Global Airport Cargo Handling Systems Market By System Type, By Cargo Type, By Component, By Technology, By Application, By Mode of Operation, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

Airport cargo handling systems are integrated mechanical, electromechanical, robotic, and software platforms engineered to efficiently load, unload, transfer, store, sort, and dispatch air cargo, mail, and unit load devices (ULDs) across cargo terminals, freighter aircraft apron operations, transit hubs, and integrator sortation facilities within airport ecosystems. The Global Airport Cargo Handling Systems Market encompasses the design, manufacturing, integration, deployment, and operation of fixed and powered roller conveyors, automated storage and retrieval systems (AS/RS), ULD handling systems, dolly and tug transporters, ULD build-up and break-down workstations, automated guided vehicles (AGVs), elevating transfer vehicles (ETVs), high-rise ULD storage racks, weighing and dimensioning systems, X-ray screening interfaces, and warehouse control software platforms governing airside-to-landside cargo flows.

The airport cargo handling systems market includes equipment supplied to dedicated cargo terminals, mixed-use passenger and cargo facilities, integrator sortation hubs, perishable transit centers, e-commerce express cargo hubs, and pharmaceutical cold chain transit centers operated within airport landside zones. Market participants include cargo handling system original equipment manufacturers, conveyor and material handling integrators, ULD handling specialists, AGV and ETV developers, AS/RS suppliers, ground support equipment OEMs, warehouse control software providers, and end-to-end airport cargo terminal integrators delivering turnkey terminal automation programs. End users span cargo airline operators, integrator express cargo operators, airport authorities, ground handling service providers, and specialized cargo terminal operators managing perishable, pharmaceutical, e-commerce, and general air freight flows. The airport cargo handling systems market explicitly excludes passenger baggage handling systems, ocean port container handling equipment, road freight cross-dock equipment, and warehouse automation deployed outside airport landside boundaries, focusing exclusively on cargo handling infrastructure supporting airfreight terminal operations globally.

Market Insights

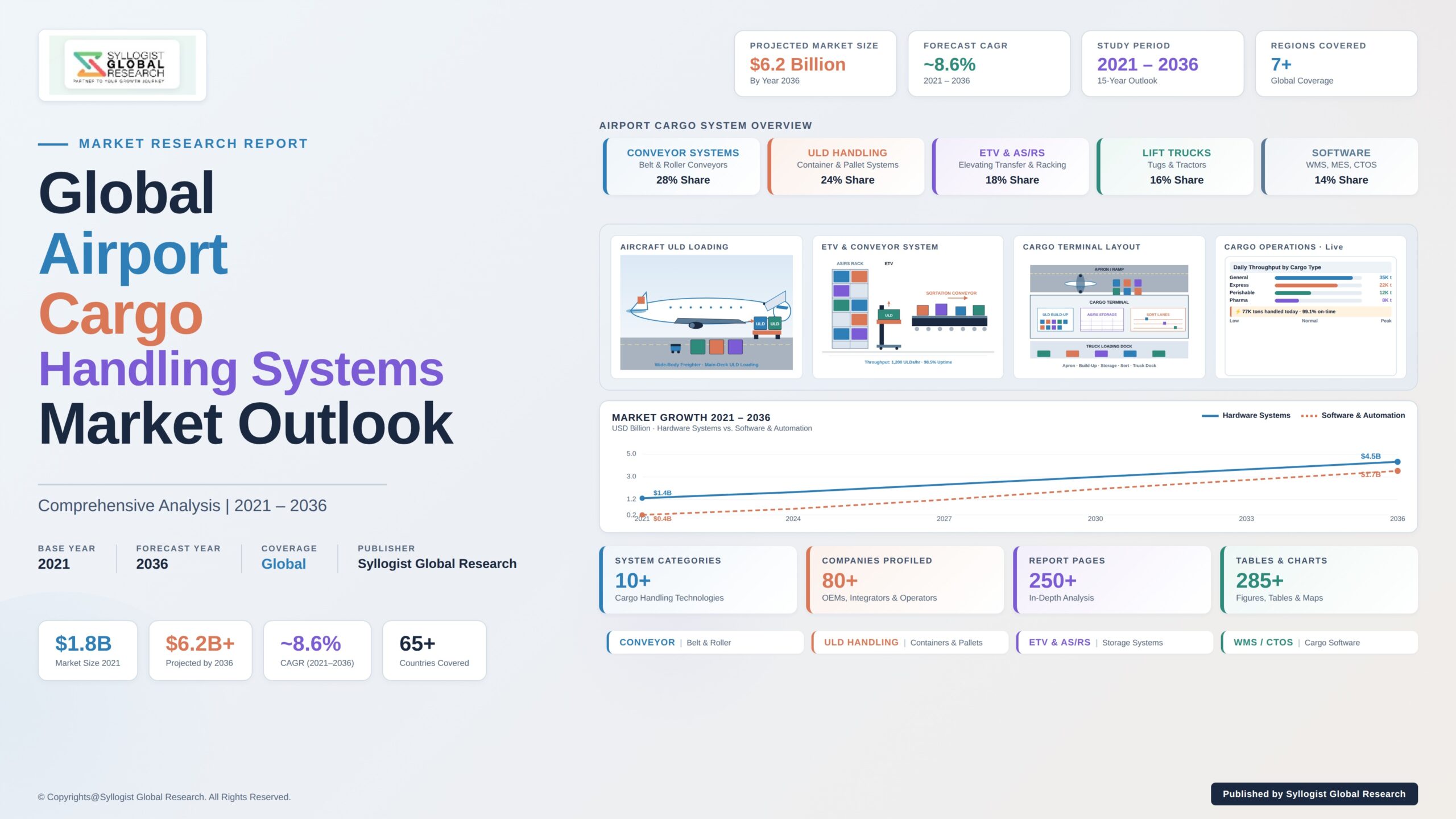

The global airport cargo handling systems market is entering a sustained expansion phase, shaped by accelerating e-commerce express airfreight volumes, recovery and growth of perishable airfreight trade lanes, the scaling of pharmaceutical cold chain airfreight infrastructure, the buildout of integrator regional sortation hubs co-located within airport ecosystems, and tightening operational efficiency expectations driving terminal automation procurement across major airfreight gateways. The airport cargo handling systems market was valued at approximately USD 1.9 billion in 2025 and is projected to reach USD 4.2 billion by 2034, advancing at a compound annual growth rate of 9.2% through the forecast period, as airport authorities, cargo airline operators, integrator express cargo operators, and ground handling service providers scale automated cargo handling capacity at major airfreight gateways across North America, Europe, Asia-Pacific, and the Middle East.

The airport cargo handling systems market trajectory is being reshaped by the commercial maturation of automated ULD storage and retrieval systems, robotic ULD build-up and break-down workstations, AGV-based airside-to-terminal ULD transfer fleets, six-sided machine vision dimensioning and verification systems, and warehouse control platforms that integrate cargo handling system data with airline cargo management systems and customs authority interfaces. Automated ULD storage systems with high-rise racking, multi-level shuttle elevators, and automated retrieval cycle times below 90 seconds have become a default specification at major cargo gateway terminals processing in excess of 1 million tonnes of annual freight. Six-sided machine vision dimensioning systems are now embedded across over 70% of newly commissioned cargo terminals, supporting accurate revenue weight capture, automated chargeable weight calculation, and seamless interface with airline cargo revenue management systems within the airport cargo handling systems market.

Automated storage and retrieval systems (AS/RS) represent the fastest-growing technology segment within the airport cargo handling systems market, propelled by high-throughput cargo gateway terminal commissioning programs across major airfreight hubs requiring high-density ULD storage with automated retrieval supporting integrated airline schedule alignment. Conveyor and roller-bed transfer systems remain the largest revenue contributor within the airport cargo handling systems market, supported by sustained demand across integrator sortation hubs and dedicated cargo terminals where high-volume non-ULD cargo flows benefit from automated conveyor sortation. E-commerce and express cargo applications represent the fastest-growing application segment within the airport cargo handling systems market, propelled by sustained double-digit growth in cross-border e-commerce airfreight, while perishable and pharmaceutical cargo terminals are gaining strategic procurement traction within the airport cargo handling systems market driven by accelerating cross-border perishable trade and biologics airfreight volumes.

Asia-Pacific represents the largest regional market within the airport cargo handling systems market, supported by major cargo gateway terminal commissioning programs at Hong Kong, Shanghai, Guangzhou, Singapore, Incheon, Tokyo Narita, and major Indian airport authorities investing in next-generation cargo terminal automation aligned with sustained cross-border airfreight volume expansion. Hong Kong International Airport handles over 4 million tonnes of cargo annually and continues to invest in next-generation cargo terminal automation capacity. The Middle East has emerged as the second largest regional position within the airport cargo handling systems market, anchored by Dubai International Airport, Doha Hamad International Airport, and emerging cargo gateway capacity in Abu Dhabi and Riyadh, supported by integrator hub expansion and sustained transit cargo flow growth. North America occupies the third regional position within the airport cargo handling systems market, propelled by integrator express cargo terminal automation at Memphis, Louisville, Cincinnati, and Indianapolis hubs, while Europe represents the fourth regional market with sustained automation modernization at Frankfurt, Liege, Amsterdam, Paris Charles de Gaulle, and Leipzig cargo gateway facilities.

Key Drivers

Accelerating Cross-Border E-Commerce Airfreight Volumes, Express Cargo Network Buildout, and Integrator Regional Sortation Hub Expansion Driving Sortation and ULD Handling Procurement

The structural acceleration of cross-border e-commerce airfreight volumes, the rapid buildout of integrator express cargo network capacity, and the commissioning of regional sortation hubs co-located within airport ecosystems are generating durable procurement demand for airport cargo handling systems across major airfreight gateways and emerging integrator hub locations. Global cross-border e-commerce airfreight volumes scaled by over 35% between 2021 and 2025, propelled by sustained marketplace platform expansion, direct-to-consumer cross-border parcel growth from Chinese e-commerce platforms, and consumer preference for expedited international delivery timelines that mandate air-mode logistics fulfillment. Integrator regional sortation hub commissioning programs have been announced or executed at multiple gateway locations including Liege, Leipzig, Cincinnati, Indianapolis, Hong Kong, Guangzhou, Singapore, and Doha, each requiring substantial airport cargo handling systems procurement supporting integrated sortation, ULD build-up, and airside-to-terminal cargo transfer functions. Airport authorities are increasingly structuring multi-year cargo terminal automation procurement frameworks aligning equipment delivery schedules with terminal commissioning timelines, generating long-duration revenue commitments that anchor manufacturer production planning and component supplier capacity scaling decisions across the airport cargo handling systems market value chain globally.

Perishable Airfreight Recovery, Pharmaceutical Cold Chain Airfreight Expansion, and Specialty Cargo Terminal Procurement Driving High-Specification Equipment Demand

The recovery and continued growth of perishable airfreight trade lanes, the structural expansion of pharmaceutical cold chain airfreight, and accelerating procurement of specialty cargo terminal capacity supporting biologics, vaccine, and specialty pharmaceutical airfreight flows are driving sustained procurement of high-specification airport cargo handling systems across major airfreight gateways. Global perishable airfreight volumes recovered above pre-pandemic levels by 2024 and scaled at 6% to 9% compound annual rates through 2025, propelled by sustained cross-border fresh produce, floral, seafood, and chilled meat trade flows requiring temperature-controlled airport cargo handling infrastructure. Pharmaceutical airfreight volumes scaled by over 18% between 2021 and 2025, with biologics, vaccines, cell and gene therapy products, and specialty pharmaceutical airfreight requiring tightly controlled temperature envelopes spanning 2 degrees Celsius to 8 degrees Celsius, minus 20 degrees Celsius, and cryogenic minus 70 degrees Celsius operating ranges. Specialty cargo terminal commissioning programs at Liege, Amsterdam, Frankfurt, Dubai, Doha, and major Asia-Pacific airfreight hubs are driving sustained airport cargo handling systems procurement supporting temperature-zoned storage, cold chain ULD handling, validated pharmaceutical transit infrastructure, and GDP-compliant cargo handling operations within the airport cargo handling systems market.

Cargo Terminal Operational Efficiency Mandates, Throughput Density Optimization, and Labor Cost Inflation Driving Automation Procurement Across Airport Authorities and Ground Handlers

Cargo terminal operational efficiency mandates, the pressure to increase throughput density per square meter of constrained airport landside real estate, and sustained labor cost inflation across major airfreight operating regions are collectively driving accelerated procurement of automated airport cargo handling systems across airport authorities, cargo airline operators, and ground handling service providers. Cargo terminal throughput density requirements have intensified materially over recent years, with major gateway terminals targeting throughput in excess of 50 tonnes per square meter of terminal floor area annually, generating procurement preference for high-density automated storage systems, robotic ULD build-up workstations, and AGV-based airside-to-terminal transfer fleets that maximize cargo throughput capacity per unit of terminal footprint. Logistics sector wages have risen by over 16% across mature airfreight operating regions between 2021 and 2025, materially reducing payback periods for cargo terminal automation capital investments to under 4 years for major gateway facilities within the airport cargo handling systems market. Ground handling service providers operating under pressure-tested commercial contracts are restructuring procurement around automated cargo handling equipment that consistently maintains throughput targets, accuracy benchmarks, and damage-rate performance levels under compressed operational schedules at high-volume airfreight gateways.

Key Challenges

High Capital Intensity, Extended Commissioning Timelines, and Site-Specific Engineering Complexity Constraining Airport Cargo Terminal Automation Procurement Decisions

Airport cargo handling systems remain capital-intensive infrastructure investments, with full-scale cargo gateway terminal automation projects typically requiring USD 50 million to USD 250 million in combined hardware, software, integration, and site preparation investments, generating procurement risk profiles that constrain adoption among second-tier airfreight gateway operators and emerging market airport authorities with constrained capital budgets. Implementation timelines for large cargo terminal automation projects routinely extend across 24 to 42 months, including site engineering, equipment manufacturing lead times, civil works, installation, commissioning, and operational ramp-up phases, generating extended payback timelines and capital deployment uncertainty for airport authorities planning gateway terminal automation rollouts within the airport cargo handling systems market. Site-specific engineering complexity remains substantial, with cargo terminal design requiring detailed cargo flow modeling, ULD throughput curve forecasting, peak surge sizing, future expansion provision, and integration with upstream airside cargo transfer infrastructure and downstream landside dispatch facilities unique to each terminal facility. The combined effect of capital intensity, extended commissioning timelines, and site-specific engineering complexity continues to constrain the pace at which airport authorities can scale cargo handling automation deployment across distributed gateway terminal networks.

Airport Slot Constraints, Landside Real Estate Scarcity, and Terminal Reconstruction Complexity in Brownfield Cargo Modernization Programs

Airport slot constraints, landside cargo terminal real estate scarcity at congested gateway airports, and the operational complexity of brownfield cargo terminal modernization while maintaining continuous freight processing operations generate substantial procurement and engineering challenges within the airport cargo handling systems market. Major cargo gateway airports including Hong Kong, Frankfurt, Amsterdam, London Heathrow, and Dubai face material constraints on incremental landside real estate available for cargo terminal expansion, requiring brownfield modernization programs that retrofit automated cargo handling systems within existing terminal building envelopes while maintaining uninterrupted commercial cargo operations. Brownfield cargo terminal modernization commissioning typically extends across multiple phased deployment cycles spanning 30 to 48 months, with operational continuity requirements constraining equipment installation timelines, requiring detailed phased changeover engineering, and generating elevated commissioning risk relative to greenfield terminal commissioning programs. Airport slot constraints affecting freighter aircraft operations and apron ground handling capacity additionally constrain the operational improvements achievable through cargo terminal automation, requiring integrated airside and landside planning that exceeds the scope of cargo handling systems integration alone and complicates total business case development for airport cargo handling systems procurement decisions across the airport cargo handling systems market.

Volatile Air Cargo Volume Cycles, Freighter Capacity Variability, and Belly Capacity Dependence Generating Demand Forecasting Complexity for Terminal Capacity Investment

The historically volatile air cargo volume cycle, sustained variability in dedicated freighter capacity deployment, and continued dependence on passenger aircraft belly cargo capacity for major airfreight trade lanes generate persistent demand forecasting complexity that constrains capital deployment decisions for airport cargo terminal automation programs and complicates business case validation within the airport cargo handling systems market. Air cargo volume cycles can fluctuate by 15% to 30% between peak and trough years on major trade lanes, with cycles driven by global trade dynamics, fuel price variability, geopolitical disruption, and underlying economic activity that resist accurate forward forecasting beyond 3-year planning horizons. Belly cargo capacity tied to passenger flight schedules adds substantial demand variability, with airline network restructuring, passenger demand fluctuations, and aircraft type rotations generating belly cargo capacity changes that propagate through cargo terminal throughput patterns. Cargo terminal capacity investments structured around peak-cycle throughput assumptions risk overbuilt capacity during cycle troughs, while capacity sized to trough demand generates capacity constraints during peak periods, creating sizing complexity that challenges procurement decision-making for airport authorities, integrator hub operators, and cargo airline operators evaluating airport cargo handling systems procurement strategies and capital deployment timing decisions.

Market Segmentation

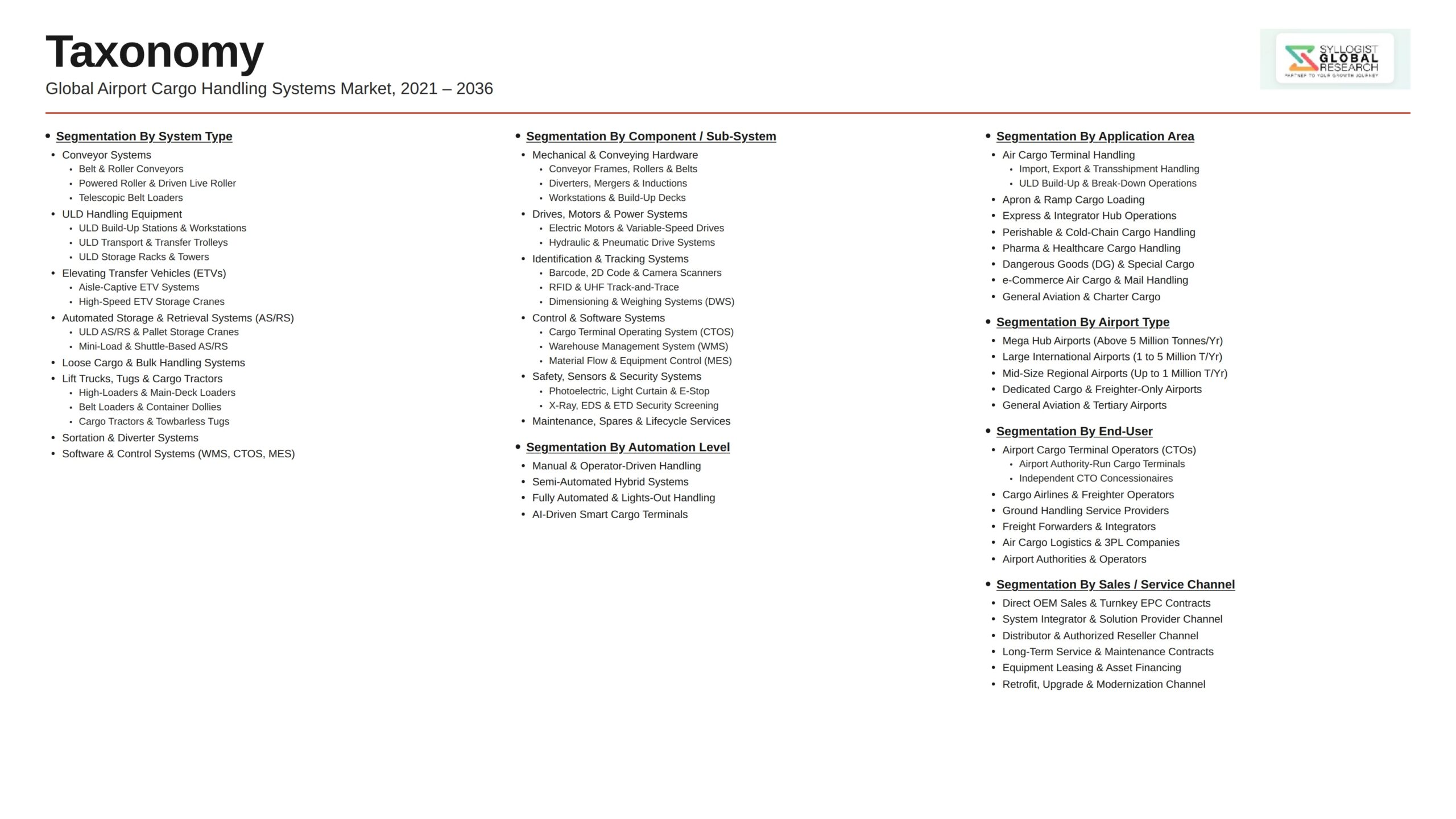

- Segmentation By System Type

- Conveyor and Roller-Bed Systems

- Automated Storage and Retrieval Systems (AS/RS)

- Unit Load Device (ULD) Handling Systems

- Elevating Transfer Vehicles (ETV)

- Automated Guided Vehicles (AGV)

- Robotic Build-Up and Break-Down Workstations

- Weighing and Dimensioning Systems

- Others

- Segmentation By Cargo Type

- General Cargo

- Perishable Cargo

- Pharmaceutical and Cold Chain Cargo

- Dangerous Goods and Hazardous Cargo

- Live Animal Cargo

- High-Value and Vulnerable Cargo

- Express and E-Commerce Cargo

- Mail and Postal Cargo

- Others

- Segmentation By Component

- Hardware (Mechanical and Electromechanical Equipment)

- Software (Warehouse Control and Cargo Management Systems)

- Services (Integration, Maintenance, Software Updates)

- Segmentation By Technology

- Manual and Semi-Automated Systems

- Fully Automated Systems

- Robotic and AI-Enabled Systems

- Segmentation By Application

- Cargo Terminal Operations

- Integrator Sortation Hubs

- Perishable Transit Centers

- Pharmaceutical Cold Chain Terminals

- E-Commerce Express Cargo Hubs

- Mail Processing Facilities

- Others

- Segmentation By Mode of Operation

- New Greenfield Cargo Terminals

- Brownfield Retrofit and Modernization

- Capacity Expansion Programs

- Segmentation By End User

- Cargo Airline Operators

- Integrator Express Cargo Operators

- Airport Authorities

- Ground Handling Service Providers

- Specialized Cargo Terminal Operators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Airport Cargo Handling Systems Market in 2025, projected through 2034, segmented by system type, cargo type, component, and application, enabling cargo handling system manufacturers, integrators, airport authorities, and aviation infrastructure investors to identify highest-growth segments and most durable revenue opportunities across the airport cargo handling systems landscape?

- How are airport authorities, cargo airline operators, integrator express cargo operators, and ground handling service providers structuring procurement frameworks for cargo terminal automation projects, and which operating models, including capital purchase, concession-based deployment, and integrator-led turnkey delivery, are shaping commercial deployment economics within the airport cargo handling systems market through 2034?

- What e-commerce volume growth, perishable airfreight recovery, and pharmaceutical cold chain airfreight expansion dynamics are shaping the pace and geographic distribution of cargo terminal automation procurement across mature and emerging airfreight gateway markets?

- Which cargo handling technologies, including automated storage and retrieval systems, ULD handling systems, AGV-based airside-to-terminal transfer fleets, and robotic ULD build-up workstations, are gaining the strongest procurement traction across general, perishable, pharmaceutical, and e-commerce cargo terminal applications, and what throughput, accuracy, and total cost of ownership metrics are shaping technology selection?

- How is the competitive landscape structured among cargo handling system original equipment manufacturers, conveyor and material handling integrators, ULD handling specialists, AGV developers, and end-to-end airport cargo terminal integrators within the airport cargo handling systems market, and what partnership, acquisition, and platform expansion strategies are enabling new entrants to compete against established cargo terminal infrastructure suppliers?

- What integrator hub expansion, regional cargo gateway commissioning, and brownfield cargo terminal modernization trends are reshaping cargo terminal automation procurement, equipment specification, and commissioning timelines across major airfreight gateway markets globally?

- Which regional markets, including Asia-Pacific, the Middle East, North America, and Europe, are projected to generate the largest incremental airport cargo handling systems procurement opportunities through 2034, and what airfreight volume, integrator hub activity, perishable trade flow, and infrastructure investment factors are shaping capability investment priorities and supplier selection decisions in each regional airport cargo handling systems market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Capital Intensity, Extended Commissioning Timeline & Site-Specific Engineering Complexity Risk

- Airport Slot Constraints, Landside Real Estate Scarcity & Brownfield Reconstruction Complexity Risk

- Air Cargo Volume Cycle Volatility, Belly Capacity Variability & Demand Forecasting Risk

- Cybersecurity Exposure, Sortation Control System Integrity & Customs System Interface Risk

- Perishable, Pharmaceutical Cargo Compliance, Temperature Integrity & GDP Liability Risk

- Regulatory Framework & Standards

- ICAO, IATA Cargo Handling Standards & Air Cargo Security Frameworks (Known Shipper, RA3, ACC3)

- Customs Pre-Clearance, Cross-Border Electronic Advance Data & Trade Documentation Standards

- Occupational Safety, Workplace Ergonomics & Robotic Cargo Handling Equipment Safety Standards (ISO 10218, ANSI/RIA R15.06)

- Good Distribution Practice (GDP), Pharmaceutical Cold Chain & Perishable Transit Compliance Standards

- Dangerous Goods (IATA DGR, ICAO Technical Instructions), Hazardous Materials & Cross-Border Air Cargo Compliance Frameworks

- Global Airport Cargo Handling Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Cargo Handling Capacity Installed in Million Tonnes per Year and Number of Active Cargo Terminal Facilities)

- Market Size & Forecast by System Type

- Conveyor and Roller-Bed Systems

- Automated Storage and Retrieval Systems (AS/RS)

- Unit Load Device (ULD) Handling Systems

- Elevating Transfer Vehicles (ETV)

- Automated Guided Vehicles (AGV)

- Robotic Build-Up and Break-Down Workstations

- Weighing and Dimensioning Systems

- Others

- Market Size & Forecast by Cargo Type

- General Cargo

- Perishable Cargo

- Pharmaceutical and Cold Chain Cargo

- Dangerous Goods and Hazardous Cargo

- Live Animal Cargo

- High-Value and Vulnerable Cargo

- Express and E-Commerce Cargo

- Mail and Postal Cargo

- Others

- Market Size & Forecast by Component

- Hardware (Mechanical and Electromechanical Equipment)

- Software (Warehouse Control and Cargo Management Systems)

- Services (Integration, Maintenance, Software Updates)

- Market Size & Forecast by Technology

- Manual and Semi-Automated Systems

- Fully Automated Systems

- Robotic and AI-Enabled Systems

- Market Size & Forecast by Application

- Cargo Terminal Operations

- Integrator Sortation Hubs

- Perishable Transit Centers

- Pharmaceutical Cold Chain Terminals

- E-Commerce Express Cargo Hubs

- Mail Processing Facilities

- Others

- Market Size & Forecast by Mode of Operation

- New Greenfield Cargo Terminals

- Brownfield Retrofit and Modernisation

- Capacity Expansion Programs

- Market Size & Forecast by End-User

- Cargo Airline Operators

- Integrator Express Cargo Operators

- Airport Authorities

- Ground Handling Service Providers

- Specialized Cargo Terminal Operators

- Others

- Market Size & Forecast by Sales Channel

- Engineering, Procurement & Construction (EPC) Turnkey Contracts

- Direct Equipment Supply with System Integration Contracts

- Public-Private Partnership (PPP), BOT & Concession Contracts

- Modular Scalable Equipment Procurement Channel

- Operations & Maintenance (O&M) Service Contracts

- North America Airport Cargo Handling Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Cargo Handling Capacity Installed in Million Tonnes per Year and Number of Active Cargo Terminal Facilities)

- By System Type

- By Cargo Type

- By Component

- By Technology

- By Application

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Airport Cargo Handling Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Cargo Handling Capacity Installed in Million Tonnes per Year and Number of Active Cargo Terminal Facilities)

- By System Type

- By Cargo Type

- By Component

- By Technology

- By Application

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Airport Cargo Handling Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Cargo Handling Capacity Installed in Million Tonnes per Year and Number of Active Cargo Terminal Facilities)

- By System Type

- By Cargo Type

- By Component

- By Technology

- By Application

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Airport Cargo Handling Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Cargo Handling Capacity Installed in Million Tonnes per Year and Number of Active Cargo Terminal Facilities)

- By System Type

- By Cargo Type

- By Component

- By Technology

- By Application

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Airport Cargo Handling Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Cargo Handling Capacity Installed in Million Tonnes per Year and Number of Active Cargo Terminal Facilities)

- By System Type

- By Cargo Type

- By Component

- By Technology

- By Application

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Airport Cargo Handling Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Cargo Handling Capacity Installed in Million Tonnes per Year and Number of Active Cargo Terminal Facilities)

- By System Type

- By Cargo Type

- By Component

- By Technology

- By Application

- By Mode of Operation

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Automated Storage and Retrieval System (AS/RS) & High-Rise ULD Storage Technology Deep-Dive

- Unit Load Device Handling, Build-Up and Break-Down Robotic Workstation Technology

- Automated Guided Vehicle (AGV) & Airside-to-Terminal Cargo Transfer Fleet Technology

- Elevating Transfer Vehicle (ETV) & Multi-Level Cargo Transfer Technology

- Six-Sided Machine Vision Dimensioning, AI Cargo Recognition & Revenue Weight Capture Technology

- Warehouse Control System (WCS) & Airline Cargo Management System Integration Technology

- Cold Chain ULD, Pharmaceutical Transit Infrastructure & Temperature-Controlled Cargo Handling Technology

- Patent & IP Landscape in Airport Cargo Handling Systems Technologies

- Value Chain & Supply Chain Analysis

- Conveyor, Roller-Bed & Cargo Sortation Hardware Manufacturing Supply Chain

- AS/RS, ULD Handling & Specialty Cargo Equipment Manufacturing Supply Chain

- AGV, ETV & Mobile Cargo Transfer Equipment Manufacturing Supply Chain

- Robotic Arm, Vision System & Sensor Component Supply Chain

- Warehouse Control Software, Cargo Management System & Customs Interface Software Supply Chain

- EPC Contractor, Project Developer & System Integrator Procurement Landscape

- Airport Authority, Cargo Airline, Integrator Operator Channel & Long-Term O&M Service

- Pricing Analysis

- Conveyor, Roller-Bed & Cargo Sortation Hardware Pricing Analysis Across Throughput Tiers

- AS/RS, High-Rise ULD Storage & Automated Storage System Pricing Analysis

- ULD Handling System & Robotic Build-Up/Break-Down Workstation Pricing Analysis

- AGV, ETV & Mobile Cargo Transfer Equipment Pricing Analysis

- Warehouse Control Software, Cargo Management System & Customs Interface Software Pricing

- Cargo Terminal Project Economics: Total Capital Cost per Million Tonnes Annual Throughput Capacity

- Operating Cost Analysis: Per-Tonne Cargo Handling Cost, Labour Reduction & Total Cost of Ownership Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Airport Cargo Handling Systems: Energy Consumption, Carbon Footprint & Material Use Across Technology Categories

- Energy Efficiency, Variable Frequency Drives & Cargo Terminal Decarbonisation Contribution

- End-of-Life Cargo Handling Equipment Recycling, Component Recovery & Circular Economy Performance

- Carbon Emissions Reduction Through Cargo Throughput Optimisation, Reduced Aircraft Ground Time & Fuel Savings

- Regulatory-Driven Sustainability, SDG 9 (Industry, Innovation and Infrastructure) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Application & Geography

- Player Classification

- Integrated Airport Cargo Handling System Original Equipment Manufacturers (OEMs)

- Conveyor and Material Handling System Integrators

- Unit Load Device Handling System Specialists

- AS/RS, High-Rise Storage & Automated Cargo Equipment Manufacturers

- Automated Guided Vehicle (AGV) & Elevating Transfer Vehicle (ETV) Manufacturers

- Robotic Build-Up and Break-Down Workstation Specialists

- Warehouse Control Software & Cargo Management System Providers

- End-to-End Airport Cargo Terminal Systems Integrators

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Airport Cargo Handling Products & Technology Portfolio

- Key Customer Relationships & Reference Cargo Terminal Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Airport Cargo Handling Systems Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Cargo Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)