Market Definition

The Global Grid Hardening and Resilient Power Infrastructure Market encompasses the planning, engineering, procurement, construction, commissioning, and operation of reinforced electrical transmission and distribution systems, substations, critical control infrastructure, and associated grid modernization technologies designed to withstand, absorb, and rapidly recover from physical threats, extreme weather events, cyberattacks, geomagnetic disturbances, electromagnetic pulse events, and other high-impact disruptions that compromise the reliability and continuity of electricity supply across industrial, commercial, residential, and critical public service end users globally.

Grid hardening refers to the systematic reinforcement of electrical infrastructure through physical protection measures, material upgrades, redundancy architectures, vegetation management programs, and advanced monitoring and protection systems that reduce vulnerability of transmission lines, distribution networks, substation equipment, and grid control systems to damage, failure, or unauthorized interference. Resilient power infrastructure encompasses hardened substations incorporating blast-resistant enclosures, seismic isolation systems, and flood barrier installations; overhead-to-underground cable conversion programs eliminating weather-related outage risk in high-exposure corridors; advanced distribution management systems and fault detection technologies enabling rapid outage restoration; microgrid systems incorporating distributed generation and battery storage providing islanded power continuity during grid disruption events; and cybersecurity frameworks protecting operational technology platforms, SCADA systems, and energy management infrastructure from coordinated attack scenarios.

Key participants include electric utilities, independent power operators, transmission system operators, government defense and homeland security agencies, grid modernization technology vendors, engineering procurement and construction contractors, advanced materials suppliers, power electronics manufacturers, and regulatory bodies whose grid reliability and security mandates define the fundamental engineering and investment requirements governing infrastructure hardening programs across all major electricity markets globally.

Market Insights

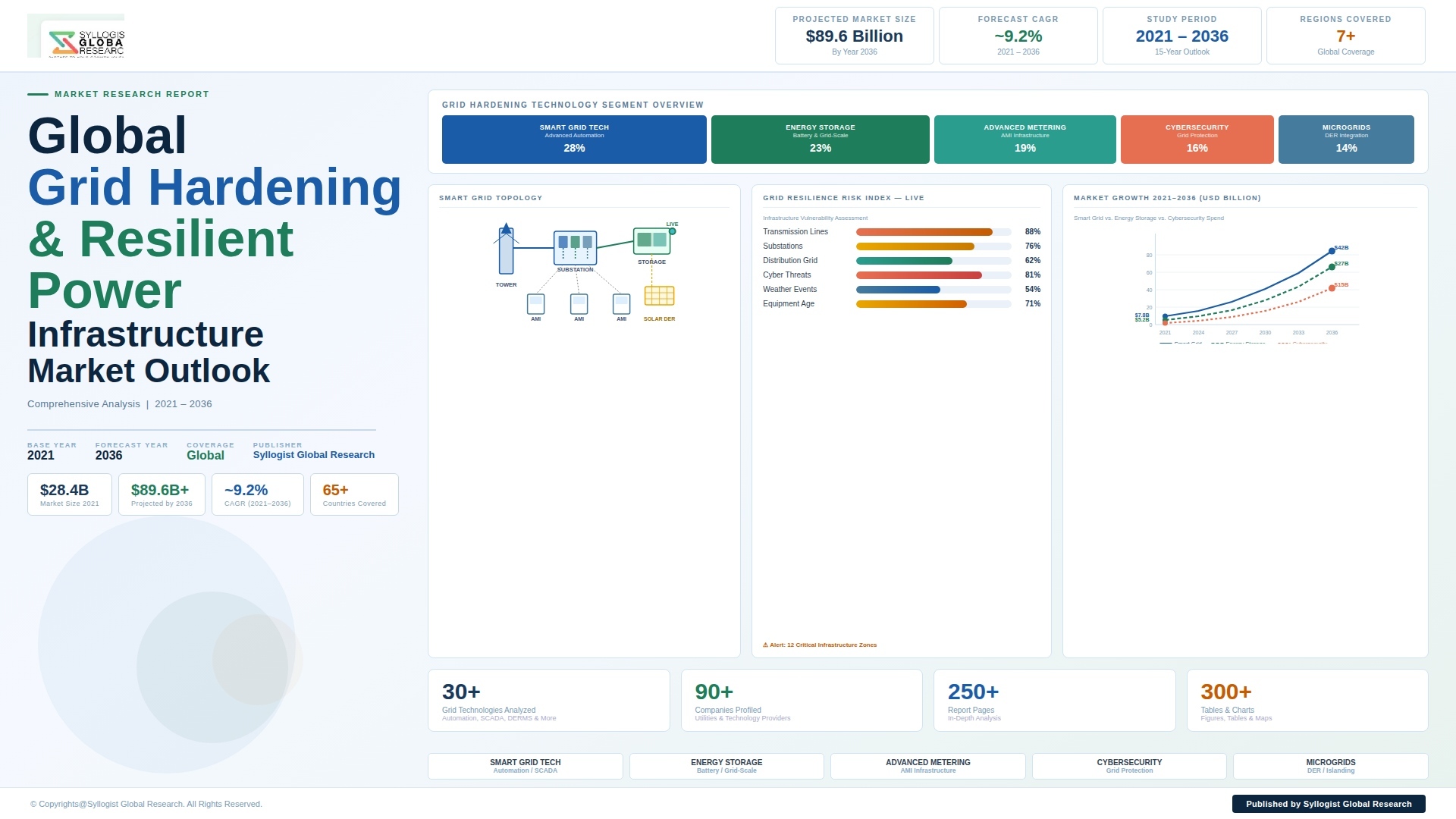

The global grid hardening and resilient power infrastructure market is experiencing a structural acceleration in investment driven by the convergence of three powerful forces: the sharply rising frequency and economic severity of climate-driven power outages, the escalating threat landscape confronting grid operational technology systems from state-sponsored and criminal cyber actors, and the mounting policy imperative across North America, Europe, and Asia-Pacific to modernize aging transmission and distribution infrastructure as a prerequisite for safely integrating large-scale renewable energy capacity and meeting net-zero electricity system transformation commitments. The global grid hardening and resilient power infrastructure market was valued at approximately USD 64.3 billion in 2025 and is projected to reach USD 112.7 billion by 2034, advancing at a compound annual growth rate of 6.4% over the forecast period from 2027 to 2034. Utilities, regulators, and governments are transitioning from reactive outage response strategies toward proactive infrastructure resilience investment frameworks, fundamentally expanding the addressable market for grid hardening technologies, services, and system solutions across all major electricity market geographies.

The technology landscape of grid hardening is broadening rapidly beyond conventional overhead line replacement and substation upgrades to encompass a sophisticated portfolio of physical reinforcement, digital intelligence, and distributed energy resource integration solutions that collectively define the modern resilient power infrastructure paradigm. Underground high-voltage cable installations, driven by hurricane and wildfire risk mitigation requirements in the United States and wind storm resilience programs across northern European markets, now represent a principal capital expenditure category within utility grid hardening programs, with underground cable deployment volumes growing at approximately 8.1% annually. Advanced distribution automation systems incorporating intelligent electronic devices, self-healing network switching capabilities, and real-time fault location analytics are enabling utilities to dramatically reduce outage duration and the number of customers affected per incident. Modular hardened substation designs utilizing prefabricated equipment enclosures, mobile transformer reserve units, and rapid-deployment switchgear systems are shortening restoration timelines following extreme weather or physical security incidents from days to hours, directly reducing the economic and social cost of grid disruption events.

The convergence of physical grid hardening with cybersecurity investment represents one of the most commercially significant structural trends reshaping the competitive landscape and solution architecture of the resilient power infrastructure market. The operational technology systems governing electrical grid control, including energy management systems, SCADA platforms, protection relay networks, and substation automation systems, have emerged as high-priority targets for cyberattacks seeking to cause electricity supply disruption, infrastructure damage, or strategic intelligence collection, compelling utilities and transmission operators to implement integrated physical-cyber resilience programs that treat grid hardening as a unified physical and digital security challenge rather than two separate investment streams. Regulatory frameworks including the North American Electric Reliability Corporation Critical Infrastructure Protection standards in North America and the Network and Information Security Directive requirements in the European Union are mandating minimum cybersecurity investment levels and incident reporting obligations that are generating durable compliance-driven demand for grid cybersecurity solutions alongside conventional physical hardening capital expenditure programs.

From a regional standpoint, North America represents the largest single regional market for grid hardening investment, driven by the United States federal grid modernization funding programs, including USD 13 billion in grid resilience and innovation grants authorized under the Infrastructure Investment and Jobs Act, the acute wildfire-driven infrastructure hardening imperative facing California, Pacific Northwest, and Mountain West utilities, and hurricane resilience investment programs across Gulf Coast and Atlantic Seaboard states. Europe constitutes the second-largest regional market, characterized by large-scale offshore wind integration transmission investment requirements in the United Kingdom, Germany, and the Netherlands, and cybersecurity-driven grid hardening programs stimulated by heightened energy security concerns following geopolitical disruptions affecting energy supply across the continent. Asia-Pacific is the fastest-growing regional market at approximately 8.7% annually, driven by India’s transmission system expansion and modernization program, Japan’s post-earthquake and tsunami grid resilience investment, and Southeast Asian grid modernization programs addressing the infrastructure requirements of rapidly growing peak electricity demand.

Key Drivers

Increasing Frequency and Economic Severity of Extreme Weather Events Compelling Structural Utility Investment in Physical Grid Hardening Programs

The measurable intensification of extreme weather events including major hurricanes, atmospheric river flooding events, prolonged heat dome episodes, severe ice storms, and expanding wildfire risk perimeters is inflicting progressively higher and more economically damaging grid outage incidents on electrical utilities across North America, Europe, and Asia-Pacific, compelling regulators and utility commissions to mandate systematic grid hardening investment programs funded through approved rate base recovery mechanisms that translate climate-driven risk exposure into durable capital expenditure commitments. The United States alone experienced 28 separate weather and climate disaster events each causing losses exceeding USD 1 billion in 2024, with power infrastructure damage and outage-related economic losses constituting a substantial component of total event costs across hurricane, tornado, flood, and wildfire incident categories. Wildfire risk mitigation has become the single largest driver of distribution grid hardening investment in the western United States, with California investor-owned utilities including Pacific Gas and Electric, Southern California Edison, and San Diego Gas and Electric collectively committing over USD 6.0 billion annually to overhead line undergrounding, covered conductor installation, enhanced vegetation management, and fast-acting protective relay deployment programs designed to eliminate utility-ignited wildfire risk from their distribution networks. The demonstrated economic return on proactive grid hardening investment, measured against the avoided outage costs, regulatory penalty avoidance, liability risk reduction, and insurance premium savings achievable through systematic infrastructure resilience programs, is increasingly recognized by utility financial planning frameworks and utility commission rate case proceedings as a commercially justified and regulatorily supportable investment priority.

Government Policy Mandates and Dedicated Funding Frameworks Creating Structural Multi-Year Demand for Grid Resilience Capital Expenditure Across Major Electricity Markets

The deployment of government policy mechanisms specifically targeting grid hardening investment, ranging from direct federal and national grid resilience funding programs to regulatory capital expenditure mandates, performance-based rate mechanisms rewarding outage reduction achievement, and national energy security legislation mandating minimum infrastructure resilience standards, is generating a policy-underwritten demand foundation for grid hardening and resilient power infrastructure investment that substantially reduces the commercial risk and cyclicality associated with utility capital expenditure programs dependent solely on voluntary utility investment decisions and traditional cost-of-service rate recovery proceedings. The United States Infrastructure Investment and Jobs Act allocated USD 65 billion for grid modernization and resilience programs, representing the largest single federal investment in electrical infrastructure in the nation’s history and creating a multi-year procurement pipeline for grid hardening technologies, underground cable installations, advanced substation equipment, and grid monitoring systems across federal, state, and utility-level programs. The European Union’s REPowerEU plan and the accompanying grid investment acceleration framework are mobilizing estimated EUR 584 billion in grid transmission and distribution investment through 2030, with grid resilience and cross-border interconnection infrastructure representing priority investment categories. National grid resilience legislation enacted in Japan, Australia, India, and multiple Southeast Asian economies is similarly translating energy security policy objectives into mandatory utility investment programs that expand the commercial demand base for grid hardening technologies and services across Asia-Pacific markets through the forecast period.

Accelerating Renewable Energy Integration Requirements Driving Transmission and Distribution Reinforcement Investment to Support Grid Stability and Power Flow Management

The large-scale integration of variable renewable energy generation, specifically utility-scale solar photovoltaic and onshore and offshore wind power, into transmission and distribution networks that were engineered for the predictable, centralized generation dispatch characteristics of conventional thermal and nuclear power plants is creating fundamental grid stability, power flow management, and voltage regulation challenges that require substantial transmission reinforcement, advanced grid protection system upgrades, and distribution automation investment to manage safely and reliably, generating a renewable integration-driven layer of grid hardening investment that is structurally linked to the accelerating deployment of renewable energy capacity across all major electricity markets. Global installed renewable energy capacity additions reached approximately 473 gigawatts in 2024, with solar and wind together accounting for the overwhelming majority of new generation investment globally, and the International Energy Agency projects that electricity grids will need to add or refurbish approximately 80 million kilometers of transmission and distribution lines by 2040 to accommodate the renewable energy transition and meet climate commitments. Grid-forming inverter technology, advanced protection coordination systems capable of operating reliably on low-inertia grids with high renewable penetration, synchronous condensers for voltage support, and high-voltage direct current transmission links for long-distance renewable energy transport represent the principal technology investment categories at the intersection of renewable integration and grid hardening, creating commercially significant demand for advanced power electronics, grid protection equipment, and high-capacity transmission infrastructure that supports both renewable integration and broader grid resilience objectives simultaneously.

Key Challenges

Capital Intensity of Comprehensive Grid Hardening Programs and the Complexity of Regulatory Cost Recovery Mechanisms in Multi-Jurisdiction Utility Markets

The scale of investment required to comprehensively harden transmission and distribution infrastructure across large utility service territories against the full spectrum of physical, weather, and cyber threats represents a capital commitment of extraordinary magnitude that strains utility balance sheets, challenges regulatory cost recovery approval processes, and creates significant pressure on residential and commercial electricity consumer tariffs, generating political and regulatory resistance to the pace and scope of grid hardening investment that utilities and independent technical assessments identify as necessary to meet evolving resilience standards. Overhead-to-underground cable conversion, consistently identified as the highest-impact distribution grid hardening measure for weather risk elimination, carries installation costs of USD 1.5 million to USD 4.5 million per mile in dense urban environments, compared to USD 0.1 million to USD 0.3 million per mile for overhead line construction, creating an economic barrier to widespread deployment that limits the pace of underground conversion programs even in high-risk geographies with clear resilience justification. Utility commission rate case proceedings governing capital expenditure recovery, which must balance utility grid hardening investment requirements against consumer bill affordability constraints, are creating approval timeline uncertainty, regulatory lag between investment commitment and authorized cost recovery, and in some jurisdictions outright capital expenditure caps that constrain the pace of grid hardening program deployment below the levels recommended by independent grid resilience assessments and mandated by evolving regulatory reliability standards.

Supply Chain Constraints and Extended Lead Times for Critical Grid Equipment Creating Execution Risk in Large-Scale Grid Hardening Program Deployment

The simultaneous acceleration of grid hardening investment, renewable energy integration transmission buildout, and grid modernization programs across North America, Europe, and Asia-Pacific is creating severe supply chain congestion and extended equipment lead times for critical power infrastructure components, particularly large power transformers, high-voltage switchgear, underground cable systems, and advanced substation control equipment, whose manufacturing capacity is concentrated in a limited number of global suppliers and cannot be rapidly expanded to meet the step-change in demand driven by converging grid investment programs across multiple electricity market geographies. Large power transformer lead times, which historically ranged from 12 to 18 months for custom high-voltage units, have extended to 24 to 48 months across North American and European markets as of 2025, creating a critical bottleneck in substation hardening and transmission upgrade programs that is delaying resilience investment deployment timelines by multiple years relative to planned program schedules. The concentration of high-voltage cable manufacturing capacity in European and Asian facilities, combined with the surge in underground cable demand from wildfire hardening programs in the western United States, offshore wind transmission in Europe, and grid expansion programs across Asia-Pacific, is generating cable procurement lead times extending to 36 months for large-diameter extra-high-voltage cable systems, compelling utilities to enter long-term supply agreements and pursue domestic manufacturing investment incentives to secure the cable volumes required to execute planned undergrounding programs within committed regulatory timelines.

Workforce Skills Gap in Specialized Grid Hardening Construction and Commissioning Disciplines Constraining Program Execution Capacity

The execution of large-scale grid hardening programs encompassing underground cable installation, advanced substation construction, grid automation system deployment, and operational technology cybersecurity implementation requires specialized engineering, construction, and commissioning workforce capabilities that are in critically short supply relative to the simultaneous surge in program demand across utility, government, and transmission operator organizations, creating a workforce capacity constraint that is limiting the pace of grid resilience investment execution independently of capital availability or regulatory approval status. Underground cable installation requires specialized directional drilling, cable pulling, splicing, and high-voltage testing expertise that is distinct from conventional overhead line construction skills, and the training pipeline for certified high-voltage cable installation professionals requires multiple years to develop the hands-on competency and safety certification credentials needed for independent deployment on live transmission system projects. Grid automation and advanced metering infrastructure deployment programs require integration engineers and commissioning specialists with combined power systems, information technology, and cybersecurity competencies that are scarce in the existing utility and contractor workforce, and whose development through university, apprenticeship, and industry certification programs lags substantially behind the demand growth generated by the accelerating digitalization of grid hardening and resilience investment programs across major electricity market geographies through the forecast period.

Market Segmentation

- Segmentation By Solution Type

- Physical Grid Hardening (Undergrounding, Covered Conductors, Pole Upgrades)

- Substation Hardening and Protection Systems

- Advanced Distribution Automation and Self-Healing Grid Systems

- Microgrid and Distributed Energy Resource Integration

- Grid Cybersecurity and Operational Technology Protection

- Transmission System Reinforcement and Expansion

- Emergency Response and Rapid Restoration Systems

- Others

- Segmentation By Technology

- High-Voltage Underground Cable Systems

- Advanced Metering and Grid Monitoring Infrastructure

- Energy Management and SCADA Systems

- Battery Energy Storage Systems for Grid Support

- Power Electronics (FACTS Devices, HVDC, Grid-Forming Inverters)

- Physical Security and Perimeter Protection Systems

- Vegetation Management Technologies

- Others

- Segmentation By Infrastructure Type

- Transmission Infrastructure (Above 100 kV)

- Sub-Transmission Infrastructure (33 kV to 100 kV)

- Distribution Infrastructure (Below 33 kV)

- Substation Infrastructure

- Grid Control and Communication Infrastructure

- Others

- Segmentation By Threat Type Addressed

- Extreme Weather and Climate Resilience (Hurricane, Wildfire, Flood, Ice)

- Seismic Resilience

- Cybersecurity and Operational Technology Protection

- Physical Security and Sabotage Prevention

- Electromagnetic Pulse and Geomagnetic Disturbance Protection

- Others

- Segmentation By Utility Type

- Investor-Owned Utilities

- Publicly Owned Utilities and Municipal Electric Utilities

- Rural Electric Cooperatives

- Independent Transmission System Operators

- National Grid and State-Owned Utilities

- Others

- Segmentation By End User

- Electric Utilities and Grid Operators

- Government and Defense Agencies

- Critical Facility Operators (Hospitals, Data Centers, Water Treatment)

- Industrial and Commercial Facility Operators

- Renewable Energy Project Developers

- Others

- Segmentation By Deployment Model

- Greenfield Infrastructure Deployment

- Brownfield Retrofit and Upgrade Programs

- Emergency and Disaster Recovery Deployment

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Grid Hardening and Resilient Power Infrastructure Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by solution type, technology, infrastructure type, and threat category, to enable utilities, grid technology vendors, engineering contractors, government agencies, and infrastructure investors to identify which resilience solution segments will generate the highest absolute revenue and most durable investment pipeline across the forecast period?

- How are the increasing frequency and economic severity of extreme weather events, including major hurricanes, wildfires, ice storms, and flooding incidents, reshaping utility grid hardening investment priorities, regulatory cost recovery frameworks, and capital expenditure program timelines across North America, Europe, and Asia-Pacific, and what is the projected aggregate incremental utility infrastructure hardening investment attributable to climate resilience requirements through 2034 by geography and infrastructure type?

- What is the projected market size, compound annual growth rate, and technology adoption trajectory of the grid cybersecurity and operational technology protection segment through 2034, and how are evolving regulatory compliance frameworks including NERC CIP standards in North America and the NIS2 Directive in Europe driving mandatory cybersecurity investment commitments across transmission operators, distribution utilities, and critical facility operators?

- How are large-scale renewable energy integration requirements, specifically the transmission and distribution reinforcement needs generated by utility-scale solar and wind capacity additions, driving convergent investment in grid hardening and power system stabilization technologies, and what is the estimated additional transmission and distribution infrastructure investment required through 2034 to simultaneously accommodate renewable energy integration targets and meet evolving grid resilience and reliability standards?

- Who are the leading grid hardening technology vendors, underground cable manufacturers, advanced substation equipment suppliers, grid automation system integrators, and grid cybersecurity solution providers currently defining the competitive landscape of the global market, and what are their respective technology portfolios, geographic market positioning, manufacturing capacity expansion plans, strategic partnerships with utilities and government agencies, and competitive differentiation strategies in response to the structural acceleration of grid resilience investment across major electricity market geographies?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Extreme Weather, Climate Change & Physical Asset Vulnerability Risk

- Cybersecurity, EMP & Physical Attack Risk to Critical Grid Infrastructure

- Regulatory, Permitting & Utility Rate Recovery Risk

- Supply Chain, Material Scarcity & Equipment Lead Time Risk

- Financing, Capital Allocation & Stranded Asset Risk in Grid Transition

- Regulatory Framework & Standards

- NERC CIP Standards, FERC Orders & National Critical Infrastructure Protection Mandates for Grid Hardening

- State & Federal Grid Modernisation, Resilience Investment & Wildfire Mitigation Regulatory Frameworks

- Building Codes, Undergrounding Mandates & Utility Resilience Planning Requirements

- Environmental, Land Use, Permitting & Right-of-Way Regulations for Grid Infrastructure Projects

- Green Finance, Climate Resilience Bonds, ESG Disclosure & Sustainable Infrastructure Procurement Standards

- Global Grid Hardening and Resilient Power Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Installed Capacity, GW and Circuit-km)

- Market Size & Forecast by Infrastructure Type

- Transmission Grid Hardening Infrastructure (Underground Cabling, Overhead Line Replacement & Storm-Hardened Towers)

- Distribution Grid Resilience & Modernisation Infrastructure

- Substation Hardening, Protection Systems & Physical Security Infrastructure

- Microgrids & Islanding-Capable Distributed Energy Systems for Critical Load Protection

- Grid-Scale Battery Energy Storage Systems (BESS) for Resilience & Backup Power

- Advanced Metering Infrastructure (AMI) & Smart Grid Communication Networks

- EMP & Geomagnetic Disturbance (GMD) Hardening Infrastructure

- Wildfire Mitigation, Rapid De-Energisation & Vegetation Management Infrastructure

- Flood, Storm & Climate Resilience Infrastructure for Grid Assets

- Market Size & Forecast by Technology

- Underground & Submarine Cable Technology

- Self-Healing Grid & Automated Fault Location, Isolation & Restoration (FLISR) Technology

- Advanced Protection Relays, SCADA & Energy Management System (EMS) Technology

- Grid-Scale BESS & Hybrid Storage Technology

- Microgrid Controller & Islanding Technology

- EMP Hardening, Faraday Protection & GMD Mitigation Technology

- Wildfire Detection, Sensor & Rapid De-Energisation Technology

- AI-Based Predictive Grid Maintenance & Digital Twin Technology

- Drone-Based Inspection & Robotic Asset Management Technology

- Market Size & Forecast by Grid Level

- Transmission (Extra-High & High Voltage, Above 115 kV)

- Sub-Transmission (33 kV to 115 kV)

- Distribution (Low & Medium Voltage, Below 33 kV)

- Behind-the-Meter & Microgrid

- Market Size & Forecast by Threat Type Addressed

- Natural Disaster Resilience (Hurricane, Wildfire, Flood & Ice Storm)

- Climate Change & Extreme Weather Adaptation

- Cyber & Physical Security

- Aging Infrastructure Replacement & Reliability Improvement

- EMP & Geomagnetic Disturbance (GMD) Hardening

- Market Size & Forecast by Project Type

- New Build & Greenfield Grid Infrastructure

- Brownfield Retrofit, Upgrade & Hardening Projects

- Emergency Restoration & Rapid Deployment

- Market Size & Forecast by Application

- Bulk Power Transmission Networks

- Urban & Suburban Distribution Networks

- Rural & Remote Grid Infrastructure

- Critical Facility & Defence Installation Power Security

- Industrial & Mining Power Infrastructure

- Renewable Energy Integration & Grid Connection Infrastructure

- Market Size & Forecast by End-User

- Investor-Owned Utilities (IOUs)

- Publicly-Owned & Municipal Utilities

- Cooperative & Rural Electric Utilities

- Transmission System Operators (TSOs) & Independent System Operators (ISOs)

- Government & Defence Agencies

- Industrial & Commercial End-Users

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Project Contract (Engineering, Procurement & Construction)

- Public-Private Partnership (PPP), BOT & Concession Contract

- Direct Equipment & Technology Supply with System Integration

- Operations & Maintenance (O&M) Service & Performance Contract

- North America Grid Hardening and Resilient Power Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW and Circuit-km)

- By Infrastructure Type

- By Technology

- By Grid Level

- By Project Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Grid Hardening and Resilient Power Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW and Circuit-km)

- By Infrastructure Type

- By Technology

- By Grid Level

- By Project Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Grid Hardening and Resilient Power Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW and Circuit-km)

- By Infrastructure Type

- By Technology

- By Grid Level

- By Project Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Grid Hardening and Resilient Power Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW and Circuit-km)

- By Infrastructure Type

- By Technology

- By Grid Level

- By Project Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Grid Hardening and Resilient Power Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW and Circuit-km)

- By Infrastructure Type

- By Technology

- By Grid Level

- By Project Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Grid Hardening and Resilient Power Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW and Circuit-km)

- By Infrastructure Type

- By Technology

- By Grid Level

- By Project Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Underground & Submarine Transmission Cable Technology Deep-Dive

- Self-Healing Grid, FLISR & Automated Distribution System Technology

- Grid-Scale BESS & Hybrid Storage Technology for Resilience Applications

- Microgrid & Islanding Technology for Critical Load Protection

- EMP Hardening, Faraday Protection & GMD Mitigation Technology

- Wildfire Detection, Rapid De-Energisation & Vegetation Management Technology

- AI-Based Predictive Maintenance, Digital Twin & Grid Analytics Technology

- Patent & IP Landscape in Grid Hardening & Resilience Technologies

- Value Chain & Supply Chain Analysis

- Underground Cable, Conduit & Accessories Manufacturing Supply Chain

- Overhead Line, Conductor, Tower & Hardware Manufacturing Supply Chain

- Substation Equipment (Transformer, Switchgear & Protection Relay) Supply Chain

- BESS Cell, Module, Inverter & System Integration Supply Chain

- Smart Grid Communication, AMI & Sensor Equipment Supply Chain

- EPC Contractor, Grid Engineer & System Integrator Procurement Landscape

- Utility Operator, Grid Owner & Offtake Partner Channel

- Pricing Analysis

- Underground Transmission & Distribution Cable Installation Capital Cost Analysis

- Substation Hardening & Protection Upgrade Capital Cost Analysis

- Grid-Scale BESS Capital Cost, Levelised Cost of Storage (LCOS) & Resilience Value Analysis

- Microgrid & Distributed Resilience Infrastructure Cost Analysis

- Grid Hardening Project Finance, Utility Rate Recovery & Revenue Structure Analysis

- Total Grid Hardening Project Economics: Levelised Cost of Resilience (LCoR) Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Grid Hardening Infrastructure: Carbon Footprint, Energy Intensity & Material Use Across Technology Routes

- Carbon Neutrality & Net Zero Contribution of Grid Hardening & Renewable Integration Infrastructure

- Climate Resilience, Adaptation Benefits & Avoided Outage Cost of Grid Hardening Investment

- Environmental Compliance, Land Use Impact & Biodiversity Consideration in Grid Infrastructure Siting

- Regulatory-Driven Sustainability, SDG 7 (Affordable Energy) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Technology & Geography

- Player Classification

- Integrated Power & Grid Technology Companies

- Specialist Underground & Overhead Transmission Cable Manufacturers

- Substation, Transformer & Switchgear Equipment Manufacturers

- Grid-Scale BESS & Energy Storage System Integrators

- Smart Grid, AMI & Grid Communication Technology Providers

- Microgrid Controller & Distributed Resilience System Providers

- EMP Hardening & Physical Security Specialist Providers

- EPC Contractors & Grid Infrastructure Project Developers Specialising in Resilience

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Grid Hardening Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Grid Hardening Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output