Global Space Economy & Satellite Constellation Infrastructure Market By Sector, By Constellation Type, By Application, By Infrastructure Component, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Space Economy and Satellite Constellation Infrastructure Market encompasses the complete economic value chain extending from upstream satellite manufacturing, launch vehicle production, ground equipment, and propulsion systems, through midstream satellite operations, orbital services, and constellation network management, to downstream space-enabled services spanning satellite broadband, Earth observation, position-navigation-timing (PNT), defense and intelligence communications, scientific research, and emerging in-orbit servicing, assembly, and manufacturing applications across commercial, civil, and government end-user environments globally. The market includes integrated satellite buses, propulsion subsystems, payloads, optical and radio frequency inter-satellite links, mission ground segments, telemetry tracking and command stations, user terminals, launch vehicles spanning small, medium, and heavy lift configurations, reusable booster systems, ride-share dispenser hardware, space situational awareness sensors, and digital orchestration platforms encompassing flight dynamics software, constellation management systems, mission planning tools, and AI-enabled satellite tasking applications. The market addresses critical operational requirements including LEO mega-constellation deployment scaling to thousands of satellites, defense space architecture resilience under contested orbital environments, sustainable orbital traffic coordination, multi-orbit network interoperability, sovereign launch capability development, and seamless integration of space-derived data across terrestrial telecommunications, geospatial intelligence, climate monitoring, agriculture, finance, transportation, and critical infrastructure protection workflows. End users span national space agencies, military and intelligence services, commercial constellation operators, telecommunications providers, geospatial data and analytics firms, scientific research institutions, and an expanding base of enterprise customers leveraging space-enabled connectivity, imagery, and PNT services, establishing space economy infrastructure as a foundational technology layer underpinning modern global communications, security, and economic activity worldwide.

Market Insights

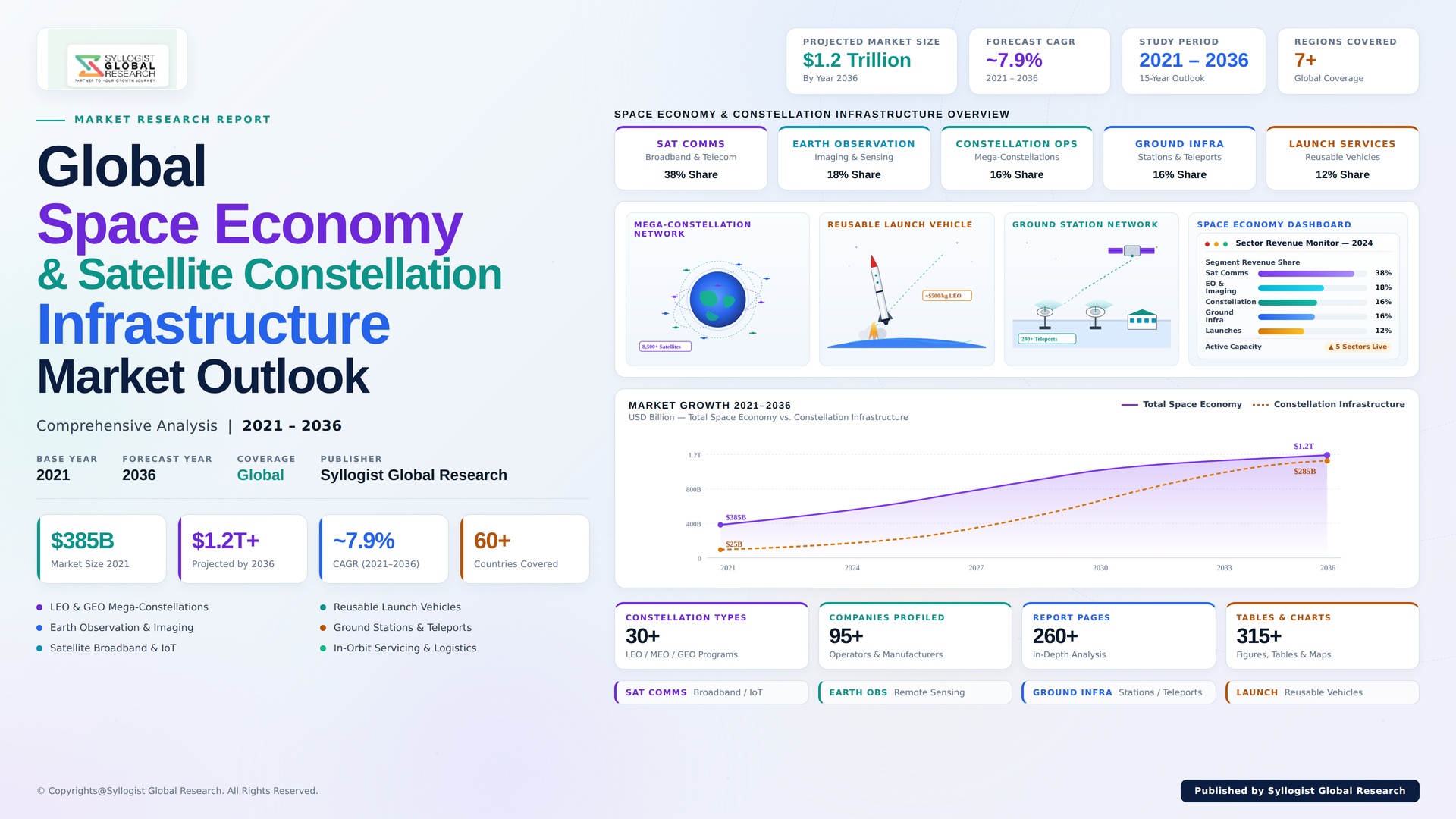

The global space economy and satellite constellation infrastructure market is moving through a transformational growth cycle shaped by the intersection of LEO mega-constellation industrialization, accelerating defense space modernization, dramatically falling launch costs enabled by reusable launch vehicles, and the progressive softwarization of orbital infrastructure that is fundamentally restructuring the economics of satellite operations across commercial, civil, and military mission categories worldwide. The market was valued at USD 630 billion in 2025 and is projected to reach USD 1.05 trillion by 2034, advancing at a compound annual growth rate of 5.9% through the forecast window, supported by Starlink, Project Kuiper, OneWeb, China Guowang, and IRIS2 broadband constellation buildouts, surging US Space Force and allied defense space spending, accelerating Earth observation satellite proliferation, and rapidly expanding commercial space-enabled services penetrating telecommunications, agriculture, finance, logistics, and critical infrastructure protection workflows globally throughout the forecast horizon.

Mega-constellation industrialization is the strongest secular force restructuring the demand profile for space economy infrastructure, as commercial operators, defense agencies, and sovereign national programs progressively recognize that distributed proliferated LEO architectures deliver superior latency, resilience, throughput, and cost economics compared to legacy bespoke geostationary satellite deployments, compelling architectural redesign of global satellite communications, Earth observation, and missile warning networks toward fleet-scale serial production paradigms. The result is a measurable shift in revenue mix from individual satellite buildouts toward integrated constellation network deployment, restructuring procurement economics in favor of suppliers offering vertically integrated satellite manufacturing, launch services, optical inter-satellite link integration, ground network operations, and managed downstream service capability. Reusable launch vehicle providers are concurrently driving launch cost reductions of 70% to 90% compared to expendable benchmarks, fundamentally altering business case viability for previously uneconomic space applications across commercial Earth observation, in-orbit servicing, and emerging space-based data processing markets globally.

Within the sector taxonomy, downstream space-enabled services anchor the highest current revenue concentration, supported by satellite broadband subscription growth, Earth observation data analytics demand, and PNT services penetration across consumer, enterprise, and government workflows. Upstream activities, including satellite manufacturing and launch services, represent the highest-engineering-content sector with revenue concentration estimated near 31% of total market activity in 2025, while midstream operations are recording the steepest growth trajectories, expanding above 8% annually as orbital services, in-orbit refueling, satellite life extension, active debris removal, and emerging in-space manufacturing applications scale commercially. LEO constellations dominate the constellation type taxonomy with approximately 92% of operational satellites in 2025, while GEO and MEO architectures retain critical roles in PNT, broadcast, and defense communications. Reusable launch vehicles, optical inter-satellite links, software-defined payloads, and AI-enabled constellation management platforms are reshaping competitive differentiation across integrated space economy infrastructure providers worldwide throughout the forecast period.

North America anchors the largest absolute revenue share of the global space economy and satellite constellation infrastructure market, valued near USD 285 billion in 2025 and underpinned by SpaceX Starlink commercial dominance, US Space Force Proliferated Warfighter Space Architecture procurement, NASA Artemis program funding, an unmatched ecosystem of commercial space startups, and vertically integrated launch, satellite manufacturing, and ground network capacity. Europe represents a structurally critical share driven by IRIS2 sovereign constellation development, Galileo and Copernicus civil program continuity, accelerating defense space investment, and growing United Kingdom, France, Italy, and Germany commercial space company emergence. Asia-Pacific is positioned to record one of the highest forecast period growth rates, supported by China Guowang and SatNet mega-constellation programs, expanding India ISRO commercial activity, accelerating Japan JAXA and South Korea KARI space economy initiatives, and ambitious Australian sovereign space investment. The Middle East contributes through United Arab Emirates and Saudi Arabia space program expansion, while Latin America anchors regional growth through Brazilian and Argentine commercial satellite activity and emerging geospatial intelligence applications.

Key Drivers

LEO Mega-Constellation Buildout and Proliferated Satellite Network Deployment Driving Industrial-Scale Demand Across Satellite Manufacturing, Launch, and Ground Infrastructure Value Chains

Accelerating LEO mega-constellation buildout across Starlink, Project Kuiper, OneWeb, China Guowang, SatNet, and the European Union IRIS2 sovereign constellation is generating industrial-scale demand spanning satellite manufacturing, launch services, optical inter-satellite link terminals, user terminals, ground station networks, and constellation management software platforms. Operators are codifying multi-thousand-satellite deployment commitments into long-cycle procurement programs, anchoring multi-decade demand visibility for vertically integrated space economy infrastructure providers across global commercial supply chains throughout the forecast horizon and beyond.

Defense Space Architecture Modernization, Sovereign Space Capability Investment, and Allied Military Space Program Expansion Anchoring Premium Demand for Resilient Constellation Infrastructure

Substantial defense investment across the US Space Force Proliferated Warfighter Space Architecture, Space Development Agency Tranche programs, NATO allied military space initiatives, and Indo-Pacific partner sovereign space capability programs is anchoring premium demand for resilient, jamming-resistant, distributed constellation infrastructure encompassing missile warning, tracking, secure communications, and space domain awareness applications. Combined US, China, European, Japanese, Indian, and Australian defense space spending exceeded USD 95 billion in 2025, anchoring durable revenue trajectories for defense space contractors and dual-use technology providers across global allied procurement programs throughout the forecast horizon globally.

Reusable Launch Vehicle Revolution and Dramatic Launch Cost Reductions Unlocking Previously Uneconomic Commercial Space Applications and Service Markets

The reusable launch vehicle revolution led by SpaceX Falcon 9, Falcon Heavy, Starship, Blue Origin New Glenn, Rocket Lab Neutron, and emerging Chinese reusable launch programs is delivering 70% to 90% launch cost reductions compared to expendable benchmarks, fundamentally altering commercial business case viability across satellite broadband, Earth observation, in-orbit servicing, space-based data processing, and emerging space manufacturing applications. Falling launch costs, combined with rising annual launch cadence and ride-share standardization, are unlocking previously uneconomic mission profiles, anchoring sustained demand for satellite manufacturing, ground services, and downstream applications across global commercial space markets.

Key Challenges

Orbital Debris Proliferation, Space Traffic Management Complexity, and Sustainability Constraints Across Increasingly Congested LEO Operating Environments

Orbital debris proliferation across increasingly congested LEO operating environments, combined with multiplying mega-constellation deployment, is creating material space traffic management complexity, conjunction risk burden, and regulatory pressure for active debris removal, satellite end-of-life disposal compliance, and orbital sustainability frameworks across global space markets. Constellation operators face mounting collision avoidance maneuver burdens, insurance complexity, and emerging regulatory requirements that elevate operational cost structures, while the long-term Kessler syndrome risk threatens the viability of certain LEO orbital shells, creating strategic uncertainty across long-cycle constellation infrastructure investment programs globally throughout the forecast period.

Radio Frequency Spectrum Congestion, International Coordination Delays, and Cross-Border Regulatory Fragmentation Across Multi-Jurisdictional Constellation Deployments

Persistent radio frequency spectrum congestion across Ka, Ku, V, and emerging higher-band allocations, combined with International Telecommunication Union coordination delays, national licensing fragmentation, and competing constellation filing priorities, is creating regulatory friction that complicates multi-jurisdictional constellation deployment timelines, frequency assignment economics, and cross-border service market access. Operators face persistent challenges navigating evolving sovereign spectrum frameworks, market access restrictions, and harmonization gaps between national regulatory bodies, while geopolitical fragmentation around export controls and technology transfer further elevates program complexity across global space economy infrastructure deployments throughout the forecast horizon.

Capital Intensity, Long Payback Horizons, and Persistent Profitability Path Uncertainty Across Mega-Constellation and Emerging Space Economy Business Models

Mega-constellation deployment, advanced launch system development, and emerging space economy business models including in-orbit servicing, space-based data processing, and lunar economy applications continue to face significant capital intensity, multi-year deployment timelines, long payback horizons, and persistent profitability path uncertainty across both commercial and dual-use ventures. Investors face ongoing challenges valuing pre-revenue and revenue-ramping space ventures, while operators must navigate sustained negative cash flow phases, competitive consolidation pressure, and customer adoption timing risk before reaching scale economics across commercial space markets globally throughout the forecast period.

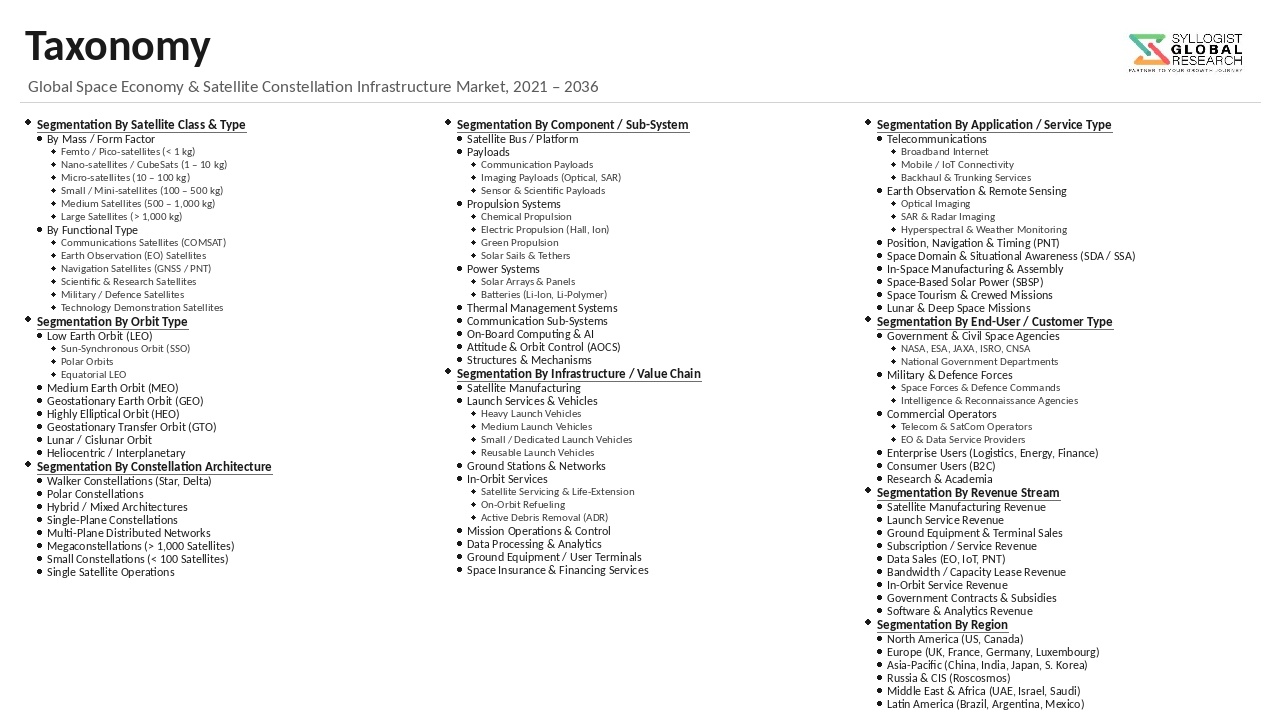

Market Segmentation

- Segmentation By Sector

- Upstream (Satellite Manufacturing, Launch Services, Ground Equipment)

- Midstream (Satellite Operations, In-Orbit Services)

- Downstream (Space-Enabled Services and Applications)

- Segmentation By Constellation Type

- LEO Mega-Constellations

- LEO Small Constellations

- Medium Earth Orbit (MEO) Constellations

- Geostationary (GEO) Single-Satellite and Cluster

- High Elliptical Orbit (HEO) and Cislunar

- Hybrid Multi-Orbit Architectures

- Segmentation By Application

- Satellite Broadband and Communications

- Earth Observation and Remote Sensing

- Position, Navigation, and Timing (PNT)

- Defense, Intelligence, and Space Domain Awareness

- Scientific Research and Deep Space Exploration

- In-Orbit Servicing, Assembly, and Manufacturing (ISAM)

- Direct-to-Device and IoT Connectivity

- Space Situational Awareness

- Others

- Segmentation By Infrastructure Component

- Satellite Buses and Payloads

- Launch Vehicles and Reusable Booster Systems

- Ground Stations and Tracking, Telemetry, Command (TT&C)

- User Terminals and Antennas

- Inter-Satellite Links (Optical and RF)

- Constellation Management and Mission Software

- Space Situational Awareness Sensors

- Others

- Segmentation By End User

- Government and Defense

- Civil Space Agencies

- Commercial Constellation Operators

- Telecommunications and Broadband Providers

- Earth Observation and Geospatial Data Providers

- Scientific Research Institutions

- Enterprise and Industrial Users

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Space Economy and Satellite Constellation Infrastructure Market in 2025, projected through 2034, disaggregated by sector, constellation type, and application, enabling satellite operators, defense contractors, launch service providers, infrastructure investors, and policymakers to identify highest-growth segments and most durable revenue opportunities across the global space economy landscape?

- How are LEO mega-constellation programs including Starlink, Project Kuiper, OneWeb, China Guowang, SatNet, and the European Union IRIS2 sovereign constellation reshaping demand requirements across satellite manufacturing, launch services, ground infrastructure, and downstream services value chains, and which constellation buildout schedules are setting the technical and procurement benchmarks defining global space economy demand architecture through 2034?

- How are US Space Force Proliferated Warfighter Space Architecture programs, Space Development Agency Tranche initiatives, NATO allied military space modernization, and Indo-Pacific sovereign space capability investments reshaping defense space infrastructure demand, resilient architecture requirements, and dual-use technology integration across global allied space markets?

- Which space economy sector and application categories, including satellite broadband, Earth observation, PNT, in-orbit servicing, direct-to-device, and space domain awareness, are recording the highest forecast period growth rates, and what business model, capital deployment, and customer adoption factors are shaping demand intensity within each segment?

- How are reusable launch vehicle commercialization, dramatic launch cost reductions, and rising annual orbital launch cadence reshaping commercial business case viability for previously uneconomic space applications, and which launch service providers and ride-share architectures are setting the cost benchmarks defining global space access economics through the forecast horizon?

- What partnership, vertical integration, sovereign infrastructure, and acquisition strategies are dominant space economy participants using to consolidate market positions, secure spectrum and orbital slot priority, and deepen long-cycle relationships with mega-constellation operators, defense agencies, civil space programs, and enterprise downstream customers across global regions?

- How are orbital debris mitigation requirements, space traffic management frameworks, radio frequency spectrum coordination challenges, and emerging international sustainability rules shaping mega-constellation deployment economics, operational risk profiles, and long-term capacity availability across LEO orbital shells through the forecast horizon globally?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Orbital Debris, Kessler Syndrome & Long-Term Space Sustainability Risk

- Spectrum Coordination, Interference & ITU Filing Conflict Risk

- Constellation Operator Bankruptcy, Launch Failure & Insurance Loss Risk

- Geopolitical, Sanctions, Export Control (ITAR, EAR) and Dual-Use Weaponisation Risk

- Critical Mineral, Semiconductor & Specialty Component Supply Chain Risk

- Regulatory Framework & Standards

- Outer Space Treaty 1967, Liability and Registration Conventions & UN COPUOS Long-Term Sustainability Guidelines

- ITU Spectrum Coordination, FCC Part 25 & National Satellite Licensing Frameworks

- FAA Part 450 Commercial Launch and Re-entry Licensing & National Spaceport Operations Standards

- IADC Debris Mitigation Guidelines, FCC 5-Year De-orbit Rule & ESA Zero Debris Charter

- ITAR Category XV, EAR Commerce Control List, Wassenaar Export Controls & Dual-Use Compliance Standards

- Global Space Economy and Satellite Constellation Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Satellites & Ground Stations)

- Market Size & Forecast by Infrastructure Segment

- Satellite Manufacturing & Subsystems

- Launch Vehicle, Spaceport & Launch Services

- Satellite Constellation Operations & In-Orbit Assets

- Ground Station, Teleport & Network Operations Centre

- User Terminal, Antenna & Direct-to-Cell Device

- In-Space Servicing, Assembly, Manufacturing (ISAM) & Active Debris Removal

- Space Situational Awareness (SSA), Space Traffic Management & Cybersecurity

- Mission Operations, Data Analytics & Cloud Distribution Software

- Hosted Payload, Constellation as a Service & Spectrum Lease

- Market Size & Forecast by Constellation Application

- Broadband Communications & Connectivity Constellations

- Internet of Things (IoT) and Machine-to-Machine Constellations

- Earth Observation, Imagery & Synthetic Aperture Radar (SAR) Constellations

- Positioning, Navigation & Timing (PNT) Constellations

- Direct-to-Cell and Direct-to-Device (D2D) Constellations

- Military, Defence ISR & Allied Forces Constellations (SDA Transport Layer & Tracking Layer)

- Scientific, Astronomy & Research Constellations

- Weather, Climate & Environmental Monitoring Constellations

- Market Size & Forecast by Orbit

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Earth Orbit (GEO)

- Highly Elliptical Orbit (HEO)

- Cislunar & Deep Space

- Market Size & Forecast by Satellite Class

- CubeSat (1U to 12U)

- SmallSat (10 to 500 kg)

- Medium Satellite (500 to 1,000 kg)

- Large Satellite (Above 1,000 kg)

- Market Size & Forecast by Launch Vehicle Class

- Small-Lift (Below 2,000 kg to LEO)

- Medium-Lift (2,000 to 20,000 kg to LEO)

- Heavy-Lift (20,000 to 50,000 kg to LEO)

- Super-Heavy Lift (Above 50,000 kg to LEO)

- Market Size & Forecast by End-User

- Commercial Constellation Operators & Service Providers

- Government Civil Space Agencies (NASA, ESA, ISRO, JAXA & National Agencies)

- Military & Defence (US Space Force, SDA, NRO & Allied Forces)

- Enterprise (Connectivity, Mobility, Maritime, Aviation & Energy)

- Consumer (Direct-to-Cell, Residential Broadband & Mobility)

- Mobile Network Operators & Telecom Service Providers

- Market Size & Forecast by Sales Channel

- Direct Defence and Civil Space Procurement (FMS, DCS & National Tender)

- Spacecraft OEM, Bus Integrator & Prime Contractor Channel

- Public-Private Partnership, Concession & Hosted Payload Programme

- Constellation as a Service, Spectrum Lease & Capacity-as-a-Service Model

- Distributor, Authorised Reseller & Regional Partner Channel

- North America Space Economy and Satellite Constellation Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Ground Stations)

- By Infrastructure Segment

- By Constellation Application

- By Orbit

- By Satellite Class

- By Launch Vehicle Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Space Economy and Satellite Constellation Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Ground Stations)

- By Infrastructure Segment

- By Constellation Application

- By Orbit

- By Satellite Class

- By Launch Vehicle Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Space Economy and Satellite Constellation Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Ground Stations)

- By Infrastructure Segment

- By Constellation Application

- By Orbit

- By Satellite Class

- By Launch Vehicle Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Space Economy and Satellite Constellation Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Ground Stations)

- By Infrastructure Segment

- By Constellation Application

- By Orbit

- By Satellite Class

- By Launch Vehicle Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Space Economy and Satellite Constellation Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Ground Stations)

- By Infrastructure Segment

- By Constellation Application

- By Orbit

- By Satellite Class

- By Launch Vehicle Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Space Economy and Satellite Constellation Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Satellites & Ground Stations)

- By Infrastructure Segment

- By Constellation Application

- By Orbit

- By Satellite Class

- By Launch Vehicle Class

- By End-User

- By Country

- By Sales Channel

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Italy, Spain, Netherlands, Luxembourg, Switzerland, Sweden, Norway, Russia, China, Japan, India, South Korea, Australia, Singapore, Taiwan, Indonesia, Brazil, Argentina, Mexico, Saudi Arabia, UAE, Qatar, Israel, Egypt, South Africa

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- Mega-Constellation Mass-Production Satellite Manufacturing & Smallsat Factory Technology Deep-Dive

- Reusable Launch Vehicle, Vertical Integration & High-Cadence Launch Operations Technology

- Electric Propulsion (Hall-Effect, Gridded Ion) & Advanced In-Space Propulsion Technology

- Optical Inter-Satellite Link, Mesh Networking & Onboard Processing Technology

- Direct-to-Cell (D2D) and Non-Terrestrial Network (NTN) Integration with 3GPP Mobile Networks Technology

- In-Space Servicing, Refuelling, Active Debris Removal & On-Orbit Manufacturing Technology

- Quantum Communications, Space-Based Quantum Key Distribution & Secure Network Technology

- Patent & IP Landscape in Space Economy and Constellation Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Critical Component (Solar Cell, Battery, Photonic IC, Specialty Alloy) and Space-Grade Material Supply Chain

- Satellite Subsystem (Bus, Payload, Avionics, Propulsion, Power) & Smallsat Factory Manufacturing Supply Chain

- Launch Vehicle, Engine, Composite Tank & Avionics Supply Chain for Reusable Launchers

- Tier-1 Spacecraft Prime Contractor, System Integrator & Programme Landscape

- Constellation Operator, Civil Space Agency & Defence Programme Procurement Landscape

- Distributor, Authorised Reseller & Regional Partner Channel

- Ground Network Operator, Teleport, Cloud Distribution & Lifecycle Support Channel

- Pricing Analysis

- Smallsat and CubeSat Average Selling Price and Cost per Spacecraft Analysis

- Standard Satellite Bus, Payload Integration & Mission Cost Analysis

- Launch Vehicle Cost per Kilogram to LEO and GTO Analysis

- Ground Station, Optical Gateway & User Terminal Capital Cost Analysis

- Constellation as a Service, Hosted Payload, Spectrum Lease & Capacity Pricing Analysis

- Total Constellation Programme Economics: Cost per Subscriber, Cost per Square Kilometre Imaged & Throughput Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Satellite Constellations: Carbon Footprint, Launch Emissions & Material Footprint Across Constellation Routes

- Orbital Debris Mitigation, 5-Year De-orbit Compliance & Pathway to Zero Debris Constellation Operations

- End-of-Life Spacecraft Disposal, Active Debris Removal & Closed-Loop Material Management for Space Assets

- Environmental Compliance, Launch Site Land Use, Stratospheric Emission & Astronomy Light Pollution Consideration

- Regulatory-Driven Sustainability, Space Sustainability Rating, ESG Disclosure & Green Finance Eligibility for Space Programmes

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Segment & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Segment, Application & Geography

- Player Classification

- Vertically Integrated Constellation Operators with In-House Manufacturing and Launch

- Tier-1 Spacecraft Prime Contractors with Integrated Satellite & Launch Portfolios

- Specialty Satellite Manufacturers & Smallsat Mass-Production Specialists

- Launch Service Providers (Small-Lift, Medium-Lift & Heavy-Lift)

- Ground Station, Teleport & Cloud Distribution Network Operators

- User Terminal, Antenna & Direct-to-Cell Device Specialists

- In-Space Servicing, Active Debris Removal & On-Orbit Manufacturing Specialists

- Space Situational Awareness, Space Traffic Management & Cybersecurity Specialists

- Mission Operations Software, Data Analytics & Earth Observation Platform Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Segment, Application & Region

- Company Profile

- Company Overview & Headquarters

- Space Economy and Constellation Infrastructure Products & Technology Portfolio

- Key Customer Relationships & Reference Programme Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Space and Constellation Infrastructure Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Segment, Application, Orbit, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)