Global Offshore Energy Hubs Market By Hub Type, By Energy Source, By Energy Output, By Infrastructure Component, By Water Depth, By End Use Application, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Offshore Energy Hubs Market encompasses the planning, development, construction, and operation of integrated offshore infrastructure platforms combining multiple renewable energy generation sources, energy conversion and storage systems, and transmission infrastructure at sea, including offshore wind farm clusters with integrated electrolysis and green hydrogen production, offshore power-to-ammonia conversion facilities, multi-energy offshore platforms, and associated subsea cable, pipeline, and floating platform systems, developed by energy companies, utilities, and government agencies to generate, process, and export clean energy to onshore and international markets.

Market Insights

The global offshore energy hubs market is emerging as one of the most strategically ambitious infrastructure development concepts of the global energy transition, representing the convergence of accelerating offshore wind technology maturity, the urgent search for scalable clean energy carrier production pathways, and the geographic reality that the world’s most exceptional wind and solar resources are frequently located far from existing onshore grid infrastructure, making offshore integration of generation, conversion, and export systems a more practical and economically compelling pathway than long-distance onshore transmission for certain resource locations and energy demand configurations. The market was valued at approximately USD 6.1 billion in 2025 and is projected to expand at a compound annual growth rate of 31.8% through 2034, as national energy strategies in Europe, Asia-Pacific, the Middle East, and increasingly North America and Latin America incorporate offshore energy hub development as a central pillar of their clean energy infrastructure investment programs, with first-generation commercial hub projects advancing from feasibility study and permitting stages toward financial close and construction commitments across multiple North Sea, Asia-Pacific, and Australian development zones.

The North Sea is the most advanced regional development environment for offshore energy hubs, anchored by the collective ambition of Denmark, Germany, the Netherlands, Belgium, the United Kingdom, and Norway to develop coordinated offshore wind and green hydrogen production infrastructure that transforms the North Sea into a pan-European clean energy production basin serving both domestic electricity grid needs and industrial hydrogen demand. The Danish Energy Islands concept, encompassing the Bornholm and North Sea energy island developments that will aggregate offshore wind generation from surrounding wind farms and convert surplus electricity to green hydrogen for export through dedicated offshore pipeline infrastructure, represents the most structurally advanced offshore energy hub program in terms of regulatory framework development, political commitment, and project definition maturity. These pioneering programs are establishing the infrastructure engineering standards, regulatory frameworks, financing structures, and technology integration models that subsequent offshore energy hub developments globally will draw upon as reference points for their own project design and financing.

Floating offshore wind technology is an enabling development for offshore energy hubs at deep water sites beyond the reach of bottom-fixed foundation systems, opening the exceptional wind resources of the deep Atlantic, Pacific, and Indian Ocean zones to commercial development for the first time and substantially expanding the geographic opportunity space for offshore energy hub siting beyond the relatively shallow and geographically constrained seabed areas suitable for monopile and jacket foundation installations. Floating wind platforms integrated with offshore electrolysis units and subsea hydrogen export pipelines represent the long-term deep-water offshore energy hub architecture whose commercial viability is advancing as floating wind turbine costs decline along their own learning curve trajectory and offshore electrolyzer system engineering matures through shallow water demonstration projects. The integration of offshore carbon capture and storage infrastructure with offshore energy hub development is attracting interest from governments in the United Kingdom, Norway, and the Netherlands as a pathway for combining renewable energy production with industrial carbon sequestration in a shared offshore infrastructure framework that leverages common platform, pipeline, and marine logistics assets.

Europe leads the global offshore energy hubs market by policy framework development, project pipeline maturity, and public investment commitment, supported by European Union hydrogen strategy targets, member state national energy island programs, and the REPowerEU framework that elevated offshore energy hub development to a continental energy security priority. Asia-Pacific is the fastest-growing regional market, driven by Japan and South Korea’s offshore wind and green hydrogen import strategies, Australia’s vast offshore wind and solar resources creating exceptional offshore hub development potential for both domestic decarbonization and Asian clean energy export, and China’s accelerating offshore wind deployment providing the foundation for future integrated offshore energy hub development. The Middle East is emerging as an offshore energy hub development frontier, leveraging sovereign wealth fund investment capacity and exceptional offshore wind and floating solar resource potential in the Red Sea and Arabian Sea to pursue offshore clean energy production for hydrogen export to European and Asian markets.

Key Drivers

Offshore Wind Capacity Scaling and Technological Maturation Creating the Generation Foundation Required for Economically Viable Integrated Offshore Energy Hub Development at Commercial Scale

The rapid maturation of offshore wind technology through successive turbine capacity generations approaching and exceeding fifteen megawatts per unit, progressively improving capacity factors achievable at deeper water and higher-wind-resource sites, and the accumulating engineering experience base from hundreds of gigawatts of installed offshore wind capacity across Europe and Asia-Pacific is establishing the technical and commercial foundation upon which offshore energy hub integration concepts can be constructed with growing confidence in generation performance, operational reliability, and project financing bankability. The convergence of declining offshore wind levelized cost of electricity with improving electrolyzer system efficiency and capital cost reduction trajectories is bringing offshore green hydrogen production economics toward viability thresholds that project developers and energy offtakers require to justify the substantial infrastructure investment commitments that offshore energy hub development necessitates.

European Energy Security Imperatives and Green Hydrogen Import Demand Creating Durable Policy and Commercial Demand Pull for Large-Scale Offshore Energy Hub Infrastructure Investment

The structural energy security vulnerability exposed by geopolitical supply disruptions has elevated offshore energy hub development from a long-term strategic option to an immediate policy priority for European governments seeking to replace fossil fuel import dependency with domestically controlled or allied-nation offshore renewable energy production infrastructure. The European Union REPowerEU plan’s explicit green hydrogen import targets, supported by developing bilateral hydrogen partnership agreements between European import nations and potential offshore hub host countries including Norway, Morocco, Namibia, and Australia, are providing the demand signal and policy framework stability that project developers require to advance offshore energy hub feasibility studies toward investment decisions. National energy island programs with government balance sheet support are further de-risking the first generation of commercial offshore hub developments.

Offshore Spatial Planning Advantages and Co-Location Efficiency Benefits of Integrated Multi-Energy Hub Development Improving Project Economics Relative to Dispersed Single-Technology Offshore Infrastructure

Developing offshore wind, electrolysis, energy conversion, and export infrastructure as an integrated hub rather than as separate dispersed installations enables sharing of offshore platform structures, marine access and logistics systems, subsea cable and pipeline installation campaigns, power management and monitoring infrastructure, and operations and maintenance vessel fleets across multiple energy system components, generating capital and operational expenditure synergies that improve overall hub project economics relative to the sum of independently developed offshore energy infrastructure components. The ability to optimize power routing between grid export, hydrogen production, and ammonia or methanol synthesis applications in real time based on market conditions, grid balancing requirements, and electrolyzer operational efficiency windows further enhances the economic value capture potential of integrated offshore hub configurations relative to single-output offshore energy development.

Key Challenges

Extreme Complexity and Capital Cost of First-Generation Offshore Energy Hub Projects Creating Financing Structures of Unprecedented Scale and Risk Profile for Infrastructure Capital Markets

Offshore energy hubs combining large-scale wind generation, offshore electrolysis facilities, energy carrier conversion systems, subsea export pipelines or high-voltage cable infrastructure, and offshore platform construction represent projects of capital cost and technical complexity that substantially exceed the investment scale and risk profile of conventional offshore wind or onshore hydrogen production projects, requiring financing structures that combine sovereign balance sheet commitments, multilateral development bank participation, export credit agency coverage, and private infrastructure capital in configurations that have limited precedent in existing project finance markets and require substantial financial structuring innovation to achieve bankable risk allocation frameworks acceptable to all investor classes simultaneously. The absence of commercially operational offshore energy hub reference projects generates first-of-a-kind risk premiums that increase the cost of capital and extend the financing timeline for early hub developments beyond what conventional offshore energy project financing processes can accommodate.

Offshore Regulatory Framework Gaps, Maritime Spatial Planning Complexity, and Multi-Jurisdictional Permitting Requirements Creating Extended Development Timeline Uncertainty for Offshore Hub Projects

Offshore energy hub development occupies a regulatory space at the intersection of offshore energy licensing, maritime safety regulation, environmental impact assessment, subsea pipeline and cable permitting, international maritime law, and in some cases bilateral treaty frameworks governing cross-border offshore infrastructure, creating multi-agency permitting processes of exceptional complexity that require coordination across national energy ministries, maritime authorities, environmental agencies, fisheries regulators, and defense establishments whose individual approval processes do not follow a common timeline or decision framework. The lack of purpose-designed regulatory pathways for integrated offshore multi-energy hub infrastructure in most jurisdictions means that developers must navigate permitting processes assembled from frameworks designed for single-technology offshore installations, introducing approval uncertainty and timeline risk that complicates project financing and investment decision scheduling.

Offshore Electrolyzer System Reliability, Marine Environment Qualification, and Operations and Maintenance Accessibility Constraints Limiting Confidence in Offshore Hydrogen Production Performance Projections

Deploying electrolysis systems in offshore marine environments introduces equipment reliability, corrosion protection, humidity management, and maintenance accessibility challenges that are substantially more demanding than onshore electrolyzer installation conditions, and the limited operational experience with offshore electrolysis systems at commercially relevant scales means that equipment manufacturers, project developers, and financing institutions cannot yet base offshore electrolyzer reliability, availability, and maintenance cost projections on statistically robust operational data from comparable deployed systems. The practical constraints on maintenance access imposed by weather window limitations, marine crew transfer vessel availability, and offshore logistics complexity reduce the corrective maintenance responsiveness achievable for offshore electrolyzer faults compared to onshore facilities, requiring higher redundancy design margins and more conservative availability assumptions that affect project financial modeling and electrolyzer procurement specifications.

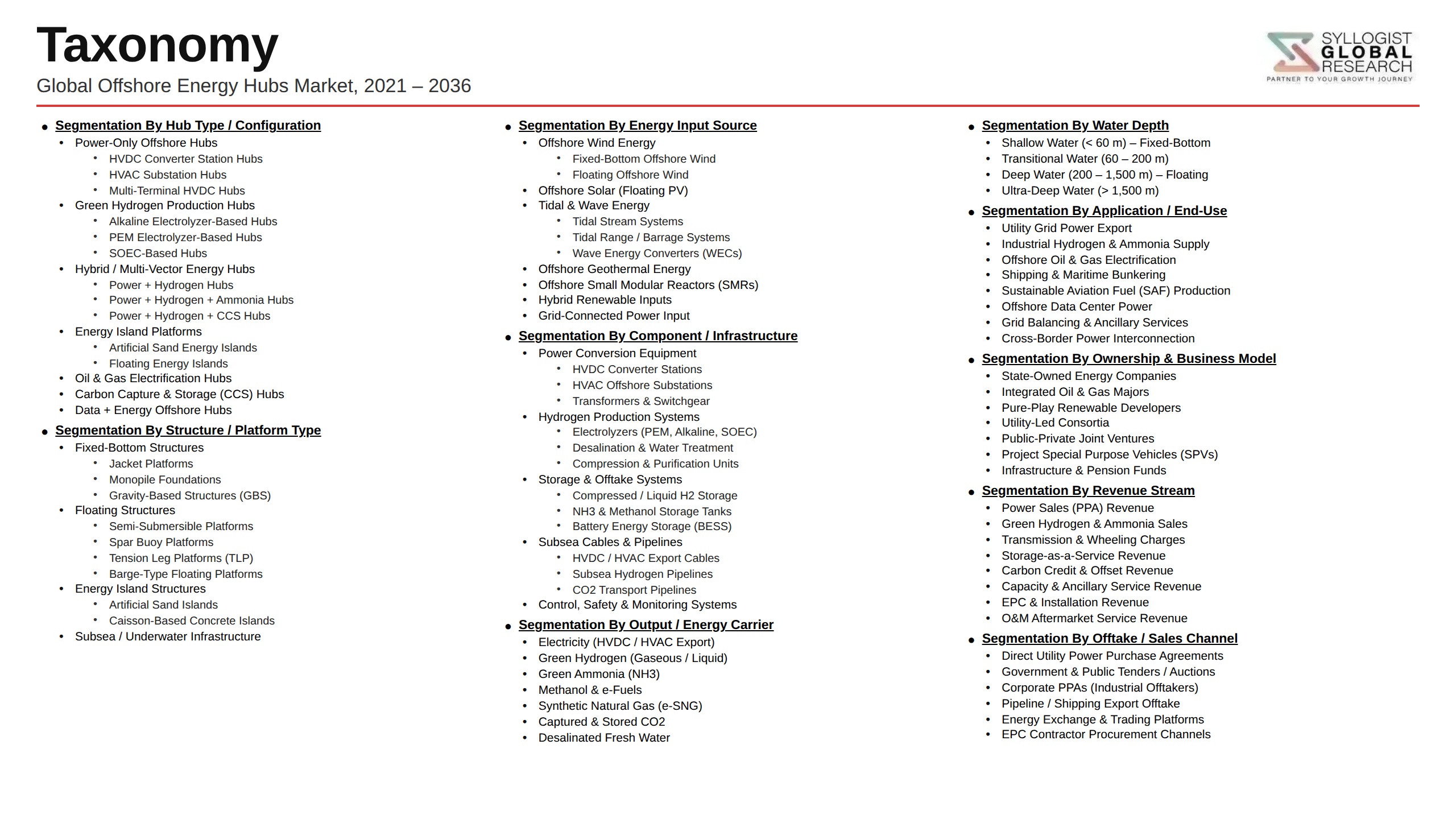

Market Segmentation

- Segmentation By Hub Type

- Offshore Wind-to-Hydrogen Energy Hubs

- Offshore Wind-to-Ammonia Production Hubs

- Offshore Wind-to-Methanol and Synthetic Fuel Hubs

- Multi-Energy Offshore Integration Platforms

- Offshore Energy Islands and Artificial Energy Platforms

- Floating Offshore Wind-Integrated Energy Hubs

- Others

- Segmentation By Energy Source

- Fixed-Bottom Offshore Wind

- Floating Offshore Wind

- Offshore Solar Photovoltaic (Floating)

- Hybrid Offshore Wind and Solar Systems

- Wave and Tidal Energy Integration

- Others

- Segmentation By Energy Output

- Green Hydrogen (Pipeline and Liquefied Export)

- Green Ammonia

- Synthetic Methane and Power-to-Gas

- Power-to-Liquid Synthetic Fuels

- Direct Electricity Grid Export

- Combined Electricity and Hydrogen Co-Export

- Others

- Segmentation By Infrastructure Component

- Offshore Wind Turbines and Foundation Systems

- Offshore Electrolysis and Hydrogen Production Systems

- Offshore Ammonia and Methanol Synthesis Plants

- Subsea Export Pipelines and Hydrogen Infrastructure

- High-Voltage Offshore Transmission Cables

- Offshore Platform and Topside Structures

- Floating Storage and Offloading Vessels

- Others

- Segmentation By Water Depth

- Shallow Water (Below 60 Meters)

- Transitional Water (60 to 200 Meters)

- Deep Water (200 to 1000 Meters)

- Ultra-Deep Water (Above 1000 Meters)

- Segmentation By End Use Application

- Industrial Hydrogen and Chemical Feedstock Supply

- Grid Electricity Export and Balancing

- Maritime Bunkering and Shipping Fuel

- Sustainable Aviation Fuel Production

- National Grid Decarbonization and Energy Security

- Cross-Border Clean Energy Export

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global offshore energy hubs market valuation in 2025, projected through 2034, segmented by hub type, energy output, and region, enabling offshore energy developers, infrastructure investors, government energy agencies, and offtake partners to identify the most commercially advanced project development opportunities and highest-value offshore hub investment pathways across the global market?

- How are national energy island programs in Denmark, Germany, and the Netherlands, combined with bilateral green hydrogen partnership agreements between European import nations and offshore hub development countries including Norway, Morocco, Namibia, and Australia, shaping the project pipeline maturity, infrastructure investment commitments, and financing structure development of the first generation of commercial offshore energy hub projects through 2034?

- Which offshore energy hub configurations, specifically offshore wind-to-hydrogen with pipeline export, offshore wind-to-ammonia with shipping export, and multi-energy hub platforms with combined electricity and hydrogen co-export, offer the most favorable project economics, offtake contract structures, and risk-adjusted investment returns at current and projected technology cost trajectories through 2034?

- How are floating offshore wind technology cost trajectories, offshore electrolyzer system marine qualification programs, and subsea hydrogen pipeline engineering standards developing to enable deep-water offshore energy hub project viability, and what technology performance milestones and capital cost reduction targets must be achieved to bring floating offshore energy hub project economics within financeable parameters?

- What regulatory framework development requirements, maritime spatial planning processes, multi-agency permitting coordination mechanisms, and cross-border offshore infrastructure treaty frameworks are most critically constraining offshore energy hub project development timelines, and what regulatory innovation and governmental coordination initiatives are being implemented to establish fit-for-purpose approval pathways for integrated offshore multi-energy hub developments?

- How is the competitive landscape structured among offshore energy hub project developers, offshore wind original equipment manufacturers, electrolyzer technology suppliers, offshore engineering procurement and construction contractors, and infrastructure financing institutions, and what consortium formation, technology partnership, and risk-sharing arrangements are emerging as the preferred project development structures for first-generation commercial offshore energy hub investments?

- Which regional offshore energy hub development zones, specifically the North Sea, Australian offshore basins, Japanese and Korean exclusive economic zones, and the Red Sea and Arabian Sea, offer the most compelling combination of renewable resource quality, water depth suitability, proximity to demand markets, regulatory framework readiness, and infrastructure development ecosystem maturity for near-term commercial offshore energy hub project advancement?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Offshore Construction Complexity, Extreme Weather Exposure & Marine Logistics Execution Risk

- Subsea Cable, Interconnector Delay & Grid Integration Bottleneck Risk

- Seabed Leasing, Maritime Spatial Planning, EEZ Jurisdiction & Multi-Stakeholder Permitting Risk

- Offtake Market Development, Energy Carrier Price Volatility & Hub Revenue Uncertainty Risk

- Geopolitical Tension, Offshore Security, Sabotage & Critical Infrastructure Protection Risk

- Technology Integration, Floating Platform Reliability & First-of-a-Kind Hub Execution Risk

- Regulatory Framework & Standards

- Offshore Wind Leasing, Seabed Rights, Maritime Spatial Planning & Exclusive Economic Zone (EEZ) Regulatory Frameworks

- Offshore Energy Hub Permitting, Environmental Impact Assessment & Habitat Regulation Compliance

- Offshore Electrical Infrastructure Standards: IEC 61400-22, Offshore Grid Connection Codes & Subsea Cable Regulatory Requirements

- Green Hydrogen, RFNBO Certification & Offshore Power-to-X Regulatory Frameworks

- Offshore Safety, Marine Operations & OSPAR Convention Environmental Standards for Energy Installations

- Cross-Border Offshore Energy Trade, HVDC Interconnector Frameworks & Multi-Nation Hub Governance

- Global Offshore Energy Hubs Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Installed Capacity, GW & Energy Output, TWh/year)

- Market Size & Forecast by Hub Type

- Offshore Wind Energy Hubs & Large-Scale Wind Power Clusters

- Offshore Green Hydrogen Production Hubs (Power-to-Hydrogen)

- Offshore Green Ammonia & Power-to-X Production Hubs

- Offshore Multi-Energy Hubs (Wind, Solar, Wave & Tidal Integration)

- Offshore Oil & Gas Platform Electrification & Energy Transition Hubs

- Artificial Energy Islands & Offshore Hub-and-Spoke Infrastructure

- Offshore Floating Energy Hubs & Deep-Water Energy Platforms

- Market Size & Forecast by Energy Source Technology

- Fixed-Bottom Offshore Wind (Monopile, Jacket & Gravity Base)

- Floating Offshore Wind (Semi-Submersible, Spar Buoy & Tension Leg Platform)

- Offshore Solar PV & Floating Solar Integrated with Hub Infrastructure

- Wave Energy Converters & Tidal Stream Turbines

- Offshore Nuclear (Floating SMR) Power Generation

- Market Size & Forecast by Energy Output & Carrier

- Grid-Connected Electricity Export via HVDC & HVAC Submarine Cables

- Green Hydrogen (Pipeline, Liquefied & Ammonia Carrier-Based Export)

- Green Ammonia & Synthetic Fuel Production & Export

- Direct Industrial Supply (Offshore Electrolysis & On-Shore Industrial Park Integration)

- Hybrid Export (Electricity & Hydrogen/Derivatives Combined)

- Market Size & Forecast by Infrastructure Component

- Offshore Wind Turbines, Foundations & Installation Vessels

- Offshore Electrical Infrastructure (Offshore Substations, Array Cables & Export Cables)

- Offshore Electrolyser Platforms & Floating Hydrogen Production Units

- Offshore Energy Storage (Battery, Hydrogen Buffer & Compressed Gas Storage)

- Offshore Platform Topside, Jacket, Floater & Marine Structural Systems

- Port, Onshore Terminal & Grid Connection Infrastructure

- Offshore Operations & Maintenance (O&M) Vessels & Remote Monitoring Systems

- Market Size & Forecast by Water Depth & Distance from Shore

- Nearshore Hubs (Below 30 km from Shore, Below 30m Water Depth)

- Mid-Distance Hubs (30 km to 80 km from Shore, 30m to 60m Water Depth)

- Far-Shore Hubs (80 km to 200 km from Shore, 60m to 150m Water Depth)

- Deep-Water & Ultra-Deep Floating Hubs (Above 200 km or Above 150m Water Depth)

- Market Size & Forecast by Application

- National Grid Power Supply & Renewable Energy Target Fulfilment

- Green Hydrogen & E-Fuel Export for Industrial Decarbonisation

- Cross-Border Electricity Trading & Multi-Nation Grid Interconnection

- Offshore Industrial Energy Supply (Oil & Gas Platform Electrification & Desalination)

- Port & Maritime Bunkering Hub (Green Ammonia & Hydrogen for Shipping)

- Island & Remote Community Energy Supply

- Market Size & Forecast by End-User

- National Transmission System Operators (TSOs) & Grid Authorities

- Offshore Wind Developers, Utilities & Independent Power Producers (IPPs)

- Green Hydrogen, PtX & Energy Carrier Producers & Exporters

- Oil & Gas Operators Pursuing Offshore Electrification & Energy Transition

- Industrial Offtakers, Port Authorities & Energy-Intensive Industry Clusters

- Government Agencies & National Energy Security Authorities

- Market Size & Forecast by Procurement & Delivery Model

- Government-Tendered Offshore Lease & Contract-for-Difference (CfD) Channel

- Developer-Led Private Investment & Corporate PPA Channel

- Public-Private Partnership (PPP) & Consortium Development Channel

- Intergovernmental & Multi-Nation Hub Development Channel

- North Sea & Northern Europe Offshore Energy Hubs Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW & Energy Output, TWh/year)

- By Hub Type

- By Energy Source Technology

- By Energy Output & Carrier

- By Infrastructure Component

- By Water Depth & Distance from Shore

- By Application

- By End-User

- By Country

- By Procurement & Delivery Model

- Market Size & Forecast

- Asia-Pacific Offshore Energy Hubs Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW & Energy Output, TWh/year)

- By Hub Type

- By Energy Source Technology

- By Energy Output & Carrier

- By Infrastructure Component

- By Water Depth & Distance from Shore

- By Application

- By End-User

- By Country

- By Procurement & Delivery Model

- Market Size & Forecast

- North America Offshore Energy Hubs Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW & Energy Output, TWh/year)

- By Hub Type

- By Energy Source Technology

- By Energy Output & Carrier

- By Infrastructure Component

- By Water Depth & Distance from Shore

- By Application

- By End-User

- By Country

- By Procurement & Delivery Model

- Market Size & Forecast

- Latin America & Caribbean Offshore Energy Hubs Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW & Energy Output, TWh/year)

- By Hub Type

- By Energy Source Technology

- By Energy Output & Carrier

- By Infrastructure Component

- By Water Depth & Distance from Shore

- By Application

- By End-User

- By Country

- By Procurement & Delivery Model

- Market Size & Forecast

- Middle East, Africa & Indian Ocean Offshore Energy Hubs Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW & Energy Output, TWh/year)

- By Hub Type

- By Energy Source Technology

- By Energy Output & Carrier

- By Infrastructure Component

- By Water Depth & Distance from Shore

- By Application

- By End-User

- By Country

- By Procurement & Delivery Model

- Market Size & Forecast

- Country-Wise* Offshore Energy Hubs Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, GW & Energy Output, TWh/year)

- By Hub Type

- By Energy Source Technology

- By Energy Output & Carrier

- By Infrastructure Component

- By Water Depth & Distance from Shore

- By Application

- By End-User

- By Country

- By Procurement & Delivery Model

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United Kingdom, Germany, Netherlands, Denmark, Belgium, Norway, France, Ireland, Sweden, Finland, Portugal, China, Japan, South Korea, Australia, Taiwan, United States, Canada, Brazil, Chile, Saudi Arabia, UAE, Oman, South Africa, Morocco

- Technology Landscape & Innovation Analysis

- Floating Offshore Wind Technology Deep-Dive: Semi-Submersible, Spar & TLP Designs, Mooring Systems & Dynamic Cable Technology

- Artificial Energy Island & Hub-and-Spoke Offshore Electrical Infrastructure: Princess Elisabeth Island & Dogger Bank Hub Concepts

- Offshore Electrolysis Technology: Onshore vs. Nearshore vs. Far-Offshore Electrolyser Siting, Power Conditioning & Saltwater Desalination

- HVDC Offshore Grid Technology: Multi-Terminal HVDC, Offshore HVDC Converter Platforms & Meshed Offshore Grid Architecture

- Offshore Energy Storage Technology: Gravity-Based, Compressed Gas, Hydrogen Buffer & Floating Battery Platform Systems

- Digital Twin, Autonomous Inspection, Drone & ROV Technology for Offshore Energy Hub Operations & Maintenance

- Next-Generation Offshore Wind Turbine Technology: 20+ MW Turbines, Direct Drive & Advanced Blade Material Advances

- Patent & IP Landscape in Offshore Energy Hub Technologies

- Value Chain & Supply Chain Analysis

- Offshore Wind Turbine, Nacelle, Blade & Tower Manufacturing Supply Chain

- Monopile, Jacket, Floater & Offshore Foundation Steel Fabrication Supply Chain

- Offshore Substation, HVDC Converter Platform & Subsea Cable Supply Chain

- Electrolyser, Hydrogen Compressor, Liquefaction & Ammonia Synthesis Equipment Supply Chain

- Offshore Installation Vessels, Jack-Up Rigs, Cable Lay Vessels & Marine Equipment Supply Chain

- Port & Staging Area, Fabrication Yard & Logistics Infrastructure Supply Chain

- Operations & Maintenance Service, Crew Transfer Vessel & Remote Monitoring Supply Chain

- Offtake Aggregator, Energy Trader, Grid Operator & Government Procurement Channel

- Pricing Analysis

- Offshore Wind Energy Hub Levelised Cost of Electricity (LCOE) Analysis by Technology & Water Depth

- Offshore Green Hydrogen Levelised Cost of Hydrogen (LCOH) Analysis: Far-Shore vs. Nearshore vs. Onshore Comparison

- Full-Chain Offshore Energy Hub Capital Cost (Capex) & Operating Cost (Opex) Structure Analysis

- CfD Strike Price, Auction Results & Hub Revenue Stack Analysis by Market

- Floating Offshore Wind vs. Fixed-Bottom Cost Parity & LCOE Trajectory to 2035 & 2040

- Project Finance, Debt Structure, Risk Premium & Equity Return Analysis for Offshore Hub Investments

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Offshore Energy Hubs: Carbon Payback Period, Full-Chain GHG Intensity & Land-Use Equivalence

- Marine Biodiversity Impact, Benthic Ecology, Bird & Bat Migration & Offshore Wind Environmental Mitigation Measures

- Offshore Decommissioning, Substructure Removal, Recyclability & Circular Economy for Offshore Wind & Hub Assets

- Subsea Cable EMF, Noise, Vibration & Cumulative Impact Assessment for Offshore Hub Infrastructure

- SDG 7, SDG 13 & SDG 14 Alignment, Blue Economy Contribution & Green Finance Eligibility for Offshore Energy Hubs

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Hub Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Hub Type, Energy Output & Geography

- Player Classification

- Integrated Energy Majors & Utilities Developing Large-Scale Offshore Energy Hubs

- Dedicated Offshore Wind Developers & Independent Power Producers (IPPs)

- Offshore Wind Turbine OEMs with Hub Integration Capabilities

- Offshore Infrastructure, EPC & Marine Contractor Companies

- Green Hydrogen, PtX & Offshore Electrolysis Project Developers

- Government-Owned Energy Companies & National Offshore Development Authorities

- Competitive Analysis Frameworks

- Market Share Analysis by Hub Type, Energy Output & Region

- Company Profile

- Company Overview & Headquarters

- Offshore Energy Hub Project Portfolio & Development Pipeline

- Key Customer Relationships, Offtake Agreements & Reference Projects

- Offshore Asset Footprint, Installed Capacity & Operational Hub Portfolio

- Revenue (Offshore Energy Segment) & Project Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Lease Awards, FID Announcements)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Hub Type, Energy Output, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Hub Development Portfolio & Technology Investment Strategy

- Offshore Supply Chain, Port Infrastructure & Localisation Strategy

- Geographic Expansion & New Market Entry Strategy

- Offtake, Customer & Industrial Partner Engagement Strategy

- Partnership, Consortium, M&A & Ecosystem Strategy

- Regulatory Engagement, Permitting & Policy Strategy

- Sustainability, Marine Environment & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output