Global Water Storage Tanks Market By Material Type, By Tank Type, By Capacity, By End Use Application, By Installation Type, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Water Storage Tanks Market encompasses the design, manufacture, supply, and installation of above-ground and underground storage vessels fabricated from steel, concrete, fiberglass, polyethylene, and composite materials, utilized for the collection, storage, and distribution of potable water, rainwater, treated wastewater, fire suppression water, and process water across municipal water infrastructure, residential and commercial buildings, industrial facilities, agricultural irrigation systems, and emergency water supply applications worldwide.

Market Insights

The global water storage tanks market is positioned at a structurally important intersection of accelerating urbanization, deteriorating legacy water infrastructure, intensifying water scarcity, and expanding industrial and agricultural water demand, with each of these forces independently generating durable procurement requirements and collectively establishing water storage capacity as a foundational element of national water security strategy across both developed and developing economies. The market was valued at approximately USD 19.3 billion in 2025 and is projected to advance at a compound annual growth rate of 6.7% through 2034, underpinned by sustained municipal infrastructure investment programs, the proliferation of rainwater harvesting initiatives in water-stressed regions, growing industrial water self-sufficiency objectives, and widespread replacement of ageing water storage assets that have exceeded their operational design lifespans across water utilities in North America, Europe, and Asia-Pacific.

Municipal water utilities represent the largest and most structurally stable demand channel for water storage tanks, with investment driven by population growth in urban agglomerations requiring expanded distribution system storage capacity, the replacement of deteriorating concrete and uncoated steel reservoirs installed during mid-twentieth century infrastructure expansion cycles, and the incorporation of additional storage buffer capacity into distribution networks to enhance resilience against supply interruptions from source disruption, treatment plant outages, and extreme weather events. In many developing country urban environments, the chronic insufficiency of treated water supply relative to demand is driving households, commercial establishments, and industrial facilities to invest in onsite water storage tanks as a service continuity measure, creating a large and geographically distributed decentralized demand segment that supplements the formal municipal infrastructure procurement market.

Rainwater harvesting and stormwater capture systems incorporating purpose-designed storage tanks are registering accelerating adoption globally, propelled by municipal water restriction programs in drought-affected regions, green building rating system requirements mandating onsite water self-sufficiency measures, and government subsidy and rebate programs that reduce the cost of residential and commercial rainwater harvesting installation. Polyethylene and fiberglass tanks are gaining market share within the rainwater harvesting, agricultural, and decentralized rural water supply segments, driven by their combination of corrosion resistance, lightweight handling characteristics, competitive installed cost relative to steel and concrete alternatives, and suitability for above-ground and below-ground installation in space-constrained settings. Industrial water storage demand is expanding across pharmaceutical manufacturing, food and beverage processing, semiconductor fabrication, and power generation, where process water supply reliability directly affects production continuity and where quality requirements for stored water demand tank materials and coatings that prevent contamination and maintain water quality over extended storage periods.

Asia-Pacific dominates the global water storage tanks market by volume and growth rate, driven by the scale of municipal water infrastructure development across China, India, Indonesia, and Vietnam, high rates of new residential and commercial construction incorporating rooftop and underground tank installations, and the critical importance of agricultural irrigation water storage in the region’s large farming economies. North America represents the second largest market by revenue, supported by a substantial municipal asset replacement pipeline, stringent drinking water quality standards that mandate tank lining and coating upgrades, and active industrial and fire suppression storage investment. The Middle East and Africa is the fastest-growing regional market in proportional terms, driven by severe water scarcity conditions, desalination distribution storage investment, and expanding housing and urban development programs requiring potable water storage infrastructure in areas with unreliable piped supply.

Key Drivers

Accelerating Urban Population Growth and Municipal Water Infrastructure Expansion Generating Sustained Large-Scale Procurement Demand for Elevated, Ground-Level, and Underground Water Storage Systems

Rapid urbanization across Asia-Pacific, Africa, the Middle East, and Latin America is compelling municipal governments and water utilities to invest continuously in expanded water distribution storage capacity to serve growing urban populations whose per capita water consumption and supply reliability expectations are simultaneously rising. New urban development zones, peri-urban housing expansion programs, and densification of existing cities all require additional distribution system storage nodes to maintain pressure zones, accommodate peak demand fluctuations, and provide emergency storage buffer capacity, driving procurement of elevated steel tanks, reinforced concrete ground-level reservoirs, and large-diameter polyethylene underground tanks across a geographically diverse and continuously expanding project development pipeline that sustains multi-year procurement volumes for water storage tank manufacturers.

Ageing Water Infrastructure Replacement Mandates and Drinking Water Quality Regulations Driving Large-Scale Tank Rehabilitation and Replacement Investment Across Developed Market Water Utilities

Municipal water storage infrastructure across North America, Europe, and Australia includes a substantial inventory of concrete reservoirs, unlined steel tanks, and welded steel standpipes installed during the infrastructure build-out period of the mid-to-late twentieth century that are approaching or exceeding their intended operational design lives, exhibiting structural deterioration, lining failure, or coating degradation that compromises water quality and storage integrity. Regulatory requirements for lead service line replacement, tank lining and coating compliance with drinking water contact material standards, and structural integrity certification are creating non-discretionary rehabilitation and replacement expenditure obligations for water utilities that generate a durable, policy-mandated procurement pipeline for new water storage tank systems and tank rehabilitation services independent of discretionary infrastructure expansion budgets.

Escalating Water Scarcity, Drought Frequency, and Rainwater Harvesting Policy Incentives Expanding the Decentralized Water Storage Tank Market Across Residential, Commercial, and Agricultural End Users

The increasing frequency and geographic breadth of drought events driven by climate variability, combined with the progressive tightening of municipal water use restrictions in water-stressed communities across Australia, the western United States, southern Europe, sub-Saharan Africa, and South Asia, is expanding the market for onsite rainwater harvesting storage tanks among residential, commercial, and agricultural end users seeking to reduce dependence on increasingly constrained and costly municipal water supply. Government grant, rebate, and tax incentive programs supporting rainwater harvesting installation, mandatory water harvesting requirements embedded in building codes for new construction in water-stressed jurisdictions, and irrigation water storage obligations for agricultural operators in regulated catchment areas are collectively sustaining a broad and geographically distributed demand base for decentralized water storage tank products.

Key Challenges

Raw Material Price Volatility and Supply Chain Disruptions for Steel, Polyethylene, and Fiberglass Inputs Creating Cost Uncertainty and Margin Pressure Across Tank Manufacturing Operations

Water storage tank manufacturers are exposed to significant input cost volatility arising from fluctuations in steel plate and coil prices driven by global steel market dynamics and trade policy developments, polyethylene resin price movements linked to petrochemical feedstock markets, and fiberglass raw material cost variability driven by glass fiber and resin supply chain conditions. These input cost pressures are difficult to fully pass through to customers in competitive public procurement tender environments where fixed-price contract structures dominate municipal and governmental purchasing, compressing manufacturer margins during commodity price upswings and creating procurement planning uncertainty for water utilities and industrial customers managing multi-year capital investment programs dependent on competitive tank supply economics.

Logistical Complexity and High Transportation Costs for Large-Capacity Tank Products Limiting Market Reach and Elevating Installed Cost for Remote and Infrastructure-Deficient Project Locations

Large-capacity water storage tanks, and particularly prefabricated above-ground steel and polyethylene tanks exceeding several hundred thousand liters in capacity, present significant transportation and logistics challenges arising from their physical dimensions, weight, and fragility during transit, which restrict shipment radius from manufacturing facilities, elevate delivered cost in remote or infrastructure-deficient locations, and require specialized heavy haulage equipment and installation crane resources that add substantial project cost beyond the tank unit price in geographically challenging deployment environments. In developing regions with limited road infrastructure quality and load capacity, the logistics complexity and cost of delivering large prefabricated tanks can fundamentally alter the competitive economics between different tank material and construction alternatives, favoring site-constructed concrete or bolted panel steel tanks over prefabricated solutions regardless of unit price competitiveness.

Water Quality Contamination Risk from Tank Material Leaching, Biofilm Formation, and Inadequate Maintenance Creating Regulatory Compliance Challenges and Reputational Risk for Manufacturers and Utilities

Water storage tanks serving potable water supply applications must comply with stringent drinking water contact material approval standards that assess the risk of chemical leaching from tank materials, coatings, linings, and sealants into stored water, and the growing sensitivity of regulatory agencies and consumers to trace contaminants including plasticizers, epoxy coating compounds, and microplastics is elevating compliance requirements and product testing obligations for tank manufacturers across major markets. The formation of bacterial biofilms and the growth of Legionella and other waterborne pathogens in inadequately maintained storage tanks creates public health risk that is generating regulatory pressure for enhanced tank design standards, inspection frequency requirements, and disinfection protocol compliance obligations that increase lifecycle ownership costs and liability exposure for tank operators and suppliers.

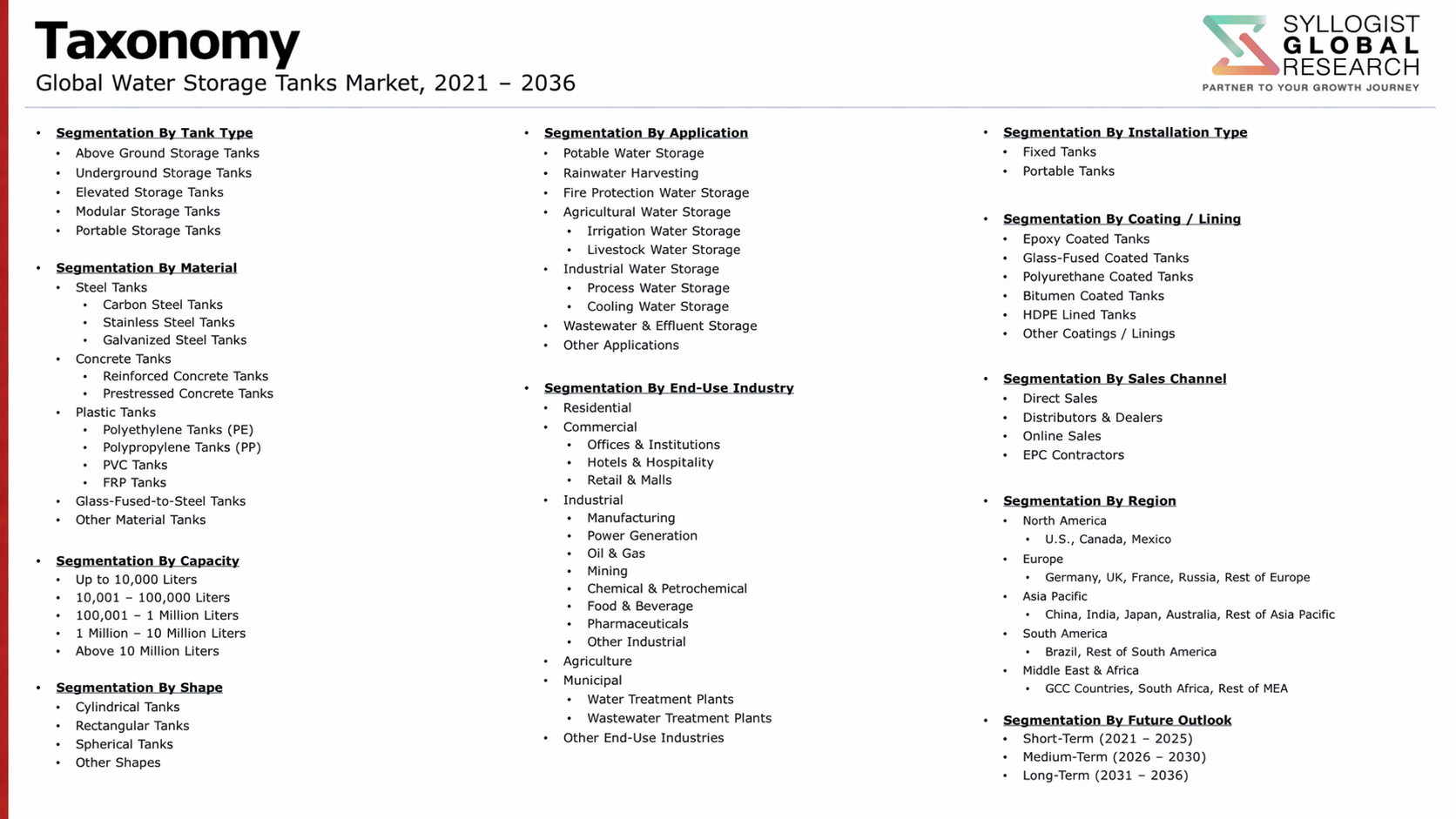

Market Segmentation

- Segmentation By Material Type

- Steel (Carbon Steel and Stainless Steel) Tanks

- Reinforced and Prestressed Concrete Tanks

- High-Density Polyethylene and Polypropylene Tanks

- Fiberglass Reinforced Plastic Tanks

- Glass-Fused-to-Steel and Enamel-Coated Steel Tanks

- Composite and Hybrid Material Tanks

- Others

- Segmentation By Tank Type

- Elevated Storage Tanks and Water Towers

- Ground-Level Reservoirs and Standpipes

- Underground and Buried Storage Tanks

- Sectional and Bolted Panel Tanks

- Pillow and Bladder Flexible Tanks

- Others

- Segmentation By Capacity

- Small Capacity (Below 10,000 Liters)

- Medium Capacity (10,000 to 100,000 Liters)

- Large Capacity (100,000 to 1,000,000 Liters)

- Very Large Capacity (Above 1,000,000 Liters)

- Segmentation By End Use Application

- Potable and Drinking Water Storage

- Rainwater Harvesting and Stormwater Storage

- Fire Suppression and Emergency Water Reserves

- Agricultural Irrigation Water Storage

- Industrial and Process Water Storage

- Wastewater and Reclaimed Water Storage

- Others

- Segmentation By Installation Type

- Above-Ground Installation

- Underground and Below-Grade Installation

- Elevated and Tower-Mounted Installation

- Segmentation By End User

- Municipal Water Utilities and Authorities

- Residential and Housing Developments

- Commercial and Institutional Buildings

- Industrial and Manufacturing Facilities

- Agricultural and Irrigation Operations

- Government and Defense Establishments

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global water storage tanks market valuation in 2025, projected through 2034, segmented by material type, tank type, and end use application, enabling tank manufacturers, distributors, and infrastructure investors to identify the highest-growth product segments and most durable procurement opportunities across the global water storage landscape?

- How are municipal infrastructure replacement mandates, drinking water quality regulations, and asset rehabilitation obligations evolving across North America, Europe, and Australia, and how are these regulatory and investment drivers shaping procurement volumes, material specifications, and lining and coating compliance requirements for water storage tank replacement and upgrade programs at municipal utilities?

- Which material segments, specifically polyethylene, glass-fused-to-steel, fiberglass reinforced plastic, and stainless steel, are gaining or losing competitive share across different end use applications and capacity ranges through 2034, and what performance characteristics, lifecycle cost economics, installation requirements, and regulatory compliance factors are driving material selection decisions among municipal, industrial, and agricultural procurement decision-makers?

- How is the competitive landscape structured among global water storage tank manufacturers, regional fabricators, and specialized lining and coating service providers, and what product innovation, geographic market expansion, service capability development, and strategic partnership strategies are enabling leading competitors to strengthen market position across key customer segments and regional markets?

- What role are rainwater harvesting mandates, water use restriction programs, and onsite water self-sufficiency incentives playing in expanding the decentralized water storage tank market among residential, commercial, and agricultural end users across water-stressed regions in Australia, the Middle East, sub-Saharan Africa, and South Asia through 2034?

- Which regional markets, specifically Asia-Pacific, the Middle East and Africa, and Latin America, are expected to generate the highest incremental water storage tank procurement growth through 2034, and what combinations of urban population expansion, industrial development, agricultural irrigation investment, and water security policy priorities are driving capacity procurement and technology selection in each regional market?

- How are water quality contamination risks from tank material leaching, biofilm formation, and drinking water contact material regulatory requirements shaping product development priorities, testing and certification investment, and material innovation strategies among water storage tank manufacturers competing for potable water supply applications in regulated markets?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility, Steel & Polymer Cost Fluctuation Risk

- Water Contamination, Leaching & Tank Integrity Failure Risk

- Regulatory Non-Compliance, NSF/ANSI Certification & Potable Water Standards Risk

- Corrosion, Structural Degradation & Asset Lifespan Risk

- Climate Change, Drought, Flood & Extreme Weather Impact on Storage Infrastructure Risk

- Regulatory Framework & Standards

- Potable Water Storage Standards, NSF/ANSI 61 Certification & WHO Drinking Water Guidelines for Tank Materials

- Structural Design, Seismic & Wind Load Standards for Above-Ground & Underground Water Tanks (AWWA, EN & IS Standards)

- Fire Protection Water Storage Tank Standards & NFPA Regulatory Requirements

- Industrial & Hazardous Liquid Storage Tank Regulations: EPA, API & Spill Prevention Standards

- Rainwater Harvesting, Greywater Reuse & Stormwater Storage Tank Regulatory Frameworks by Jurisdiction

- Green Building, LEED, BREEAM & Sustainable Infrastructure Procurement Standards for Water Storage

- Global Water Storage Tanks Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Sold & Total Storage Capacity, Million Litres)

- Market Size & Forecast by Material

- Steel Water Storage Tanks (Carbon Steel & Stainless Steel)

- Glass-Fused-to-Steel (GFS) & Enamel-Coated Steel Tanks

- Reinforced Concrete & Prestressed Concrete Tanks

- Fibre-Reinforced Plastic (FRP) & GRP Tanks

- High-Density Polyethylene (HDPE) & Polyethylene (PE) Tanks

- Polypropylene (PP) & Other Thermoplastic Tanks

- Liner-Based & Geomembrane-Lined Tanks & Reservoirs

- Composite & Multi-Layer Material Tanks

- Market Size & Forecast by Tank Type

- Above-Ground Water Storage Tanks

- Underground & Buried Water Storage Tanks

- Elevated & Tower Water Storage Tanks

- Bladder & Flexible Collapsible Water Storage Tanks

- Modular & Panel-Assembled Water Storage Tanks

- Potable Water Sectional & Bolted Storage Tanks

- Market Size & Forecast by Capacity

- Small-Capacity Tanks (Below 5,000 Litres)

- Medium-Capacity Tanks (5,000 to 100,000 Litres)

- Large-Capacity Tanks (100,000 to 1,000,000 Litres)

- Very Large & Mega-Capacity Tanks (Above 1,000,000 Litres)

- Market Size & Forecast by Installation Type

- New Installation & Greenfield Projects

- Replacement, Rehabilitation & Retrofit of Existing Storage Infrastructure

- Temporary & Emergency Deployable Water Storage

- Market Size & Forecast by Application

- Municipal Drinking Water Storage & Distribution

- Wastewater Treatment & Effluent Storage

- Rainwater Harvesting, Stormwater & Greywater Reuse Storage

- Fire Protection & Emergency Water Storage

- Agricultural Irrigation & Livestock Water Storage

- Industrial Process Water & Cooling Water Storage

- Oil & Gas, Chemical & Petrochemical Liquid Storage

- Mining & Minerals Processing Water Storage

- Food & Beverage & Pharmaceutical Process Water Storage

- Market Size & Forecast by End-User

- Municipal Water & Wastewater Utilities

- Residential & Commercial Building Owners

- Industrial & Manufacturing Facilities

- Agricultural & Rural Water Users

- Oil & Gas & Petrochemical Operators

- Mining & Metals Companies

- Government & Defence Agencies

- Humanitarian, NGO & Emergency Relief Organisations

- Market Size & Forecast by Sales Channel

- Direct OEM & Manufacturer Sales

- Distributor, Dealer & Merchant Wholesaler Network

- EPC Contractor & System Integrator Channel

- Online & E-Commerce Sales Platforms

- Government Tender & Public Procurement Channel

- North America Water Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold & Total Storage Capacity, Million Litres)

- By Material

- By Tank Type

- By Capacity

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Water Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold & Total Storage Capacity, Million Litres)

- By Material

- By Tank Type

- By Capacity

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Water Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold & Total Storage Capacity, Million Litres)

- By Material

- By Tank Type

- By Capacity

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Water Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold & Total Storage Capacity, Million Litres)

- By Material

- By Tank Type

- By Capacity

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Water Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold & Total Storage Capacity, Million Litres)

- By Material

- By Tank Type

- By Capacity

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Water Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Sold & Total Storage Capacity, Million Litres)

- By Material

- By Tank Type

- By Capacity

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Glass-Fused-to-Steel (GFS) & Factory-Coated Bolted Steel Tank Technology: Corrosion Protection, Assembly & Lifecycle Performance

- Advanced FRP & GRP Tank Manufacturing Technology: Filament Winding, Resin Transfer Moulding & Structural Design

- HDPE & Thermoplastic Tank Rotational Moulding, Blow Moulding & Extrusion Welding Technology

- Modular & Panel Tank System Technology: Precision Fabrication, Site Assembly & Leak-Proof Jointing

- Smart Tank Monitoring: IoT Sensors, Level Measurement, Water Quality Monitoring & Remote SCADA Integration

- Structural Health Monitoring, Corrosion Inspection & Digital Twin Technology for Large Water Storage Assets

- Liner & Geomembrane Technology: HDPE, EPDM & Reinforced Polyolefin Liners for Open Reservoirs & Covered Tanks

- Patent & IP Landscape in Water Storage Tank Technologies

- Value Chain & Supply Chain Analysis

- Steel Plate, Coil, Structural Steel & Coating Materials Supply Chain

- Polymer Resin, HDPE, FRP & Composite Raw Material Supply Chain

- Concrete, Cement, Rebar & Prestressing Component Supply Chain

- Tank Fabrication, Panel Manufacturing & Modular Assembly Supply Chain

- Fittings, Valves, Pipework, Access Hatches & Ancillary Equipment Supply Chain

- EPC Contractor, Civil & Structural Engineering & Site Installation Channel

- Aftermarket Inspection, Lining, Coating Repair & Maintenance Service Channel

- Pricing Analysis

- Tank Unit Price Analysis by Material & Capacity Range

- Installed Cost Analysis: Tank Supply, Civil Works, Pipework & Commissioning

- Total Cost of Ownership (TCO): Capex, Maintenance, Lining Renewal & Asset Replacement Analysis

- Material Cost Comparison: Steel vs. GFS vs. FRP vs. HDPE vs. Concrete Tank Economics

- Price Trend Analysis: Impact of Steel Prices, Polymer Costs & Labour on Tank Pricing

- Leasing, Hire & Temporary Water Storage Pricing Model Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Water Storage Tank Materials: Carbon Footprint, Embodied Energy & End-of-Life Recyclability

- Water Quality Protection, Leaching Risk & Non-Toxic Material Standards for Potable Water Tank Compliance

- Tank Cover, Algae Control & Evaporation Reduction Technologies for Sustainable Water Storage

- Role of Water Storage Infrastructure in Climate Adaptation, Drought Resilience & Water Security

- SDG 6 (Clean Water & Sanitation) Contribution, ESG Alignment & Green Infrastructure Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Material, Tank Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Material, Application & Geography

- Player Classification

- Large Diversified Water Storage Tank Manufacturers (Multi-Material & Multi-Market)

- Specialist Steel & Glass-Fused-to-Steel Tank Manufacturers

- Specialist FRP & GRP Water Tank Manufacturers

- Specialist HDPE & Thermoplastic Tank Manufacturers

- Concrete & Prestressed Concrete Tank Specialists

- Modular, Panel & Sectional Tank System Providers

- Tank Lining, Coating & Rehabilitation Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Material, Tank Type & Region

- Company Profile

- Company Overview & Headquarters

- Water Storage Tank Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Water Storage Tank Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Material, Tank Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output