Global Advanced Air Mobility Ground Infrastructure Market By Infrastructure Type, By Location, By Component, By Application, By Power Source, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Advanced Air Mobility Ground Infrastructure Market encompasses the planning, design, construction, deployment, and operational management of physical and digital infrastructure platforms required to enable safe, scalable, and commercially viable operation of electric vertical take-off and landing (eVTOL) aircraft, electric short take-off and landing (eSTOL) platforms, autonomous cargo drones, and emerging hybrid-electric advanced air mobility vehicles across urban, suburban, regional, and airport-integrated operating environments globally. The market includes vertiports spanning vertihubs, vertibases, and vertipads, alongside high-power eVTOL charging stations, battery swap systems, hydrogen fueling installations, dedicated maintenance, repair and overhaul facilities, integrated unmanned and manned traffic management platforms, ground support equipment, passenger terminals, cargo handling infrastructure, ground power units, fire and rescue systems, and digital orchestration platforms encompassing flight scheduling software, booking interfaces, predictive maintenance analytics, and weather and airspace integration services. The market addresses critical operational requirements including FAA Engineering Brief 105 vertiport design compliance, EASA Vertiport Prototype Technical Specifications certification, secure rooftop structural reinforcement, high-power grid interconnection capable of supporting megawatt-class fast charging cycles, fire suppression for lithium battery thermal events, and seamless integration with existing aviation, urban transit, and last-mile mobility networks. End users span dedicated eVTOL operators, airport authorities, real estate developers, urban transit agencies, logistics and parcel delivery providers, emergency medical service operators, government agencies, and infrastructure investment funds backing greenfield vertiport portfolio development. Geographic deployment spans early-mover North American and European urban air mobility markets, rapidly scaling Asia-Pacific deployment hubs, and ambitious Middle Eastern smart city programs, establishing AAM ground infrastructure as the foundational enabling layer underpinning the commercial launch and long-term scaling of urban and regional advanced air mobility ecosystems worldwide.

Market Insights

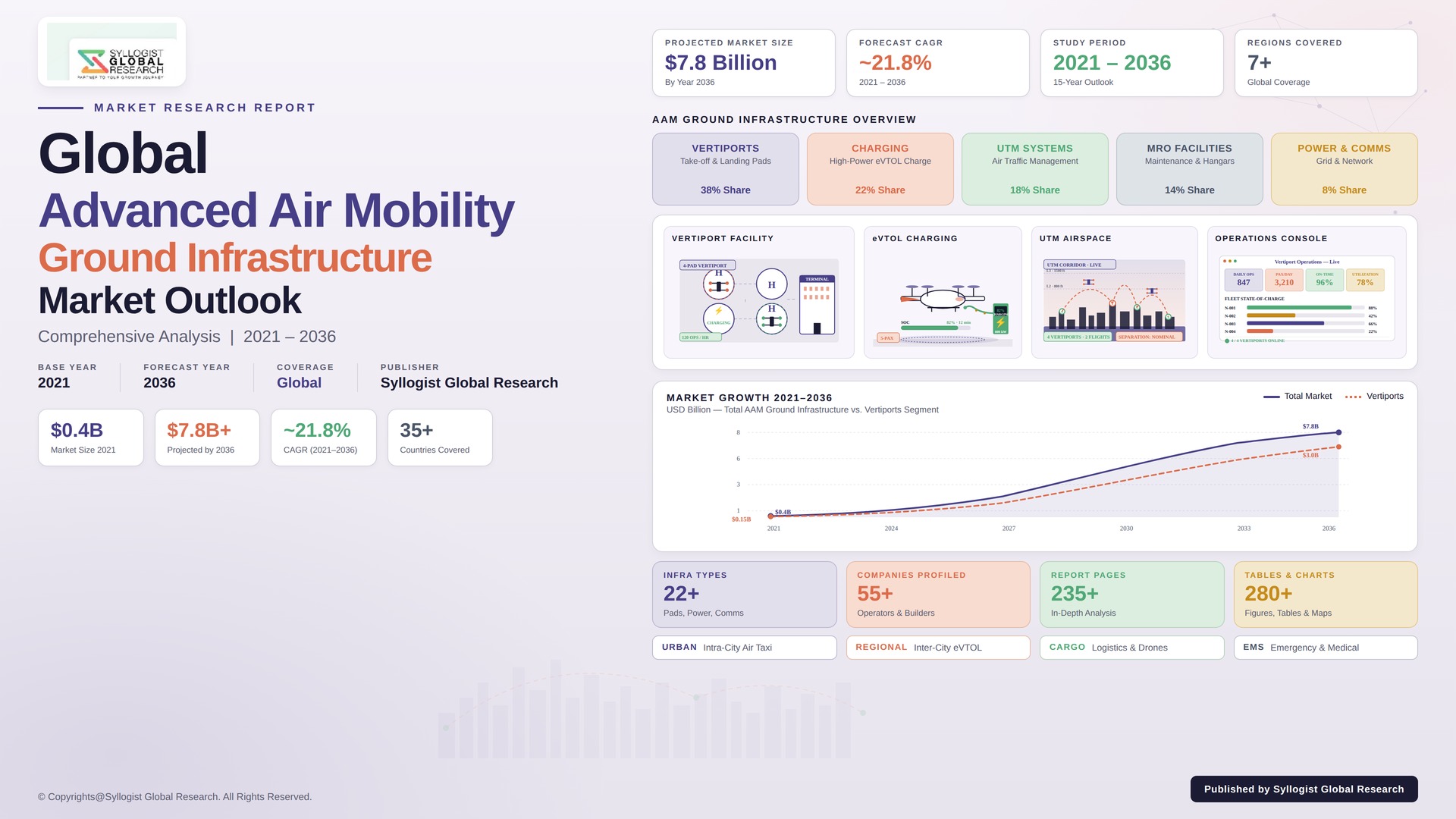

The global advanced air mobility ground infrastructure market is moving through an early-stage hyper-growth phase shaped by accelerating eVTOL aircraft type certification milestones across leading platform developers, surging public and private capital flowing into vertiport portfolio development, and progressively maturing regulatory frameworks across the FAA, EASA, and Asia-Pacific civil aviation authorities that are systematically de-risking commercial launch timelines for urban air mobility services. The market was valued at USD 1.4 billion in 2025 and is projected to reach USD 19.0 billion by 2034, advancing at a compound annual growth rate of 33.6% through the forecast window, supported by accelerating Joby, Archer, Volocopter, Vertical Aerospace, and Lilium type certification progress, expanding US Department of Transportation AAM National Strategy implementation, and broadening Middle Eastern and Asian smart city programs anchoring greenfield vertiport portfolio buildouts across major metropolitan corridors worldwide.

Infrastructure capital intensity is the strongest secular force restructuring the demand profile for AAM ground infrastructure, as vertiport developers, eVTOL operators, and airport authorities increasingly recognize that scalable urban air mobility services cannot launch commercially without coordinated investment in vertiport real estate, megawatt-class fast charging networks, integrated traffic management platforms, and seamless ground transportation connections. The result is a measurable shift in revenue mix from individual vertipad demonstrators toward integrated network buildouts incorporating multiple vertihubs, mid-tier vertibases, charging-equipped vertipads, ground support equipment depots, and digital orchestration platforms enabling fleet-scale operation across regional networks. Real estate developers, infrastructure investment funds, and airport operators are simultaneously consolidating early-stage development under integrated network concession agreements, restructuring infrastructure economics in favor of partners offering integrated vertiport design, construction, charging deployment, and long-term operations and maintenance service capability across multi-site portfolio scaleups globally.

Within the infrastructure taxonomy, vertiports anchor the highest current revenue concentration, encompassing vertihub flagship facilities at major airport interfaces, mid-tier vertibases serving suburban and regional hubs, and distributed vertipads supporting last-mile commuter services. eVTOL charging infrastructure represents the fastest-growing component category, expanding at rates above 31% annually as operators deploy fleet-scale fast charging networks supporting frequent turnaround cycles, while battery swap stations and emerging hydrogen fueling installations are gaining attention for hybrid-electric platform applications. Air traffic management and unmanned traffic management platforms, including UTM systems integrated with controlled airspace, are scaling rapidly under FAA, EASA, and ASTM-led standardization initiatives. Rooftop and elevated vertiport configurations are gaining priority for dense urban deployment, while ground-based airport-integrated configurations dominate near-term revenue, reshaping competitive differentiation among integrated AAM ground infrastructure providers worldwide.

North America anchors the largest absolute revenue share of the global advanced air mobility ground infrastructure market, valued near USD 480 million in 2025 and underpinned by accelerating FAA Engineering Brief 105 vertiport design adoption, US Department of Transportation AAM National Strategy implementation, and high-profile Joby, Archer, and Beta Technologies infrastructure partnerships across New York, Los Angeles, Miami, and Dallas metropolitan corridors. Europe represents a structurally critical share driven by EASA Vertiport Prototype Technical Specifications, expanding Skyports, Ferrovial, Groupe ADP, and UrbanV portfolio buildouts, and Olympic-driven vertiport deployment in Paris alongside German and United Kingdom pilot programs. Asia-Pacific is positioned to record the highest forecast period CAGR, supported by South Korea K-UAM Grand Challenge, Japan Osaka Expo deployment, Singapore CAAS-led pilot programs, and ambitious Chinese eVTOL infrastructure rollouts across the Greater Bay Area. The Middle East contributes through ambitious United Arab Emirates and Saudi Arabia smart city integration, including the Dubai-Abu Dhabi air taxi corridor and NEOM AAM development.

Key Drivers

Accelerating eVTOL Aircraft Type Certification Progress and Commercial Launch Timelines Driving Urgent Vertiport and Charging Infrastructure Deployment

Accelerating eVTOL aircraft type certification progress across Joby Aviation, Archer Aviation, Beta Technologies, Volocopter, Vertical Aerospace, Lilium, EHang, and emerging Chinese platform developers is creating compressed timelines for matching ground infrastructure deployment, as commercial launch dates anchored to 2026 and 2027 require vertiports, charging networks, and traffic management systems operational well in advance of first revenue flights. Vertiport developers, airport authorities, and infrastructure investment funds are responding with capital deployment, network design contracts, and long-term concession agreements anchoring multi-year demand visibility for AAM ground infrastructure suppliers across global metropolitan markets.

Government and Civil Aviation Authority Investment in Urban Air Mobility Programs and Smart City Integration Frameworks Anchoring Public-Sector Infrastructure Demand

Substantial government investment across the United States Department of Transportation AAM National Strategy, FAA Engineering Brief 105, EASA Vertiport Prototype Technical Specifications, South Korea K-UAM Grand Challenge, Japan AAM roadmap, Singapore CAAS pilot programs, and ambitious United Arab Emirates and Saudi Arabia smart city integration initiatives is anchoring durable demand for vertiport design, construction, traffic management, and operations services across global metropolitan corridors. Public-sector co-funding, regulatory certainty, and airspace integration commitments are progressively de-risking infrastructure development economics for private sector vertiport operators and infrastructure investors worldwide throughout the forecast horizon.

Urban Congestion, Decarbonization Mandates, and Sustainable Urban Mobility Pressures Driving Long-Cycle Investment in eVTOL Ground Infrastructure Networks

Persistent urban congestion across major global metropolitan areas, alongside ambitious decarbonization mandates targeting transportation sector emission reductions, is accelerating long-cycle investment in eVTOL ground infrastructure networks positioned as foundational enablers of zero-emission, low-noise, time-saving urban and regional air mobility services. Real estate developers, transit authorities, airport operators, and infrastructure investment funds increasingly view vertiport portfolio development as strategically aligned with sustainable urban mobility roadmaps, anchoring multi-decade demand visibility for AAM ground infrastructure design, construction, charging, and operations service providers across global metropolitan markets.

Key Challenges

Capital Intensity, Urban Land Acquisition Costs, and Real Estate Constraints Limiting Vertiport Network Scaleup in Dense Metropolitan Areas

Vertiport network scaleup faces persistent capital intensity challenges driven by urban land acquisition costs, rooftop structural reinforcement requirements, fire suppression mandates for lithium battery thermal events, and integration costs with existing buildings and ground transportation networks across dense metropolitan areas where eVTOL passenger demand is concentrated. Vertiport developers face extended development timelines, complex zoning approval processes, and elevated capital requirements per site, particularly for vertihub flagship installations supporting multi-aircraft simultaneous operations, constraining the pace of network buildout across major global cities throughout the forecast period.

Maturing Regulatory Frameworks, Vertiport Certification Standards, and Airspace Integration Complexity Constraining Commercial Launch Timelines

Vertiport certification standards, eVTOL operational rules, pilot certification frameworks, and integration of urban airspace with existing controlled airspace remain in maturation across the FAA, EASA, Transport Canada, CAAS, and other civil aviation authorities, creating regulatory uncertainty that constrains commercial launch timelines, infrastructure investment risk profiles, and deployment economics across global AAM ground infrastructure markets. Vertiport developers, eVTOL operators, and infrastructure investment funds face persistent challenges navigating evolving rulemaking, public comment cycles, and harmonization gaps between national frameworks, elevating program timelines and certification cost burdens across multi-jurisdictional vertiport portfolio deployments globally.

Grid Capacity Constraints, Megawatt-Class Charging Power Requirements, and Battery Technology Limitations Pressuring Vertiport Energy Infrastructure Economics

eVTOL ground charging infrastructure faces persistent grid capacity constraints, megawatt-class fast charging power demands, and battery technology limitations spanning energy density, cycle life, and thermal management that pressure vertiport energy infrastructure economics across high-density metropolitan deployment scenarios. Vertiport operators must coordinate utility interconnection upgrades, deploy on-site battery energy storage systems, integrate renewable generation where feasible, and manage charging schedules around utility demand charges, while ongoing battery technology evolution introduces equipment refresh risk across deployed charging assets, complicating long-term infrastructure investment planning across global AAM ground infrastructure programs throughout the forecast period.

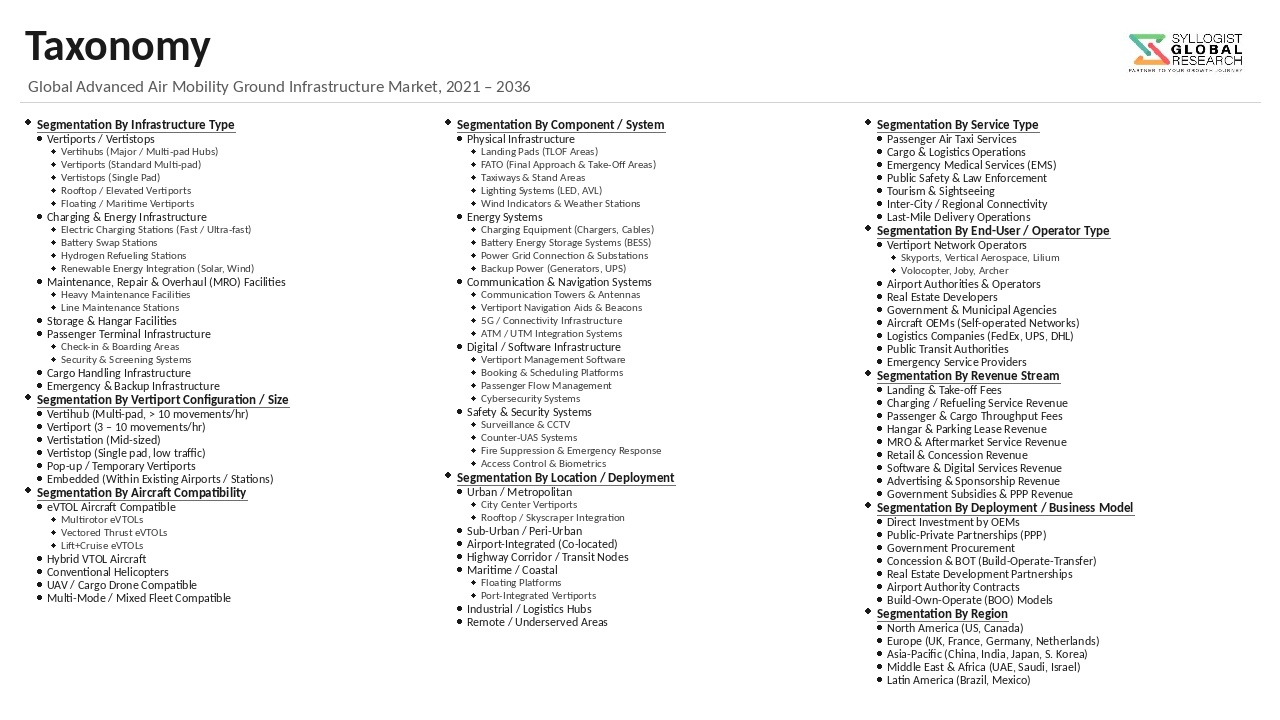

Market Segmentation

- Segmentation By Infrastructure Type

- Vertiports – Vertihubs

- Vertiports – Vertibases

- Vertiports – Vertipads

- Charging Infrastructure (Fast Charging, Slow Charging, Battery Swap)

- Hydrogen Fueling Stations

- Maintenance, Repair, and Overhaul (MRO) Facilities

- Air Traffic Management and Unmanned Traffic Management (UTM)

- Ground Support Equipment

- Passenger Terminals and Cargo Handling

- Others

- Segmentation By Location

- Urban (Rooftop and Elevated)

- Suburban (Ground-Based)

- Rural and Regional

- Airport-Integrated

- Heliport Conversion and Brownfield Reuse

- Segmentation By Component

- Hardware (Pads, Charging Stations, Lighting, Ground Power, Fire Suppression)

- Software (Operations Management, Booking, ATM, UTM, Predictive Maintenance)

- Services (Design, Construction, Operations and Maintenance, Consulting)

- Segmentation By Application

- Passenger Air Taxi and Premium Mobility

- Cargo and Logistics Delivery

- Emergency Medical Services (EMS) and Air Ambulance

- Public Safety, Defense, and Border Protection

- Inspection, Surveillance, and Aerial Work

- Others

- Segmentation By Power Source

- Grid-Connected Conventional Energy

- Renewable Energy (Solar, Wind, Battery Energy Storage)

- Hybrid Power Architectures

- Segmentation By End User

- eVTOL Operators and Air Taxi Service Providers

- Airport Authorities

- Real Estate and Infrastructure Developers

- Government and Civil Aviation Authorities

- Logistics and Parcel Delivery Companies

- Healthcare and Emergency Medical Service Providers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Advanced Air Mobility Ground Infrastructure Market in 2025, projected through 2034, disaggregated by infrastructure type, location, and end-user application, enabling vertiport developers, eVTOL operators, infrastructure investment funds, and civil aviation planners to identify highest-growth segments and most durable revenue opportunities across the global AAM infrastructure landscape?

- How are eVTOL aircraft type certification milestones across Joby Aviation, Archer Aviation, Beta Technologies, Volocopter, Vertical Aerospace, Lilium, and emerging Chinese platform developers reshaping vertiport deployment timelines, charging infrastructure capacity planning, and commercial launch readiness across global metropolitan markets through 2034?

- How are FAA Engineering Brief 105, EASA Vertiport Prototype Technical Specifications, South Korea K-UAM Grand Challenge, Singapore CAAS pilot programs, and equivalent regulatory frameworks shaping vertiport certification, design standards, airspace integration, and commercial deployment economics across global AAM ground infrastructure markets?

- Which AAM ground infrastructure component categories, including vertiports, eVTOL charging stations, battery swap systems, MRO facilities, and air traffic management platforms, are recording the highest forecast period growth rates, and what eVTOL fleet scaling, charging cycle, and operational throughput factors are shaping demand intensity within each segment?

- How are urban land acquisition costs, rooftop structural engineering requirements, megawatt-class grid interconnection challenges, and integration with existing ground transportation networks shaping vertiport site selection, capital deployment economics, and network buildout pacing across major global metropolitan markets through the forecast horizon?

- What partnership, public-private partnership, infrastructure investment fund, real estate developer, and airport authority strategies are dominant AAM ground infrastructure providers using to consolidate early-mover advantage, secure metropolitan-scale concessions, and scale vertiport portfolios across global regions?

- Which regional markets, specifically the United States, the United Kingdom, France, Germany, the United Arab Emirates, Saudi Arabia, South Korea, Japan, Singapore, and China, are expected to generate the most substantial incremental advanced air mobility ground infrastructure investment through 2034, and what smart city, decarbonization, and urban congestion factors are anchoring procurement growth in each market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Vertiport Certification, Regulatory Uncertainty (FAA EB-105, EASA PS-VPT) & Approval Delay Risk

- eVTOL OEM Bankruptcy, Programme Cancellation & Aircraft Type Certification Delay Risk

- Power Grid Capacity, Megawatt Charging Demand & Local Distribution Network Reliability Risk

- Public Acceptance, Noise, Land Use, Zoning & NIMBY Risk

- Project Financing, Capital Structure, Long Payback & Demand Ramp-Up Risk

- Regulatory Framework & Standards

- FAA Engineering Brief 105 (EB-105) Vertiport Design & Advisory Circular 150/5390 Heliport Design Standards

- EASA Prototype Specifications for Design of VFR Vertiports (PS-VPT-DSN) & AAM Implementation Plan

- ICAO Annex 14 Volume II (Heliports), AAM Concept of Operations & International Coordination Standards

- Local Zoning, Building Code, Noise Ordinance, NEPA Environmental Review & Land Use Regulation

- Spectrum Allocation, UTM Cybersecurity & Communication Infrastructure Compliance Standards

- Global Advanced Air Mobility Ground Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Vertiports & Charging Stations)

- Market Size & Forecast by Infrastructure Type

- Vertiports & Vertihubs (Including FATO and TLOF Areas)

- Passenger Terminal & Ground Handling Facility

- Maintenance, Repair & Overhaul (MRO) Hangar

- eVTOL Charging Station (DC Fast Charge & Megawatt-Class)

- Battery Swap Station & Mobile Energy Cube

- Hydrogen Refuelling Station for Hydrogen eVTOL

- SAF and Hybrid Refuelling Station

- UAM Air Traffic Management (UTM), Communication & Surveillance Infrastructure

- Power, Microgrid & Energy Storage Infrastructure

- Multimodal Connectivity & Ground Transportation Integration

- Market Size & Forecast by Vertiport Class

- Class 1 Vertistop (Single FATO/TLOF, Limited Operations)

- Class 2 Vertistation (Multiple FATO/TLOF, Medium Throughput)

- Class 3 Vertihub (Full Hub Operations, High Throughput)

- Class 4 Vertibase (Operations and Maintenance Base)

- Market Size & Forecast by Component

- Civil Works (Pavement, Lighting, Signage, Drainage & Perimeter Security)

- Power & Energy (Substation, Transformer, EV Charger & Battery Storage)

- Communications & Surveillance (Radar, ADS-B, Weather Sensor & ATC)

- Passenger Handling (Terminal, Security, Boarding & Gate)

- Maintenance Hangar & Service Facility

- Software & Systems (Vertiport Management, UTM, Fleet & Booking)

- Safety, Fire Suppression & Emergency Response Equipment

- Market Size & Forecast by Location

- Urban Rooftop & Parking Deck

- Ground-Level Urban Site

- Suburban & Greenfield

- Airport-Integrated Vertiport

- Heliport-Converted Vertiport

- Maritime, Harbour & Floating Vertiport

- Off-Grid & Remote Site

- Market Size & Forecast by Mode of Operation

- Passenger Urban Air Mobility (UAM)

- Cargo & Logistics

- Air Ambulance & Medical Transport

- Public Safety, Law Enforcement & Disaster Response

- Military Logistics & Defence Operations

- Market Size & Forecast by End-User

- Commercial AAM Operators (Passenger & Cargo)

- Airport Operators & Aviation Authorities

- Real Estate Developers & Property Owners

- Municipalities & Public Authorities

- Military & Defence Forces

- Healthcare and Emergency Medical Service Providers

- Tourism & Sightseeing Operators

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Project Contract (Engineering, Procurement & Construction)

- Public-Private Partnership (PPP), BOT & Concession Contract

- Direct Equipment & Technology Supply with System Integration

- Operations & Maintenance (O&M) Service & Performance Contract

- North America Advanced Air Mobility Ground Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Vertiports & Charging Stations)

- By Infrastructure Type

- By Vertiport Class

- By Component

- By Location

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Advanced Air Mobility Ground Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Vertiports & Charging Stations)

- By Infrastructure Type

- By Vertiport Class

- By Component

- By Location

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Advanced Air Mobility Ground Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Vertiports & Charging Stations)

- By Infrastructure Type

- By Vertiport Class

- By Component

- By Location

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Advanced Air Mobility Ground Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Vertiports & Charging Stations)

- By Infrastructure Type

- By Vertiport Class

- By Component

- By Location

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Advanced Air Mobility Ground Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Vertiports & Charging Stations)

- By Infrastructure Type

- By Vertiport Class

- By Component

- By Location

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Advanced Air Mobility Ground Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Vertiports & Charging Stations)

- By Infrastructure Type

- By Vertiport Class

- By Component

- By Location

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, United Kingdom, Germany, France, Italy, Spain, Netherlands, Switzerland, Sweden, Norway, China, Japan, India, South Korea, Singapore, Australia, Indonesia, Thailand, Brazil, Argentina, Chile, Saudi Arabia, UAE, Qatar, Israel, Egypt, South Africa, Morocco

- Technology Landscape & Innovation Analysis

- Megawatt-Class DC Fast Charging, Battery Swap Automation & High-Power Energy Delivery Technology Deep-Dive

- Vertiport Operations Centre, Digital Twin & AI-Based Slot Allocation Technology

- Unmanned Aircraft System Traffic Management (UTM), 5G Tactical Mesh & Low-Latency Communication Technology

- Cooperative Surveillance, ADS-B In/Out, Multi-Static Radar & Wake Turbulence Prediction Technology

- Hydrogen Storage, Cryogenic Dispensing & SAF Refuelling Infrastructure Technology

- Distributed Acoustic Sensing, Low-Noise Pad Design & Acoustic Mitigation Technology

- Microgrid, Renewable Integration & Vehicle-to-Grid (V2G) Energy Management Technology

- Patent & IP Landscape in AAM Ground Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Civil Works Contractor, Pavement, Steel & Concrete Material Supply Chain

- Power Equipment, Substation, Transformer & Megawatt Charger Manufacturing Supply Chain

- Surveillance Radar, Weather Sensor, ADS-B & UTM Equipment Supply Chain

- Vertiport Management Software, UTM Platform & Fleet Operations System Development Supply Chain

- EPC Contractor, Project Developer & System Integrator Procurement Landscape

- AAM Operator, Airport Authority & Municipal Authority Procurement Landscape

- Operations & Maintenance Service Provider, Charging Network Operator & Lifecycle Support Channel

- Pricing Analysis

- Vertistop and Vertistation Capital Cost & Cost per Stand Analysis

- Vertihub & Full Hub Vertiport Capital Cost and Cost per FATO Analysis

- Megawatt Charging Equipment, Battery Swap Station & Energy Infrastructure Capital Cost Analysis

- UTM, Surveillance & Vertiport Management System Capital and Subscription Pricing Analysis

- Public-Private Partnership, Concession & Long-Term Lease Tariff Structure Analysis

- Total AAM Ground Infrastructure Programme Economics: Cost per Movement and Throughput Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of AAM Ground Infrastructure: Carbon Footprint, Embodied Energy & Material Footprint Across Vertiport Routes

- Renewable Energy Integration, Microgrid Self-Sufficiency & Pathway to Net-Zero Vertiport Operations

- Noise Footprint, Acoustic Mitigation & Community Sound Management Contribution of Modern Vertiport Design

- Environmental Compliance, Stormwater, Wildlife & Land Use Impact Assessment in Vertiport Siting

- Regulatory-Driven Sustainability, SDG 11 (Sustainable Cities) Alignment & Green Finance Eligibility for AAM Infrastructure

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Component & Geography

- Player Classification

- Vertiport Developer & Operator Companies with Integrated AAM Portfolios

- eVTOL OEM with Vertically-Integrated Vertiport Programmes

- Airport Operators Extending into AAM Ground Infrastructure

- EPC Contractors & Engineering Firms Specialising in Aviation Infrastructure

- Charging Network, Megawatt Power & Energy Infrastructure Specialists

- UTM, Air Traffic Management & Surveillance Technology Providers

- Vertiport Management Software & Digital Operations Platform Providers

- Real Estate Developers, Property Owners & Land Use Specialists

- Distributors, Equipment Suppliers & Lifecycle Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Component & Region

- Company Profile

- Company Overview & Headquarters

- AAM Ground Infrastructure Products & Technology Portfolio

- Key Customer Relationships & Reference Vertiport Deployments

- Manufacturing Footprint & Project Execution Capacity

- Revenue (AAM Infrastructure Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Infrastructure Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Vertiport Class, Component, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)