Market Definition

The Global Green Ammonia Market encompasses the production, storage, transportation, and end-use application of ammonia synthesised through processes powered entirely by renewable energy sources, with hydrogen feedstock derived from electrolysis of water using wind, solar, hydropower, or other zero-carbon electricity rather than from natural gas steam methane reforming or coal gasification that characterise conventional grey and blue ammonia production. Green ammonia is produced through a three-stage process comprising renewable-powered water electrolysis to generate green hydrogen, air separation to produce nitrogen, and the catalytic Haber-Bosch synthesis process operating under high pressure and temperature conditions using electricity from renewable sources to drive compression and maintain reaction conditions, yielding a product that carries a near-zero or net-zero lifecycle carbon footprint compared to the approximately 1.8 to 2.4 metric tons of carbon dioxide equivalent emitted per metric ton of grey ammonia produced from natural gas feedstock. The market encompasses the full value chain from renewable energy generation and electrolysis equipment supply through green hydrogen production, air separation, Haber-Bosch synthesis plant construction and operation, liquid and compressed ammonia storage infrastructure, maritime and pipeline transportation logistics, and the end-use applications consuming green ammonia as a zero-carbon fertilizer input for sustainable agriculture, as a maritime shipping fuel in ammonia-fuelled vessel engines and fuel cells, as a hydrogen carrier enabling long-distance renewable energy transport and storage, as a direct combustion fuel for power generation and industrial heating, and as an industrial feedstock for chemicals and materials production that currently relies on carbon-intensive conventional ammonia supply. Key participants include renewable energy developers, green hydrogen electrolyser manufacturers, engineering procurement and construction contractors for synthesis plant delivery, ammonia shipping and terminal operators, fertilizer producers transitioning toward green ammonia supply, shipping companies evaluating ammonia fuel adoption, and the national governments and multilateral institutions whose policy frameworks and green hydrogen investment programs are defining the commercial trajectory of green ammonia market development globally.

Market Insights

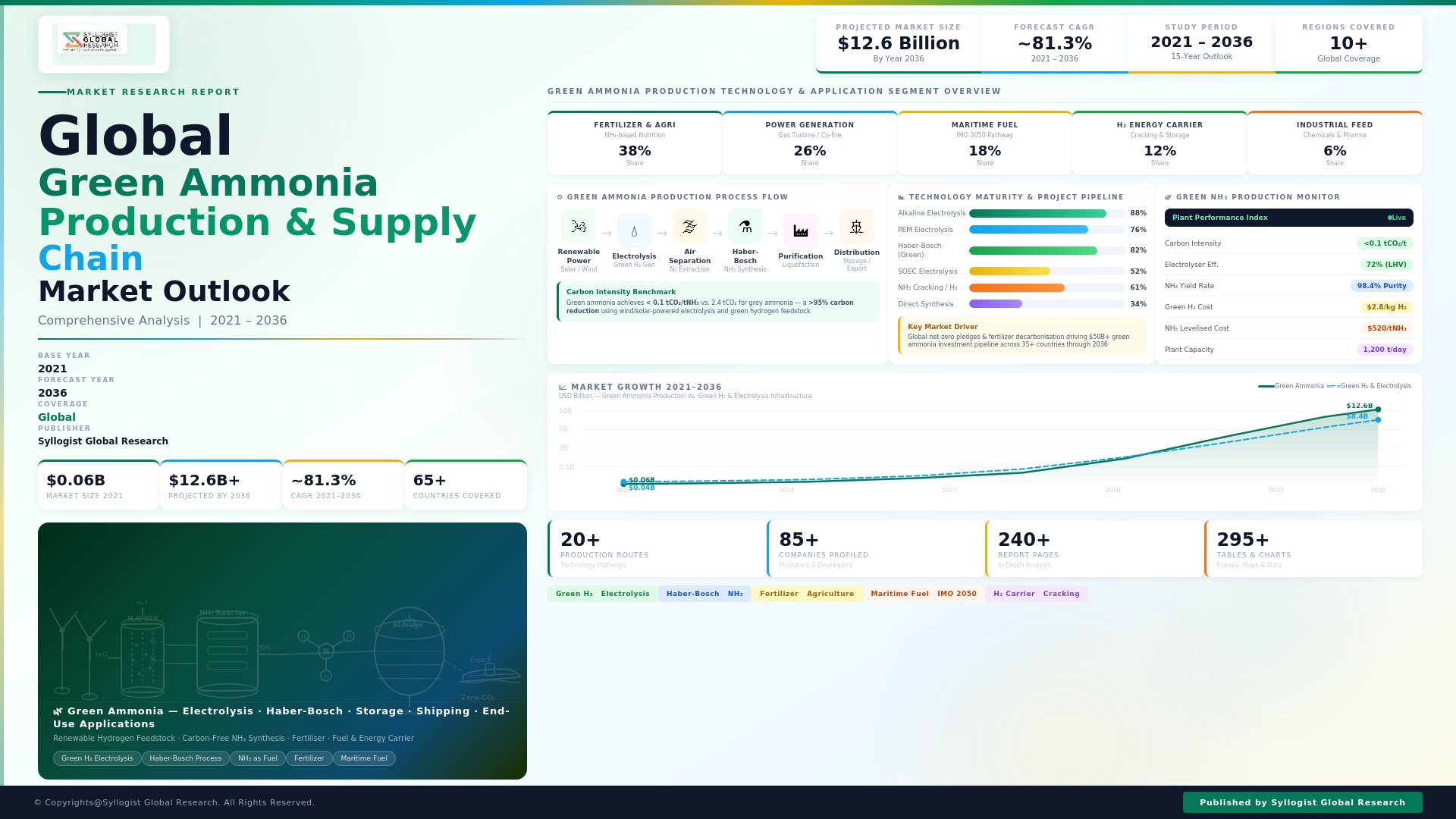

The global green ammonia market was valued at approximately USD 0.9 billion in 2025, reflecting the early commercial stage of the industry, and is projected to reach USD 14.7 billion by 2034, advancing at a compound annual growth rate of 36.4% over the forecast period from 2027 to 2034, representing one of the most rapid commercialisation trajectories of any clean energy transition technology as electrolyser cost reduction, renewable energy price deflation, and policy-driven demand creation from maritime decarbonisation, sustainable agriculture, and hydrogen energy export programs collectively accelerate the transition of green ammonia from demonstration-scale pilot projects toward commercially viable large-scale production. The production cost of green ammonia, currently at approximately USD 600 to USD 900 per metric ton at the most cost-advantaged locations with high-capacity factor renewable electricity, is projected to decline toward USD 300 to USD 450 per metric ton by 2034 at best-practice sites as electrolyser capital costs continue their learning curve reduction trajectory, renewable electricity purchase agreement prices decline, and large-scale synthesis plant construction achieves engineering and procurement cost efficiency improvements, narrowing the cost gap with grey ammonia priced at approximately USD 250 to USD 350 per metric ton under moderate natural gas price assumptions.

The fertilizer sector represents the largest near-term addressable market for green ammonia, with global conventional ammonia production of approximately 185 million metric tons annually in 2025 serving primarily the agricultural nitrogen fertilizer market whose direct ammonia, urea, ammonium nitrate, and ammonium sulphate products collectively constitute the world’s largest volume application of ammonia, and whose progressive decarbonisation through green ammonia substitution represents a commercially well-defined demand pathway supported by the growing market premium for low-carbon agricultural products, corporate sustainability commitments of major food and beverage companies, and the emerging regulatory frameworks for agricultural emissions accounting that are creating financial incentives for fertilizer producers and farmers to adopt green ammonia inputs. Premium pricing for green ammonia in the agricultural segment is validated by the European Union’s carbon border adjustment mechanism, which imposes carbon cost levies on imported fertilizers manufactured using carbon-intensive conventional ammonia that are creating a competitive cost advantage for green ammonia-derived fertilizers sold into European markets estimated at EUR 50 to EUR 120 per metric ton of ammonia equivalent by 2030 depending on prevailing European Union Emissions Trading System carbon price levels. The maritime shipping fuel application for green ammonia is the most strategically significant emerging demand segment, with the International Maritime Organization’s 2023 revised greenhouse gas strategy targeting net-zero shipping emissions by or around 2050 creating a definitive regulatory framework for zero-carbon fuel adoption whose implementation timeline and commercial scale generate a projected demand for green ammonia as marine fuel of approximately 8.4 million metric tons annually by 2034 as early-adopting shipping companies and port operators commission dual-fuel vessels and ammonia bunkering infrastructure.

The geographic development of green ammonia production capacity is concentrated in regions combining the world’s best renewable energy resources with proximity to export shipping infrastructure, government policy support, and established industrial ammonia production expertise, with Australia, Chile, Saudi Arabia, the United Arab Emirates, Morocco, Namibia, and Oman collectively hosting the largest pipeline of announced and under-development green ammonia projects whose aggregate announced capacity exceeds 60 million metric tons annually by 2035 across projects at various stages of feasibility study, front-end engineering and design, and financial investment decision. Australia has established itself as the most advanced national market for large-scale green ammonia project development, with multiple projects in the Pilbara and Kimberley regions leveraging among the world’s highest solar irradiance and wind resource quality, existing port and ammonia export infrastructure, and government support through the Hydrogen Headstart program and National Hydrogen Strategy, targeting export of green hydrogen and green ammonia to Japan, South Korea, Germany, and Singapore under long-term offtake frameworks being negotiated with importing country utilities and industrial consumers. Japan and South Korea are the most commercially committed importing nations, with both countries having established green hydrogen and ammonia import targets, government co-financing programs for export project development in partner countries, and utility and industrial sector procurement programs that are creating the demand-side certainty required for large-scale green ammonia export project financing, with Japan’s government targeting 3 million metric tons of annual hydrogen-equivalent imports, largely as ammonia, by 2030 under its Green Transformation program.

The electrolysis technology landscape underpinning green ammonia production is evolving rapidly, with alkaline electrolysis, proton exchange membrane electrolysis, and solid oxide electrolyser cell technologies competing for commercial dominance across different green ammonia project scale, operating profile, and cost optimisation scenarios, and with electrolyser capital costs having declined by approximately 40% between 2020 and 2025 across leading manufacturers, with further cost reduction of 40% to 60% projected through 2030 as manufacturing scale increases and design standardisation reduces component costs toward levels comparable with other mature industrial manufacturing sectors. The integration of green ammonia with renewable energy variability management is a significant operational and economic challenge, as Haber-Bosch synthesis requires stable hydrogen feed to maintain catalyst activity and avoid thermal cycling damage, while electrolysis can operate flexibly to absorb variable renewable generation, requiring buffer hydrogen storage capacity and synthesis plant design flexibility to accommodate the intermittency mismatch between optimal renewable energy generation profiles and continuous ammonia synthesis requirements. Ammonia cracking technology, which converts green ammonia back to hydrogen and nitrogen at the point of end use through thermal decomposition over catalysts at temperatures above 400 degrees Celsius, is advancing toward commercial readiness as an enabling technology for using green ammonia as a hydrogen carrier in markets where hydrogen rather than ammonia is the preferred final energy carrier, with ammonia cracker capital costs declining from approximately USD 1,200 per kilowatt of hydrogen output in 2022 toward projected levels of USD 400 to USD 600 per kilowatt by 2030 as commercial projects accumulate operating experience and catalyst and heat exchanger designs are optimised for large-scale continuous operation.

Key Drivers

Maritime Shipping Decarbonisation Mandates and International Maritime Organization Greenhouse Gas Strategy Creating Definitive Long-Term Demand for Green Ammonia as Zero-Carbon Marine Fuel

The International Maritime Organization’s 2023 revised greenhouse gas strategy, establishing binding targets for 20% to 30% reduction in total shipping emissions by 2030, 70% to 80% reduction by 2040, and net-zero by 2050 relative to 2008 levels, is creating a definitive and commercially unprecedented regulatory mandate for the adoption of zero-carbon fuels by the global shipping fleet whose approximately 100,000 commercial vessels collectively account for approximately 2.9% of global greenhouse gas emissions, with green ammonia identified alongside green methanol and green hydrogen as the primary candidate zero-carbon fuel options for the deep-sea shipping segment where battery electrification is technically and volumetrically impractical. Green ammonia’s attributes as a marine fuel, including its high energy density relative to compressed hydrogen at ambient temperature, existing global ammonia production and storage infrastructure that can be repurposed for bunkering operations, and the commercial maturity of large-scale ammonia handling at port terminals, position it as the leading candidate zero-carbon marine fuel for the bulk carrier, tanker, and container shipping segments whose large vessel size and long voyage distances require the volumetric energy density advantages that ammonia provides relative to compressed or liquefied hydrogen alternatives. The European Union FuelEU Maritime regulation and the United States Environmental Protection Agency’s proposed ocean-going vessel emission standards are reinforcing the International Maritime Organization framework with regional market-specific requirements that create additional commercial urgency for shipping companies whose vessel fleets serving European and American ports must demonstrate compliance with progressively tightening carbon intensity standards whose achievement without zero-carbon fuel adoption is not credible at the emission reduction levels targeted by 2040.

Renewable Energy Cost Deflation, Electrolyser Manufacturing Scale-Up, and Green Hydrogen Production Cost Reduction Improving Green Ammonia Commercial Competitiveness

The sustained decline in utility-scale solar and onshore wind electricity generation costs, which have fallen by approximately 89% and 70% respectively since 2010 and continue to decline at locations with high resource quality as technology learning curves advance and project financing costs decrease, is progressively improving the production economics of green hydrogen and green ammonia by reducing the single largest cost component of electrolysis-based green hydrogen production, with solar photovoltaic electricity purchase agreement prices reaching below USD 0.015 per kilowatt hour in resource-advantaged locations in the Middle East, Chile, and Australia that represent the most cost-competitive green ammonia production geographies globally. Proton exchange membrane electrolyser capital costs declined from approximately USD 1,200 per kilowatt of electrolyser capacity in 2020 to approximately USD 600 to USD 750 per kilowatt in 2025 and are projected to reach USD 200 to USD 350 per kilowatt by 2030 as gigawatt-scale manufacturing facilities reach full production capacity, with this cost reduction trajectory being the single most important determinant of green ammonia production cost competitiveness with conventional grey ammonia and driving the investment decisions of the commercial scale green ammonia projects whose financial investment decisions will define the market volume trajectory through 2034. Government green hydrogen investment programs in the United States, European Union, Australia, Japan, India, and China are providing production tax credits, capital grants, and concessional loan guarantees that effectively subsidise green ammonia production economics in the near term, with the United States Inflation Reduction Act hydrogen production tax credit of USD 3 per kilogram of clean hydrogen equivalent to approximately USD 500 per metric ton of green ammonia cost reduction at current green hydrogen yield ratios, making United States-produced green ammonia cost-competitive with grey ammonia at current natural gas prices under full tax credit utilisation.

Agricultural Sustainability Imperatives, Carbon Border Adjustment Mechanisms, and Food Supply Chain Decarbonisation Commitments Creating Premium Green Ammonia Fertilizer Demand

The agricultural sector’s exposure to escalating scrutiny of its greenhouse gas emission contribution, which accounts for approximately 10% to 12% of global greenhouse gas emissions with nitrogen fertilizer production and application representing a significant proportion of the agricultural supply chain carbon footprint, is creating structural demand for low-carbon and green ammonia-derived fertilizers from food and beverage companies with science-based emission reduction targets, retailers committing to scope three supply chain decarbonisation, and farmers in regulated markets facing increasing financial exposure to carbon pricing mechanisms applied to agricultural inputs and activities. The European Union Carbon Border Adjustment Mechanism, which began its transitional phase in October 2023 and enters full implementation in 2026, imposes carbon price levies on imported goods including fertilizers manufactured in countries without equivalent carbon pricing, creating a direct financial advantage for green ammonia-derived fertilizers entering the European Union market relative to grey ammonia-derived fertilizers produced in non-carbon-priced jurisdictions and generating a quantifiable market premium for green fertilizer certification that is accelerating European fertilizer producer investment in green ammonia supply agreements. Consumer willingness to pay premiums for products with verified low-carbon agricultural supply chains, documented through surveys indicating 30% to 45% of consumers in developed market economies would pay a 5% to 15% premium for food products with certified lower agricultural emission intensity, is creating a commercial signal that food and beverage brand owners are acting on through supply chain sustainability procurement requirements that include fertilizer carbon intensity specifications, accelerating demand for green ammonia in agricultural markets where sustainable food production labelling creates measurable revenue premium justification for the green ammonia price premium.

Key Challenges

Green Ammonia Production Cost Premium Over Conventional Grey Ammonia and Long-Term Offtake Contract Financing Requirements Constraining Commercial Project Development Pace

Green ammonia production costs at most project locations in 2025 remain 2.0 to 3.5 times higher than conventional grey ammonia production costs at prevailing natural gas prices, creating a cost competitiveness gap whose closure through electrolyser cost reduction, renewable energy price deflation, and carbon price mechanisms is projected to occur between 2030 and 2038 depending on location, policy support intensity, and natural gas price trajectory, but whose current magnitude requires either significant government subsidy, carbon price support, or end-use market premium pricing to underpin the project economics of commercial green ammonia facilities that must achieve financial investment decision on 20-year project financing horizons whose lender requirements for long-term fixed-price offtake contracts are difficult to secure when green ammonia buyers are themselves uncertain about the pace of their green fuel or fertilizer transition commitments. Project financing for green ammonia production facilities, which require capital investment of USD 800 million to USD 4.5 billion depending on production capacity and integration with dedicated renewable energy generation, is complicated by the technology risk associated with first-of-a-kind large-scale integrated renewable energy plus electrolysis plus synthesis systems whose individual components are commercially proven but whose integrated operation at the scale and reliability requirements of project finance lenders lacks the multi-year operating track record that infrastructure debt capital markets require for investment-grade project financing terms, compelling project developers to pursue construction in phases, government-backed financing structures, or strategic partnerships with established industrial gas or fertilizer companies whose balance sheet participation reduces technology and completion risk to bankable levels.

Ammonia Toxicity Hazards, Safety Regulation Complexity, and Public Acceptance Barriers for Ammonia Fuel Infrastructure Development

Ammonia is a highly toxic substance whose inhalation at concentrations above 300 parts per million is immediately dangerous to life and health, whose liquid anhydrous form requires pressurised storage or refrigerated cryogenic containment at minus 33 degrees Celsius, and whose accidental release from storage, pipeline, or maritime bunkering infrastructure presents severe acute hazard risks that require comprehensive safety management systems, emergency response capability, and regulatory compliance programs whose cost and operational complexity substantially exceed those applicable to conventional marine fuels, creating safety and liability management challenges that are slowing the pace of ammonia bunkering infrastructure development at ports and the adoption of ammonia fuel by shipping companies whose crew training, safety culture, and insurance underwriting requirements must be substantially upgraded for ammonia fuel operations. The regulatory framework governing ammonia as a marine fuel remains under development by the International Maritime Organization, with the International Code of Safety for Ships using Gases or other Low-flashpoint Fuels currently undergoing revision to incorporate ammonia-specific provisions for ship design, storage, fuel handling, and emergency response whose finalisation is expected between 2026 and 2028, creating regulatory uncertainty that is delaying vessel design approvals and ammonia fuel system procurement commitments at shipyards and shipping companies whose investment decisions require regulatory clarity. Port terminal operators considering ammonia bunkering infrastructure investment face public acceptance challenges from local communities and environmental advocacy groups concerned about ammonia release risk whose opposition through planning and permitting processes can substantially extend infrastructure development timelines beyond the commercial schedules required to support early-mover shipping company ammonia fuel adoption programs.

Green Hydrogen Supply Chain Bottlenecks, Electrolyser Manufacturing Capacity Constraints, and Renewable Energy Permitting Delays Limiting Green Ammonia Project Execution Timelines

The green ammonia production chain is critically dependent on the timely availability of large-scale electrolyser systems whose manufacturing capacity is currently constrained by the capital investment programs of electrolyser manufacturers who must simultaneously scale production facilities, develop supply chains for membrane, bipolar plate, and balance-of-plant components, and reduce specific manufacturing costs, with the aggregate announced electrolyser manufacturing capacity expansion of leading proton exchange membrane and alkaline electrolyser producers projected to reach approximately 40 gigawatts per year by 2027 but whose actual achievement is subject to execution risk from equipment supplier bottlenecks, skilled workforce shortages in electrochemical manufacturing, and capital availability constraints that could delay capacity ramp beyond planned timelines. Renewable energy development permitting and grid connection timelines in major green ammonia production candidate locations including Australia, Chile, and the United States have extended substantially, with large-scale solar and wind project permitting processes that historically required 2 to 4 years now commonly extending to 5 to 8 years due to environmental impact assessment requirements, indigenous land consultation obligations, visual amenity objections, and interconnection queue congestion at electricity transmission systems whose infrastructure expansion is not keeping pace with renewable energy project application volumes. The water supply requirement for large-scale electrolysis, with approximately 9 kilograms of demineralised water required per kilogram of hydrogen produced, creates a significant freshwater consumption demand at green ammonia production sites in the arid and semi-arid locations that offer the best renewable energy resources, requiring investment in seawater desalination and water treatment systems that add capital cost and energy consumption to green ammonia production economics and introduce an additional infrastructure permitting and water rights allocation complexity into project development programs in water-stressed jurisdictions.

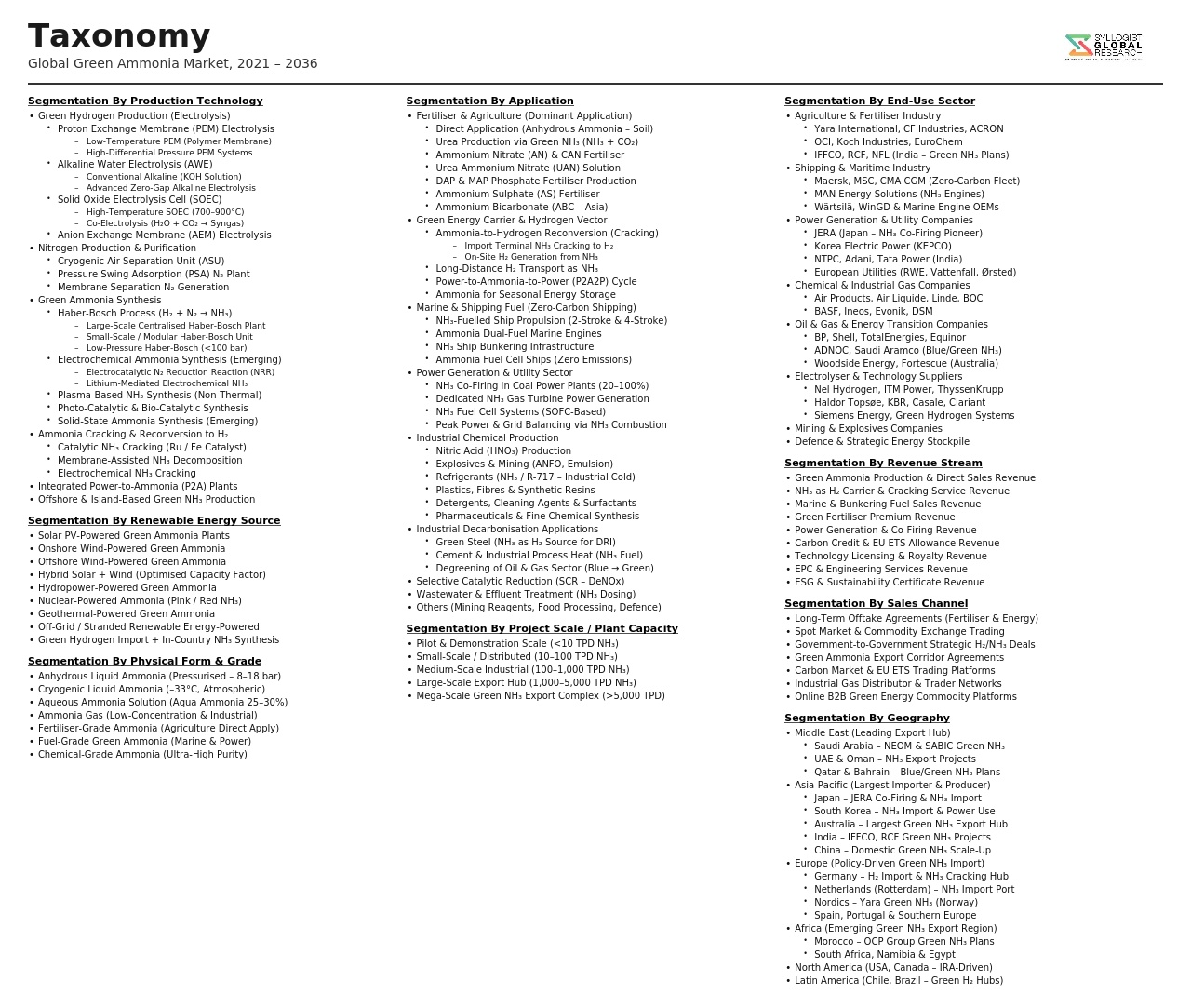

Market Segmentation

- Segmentation By Production Technology

- Alkaline Water Electrolysis (AWE) Based Green Ammonia

- Proton Exchange Membrane (PEM) Electrolysis Based Green Ammonia

- Solid Oxide Electrolyser Cell (SOEC) Based Green Ammonia

- Anion Exchange Membrane (AEM) Electrolysis Based Green Ammonia

- Biomass-Based Ammonia with Renewable Energy

- Segmentation By Renewable Energy Source

- Solar Photovoltaic Powered Green Ammonia

- Onshore Wind Powered Green Ammonia

- Offshore Wind Powered Green Ammonia

- Hydropower Powered Green Ammonia

- Hybrid Renewable Energy Powered Green Ammonia

- Grid-Supplied Certified Renewable Electricity

- Segmentation By End-Use Application

- Nitrogen Fertilizers (Direct Ammonia, Urea, and Ammonium Nitrate)

- Maritime Shipping Fuel (Dual-Fuel and Ammonia-Dedicated Vessels)

- Green Hydrogen Carrier and Long-Distance Energy Transport

- Power Generation (Ammonia Co-Firing and Dedicated Combustion)

- Industrial Feedstock (Chemicals, Explosives, and Refrigerants)

- Stationary Energy Storage and Grid Balancing

- Others

- Segmentation By Plant Scale

- Small-Scale Distributed Green Ammonia Plants (Below 10,000 tonnes per year)

- Medium-Scale Plants (10,000 to 100,000 tonnes per year)

- Large-Scale Export-Oriented Plants (100,000 to 1,000,000 tonnes per year)

- Mega-Scale Green Ammonia Hubs (Above 1,000,000 tonnes per year)

- Segmentation By Project Stage

- Operating Commercial Scale Production

- Under Construction and Commissioning

- Front-End Engineering and Design (FEED)

- Feasibility Study and Pre-FEED

- Concept and Early Development Stage

- Segmentation By End User

- Fertilizer Producers and Agricultural Cooperatives

- Shipping Companies and Fleet Operators

- Power Utilities and Grid Operators

- Industrial Chemical Manufacturers

- Energy Trading and Commodity Companies

- Government Strategic Reserve and Energy Security Programs

- Segmentation By Distribution and Logistics

- Maritime Seaborne Transport (Refrigerated Ammonia Tankers)

- Pipeline Transmission (Ammonia and Repurposed Natural Gas Pipelines)

- Truck and Rail Transport for Domestic Distribution

- Port Terminal Storage and Bunkering Infrastructure

- On-Site Production and Direct Consumption

- Segmentation By Region

- Asia-Pacific (Australia, Japan, South Korea, India, and Others)

- Middle East and North Africa (Saudi Arabia, UAE, Oman, and Morocco)

- Europe (Germany, Netherlands, United Kingdom, and Others)

- North America (United States and Canada)

- Sub-Saharan Africa (Namibia, South Africa, and Others)

- Latin America (Chile, Brazil, and Others)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Green Ammonia Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by end-use application, fertilizers, maritime fuel, hydrogen carrier, power generation, and industrial feedstock, by production technology, alkaline electrolysis, proton exchange membrane, and solid oxide electrolyser, and by geography, to enable green ammonia project developers, electrolyser manufacturers, shipping companies, fertilizer producers, and investors to identify which end-use segments and regional markets will generate the highest absolute revenue and most commercially significant adoption momentum across the forecast period?

- What is the projected green ammonia production cost trajectory at best-practice locations in Australia, Chile, Saudi Arabia, Morocco, and the United States through 2034, at what renewable electricity price and electrolyser capital cost combinations will green ammonia achieve cost parity with grey ammonia at various natural gas price assumptions, how will the United States Inflation Reduction Act hydrogen production tax credit, European Union Green Deal industrial policy, and equivalent national green hydrogen support programs affect the effective production economics and commercial competitiveness of green ammonia in key import and export markets, and what are the project financing structures and offtake agreement frameworks enabling the first wave of commercial scale green ammonia production facilities to reach financial investment decision?

- How is the maritime shipping sector expected to adopt green ammonia as a zero-carbon marine fuel through 2034 in response to International Maritime Organization greenhouse gas strategy mandates, EU FuelEU Maritime regulation, and major shipping company decarbonisation commitments, what is the projected number of ammonia dual-fuel vessel orders and deliveries through 2034, which shipping segments encompassing bulk carriers, tankers, and container vessels are generating the most near-term commercial momentum for ammonia fuel adoption, and what port infrastructure investment and safety regulatory framework developments are required to enable commercial-scale ammonia bunkering operations at major global shipping hubs?

- What is the projected development pipeline and financial investment decision timeline for large-scale green ammonia export projects across Australia, the Middle East, North Africa, Chile, and Namibia through 2034, which projects are most likely to achieve commercial scale production by 2030, what are the long-term offtake agreement structures and import market commitments from Japan, South Korea, European Union, and Singapore that are underpinning project financing, and how are geopolitical factors, infrastructure investment requirements, and water availability constraints differentiating the near-term commercial viability of competing green ammonia export project geographies?

- Who are the leading green ammonia project developers, electrolyser technology manufacturers, engineering procurement and construction contractors, fertilizer producers transitioning toward green ammonia supply, shipping companies and vessel designers evaluating ammonia fuel, and port terminal operators developing ammonia bunkering infrastructure, and what are their respective project portfolio scales and development timelines, technology partnerships and strategic supply chain investments, policy engagement and government funding program participation, safety management and regulatory compliance program development, and competitive positioning in the emerging global green ammonia value chain through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Green Hydrogen Cost Reduction Timeline & Electrolyser Scale-Up Execution Risk

- Renewable Energy Availability, Curtailment & Power Purchase Agreement (PPA) Bankability Risk

- Ammonia Storage, Handling, Transportation & Safety Infrastructure Risk

- Regulatory Uncertainty, Green Certification & Carbon Accounting Framework Risk

- Capital Intensity, Project Finance, Offtake Agreement & First-of-Kind Commercial Risk

- Regulatory Framework & Standards

- Green Hydrogen & Green Ammonia Definition, Certification & Guarantee of Origin (GO) Frameworks

- EU Renewable Energy Directive (RED III), RFNBO Criteria & Renewable Fuels of Non-Biological Origin Standards

- Ammonia Handling, Transport, Storage Safety Regulations: IFA, IMDG, ADR & National Chemical Safety Standards

- Carbon Border Adjustment Mechanism (CBAM), Emissions Trading & Low-Carbon Fuel Standard Frameworks

- Government Incentive Programmes, Production Tax Credits, Contracts for Difference & Green Ammonia Investment Policy

- Global Green Ammonia Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes)

- Market Size & Forecast by Production Technology

- Alkaline Water Electrolysis (AWE) with Haber-Bosch Synthesis

- Proton Exchange Membrane (PEM) Electrolysis with Haber-Bosch Synthesis

- Solid Oxide Electrolysis (SOEC) with Haber-Bosch Synthesis

- Electrochemical Nitrogen Reduction Reaction (NRR) Direct Synthesis

- Photocatalytic & Solar-Driven Ammonia Synthesis

- Market Size & Forecast by Renewable Energy Source

- Solar Photovoltaic (PV) Powered

- Wind-Powered (Onshore & Offshore)

- Hybrid Solar-Wind Powered

- Hydropower & Other Renewable Sources

- Market Size & Forecast by Electrolyser Type

- Alkaline Electrolyser (AWE)

- Proton Exchange Membrane (PEM) Electrolyser

- Solid Oxide Electrolyser Cell (SOEC)

- Anion Exchange Membrane (AEM) Electrolyser

- Market Size & Forecast by End-Use Application

- Fertilisers & Agriculture (Direct Application & Downstream Fertiliser Production)

- Green Shipping Fuel & Maritime Bunkering

- Power Generation & Grid Balancing (Co-Firing & Direct Combustion)

- Green Hydrogen Carrier & Long-Distance Hydrogen Transport

- Industrial Feedstock (Explosives, Plastics, Pharmaceuticals & Chemicals)

- Carbon-Free Steel & Metals Production

- Market Size & Forecast by Project Scale

- Large-Scale Export-Oriented Green Ammonia Plants (Above 100,000 Tonnes per Annum)

- Medium-Scale Regional & Industrial Green Ammonia Projects (10,000 to 100,000 Tonnes per Annum)

- Small-Scale & Modular Distributed Green Ammonia Systems (Below 10,000 Tonnes per Annum)

- Market Size & Forecast by Sales Channel

- Long-Term Offtake Agreement & Bilateral Supply Contract

- Spot Market & Commodity Trading

- Government Procurement & Strategic Reserve Contract

- Vertically Integrated Production & Self-Consumption

- North America Green Ammonia Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Technology

- By Renewable Energy Source

- By Electrolyser Type

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Europe Green Ammonia Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Technology

- By Renewable Energy Source

- By Electrolyser Type

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Asia-Pacific Green Ammonia Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Technology

- By Renewable Energy Source

- By Electrolyser Type

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Latin America Green Ammonia Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Technology

- By Renewable Energy Source

- By Electrolyser Type

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Middle East & Africa Green Ammonia Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Technology

- By Renewable Energy Source

- By Electrolyser Type

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- Country-Wise* Green Ammonia Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes)

- By Production Technology

- By Renewable Energy Source

- By Electrolyser Type

- By End-Use Application

- By Project Scale

- By Sales Channel

- By Country

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Alkaline Electrolyser Technology Deep-Dive: Stack Design, Diaphragm Materials, Scale-Up & Gigawatt Manufacturing Readiness

- PEM Electrolyser Technology: Membrane, Catalyst Layer, Bipolar Plate Innovation & Cost Reduction Pathway

- Solid Oxide Electrolyser Cell (SOEC) Technology: High-Temperature Operation, Co-Electrolysis & System Integration

- Haber-Bosch Process Optimisation for Intermittent Renewable Energy Input: Dynamic Operation & Small-Scale Reactor Technology

- Electrochemical & Photocatalytic Direct Ammonia Synthesis: Technology Readiness & Pathway to Commercial Scale

- Green Ammonia Storage, Liquefaction, Cracking & Reconversion to Hydrogen Technology

- Digital Twin, AI-Driven Process Optimisation & Remote Monitoring Technology for Green Ammonia Plants

- Patent & IP Landscape in Green Ammonia Production & Utilisation Technologies

- Value Chain & Supply Chain Analysis

- Renewable Energy Generation, PPA Structuring & Power Supply Chain for Green Ammonia Projects

- Electrolyser Stack, Balance-of-Plant & Green Hydrogen Production Equipment Supply Chain

- Air Separation Unit (ASU), Nitrogen Purification & Haber-Bosch Reactor Supply Chain

- Ammonia Storage, Liquefaction, Terminal & Export Infrastructure Supply Chain

- Shipping, Pipeline & Distribution Logistics for Green Ammonia

- EPC Contractor, Project Developer & System Integrator Channel

- Offtaker, Fertiliser Producer, Shipping Operator & Industrial End-User Channel

- Pricing Analysis

- Green Ammonia Levelised Cost of Production (LCOP) Analysis by Technology Route & Renewable Energy Source

- Green vs. Grey vs. Blue Ammonia Cost Parity & Competitiveness Analysis

- Electrolyser Capital Cost, Renewable Energy Cost & Capacity Factor Impact on Green Ammonia LCOP

- Green Ammonia Spot Price & Long-Term Offtake Contract Price Structure Analysis

- Green Ammonia Project Finance, Subsidy Requirement & Contract for Difference (CfD) Pricing Analysis

- Green Ammonia Cost Reduction Roadmap: 2025 to 2040 LCOP Trajectory by Region & Technology

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Green Ammonia: Carbon Footprint, Energy Intensity, Water Consumption & Land Use Across Production Routes

- Green Ammonia Contribution to Decarbonisation of Fertiliser Production & Global Food Security

- Green Ammonia as a Maritime Fuel: IMO 2050 Decarbonisation Pathway, Emission Reduction & Safety Considerations

- Green Ammonia for Power Generation: Grid Flexibility, Co-Firing with Coal & Gas & Pathway to Zero-Carbon Dispatchable Power

- Regulatory-Driven Sustainability, SDG 2 (Zero Hunger), SDG 7 (Clean Energy) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Production Technology, Application & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Production Technology, Application & Geography

- Player Classification

- Integrated Green Ammonia Project Developers & Producers

- Electrolyser Manufacturers Targeting Green Ammonia Applications

- Established Ammonia Producers Transitioning to Green Production

- Renewable Energy Companies & Utilities Developing Green Ammonia Projects

- Shipping Companies & Maritime Fuel Suppliers Investing in Green Ammonia

- EPC Contractors & Technology Licensors for Green Ammonia Plants

- Trading Houses, Offtakers & Green Commodity Platform Operators

- Competitive Analysis Frameworks

- Market Share Analysis by Production Technology, Application & Region

- Company Profile

- Company Overview & Headquarters

- Green Ammonia Production Assets, Technology Portfolio & Project Pipeline

- Key Offtake Agreements, Customer Relationships & Reference Projects

- Production Capacity (Operational, Under Construction & Planned)

- Revenue (Green Ammonia Segment) & Project Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (FID Announcements, Offtake Deals, Capacity Additions)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Production Cost Competitiveness vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Production Technology, Renewable Energy Source, Application, Project Scale & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output