Global Counter-UAS Detection and Neutralization Systems Market By Technology, By Platform, By Range, By Application, By Component, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Counter-UAS Detection and Neutralization Systems Market encompasses the development, integration, procurement, and operational deployment of integrated technology platforms designed to detect, track, identify, classify, and neutralize unauthorized, hostile, or rogue unmanned aerial systems operating within protected airspace across military, homeland security, critical infrastructure, commercial, and public safety environments globally. The market includes detection technologies such as radar systems, radio frequency sensors, electro-optical and infrared cameras, acoustic sensor arrays, and AI-enabled multi-sensor fusion platforms, alongside neutralization technologies including radio frequency jammers, GPS spoofers, directed energy laser weapons, high-power microwave systems, kinetic interceptor drones, net capture launchers, cyber-takeover effectors, and integrated command and control architectures coordinating layered defense responses. The market addresses critical operational requirements including airspace surveillance around airports, military bases, energy facilities, government installations, prisons, stadiums, and border zones, along with mobile force protection for deployed military units, convoy security, and special event coverage requiring rapid deployment counter-drone coverage envelopes. End users span defense ministries, military commands, homeland security agencies, federal law enforcement, airport authorities, energy operators, public safety organizations, prison administrations, stadium and event security providers, and private critical infrastructure protection contractors operating across both regulated civilian airspace and active military theaters. Geographic deployment spans mature North American and European defense markets, rapidly expanding Asia-Pacific homeland security investments, and conflict-driven Middle East procurement, with delivery models encompassing fixed installation perimeter coverage, vehicle-mounted mobile platforms, portable handheld devices, and integrated multi-domain layered defense architectures coordinated through C4ISR command frameworks, establishing counter-UAS technology as a foundational element within modern airspace security, force protection, and critical asset defense ecosystems worldwide.

Market Insights

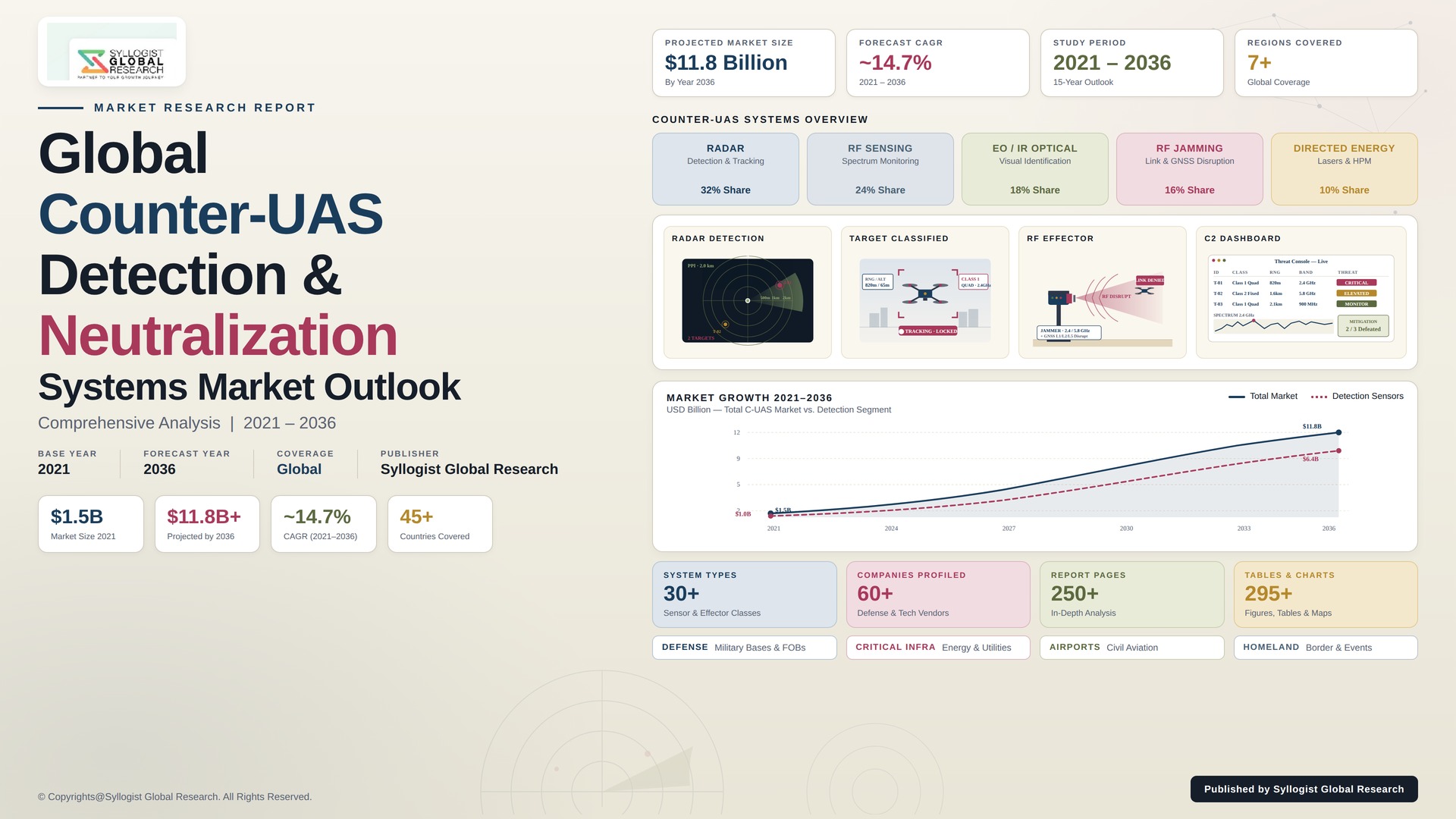

The global counter-UAS detection and neutralization systems market is moving through an unprecedented acceleration phase shaped by direct operational evidence from active conflict environments, where weaponized small drones, loitering munitions, and autonomous swarming platforms have demonstrated decisive battlefield impact and exposed defensive gaps across previously secure airspace, compelling defense ministries, homeland security agencies, and critical infrastructure operators to compress procurement timelines for layered counter-drone defenses. The market was valued at USD 6.0 billion in 2025 and is projected to reach USD 28.5 billion by 2034, advancing at a compound annual growth rate of 18.9% through the forecast window, supported by surging defense AI investment, accelerated operational lessons absorbed from Ukraine and Middle East conflict theaters, expanding airport and energy facility protection mandates, and broadening adoption of AI-enabled radar, radio frequency sensor, and electro-optical fusion architectures across both military and civilian counter-drone deployment scenarios worldwide.

Technology layering is the strongest secular force restructuring the demand profile for counter-UAS systems, as procurement officers increasingly recognize that single-modality solutions cannot reliably defeat the spectrum of modern threats spanning consumer quadcopters, FPV racing drones, fiber-optic-controlled platforms, fixed-wing UAVs, and autonomous swarm formations operating across radio-frequency-denied environments. The result is a measurable shift in revenue mix toward integrated layered defense architectures combining radar detection, RF spectrum monitoring, EO/IR tracking, acoustic sensing, and AI-enabled threat classification feeding hard-kill and soft-kill effector chains including jamming, spoofing, directed energy lasers, high-power microwave systems, and autonomous interceptor drones. End users are simultaneously prioritizing modular open-architecture platforms supporting rapid software updates, multi-vendor effector integration, and seamless connectivity into broader integrated air and missile defense networks, restructuring procurement economics in favor of suppliers offering scalable, upgradable, and interoperable counter-UAS technology stacks across heterogeneous threat environments globally.

Within the technology taxonomy, radar and radio frequency detection systems anchor the highest current revenue concentration within the detection segment, while neutralization solutions, including jamming, directed energy, and kinetic interceptor systems, are recording the steepest growth trajectories as procurement priorities shift from situational awareness toward decisive hard-kill engagement capability. Directed energy weapons, encompassing high-energy laser and high-power microwave platforms, are scaling rapidly under multi-billion-dollar US, UK, Israel, and allied development programs, while autonomous interceptor drone systems and AI-coordinated swarm-versus-swarm architectures are emerging as breakthrough technology categories. Ground-based fixed and vehicle-mounted platforms continue to lead deployment volume, capturing approximately 68% of platform revenue, while handheld portable counter-drone systems are scaling rapidly across border patrol, dismounted infantry, and law enforcement applications, reshaping competitive differentiation among integrated counter-UAS technology providers worldwide.

North America anchors the largest absolute revenue share of the global counter-UAS detection and neutralization systems market, valued near USD 2.4 billion in 2025 and underpinned by US Department of Defense Replicator-aligned counter-drone investment, Pentagon multi-billion-dollar layered counter-UAS funding, FAA airport detection mandates, and accelerating Department of Homeland Security procurement programs spanning border, infrastructure, and public event protection. Europe represents a structurally critical share driven by NATO airspace protection commitments, conflict-driven counter-drone capability expansion across Eastern European border states, and growing United Kingdom directed energy weapon procurement. The Middle East is recording exceptional procurement velocity supported by Israel, Saudi Arabia, the United Arab Emirates, and Qatar deploying multi-billion-dollar layered counter-drone defenses against asymmetric drone threats. Asia-Pacific is positioned to record the highest forecast period CAGR, supported by India, Japan, South Korea, Australia, and Taiwan investment programs responding to regional drone threat proliferation across border and coastal zones, while Latin America and Africa contribute incremental procurement growth through critical infrastructure and counter-narcotics applications.

Key Drivers

Operational Lessons from Ukraine and Middle East Conflicts Demonstrating Decisive Battlefield Impact of Weaponized Drones Driving Urgent Counter-UAS Procurement Mandates

Direct operational evidence from active conflict theaters in Ukraine, Israel, the Red Sea, and the Sahel has demonstrated the asymmetric battlefield impact of low-cost weaponized drones, FPV first-person-view munitions, and loitering munitions against high-value military and civilian targets, creating durable procurement urgency among defense establishments worldwide that recognize the strategic risk of delayed counter-drone modernization. Defense ministries are compressing traditional acquisition timelines, prioritizing rapid fielding contracts, and elevating counter-UAS spend within force protection, base defense, and forward-deployed unit equipping budgets across NATO, Indo-Pacific, and Middle East allied procurement programs.

Critical Infrastructure Protection Mandates and Airport Drone Incursion Incidents Driving Civilian Counter-UAS Adoption Across Energy, Aviation, Government, and Public Event Sectors

Recurring drone incursion incidents at major international airports, energy facilities, government installations, prisons, and high-profile public events are accelerating civilian counter-UAS procurement under federal aviation, homeland security, and critical infrastructure protection regulatory frameworks. The progressive codification of detection and reporting requirements at protected airspace boundaries, combined with insurance-driven asset protection imperatives across utilities, oil and gas operators, and event venues, is reinforcing structural demand for fixed installation, mobile, and rapidly deployable counter-drone technology suites across non-defense end-user verticals globally throughout the forecast horizon.

AI-Enabled Multi-Sensor Fusion, Directed Energy Weapon Maturation, and Autonomous Interceptor Drone Development Generating Premium Demand for Next-Generation Counter-UAS Capability

The accelerating maturation of AI-enabled multi-sensor fusion platforms, high-energy laser weapons, high-power microwave effectors, and autonomous AI-coordinated interceptor drone systems is generating premium demand for next-generation counter-UAS capabilities engineered to defeat increasingly autonomous, swarming, and RF-resilient drone threats. Substantial defense research, development, test, and evaluation funding across the United States, United Kingdom, Israel, Germany, and allied nations is anchoring durable revenue visibility for technology-leading counter-UAS prime contractors and specialist startups developing breakthrough effector and command-and-control architectures across global counter-drone procurement programs.

Key Challenges

Civilian Airspace Regulatory Complexity, Radio Frequency Jamming Restrictions, and Federal Authority Limitations Constraining Counter-UAS Deployment Outside Defense Environments

Civilian airspace regulatory frameworks across the United States, European Union, and other jurisdictions impose significant restrictions on radio frequency jamming, GPS spoofing, and kinetic engagement of unmanned aircraft outside narrowly defined federal authorities, creating compliance complexity that materially constrains counter-UAS deployment across non-defense end users including airports, energy operators, stadiums, and law enforcement agencies. The current authority gap between federal counter-drone privileges and state, local, and private sector protection needs continues to slow civilian market expansion despite escalating threat exposure, requiring legislative reform and authority delegation frameworks to fully unlock commercial counter-UAS demand globally.

Rapidly Evolving Drone Threats Including Fiber-Optic-Controlled Platforms, Autonomous Swarms, and AI-Enabled Drones Outpacing Existing Counter-UAS Countermeasures

Rapidly evolving drone threats including fiber-optic-tethered FPV platforms immune to RF jamming, autonomous AI-guided swarm formations capable of saturating defensive engagement capacity, and edge-AI-enabled drones operating in fully GPS-denied and communications-denied conditions are systematically outpacing existing counter-UAS countermeasure capabilities, creating recurring obsolescence risk across deployed defensive systems. Counter-UAS suppliers face persistent technology refresh pressure, requiring continuous research and development investment to keep pace with adversary innovation cycles that frequently outpace traditional defense acquisition response timelines across global counter-drone programs.

Multi-Vendor Integration Complexity, Interoperability Gaps, and Total Cost of Ownership Pressures Across Layered Counter-UAS Defense Architectures

Layered counter-UAS architectures integrating radar, RF, EO/IR, acoustic, jamming, directed energy, and kinetic effectors across multiple vendor product lines introduce significant integration complexity, interoperability challenges, and command and control coordination requirements that elevate program timelines, certification burdens, and total cost of ownership across deployed counter-drone defenses. Procurement agencies face persistent challenges harmonizing data standards, message formats, and engagement authorization protocols across heterogeneous sensor and effector ecosystems, while training, sustainment, and software upgrade requirements compound lifecycle support cost pressures across counter-UAS deployment programs globally.

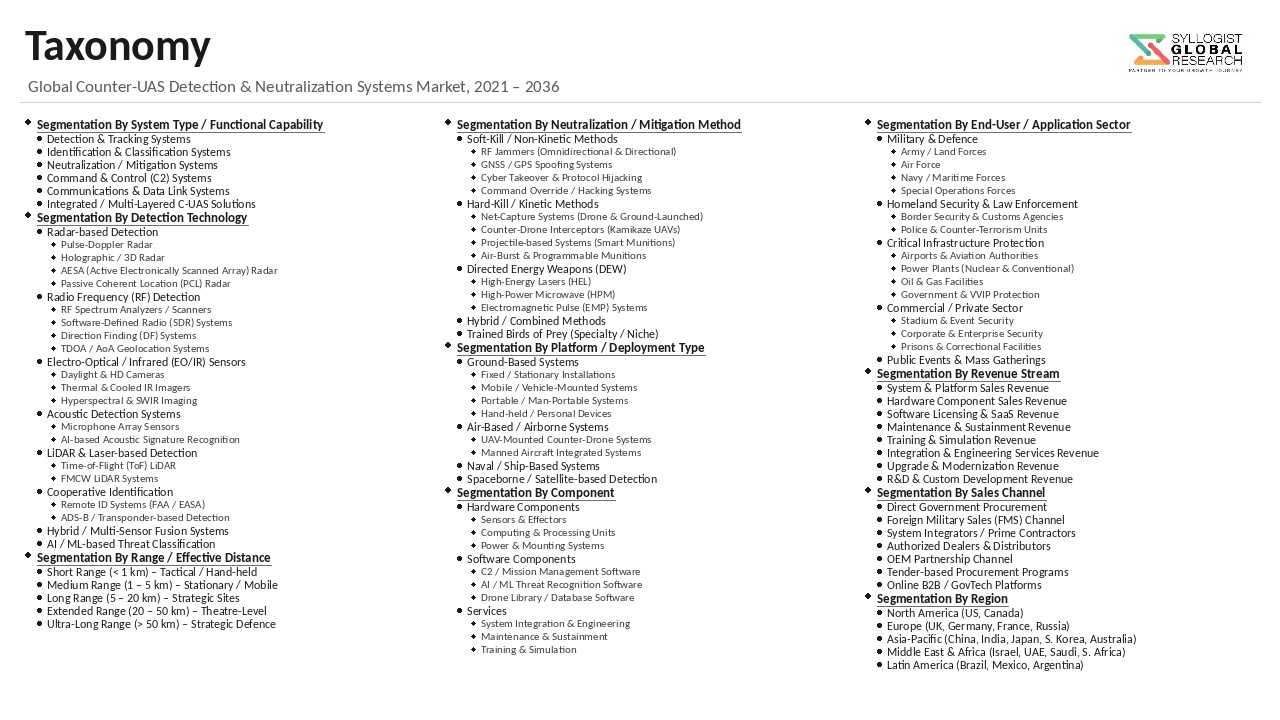

Market Segmentation

- Segmentation By Technology

- Detection (Radar, Radio Frequency, Electro-Optical / Infrared, Acoustic, Multi-Sensor Fusion)

- Identification, Tracking, and Classification

- Neutralization – Radio Frequency Jamming and GPS Spoofing

- Neutralization – Directed Energy Weapons (High-Energy Laser, High-Power Microwave)

- Neutralization – Kinetic and Interceptor Drones

- Neutralization – Net Capture and Physical Effectors

- Neutralization – Cyber-Takeover and Protocol Exploitation

- Command and Control (C2) Systems

- Others

- Segmentation By Platform

- Ground-Based Fixed Installation

- Ground-Based Mobile and Vehicle-Mounted

- Handheld and Portable

- UAV-Mounted and Airborne

- Naval and Maritime

- Others

- Segmentation By Range

- Short Range (up to 5 km)

- Medium Range (5 km to 50 km)

- Extended Range (above 50 km)

- Segmentation By Application

- Military and Defense

- Homeland Security and Border Protection

- Critical Infrastructure (Airports, Energy, Government Facilities)

- Public Safety and Law Enforcement

- Commercial and Public Events

- Correctional Facilities

- Others

- Segmentation By Component

- Sensors and Radars

- Cameras and Optical Payloads

- Effectors and Mitigation Hardware

- Command, Control, and Communication Systems

- AI and Software Platforms

- Power Supply and Auxiliary Subsystems

- Others

- Segmentation By End User

- Army and Land Forces

- Air Force and Aerospace Commands

- Naval and Maritime Forces

- Special Operations and Intelligence Agencies

- Homeland Security and Federal Law Enforcement

- Airport and Aviation Authorities

- Energy and Utility Operators

- Commercial and Private Security Providers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Counter-UAS Detection and Neutralization Systems Market in 2025, projected through 2034, disaggregated by technology, platform, and end-user application, enabling defense contractors, homeland security agencies, critical infrastructure operators, and investors to identify highest-growth segments and most durable revenue opportunities across the global counter-drone capability landscape?

- How are the United States, NATO members, Indo-Pacific allies, and Middle East partners allocating counter-UAS investment across detection, identification, and neutralization solutions, and which national programs are setting the technical and procurement benchmarks shaping global counter-drone market architecture through 2034?

- How are operational lessons from Ukraine, Middle East, and Red Sea conflict environments reshaping counter-UAS technology requirements, layered defense doctrine, and procurement priorities across military, homeland security, and critical infrastructure protection programs globally?

- Which counter-UAS neutralization technology categories, including radio frequency jamming, directed energy lasers, high-power microwave systems, kinetic interceptor drones, and cyber-takeover effectors, are recording the highest forecast period growth rates, and what threat evolution and operational performance factors are shaping demand intensity within each segment?

- What civilian airspace regulatory reforms, federal counter-drone authority delegations, and FAA, EASA, and equivalent rulemaking initiatives are most critical to unlocking expanded commercial counter-UAS adoption across airports, energy facilities, stadiums, and other non-defense end-user environments?

- How is the competitive landscape structured among defense prime contractors, specialist counter-UAS technology firms, dual-use AI software developers, and autonomous interceptor drone startups, and what partnership, acquisition, and teaming strategies are reshaping market positioning across global counter-drone procurement programs?

- Which regional markets, specifically Asia-Pacific, the Middle East, and Eastern Europe, are expected to generate the most substantial incremental counter-UAS procurement through 2034, and what geopolitical, threat environment, and defense modernization factors are driving capability investment priorities and supplier selection decisions across each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Drone Threat Evolution, Autonomous Swarm & Fibre-Optic Guided Drone Risk

- Spectrum Allocation, RF Interference & Collateral Disruption Risk

- Legal and Regulatory Authority for Non-Military Counter-UAS Engagement Risk

- Defence Procurement Cycle, Budget Volatility & Programme Delay Risk

- Export Control (ITAR, EAR, Wassenaar) & Geopolitical Restriction Risk

- Regulatory Framework & Standards

- National Counter-UAS Authority, Use of Force & Civilian Site Protection Policy Frameworks

- Spectrum Management, FCC/Ofcom Jamming Restriction & Frequency Allocation Standards

- Export Control Regimes (ITAR, EAR, Wassenaar Arrangement & MTCR) Applicable to Counter-UAS Equipment

- ICAO, FAA & Civil Aviation Authority Integration Standards for Counter-UAS Operations in Controlled Airspace

- Defence Procurement, Information Assurance, Cybersecurity & Test and Evaluation Compliance Standards

- Global Counter-UAS Detection and Neutralization Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by System Function

- Detection & Tracking Systems

- Identification & Classification Systems

- Neutralization & Mitigation Systems (Effectors)

- Integrated & Fused Counter-UAS Systems with Command and Control

- Command, Control, Communications & Battle Management (C2) Systems

- Market Size & Forecast by Detection Technology

- Radar (Pulse Doppler, FMCW, AESA & Holographic)

- Radio Frequency (RF) Detection & Spectrum Analyser

- Electro-Optical & Infrared (EO/IR) Camera

- Acoustic Sensor

- LiDAR & Other Optical Detection

- Multi-Sensor Fusion & AI-Enabled Detection

- Market Size & Forecast by Neutralization Technology

- RF & GNSS Jamming

- GNSS Spoofing & Cyber Protocol Takeover

- High-Energy Laser (HEL) Directed Energy

- High-Power Microwave (HPM) Directed Energy

- Net Capture & Tethered Interceptor

- Kinetic Interceptor Drone (Drone-on-Drone)

- Projectile, Missile & Gun-Based Kinetic Effector

- Hybrid & Multi-Effect Neutralization

- Market Size & Forecast by Platform

- Fixed Site (Ground-Based Stationary)

- Mobile & Vehicle-Mounted Ground Platform

- Man-Portable & Handheld

- Naval & Maritime

- Airborne (Manned Aircraft & UAV-Mounted)

- Market Size & Forecast by Range

- Short-Range (Below 5 km)

- Medium-Range (5 to 20 km)

- Long-Range (Above 20 km)

- Market Size & Forecast by UAS Threat Class

- Group 1 (Micro and Small UAS Below 9 kg)

- Group 2 (Below 25 kg)

- Group 3 (Below 600 kg, Tactical UAS)

- Group 4 and 5 (MALE, HALE & Larger Strategic UAS)

- Swarm, Loitering Munition & Multi-Drone Threats

- Market Size & Forecast by Component

- Hardware (Sensors, Effectors, Antennas & Displays)

- Software (Command and Control, AI Threat Classification & Sensor Fusion)

- Services (Training, Integration, Maintenance & Mission Support)

- Market Size & Forecast by End-User

- Military & Defence Forces (Army, Navy, Air Force & Special Operations)

- Homeland Security & Law Enforcement

- Critical Infrastructure Protection (Airports, Energy, Nuclear & Telecom)

- Commercial & Private Sector (Stadiums, Prisons, VIP & Data Centres)

- Border Protection & Customs Agencies

- Government & Diplomatic Facilities

- Market Size & Forecast by Sales Channel

- Direct Defence Procurement & Government Contract (FMS, DCS & National Tender)

- System Integrator & Prime Contractor Channel

- Distributor, Authorised Reseller & Regional Partner Channel

- Sustainment, Lifecycle Support & Performance-Based Logistics Programme

- North America Counter-UAS Detection and Neutralization Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Function

- By Detection Technology

- By Neutralization Technology

- By Platform

- By UAS Threat Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Counter-UAS Detection and Neutralization Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Function

- By Detection Technology

- By Neutralization Technology

- By Platform

- By UAS Threat Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Counter-UAS Detection and Neutralization Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Function

- By Detection Technology

- By Neutralization Technology

- By Platform

- By UAS Threat Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Counter-UAS Detection and Neutralization Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Function

- By Detection Technology

- By Neutralization Technology

- By Platform

- By UAS Threat Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Counter-UAS Detection and Neutralization Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Function

- By Detection Technology

- By Neutralization Technology

- By Platform

- By UAS Threat Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Counter-UAS Detection and Neutralization Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Function

- By Detection Technology

- By Neutralization Technology

- By Platform

- By UAS Threat Class

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Italy, Spain, Netherlands, Sweden, Norway, Poland, Ukraine, Russia, Turkey, China, Japan, India, South Korea, Australia, Singapore, Taiwan, Brazil, Mexico, Argentina, Saudi Arabia, UAE, Israel, Qatar, Egypt, South Africa

- Technology Landscape & Innovation Analysis

- Multi-Sensor Fusion, AI-Based Threat Classification & Counter-Swarm Battle Management Technology Deep-Dive

- Holographic, AESA & Cognitive Radar Counter-UAS Detection Technology

- RF Detection, Protocol Decoding & Cyber Drone Takeover Technology

- High-Energy Laser (HEL) Directed Energy Counter-UAS Technology

- High-Power Microwave (HPM) Directed Energy & Pulsed Power Technology

- Kinetic Interceptor Drone, Hard-Kill Effector & Counter-Loitering Munition Technology

- Counter-Swarm, Counter-Autonomous & Counter-Fibre-Optic Guided Drone Technology

- Patent & IP Landscape in Counter-UAS Technologies

- Value Chain & Supply Chain Analysis

- Sensor (Radar, EO/IR, RF) Component & Subsystem Manufacturing Supply Chain

- Effector, Directed Energy Source & Pulsed Power Component Supply Chain

- Software, AI Algorithm & Battle Management System Development Supply Chain

- Prime Contractor, System Integrator & Platform Integration Landscape

- Defence Operator, Homeland Security & Critical Infrastructure Procurement Landscape

- Distributor, Authorised Reseller & Regional Partner Channel

- Lifecycle Support, Sustainment, Training & Mission Software Update

- Pricing Analysis

- Detection-Only System Average Selling Price and Cost per Site Analysis

- Integrated Detect-Track-Identify-Defeat System Pricing & Total Acquisition Cost Analysis

- RF Jammer & Soft-Kill Effector Pricing Analysis

- High-Energy Laser & High-Power Microwave Directed Energy System Pricing Analysis

- Kinetic Interceptor & Hard-Kill Effector per-Engagement Cost Analysis

- Total Counter-UAS Programme Economics: Cost per Engagement and Force Protection Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Counter-UAS Systems: Energy Intensity, Material Footprint & Critical Mineral Intensity Across System Routes

- Green Defence Manufacturing & Pathway to Energy-Efficient, Critical Mineral Lean & Circular Counter-UAS Portfolios

- End-of-Life Effector, Battery & Pulsed Power Equipment Recovery and Closed-Loop Material Management

- Environmental Compliance, Spectrum Pollution & Collateral Disruption Consideration in Counter-UAS Operations

- Regulatory-Driven Sustainability, Defence Decarbonisation & ESG Disclosure Alignment for Defence Programmes

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Function & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Function, Technology & Geography

- Player Classification

- Tier-1 Defence Prime Contractors with Integrated Counter-UAS Portfolios

- Specialty Counter-UAS System Integrators & Pure-Play Vendors

- Radar & Sensor Technology Specialists Integrating into Counter-UAS Solutions

- Directed Energy & Pulsed Power Specialists (HEL & HPM)

- Software, AI Threat Classification & Battle Management Platform Providers

- Soft-Kill (RF Detection, Jammer & Cyber Takeover) Specialists

- Hard-Kill (Interceptor Drone, Net Capture & Kinetic Effector) Specialists

- Distributors, Authorised Resellers & Sustainment Service Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by System Function, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Counter-UAS Products & Technology Portfolio

- Key Customer Relationships & Reference Programme Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Counter-UAS Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (System Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By System Function, Technology, Platform, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)