Global Space Tourism Infrastructure Market By Infrastructure Type, By Mission Type, By Component, By Vehicle Type, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Space Tourism Infrastructure Market encompasses the planning, design, construction, operation, and aftermarket support of physical and digital infrastructure platforms required to enable safe, scalable, and commercially viable suborbital, orbital, stratospheric, and emerging lunar tourism missions across commercial spaceports, vertical and horizontal launch facilities, astronaut training campuses, mission control centers, passenger terminals, recovery operations bases, and orbital habitat platforms globally. The market includes commercial spaceports supporting vertical takeoff vertical landing (VTVL) and horizontal takeoff horizontal landing (HTHL) operations, vehicle integration hangars, launch pads, propellant storage and handling systems, centrifuge and high-G simulation training facilities, microgravity preparation pools, mission control and telemetry centers, dedicated passenger terminals with pre-flight medical and orientation services, recovery vessels and landing pads, stratospheric balloon launch and ground infrastructure, and emerging orbital tourist habitats including the Vast Haven-1, Axiom Station modules, and successor commercial space stations engineered to host civilian crews. The market addresses critical operational requirements including FAA Office of Commercial Space Transportation licensing, Air Force Eastern Range and Vandenberg coordination, dedicated commercial spaceport site licensing, environmental impact compliance, passenger informed-consent regulatory regimes, comprehensive astronaut training and medical screening programs, and seamless integration with global luxury hospitality, insurance, and concierge service ecosystems. End users span commercial space tourism operators, civil space agencies operating dual-use facilities, defense and aerospace contractors, luxury hospitality and experiential travel companies, high-net-worth individual customers, research and microgravity training institutions, and infrastructure investment funds backing greenfield spaceport development, establishing space tourism infrastructure as a foundational enabling layer underpinning the commercial scaling of suborbital adventure tourism, orbital experiential travel, and emerging lunar and deep space tourism ecosystems worldwide.

Market Insights

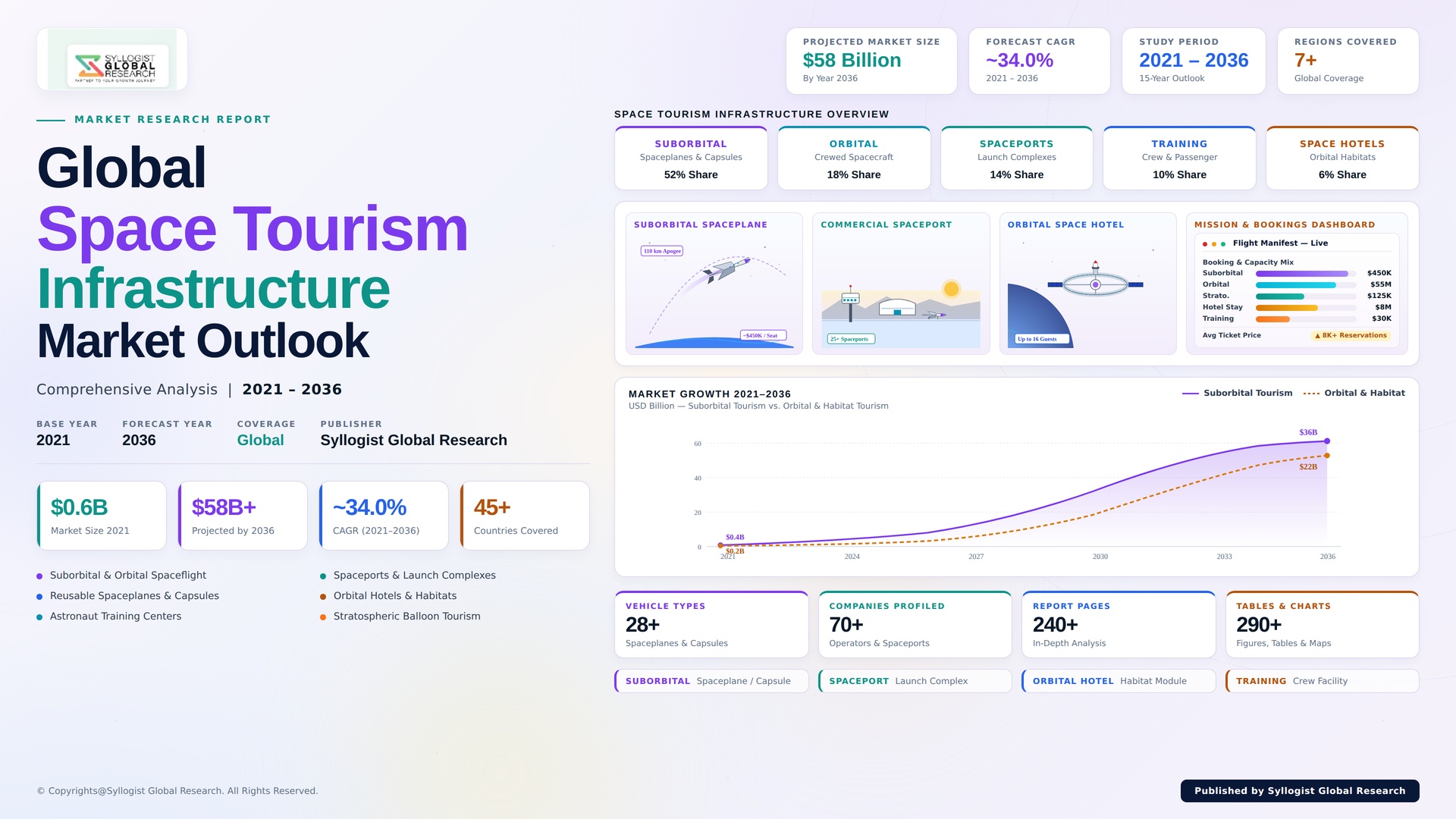

The global space tourism infrastructure market is moving through an early-stage hyper-growth phase shaped by accelerating commercial human spaceflight maturation, rising volumes of suborbital revenue flights, expanding orbital tourism through the Axiom Station and Vast Haven-1 commercial space stations, and progressively maturing commercial spaceport licensing frameworks across the FAA, EASA, and emerging Asian civil aviation authorities that are systematically de-risking infrastructure investment for greenfield space tourism deployment. The market was valued at USD 1.5 billion in 2025 and is projected to reach USD 16.0 billion by 2034, advancing at a compound annual growth rate of 30.0% through the forecast window, supported by Blue Origin New Shepard cadence acceleration, Virgin Galactic Delta-class spaceplane fleet entry, SpaceX Starship orbital tourism roadmap progression, Axiom Space Station modular deployment, and ambitious Middle Eastern, Asian, and Latin American spaceport infrastructure programs anchoring greenfield commercial spaceflight ecosystems globally throughout the forecast horizon.

Reusable launch vehicle maturation is the strongest secular force restructuring the demand profile for space tourism infrastructure, as commercial operators progressively recognize that sustainable per-passenger economics require not only reusable rocket platforms but also matching ground infrastructure capable of supporting frequent turnaround cycles, integrated medical screening, comprehensive astronaut training, and luxury-grade passenger experience design. The result is a measurable shift in revenue mix from individual demonstration flight operations toward integrated spaceport campus development incorporating launch facilities, hangars, training centers, mission control, and dedicated passenger experience terminals at single sites, restructuring procurement economics in favor of partners offering comprehensive design, construction, and long-term operations and maintenance service capability across multi-decade greenfield spaceport development programs globally. Passenger seat prices currently spanning USD 250,000 for stratospheric balloon experiences, USD 450,000 for suborbital flights, and exceeding USD 50 million for orbital missions are progressively converging toward broader-market accessibility under reusability-driven cost compression.

Within the infrastructure taxonomy, commercial spaceports anchor the highest current revenue concentration, encompassing flagship facilities such as Spaceport America, Mojave Air and Space Port, Cornwall Spaceport, Andoya Spaceport, and emerging Saudi NEOM and United Arab Emirates spaceport investments. Astronaut training centers, including centrifuge facilities, microgravity simulation pools, and integrated medical screening campuses, represent the highest engineering content infrastructure category capturing critical operational value. Orbital tourism habitats and emerging space hotels, including Vast Haven-1, Axiom Station modules, and successor commercial space stations, are scaling rapidly toward commercial deployment, while stratospheric balloon launch and recovery infrastructure supporting Space Perspective Neptune capsule operations and World View commercial flights is gaining traction as a lower-altitude entry-tier segment. Suborbital missions account for approximately 58% of forecast period passenger volumes, while orbital and emerging lunar missions reshape competitive differentiation among integrated space tourism infrastructure providers worldwide.

North America anchors the largest absolute revenue share of the global space tourism infrastructure market, valued near USD 825 million in 2025 and underpinned by Blue Origin Launch Site One operations in West Texas, Virgin Galactic Spaceport America in New Mexico, SpaceX Starbase in Boca Chica, Cape Canaveral Space Force Station commercial integration, and an expanding network of FAA-licensed commercial spaceports across the United States. Europe represents a structurally important share driven by Andoya Spaceport in Norway, Cornwall Spaceport, SaxaVord Spaceport in Shetland, and emerging Italian and German commercial spaceflight initiatives. Asia-Pacific is positioned to record the highest forecast period CAGR, supported by ambitious Chinese commercial spaceflight infrastructure investment through Deep Blue Aerospace and CAS Space, expanding Japanese suborbital and lunar tourism programs, and growing Australian, Indian, and Singaporean spaceport development. The Middle East contributes through ambitious Saudi Arabia NEOM spaceport plans and United Arab Emirates commercial spaceflight ambitions, while Latin America anchors regional growth through Brazilian Alcantara spaceport modernization and emerging Argentine spaceflight infrastructure development.

Key Drivers

Reusable Launch Vehicle Commercialization and Falling Per-Passenger Spaceflight Costs Driving Spaceport Infrastructure Capacity Expansion Globally

Accelerating reusable launch vehicle commercialization across SpaceX Falcon 9, Blue Origin New Shepard, Virgin Galactic Delta-class spaceplanes, and emerging Chinese reusable suborbital platforms is delivering significant per-passenger cost reductions, fundamentally enabling broader space tourism market accessibility and driving greenfield spaceport infrastructure capacity expansion globally. Operators are codifying frequent flight cadence requirements into spaceport master planning, anchoring multi-year infrastructure development commitments across commercial spaceport authorities, infrastructure investment funds, and integrated launch service operators worldwide throughout the forecast horizon and beyond.

Rising Ultra-High-Net-Worth Individual Demand for Adventure, Luxury, and Experiential Travel Driving Sustained Commercial Bookings and Premium Infrastructure Investment

Rising ultra-high-net-worth individual demand for adventure, luxury, and experiential travel is anchoring sustained commercial space tourism bookings, with more than 8,000 private individuals registering interest in commercial spaceflight experiences over recent years and waiting lists for suborbital missions extending multiple years into the future. Luxury hospitality companies, premium travel concierges, and integrated experience operators are progressively investing in matching ground infrastructure including dedicated passenger terminals, pre-flight resort accommodations, and post-flight celebration facilities, supporting durable demand for premium space tourism infrastructure across the global commercial spaceflight value chain.

Government Spaceport Investment, Public-Private Partnership Frameworks, and Sovereign Commercial Spaceflight Ambitions Driving Global Infrastructure Buildout Cycles

Substantial government spaceport investment, public-private partnership frameworks, and sovereign commercial spaceflight ambitions across the United States, United Kingdom, Norway, Saudi Arabia, the United Arab Emirates, China, Japan, India, and Australia are driving global space tourism infrastructure buildout cycles spanning greenfield commercial spaceports, dual-use civil-military launch facility upgrades, astronaut training campuses, and national space tourism economic development programs. Government co-funding, regulatory certainty, and airspace integration commitments are progressively de-risking infrastructure development economics for private sector spaceport operators and infrastructure investors worldwide throughout the forecast horizon.

Key Challenges

Capital Intensity, Multi-Year Spaceport Development Timelines, and Long Investment Payback Horizons Constraining Infrastructure Buildout Pace

Commercial spaceport infrastructure development faces persistent capital intensity challenges driven by significant land acquisition requirements, runway and launch pad construction costs, environmental impact assessment timelines, propellant handling system buildouts, and integrated training and mission control facility deployment that collectively extend payback horizons across multi-year and multi-decade investment windows. Spaceport developers face complex zoning approval processes, environmental review requirements, and elevated capital expenditure per site, while sustained negative cash flow phases during early operational ramp pressure financial sustainability across commercial space tourism infrastructure programs globally throughout the forecast period.

Maturing Commercial Human Spaceflight Regulatory Frameworks, Informed Consent Regimes, and Cross-Border Licensing Complexity Constraining Operational Scaling

Commercial human spaceflight regulatory frameworks across the FAA Office of Commercial Space Transportation, EASA, and emerging Asia-Pacific civil aviation authorities remain in active maturation, particularly around informed-consent regimes, passenger safety certification, medical screening standards, and cross-border licensing reciprocity arrangements, creating regulatory uncertainty that constrains commercial scaling timelines and infrastructure investment risk profiles. Spaceport operators, commercial spaceflight providers, and infrastructure investment funds face persistent challenges navigating evolving rulemaking, public comment cycles, and harmonization gaps between national frameworks across global multi-jurisdictional space tourism infrastructure deployments throughout the forecast horizon.

Safety Incident Risk Management, Insurance Market Capacity Constraints, and Public Confidence Sensitivity Across Nascent Commercial Space Tourism Operations

The nascent commercial space tourism sector remains highly sensitive to safety incident occurrences, with individual mishaps capable of triggering temporary fleet groundings, regulatory reviews, insurance market capacity contraction, and material public confidence impacts that ripple across the entire space tourism infrastructure ecosystem. Commercial spaceflight operators must coordinate stringent safety culture, redundant flight system architectures, comprehensive crew and passenger training, and adequate hull and third-party liability insurance coverage, while limited insurance market capacity for novel commercial human spaceflight risks pressures premium economics and constrains operational scaling across global space tourism infrastructure programs throughout the forecast period.

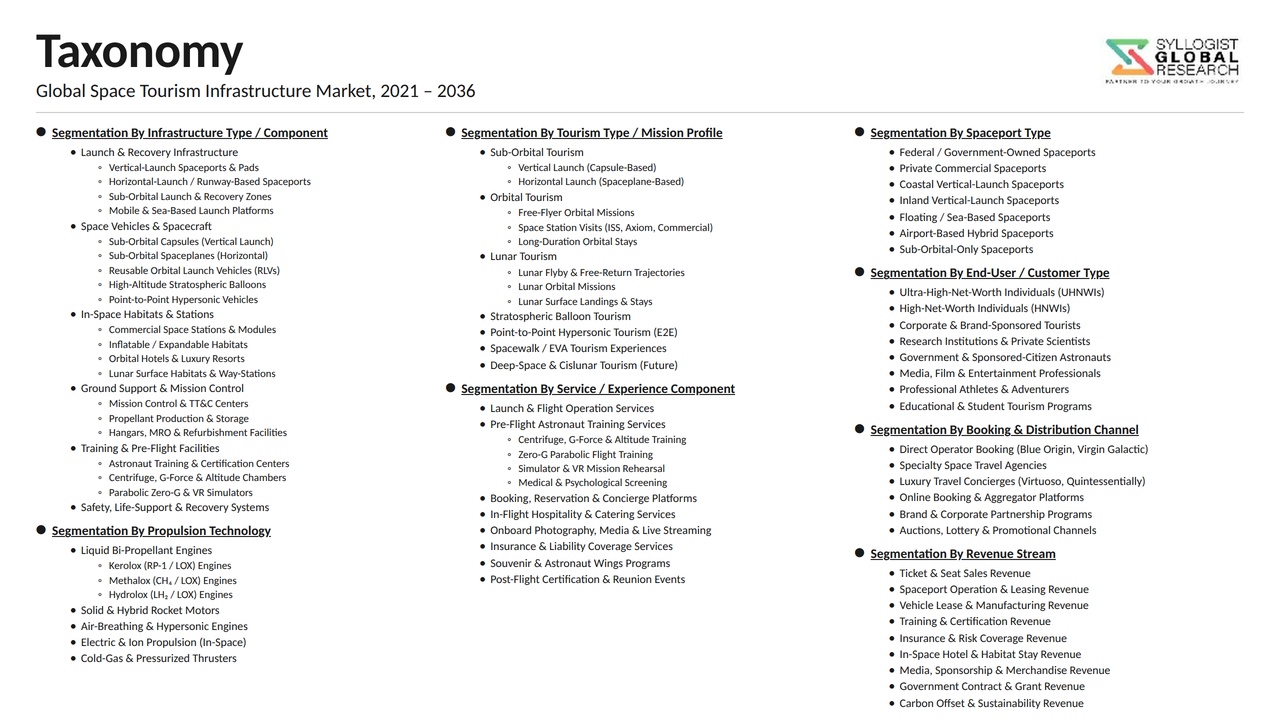

Market Segmentation

- Segmentation By Infrastructure Type

- Commercial Spaceports (Vertical Launch, Horizontal Launch, Hybrid)

- Launch Pads and Vehicle Integration Facilities

- Astronaut Training Centers and Centrifuge Facilities

- Mission Control and Operations Centers

- Passenger Terminals and Pre-Flight Facilities

- Recovery and Landing Infrastructure

- Stratospheric Balloon Launch Infrastructure

- Orbital Habitats and Space Hotels

- Lunar Surface Tourism Infrastructure (Emerging)

- Others

- Segmentation By Mission Type

- Suborbital

- Orbital

- Stratospheric (High-Altitude Balloon)

- Lunar Expeditions

- Space Hotel and Habitat Stays

- Segmentation By Component

- Hardware (Pads, Hangars, Propellant Systems, Crew Modules)

- Software (Booking, Mission Planning, Training Simulation)

- Services (Training, MRO, Hospitality, Insurance, Medical Screening)

- Segmentation By Vehicle Type Supported

- Sub-Orbital Reusable Vehicles (SRVs)

- Vertical Takeoff Vertical Landing (VTVL) Rockets

- Spaceplanes (Horizontal Takeoff Horizontal Landing)

- High-Altitude Stratospheric Balloons

- Crewed Orbital Capsules

- Others

- Segmentation By End User

- Commercial Space Tourism Operators

- Civil Space Agencies

- Defense and Aerospace Contractors

- Luxury Hospitality and Experiential Travel Companies

- Research and Microgravity Training Institutions

- Government and Public Spaceport Authorities

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Space Tourism Infrastructure Market in 2025, projected through 2034, disaggregated by infrastructure type, mission type, and end-user application, enabling spaceport developers, commercial spaceflight operators, infrastructure investment funds, and luxury hospitality strategists to identify highest-growth segments and most durable revenue opportunities across the global commercial space tourism landscape?

- How are reusable launch vehicle commercialization milestones across SpaceX Falcon 9 and Starship, Blue Origin New Shepard, Virgin Galactic Delta-class spaceplanes, and emerging Chinese reusable suborbital platforms reshaping spaceport infrastructure capacity planning, turnaround cycle requirements, and per-passenger cost economics through 2034?

- How are FAA Office of Commercial Space Transportation, EASA, Civil Aviation Authority, and equivalent regulatory frameworks shaping commercial spaceport licensing, informed-consent regimes, passenger safety certification, and cross-border operational reciprocity across global space tourism infrastructure markets?

- Which space tourism infrastructure component categories, including spaceports, training centers, mission control, passenger terminals, orbital habitats, stratospheric balloon facilities, and emerging space hotels, are recording the highest forecast period growth rates, and what mission profile, throughput, and customer experience factors are shaping demand intensity within each segment?

- How are orbital tourism platforms including Vast Haven-1, Axiom Station, and successor commercial space stations reshaping demand for orbital habitat infrastructure, multi-day passenger life support systems, and luxury hospitality integration across emerging long-duration commercial spaceflight markets?

- What partnership, vertical integration, public-private partnership, and luxury hospitality collaboration strategies are dominant space tourism infrastructure providers using to consolidate early-mover advantage, secure greenfield spaceport concessions, and scale integrated commercial spaceflight ecosystems across global regions?

- Which regional markets, specifically the United States, the United Kingdom, Norway, Saudi Arabia, the United Arab Emirates, China, Japan, India, and Australia, are expected to generate the most substantial incremental space tourism infrastructure investment through 2034, and what sovereign space ambitions, luxury travel demand, and decarbonization-aligned tourism factors are anchoring procurement growth in each market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Vehicle Safety, In-Flight Anomaly & Catastrophic Loss Risk

- Insurance, Liability, Maximum Probable Loss & Catastrophic Event Underwriting Risk

- Regulatory Uncertainty (FAA Learning Period Expiry, Informed Consent Framework) and Permitting Delay Risk

- Customer Acquisition, Demand Softness & Ultra-High Ticket Price Sensitivity Risk

- Public Perception, Environmental Concern & Stratospheric Emission Reputational Risk

- Regulatory Framework & Standards

- FAA Part 460 Human Space Flight Requirements, Part 450 Launch Licensing & Commercial Spaceflight Informed Consent Standards

- ASTM F47 Commercial Spaceflight Industry Consensus Standards & Best Practices

- Outer Space Treaty 1967, Liability Convention 1972 & Long-Term Sustainability of Outer Space Activities (LTS) Guidelines

- ICAO Sub-Orbital Vehicle Classification, EASA Sub-Orbital Operations & National Aviation Authority Frameworks

- ITAR Category XV, EAR Commerce Control List & Crew/Passenger Medical Screening Standards

- Global Space Tourism Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Flights & Customer Seats)

- Market Size & Forecast by Infrastructure Type

- Spaceports & Launch/Landing Sites

- Suborbital Tourism Vehicles (Vertical and Spaceplane)

- Orbital Crew Vehicles & Capsules

- High-Altitude Stratospheric Balloon Vehicles & Pressurised Capsules

- Commercial Space Stations & Orbital Habitats

- Lunar Tourism Vehicles & Cislunar Infrastructure

- Astronaut Training Facilities, Centrifuges & Simulators

- Mission Control, Recovery & Ground Support Operations

- Spaceport Hospitality, Visitor Centre & Pre-Flight Customer Experience

- Insurance, Medical Screening & Customer Support Services

- Market Size & Forecast by Mission Profile

- Suborbital Spaceflight (Above Karman Line and 80 km US Definition)

- High-Altitude Stratospheric Balloon Flight (Up to 30 km)

- Orbital Free-Flying Spaceflight (LEO, Multi-Day Mission)

- Commercial Space Station Stay (LEO Habitat Visit)

- Lunar Flyby and Cislunar Mission

- Lunar Orbit and Surface Mission

- Parabolic Zero-Gravity Flight (Sub-Orbital Aircraft Simulation)

- Market Size & Forecast by Spaceport Type

- Vertical Launch Spaceport (Conventional Rocket Operations)

- Horizontal Take-off Spaceport with Spaceplane Runway

- Stratospheric Balloon Launch Site

- Floating, Sea-Based & Equatorial Launch Site

- Lunar and Off-Earth Landing Site

- Market Size & Forecast by Component

- Civil Works (Pads, Hangars, Fuel Storage, Runways & Recovery Zones)

- Vehicle, Capsule & Spacecraft Assets

- Mission Control, Tracking & Communications Systems

- Astronaut Training, Centrifuge & Simulator Equipment

- Hospitality, Terminal, Visitor Centre & Customer-Facing Facilities

- Recovery, Search and Rescue & Emergency Response Equipment

- Booking, Reservation & Customer Experience Platform Software

- Market Size & Forecast by Customer Segment

- Ultra-High-Net-Worth & High-Net-Worth Individuals

- Sponsored, Lottery & Charity Mission Customers

- Corporate & Brand Marketing Customers

- Research, Educational & Scientific Mission Customers

- Government Astronauts Flying on Commercial Vehicles

- Tour Operators, Luxury Travel Agencies & Concierge Resellers

- Market Size & Forecast by Service Model

- Per-Seat Ticket Sale (Single Mission)

- Per-Flight Charter & Private Mission Booking

- Subscription, Membership & Loyalty Programme

- Multi-Mission and Bundled Experience Package

- Hosted Research, Sponsorship & Branded Mission Programme

- Market Size & Forecast by Sales Channel

- Direct Sale by Vehicle Operator

- Authorised Travel Agent, Concierge & Luxury Tourism Reseller

- Corporate Brand Partnership & Marketing Programme

- Sponsorship, Lottery & Foundation Programme

- North America Space Tourism Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Flights & Customer Seats)

- By Infrastructure Type

- By Mission Profile

- By Spaceport Type

- By Component

- By Customer Segment

- By Service Model

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Space Tourism Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Flights & Customer Seats)

- By Infrastructure Type

- By Mission Profile

- By Spaceport Type

- By Component

- By Customer Segment

- By Service Model

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Space Tourism Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Flights & Customer Seats)

- By Infrastructure Type

- By Mission Profile

- By Spaceport Type

- By Component

- By Customer Segment

- By Service Model

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Space Tourism Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Flights & Customer Seats)

- By Infrastructure Type

- By Mission Profile

- By Spaceport Type

- By Component

- By Customer Segment

- By Service Model

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Space Tourism Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Flights & Customer Seats)

- By Infrastructure Type

- By Mission Profile

- By Spaceport Type

- By Component

- By Customer Segment

- By Service Model

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Space Tourism Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Flights & Customer Seats)

- By Infrastructure Type

- By Mission Profile

- By Spaceport Type

- By Component

- By Customer Segment

- By Service Model

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Italy, Spain, Netherlands, Switzerland, Sweden, Norway, Russia, China, Japan, India, South Korea, Australia, Singapore, Thailand, Indonesia, Brazil, Argentina, Chile, Mexico, Saudi Arabia, UAE, Qatar, Israel, Egypt, South Africa

- Technology Landscape & Innovation Analysis

- Reusable Suborbital Vehicle, Spaceplane Hybrid Propulsion & Vertical Take-off / Vertical Landing Technology Deep-Dive

- Orbital Crew Capsule, Launch Abort System & Auto-Docking Technology

- High-Altitude Stratospheric Balloon, Pressurised Capsule & Helium/Hydrogen Lift Technology

- Inflatable Habitat, Commercial Space Station Module & Regenerative Life Support Technology

- Astronaut Training, Centrifuge, Augmented Reality Simulator & Biotelemetry Technology

- Lunar Tourism Vehicle, Cislunar Mission & Surface Excursion Technology

- Customer Experience, In-Cabin Sensor, Health Monitoring & Real-Time Earth-View Technology

- Patent & IP Landscape in Space Tourism Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Reusable Vehicle, Engine, Composite Tank & Heat Shield Component Supply Chain

- Crew Capsule, Life Support, Spacesuit & Cabin Interior Component Supply Chain

- Stratospheric Balloon, Capsule, Helium and Hydrogen Lift Gas Supply Chain

- Tier-1 Vehicle Operator, Spaceport Developer & System Integrator Landscape

- Spaceport Authority, Tourism Operator & Customer Acquisition Procurement Landscape

- Authorised Travel Agent, Luxury Concierge & Tourism Reseller Channel

- Astronaut Training Provider, Insurance Underwriter, Medical Screening & Lifecycle Customer Support Channel

- Pricing Analysis

- Suborbital Spaceflight Per-Seat Ticket Pricing & Cost per Mission Analysis

- High-Altitude Stratospheric Balloon Flight Per-Seat Pricing Analysis

- Orbital Free-Flying Mission and Commercial Space Station Stay Pricing Analysis

- Lunar Flyby, Cislunar and Lunar Surface Mission Pricing Analysis

- Charter Mission, Private Booking & Branded Sponsorship Programme Pricing Analysis

- Total Space Tourism Programme Economics: Cost per Customer and Vehicle Reuse Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Space Tourism Operations: Carbon Footprint, Stratospheric Emission & Material Footprint Across Mission Profiles

- Reusable Vehicle, Green Propellant & Pathway to Lower-Carbon Suborbital and Orbital Tourism Operations

- End-of-Life Vehicle Disposal, Capsule Refurbishment & Closed-Loop Material Management for Tourism Assets

- Environmental Compliance, Spaceport Land Use, Wildlife and Sonic Boom Consideration in Spaceport Operations

- Regulatory-Driven Sustainability, Ozone Layer Protection Alignment & ESG Disclosure for Space Tourism Operators

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Mission Profile & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Mission Profile, Infrastructure Type & Geography

- Player Classification

- Vertically Integrated Space Tourism Operators with In-House Vehicle and Spaceport Programmes

- Suborbital Spaceflight Operators (Vertical Take-off and Spaceplane)

- Orbital Crew Mission and Commercial Space Station Operators

- High-Altitude Stratospheric Balloon Tourism Operators

- Lunar and Cislunar Tourism Mission Specialists

- Spaceport Developers, Operators & Authority Bodies

- Astronaut Training Academies, Simulator and Centrifuge Service Providers

- Booking Platform, Luxury Travel Concierge & Authorised Reseller Specialists

- Insurance, Medical Screening & Lifecycle Customer Support Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Mission Profile, Infrastructure Type & Region

- Company Profile

- Company Overview & Headquarters

- Space Tourism Infrastructure Products, Vehicles & Service Portfolio

- Key Customer Relationships & Reference Mission Deployments

- Manufacturing Footprint, Vehicle Fleet & Spaceport Capacity

- Revenue (Space Tourism Segment) & Customer Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Mission Wins, Capacity Expansion, Vehicle Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Mission Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Mission Profile, Customer Segment, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)