Global Military Edge Computing Systems Market By Component, By Deployment, By Application, By Platform, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Military Edge Computing Systems Market encompasses the development, integration, procurement, and operational deployment of ruggedized hardware, embedded software platforms, and AI-enabled inference architectures designed to perform low-latency data processing, sensor fusion, autonomous decision support, and mission-critical analytics directly at the tactical edge across forward operating bases, dismounted soldier systems, manned and unmanned ground vehicles, combat aircraft, naval surface and subsurface platforms, satellite buses, and contested communications environments where reliance on centralized cloud infrastructure is impractical, denied, degraded, intermittent, or limited. The market includes ruggedized edge servers and micro data centers, GPU-accelerated tactical computing nodes, AI accelerator chips, embedded inference modules, secure software-defined radios, edge cybersecurity appliances, tactical 5G base stations, post-quantum cryptographic modules, and software platforms encompassing edge AI inference engines, autonomous mission management software, federated learning frameworks, secure container orchestration, and tactical cloud middleware engineered to deliver compute capability where bandwidth-constrained, latency-sensitive, and high-assurance defense workloads cannot wait for backhaul transmission. The market addresses critical operational requirements including real-time intelligence, surveillance, and reconnaissance processing, autonomous weapons system targeting, cybersecurity threat detection at network ingress, predictive maintenance for forward-deployed assets, multi-domain Joint All Domain Command and Control coordination, sensor-to-shooter timeline compression, and resilient operations under denied, degraded, intermittent, and limited communications conditions. End users span US Department of Defense services, NATO and Indo-Pacific allied militaries, intelligence agencies, special operations commands, homeland security organizations, and defense prime contractors integrating tactical edge architectures into next-generation platforms across land, air, maritime, space, and cyber operational domains, establishing military edge computing as a foundational technology layer underpinning modern joint multi-domain warfare capability worldwide.

Market Insights

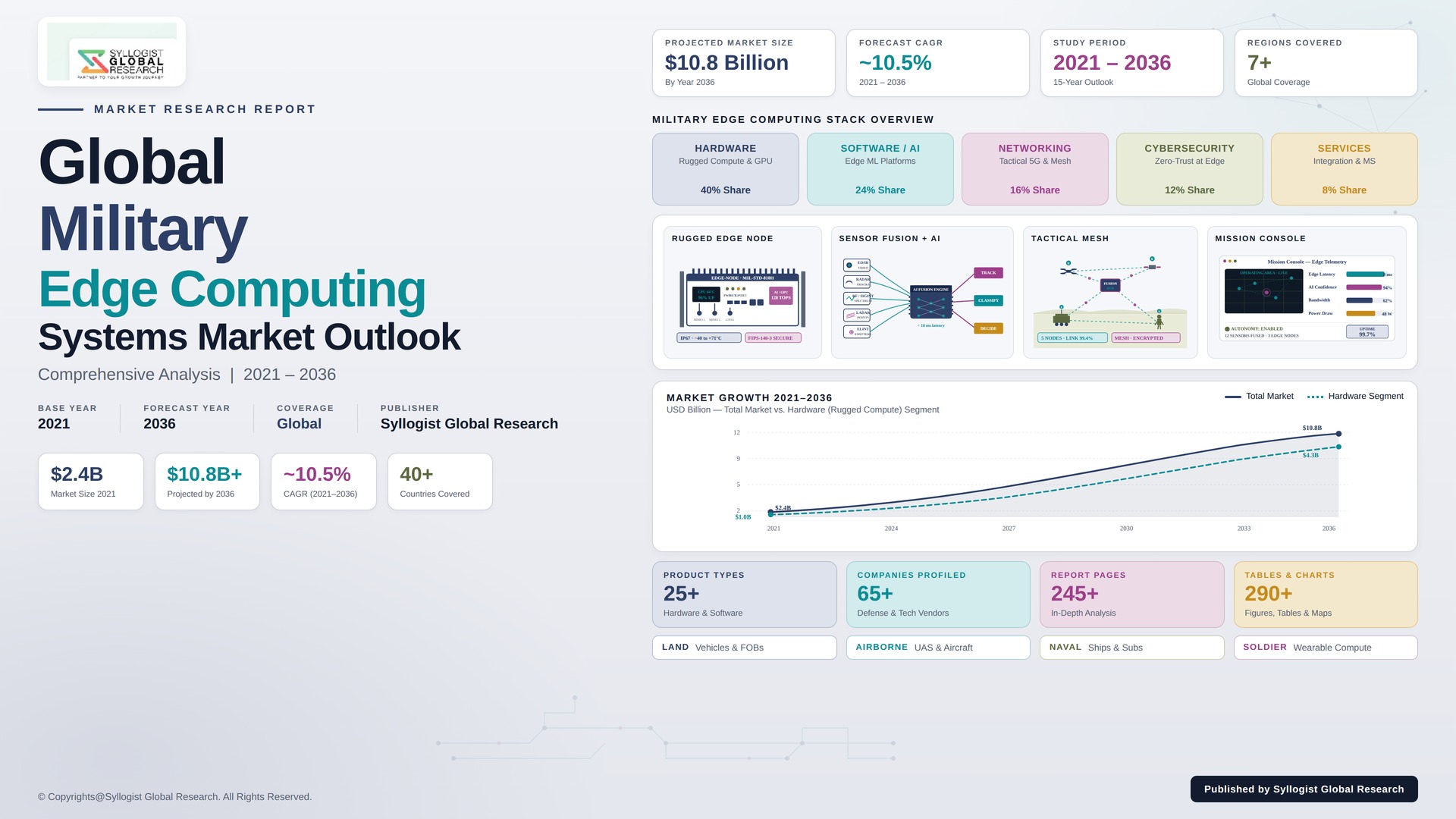

The global military edge computing systems market is moving through an unprecedented acceleration phase shaped by the operational imperatives of distributed warfare, contested electromagnetic environments, and AI-enabled autonomous decision-making at the tactical edge, where centralized cloud connectivity cannot reliably meet the latency, bandwidth, or survivability requirements of modern multi-domain combat operations. The market was valued at USD 3.3 billion in 2025 and is projected to reach USD 11.0 billion by 2034, advancing at a compound annual growth rate of 14.3% through the forecast window, supported by surging defense AI investment, accelerated operational lessons absorbed from Ukraine and Indo-Pacific posture environments, expanding Joint All Domain Command and Control program funding, and broadening adoption of ruggedized edge servers, GPU-accelerated tactical computing nodes, and AI inference accelerators across manned and unmanned platforms operating in denied and degraded communications environments worldwide.

Operational survivability is the strongest secular force restructuring the demand profile for military edge computing systems, as defense planners progressively recognize that adversary electronic warfare, cyber attacks, and anti-satellite capabilities can deny, degrade, or disrupt the centralized cloud connectivity historically underpinning data-driven military decision-making, compelling architectural redesign toward distributed compute resilience at the tactical edge. The result is a measurable shift in revenue mix from centralized data center investments toward ruggedized edge servers, embedded AI inference modules, tactical 5G base stations, edge cybersecurity appliances, and software-defined radio computing payloads engineered to operate autonomously through DDIL (denied, degraded, intermittent, limited) communications conditions. Defense procurement officers are simultaneously prioritizing modular open systems architecture compliance, post-quantum cryptography readiness, and seamless C4ISR interoperability, restructuring acquisition economics in favor of suppliers offering scalable, upgradable, and standards-compliant tactical edge computing technology stacks across heterogeneous mission environments globally.

Within the application taxonomy, command and control systems anchor the highest current revenue concentration, supported by sustained investment in JADC2, NATO Federated Mission Networking, and allied multi-domain command architectures requiring edge processing of fused sensor data into actionable course-of-action recommendations within decision timelines centralized cloud platforms cannot match. Intelligence, surveillance, and reconnaissance edge processing represents the fastest-growing application category, expanding at rates above 16% annually as autonomous unmanned aerial system, satellite, and ground sensor proliferation generates data volumes that exceed available backhaul bandwidth, forcing pre-processing, anomaly detection, and target classification onto the edge node itself. Cybersecurity edge appliances and predictive maintenance edge analytics are scaling rapidly across forward operating bases and forward-deployed platforms, while autonomous weapons targeting and human-machine teaming applications represent strategically critical emerging segments reshaping competitive differentiation among integrated military edge computing technology providers worldwide.

North America anchors the largest absolute revenue share of the global military edge computing systems market, valued near USD 1.4 billion in 2025 and underpinned by US Department of Defense JADC2 program funding, accelerating Replicator-aligned autonomous system procurement, sustained Defense Innovation Unit and DARPA edge AI investment, and a deep ecosystem of ruggedized computing OEMs, defense prime contractors, and dual-use AI software developers. Europe represents a structurally critical share driven by NATO multi-domain operations investments, conflict-driven tactical edge capability acceleration across Eastern European border states, and growing United Kingdom, France, and Germany sovereign defense AI programs. Asia-Pacific is positioned to record the highest forecast period CAGR, supported by India, Japan, South Korea, Australia, Taiwan, and Singapore investment programs responding to regional posture requirements, while the Middle East contributes incremental growth through Israel, Saudi Arabia, and United Arab Emirates tactical edge procurement. Latin America anchors regional demand through homeland security and counter-narcotics edge computing applications.

Key Drivers

Joint All Domain Command and Control Initiatives and Multi-Domain Operations Doctrine Driving Sustained Defense Investment in Tactical Edge Computing Architectures

Joint All Domain Command and Control program investment across the US Department of Defense, NATO Federated Mission Networking initiatives, and Indo-Pacific allied multi-domain command architectures is generating durable demand for tactical edge computing infrastructure capable of fusing sensor data, generating AI-enabled course-of-action recommendations, and synchronizing engagement decisions across joint air, land, maritime, space, and cyber domains within machine-speed decision timelines. Defense ministries are codifying edge computing capability requirements into multi-year procurement programs, anchoring long-cycle revenue visibility for ruggedized server, AI accelerator, and tactical software providers across the global defense industrial base.

Operational Lessons from Ukraine and Indo-Pacific Posture Environments Demonstrating Critical Need for Disconnected, Denied, and Degraded Communications Edge Resilience

Direct operational evidence from active conflict environments in Ukraine, the Black Sea, and Indo-Pacific posture exercises has demonstrated the indispensable role of distributed tactical edge computing in maintaining mission effectiveness when adversary electronic warfare, anti-satellite capabilities, and cyber attacks deny, degrade, or disrupt centralized cloud connectivity. Defense procurement urgency around DDIL-resilient computing architectures is driving compressed acquisition timelines, rapid fielding contracts, and elevated edge computing allocation within force protection, ISR, autonomous systems, and forward operating base equipping budgets across NATO, Indo-Pacific, and Middle East allied procurement programs globally throughout the forecast horizon.

Proliferation of Autonomous Unmanned Systems and AI-Enabled Sensor Networks Generating Massive Data Volumes Requiring Onboard Edge Inference Processing

The accelerating proliferation of autonomous unmanned aerial systems, autonomous ground vehicles, autonomous maritime surface and subsurface platforms, and distributed sensor networks is generating sensor data volumes that exceed available tactical backhaul bandwidth, compelling defense system designers to integrate onboard AI inference, autonomous mission management, and edge data pre-processing capability directly into platform architectures. This shift is anchoring durable demand for compact, ruggedized, low-power AI accelerator chips, embedded GPU modules, and autonomous mission software supporting persistent autonomous operations across contested operational environments worldwide throughout the forecast period.

Key Challenges

Size, Weight, Power, and Cost Constraints at the Tactical Edge Limiting Computational Density Available for Deployed Military Edge Computing Platforms

Stringent size, weight, power, and cost (SWaP-C) constraints across dismounted soldier kit, unmanned aerial system payloads, satellite buses, and forward-deployed vehicle platforms impose material limitations on the computational density, AI accelerator capacity, and thermal management envelope available for tactical edge computing deployment, creating a persistent gap between AI workload performance demands and edge platform delivery capability. Suppliers must continuously invest in low-power AI accelerator architectures, advanced packaging technologies, and energy-efficient inference engines to keep pace with expanding mission workload requirements across the diverse spectrum of tactical edge deployment scenarios globally.

Adversarial Cyber Threats, Edge Node Attack Surface Expansion, and Supply Chain Security Risks Across Distributed Military Edge Computing Architectures

Distributed military edge computing architectures by design expand the cybersecurity attack surface available to sophisticated state-level adversaries seeking to compromise mission-critical computing nodes through communications link exploitation, edge device firmware infiltration, AI model poisoning, and supply chain interdiction of computing hardware, accelerator chips, and embedded software components. Defense edge computing programs face sustained pressure to certify trusted computing supply chains, validate post-quantum cryptographic readiness, and mandate adversarial AI robustness testing, increasing program timelines, certification costs, and lifecycle sustainment burdens across deployed tactical edge systems globally throughout the forecast horizon.

Data Classification Complexity, Multi-Level Security Architecture Requirements, and Allied Interoperability Constraints Across Multinational Defense Edge Programs

Multi-level security architecture requirements, data classification handling complexity, and allied interoperability constraints across multinational defense edge programs introduce significant integration challenges that elevate program timelines, cross-domain solution certification burdens, and total cost of ownership across deployed tactical edge computing systems. Procurement agencies face persistent challenges harmonizing cross-classification data handling protocols, NATO and bilateral allied interoperability standards, and federal-level cybersecurity authorization frameworks, while program export control restrictions further complicate multinational coalition tactical edge architecture deployment across global defense procurement programs throughout the forecast period.

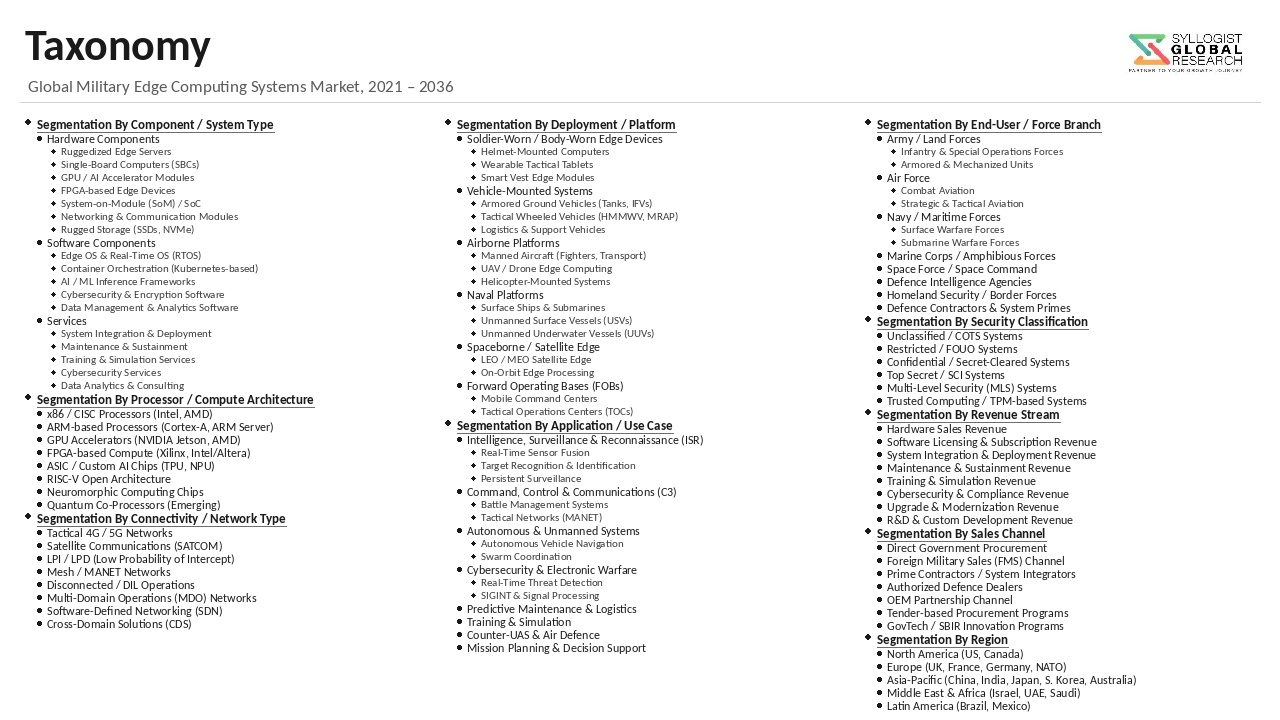

Market Segmentation

- Segmentation By Component

- Hardware – Ruggedized Edge Servers and Micro Data Centers

- Hardware – Embedded Computing Modules and AI Accelerator Chips

- Hardware – Edge Sensors and Tactical Networking Devices

- Software – Edge AI Inference and Autonomous Mission Management

- Software – Tactical Cloud Middleware and Container Orchestration

- Software – Edge Cybersecurity and Cryptographic Platforms

- Services – Integration, Sustainment, and Managed Services

- Others

- Segmentation By Deployment

- On-Premises (Forward Operating Base, Tactical Operations Center)

- Mobile and Vehicle-Mounted

- Hybrid Edge-Cloud

- Disconnected and Air-Gapped

- Segmentation By Application

- Command, Control, Communications, and Computers (C4)

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Cybersecurity and Electronic Warfare

- Autonomous Systems and Unmanned Platform Operations

- Predictive Maintenance and Logistics

- Targeting and Fire Control

- Battlefield Communications and Tactical Networking

- Others

- Segmentation By Platform

- Land – Combat Vehicles, Dismounted Soldier, Forward Operating Base

- Airborne – Manned Aircraft, Unmanned Aerial Systems, Loitering Munitions

- Naval – Surface Ships, Submarines, Unmanned Maritime Platforms

- Space – Satellites and On-Orbit Edge Processing

- Cyber and Electronic Warfare Platforms

- Others

- Segmentation By End User

- Army and Land Forces

- Air Force and Aerospace Commands

- Naval and Maritime Forces

- Space Force and Space Operations Commands

- Special Operations Commands

- Intelligence Agencies

- Homeland Security and Border Defense Organizations

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Military Edge Computing Systems Market in 2025, projected through 2034, disaggregated by component, deployment, and application, enabling defense contractors, ruggedized computing OEMs, AI software developers, and investors to identify highest-growth segments and most durable revenue opportunities across the global tactical edge computing landscape?

- How are Joint All Domain Command and Control programs, NATO Federated Mission Networking, and Indo-Pacific allied multi-domain operations doctrine reshaping demand requirements for ruggedized edge servers, AI accelerator chips, and tactical cloud software architectures, and which national programs are setting the benchmarks shaping global military edge computing demand architecture through 2034?

- How are operational lessons from Ukraine, the Black Sea, and Indo-Pacific posture environments reshaping tactical edge computing technology requirements, denied-degraded-intermittent-limited communications resilience doctrine, and procurement priorities across military, intelligence, and homeland security programs globally?

- Which military edge computing application categories, including command and control, ISR, cybersecurity, autonomous systems, predictive maintenance, and targeting, are recording the highest forecast period growth rates, and what threat environment, sensor proliferation, and AI workload factors are shaping demand intensity within each segment?

- How are size, weight, power, and cost constraints across dismounted soldier kit, unmanned aerial system payloads, satellite buses, and combat vehicle platforms shaping the trajectory of low-power AI accelerator development, advanced packaging technologies, and energy-efficient edge inference architectures across global defense markets?

- What partnership, acquisition, dual-use technology integration, and Tier 1 systems integrator strategies are dominant military edge computing providers using to consolidate market positions, secure trusted computing supply chains, and deepen long-cycle relationships with defense ministries and prime contractors across global regions?

- Which regional markets, specifically Asia-Pacific, the Middle East, and Eastern Europe, are expected to generate the most substantial incremental military edge computing procurement through 2034, and what geopolitical, threat environment, and defense modernization factors are driving capability investment priorities and supplier selection decisions across each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Cybersecurity, Supply Chain Compromise, Firmware & Side-Channel Attack Risk

- Defence Procurement Cycle, Budget Volatility & Programme Delay Risk

- Disconnected, Denied, Intermittent and Limited (DDIL) Environment Reliability Risk

- Critical Semiconductor & Strategic Material (Rare Earth, Gallium, Germanium) Supply Risk

- Export Control (ITAR, EAR, Wassenaar) and Quantum Computing Threat to Encryption Risk

- Regulatory Framework & Standards

- DoD Risk Management Framework (RMF), NIST 800-53, NIST 800-171 & DoDI 8500.01 Cybersecurity Standards

- Cybersecurity Maturity Model Certification (CMMC) & Defence Industrial Base Compliance Standards

- MIL-STD-810, MIL-STD-461 and MIL-STD-1275 Defence Environmental, EMI/EMC and Vehicle Power Standards

- SOSA (Sensor Open Systems Architecture), MOSA (Modular Open Systems Approach) & JADC2 Open Standards

- ITAR, EAR, Wassenaar Export Controls & NSA Type 1 / Type 2 Cryptographic Approval Standards

- Global Military Edge Computing Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Component

- Hardware (Rugged Servers, Edge Gateways, VPX/OpenVPX/SOSA Modules & Storage)

- AI/ML Accelerators (GPUs, Tensor Processors, FPGAs & Neuromorphic)

- Networking & Communication Hardware (Tactical Routers, SDN Appliances & Rugged Switches)

- Software & Operating System (RTOS, Hardened Linux & Container Orchestration)

- Cybersecurity Software (Zero Trust, Encryption & Endpoint Protection)

- Services (Integration, Sustainment, Training & Managed DevSecOps)

- Market Size & Forecast by Platform

- Soldier-Mounted, Wearable & Man-Portable

- Ground Vehicle & Tactical Vehicle Mounted

- Airborne (Manned Aircraft, UAV & Helicopter)

- Naval (Surface Ship & Submarine)

- Forward Operating Base & Tactical Operations Centre

- Space-Based & Low Earth Orbit (LEO) Edge

- Fixed Site, Bunker & Hardened Facility

- Market Size & Forecast by Deployment Type

- Tactical Edge (Forward, Contested & DDIL Environment)

- Operational Edge (Theatre Headquarters & Regional Command)

- Strategic Edge (CONUS, Fixed Site & Hardened Facility)

- Mobile Edge (Vehicle & Airborne Platforms)

- Disconnected & Autonomous Edge Node

- Market Size & Forecast by Application

- Intelligence, Surveillance & Reconnaissance (ISR)

- C4I, C5ISR & Joint All-Domain Command and Control (JADC2)

- Electronic Warfare, SIGINT & Signal Processing

- Targeting, Fire Control & Precision Strike

- Autonomous Systems, Robotics & Unmanned Platform Control

- Cyber Operations & Cyber Defence

- Logistics, Predictive Maintenance & Mission Sustainment

- Soldier Systems, Wearable Computing & Augmented Reality

- Mission Planning, Battle Management & Common Operating Picture

- AI/ML Inference & Real-Time Sensor Fusion at the Edge

- Market Size & Forecast by Workload Technology

- AI/ML Inference & Computer Vision Workloads

- Sensor Fusion, Multi-Domain Data Processing & Real-Time Analytics

- Cybersecurity, Zero Trust & Quantum-Safe Cryptography Workloads

- 5G Tactical Network, Software-Defined Radio & Communication Workloads

- Market Size & Forecast by End-User

- Army & Land Forces

- Navy & Coast Guard

- Air Force

- Marine Corps

- Special Operations Forces (SOF)

- Space Force & Space Command

- Intelligence Agencies

- Coalition & Allied Defence Forces

- Market Size & Forecast by Sales Channel

- Direct Defence Procurement & Government Contract (FMS, DCS & National Tender)

- Prime Contractor & System Integrator Channel

- Distributor, Authorised Reseller & Regional Partner Channel

- Sustainment, Lifecycle Support & Performance-Based Logistics Programme

- North America Military Edge Computing Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Component

- By Platform

- By Deployment Type

- By Application

- By Workload Technology

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Military Edge Computing Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Component

- By Platform

- By Deployment Type

- By Application

- By Workload Technology

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Military Edge Computing Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Component

- By Platform

- By Deployment Type

- By Application

- By Workload Technology

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Military Edge Computing Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Component

- By Platform

- By Deployment Type

- By Application

- By Workload Technology

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Military Edge Computing Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Component

- By Platform

- By Deployment Type

- By Application

- By Workload Technology

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Military Edge Computing Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Component

- By Platform

- By Deployment Type

- By Application

- By Workload Technology

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Italy, Spain, Netherlands, Sweden, Norway, Poland, Ukraine, Russia, Turkey, China, Japan, India, South Korea, Australia, Singapore, Taiwan, Indonesia, Brazil, Mexico, Argentina, Saudi Arabia, UAE, Israel, Egypt, South Africa

- Technology Landscape & Innovation Analysis

- AI/ML Inference Acceleration, Tactical GPU & Neuromorphic Computing Technology Deep-Dive

- SOSA & MOSA Aligned VPX Module, Embedded Compute Card & Open Architecture Technology

- Tactical 5G, Software-Defined Radio & Multi-Domain Communications Edge Technology

- Rugged Containerization, Kubernetes at the Edge & DevSecOps Pipeline Technology

- Zero Trust Architecture, Multi-Level Security & Quantum-Resistant Cryptography Technology

- Heterogeneous Computing (CPU, GPU, FPGA & DSP) and Power-Efficient Tactical Compute Technology

- Disconnected Cloud, Mobile Data Centre & Tactical AWS Snowblade / Azure Stack Edge Technology

- Patent & IP Landscape in Military Edge Computing Technologies

- Value Chain & Supply Chain Analysis

- Semiconductor (CPU, GPU, FPGA, ASIC) & Critical Component Supply Chain for Defence-Grade Compute

- Rugged Chassis, VPX/OpenVPX Backplane & Modular Hardware Manufacturing Supply Chain

- Embedded Software, RTOS, Cybersecurity Software & AI Model Development Supply Chain

- Tier-1 Edge Compute System Integrator & Defence Prime Programme Landscape

- Defence Operator, Combatant Command & Coalition Partner Procurement Landscape

- Distributor, Authorised Reseller & Regional Defence Channel

- Lifecycle Support, Sustainment, Cybersecurity Patching & Mission Software Update

- Pricing Analysis

- Tactical Edge Server & Rugged Compute Node Average Selling Price and Cost per Node Analysis

- AI/ML Accelerator & Edge Inference Card Pricing Analysis

- Tactical Networking, SDN Appliance & 5G Tactical Radio Pricing Analysis

- Cybersecurity, Zero Trust Software & Edge Security Subscription Pricing Analysis

- Long-Term Defence Contract, IDIQ & Performance-Based Logistics Pricing Analysis

- Total Military Edge Computing Programme Economics: Cost per Node and Mission Effectiveness Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Military Edge Computing Systems: Energy Intensity, Material Footprint & Critical Mineral Intensity Across Architecture Routes

- Power-Efficient Tactical Compute & Pathway to Low-Power, Heat-Tolerant and Thermally Optimised Edge Portfolios

- End-of-Life Hardware Recovery, Critical Material Reclamation and Closed-Loop Material Management for Defence Systems

- Environmental Compliance, Hazardous Material & Battery Disposal Consideration in Defence Manufacturing and Operations

- Regulatory-Driven Sustainability, Defence Decarbonisation Alignment & ESG Disclosure for Defence Programmes

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Component & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Component, Application & Geography

- Player Classification

- Tier-1 Defence Prime Contractors with Integrated Edge Computing Portfolios

- Specialty Rugged Compute & Embedded System Manufacturers (VPX & SOSA-Aligned)

- Defence-Adjacent Hyperscale Cloud Providers (Tactical Cloud & Edge Solutions)

- AI/ML, Mission Software & Battle Management Platform Providers

- Tactical Networking, 5G & SDN Specialists

- Cybersecurity, Zero Trust & Cryptographic Module Specialists

- Semiconductor & AI Accelerator Specialists Integrating into Defence Edge Solutions

- Distributors, Authorised Resellers & Sustainment Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Component, Application & Region

- Company Profile

- Company Overview & Headquarters

- Military Edge Computing Products & Technology Portfolio

- Key Customer Relationships & Reference Programme Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Military Edge Computing Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (System Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Component, Platform, Deployment Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)