Market Definition

The Global Climate Tech Investment Landscape Market encompasses the aggregate private and public capital flows directed toward the research, development, commercialization, scale-up, and deployment of technologies, business models, and infrastructure solutions that mitigate greenhouse gas emissions, remove carbon dioxide from the atmosphere, adapt human systems to the physical impacts of climate change, or improve resource efficiency in ways that reduce the climate impact of economic activity. Climate technology, broadly defined, spans a wide spectrum of innovation maturity stages from early-stage fundamental research and technology incubation through demonstration projects, first commercial deployments, and large-scale rollout of proven solutions, with investment instruments correspondingly ranging from government research grants, angel investment, and seed-stage venture capital through Series A to C growth equity, late-stage private equity, project finance, green bonds, corporate strategic investment, and public market financing via initial public offerings and listed infrastructure funds. The climate tech investment landscape encompasses technology domains including renewable energy generation and storage, green hydrogen production and distribution, electric vehicle systems and charging infrastructure, sustainable aviation and maritime fuels, industrial decarbonization technologies for steel, cement, chemicals, and aluminum, carbon capture utilization and storage, enhanced weathering and soil carbon sequestration, direct air capture, precision agriculture and sustainable food systems, building efficiency and electrification, smart grid and energy management software, climate risk analytics and adaptation infrastructure, circular economy and sustainable materials platforms, water technology and climate resilience infrastructure, and nature-based solutions financed through carbon market and biodiversity credit mechanisms. The market additionally encompasses the financial services infrastructure supporting climate tech investment including climate-specialized venture capital and private equity funds, green and sustainability-linked bond markets, blended finance facilities, climate risk assessment and disclosure services, transition finance advisory, and the measurement, reporting, and verification tools that substantiate climate impact claims for investors and regulators. Key participants include climate tech startups and scaleups, corporate venture arms, specialist climate funds, development finance institutions, sovereign wealth funds, corporate strategic investors, and government innovation agencies.

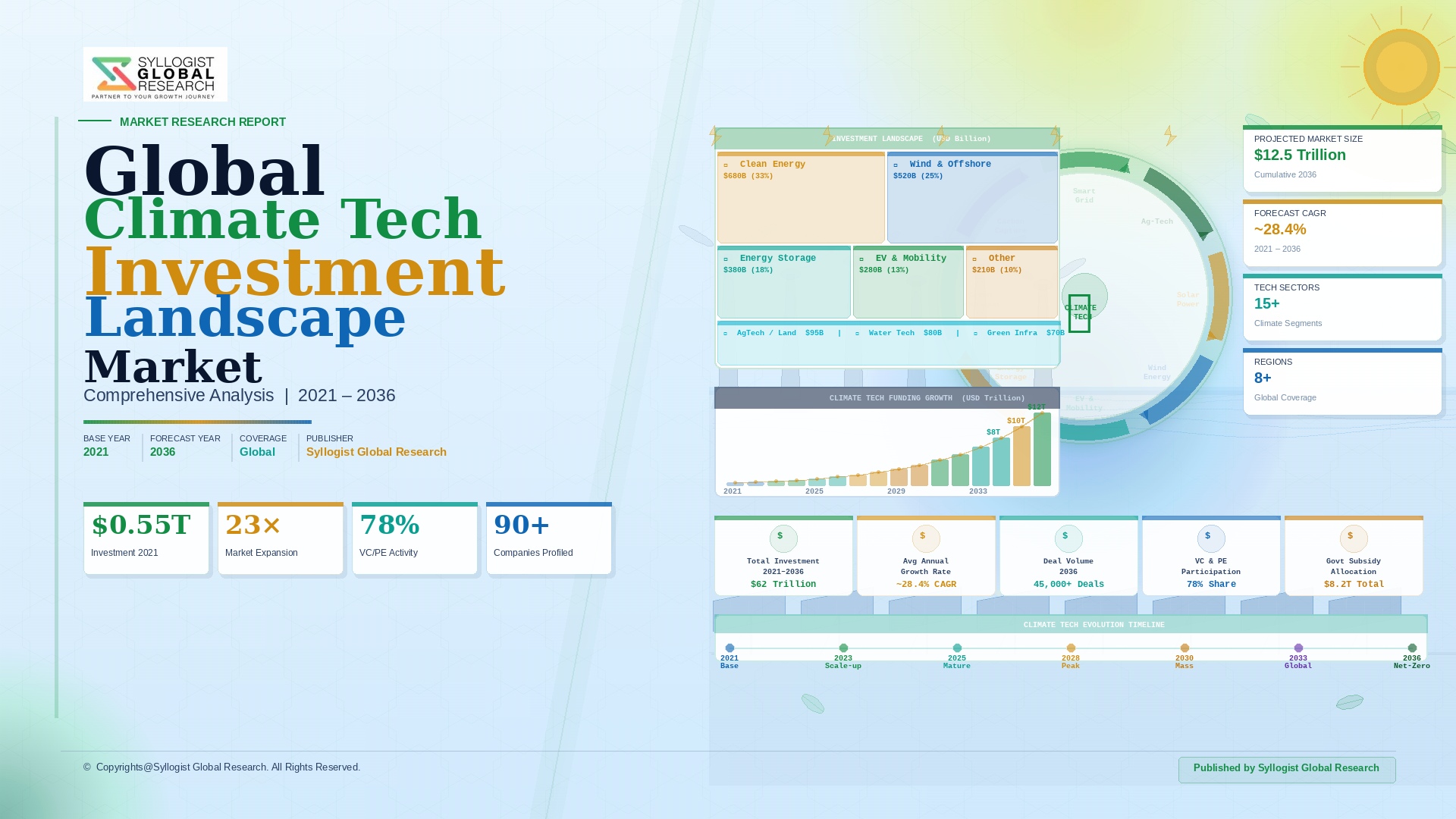

Market Insights

Global climate tech investment reached approximately USD 502 billion in 2025 across all stages from seed-stage venture capital through large-scale project finance and public market issuance, representing a compound annual growth rate of approximately 18.4% from USD 165 billion in 2020, establishing climate technology as the fastest-growing major investment category in the global private and institutional capital markets and the dominant theme in infrastructure and technology investment across the leading venture capital, private equity, and institutional asset management ecosystems. The investment landscape is structured by a pronounced maturity distribution, with early-stage venture and growth equity investment of approximately USD 68 billion in 2025 funding the next generation of climate technology solutions across pre-revenue and emerging commercial stage companies, while project finance, infrastructure equity, and corporate capital expenditure directed at deployed renewable energy, storage, electric vehicle, and building efficiency assets account for the majority of total climate tech investment at approximately USD 434 billion as commercially proven technologies scale into mass deployment phases. The United States, China, and the European Union collectively account for approximately 78% of global climate tech investment, with the United States attracting approximately USD 196 billion driven by Inflation Reduction Act incentive structures that have mobilized private capital at an estimated four-to-one leverage ratio relative to direct government expenditure, China deploying approximately USD 148 billion concentrated in solar manufacturing, electric vehicles, and battery supply chain expansion, and the European Union directing approximately USD 88 billion through a combination of corporate investment, REPowerEU program support, and European Investment Bank green financing mechanisms that collectively position Europe as the most diverse regional climate tech investment ecosystem by technology breadth.

The energy transition hardware segment, encompassing solar photovoltaic manufacturing and project investment, onshore and offshore wind, utility-scale battery energy storage, and electric vehicle and charging infrastructure, accounts for approximately 68% of total climate tech investment at USD 341 billion in 2025, reflecting the commercial maturity and proven economics of these foundational decarbonization technologies whose investment requirements are driven more by deployment scale imperatives and supply chain expansion than by technology de-risking. However, the most commercially compelling investment opportunity within the climate tech landscape from a return generation and market creation perspective is the emerging deep technology segment targeting hard-to-abate industrial emissions and negative emissions technologies, with green hydrogen and electrolytic industrial processes attracting approximately USD 34 billion in 2025, carbon capture utilization and storage receiving approximately USD 8.4 billion, direct air capture and enhanced weathering receiving approximately USD 3.2 billion, and sustainable aviation and maritime fuel technologies receiving approximately USD 12.6 billion, collectively representing technology categories whose commercial scale transition over the forecast period will create multi-trillion-dollar addressable markets for the innovators and investors who successfully navigate the valley of death between demonstration scale and commercial viability. The climate tech venture capital segment reached approximately USD 68 billion globally in 2025, with the average deal size at growth equity stage expanding to approximately USD 124 million as investors concentrate capital in companies that have demonstrated initial commercial traction and require large-scale capital for manufacturing facility construction, sales force expansion, and geographic market entry, reflecting a maturation of the climate tech venture ecosystem from the predominantly early-stage portfolio of the first climate tech investment wave in 2007 to 2012 toward a more commercially anchored investment environment with clearer pathways to large-scale revenue generation.

The industrial decarbonization investment segment is emerging as the defining frontier of the second generation of climate tech investment, as the relatively straightforward decarbonization pathways available through renewable electricity deployment, electric vehicle adoption, and building efficiency improvement are progressively implemented in leading markets, shifting investor and policy attention toward the structurally more challenging emissions from steel, cement, aluminum, chemicals, shipping, and aviation that collectively account for approximately 30% of global greenhouse gas emissions and cannot be cost-effectively addressed through direct electrification within current technology and infrastructure constraints. Green hydrogen as a feedstock and reductant for industrial processes is attracting the largest concentration of industrial decarbonization venture and growth investment, with electrolyzer manufacturers including Nel Hydrogen, ITM Power, and ThyssenKrupp Nucera receiving substantial private equity backing alongside the project finance pipeline for green hydrogen production facilities in Australia, the Middle East, Chile, and Northern Europe, while novel cement production pathways including low-calcium silicate clinker chemistry, calcined clay substitution, and electrochemical cement synthesis are attracting first commercial scale investment from corporate venture arms and climate-specialized funds. Sustainable aviation fuel technology represents a particularly high-value investment opportunity within industrial decarbonization, with aviation accounting for approximately 2.5% of global carbon dioxide emissions and facing limited electrification options for long-haul flights that make sustainable aviation fuel the primary decarbonization pathway, with power-to-liquid sustainable aviation fuel from green hydrogen and captured carbon dioxide, alcohol-to-jet processes, and bio-based feedstock pathways each attracting investment commitments from airlines, oil majors, and dedicated climate tech investors seeking to participate in a sustainable aviation fuel market projected to grow from approximately USD 1.2 billion in 2025 to over USD 28 billion by 2034 as regulatory blending mandates and corporate sustainability commitments scale demand.

The climate adaptation and resilience investment segment, which addresses the physical risks and systemic disruptions created by climate change impacts already locked in by historical emissions, represents a rapidly growing but significantly undercapitalized component of the broader climate tech investment landscape, with adaptation investment estimated at approximately USD 46 billion in 2025 against an adaptation financing need of approximately USD 300 to USD 500 billion annually by 2030 identified in the United Nations Environment Programme Adaptation Gap Report, creating an investment opportunity of extraordinary scale for technology and infrastructure solutions that reduce the economic damage, health impacts, and systemic vulnerability created by rising temperatures, extreme weather events, sea level rise, and water stress. Climate risk analytics and physical risk assessment platforms, which provide corporations, financial institutions, real estate investors, and governments with quantitative assessments of climate-related financial risks to asset portfolios under different warming scenarios and adaptation strategy options, attracted approximately USD 4.8 billion in investment in 2025 growing at approximately 34.2% annually, driven by mandatory climate risk disclosure requirements under the International Sustainability Standards Board framework, the European Corporate Sustainability Reporting Directive, the US Securities and Exchange Commission climate disclosure rule, and the Task Force on Climate-related Financial Disclosures recommendations adopted by financial regulators in major economies. Nature-based solutions investment, encompassing funding flows into reforestation, wetland restoration, regenerative agriculture, blue carbon conservation, and biodiversity credit market development, reached approximately USD 18.4 billion in 2025 and is growing at approximately 22.8% annually as corporate biodiversity commitments, emerging biodiversity credit markets aligned with the Global Biodiversity Framework adopted at COP15, and carbon credit revenue from nature-based projects collectively improve the investment returns available from ecosystem conservation and restoration at commercial scale.

Key Drivers

Landmark Government Industrial Policy Programs Deploying Unprecedented Direct and Incentive-Based Public Capital to De-Risk Climate Technology Commercialization and Scale Manufacturing

The enactment of transformational government industrial policy programs specifically designed to accelerate climate technology commercialization and manufacturing scale-up is providing the policy certainty, demand stimulus, and risk-sharing mechanisms that are mobilizing private capital into climate tech at multiples of direct government expenditure, fundamentally altering the investment calculus for climate tech across every stage from seed funding through large-scale project finance by reducing the revenue uncertainty, technology risk, and first-mover cost disadvantage that previously constrained climate tech investment well below what commercial opportunity alone would warrant. The United States Inflation Reduction Act’s production tax credits for clean electricity, clean hydrogen, sustainable aviation fuel, advanced manufacturing, and electric vehicles, combined with the Department of Energy Loan Programs Office’s USD 400 billion in loan authority for advanced energy technologies and the Industrial Demonstrations Program’s USD 6 billion for hard-to-abate industrial process decarbonization, collectively represent the most comprehensive and largest public investment program in climate technology history, having triggered over USD 380 billion in announced private clean energy investment across the United States within eighteen months of enactment according to official Treasury assessments that demonstrate the investment multiplier effect of well-designed production incentive structures. The European Union’s Green Deal Industrial Plan, Hydrogen Bank auction mechanism providing up to EUR 800 million in direct subsidies for green hydrogen production, and Innovation Fund deploying EUR 38 billion in grants for innovative low-carbon technology demonstration represent Europe’s parallel industrial policy response whose combined effect alongside Carbon Border Adjustment Mechanism carbon cost pressure is establishing Europe as a highly competitive destination for climate tech scale-up investment from global funds seeking the combination of policy certainty, deep capital markets, and strong regulatory demand pull that European policy frameworks uniquely provide.

Institutional Capital Mobilization, Net-Zero Portfolio Alignment Mandates, and Mandatory Climate Risk Disclosure Creating Structural Demand for Climate Tech Investment Opportunities

The convergence of institutional investor net-zero portfolio alignment commitments, mandatory climate risk disclosure requirements, and the growing evidence that climate technology represents a superior risk-adjusted return opportunity relative to fossil fuel-intensive alternatives is creating structural and growing demand from the world’s largest pools of investable capital for climate tech investment products across all asset classes and risk-return profiles, providing the demand side of the capital market equation that is meeting the supply of investment-ready climate tech opportunities at progressively larger deal sizes and earlier technology maturity stages. Pension funds and insurance companies managing aggregate assets of approximately USD 50 trillion within the Net-Zero Asset Managers initiative and Net-Zero Asset Owner Alliance have committed to decarbonize their investment portfolios in alignment with 1.5-degree Celsius pathways by 2050 with interim 2025 and 2030 milestones, creating active allocation mandates for climate tech investment that infrastructure and private equity fund managers are designing products to serve, with climate-focused infrastructure fund raises reaching approximately USD 78 billion in 2025 as institutional allocators compete for access to quality climate tech equity at commercial scale. Mandatory climate risk disclosure under the International Sustainability Standards Board IFRS S2 standard, adopted by regulatory authorities in the United Kingdom, Australia, Canada, Singapore, Japan, and progressively across additional jurisdictions, requires institutional investors and the corporations in their portfolios to disclose material climate-related financial risks and transition plans, creating financial accountability for climate risk exposure that is redirecting capital allocation decisions away from high-carbon assets toward climate-aligned investments as portfolio managers seek to reduce disclosure-documented stranded asset risk while capturing the return opportunities created by the accelerating energy transition.

Climate Technology Cost Deflation, Demonstrated Commercial Viability, and Expanding Investment Exit Ecosystem Improving Climate Tech Returns and Attracting Mainstream Financial Investor Participation

The dramatic and continuing reduction in the cost of foundational climate technologies including solar photovoltaic, wind, batteries, and electric vehicles, combined with the demonstrated commercial success of the first generation of climate tech unicorns and the development of a diverse ecosystem of investment exit pathways through initial public offerings, strategic acquisitions, infrastructure fund sales, and secondary market transactions, is transforming climate tech from a financially niche and impact-oriented investment category into a mainstream asset class delivering competitive risk-adjusted returns that is attracting participation from generalist institutional investors, sovereign wealth funds, and traditional private equity firms who were previously deterred by the capital intensity, long commercialization timelines, and uncertain exit liquidity that characterized climate tech investment in earlier market development phases. Climate technology companies achieved aggregate initial public offering and special purpose acquisition company listing proceeds of approximately USD 28.4 billion in 2025 across renewable energy developers, battery storage companies, electric vehicle technology providers, climate risk analytics platforms, and carbon market infrastructure businesses, establishing a public market liquidity pathway that enables institutional venture and growth equity investors to demonstrate realized financial returns that justify continued and expanded fund commitments from their limited partners. The growing strategic acquisition activity from major oil and gas companies, utilities, automotive manufacturers, industrial conglomerates, and technology corporations seeking to acquire climate technology capabilities, customer relationships, and intellectual property portfolios rather than develop them organically is providing a robust merger and acquisition exit pathway for climate tech investors at valuation multiples that reflect strategic premium pricing, with total climate tech merger and acquisition transaction value reaching approximately USD 94 billion in 2025, reinforcing the financial attractiveness of the asset class beyond the impact motivation that characterized its early investor base.

Key Challenges

Valley of Death for Deep Decarbonization Technologies: Capital Gap Between Demonstration Scale and Commercial Viability for Industrial and Negative Emissions Solutions

The most structurally consequential challenge within the global climate tech investment landscape is the persistent capital gap between successful technology demonstration and first commercial deployment for the deep decarbonization technologies targeting industrial processes, long-duration energy storage, carbon removal, and sustainable fuels whose commercialization is essential for achieving net-zero emissions pathways but whose investment requirements, technology risk profiles, and revenue certainty challenges place them beyond the risk tolerance and return timelines of conventional venture capital while simultaneously exceeding the demonstrated commercial viability thresholds required by project finance and infrastructure debt capital. Direct air capture of carbon dioxide from the atmosphere, enhanced geothermal energy systems, long-duration energy storage technologies including iron-air batteries, liquid air storage, and thermal storage, novel cement and steel production processes, and power-to-liquid sustainable aviation fuel production each require first-of-kind commercial scale facilities costing USD 200 million to over USD 2 billion to demonstrate commercially viable economics, with capital at risk for technology failure, market price uncertainty, and permitting delays that neither growth equity investors with five-to-seven-year fund horizons nor project finance lenders requiring proven technology and contracted revenue streams are structured to absorb alone. The structural financing gap between demonstration scale and first commercial deployment for these technologies is being partially addressed through government mechanisms including the United States Department of Energy Loan Programs Office, the European Innovation Fund, and bilateral grant programs, but the pace of government capital deployment remains substantially below what is required to advance the full portfolio of commercially promising deep decarbonization technologies through the valley of death within the timeframe required to contribute meaningfully to 2030 and 2035 emissions reduction milestones.

Geopolitical Competition, Supply Chain Nationalism, and Trade Barrier Proliferation Fragmenting the Global Climate Tech Investment and Manufacturing Landscape

The rapid escalation of geopolitical competition for leadership in climate technology manufacturing, supply chain control, and market share across solar photovoltaic, battery, electric vehicle, electrolyzer, and wind turbine value chains is creating an increasingly fragmented global climate tech investment landscape characterized by competing national industrial policies, trade barriers, and market access restrictions that reduce the economic efficiency of global climate technology deployment, increase system costs, and create investment uncertainty for multinational climate tech companies seeking to optimize manufacturing locations across the global cost landscape. The United States imposition of escalating tariffs on Chinese solar modules, electric vehicles, batteries, and critical minerals components reaching as high as 100% on Chinese electric vehicles in 2024, combined with the European Union’s provisional countervailing duties of up to 38.1% on Chinese electric vehicle imports, is creating a bifurcated global market in which Chinese and non-Chinese climate technology supply chains increasingly operate in parallel rather than integrated global value chains, with Chinese manufacturers investing in production capacity in Southeast Asia, Mexico, Hungary, and Morocco to circumvent tariff barriers while non-Chinese manufacturers invest in high-cost domestic production with government subsidy support. The competition between the United States Inflation Reduction Act domestic content requirements, the European Union Net-Zero Industry Act local manufacturing support provisions, and China’s industrial policy support for domestic climate technology champions is incentivizing climate tech investment in each jurisdiction on terms that prioritize domestic economic benefit over global cost optimization, increasing the per-unit cost of climate technology deployment in non-Chinese markets by an estimated 15% to 30% relative to fully globalized supply chain scenarios and creating policy-dependent investment returns that are vulnerable to political reversals.

Talent Scarcity, Specialized Engineering Workforce Shortages, and Technical Expertise Gaps Constraining Climate Tech Startup Scaling and Project Delivery Capacity

The rapid scaling of climate tech investment and project development activity is generating acute shortages of the specialized engineering, scientific, and technical talent required to translate capital commitments into operating assets and deployed technologies, with critical workforce gaps identified across offshore wind installation engineering, electrolysis and green hydrogen process engineering, direct air capture systems engineering, carbon capture and storage geotechnical expertise, advanced battery cell and module engineering, sustainable aviation fuel process chemistry, and climate risk modeling and data science, whose combined scarcity is creating execution bottlenecks that delay project commissioning, increase construction costs, and constrain the pace at which investment commitments can be converted into operational capacity. The offshore wind sector faces a particularly acute installation vessel and specialized workforce shortage, with the global fleet of purpose-designed offshore wind turbine installation vessels fully committed through 2028 at current project pipeline growth rates, and the specialized marine engineering, geotechnical survey, subsea cable installation, and electrical systems commissioning workforce growing at less than 30% of the pace required to staff projects in the current development pipeline, creating a fundamental physical deployment constraint that is extending project commissioning timelines and generating cost inflation for equipment, vessels, and personnel that is squeezing project returns and in some cases prompting cancellations of contracted offshore wind developments. University and vocational training pipeline development for climate tech-specific engineering disciplines is increasing globally in response to employer demand signals and government workforce development programs, but the three-to-five-year minimum development timeline from curriculum design through graduate entry into the workforce means that talent supply gaps will persist as a material constraint on climate tech project delivery capacity through at least the late 2020s, requiring climate tech employers to compete aggressively for available specialized talent through compensation, career development, and mission alignment strategies that add to project development cost structures.

Market Segmentation

- Segmentation By Technology Domain

- Solar Photovoltaic and Concentrated Solar Power

- Onshore and Offshore Wind Energy

- Battery Energy Storage and Long-Duration Storage

- Green Hydrogen, Electrolyzers, and Fuel Cells

- Electric Vehicles and Charging Infrastructure

- Sustainable Aviation Fuels (SAF) and Green Maritime Fuels

- Industrial Decarbonization (Green Steel, Cement, and Chemicals)

- Carbon Capture, Utilization, and Storage (CCUS)

- Direct Air Capture and Carbon Removal Technologies

- Building Efficiency and Heat Pumps

- Smart Grid, Energy Management, and Demand Response

- Sustainable Food, Agriculture, and Land Use

- Climate Risk Analytics and Adaptation Technology

- Circular Economy and Sustainable Materials

- Nature-Based Solutions and Biodiversity Finance

- Others

- Segmentation By Investment Stage

- Seed and Pre-Seed (Angel, Grants, and Incubators)

- Early-Stage Venture Capital (Series A and B)

- Growth Equity (Series C and Later Venture Rounds)

- Late-Stage Private Equity and Pre-IPO

- Project Finance and Infrastructure Debt

- Infrastructure Equity Funds

- Public Market and Listed Infrastructure

- Corporate Strategic Investment and Joint Ventures

- Government Grants and Concessional Finance

- Others

- Segmentation By Investor Type

- Climate-Specialized Venture Capital Funds

- Generalist Venture Capital and Growth Equity Funds

- Infrastructure and Real Asset Funds

- Corporate Venture Capital Arms

- Institutional Investors (Pension Funds and Insurance Companies)

- Sovereign Wealth Funds

- Multilateral Development Banks and Development Finance Institutions

- Government Innovation Agencies and Public Sector Investors

- Family Offices and High-Net-Worth Impact Investors

- Others

- Segmentation By Decarbonization Pathway

- Emissions Reduction and Mitigation Technologies

- Carbon Dioxide Removal and Negative Emissions

- Climate Adaptation and Resilience Infrastructure

- Nature-Based Solutions and Ecosystem Services

- Circular Economy and Waste Reduction

- Others

- Segmentation By End-Use Sector

- Power and Utilities

- Transportation and Mobility

- Industry and Manufacturing

- Buildings and Real Estate

- Agriculture and Food Systems

- Finance and Insurance

- Information Technology and Digital Infrastructure

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All investment values are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global climate tech investment in the base year 2025, and what is the projected investment trajectory and compound annual growth rate through 2034, disaggregated by technology domain including solar, wind, battery storage, green hydrogen, electric vehicles, sustainable fuels, industrial decarbonization, carbon capture, direct air capture, building efficiency, climate adaptation, and nature-based solutions, by investment stage including seed and venture capital, growth equity, project finance, infrastructure equity, and public market issuance, and by investor type including climate-specialized venture funds, institutional investors, corporate venture, sovereign wealth funds, and development finance institutions, to enable technology developers, fund managers, corporate strategic investors, development finance institutions, and policy designers to quantify capital deployment requirements and identify the most attractive investment opportunities across technology maturity and geographic segments through 2034?

- How are the United States Inflation Reduction Act production tax credits and Department of Energy Loan Programs Office authority, the European Union Green Deal Industrial Plan, Hydrogen Bank, and Innovation Fund, and comparable national industrial policy programs in Japan, India, Australia, Canada, South Korea, and the United Kingdom collectively shaping the geographic distribution of climate tech investment, the technology categories attracting the largest capital mobilization, and the investment return profiles available to private investors co-investing alongside government capital, and what is the estimated private investment leverage ratio and total climate tech investment mobilization attributed to each major policy instrument, and which policy design features including tax credit structures, grant competition frameworks, and first-loss capital provisions are proving most effective at mobilizing private capital at favorable leverage ratios for early-stage versus commercial-scale climate technology investment?

- What is the current investment pipeline, technology readiness level, first commercial deployment cost structure, projected cost reduction trajectory, key investor and project developer ecosystem, and policy support requirements for the deep decarbonization technology categories at the frontier of climate tech investment including direct air capture, enhanced geothermal systems, long-duration energy storage, green steel and cement, sustainable aviation fuel via power-to-liquid pathways, and offshore floating wind, and how are the specific valley of death financing mechanisms including the Department of Energy Loan Programs Office, European Innovation Fund, bilateral government grants, and novel first-of-kind commercial project financing structures being designed to bridge the capital gap between demonstration success and first commercial scale deployment for these technologies whose commercialization is critical for achieving 2050 net-zero targets but whose investment risk profiles exceed the tolerance of conventional venture or project finance capital alone?

- How are the United States tariffs on Chinese solar modules and electric vehicles, the European Union countervailing duties on Chinese electric vehicles, the Inflation Reduction Act domestic content requirements, the European Union Net-Zero Industry Act local manufacturing provisions, and bilateral trade agreements and technology partnership frameworks collectively reshaping the global climate tech manufacturing investment landscape, supply chain geography, and cost structure for solar photovoltaic, battery, electrolyzer, and electric vehicle value chains, and what are the quantified cost implications, investment location decisions, and competitive dynamics between US, European, Chinese, and emerging market climate tech manufacturers operating within increasingly fragmented trade policy environments, and which climate technology categories and geographic markets offer the most resilient investment propositions within this geopolitically complex landscape through 2034?

- What is the current investment scale, exit ecosystem maturity, return profile, and competitive landscape of the global climate tech venture capital and growth equity market including the fundraising activity and portfolio focus of leading climate-specialized funds, the deal flow and valuation trends across seed through Series C rounds in solar, battery, hydrogen, sustainable food, climate analytics, and adaptation technology categories, the merger and acquisition activity from strategic acquirers including oil majors, utilities, automotive companies, and technology corporations, and the public market listing performance of climate tech companies, and what technology categories and company archetypes are generating the most attractive investment returns in the current climate tech funding environment as the market transitions from the capital abundance of 2021 to 2022 toward a more selective and returns-focused investment discipline that is separating genuine breakthrough innovation from incremental improvement within an increasingly crowded competitive landscape?

- Scope Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Universe Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Investment Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Investment Landscape Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Investment Climate & Market Dynamics

- Regional Investment Summary

- Investor & Ecosystem Landscape Snapshot

- Climate Tech Sector & Deal Highlights

- Investment Market Dynamics

- Investment Drivers

- Investment Restraints

- Investment Opportunities

- Investment Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Investment Trends & Developments

- Emerging Climate Tech Investment Trends

- Deal Structure, Instrument & Financing Model Developments

- Regulatory, Policy & Public Finance Changes Impacting Investment Flows

- Capital Market, Fundraising & LP Commitment Trends

- Corporate Venture, Strategic M&A & Consolidation Trends

- Notable Deal Activity, Mega-Rounds & Landmark Transactions

- ESG, Impact Measurement & Climate Disclosure Trends

- Investment Risk Assessment Framework

- Technology Maturity, Scale-Up Risk & Commercialisation Uncertainty in Early-Stage Climate Tech

- Policy, Subsidy Discontinuity & Regulatory Risk Affecting Climate Tech Returns

- Macroeconomic, Interest Rate, Inflation & Cost of Capital Risk

- Geopolitical, Critical Material Supply Chain & Trade Policy Risk

- Greenwashing, Impact Integrity & Reputational Risk for Climate Tech Investors

- Regulatory & Policy Framework

- National Climate Tech & Clean Energy Industrial Policy: US Inflation Reduction Act (IRA), EU Green Deal & Net Zero Industry Act, UK Net Zero Strategy, India Mission Innovation & China Dual Carbon Policy

- Venture Capital & Private Equity Regulatory Framework: SEC Investment Adviser Rules, AIFMD, FCA Sustainable Finance Rules & National VC Incentive Schemes

- Green Taxonomy, SFDR, EU Taxonomy & National Sustainable Finance Classification Frameworks Directing Climate Tech Capital Allocation

- R&D Tax Credit, Innovation Grant, Production Incentive & Capital Allowance Policy Supporting Climate Tech Startup & Scale-Up Investment Economics

- TCFD, ISSB S2, SEC Climate Disclosure & Mandatory Climate-Related Financial Risk Reporting Standards for Institutional Climate Tech Investors

- Global Climate Tech Investment Landscape Outlook

- Total Climate Tech Investment Volume & Forecast by Value (USD Billion)

- Total Climate Tech Investment Volume & Forecast by Deal Count

- Investment Volume & Forecast by Climate Tech Sector

- Clean Energy Generation & Storage (Solar, Wind, Battery, Next-Gen Nuclear & Geothermal)

- Sustainable Mobility & Transportation (EV, Charging Infrastructure, SAF, Green Shipping & Logistics)

- Carbon Management & Removal (CCUS, DAC, Biochar, Enhanced Weathering & Carbon Accounting Tech)

- Sustainable Agriculture, Food Systems & Alternative Protein (AgTech, FoodTech & Land Use)

- Circular Economy, Sustainable Materials & Waste Technology (Recycling, Biomaterials & Green Packaging)

- Industrial Decarbonisation & Hard-to-Abate Sectors (Green Hydrogen, Green Steel, Green Cement & Heat)

- Built Environment, Smart Buildings & Urban Climate Tech (Green HVAC, Smart Grid & Building Efficiency)

- Climate Data, Analytics, AI & ESG FinTech (Climate Intelligence, Risk Analytics & Sustainability Software)

- Water Technology & Climate Resilience (Water Security, Flood Tech, Climate Adaptation Infrastructure)

- Ocean, Blue Economy & Nature-Based Solutions Technology

- Investment Volume & Forecast by Investment Instrument / Asset Class

- Venture Capital: Seed, Pre-Seed & Angel Investment

- Venture Capital: Early Stage (Series A & Series B)

- Venture Capital: Growth Stage (Series C, D & E)

- Private Equity & Infrastructure Equity

- Corporate Venture Capital (CVC) & Strategic Investment

- Project Finance, Asset Finance & Infrastructure Debt

- Public Market: IPO, SPAC, Secondary Listing & Listed Climate Tech Fund

- Government Grant, R&D Funding, Production Tax Credit & Public Finance

- Blended Finance, Impact Investment & Concessional Capital

- Investment Volume & Forecast by Investor Type

- Dedicated Climate Tech & Clean Energy Venture Capital Fund

- Generalist Venture Capital Fund with Climate Tech Portfolio

- Corporate Venture Capital (CVC) & Energy Major Investment Arm

- Private Equity & Specialist Infrastructure Fund Manager

- Development Finance Institution (DFI) & Multilateral Development Bank (MDB)

- Government Innovation Agency, National Lab & Public Programme

- Family Office, High-Net-Worth Impact Investor & Philanthropic Capital

- ESG-Focused Institutional Investor, Pension Fund & Insurance Company

- Investment Volume & Forecast by Investment Stage

- Seed & Pre-Seed (Concept, Prototype & Early Validation)

- Early Stage (Series A & B: Pilot, Demo & Initial Commercial Traction)

- Growth Stage (Series C, D & E: Scale-Up & Market Expansion)

- Late Stage & Pre-IPO (Series F Plus, Mezzanine & Pre-Public)

- Infrastructure & Asset Stage (Operational Project & Secondary Market)

- Investment Volume & Forecast by Deal Type

- VC Funding Round (Seed through Series E Plus)

- Strategic Acquisition, Corporate M&A & Platform Build-Out

- IPO, SPAC Merger & Public Market Debut

- Project Finance, Asset Finance & Infrastructure Deal

- Government Grant, Non-Dilutive Award & R&D Co-Funding

- Secondary Transaction, LP Stake Sale & Fund Recapitalisation

- Investment Volume & Forecast by Technology Readiness Level (TRL)

- TRL 1 to 3: Fundamental Research, Concept & Lab-Scale Validation

- TRL 4 to 6: Pilot, Demonstration & Pre-Commercial Scale-Up

- TRL 7 to 9: Commercial Deployment, Market Scaling & Proven Technology

- Investment Volume & Forecast by Market Maturity

- Developed Markets (OECD: North America, Europe, Japan, Australia & New Zealand)

- Emerging Markets & Developing Economies (EMDE: Asia Ex-Japan, Latin America, MENA & Sub-Saharan Africa)

- Frontier & Just Energy Transition Partnership (JETP) Priority Markets

- Investment Volume & Forecast by Exit Mechanism

- Strategic Trade Sale & Corporate Acquisition

- Initial Public Offering (IPO) & Secondary Listing

- Secondary Sale, GP-Led Continuation Fund & LP Stake Transfer

- Asset Refinancing, Dividend Recapitalisation & Infrastructure Exit

- Investment Volume & Forecast by Distribution & Placement Channel

- Direct Investment & Proprietary Deal Sourcing

- Syndicated Round, Co-Investment Consortium & Club Deal

- Platform, Marketplace & Digital Climate Tech Deal Flow Channel

- Accelerator, Incubator, University Spin-Out & Government Programme Pipeline

- North America Climate Tech Investment Landscape Outlook

- Investment Volume & Forecast

- By Investment Value (USD Billion)

- By Deal Count

- By Climate Tech Sector

- By Investment Instrument / Asset Class

- By Investor Type

- By Investment Stage

- By Deal Type

- By Technology Readiness Level

- By Country

- By Market Maturity

- Investment Volume & Forecast

- Europe Climate Tech Investment Landscape Outlook

- Investment Volume & Forecast

- By Investment Value (USD Billion)

- By Deal Count

- By Climate Tech Sector

- By Investment Instrument / Asset Class

- By Investor Type

- By Investment Stage

- By Deal Type

- By Technology Readiness Level

- By Country

- By Market Maturity

- Investment Volume & Forecast

- Asia-Pacific Climate Tech Investment Landscape Outlook

- Investment Volume & Forecast

- By Investment Value (USD Billion)

- By Deal Count

- By Climate Tech Sector

- By Investment Instrument / Asset Class

- By Investor Type

- By Investment Stage

- By Deal Type

- By Technology Readiness Level

- By Country

- By Market Maturity

- Investment Volume & Forecast

- Latin America Climate Tech Investment Landscape Outlook

- Investment Volume & Forecast

- By Investment Value (USD Billion)

- By Deal Count

- By Climate Tech Sector

- By Investment Instrument / Asset Class

- By Investor Type

- By Investment Stage

- By Deal Type

- By Technology Readiness Level

- By Country

- By Market Maturity

- Investment Volume & Forecast

- Middle East & Africa Climate Tech Investment Landscape Outlook

- Investment Volume & Forecast

- By Investment Value (USD Billion)

- By Deal Count

- By Climate Tech Sector

- By Investment Instrument / Asset Class

- By Investor Type

- By Investment Stage

- By Deal Type

- By Technology Readiness Level

- By Country

- By Market Maturity

- Investment Volume & Forecast

- Country-Wise* Climate Tech Investment Landscape Outlook

- Investment Volume & Forecast

- By Investment Value (USD Billion)

- By Deal Count

- By Climate Tech Sector

- By Investment Instrument / Asset Class

- By Investor Type

- By Investment Stage

- By Deal Type

- By Technology Readiness Level

- By Country

- By Market Maturity

- Investment Volume & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Sweden, Denmark, Netherlands, Norway, Switzerland, China, Japan, South Korea, India, Australia, Singapore, Israel, Brazil, Chile, Mexico, South Africa, UAE, Indonesia

- Investment Analytics & Innovation Landscape

- Climate Tech Deal Tracking, Venture Intelligence & Investment Database Platform Technology Deep-Dive

- Climate Tech Startup Ecosystem Mapping, Competitive Benchmarking & Portfolio Analytics Platform Technology

- AI-Driven Due Diligence, Technology Readiness Assessment (TRA) & Commercial Viability Scoring for Climate Tech

- ESG Impact Measurement, GHG Attribution & Science-Based Investment Alignment Analytics Platform

- Lifecycle Assessment (LCA), Total Cost of Ownership & Levelised Cost Modelling for Climate Tech Commercial Validation

- Climate Scenario Modelling, Physical & Transition Risk Analytics & TCFD-ISSB Portfolio Reporting Platform

- Digital Deal Platform, Co-Investment Marketplace & Syndication Technology for Climate Tech

- Patent & IP Landscape in Climate Tech Investment Analytics & Platform Technologies

- Investment Ecosystem & Value Chain Analysis

- Deal Origination: Startup Scouting, Accelerator Pipeline, University Transfer & Corporate Spin-Out

- Due Diligence: Technical Assessment, Market Sizing, Financial Modelling, ESG & Legal Review

- Investment Committee, Term Sheet, Deal Structuring & Capital Deployment

- Portfolio Support: Value Creation, Commercial Scale-Up, Ecosystem Access & Follow-On Funding

- Exit Preparation: IPO Readiness, M&A Process, Secondary Sale & Asset Refinancing

- Fund Administration, LP Reporting, ESG Impact Disclosure & Regulatory Compliance

- Advisory, Legal, Accounting, Valuation & Third-Party Ecosystem Service Providers

- Investment Return & Valuation Analysis

- Climate Tech VC IRR & MOIC Benchmarking by Sector, Stage & Vintage Year vs. Broader Tech & Generalist VC

- Climate Tech Private Equity & Infrastructure Return Analysis: Equity IRR, Cash Yield & Total Return by Asset Type

- Valuation Methodology for Climate Tech: Revenue Multiple, DCF, Comparable Transaction & Technology Option Value Approach

- Climate Tech IPO & SPAC Performance Analysis: Post-Listing Return, Valuation Premium & Public Market Re-Rating

- Cost of Capital, WACC & Financing Structure Impact on Climate Tech Project & Company Investment Economics

- Impact-Adjusted Return Analysis: Integrating GHG Abatement Cost, Social Co-Benefit Value & Avoided Damage into Total Return Assessment

- Sustainability, Impact & Climate Alignment Analysis

- Portfolio Climate Alignment & Paris Agreement 1.5 Degree Celsius Compatibility Assessment: GFANZ, Net Zero Asset Managers Initiative & SBTi Portfolio Alignment Tools

- GHG Abatement Impact Quantification: Tonnes of CO2 Avoided Per USD Invested Across Climate Tech Sectors & Investment Stages

- Social Co-Benefits, Just Transition & Inclusive Innovation Metrics: Job Creation, Energy Access, Community Benefit & Gender Lens Investing in Climate Tech

- Nature Positive & Biodiversity Impact: TNFD Framework, Natural Capital Accounting & Land-Use Impact Assessment for Nature-Based Climate Tech Investment

- Regulatory-Driven Impact Reporting: EU SFDR PAI Indicators, ISSB S2 Climate Disclosure, SEC Climate Rule & Emerging National Mandatory Climate Finance Reporting

- Investor & Competitive Landscape

- Market Structure & Concentration

- Investment Concentration Level by Sector, Instrument & Geography (Fragmented vs. Concentrated)

- Top 10 Investors by Deployed Capital, Portfolio Size & AUM in Climate Tech

- HHI (Herfindahl-Hirschman Index) Concentration Analysis by Investor Type & Climate Tech Sector

- Competitive Intensity Map by Investment Instrument, Climate Tech Sector & Geography

- Investor Classification

- Dedicated Climate Tech & Clean Energy Venture Capital Firms

- Generalist Tier-1 VC Firms with Significant Climate Tech Allocation

- Corporate Venture Capital (CVC) Arms of Energy Majors, Utilities & Industrial Corporates

- Private Equity & Infrastructure Fund Managers with Climate Strategy

- Development Finance Institutions (DFIs), MDBs & National Climate Finance Bodies

- Government Innovation Funding Body, National Lab & Public Accelerator Programme

- Impact Investment Manager, Family Office & Philanthropic Capital with Climate Mandate

- ESG FinTech, Climate Data Provider & Investment Intelligence Platform Company

- Competitive Analysis Frameworks

- Market Share Analysis by Capital Deployed, AUM, Sector Focus & Geography

- Investor & Firm Profile

- Firm Overview & Headquarters

- Climate Tech Investment Mandate, Strategy, Thesis & Target Sectors

- Key Portfolio Companies, Reference Investments & Notable Exits

- Fund Size, AUM & Total Climate Tech Capital Deployed

- Revenue, Management Fee, Carried Interest & Fund Performance Metrics

- Investment Differentiators, Proprietary Deal Flow & Value-Add Capability

- Key Strategic Partnerships, Co-Investment Relationships & M&A Activity

- Recent Developments (New Fund Close, Notable Investments, ESG Commitments)

- SWOT Analysis

- Strategic Focus Areas & Investment Roadmap

- Competitive Positioning Map (Capital Deployed vs. Sector Breadth & TRL Range)

- Key Investor & Firm Profiles

- Market Structure & Concentration

- Investment Analytics & Innovation Landscape

- Strategic Output

- Investment Opportunity Matrix: By Climate Tech Sector, Instrument, Investor Type, Stage & Geography

- White Space & Underfunded Climate Tech Segment Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Portfolio Construction & Climate Tech Sector Allocation Strategy

- Fund Structuring, Instrument Innovation & Capital Mobilisation Strategy

- Geographic Expansion & Emerging Market Climate Tech Entry Strategy

- LP, Co-Investor & Corporate Partner Engagement Strategy

- Partnership, M&A & Ecosystem Platform Build-Out Strategy

- Impact Measurement, ESG Integration & Climate Alignment Strategy

- Risk Mitigation, Diversification & Downside Protection Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)