Global Power Distribution Systems Market By System Type, By Voltage Level, By Component, By Technology, By End Use Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Power Distribution Systems Market encompasses the design, manufacture, supply, and integration of medium and low voltage electrical infrastructure used to receive bulk power from transmission networks and deliver it to industrial, commercial, and residential end users, including distribution transformers, switchgear, switchboards, busbar systems, ring main units, reclosers, capacitor banks, voltage regulators, energy management systems, and associated protection and automation equipment procured by electric utilities, industrial facilities, commercial buildings, data centers, and infrastructure operators globally.

Market Insights

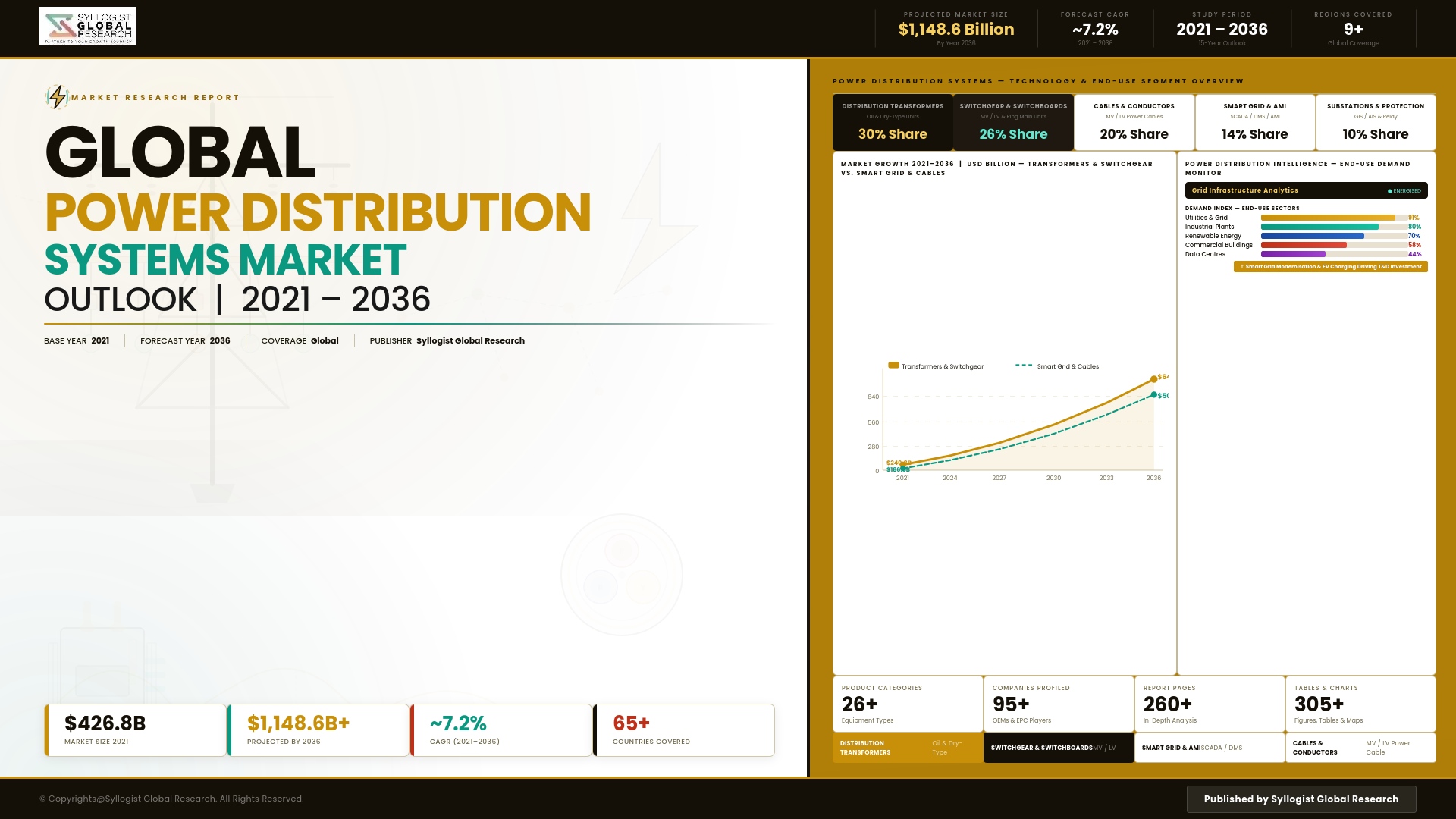

The global power distribution systems market is navigating a structural transformation of unparalleled breadth, driven by the simultaneous imperatives of integrating distributed renewable energy generation and battery storage into distribution networks engineered for unidirectional power flow, electrifying transportation and industrial loads that are fundamentally reshaping the demand profile and peak capacity requirements of existing distribution infrastructure, modernizing ageing network assets whose operational limitations increasingly constrain grid reliability and energy efficiency performance, and deploying digitally instrumented smart grid capabilities that enable active distribution network management at a granularity and responsiveness that passive legacy infrastructure cannot support. The market was valued at approximately USD 112.7 billion in 2025 and is projected to grow at a compound annual growth rate of 7.1% through 2034, as the energy transition imposes distribution system upgrade and expansion investment requirements across virtually every national electricity network that are substantially larger in aggregate scale than the normal asset replacement and load growth-driven investment cycles that historically governed distribution system capital expenditure.

The distribution transformer segment represents the largest single component category within the power distribution systems market, reflecting the fundamental role of medium-to-low voltage transformation in every electricity distribution system globally and the large installed base of transformers approaching end of service life across developed market utilities that are managing multi-year replacement programs while simultaneously upgrading to higher-efficiency transformer designs mandated by increasingly stringent energy efficiency regulations in the European Union, United States, and Australia. Amorphous core distribution transformer technology is gaining market share in efficiency-sensitive replacement programs, achieving no-load loss reductions of sixty to seventy percent compared to conventional silicon steel core designs whose aggregate standby losses across the global distribution transformer fleet represent a recoverable energy efficiency opportunity of substantial environmental and economic value. Medium voltage switchgear and ring main unit procurement is registering growing demand driven by underground cable network densification in urban areas, smart grid reconfiguration capability upgrades, and the need for additional network switching points to accommodate bidirectional power flows from distributed generation resources connecting at distribution voltage levels.

The integration of distributed energy resources including rooftop solar photovoltaic systems, residential and commercial battery storage, demand response programs, and electric vehicle smart charging into active distribution network management frameworks is driving investment in advanced distribution automation, volt-var optimization systems, distributed energy resource management platforms, and real-time power quality monitoring infrastructure that collectively constitute a rapidly growing intelligent grid component segment within the broader distribution systems market. Distribution system operators are deploying sensor networks, smart meters, phasor measurement units, and communication infrastructure across medium voltage feeders and low voltage networks to develop the situational awareness and control capability required for managing increasingly complex and dynamic power flows in distribution networks that were designed for fundamentally different operating conditions. Digital twins of distribution networks, AI-powered load forecasting and network planning tools, and predictive asset condition monitoring platforms are emerging as commercially distinct software and services categories generating growing procurement investment from progressive distribution utilities seeking to optimize capital allocation across network reinforcement, asset replacement, and demand-side flexibility alternatives.

Asia-Pacific dominates the global power distribution systems market by procurement volume, anchored by the scale of Chinese and Indian distribution network expansion and modernization investment, the pace of Southeast Asian urban infrastructure development requiring primary distribution system deployment, and the large rural electrification programs in Indonesia, Vietnam, Bangladesh, and the Philippines that require extensive low voltage distribution infrastructure deployment in areas transitioning from off-grid to grid-connected electricity supply. North America represents the second largest regional market, driven by a substantial distribution system modernization backlog reflecting decades of underinvestment in network upgrades, federal and state programs funding grid hardening and smart grid deployment, and the growing load growth requirements of data center proliferation and electric vehicle charging network expansion. Europe is the most advanced regional market in smart grid technology deployment and distributed energy resource integration, driven by ambitious renewable energy targets, progressive distribution network regulation frameworks, and a mature electricity sector with sophisticated network management capability.

Key Drivers

Distributed Renewable Energy Integration and Bidirectional Power Flow Management Requirements Compelling Fundamental Distribution System Architecture Upgrades Across Global Electricity Networks

The proliferation of rooftop solar photovoltaic systems, community-scale battery storage, wind micro-generation, and demand response resources connecting at distribution voltage levels is imposing bidirectional power flow conditions, voltage rise phenomena, and harmonic distortion challenges on distribution networks engineered and operated for unidirectional bulk power delivery, requiring utilities to invest in network reinforcement, advanced protection system upgrades, voltage regulation equipment, reactive power compensation devices, and distribution automation infrastructure that can safely and efficiently manage the increasingly variable and bidirectional energy flows characterizing modern distribution networks. The growing penetration of distributed energy resources in residential and commercial feeders is simultaneously creating the data acquisition and real-time monitoring infrastructure investment requirement for distribution system operators to maintain the operational visibility required for safe and reliable network management under dynamic generation and load conditions.

Electric Vehicle Charging Infrastructure Expansion and Industrial Electrification Programs Driving Distribution Network Capacity Reinforcement and Load Management Investment at Unprecedented Scale

The mass adoption of battery electric vehicles is creating concentrated and high-power electrical load additions at residential and commercial distribution connection points that are progressively exceeding the capacity margins of low voltage distribution transformers and medium voltage feeders engineered for pre-electrification load profiles, compelling distribution utilities to invest in transformer upgrades, cable reinforcement, smart charging management systems, and demand flexibility programs that manage electric vehicle charging load to prevent network congestion while maintaining supply reliability standards. Industrial heat pump deployment, electric arc furnace adoption in steel production, and the electrification of chemical and manufacturing process loads are simultaneously adding large new industrial distribution connection requirements that necessitate medium voltage network capacity upgrades and substation expansion investment to accommodate the step-change load growth that industrial electrification programs impose on local distribution system capacity.

Grid Resilience Mandates, Extreme Weather Event Frequency Escalation, and Digital Grid Modernization Programs Generating Sustained Smart Grid and Distribution Automation Investment Demand

The increasing frequency and severity of extreme weather events including hurricanes, ice storms, wildfires, and floods that cause widespread distribution network outages is compelling utilities and regulators to invest in grid hardening programs encompassing underground cable conversion, surge protection upgrades, automated fault isolation and service restoration systems, and advanced distribution management platforms that minimize outage duration and affected customer numbers when distribution infrastructure sustains weather-related damage. Simultaneously, cybersecurity threats to grid operational technology, critical infrastructure protection regulations, and the growing connectivity of distribution system components through smart grid communication networks are driving investment in secure communications infrastructure, operational technology cybersecurity systems, and network segmentation architectures that protect distribution automation platforms from cyber compromise while enabling the data exchange required for advanced grid management.

Key Challenges

Distribution Network Planning Complexity Under High Distributed Energy Resource Penetration Creating Capacity Forecasting Uncertainty and Suboptimal Capital Allocation Risk for Utility Investment Programs

Traditional distribution network capacity planning methodologies based on deterministic peak load growth forecasting are becoming increasingly inadequate for networks with high and growing penetrations of rooftop solar, battery storage, electric vehicles, and demand response resources whose aggregate impact on local network loading is highly variable, location-dependent, and difficult to predict with the accuracy required for multi-year capital investment planning, creating the risk of both over-investment in network reinforcement that is rendered unnecessary by demand flexibility and under-investment that results in network congestion and reliability deterioration as distributed energy resource adoption accelerates beyond forecast assumptions. Developing probabilistic planning frameworks, flexible network solutions, and non-network alternatives assessment methodologies that can optimally allocate capital between traditional reinforcement and demand-side management alternatives represents a significant operational capability development challenge for distribution utilities globally.

Skilled Workforce Shortages in Distribution System Engineering, Digitalization Implementation, and Smart Grid Operations Constraining the Pace of Network Modernization Program Delivery

The accelerating expansion of distribution system investment programs, the increasing technical complexity of smart grid technology deployment, and the growing requirement for data analytics, cybersecurity, and software engineering expertise within distribution utility operations are creating acute workforce capability gaps across electrical engineering, grid operations, information technology integration, and digital asset management disciplines that are constraining the pace and quality of distribution modernization program delivery across multiple major markets simultaneously. The competitive labor market for electrical and software engineers, combined with the long lead time required to develop the specialized operational experience in distribution system design and smart grid technology integration that complex network projects demand, limits the ability of utilities and their supply chain contractors to rapidly scale workforce capacity in proportion to the growing volume of distribution system investment programs requiring concurrent execution.

Regulatory Framework Lag and Cost Recovery Uncertainty for Smart Grid and Distributed Energy Resource Integration Investments Dampening Utility Innovation and Capital Deployment Rates

Distribution utility investment in smart grid technology, advanced distribution management systems, distributed energy resource integration infrastructure, and digital network monitoring platforms is constrained in many regulatory jurisdictions by rate case approval processes that apply traditional cost-benefit assessment frameworks ill-suited to evaluating the system-wide and long-term value of intelligent grid capabilities that deliver benefits across multiple stakeholders and over extended time horizons exceeding the regulatory review cycle. The uncertainty over whether innovative distribution system investments will receive timely and adequate cost recovery through regulatory mechanisms, combined with the risk that technology investment made ahead of regulatory framework development may not qualify for recovery under subsequently established standards, creates a regulatory risk premium that depresses utility innovation investment below the level that would be economically and societally optimal given the scale and urgency of distribution system transformation requirements.

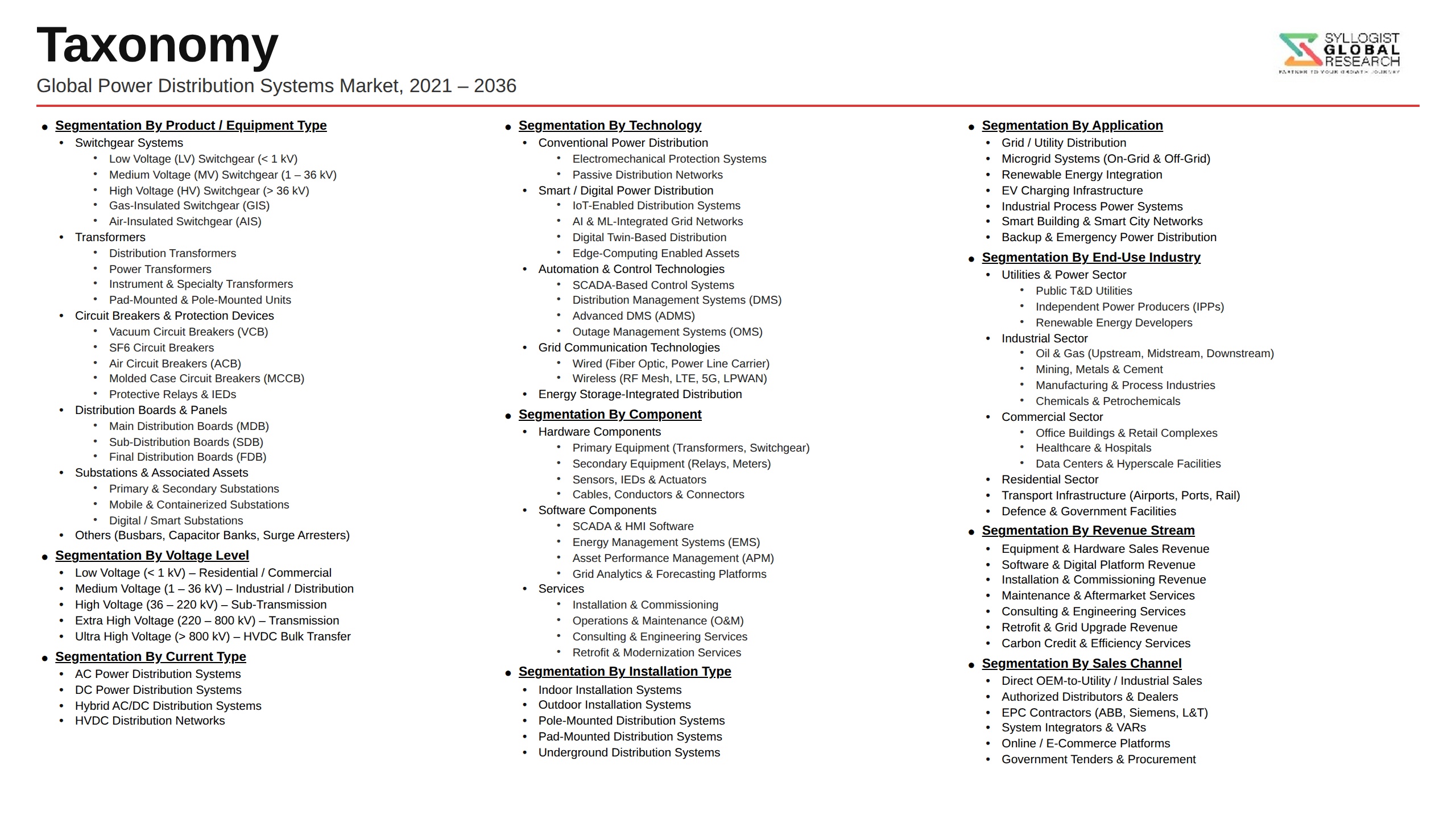

Market Segmentation

- Segmentation By System Type

- Primary Distribution Systems (Medium Voltage)

- Secondary Distribution Systems (Low Voltage)

- Industrial Power Distribution Systems

- Commercial Building Distribution Systems

- Smart and Active Distribution Systems

- Microgrid Distribution Systems

- Others

- Segmentation By Voltage Level

- Low Voltage (Below 1 kV)

- Medium Voltage (1 kV to 36 kV)

- High Voltage Distribution (36 kV to 132 kV)

- Segmentation By Component

- Distribution Transformers

- Medium and Low Voltage Switchgear

- Ring Main Units and Reclosers

- Busbar and Busduct Systems

- Capacitor Banks and Voltage Regulators

- Protection Relays and Control Panels

- Advanced Distribution Management Systems

- Others

- Segmentation By Technology

- Conventional Passive Distribution Systems

- Smart Grid and Advanced Metering Infrastructure

- Distribution Automation and SCADA Systems

- Distributed Energy Resource Management Systems

- Gas-Insulated Switchgear Systems

- Others

- Segmentation By End Use Application

- Utility and Grid Distribution Infrastructure

- Industrial Facility Power Distribution

- Commercial and Institutional Building Power

- Data Center Power Distribution

- Renewable Energy Farm Distribution

- Electric Vehicle Charging Network Infrastructure

- Rural Electrification and Microgrid Systems

- Others

- Segmentation By End User

- Electric Power Utilities and Distribution Network Operators

- Industrial and Manufacturing Corporations

- Commercial Real Estate and Building Developers

- Data Center and Technology Infrastructure Operators

- Renewable Energy Project Developers

- Government and Public Infrastructure Agencies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global power distribution systems market valuation in 2025, projected through 2034, segmented by system type, component, and end use application, enabling equipment manufacturers, utility procurement teams, and infrastructure investors to identify the highest-growth product categories and most durable capital investment opportunities across the global power distribution landscape?

- How are distributed renewable energy resource integration requirements, bidirectional power flow management challenges, and active distribution network management technology investments reshaping distribution system architecture, component specification, and capital expenditure priorities for electric utilities across North America, Europe, and Asia-Pacific through 2034?

- Which distribution system component segments, specifically distribution transformers, medium voltage switchgear, advanced distribution management systems, and distributed energy resource management platforms, are generating the highest procurement growth, and what energy efficiency regulations, smart grid mandates, and grid reliability standards are driving specification upgrades and technology modernization in each category?

- How is the competitive landscape structured among global power distribution equipment manufacturers, regional switchgear and transformer producers, and smart grid technology platform providers, and what product portfolio integration, digital solutions development, utility partnership, and geographic market expansion strategies are enabling leading competitors to strengthen market share across key distribution system categories?

- What planning methodology challenges, probabilistic load forecasting requirements, and non-network alternative assessment frameworks are distribution utilities developing to optimize capital allocation between traditional network reinforcement and demand-side flexibility solutions under high distributed energy resource penetration scenarios, and how are these evolving planning approaches reshaping long-term distribution investment program structure and procurement timing?

- How are electric vehicle charging load growth, industrial electrification programs, and data center proliferation reshaping medium and low voltage distribution network capacity requirements, transformer upgrade investment cycles, and smart charging management system procurement across urban, suburban, and industrial distribution network segments through 2034?

- Which regional distribution systems markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most significant incremental investment through 2034, and what combinations of rural electrification demand, smart grid modernization mandates, distributed energy resource integration requirements, and industrial load growth are defining distribution system procurement priorities and technology adoption trajectories in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility: Copper, Aluminium, Steel & Transformer Core Material Cost Fluctuation Risk

- Supply Chain Disruption, Long Lead Time & Component Shortage Risk for Transformers & Switchgear

- Cybersecurity, SCADA Vulnerability & Digital Grid Attack Surface Risk

- Ageing Grid Infrastructure, Asset Failure & Unplanned Outage Risk

- Regulatory Compliance Complexity, Grid Code Changes & Permitting Delay Risk

- Regulatory Framework & Standards

- IEC 61936, IEC 62271 & IEEE C37 Switchgear & Switchboard Standards for Power Distribution Equipment

- IEC 60076 & IEEE C57 Power Transformer Standards, Efficiency Classes & No-Load Loss Regulations

- IEC 61850 Substation Communication, Protection Relay & Digital Substation Interoperability Standards

- Grid Code Requirements, Voltage Regulation, Power Quality & Distribution Network Connection Standards

- SF6 Phase-Out Regulations, F-Gas Directive & Alternative Insulation Gas Standards for Switchgear

- Energy Efficiency Directives, Minimum Energy Performance Standards (MEPS) & Ecodesign Regulation for Distribution Transformers

- Global Power Distribution Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped & MVA Capacity)

- Market Size & Forecast by Equipment Type

- Distribution Transformers (Liquid-Filled & Dry-Type)

- Medium Voltage Switchgear & Ring Main Units (RMUs)

- Low Voltage Switchgear, Switchboards & Distribution Boards

- Busbar Trunking Systems & Busway Distribution

- Power Distribution Units (PDUs) & Rack PDUs

- Automatic Transfer Switches (ATS) & Static Transfer Switches (STS)

- Protection Relays, Current Transformers (CTs) & Metering Units

- Reclosers, Sectionalizers & Fault Interrupters

- Capacitor Banks & Reactive Power Compensation Systems

- Integrated Smart Distribution Systems & Digital Substations

- Market Size & Forecast by Voltage Level

- Low Voltage (LV) Distribution Systems (Below 1 kV)

- Medium Voltage (MV) Distribution Systems (1 kV to 36 kV)

- High Voltage (HV) Distribution Systems (36 kV to 150 kV)

- Market Size & Forecast by Insulation Technology

- Air-Insulated Switchgear (AIS) & Distribution Equipment

- Gas-Insulated Switchgear (GIS) & Gas-Insulated Distribution Systems

- Solid-Insulated Switchgear (SIS) & Eco-Efficient Insulation Systems

- Vacuum Interrupter-Based Switchgear & Circuit Breakers

- SF6-Free & Alternative Gas (g3, Clean Air & CO2) Insulated Switchgear

- Market Size & Forecast by Installation

- Overhead Distribution Line Systems

- Underground & Cable Distribution Systems

- Indoor Substation & Panel Distribution Systems

- Compact Secondary Substation & Package Substation Systems

- Prefabricated & Modular Distribution Substation Systems

- Market Size & Forecast by Grid Type

- Centralised Utility Grid Distribution Systems

- Smart Grid & Advanced Distribution Management Systems (ADMS)

- Microgrid & Distributed Energy Resource (DER) Distribution Systems

- DC Microgrid & Hybrid AC/DC Distribution Systems

- Market Size & Forecast by Application

- Utility & Public Distribution Network Infrastructure

- Renewable Energy Grid Integration & Distributed Generation

- Industrial Plants, Factories & Process Industry Facilities

- Commercial Buildings, Offices & Retail Complexes

- Data Centres & Critical IT Infrastructure

- Healthcare Facilities & Hospitals

- Transportation Infrastructure (Railways, Metros & EV Charging Networks)

- Oil & Gas, Petrochemical & Mining Facilities

- Residential & Smart Building Electrification

- Market Size & Forecast by End-User

- Electric Utilities & Distribution Network Operators (DNOs)

- Industrial & Manufacturing Companies

- Commercial Real Estate & Building Owners

- Data Centre & Hyperscale Technology Operators

- Oil & Gas, Petrochemical & Mining Operators

- Transportation & Infrastructure Authorities

- Healthcare & Institutional Facility Operators

- Government & Public Sector Infrastructure Programmes

- Market Size & Forecast by Sales Channel

- Direct OEM & Manufacturer Sales

- EPC Contractor, Panel Builder & System Integrator Channel

- Electrical Distributor & Wholesaler Network

- Government Tender & Public Utility Procurement Channel

- Online & Digital Procurement Platform Channel

- North America Power Distribution Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & MVA Capacity)

- By Equipment Type

- By Voltage Level

- By Insulation Technology

- By Installation

- By Grid Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Power Distribution Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & MVA Capacity)

- By Equipment Type

- By Voltage Level

- By Insulation Technology

- By Installation

- By Grid Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Power Distribution Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & MVA Capacity)

- By Equipment Type

- By Voltage Level

- By Insulation Technology

- By Installation

- By Grid Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Power Distribution Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & MVA Capacity)

- By Equipment Type

- By Voltage Level

- By Insulation Technology

- By Installation

- By Grid Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Power Distribution Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & MVA Capacity)

- By Equipment Type

- By Voltage Level

- By Insulation Technology

- By Installation

- By Grid Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Power Distribution Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & MVA Capacity)

- By Equipment Type

- By Voltage Level

- By Insulation Technology

- By Installation

- By Grid Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Sweden, China, Japan, South Korea, India, Australia, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- SF6-Free Switchgear Technology Deep-Dive: g3 Gas, Clean Air, CO2 & Vacuum Interrupter Alternatives for MV & HV Applications

- Digital Substation Technology: IEC 61850 Process Bus, Merging Units, Intelligent Electronic Devices (IEDs) & Protection Automation

- Advanced Distribution Management System (ADMS) & Distribution SCADA Technology for Smart Grid Operations

- Solid-State Transformer (SST) & Power Electronics-Based Distribution Technology

- DC Distribution & Hybrid AC/DC Microgrid Technology for Renewable Integration & Data Centre Power Delivery

- Amorphous Core, High-Efficiency & Bio-Based Oil Distribution Transformer Technology

- IoT-Enabled Asset Monitoring, Partial Discharge Detection & Predictive Maintenance Technology for Distribution Equipment

- Patent & IP Landscape in Power Distribution System Technologies

- Value Chain & Supply Chain Analysis

- Copper, Aluminium, Silicon Steel & Transformer Core Material Supply Chain

- Transformer Insulating Oil, Solid Insulation & Winding Material Supply Chain

- Switchgear Enclosure, Busbar, Vacuum Bottle & Gas Insulation Component Supply Chain

- Protection Relay, Current Transformer, Metering & Digital Control Component Supply Chain

- Transformer & Switchgear Manufacturing, Assembly & Testing Supply Chain

- EPC Contractor, Panel Builder & System Integration Channel

- Aftermarket Service, Maintenance, Retrofit & Spare Parts Supply Chain

- Pricing Analysis

- Distribution Equipment Unit Price Analysis by Equipment Type & Voltage Level

- Distribution Transformer Price Analysis: Liquid-Filled vs. Dry-Type & Standard vs. High-Efficiency Comparison

- SF6-Based vs. SF6-Free Switchgear Capital Cost & Total Cost of Ownership (TCO) Comparison

- Smart & Digital Distribution System Premium vs. Conventional Equipment Pricing Analysis

- Impact of Copper & Silicon Steel Price Movements on Transformer & Distribution Equipment Pricing

- Service Contract, Maintenance & Asset Management Pricing Model Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Power Distribution Equipment: Carbon Footprint, Material Use & End-of-Life Impact

- SF6 Greenhouse Gas Phasedown: Regulatory Timeline, Technology Transition Pathway & Industry Readiness Assessment

- Distribution Transformer Energy Efficiency: No-Load & Load Loss Reduction, Amorphous Core & High-Efficiency Designs

- Bio-Based Transformer Oil, Recyclable Insulation & Sustainable Material Use in Distribution Equipment

- Role of Smart Distribution Systems in Enabling Renewable Integration, Demand Response & Grid Decarbonisation

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Equipment Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Equipment Type, Voltage Level & Geography

- Player Classification

- Global Integrated Power Distribution System Manufacturers (Full Portfolio)

- Specialist Distribution Transformer Manufacturers

- Specialist Medium & High Voltage Switchgear Manufacturers

- Specialist Low Voltage Switchgear, Switchboard & Panel Manufacturers

- Smart Grid, Digital Substation & ADMS Technology Providers

- Busbar Trunking, PDU & Secondary Distribution Equipment Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Equipment Type, Voltage Level & Region

- Company Profile

- Company Overview & Headquarters

- Power Distribution Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Power Distribution Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Equipment Type, Voltage Level, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output