Global Power-to-X Technologies Market By Technology Type, By Energy Carrier Output, By Renewable Energy Source, By Scale of Operation, By End Use Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Power-to-X Technologies Market encompasses the development, manufacture, and commercial deployment of electrolyzer systems, methanation reactors, Fischer-Tropsch synthesis units, ammonia synthesis plants, and associated balance-of-plant infrastructure that convert surplus or dedicated renewable electricity into storable and transportable energy carriers including green hydrogen, synthetic methane, synthetic liquid fuels, green ammonia, and methanol, serving industrial decarbonization, grid balancing, long-duration energy storage, heavy transport, and chemical feedstock applications across energy, industrial, and transportation sectors worldwide.

Market Insights

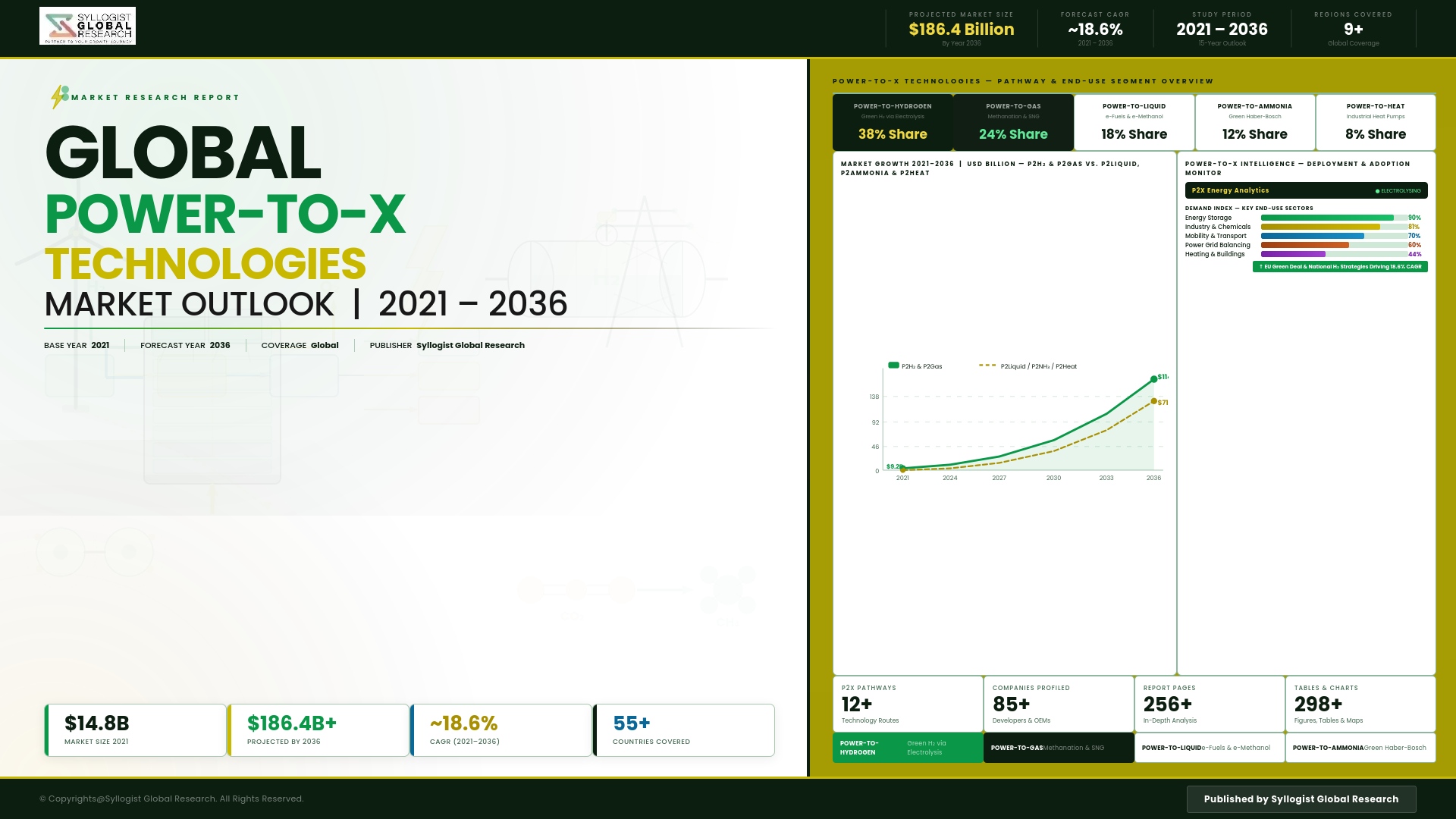

The global Power-to-X technologies market is advancing through a pivotal commercial scaling phase, propelled by the recognition among energy policymakers, industrial corporations, and infrastructure investors that electrolysis-based renewable energy conversion represents the most technically credible and economically scalable pathway for decarbonizing energy consumption in sectors that cannot be directly electrified, including long-haul aviation, maritime shipping, steel production, chemical manufacturing, and high-temperature industrial processes. The market was valued at approximately USD 5.3 billion in 2025 and is projected to expand at a compound annual growth rate of 29.7% through 2034, driven by the accelerating commercialization of proton exchange membrane and alkaline electrolyzer technologies, the maturing policy frameworks supporting green hydrogen and e-fuel production in the European Union, Japan, South Korea, Australia, and the United States, and the growing pipeline of large-scale Power-to-X project commitments from energy companies, industrial corporations, and sovereign energy development agencies.

Green hydrogen produced through water electrolysis powered by renewable electricity is the foundational energy carrier of the Power-to-X value chain, and the economics of green hydrogen production are improving rapidly as electrolyzer capital costs decline along manufacturing scale-up and technology learning curves, renewable electricity generation costs continue their long-term downward trajectory, and project developers accumulate operational experience with large-scale electrolyzer system integration, stack management, and performance optimization at demonstration and early commercial project scales. Proton exchange membrane electrolysis is gaining market share for projects requiring dynamic load-following operation aligned with variable renewable electricity input profiles, while alkaline electrolysis maintains its position in large baseload green hydrogen production applications where its lower capital cost per unit of installed capacity and established long-term reliability record support favorable project financing assumptions. Solid oxide electrolyzer technology is progressing toward commercial deployment in high-efficiency applications including co-electrolysis of water and carbon dioxide that directly produces synthesis gas for downstream conversion to synthetic methane or liquid fuels.

The Power-to-Ammonia pathway is emerging as one of the most commercially advanced and near-term scalable Power-to-X applications, driven by the dual value proposition of green ammonia as both a directly deployable zero-carbon fertilizer feedstock and a hydrogen energy carrier with superior volumetric energy density and established global maritime shipping and storage infrastructure relative to compressed or liquefied hydrogen. Maritime shipping decarbonization is creating strong demand pull for green ammonia as a marine fuel, with major shipping companies placing orders for ammonia-fueled vessels and port operators investing in green ammonia bunkering infrastructure, establishing a durable long-term demand anchor for Power-to-Ammonia projects. Synthetic aviation fuel produced through Power-to-Liquid pathways combining green hydrogen with captured carbon dioxide is attracting intensifying investment and offtake commitment from commercial airlines facing regulatory mandates for sustainable aviation fuel blending obligations in the European Union and United Kingdom that are progressively increasing the required sustainable fuel content of aviation fuel pools.

Europe dominates the global Power-to-X market by installed capacity and policy framework maturity, anchored by the European Union Hydrogen Strategy, REPowerEU biomethane and renewable hydrogen production targets, the Renewable Energy Directive provisions establishing renewable hydrogen and renewable fuels of non-biological origin standards, and the Hydrogen Bank auction mechanisms providing production subsidies that improve the economics of early commercial Power-to-X projects. The Middle East and North Africa region is emerging as a globally significant Power-to-X production hub, leveraging the combination of exceptional solar and wind resource endowments, low-cost land availability, and strategic geographic positioning for renewable energy carrier export to European and Asian demand markets through dedicated hydrogen pipeline infrastructure and ammonia export shipping terminals under development in Saudi Arabia, the United Arab Emirates, Oman, Morocco, and Mauritania. Asia-Pacific is the fastest-growing consumption market for Power-to-X products, driven by Japan and South Korea’s hydrogen society policy frameworks and the scale of industrial decarbonization demand from the region’s energy-intensive chemical, steel, and manufacturing industries.

Key Drivers

Hard-to-Abate Sector Decarbonization Obligations and the Absence of Cost-Effective Direct Electrification Pathways Establishing Power-to-X as the Preferred Decarbonization Technology for Energy-Intensive Industries

Carbon pricing mechanisms, emissions trading scheme obligations, corporate net zero commitments, and sector-specific decarbonization regulations are compelling steel producers, chemical manufacturers, cement companies, refineries, and aviation operators to invest in deep decarbonization pathways for process energy and feedstock needs that cannot be practically addressed through direct electrification given current technology performance and economics. Power-to-X technologies provide these hard-to-abate sectors with access to green hydrogen, green ammonia, and synthetic fuels that can substitute for fossil fuel inputs in existing and adapted process infrastructure with manageable technology transition risk, creating a structurally mandated demand base for Power-to-X products that is governed by regulatory compliance timelines rather than purely discretionary investment decisions and therefore provides greater procurement visibility and offtake contract durability than speculative demand projections.

Declining Renewable Electricity and Electrolyzer Capital Costs Improving Green Hydrogen Production Economics and Progressively Closing the Cost Gap with Fossil-Derived Hydrogen Across Key Markets

The sustained reduction in solar photovoltaic and wind power generation costs over the past decade has dramatically improved the economics of renewable electricity-powered electrolysis, and continued electrolyzer manufacturing scale-up, stack performance improvement, and system integration efficiency advances are driving electrolyzer capital cost reductions that industry roadmaps project will reduce green hydrogen production costs to levels competitive with natural gas-derived grey hydrogen in resource-advantaged locations within the forecast period. Government production incentives including the United States Inflation Reduction Act clean hydrogen production tax credit, European Union Hydrogen Bank auction subsidies, and Australian and Middle Eastern government-backed offtake support programs are further improving project economics and accelerating investment decisions for large-scale Power-to-X projects that will in turn generate the manufacturing volume and operational learning required to sustain the electrolyzer cost reduction trajectory.

Renewable Energy Grid Balancing Requirements and Long-Duration Energy Storage Demand Creating a Systemic Grid Infrastructure Role for Power-to-X That Expands Its Value Beyond Fuel Production

As the share of variable renewable electricity in national grid mixes surpasses thresholds where curtailment of surplus generation during high-output, low-demand periods becomes a significant grid management and economic efficiency challenge, Power-to-X electrolysis systems operating as flexible demand-side loads that convert excess renewable electricity into stored hydrogen, ammonia, or synthetic methane provide a grid balancing service with substantial system value that complements their primary role as clean energy carrier producers. The ability of Power-to-X systems to provide long-duration seasonal energy storage through conversion of renewable electricity to chemical energy carriers that can be stored and reconverted to electricity or delivered as industrial fuel months later addresses a critical gap in the energy storage technology portfolio that battery and pumped hydro storage cannot economically fill at the multi-week to multi-month storage durations required for seasonal renewable energy balancing.

Key Challenges

Green Hydrogen and Power-to-X Product Cost Competitiveness Gap with Fossil Fuel Alternatives Constraining Near-Term Commercial Project Economics Without Sustained Policy Support

Despite significant progress in reducing electrolyzer capital costs and renewable electricity generation costs, green hydrogen and Power-to-X derived fuels and chemicals currently carry production cost premiums relative to their fossil-derived equivalents that make unsubsidized commercial deployment economically unviable in most market contexts, requiring sustained and substantial government financial support through production subsidies, carbon pricing mechanisms, blending mandates, or offtake price guarantees to bridge the cost competitiveness gap across the period until technology learning curve cost reductions and fossil fuel carbon cost internalization improve the unaided economics of Power-to-X projects. The policy continuity risk inherent in dependence on government support programs that are subject to political cycle changes, budget pressures, and competing energy priority claims represents a material investment uncertainty for Power-to-X projects requiring long-term financing commitments.

Green Hydrogen Transport, Storage, and Distribution Infrastructure Immaturity Creating Supply Chain Gaps That Constrain Power-to-X Market Development Across Both Production and Consumption Geographies

The development of a commercially functional Power-to-X market requires not only electrolyzer production capacity and renewable electricity supply but a comprehensive infrastructure ecosystem encompassing hydrogen pipeline networks or conversion to ammonia or liquid organic hydrogen carrier for long-distance transport, hydrogen refueling stations for mobility applications, port bunkering infrastructure for maritime ammonia fuel, industrial hydrogen offtake connection infrastructure, and safety and standards frameworks governing hydrogen handling across the entire supply chain, none of which exist at the scale required to support the large Power-to-X market volumes projected through the forecast period. The capital investment required to build this infrastructure in parallel with Power-to-X production capacity development creates a chicken-and-egg market development challenge that governments and industry consortia must coordinate to resolve.

Renewable Electricity Supply Additionality Requirements, Temporal Correlation Rules, and Geographic Matching Constraints Limiting the Volume of Electrolysis Capacity Eligible for Green Hydrogen Certification

Regulatory frameworks governing the certification of green hydrogen and renewable fuels of non-biological origin, particularly the European Union delegated regulations establishing the criteria for renewable hydrogen qualification, impose additionality requirements mandating that electrolysis be powered by newly installed renewable generation capacity, temporal correlation rules requiring hourly matching of renewable electricity consumption to hydrogen production, and geographic proximity constraints limiting the distance between renewable generation and electrolyzer operation, collectively restricting the volume of electrolysis capacity that can qualify for green hydrogen certification and premium market pricing. These certification requirements are significantly more constraining than project developers anticipated and are causing project rescoping, investment delays, and electrolyzer deployment plan revisions across multiple European Power-to-X project pipelines.

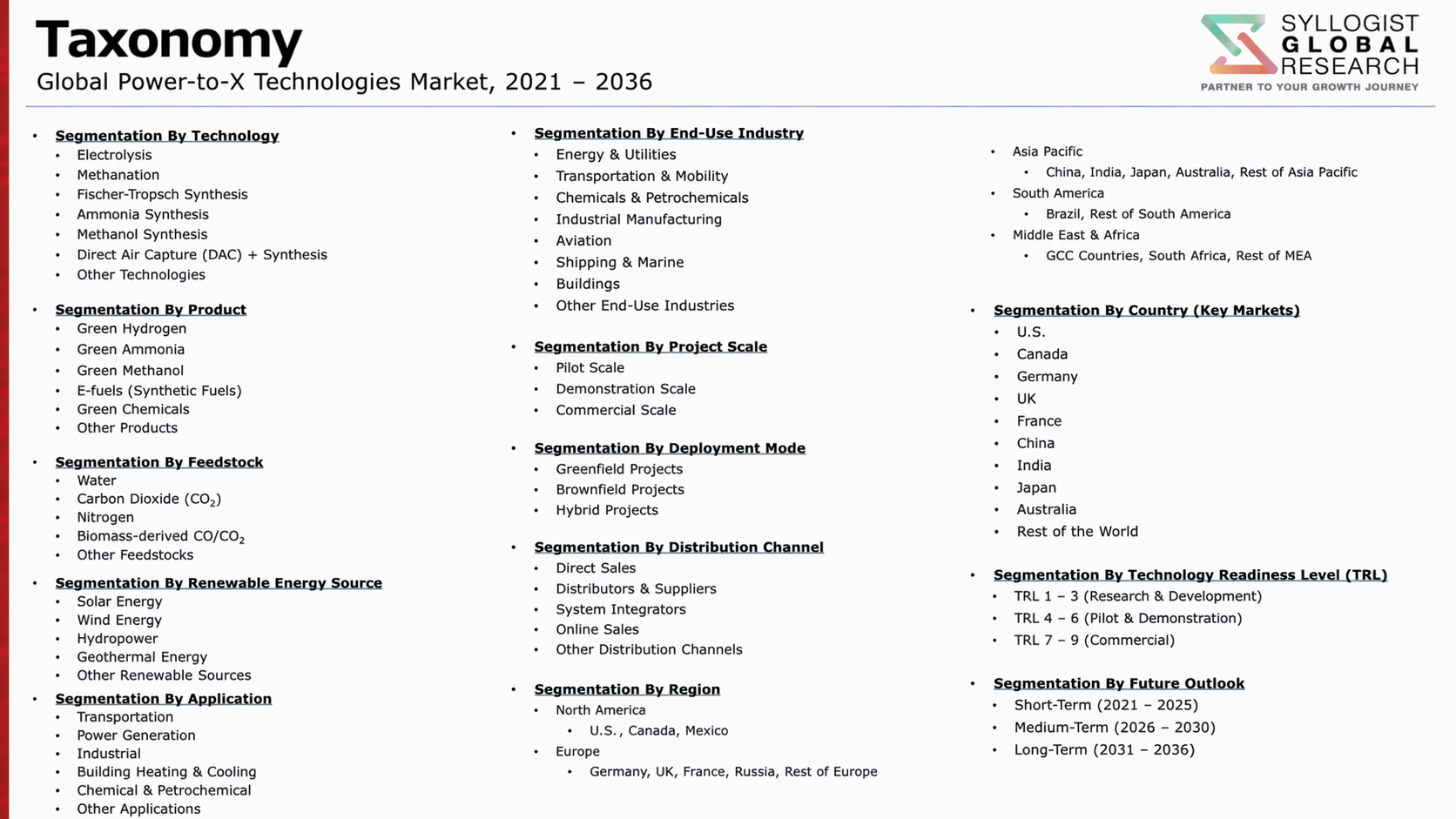

Market Segmentation

- Segmentation By Technology Type

- Alkaline Water Electrolysis Systems

- Proton Exchange Membrane Electrolysis Systems

- Solid Oxide Electrolysis and Co-Electrolysis Systems

- Anion Exchange Membrane Electrolysis Systems

- Methanation and Power-to-Gas Reactors

- Fischer-Tropsch and Power-to-Liquid Synthesis Units

- Haber-Bosch and Power-to-Ammonia Plants

- Others

- Segmentation By Energy Carrier Output

- Green Hydrogen (Gaseous and Liquefied)

- Green Ammonia

- Synthetic Methane and Power-to-Gas

- Synthetic Aviation Fuel and Power-to-Liquid

- Green Methanol and Synthetic Chemical Feedstocks

- Liquid Organic Hydrogen Carriers

- Others

- Segmentation By Renewable Energy Source

- Solar Photovoltaic-Powered Electrolysis

- Wind Power-Powered Electrolysis

- Hybrid Solar and Wind Power Systems

- Hydropower-Powered Electrolysis

- Grid-Connected Renewable Electricity

- Others

- Segmentation By Scale of Operation

- Small-Scale and Distributed Systems (Below 1 MW)

- Medium-Scale Industrial Systems (1 MW to 100 MW)

- Large-Scale Commercial Hubs (100 MW to 1 GW)

- Gigawatt-Scale Export Production Facilities

- Segmentation By End Use Application

- Industrial Feedstock and Chemical Production

- Heavy Industry Decarbonization (Steel, Cement, Refining)

- Maritime and Shipping Fuel

- Sustainable Aviation Fuel Production

- Grid Balancing and Long-Duration Energy Storage

- Road Transport and Heavy Mobility Fuel

- Residential and Commercial Heating (Power-to-Gas)

- Others

- Segmentation By End User

- Energy Utilities and Renewable Power Developers

- Industrial and Chemical Corporations

- Oil and Gas Companies Transitioning to Clean Energy

- Aviation and Maritime Operators

- Government and Sovereign Energy Agencies

- Independent Power-to-X Project Developers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global Power-to-X technologies market valuation in 2025, projected through 2034, segmented by technology type, energy carrier output, and end use application, enabling electrolyzer manufacturers, project developers, industrial offtakers, and infrastructure investors to identify the highest-growth technology pathways and most commercially viable near-term Power-to-X deployment opportunities across the global market?

- How are proton exchange membrane, alkaline, and solid oxide electrolyzer technology platforms comparing in terms of capital cost reduction trajectories, stack efficiency improvements, dynamic load-following capability, and operational lifetime performance, and which electrolyzer technology is best positioned to achieve the lowest levelized cost of green hydrogen production at large commercial scale through 2034?

- Which Power-to-X energy carrier pathways, specifically green hydrogen, green ammonia, power-to-liquid synthetic aviation fuel, synthetic methane, and green methanol, are generating the most commercially advanced offtake agreements, project financial close activity, and infrastructure investment commitments through 2034, and what end use regulatory mandates and carbon pricing mechanisms are underpinning demand pull in each pathway?

- How are the European Union Renewable Energy Directive hydrogen certification requirements, Inflation Reduction Act clean hydrogen production tax credit rules, and national hydrogen strategy frameworks in Japan, South Korea, Australia, and the Middle East shaping project economics, electrolyzer deployment investment decisions, and the geographic distribution of large-scale Power-to-X production capacity development through 2034?

- What hydrogen transport, storage, and distribution infrastructure gaps, green ammonia bunkering network development requirements, and Power-to-Liquid sustainable aviation fuel supply chain constraints are most significantly limiting the pace of Power-to-X market scaling, and what coordinated industry and government investment programs are being pursued to develop the infrastructure ecosystem required for commercially functional Power-to-X supply chains?

- How is the competitive landscape structured among electrolyzer manufacturers, integrated energy company Power-to-X project developers, independent project developers, and industrial corporation offtakers, and what technology leadership, project development capability, supply chain integration, offtake contract structuring, and export market positioning strategies are enabling leading players to build durable commercial positions across the global Power-to-X market?

- Which regional Power-to-X production hubs, specifically the Middle East and North Africa, Australia, Chile, and Northern Europe, are best positioned to become large-scale renewable energy carrier export centers through 2034, and what combinations of renewable resource endowment, land availability, export infrastructure investment, government support frameworks, and proximity to demand markets are defining competitive advantage in global Power-to-X production and trade?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Renewable Electricity Cost, Curtailment Availability & Grid Congestion Risk Affecting PtX Economics

- Electrolyser Cost Reduction, Degradation Rate & Stack Lifetime Performance Risk

- Offtake Market Development, End-Product Demand Uncertainty & Price Volatility Risk

- Permitting, Regulatory Approval, Hydrogen Safety Standards & Cross-Border Certification Risk

- CO2 Feedstock Availability, Quality & Long-Term Supply Reliability Risk for Power-to-Liquids & Power-to-Chemicals

- Project Finance, Investment Risk Premium & Long-Term Revenue Certainty for First-of-a-Kind PtX Projects

- Regulatory Framework & Standards

- EU Renewable Energy Directive (RED III), Delegated Acts & Renewable Fuels of Non-Biological Origin (RFNBO) Certification

- Green Hydrogen Standards, GHG Lifecycle Threshold & Additionality, Temporal & Geographic Correlation Rules

- Synthetic Fuels & E-Fuel Mandates: EU ReFuelEU Aviation, FuelEU Maritime & Road Transport Blending Obligations

- Carbon Capture, Utilisation & Storage (CCUS) Regulatory Frameworks & CO2 Transport & Storage Permitting

- Hydrogen Safety, Pressure Equipment, Piping & Storage Standards: ISO, IEC, ASME & Regional Regulatory Codes

- Green Finance Taxonomy, Carbon Border Adjustment Mechanism (CBAM) & Government Incentive Scheme Frameworks

- Global Power-to-X Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Installed Electrolyser Capacity, GW & Output Product, Mt/year)

- Market Size & Forecast by Technology Pathway

- Power-to-Hydrogen (PtH2): Green Hydrogen Production via Water Electrolysis

- Power-to-Ammonia (PtNH3): Green Ammonia Synthesis via Haber-Bosch & Electrochemical Routes

- Power-to-Methanol (PtMeOH): Electro-Methanol via CO2 Hydrogenation

- Power-to-Synthetic Natural Gas (PtSNG): Methanation via Sabatier Process

- Power-to-Liquid (PtL): Fischer-Tropsch & Co-Electrolysis Based Synthetic Fuels (e-Kerosene, e-Diesel & e-Naphtha)

- Power-to-Heat (PtHeat): Industrial Heat Pumps, Electric Boilers & Electrode Boilers

- Power-to-Chemicals (PtChem): E-Methane, Formic Acid, Ethylene & Specialty Chemical Production

- Power-to-Steel (PtSteel): Hydrogen Direct Reduced Iron (H-DRI) & Electric Arc Furnace Route

- Market Size & Forecast by Electrolyser Technology

- Alkaline Water Electrolysis (AWE)

- Proton Exchange Membrane (PEM) Electrolysis

- Anion Exchange Membrane (AEM) Electrolysis

- Solid Oxide Electrolysis (SOEC) & Co-Electrolysis

- Photoelectrochemical (PEC) & Solar-Driven Electrolysis

- Market Size & Forecast by Renewable Power Source

- Solar PV-Powered PtX Systems

- Onshore Wind-Powered PtX Systems

- Offshore Wind-Powered PtX Systems

- Hybrid Renewable (Solar & Wind) Powered PtX Systems

- Grid-Connected & Renewable Certificate (REC)-Based PtX Systems

- Nuclear-Powered PtX (Pink Hydrogen & Nuclear-to-X) Systems

- Market Size & Forecast by System Scale

- Small-Scale & Distributed PtX Systems (Below 10 MW Electrolyser Capacity)

- Medium-Scale Industrial PtX Systems (10 MW to 100 MW)

- Large-Scale Hub & Export-Oriented PtX Projects (100 MW to 1 GW)

- Giga-Scale PtX Export & Industrial Cluster Projects (Above 1 GW)

- Market Size & Forecast by Output Product

- Green Hydrogen (Compressed, Liquefied & Pipeline-Grade)

- Green Ammonia (Fertiliser, Shipping Fuel & Hydrogen Carrier)

- Electro-Methanol (Marine Fuel, Chemical Feedstock & H2 Carrier)

- Synthetic Natural Gas (SNG) & Biomethane Blends

- Sustainable Aviation Fuel (SAF) & E-Kerosene

- E-Diesel, E-Naphtha & Fischer-Tropsch Liquid Fuels

- Industrial Process Heat & Steam

- Green Steel (H-DRI) & Decarbonised Metal Products

- Market Size & Forecast by Application

- Industrial Decarbonisation (Steel, Cement, Chemicals & Refining)

- Aviation & Sustainable Aviation Fuel (SAF) Supply

- Maritime Shipping & Port Bunkering

- Road & Heavy-Duty Transport Fuel Supply

- Grid Balancing, Long-Duration Energy Storage & Sector Coupling

- Agricultural Fertiliser Production (Green Ammonia for Urea & AN)

- Gas Grid Injection, Hydrogen Blending & Green Gas Supply

- Export & International Green Hydrogen & Derivatives Trade

- Market Size & Forecast by End-User

- Energy Utilities, Renewable IPPs & Power-to-X Project Developers

- Industrial & Chemical Companies (Refiners, Fertiliser & Petrochemical Producers)

- Steel, Cement & Hard-to-Abate Industry Operators

- Aviation & Aerospace Companies

- Shipping Companies & Port Operators

- Gas Utilities, Pipeline Operators & Gas Grid Companies

- Government, National Energy Agencies & Strategic Reserve Operators

- Market Size & Forecast by Sales Channel

- EPC & Turnkey PtX Project Contract Channel

- Electrolyser & Equipment Direct OEM Sales Channel

- Power Purchase Agreement (PPA) & Hydrogen Offtake Agreement Channel

- Public-Private Partnership (PPP) & Government Grant Co-Funding Channel

- Hydrogen-as-a-Service & PtX-as-a-Service Channel

- North America Power-to-X Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Electrolyser Capacity, GW & Output Product, Mt/year)

- By Technology Pathway

- By Electrolyser Technology

- By Renewable Power Source

- By System Scale

- By Output Product

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Power-to-X Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Electrolyser Capacity, GW & Output Product, Mt/year)

- By Technology Pathway

- By Electrolyser Technology

- By Renewable Power Source

- By System Scale

- By Output Product

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Power-to-X Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Electrolyser Capacity, GW & Output Product, Mt/year)

- By Technology Pathway

- By Electrolyser Technology

- By Renewable Power Source

- By System Scale

- By Output Product

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Power-to-X Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Electrolyser Capacity, GW & Output Product, Mt/year)

- By Technology Pathway

- By Electrolyser Technology

- By Renewable Power Source

- By System Scale

- By Output Product

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Power-to-X Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Electrolyser Capacity, GW & Output Product, Mt/year)

- By Technology Pathway

- By Electrolyser Technology

- By Renewable Power Source

- By System Scale

- By Output Product

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Power-to-X Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Electrolyser Capacity, GW & Output Product, Mt/year)

- By Technology Pathway

- By Electrolyser Technology

- By Renewable Power Source

- By System Scale

- By Output Product

- By Application

- By End-User

- By Country

- By Sales Channel

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Portugal, Norway, Denmark, Sweden, Australia, China, Japan, South Korea, India, Brazil, Chile, Saudi Arabia, UAE, Oman, Egypt, Morocco, South Africa

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- PEM Electrolyser Technology Deep-Dive: Stack Design, Membrane Advances, Iridium Catalyst Loading Reduction & Scale-Up Roadmap

- Alkaline Electrolyser Technology: Advanced Zero-Gap Design, Dynamic Operation & Cost Reduction to 2030 & Beyond

- Solid Oxide Electrolyser (SOEC) & Co-Electrolysis Technology: H2O/CO2 Co-Feeding, High Efficiency & Integration with Industrial Heat

- Power-to-Ammonia Technology: Electrochemical Ammonia Synthesis, Small-Scale Haber-Bosch & Distributed Green Ammonia

- Fischer-Tropsch & Methanol-to-Jet (MtJ) Synthesis Technology for E-Fuels & Sustainable Aviation Fuel (SAF) Production

- Direct Air Capture (DAC) & CO2 Utilisation Integration with Power-to-Liquids & Power-to-Chemicals Pathways

- Digital Twin, AI Process Optimisation & Smart Grid Integration Technology for Dynamic PtX Plant Operations

- Patent & IP Landscape in Power-to-X Technologies

- Value Chain & Supply Chain Analysis

- Platinum Group Metal (PGM), Iridium & Membrane Material Supply Chain for PEM Electrolysers

- Nickel, Stainless Steel & Diaphragm Material Supply Chain for Alkaline Electrolysers

- Electrolyser Stack, Balance-of-Plant & Power Electronics Manufacturing Supply Chain

- Renewable Power Generation, Grid Connection & PPA Procurement Supply Chain

- CO2 Capture, Compression, Transport & Purification Supply Chain for PtL & PtChem

- Hydrogen Storage, Compression, Liquefaction & Transport Infrastructure Supply Chain

- Synthesis Reactor, Catalyst & Downstream Processing Equipment Supply Chain for PtX Products

- EPC Contractor, Project Developer, Offtake Partner & Certification Body Channel

- Pricing Analysis

- Green Hydrogen Production Cost (LCOH) Analysis: Electrolyser Capex, Renewable Electricity Cost & Capacity Factor Sensitivity

- Green Ammonia, E-Methanol & SAF Production Cost Analysis vs. Fossil-Fuel Equivalent Benchmarks

- Electrolyser Capital Cost Trend Analysis: Current Cost, 2030 Target & NOAK Cost Reduction Pathway

- PtX Full-Chain Project Capex & Levelised Cost of Output (LCOx) Analysis by Technology Pathway & Geography

- Green Hydrogen Offtake Price, Contract Structure & Market Price Discovery Analysis

- Impact of Subsidy Schemes, H2 Production Tax Credit (PTC), IPCEI & Government Incentives on PtX Project Economics

- Sustainability & Environmental Analysis

- Lifecycle GHG Emissions Analysis of PtX Pathways: Well-to-Wake, Well-to-Gate & Well-to-Wheel Carbon Intensity

- Water Consumption, Freshwater Demand & Seawater Desalination Requirements for Large-Scale Green Hydrogen Production

- Land Use, Biodiversity Impact & Spatial Planning for Renewable-Powered PtX Facilities

- Iridium, Platinum & Critical Mineral Circularity: Electrolyser Catalyst Recovery, Recycling & Supply Security

- SDG 7 (Affordable Clean Energy), SDG 13 (Climate Action) & SDG 9 (Industry & Innovation) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology Pathway & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Pathway, Output Product & Geography

- Player Classification

- Large Electrolyser Manufacturers & Integrated PtX System Providers

- Specialist PEM Electrolyser Companies

- Specialist Alkaline & AEM Electrolyser Companies

- Solid Oxide Electrolyser (SOEC) & High-Temperature Technology Providers

- Green Ammonia & Power-to-Chemicals Technology & Project Developers

- E-Fuel, Power-to-Liquids & SAF Technology & Project Developers

- Energy Majors, Utilities & Renewable IPPs Developing Large-Scale PtX Projects

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Pathway, Electrolyser Type & Region

- Company Profile

- Company Overview & Headquarters

- Power-to-X Products, Technology Portfolio & Pipeline

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (PtX Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Pathway, Output Product, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing Scale-Up & Gigafactory Operational Excellence Strategy

- Geographic Expansion & Export Market Entry Strategy

- Customer, Offtake Partner & End-User Engagement Strategy

- Partnership, M&A & PtX Ecosystem Strategy

- Policy Engagement, Certification & Regulatory Strategy

- Sustainability, Critical Mineral Circularity & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output