Global Oilfield Chemicals Market By Product Type, By Application, By Well Type, By Location of Deployment, By Form, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Oilfield Chemicals Market encompasses the manufacturing, distribution, and field application of specialty and commodity chemical formulations deployed across upstream and midstream oil and gas operations spanning drilling, well cementing, completion, stimulation, production, enhanced oil recovery, and pipeline integrity management. Oilfield chemicals comprise a diverse portfolio of functional product categories including corrosion inhibitors, scale inhibitors, demulsifiers, biocides, surfactants, friction reducers, polymers, hydrogen sulfide scavengers, paraffin and asphaltene control agents, gas well foamers, water clarifiers, drilling fluid additives, and cementing additives engineered to optimize hydrocarbon recovery, protect reservoir productivity, and safeguard downhole and surface infrastructure assets across onshore and offshore production environments. The market addresses critical operational requirements including microbial control in injection water systems, flow assurance management in subsea and deepwater pipelines, fluid loss prevention during drilling operations, formation damage mitigation during completion activities, and emulsion separation across upstream production handling. End users include international oil companies, national oil companies, independent exploration and production operators, oilfield service contractors, and integrated chemical management programs supporting conventional crude oil, shale, tight oil, heavy oil, gas condensate, deepwater, and arctic field developments. Geographic deployment spans mature producing basins, unconventional shale plays, deepwater offshore frontiers, and emerging exploration regions, with delivery models encompassing bulk chemical supply, performance-based chemical management contracts, digital chemical monitoring platforms, and integrated production chemistry services. The oilfield chemicals industry further supports field life extension activities, intervention workover programs, hydraulic fracturing operations, and matrix acidizing treatments, establishing a foundational position within global hydrocarbon production economics, refinery feedstock continuity, and energy security architectures across both established and emerging upstream operating environments worldwide.

Market Insights

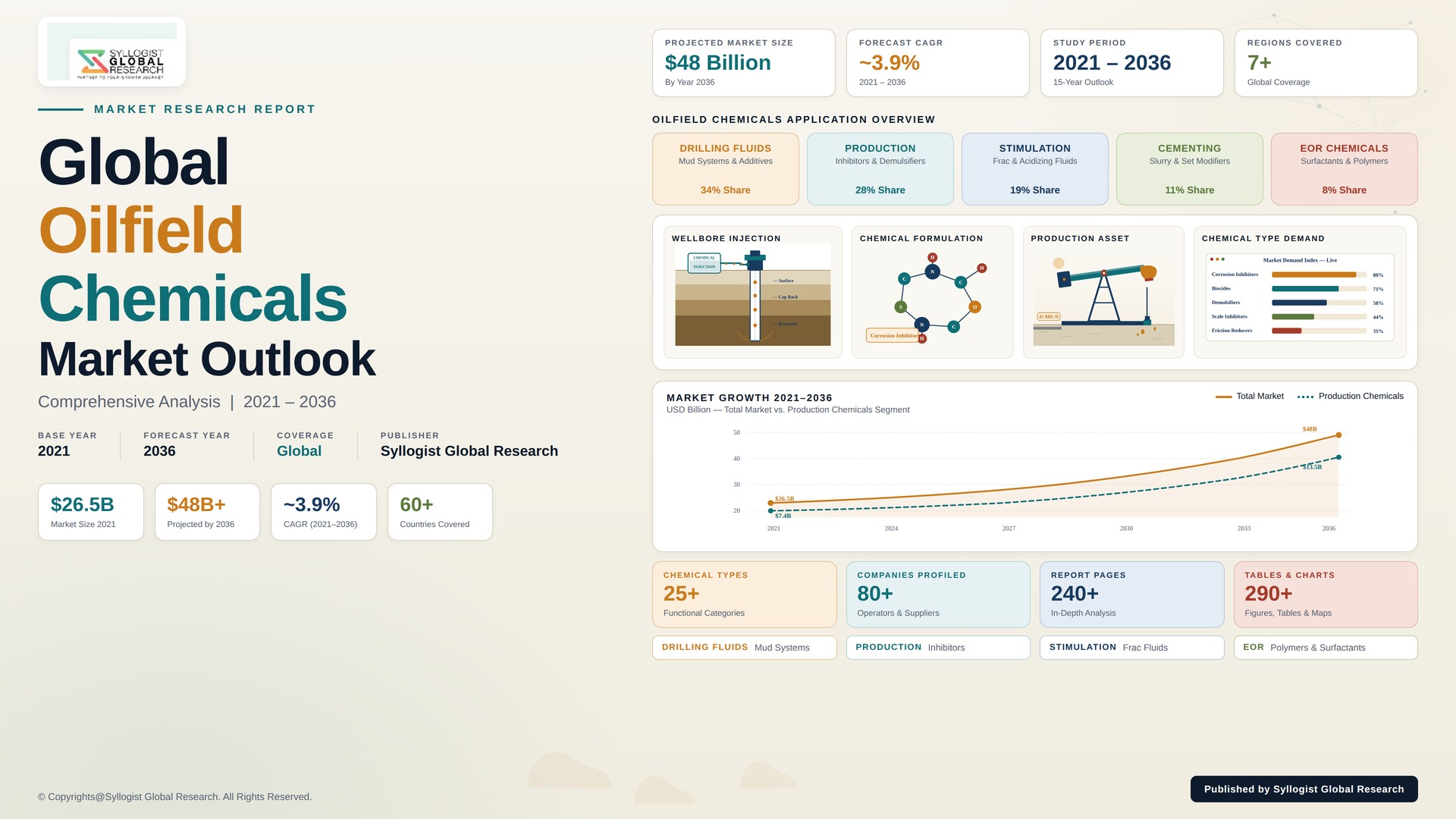

The global oilfield chemicals market is moving through a structural growth cycle propelled by intensifying upstream activity, deepening unconventional resource development, and an accelerating push toward extraction efficiency from mature producing assets, all of which compel operators to rely on specialty chemistries to sustain output, defend asset integrity, and meet evolving environmental compliance benchmarks. The market was valued at USD 33.4 billion in 2025 and is projected to reach USD 50.8 billion by 2034, advancing at a compound annual growth rate of 4.8% through the forecast window, supported by sustained drilling intensity in North American shale, large-scale enhanced oil recovery programs across the Middle East, Latin America, and Asia, and a growing volume of subsea and deepwater developments requiring high-performance flow assurance, corrosion management, and microbial control formulations across complex production systems globally.

Operational complexity is the strongest secular force redrawing the demand profile for oilfield chemicals, as operators increasingly drill longer horizontal laterals, exploit deeper and hotter reservoirs, and contend with progressively saline, sour, and high-pressure fluid environments that elevate the technical performance threshold required of every chemical injected into the wellbore or production stream. The result is a measurable shift in revenue mix from commodity bulk chemicals toward formulated specialty chemistries, including high-temperature corrosion inhibitors, sulfate-tolerant scale inhibitors, friction reducers engineered for high-salinity slickwater fracturing, multifunctional production chemistries, and polymer-surfactant blends optimized for tertiary recovery. Operators are simultaneously consolidating chemical supply under integrated production chemistry contracts that bundle treatment programs, real-time monitoring, automated dosing, and performance guarantees, restructuring procurement economics in favor of suppliers offering measurable production uplift and verifiable asset-integrity outcomes across the entire field lifecycle.

Within the product taxonomy, corrosion inhibitors and demulsifiers continue to anchor the highest revenue concentration owing to their indispensable role in preserving pipeline integrity and separating water from crude oil across virtually every production environment globally. Production chemicals collectively represent the fastest-growing application category, expanding at a rate exceeding 5% annually as aging fields require higher chemical intensity to maintain flow rates, manage rising water cuts, and limit equipment fouling. Enhanced oil recovery chemistries, particularly polyacrylamide-based polymers and tailored surfactants, are scaling rapidly in response to large polymer flood programs in China, the Middle East, and offshore Brazil, where high-salinity, high-temperature reservoir conditions demand advanced chemistries capable of withstanding extreme downhole environments. Digital dosing platforms, AI-driven injection optimization, and bio-based green oilfield chemistry portfolios are further reshaping competitive differentiation among integrated chemical service providers worldwide.

North America anchors the largest absolute revenue share of the global oilfield chemicals market, valued near USD 9.2 billion in 2025 and underpinned by sustained Permian Basin shale activity, Gulf of Mexico deepwater development, and expanding gas-directed drilling supporting LNG export capacity additions. The Middle East and Africa region holds a structurally critical share driven by sour-gas processing, brownfield enhanced oil recovery in Saudi Arabia, ADNOC offshore development in the United Arab Emirates, and growing pre-salt activity offshore West Africa. Asia-Pacific is positioned to record the highest forecast period CAGR, supported by polymer flooding investment in China, intensifying drilling activity in India, deepwater plays offshore Malaysia and Indonesia, and continued operator focus on extending production from mature field assets across the regional upstream footprint. Latin America, anchored by Brazilian pre-salt development and Argentine Vaca Muerta unconventional programs, contributes incremental specialty chemistry demand growth.

Key Drivers

Unconventional Resource Development and Shale Production Expansion Driving Sustained Demand for Specialized Drilling and Completion Chemistries

The global expansion of unconventional resource development across North American shale plays, Argentine Vaca Muerta, Chinese tight gas formations, and Middle Eastern unconventional reservoirs is generating durable demand for high-performance friction reducers, slickwater additives, biocides, and multifunctional fracturing chemistries engineered to operate in high-salinity, high-temperature downhole environments. Longer horizontal laterals and rising proppant intensity per stage are translating into increasing chemical consumption per well, sustaining elevated specialty chemistry demand across active onshore unconventional drilling programs globally.

Enhanced Oil Recovery Investment and Mature Field Optimization Programs Supporting Long-Cycle Specialty Polymer and Surfactant Demand

Large-scale enhanced oil recovery programs across China, the Middle East, Latin America, and Russia are channeling sustained investment into polymer-surfactant chemistries capable of mobilizing residual hydrocarbons in mature reservoirs, with operators deploying polyacrylamide polymer floods, alkali-surfactant-polymer blends, and CO2-tolerant chemistries to extend asset productivity. Steep decline curves in legacy fields are reinforcing operator commitment to chemically intensive tertiary recovery techniques, generating multi-year contracted demand visibility for specialty oilfield chemical suppliers serving brownfield optimization programs globally.

Asset Integrity Imperatives and Flow Assurance Requirements Across Subsea, Deepwater, and Aging Pipeline Infrastructure

The rising operational cost of unplanned downtime across subsea, deepwater, and aging pipeline infrastructure is anchoring multi-year procurement budgets for corrosion inhibitors, hydrogen sulfide scavengers, paraffin control agents, and asphaltene dispersants protecting production continuity across complex flow assurance environments. Operators increasingly treat chemical management as a core asset-integrity discipline rather than discretionary spending, supporting durable consumption of high-specification production chemistries across deepwater Gulf of Mexico, North Sea, West Africa, and Brazilian pre-salt developments.

Key Challenges

Tightening Environmental Regulations, Discharge Limits, and Sustainability Mandates Reshaping Chemical Formulation Economics

Tightening environmental regulations governing chemical discharge into marine and inland water bodies, combined with intensifying corporate sustainability commitments and operator-led decarbonization mandates, are forcing oilfield chemical suppliers to reformulate legacy product portfolios toward biodegradable, low-toxicity, and reduced-carbon-footprint chemistries while maintaining performance equivalence under demanding downhole conditions. Compliance with North Sea OSPAR rules, Gulf of Mexico discharge standards, and emerging Asia-Pacific environmental frameworks is elevating research and development costs and lengthening product qualification cycles industrywide.

Crude Oil Price Volatility and Capital Discipline Pressures Constraining Upstream Chemical Procurement Budgets

Persistent volatility in global crude oil benchmarks, combined with reinforced capital discipline among publicly listed exploration and production operators, is constraining flexibility in upstream chemical procurement budgets and intensifying price pressure on commodity chemical categories where differentiation is limited. Operators routinely defer non-essential chemical treatments, renegotiate supply contracts, and consolidate vendor relationships during downturn cycles, exposing chemical providers to revenue compression, margin erosion, and inventory imbalance risks across the broader oilfield service supply chain.

Raw Material Supply Chain Disruption and Feedstock Cost Inflation Affecting Specialty Chemical Production Economics

Supply chain disruptions affecting key petrochemical feedstocks, polymer intermediates, and specialty surfactant precursors are introducing material cost inflation, lengthening lead times, and elevating inventory carrying costs for oilfield chemical manufacturers serving global upstream customers. Geopolitical tension affecting trade routes, regional manufacturing concentration risks, and tightening logistics capacity in offshore-supply corridors are compounding procurement complexity, while ESG-driven scrutiny of feedstock sourcing further constrains supplier flexibility, pressuring formulation cost structures across both commodity and specialty oilfield chemistry portfolios.

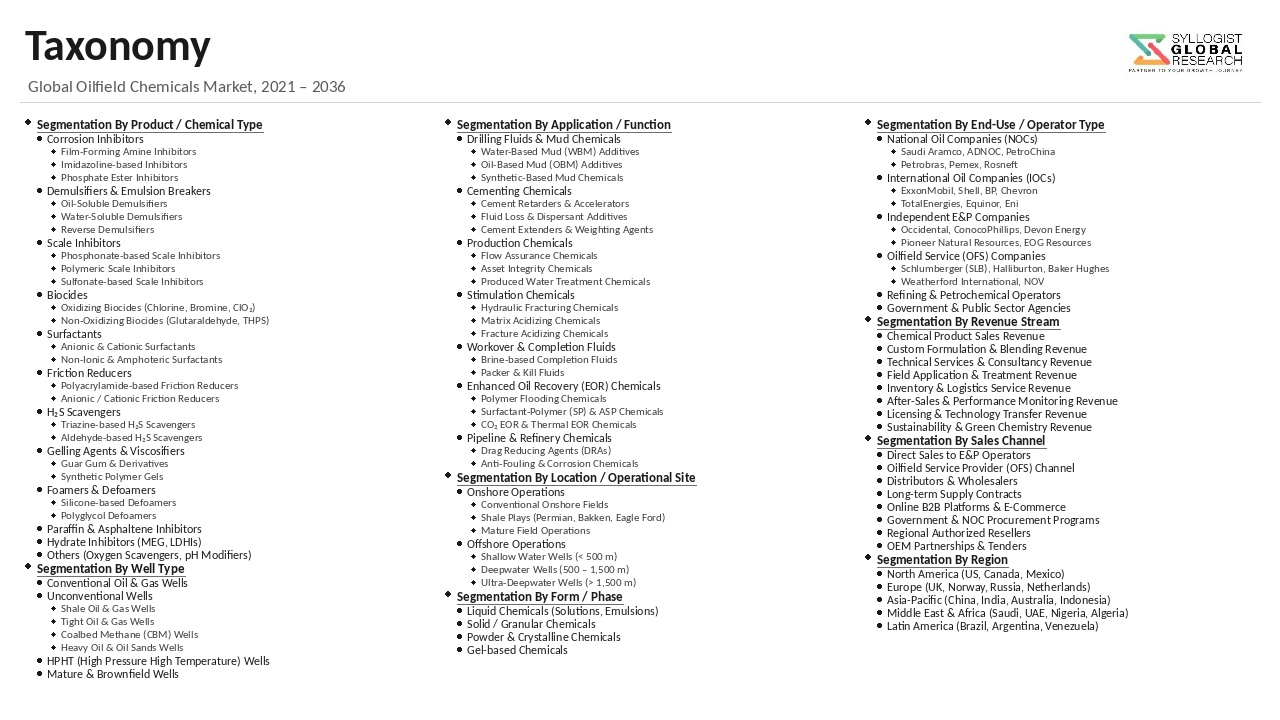

Market Segmentation

- Segmentation By Product Type

- Corrosion Inhibitors

- Scale Inhibitors

- Demulsifiers

- Biocides

- Surfactants

- Friction Reducers

- Polymers

- Hydrogen Sulfide Scavengers

- Paraffin and Asphaltene Inhibitors

- Cementing Additives

- Others

- Segmentation By Application

- Drilling Fluids

- Cementing

- Production Chemicals

- Well Stimulation and Hydraulic Fracturing

- Enhanced Oil Recovery (EOR)

- Workover and Completion

- Others

- Segmentation By Well Type

- Vertical Wells

- Directional Wells

- Horizontal Wells

- Multilateral Wells

- Segmentation By Location of Deployment

- Onshore

- Offshore (Shallow Water)

- Offshore (Deepwater and Ultra-Deepwater)

- Segmentation By Form

- Liquid

- Solid (Powder and Granules)

- Gas

- Segmentation By End User

- International Oil Companies (IOCs)

- National Oil Companies (NOCs)

- Independent Exploration and Production Operators

- Oilfield Service Companies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Oilfield Chemicals Market in 2025, projected through 2034, disaggregated by product type, application, and well architecture, enabling chemical manufacturers, oilfield service providers, investors, and procurement planners to identify highest-growth segments and most durable revenue opportunities across the upstream chemistry landscape?

- How are upstream operators across North America, the Middle East, Asia-Pacific, and Latin America allocating chemical procurement budgets across drilling, production, well stimulation, and enhanced oil recovery applications, and which national programs and basin-level activity benchmarks are defining global oilfield chemicals demand architecture through 2034?

- Which oilfield chemical product categories, including corrosion inhibitors, demulsifiers, friction reducers, biocides, surfactants, and polymers, are recording the highest forecast period growth rates, and what reservoir, regulatory, and operational performance factors are shaping demand intensity within each segment?

- How are environmental discharge regulations, ESG mandates, and decarbonization commitments reshaping the formulation, qualification, and commercial deployment of next-generation biodegradable, low-toxicity, and bio-based oilfield chemistries across offshore and onshore operating environments globally?

- What partnership, integration, acquisition, and digital chemical management strategies are dominant chemical service providers, integrated oilfield contractors, and specialty formulators using to consolidate market positions and deepen operator relationships across global upstream basins through the forecast horizon?

- Which regional markets, specifically Asia-Pacific, the Middle East and Africa, and Latin America, are expected to generate the most substantial incremental oilfield chemicals demand through 2034, and what unconventional resource development, deepwater exploration, and mature field optimization programs are anchoring procurement growth in each region?

- What raw material supply chain dynamics, petrochemical feedstock pricing trajectories, and logistics constraints are most critical to the operational performance and margin sustainability of oilfield chemical manufacturers serving global exploration and production customers across both commodity and specialty product categories?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil & Natural Gas Price Volatility & Upstream Capex Cycle Risk

- Petrochemical Feedstock, Raw Material Price & Specialty Active Ingredient Supply Risk

- Regulatory, Environmental Compliance, Toxicity Disclosure & Frac Fluid Reporting Risk

- Field Performance, Reservoir Compatibility, Well Integrity & Asset Damage Risk

- Geopolitical, Sanctions, Cross-Border Operations & License-to-Operate Risk

- Regulatory Framework & Standards

- National Upstream Petroleum Operations, Well Construction & Chemical Use Policy Frameworks

- REACH, TSCA & Globally Harmonised System (GHS) Chemical Registration, Hazard Classification & Disclosure Standards

- Discharge, Disposal, Produced Water Treatment & Offshore OSPAR/HOCNF Compliance Standards for Onshore and Offshore Operations

- Environmental Impact Assessment, Hydraulic Fracturing Fluid Disclosure (FracFocus) & Spill Response Regulations

- Green Chemistry, Bio-based Product Certification, ESG Disclosure & Sustainable Procurement Standards for Operators

- Global Oilfield Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilo Tons)

- Market Size & Forecast by Product Type

- Biocides (Glutaraldehyde, THPS, Quaternary Ammonium & Bronopol Based)

- Corrosion Inhibitors (Imidazolines, Quaternary Amines, Phosphate Esters & Film-Forming Amines)

- Scale Inhibitors (Phosphonates, Polyacrylates, Polymeric & Green Scale Inhibitors)

- Demulsifiers & Emulsion Breakers (Oxyalkylated Resins, Polyethers & Polyamines)

- Surfactants (Anionic, Cationic, Non-Ionic & Amphoteric)

- Polymers, Rheology Modifiers & Friction Reducers (Polyacrylamides, Xanthan Gum, Guar & Cellulose Derivatives)

- Foamers, Defoamers & Antifoam Agents

- Hydrate Inhibitors (Thermodynamic, Kinetic & Anti-Agglomerant)

- H2S Scavengers, Oxygen Scavengers & Mercury Removal Chemicals

- Acid Stimulation Additives, Cementing Additives & Specialty Oilfield Chemicals

- Market Size & Forecast by Application

- Drilling Fluid & Mud Chemicals

- Cementing & Well Construction Chemicals

- Well Stimulation Chemicals (Hydraulic Fracturing & Acidising)

- Production Chemicals (Flow Assurance, Asset Integrity & Separation)

- Workover & Completion Chemicals

- Enhanced Oil Recovery (EOR) Chemicals (Polymer, Surfactant & Alkali-Surfactant-Polymer Flooding)

- Market Size & Forecast by Well Location

- Onshore Conventional & Unconventional (Shale, Tight Oil and Tight Gas)

- Offshore Shallow Water (Up to 500 m)

- Offshore Deepwater (500 to 1,500 m)

- Offshore Ultra-Deepwater (Above 1,500 m)

- Market Size & Forecast by Reservoir Type

- Conventional Oil & Gas Reservoir

- Unconventional Shale Oil & Tight Gas Reservoir

- Heavy Oil, Oil Sands & Bitumen Reservoir

- High Temperature High Pressure (HTHP) & Sour (H2S/CO2 Bearing) Reservoir

- Market Size & Forecast by Well Type

- New Well (Drilling & Completion Phase)

- Existing Producing Well (Production & Workover Phase)

- Mature Field (Enhanced Oil Recovery & Late-Life Production)

- Market Size & Forecast by End-User

- International Oil Companies (IOCs)

- National Oil Companies (NOCs)

- Independent Exploration & Production (E&P) Companies

- Oilfield Service Companies & Specialty Chemical Distributors

- Market Size & Forecast by Sales Channel

- Direct Supply to Operators (Long-Term Supply Contract & Frame Agreement)

- Oilfield Service Bundled Chemical Programme (Integrated Service Contract)

- Distributor, Trading House & Regional Specialty Channel

- Tolling, Custom Manufacturing & Private Label Supply

- North America Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Product Type

- By Application

- By Well Location

- By Reservoir Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Product Type

- By Application

- By Well Location

- By Reservoir Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Product Type

- By Application

- By Well Location

- By Reservoir Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Product Type

- By Application

- By Well Location

- By Reservoir Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Product Type

- By Application

- By Well Location

- By Reservoir Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Oilfield Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Product Type

- By Application

- By Well Location

- By Reservoir Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Russia, China, Japan, India, Australia, South Korea, Indonesia, Malaysia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Qatar, Kuwait, Iraq, Egypt, Algeria, Nigeria, Angola

- Technology Landscape & Innovation Analysis

- Drilling Fluid Chemistry & High-Performance Water-Based Mud Technology Deep-Dive

- Hydraulic Fracturing Fluid System, Slickwater & Friction Reducer Technology

- Green & Bio-based Oilfield Chemistry, Low Toxicity Demulsifier & Biocide Technology

- Polymer Flooding, Surfactant-Polymer & Chemical Enhanced Oil Recovery Technology

- High Temperature High Pressure (HTHP) & Sour Service Inhibitor Chemistry

- Nanotechnology, Smart Tracer & Encapsulated Slow-Release Chemical Technology

- Digital Chemical Management, IoT Dosing & AI-Based Production Optimisation Platform Technology

- Patent & IP Landscape in Oilfield Chemicals Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock, Olefin & Specialty Monomer Supply Chain

- Specialty Chemical Manufacturing, Toll Blending & Formulation Plant Supply Chain

- Polymer, Surfactant & Active Ingredient Supplier Landscape for Oilfield Formulations

- Logistics, Bulk Storage, Tank Terminal & Last-Mile Wellsite Delivery Network

- Oilfield Service Company, Operator Procurement & Frame Agreement Landscape

- Distributor, Wellsite Service Provider & Field Engineer Channel

- Spent Chemical, Produced Water Treatment & Circular Economy

- Pricing Analysis

- Drilling Fluid & Mud Chemical Average Selling Price and Total Cost of Use Analysis

- Hydraulic Fracturing Chemical Cost per Treated Well & Cost per Stage Analysis

- Production Chemical Dosage-Based Pricing & Cost per Barrel of Oil Treated Analysis

- Specialty Chemical & Active Ingredient Raw Material Index Linked Pricing Analysis

- Long-Term Supply Contract, Integrated Service Programme & Performance-Based Pricing Analysis

- Total Oilfield Chemical Programme Economics: Cost per Barrel and Production Uplift Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Oilfield Chemical Programmes: Carbon Footprint, Toxicity & Biodegradability Across Product Routes

- Green Oilfield Chemistry & Pathway to Bio-based, Low Toxicity & Readily Biodegradable Product Portfolios

- Produced Water Treatment, Reuse & Closed-Loop Water Management Contribution of Specialty Chemical Programmes

- Environmental Compliance, Marine Discharge, Aquatic Ecosystem & Soil Impact Consideration in Offshore and Sensitive Onshore Basins

- Regulatory-Driven Sustainability, Methane and Flaring Reduction Alignment & Green Finance Eligibility of Operators

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Application & Geography

- Player Classification

- Integrated Oilfield Service Companies with In-House Chemical Programmes

- Specialty Oilfield Chemical Manufacturers & Pure-Play Producers

- Diversified Specialty & Industrial Chemical Companies with Oilfield Divisions

- Petrochemical Majors Supplying Active Ingredients & Base Polymers

- Regional & Local Oilfield Chemical Formulators

- Green & Bio-based Oilfield Chemistry Specialists

- Digital Chemical Management & IoT Dosing Platform Providers

- Distributors, Tolling Partners & Private Label Supply Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Oilfield Chemicals Products & Technology Portfolio

- Key Customer Relationships & Reference Field Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Oilfield Chemicals Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Product Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Application, Well Location, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)