thermal Shock)

In control and high-duty applications, failures often stem from trim selection, sizing errors, cavitation/flash, erosion, and frequent cycling, not just the valve body. This drives higher engineering requirements and increases liability exposure for suppliers that lack application expertise.

Market Segmentation

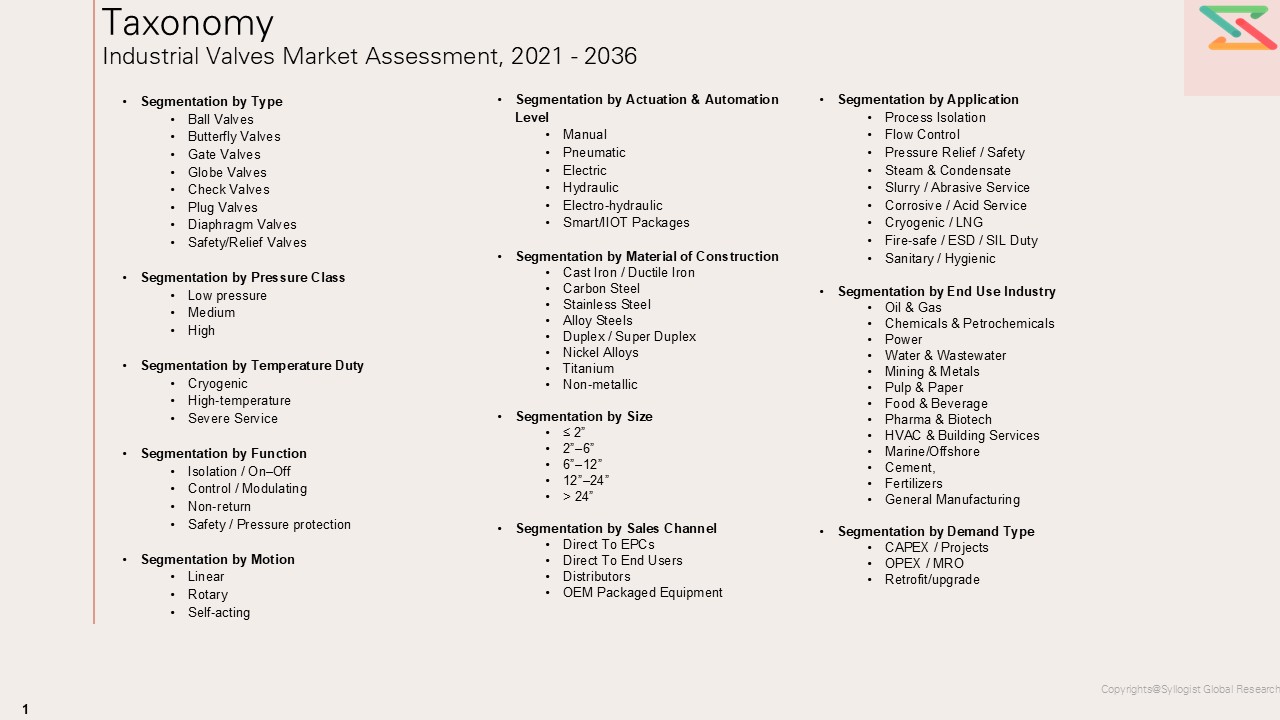

- Segmentation by Type

- Ball Valves

- Butterfly Valves

- Gate Valves

- Globe Valves

- Check Valves

- Plug Valves

- Diaphragm Valves

- Safety/Relief Valves

- Segmentation by Pressure Class

- Low pressure

- Medium

- High

- Segmentation by Temperature Duty

- Cryogenic

- High-temperature

- Severe Service

- Segmentation by Function

- Isolation / On–Off

- Control / Modulating

- Non-return

- Safety / Pressure Protection

- Segmentation by Motion

- Linear

- Rotary

- Self-acting

- Segmentation by Actuation & Automation Level

- Manual

- Pneumatic

- Electric

- Hydraulic

- Electro-hydraulic

- Smart/IIOT Packages

- Segmentation by Material of Construction

- Cast Iron / Ductile Iron

- Carbon Steel

- Stainless Steel

- Alloy Steels

- Duplex / Super Duplex

- Nickel Alloys

- Titanium

- Non-metallic

- Segmentation by Size

- ≤ 2”

- 2”–6”

- 6”–12”

- 12”–24”

- > 24”

- Segmentation by Sales Channel

- Direct To EPCs

- Direct To End Users

- Distributors

- OEM Packaged Equipment

- Segmentation by Application

- Process Isolation

- Flow Control

- Pressure Relief / Safety

- Steam & Condensate

- Slurry / Abrasive Service

- Corrosive / Acid Service

- Cryogenic / LNG

- Fire-safe / ESD / SIL Duty

- Sanitary / Hygienic

- Segmentation by End Use Industry

- Oil & Gas

- Chemicals & Petrochemicals

- Power

- Water & Wastewater

- Mining & Metals

- Pulp & Paper

- Food & Beverage

- Pharma & Biotech

- HVAC & Building Services

- Marine/Offshore

- Cement,

- Fertilizers

- General Manufacturing

- Segmentation by Demand Type

- CAPEX / Projects

- OPEX / MRO

- Retrofit/upgrade

All market revenues are presented in USD, with production volumes expressed in units.

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Industrial Valves Market, including revenue size, unit shipments, and installed base, with performance segmentation across valve types (ball, gate, globe, butterfly, plug, diaphragm, check, safety/relief, control valves), function (on–off vs modulating), pressure class/temperature duty (low/medium/high pressure; high-temp/cryogenic), size bands (≤2”, 2–6”, 6–12”, 12–24”, >24”), and actuation/automation levels (manual, pneumatic, electric, hydraulic, smart positioners)?

- How do supply–demand fundamentals vary across key regions and end-use clusters, and what role do project vs MRO demand mix, local fabrication/forging/casting ecosystems, machining capacity, and procurement structures (EPC-led projects vs end-user MRO vs distributor/stockist channels) play in shaping regional competitiveness across oil & gas, chemicals, power, water & wastewater, mining/metals, pulp & paper, and HVAC/building services?

- In what ways are raw material and component price volatility (carbon steel, stainless/duplex, nickel alloys; forgings/castings; elastomers like PTFE/FFKM; actuator components), lead-time constraints (forgings, special alloys, large-size valves), and evolving standards/regulations (API/ASME/EN, fire-safe API 607/6FA, fugitive emissions API 624/641 & ISO 15848, NACE MR0175/ISO 15156 for sour service, PED/CE where relevant) influencing cost structures, pricing, aftermarket spares economics, and supplier profitability?

- Who are the leading global and regional industrial valve manufacturers and specialists, and how do they benchmark across severe-service capability (anti-cavitation trims, erosion-resistant designs, slurry duty), engineering depth (custom trims, metallurgical know-how, CFD-based sizing), actuation & controls integration (positioners, partial-stroke testing, SIL/ESD packages), fugitive-emissions performance, and portfolio breadth across process isolation, control, and safety applications?

- What strategic insights emerge from primary discussions with end users and channel stakeholders, including refineries/petrochem complexes, chemical plants, utilities, municipal/industrial water operators, mining operators, EPC contractors, and distributors/valve service centers, regarding turnaround/shutdown cycles, spec evolution (low-emission packing, smart diagnostics, higher alloy substitution, metal-seated designs), qualification pathways (vendor approvals, FAT/SAT), lead times for engineered-to-order valves, and key purchase criteria (total cost of ownership vs initial CapEx, reliability, delivery assurance, service network coverage, spares availability)?

- Market Foundations & Dynamics

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Ecosystem & Value Chain

- Overview of Value Chain Participants

- Flow of Value and Material Through the Chain

- Value Addition and Margins at Each Stage

- Market Trends & Developments

- Emerging Raw Material Trends

- Raw Material Availability

- Technological Advancements

- Demand–Supply Gaps

- Investment Hotspots

- Unmet Needs and White Market Spaces

- Risk Assessment Framework

- Political / Geopolitical Risk

- Raw Material Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Policy and Mandate Overview

- Transportation and Storage Regulations

- Sustainability and GHG Reduction Standards

- Environmental & Liability Considerations

- Technology Landscape

- Overview of Technologies

- Cost Optimization Technologies

- Future Outlook

- Global Industrial Valves Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Type

- Ball Valves

- Butterfly Valves

- Gate Valves

- Globe Valves

- Check Valves

- Plug Valves

- Diaphragm Valves

- Safety/Relief Valves

- Market Size & Forecast by Pressure Class

- Low pressure

- Medium

- High

- Market Size & Forecast by Temperature Duty

- Cryogenic

- High Temperature

- Severe Service

- Market Size & Forecast by Function

- Isolation / On–Off

- Control / Modulating

- Non-return

- Safety / Pressure Protection

- Market Size & Forecast by Motion

- Linear

- Rotary

- Self-acting

- Market Size & Forecast by Actuation & Automation Level

- Manual

- Pneumatic

- Electric

- Hydraulic

- Electro-hydraulic

- Smart/IIOT Packages

- Market Size & Forecast by Material of Construction

- Cast Iron / Ductile Iron

- Carbon Steel

- Stainless Steel

- Alloy Steels

- Duplex / Super Duplex

- Nickel Alloys

- Titanium

- Non-metallic

- Market Size & Forecast by Size

- ≤ 2”

- 2”–6”

- 6”–12”

- 12”–24”

- > 24”

- Market Size & Forecast by Sales Channel

- Direct To EPCs

- Direct To End Users

- Distributors

- OEM Packaged Equipment

- Market Size & Forecast by Application

- Process Isolation

- Flow Control

- Pressure Relief / Safety

- Steam & Condensate

- Slurry / Abrasive Service

- Corrosive / Acid Service

- Cryogenic / LNG

- Fire-safe / ESD / SIL Duty

- Sanitary / Hygienic

- Market Size & Forecast by End Use Industry

- Conventional / Core Industries

- Oil & Gas

- Chemicals & Petrochemicals

- Power

- Water & Wastewater

- Mining & Metals

- Cement

- Fertilizers

- Marine / Offshore

- General Manufacturing

- Specialized / Regulated Industries

- Pharma & Biotech

- Food & Beverage

- Industrial Gases

- Specialty Chemicals

- Paints & Coatings

- Agrochemicals

- Semiconductor Manufacturing

- Infrastructure & Building Systems

- HVAC & Building Services

- District Cooling / Heating

- Fire Protection

- Municipal Utilities

- Airports / Rail / Smart Cities

- Commercial Complexes / Campuses

- High-Growth Industries

- Data Centers

- Desalination

- Battery Gigafactories

- Water Reuse / ZLD

- LNG / Gas Processing

- Waste-to-Energy

- EV Manufacturing

- Emerging / Future-Focused Industries

- Green Hydrogen

- CCUS

- e-Fuels

- SAF

- Geothermal

- SMRs / Advanced Nuclear

- Recycling / Circular Economy

- Rare Earth & Critical Minerals Processing

- Market Size & Forecast by Demand Type

- CAPEX / Projects

- OPEX / MRO

- Retrofit/upgrade

- Asia-Pacific Industrial Valves Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Type

- Market Size & Forecast by Pressure Class

- Market Size & Forecast by Temperature Duty

- Market Size & Forecast by Function

- Market Size & Forecast by Motion

- Market Size & Forecast by Actuation & Automation Level

- Market Size & Forecast by Material of Construction

- Market Size & Forecast by Size

- Market Size & Forecast by Sales Channel

- Market Size & Forecast by Application

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Demand Type

- Europe Industrial Valves Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Type

- Market Size & Forecast by Pressure Class

- Market Size & Forecast by Temperature Duty

- Market Size & Forecast by Function

- Market Size & Forecast by Motion

- Market Size & Forecast by Actuation & Automation Level

- Market Size & Forecast by Material of Construction

- Market Size & Forecast by Size

- Market Size & Forecast by Sales Channel

- Market Size & Forecast by Application

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Demand Type

- North America Industrial Valves Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Type

- Market Size & Forecast by Pressure Class

- Market Size & Forecast by Temperature Duty

- Market Size & Forecast by Function

- Market Size & Forecast by Motion

- Market Size & Forecast by Actuation & Automation Level

- Market Size & Forecast by Material of Construction

- Market Size & Forecast by Size

- Market Size & Forecast by Sales Channel

- Market Size & Forecast by Application

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Demand Type

- Latin America Industrial Valves Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Type

- Market Size & Forecast by Pressure Class

- Market Size & Forecast by Temperature Duty

- Market Size & Forecast by Function

- Market Size & Forecast by Motion

- Market Size & Forecast by Actuation & Automation Level

- Market Size & Forecast by Material of Construction

- Market Size & Forecast by Size

- Market Size & Forecast by Sales Channel

- Market Size & Forecast by Application

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Demand Type

- Middle East & Africa Industrial Valves Market Outlook

- Market Size & Forecast by Value & Volume

- Market Size & Forecast by Type

- Market Size & Forecast by Pressure Class

- Market Size & Forecast by Temperature Duty

- Market Size & Forecast by Function

- Market Size & Forecast by Motion

- Market Size & Forecast by Actuation & Automation Level

- Market Size & Forecast by Material of Construction

- Market Size & Forecast by Size

- Market Size & Forecast by Sales Channel

- Market Size & Forecast by Application

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Demand Type

- Country Market Size & Forecast by Value & Volume

- Market Size & Forecast by Type

- Market Size & Forecast by Pressure Class

- Market Size & Forecast by Temperature Duty

- Market Size & Forecast by Function

- Market Size & Forecast by Motion

- Market Size & Forecast by Actuation & Automation Level

- Market Size & Forecast by Material of Construction

- Market Size & Forecast by Size

- Market Size & Forecast by Sales Channel

- Market Size & Forecast by Application

- Market Size & Forecast by End Use Industry

- Market Size & Forecast by Demand Type

- Conventional / Core Industries

Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Brazil, Argentina, Chile, Colombia, Peru, United Kingdom, Germany, France, Italy, Spain, Netherlands, Belgium, Switzerland, Austria, Sweden, Norway, Denmark, Finland, Poland, Czechia, Hungary, Romania, Turkey, Russia, Ukraine, Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, Egypt, South Africa, Nigeria, Morocco, Israel, India, China, Japan, South Korea, Taiwan, Singapore, Malaysia, Thailand, Indonesia, Vietnam, Australia

- Pricing Analysis

- Overview of Pricing Structures

- Average Selling Price Trends Type and End Use

- Cost Benchmark

- Historical Price Evolution

- Forecast Pricing Curve

- Factors Influencing Price:

- Regional Pricing Differentiation

- Competition Outlook

- Market Concentration and Fragmentation Level

- Company Market Shares (Top 10 Producers)

- Competitive Strategies

- Benchmarking Matrix

- Recent Developments: Partnerships, M&A, and Policy-Driven Expansions

- Cost Structure & Margin Analysis

- Average Cost per Liter

- Profitability and Margin Distribution Along the Value Chain

- Sensitivity Analysis: How Raw Material Price and Policy Incentives Impact Margin

- Cost Reduction Opportunities through Process Optimization

- Business Models & Strategic Insights

- Sales & Distribution Channel Analysis

- Overview of Go-to-Market Channels

- Channel Share by Region

- Distribution Strategies by Leading Players

- Strategic Recommendations & Roadmap

- Competitors’ Strategic Initiatives

- Future Outlook (Next 5–10 Years, Emerging Players, Success Factors)

- Strategic Recommendations

- Technology Advancements to Watch

- Market Acceleration Roadmap

- Short-Term

- Mid-Term

- Long-Term

- Tailored Recommendations for:

- Producers

- Raw Material Suppliers

- Policymakers / Regulators

- Investors

- Recommendations on Key Success Factors

- Raw Material Security

- Technology Partnerships

- Policy Alignment

- Supply Chain Integration

- Investor Confidence