Global Water Filtration Cartridges Market By Filtration Technology, By Filter Media, By Micron Rating, By End Use Application, By Distribution Channel, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Water Filtration Cartridges Market encompasses the manufacture, distribution, and replacement supply of consumable and semi-permanent filtration cartridge assemblies deployed within point-of-use, point-of-entry, and industrial water treatment systems to remove suspended solids, sediments, chlorine, heavy metals, organic compounds, bacteria, and dissolved contaminants through mechanical, activated carbon, ion exchange, reverse osmosis membrane, and ultraviolet media technologies, serving residential, commercial, industrial, and municipal water purification and process water applications globally.

Market Insights

The global water filtration cartridges market is experiencing a sustained demand expansion cycle, driven by the convergence of deteriorating source water quality in municipal distribution systems, heightened consumer awareness of tap water safety following widely publicized contamination events, escalating regulatory scrutiny of emerging contaminants including per- and polyfluoroalkyl substances, microplastics, pharmaceutically active compounds, and lead, and a structural shift in consumer and institutional water procurement behavior toward filtration-based alternatives to bottled water consumption. The market was valued at approximately USD 6.4 billion in 2025 and is projected to grow at a compound annual growth rate of 8.2% through 2034, as filtration cartridge adoption expands beyond its traditional residential and light commercial base into industrial process water, food and beverage manufacturing, pharmaceutical production, and healthcare water quality management applications that collectively represent a high-value and rapidly growing end use segment with demanding performance and compliance requirements.

Activated carbon block and granular activated carbon cartridges maintain their position as the largest product category within the global filtration cartridges market, reflecting their broad deployment in point-of-use drinking water systems and refrigerator-integrated filtration applications where chlorine, taste, odor, and volatile organic compound removal represent the primary treatment objective for residential consumers in markets with chlorinated municipal water supply. Reverse osmosis membrane cartridge systems are registering the fastest volume growth across both residential and light commercial segments in markets characterized by elevated total dissolved solids, nitrate contamination, or heavy metal concerns in source water, driven by continued reduction in system purchase price, the development of more water-efficient membrane designs that reduce wastewater discharge ratios, and growing consumer willingness to invest in comprehensive whole-water purification solutions delivering measurable improvements in water quality across a broad contaminant spectrum.

The replacement cartridge aftermarket represents a structurally distinctive and commercially attractive segment within the broader market, as the installed base of point-of-use and point-of-entry filtration systems generates recurring consumable demand with relatively predictable replacement cycles governed by manufacturer service interval recommendations and contaminant loading conditions. Original equipment manufacturers and specialist filtration brands invest significantly in proprietary cartridge form factor design, filter housing engineering, and smart connectivity features that notify users of replacement timing requirements, creating a durable aftermarket revenue base with significantly higher customer retention characteristics than durable goods categories lacking consumable replacement dependencies. Industrial filtration cartridge applications in pharmaceutical manufacturing, semiconductor fabrication, food and beverage processing, and petrochemical operations are the highest unit value segments within the market, requiring validated performance specifications, regulatory compliance documentation, and application-specific media chemistry that support premium pricing and long-term supply relationship stability with qualified cartridge manufacturers.

Asia-Pacific represents the largest and fastest-growing regional market for water filtration cartridges, underpinned by the massive scale of point-of-use water purifier adoption in China and India, where concerns about tap water safety and microbiological contamination risk have established household water filtration as a near-universal consumer expenditure category in urban and peri-urban populations, generating both substantial cartridge unit volumes and a large and growing replacement cartridge aftermarket. North America is the second largest regional market, characterized by high system penetration in residential applications, strong brand loyalty among established filtration system manufacturers, and a growing industrial and commercial water treatment cartridge segment driven by food service, healthcare, and light manufacturing applications. Europe represents the third major regional market, with growth driven by expanding consumer concern about emerging contaminants, progressive adoption of point-of-use filtration as an alternative to bottled water in environmentally conscious consumer segments, and industrial process water quality compliance investment across pharmaceutical and food manufacturing.

Key Drivers

Growing Consumer Awareness of Tap Water Contamination Risks and Emerging Contaminant Regulatory Expansion Driving Residential and Commercial Point-of-Use Filtration Cartridge Adoption

Increasing consumer concern about the presence of lead from ageing service line infrastructure, per- and polyfluoroalkyl substance contamination in municipal source water, microplastic particles detected in treated drinking water, pharmaceutical residues, and disinfection byproducts is compelling a growing proportion of residential and commercial water users to invest in point-of-use and point-of-entry filtration systems that deliver measurable contaminant reduction performance beyond the treatment capabilities of municipal water systems. Regulatory actions mandating maximum contaminant level reductions for an expanding list of emerging pollutants are simultaneously reinforcing consumer demand for advanced filtration media cartridges capable of addressing contaminants not previously subject to drinking water quality standards, elevating average system complexity and cartridge unit value across the residential and commercial market.

Sustainability-Driven Transition from Single-Use Plastic Bottled Water to Filtration-Based Drinking Water Solutions Expanding the Installed Base of Cartridge-Dependent Filtration Systems Globally

The accelerating global movement to reduce single-use plastic consumption is generating a structural behavioral shift among environmentally conscious consumers, corporate campuses, hospitality operators, educational institutions, and government facilities away from bottled water procurement toward investment in plumbed-in and countertop filtration systems that deliver purified drinking water on demand through replaceable filtration cartridges. Municipal governments and corporate sustainability programs implementing single-use plastic reduction policies are actively facilitating this transition by funding filtration system installation in public buildings, parks, and transportation infrastructure, creating institutional procurement demand for cartridge-dependent filtration systems that supplements organic consumer adoption growth and establishes a recurring public sector replacement cartridge procurement channel with predictable multi-year demand characteristics.

Industrial Water Quality Standards Intensification and Ultrapure Water Requirements in Pharmaceutical, Semiconductor, and Food Processing Applications Elevating Demand for High-Performance Specialty Filtration Cartridges

The stringent process water purity requirements of pharmaceutical drug manufacturing, sterile injectable production, semiconductor wafer fabrication, food and beverage hygienic processing, and medical device manufacturing are generating sustained investment in high-performance filtration cartridge systems that deliver validated particulate removal, bacterial reduction, endotoxin elimination, and dissolved organic compound rejection performance to levels substantially exceeding those achievable by standard residential and commercial filtration products. Regulatory frameworks governing pharmaceutical water quality including United States Pharmacopeia purified water and water for injection standards and semiconductor ultrapure water specifications are driving continuous cartridge performance improvement and validation investment by manufacturers seeking to maintain qualification status with high-value industrial and pharmaceutical customer accounts.

Key Challenges

Proliferation of Low-Cost Counterfeit and Non-Compliant Filtration Cartridges Undermining Consumer Trust, Depressing Market Pricing, and Creating Product Performance and Safety Risks

The global water filtration cartridges market is significantly affected by the widespread availability of counterfeit, substandard, and non-certified replacement cartridges sold through e-commerce platforms and informal distribution channels at prices substantially below those of authenticated branded products, representing a serious challenge for established filtration system manufacturers whose aftermarket replacement cartridge revenue streams and brand reputation are directly threatened by consumer substitution of inferior products that may fail to deliver claimed contaminant reduction performance and may introduce secondary contamination risks from unvalidated filter media materials. Effectively policing counterfeit cartridge distribution across fragmented online retail ecosystems, particularly in Asia-Pacific and Latin American markets, remains an ongoing enforcement challenge for brand owners and regulatory authorities.

Environmental Concerns Over Spent Filtration Cartridge Disposal and Single-Use Plastic Filter Housing Waste Creating Reputational Risk and Regulatory Pressure for Cartridge Manufacturers

The growing volume of spent water filtration cartridges generating solid waste in landfill disposal streams is attracting increasing scrutiny from environmental regulators, sustainability-focused consumers, and plastic waste reduction advocacy groups, as the combination of plastic filter housings, saturated filter media, and mixed-material composite construction of many cartridge products renders them unsuitable for conventional municipal recycling programs and difficult to recover through specialized take-back schemes at the scale of market volumes generated by the global installed base of residential, commercial, and industrial filtration systems. Developing technically feasible, economically viable, and operationally convenient cartridge recycling and circular economy solutions that reduce end-of-life waste without compromising the hygienic handling and disposal of contaminated filter media represents a material product design and sustainability strategy challenge for cartridge manufacturers.

Consumer Price Sensitivity and Inconsistent Cartridge Replacement Compliance Limiting Revenue Realization and Water Quality Performance Outcomes Across Price-Sensitive End User Segments

Consumer price sensitivity to replacement cartridge costs in residential and light commercial market segments creates persistent downward pressure on aftermarket cartridge pricing, incentivizes substitution with low-cost non-branded alternatives, and contributes to replacement interval non-compliance where users extend cartridge service lives beyond recommended replacement schedules to reduce ongoing filtration expenditure, compromising contaminant reduction performance and creating false consumer confidence in filtration effectiveness that undermines both public health outcomes and brand credibility. Educating diverse consumer segments across varying literacy levels, cultural contexts, and income groups about the critical importance of timely cartridge replacement for maintaining filtration performance represents a sustained marketing and consumer engagement challenge for filtration system brands and distribution channel partners globally.

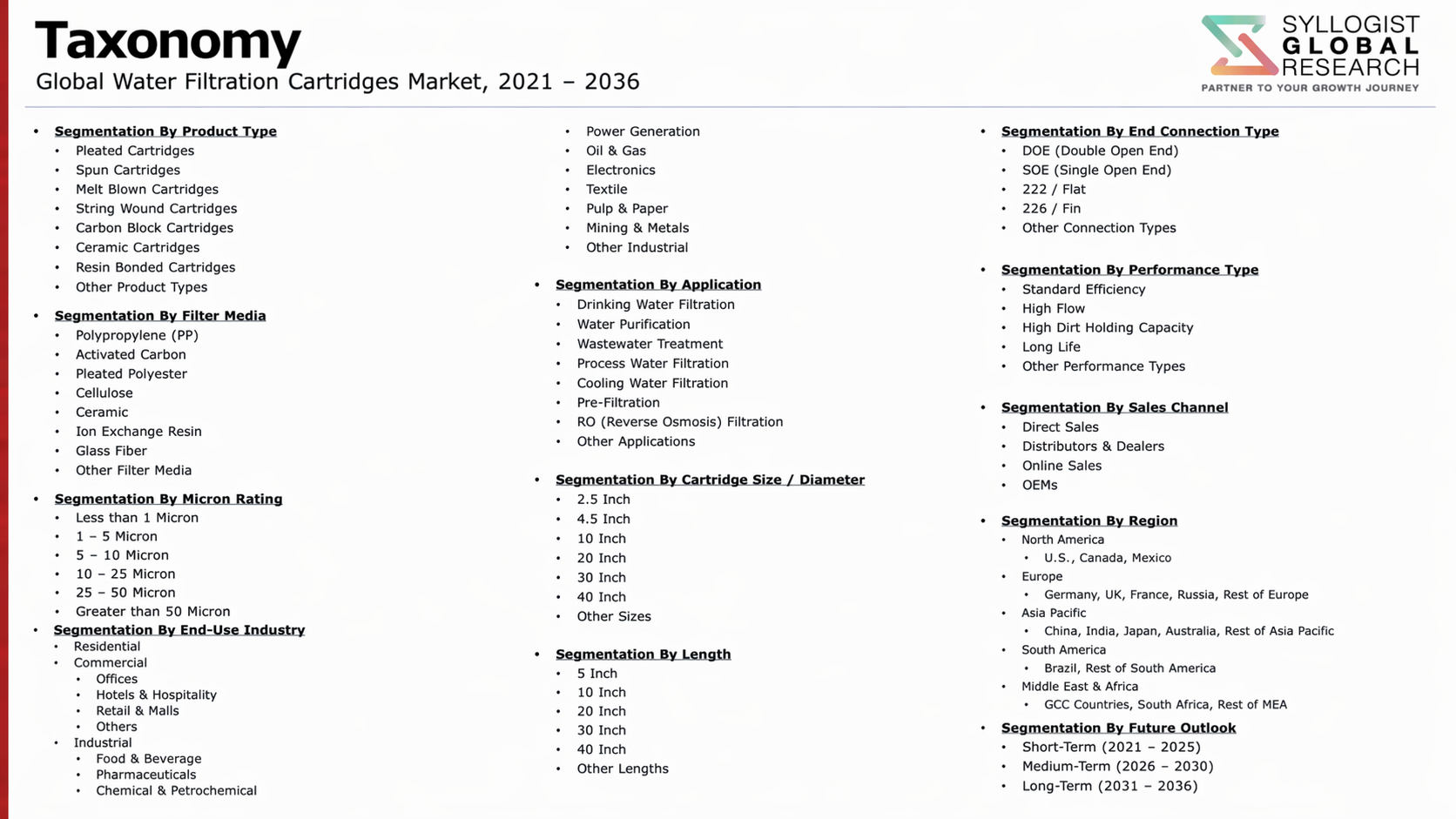

Market Segmentation

- Segmentation By Filtration Technology

- Mechanical and Sediment Depth Filtration Cartridges

- Activated Carbon Block and Granular Carbon Cartridges

- Reverse Osmosis Membrane Cartridges

- Ion Exchange and Water Softening Cartridges

- Ultrafiltration and Hollow Fiber Membrane Cartridges

- Ultraviolet Disinfection Lamp Cartridges

- Multi-Stage and Combination Media Cartridges

- Others

- Segmentation By Filter Media

- Activated Carbon (Block and Granular)

- Polypropylene and Polyester Fiber

- Ceramic and Diatomaceous Earth

- Ion Exchange Resin

- Reverse Osmosis and Ultrafiltration Membranes

- Specialty and Composite Media

- Others

- Segmentation By Micron Rating

- Absolute Rated Below 1 Micron (Ultrafine Filtration)

- 1 to 5 Micron (Fine Particle Filtration)

- 5 to 25 Micron (Standard Sediment Filtration)

- Above 25 Micron (Coarse Pre-Filtration)

- Segmentation By End Use Application

- Drinking Water and Point-of-Use Purification

- Whole-House and Point-of-Entry Filtration

- Industrial Process and Ultrapure Water Treatment

- Food and Beverage Processing and Quality Control

- Pharmaceutical and Sterile Water Production

- Aquarium, Pool, and Recreational Water Filtration

- Others

- Segmentation By Distribution Channel

- Direct Sales and Original Equipment Manufacturer Supply

- Specialty Water Treatment Retailers and Distributors

- E-Commerce and Online Marketplace Platforms

- Home Improvement and Mass Retail Channels

- Others

- Segmentation By End User

- Residential Households

- Commercial Buildings and Food Service Operators

- Industrial and Manufacturing Facilities

- Healthcare and Medical Facilities

- Municipal Water Treatment Utilities

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global water filtration cartridges market valuation in 2025, projected through 2034, segmented by filtration technology, filter media, and end use application, enabling cartridge manufacturers, filtration system brands, and channel distributors to identify the highest-growth product categories and most durable procurement opportunities across the global water filtration cartridge landscape?

- How are evolving regulatory frameworks governing emerging contaminants including per- and polyfluoroalkyl substances, lead, microplastics, and disinfection byproducts across North America, Europe, and Asia-Pacific reshaping consumer demand profiles, performance specification requirements, and certification standards for residential, commercial, and industrial water filtration cartridge products through 2034?

- Which filtration technology segments, specifically activated carbon block cartridges, reverse osmosis membrane systems, ultrafiltration hollow fiber cartridges, and multi-stage combination media products, are generating the highest adoption growth through 2034, and what contaminant removal performance, installation convenience, water efficiency, and total cost of ownership factors are driving consumer and commercial purchasing decisions in each category?

- How is the competitive landscape structured among global filtration cartridge manufacturers, private label producers, and e-commerce marketplace participants, and what brand investment, product innovation, proprietary cartridge form factor design, retail channel management, and counterfeit enforcement strategies are enabling established manufacturers to defend aftermarket replacement cartridge revenue share against low-cost competition?

- What sustainability pressures, single-use plastic reduction regulations, and end-of-life cartridge waste management challenges are shaping product design innovation priorities for filtration cartridge manufacturers, and what recycling program structures, cartridge take-back schemes, biodegradable media developments, and refillable cartridge formats are emerging to address environmental concerns without compromising water treatment performance or hygienic safety standards?

- How is the structural shift from single-use bottled water to filtration-based drinking water solutions, driven by plastic waste reduction policies and corporate sustainability commitments, translating into quantifiable demand growth for point-of-use filtration systems and replacement cartridges across residential, institutional, hospitality, and public infrastructure end user segments in key regional markets through 2034?

- What industrial process water quality requirements, pharmaceutical water purity standards, semiconductor ultrapure water specifications, and food and beverage hygienic processing obligations are defining the performance, validation, and compliance characteristics of high-value specialty filtration cartridge categories, and how are leading manufacturers differentiating through application engineering expertise, regulatory documentation support, and long-term qualification maintenance with industrial and pharmaceutical customers?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Cost Volatility, Polymer & Filter Media Price Fluctuation Risk

- Counterfeit & Low-Quality Cartridge Products, Brand Integrity & Consumer Safety Risk

- Regulatory Tightening, NSF/ANSI Certification & Contaminant Reduction Claim Compliance Risk

- Technology Substitution, Point-of-Use Purifier & Alternative Filtration Solution Competition Risk

- Supply Chain Disruption, Single-Source Dependency & Logistics Cost Risk

- Regulatory Framework & Standards

- NSF/ANSI 42, 53, 58 & 401 Certification Standards for Drinking Water Filtration Cartridges

- WHO Drinking Water Quality Guidelines & International Standards for Cartridge Contaminant Reduction

- EU Drinking Water Directive, KTW & ACS Material Standards for Cartridge Components in Contact with Potable Water

- FDA, USP & Pharmaceutical Grade Filtration Cartridge Standards for Food, Beverage & Life Sciences Applications

- Industrial Filtration Cartridge Standards: ISO 4572, ISO 16889 & Filter Performance Test Protocols

- Single-Use Plastics Regulation, Extended Producer Responsibility (EPR) & Cartridge Recyclability Standards

- Global Water Filtration Cartridges Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped)

- Market Size & Forecast by Cartridge Type

- Sediment Filtration Cartridges (Spun Polypropylene, Melt-Blown & String-Wound)

- Activated Carbon Block (ACB) Filtration Cartridges

- Granular Activated Carbon (GAC) Filtration Cartridges

- Reverse Osmosis (RO) Membrane Cartridges & Elements

- Ultrafiltration (UF) & Microfiltration (MF) Membrane Cartridges

- Ceramic & Candle Filter Cartridges

- Ion Exchange & Water Softening Cartridges

- Inline & Quick-Connect Refrigerator & Ice Maker Filter Cartridges

- Multi-Stage & Combination Filter Cartridges

- Specialty Cartridges: Fluoride, Arsenic, Nitrate & Heavy Metal Reduction Cartridges

- Industrial Depth & Pleated Filter Cartridges

- Market Size & Forecast by Filter Media

- Polypropylene (PP) Filter Media

- Activated Carbon (Coconut Shell, Coal & Wood-Based) Filter Media

- Ceramic & Diatomaceous Earth Filter Media

- Polyethersulfone (PES), PVDF & Polymeric Membrane Filter Media

- Ion Exchange Resin Filter Media

- Glass Fibre, Cellulose & Natural Fibre Filter Media

- Nanofibre & Advanced Composite Filter Media

- Market Size & Forecast by Micron Rating

- Coarse Filtration (Above 50 Microns)

- Standard Sediment Filtration (5 to 50 Microns)

- Fine Filtration (1 to 5 Microns)

- Sub-Micron & Ultrafine Filtration (Below 1 Micron)

- Market Size & Forecast by Housing Compatibility & Form Factor

- Standard 10-Inch & 20-Inch Big Blue Cartridges (Threaded & Sump-Style Housing)

- Inline & Quick-Connect Cartridges (Push-Fit, Twist-Lock & Snap-In)

- OEM & Proprietary Branded Cartridges (Appliance-Specific Formats)

- Industrial & High-Flow Cartridges (30-Inch, 40-Inch & Jumbo Format)

- Capsule, Mini-Pleated & Single-Use Cartridge Formats

- Market Size & Forecast by Application

- Residential Point-of-Use (POU) & Under-Sink Water Filtration

- Residential Point-of-Entry (POE) & Whole-House Filtration

- Commercial & Office Water Filtration (Dispensers, Coolers & Coffee Machines)

- Municipal Drinking Water Treatment & Pre-Treatment Filtration

- Food & Beverage Processing & Ingredient Water Filtration

- Pharmaceutical, Biotech & Laboratory Ultrapure Water Filtration

- Industrial Process Water & Cooling Water Filtration

- Hospitality, Healthcare & Institutional Water Filtration

- Aquarium, Pool & Recreational Water Filtration

- Market Size & Forecast by End-User

- Residential Consumers

- Commercial & Institutional Buildings

- Municipal Water Utilities

- Food & Beverage Producers

- Pharmaceutical & Life Sciences Companies

- Industrial & Manufacturing Facilities

- Healthcare & Hospital Facilities

- Market Size & Forecast by Sales Channel

- OEM & Direct Manufacturer Sales (Appliance & System Bundled Cartridges)

- Retail & Home Improvement Store Channel

- Online & E-Commerce Channel

- Distributor, Wholesaler & Water Treatment Dealer Network

- Subscription & Auto-Replenishment Service Channel

- Industrial & Commercial Direct Supply Channel

- North America Water Filtration Cartridges Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Cartridge Type

- By Filter Media

- By Micron Rating

- By Housing Compatibility & Form Factor

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Water Filtration Cartridges Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Cartridge Type

- By Filter Media

- By Micron Rating

- By Housing Compatibility & Form Factor

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Water Filtration Cartridges Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Cartridge Type

- By Filter Media

- By Micron Rating

- By Housing Compatibility & Form Factor

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Water Filtration Cartridges Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Cartridge Type

- By Filter Media

- By Micron Rating

- By Housing Compatibility & Form Factor

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Water Filtration Cartridges Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Cartridge Type

- By Filter Media

- By Micron Rating

- By Housing Compatibility & Form Factor

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Water Filtration Cartridges Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Cartridge Type

- By Filter Media

- By Micron Rating

- By Housing Compatibility & Form Factor

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Activated Carbon Block (ACB) Cartridge Technology: Formulation, Pore Structure, Contaminant Reduction Performance & NSF Certification

- Hollow Fibre UF & MF Membrane Cartridge Technology: Module Design, Backwashability & Point-of-Use Performance

- Nanofibre, Electrospun & Advanced Composite Filter Media Technology for Sub-Micron Particle & Pathogen Removal

- Emerging Contaminant Removal Technology: PFAS, Microplastics, Pharmaceuticals & Endocrine Disruptors in Filter Cartridges

- Smart & IoT-Enabled Cartridge Monitoring: Filter Life Sensors, Flow Meters & Auto-Replacement Alert Systems

- Sustainable & Bio-Based Cartridge Materials: Biodegradable Housings, Compostable Media & Recyclable Cartridge Design

- Antimicrobial, Silver-Impregnated & Bacteriostatic Filter Cartridge Technology

- Patent & IP Landscape in Water Filtration Cartridge Technologies

- Value Chain & Supply Chain Analysis

- Polypropylene, Activated Carbon & Specialty Filter Media Raw Material Supply Chain

- Membrane Polymer, Ion Exchange Resin & Ceramic Material Supply Chain

- Cartridge Housing, End-Cap & Structural Component Manufacturing Supply Chain

- Cartridge Assembly, Filling, Pleating & Quality Testing Manufacturing Supply Chain

- OEM, Private Label & Contract Manufacturing Channel

- Retail, E-Commerce, Distributor & Dealer Channel

- Aftermarket Replacement Cartridge & Subscription Replenishment Channel

- Pricing Analysis

- Cartridge Unit Price Analysis by Cartridge Type & Filter Media

- OEM Branded vs. Compatible & Private Label Cartridge Price Comparison

- Total Cost of Ownership (TCO): Cartridge Replacement Frequency, Annual Cost & System Lifecycle Analysis

- Retail vs. Online vs. Subscription Channel Pricing Structure Analysis

- Industrial & High-Flow Cartridge Pricing vs. Consumer Grade Cartridge Pricing Analysis

- Price Trend Analysis: Impact of Activated Carbon, Polymer & Membrane Costs on Cartridge Pricing

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Water Filtration Cartridges: Carbon Footprint, Plastic Waste Generation & End-of-Life Impact

- Cartridge Recyclability, Take-Back Programmes & Manufacturer Extended Producer Responsibility (EPR) Initiatives

- Transition to Biodegradable, Compostable & Sustainable Filter Cartridge Materials

- Comparison of Filtered Tap Water vs. Bottled Water: Carbon Footprint, Plastic Reduction & SDG 12 Contribution

- SDG 6 (Clean Water & Sanitation) Contribution, ESG Alignment & Green Procurement Standards

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Cartridge Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Cartridge Type, Application & Geography

- Player Classification

- Large Diversified Water Treatment & Filtration Companies (Multi-Product Portfolio)

- Specialist Residential & Commercial POU/POE Filtration Cartridge Manufacturers

- OEM & Appliance-Integrated Cartridge Suppliers (Refrigerator, Dispenser & RO System)

- Industrial & High-Flow Filtration Cartridge Specialists

- Private Label, Contract & Compatible Replacement Cartridge Manufacturers

- Sustainable & Next-Generation Filtration Material & Cartridge Innovators

- Competitive Analysis Frameworks

- Market Share Analysis by Cartridge Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Water Filtration Cartridge Products & Technology Portfolio

- Key Customer Relationships & Reference Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Water Filtration Cartridge Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Cartridge Type, Filter Media, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output