Global Fuel Additives Market By Product Type, By Application, By End-Use Industry, By Form, By Distribution Channel, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Fuel Additives Market encompasses the formulation, manufacture, distribution, and end-use deployment of specialty chemical compounds blended into gasoline, diesel, aviation kerosene, marine bunker fuel, biofuels, and alternative fuel blends to enhance combustion efficiency, reduce harmful tailpipe and stack emissions, protect engine components, extend storage stability, and ensure compliance with progressively tightening fuel quality standards across automotive, aviation, marine, industrial, and power generation applications globally. Fuel additives include functional product categories such as deposit control additives, cetane improvers, octane boosters, lubricity improvers, cold flow improvers, stability improvers, antioxidants, corrosion inhibitors, anti-icing agents, metal deactivators, biocides, dyes, markers, and demulsifiers, each engineered to address specific fuel performance, equipment protection, or regulatory compliance objectives. End-use customers span integrated oil refiners, fuel terminal operators, retail fuel marketers, original equipment manufacturers, fleet operators, aviation jet fuel suppliers, marine bunker fuel providers, biofuel producers, and aftermarket consumer brands. The market addresses critical performance requirements including injector and intake valve cleanliness in modern direct-injection gasoline engines, particulate and nitrogen oxide reduction in compression ignition diesel engines, ultra-low sulfur diesel lubricity restoration, jet fuel thermal stability and anti-icing protection, marine residual fuel stability under low-sulfur regulatory regimes, and oxidation control in long-term fuel storage. Geographic deployment spans regulated mature markets governed by Euro 7, EPA Tier 3, and equivalent emission standards, alongside high-growth emerging economies upgrading domestic fuel quality benchmarks. Delivery models include refinery-injected additive packages, terminal-blended performance formulations, and consumer aftermarket products, establishing fuel additives as a foundational component within global combustion fuel value chains, transportation decarbonization pathways, and engine performance assurance frameworks across both established and emerging mobility ecosystems worldwide.

Market Insights

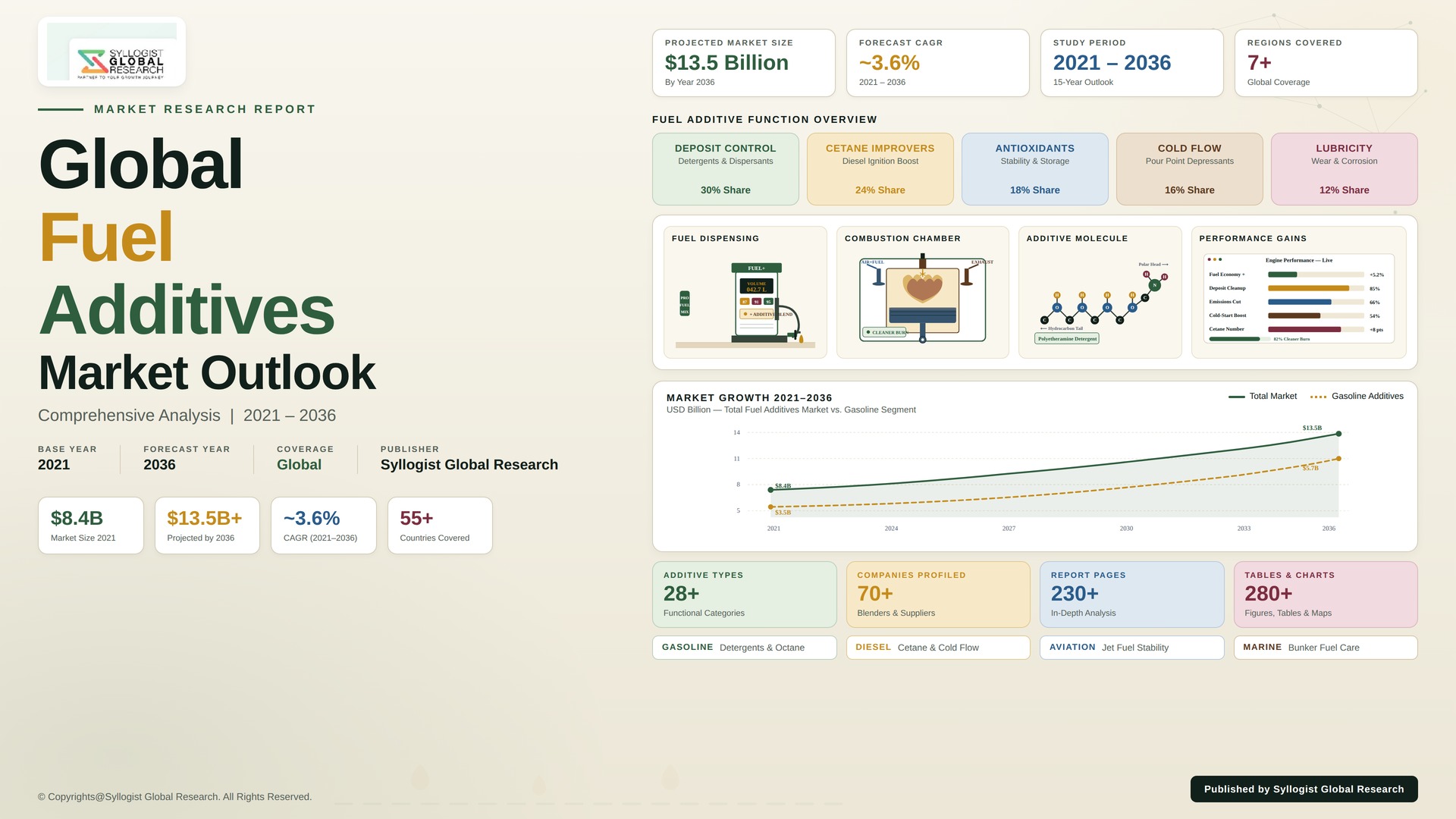

The global fuel additives market is moving through a structurally resilient growth phase shaped by tightening emission compliance regimes, rising fuel quality benchmarks, and durable demand from the world’s expanding internal combustion vehicle fleet, even as longer-term electrification trajectories begin to redirect investment within the broader transportation fuel ecosystem. The market was valued at USD 10.0 billion in 2025 and is projected to reach USD 16.5 billion by 2034, advancing at a compound annual growth rate of 5.4% through the forecast window, propelled by sustained gasoline and diesel demand in emerging Asian and African economies, ongoing aviation sector expansion driving jet fuel additive consumption, and progressively stringent global sulfur, particulate, and greenhouse gas emission rules that are systematically elevating per-liter additive intensity across the global refined fuel pool worldwide.

Engine technology evolution is the strongest secular force restructuring the demand profile for fuel additives, as automakers continue to deploy turbocharged direct-injection gasoline engines, high-efficiency modern diesel platforms, and gasoline particulate filter equipped powertrains, all of which place elevated performance demands on deposit control, lubricity, and detergency chemistries blended into the fuel stream. The result is a measurable shift in revenue mix from commodity cetane improvers and octane boosters toward formulated multifunctional additive packages incorporating advanced polyetheramine deposit control chemistries, friction modifiers, corrosion inhibitors, and combustion catalysts engineered to meet original equipment manufacturer keep-clean and clean-up performance protocols. Fuel marketers are simultaneously consolidating supply contracts under premium branded fuel programs, restructuring procurement economics in favor of suppliers offering measurable mileage uplift, emission reduction validation, and engine durability outcomes across the fuel value chain globally.

Within the product taxonomy, deposit control additives anchor the highest revenue concentration, capturing approximately 37% of total market revenue in 2025 owing to their indispensable role in maintaining injector and combustion chamber cleanliness across modern gasoline and diesel engines. Cetane improvers and lubricity additives represent the fastest-growing functional categories, supported respectively by widening diesel particulate compliance requirements and expanding ultra-low sulfur diesel adoption that strips natural lubricity from finished diesel fuel. Aviation fuel additives, including thermal stability improvers, anti-icing agents, and static dissipators, are scaling alongside global commercial aviation traffic recovery and military jet fuel demand, while marine fuel additives are gaining traction under post-IMO 2020 low-sulfur bunker fuel regimes. Bio-fuel-compatible stabilizer and antioxidant chemistries are emerging as a critical growth vertical as renewable diesel and biodiesel blend volumes expand globally.

North America anchors the largest absolute revenue share of the global fuel additives market, valued near USD 3.4 billion in 2025 and underpinned by stringent EPA Tier 3 emission rules, Top Tier gasoline programs, and large-scale ultra-low sulfur diesel consumption across heavy-duty trucking and rail freight applications. Europe represents a structurally critical share driven by Euro 7 emission compliance, advanced biodiesel blending mandates, and high-quality premium fuel demand across Germany, France, and the United Kingdom. Asia-Pacific is positioned to record the highest forecast period CAGR, supported by rapidly expanding vehicle parc in China and India, Bharat Stage VI and China 6 emission standards, growing jet fuel demand across regional aviation networks, and accelerating refinery capacity additions across Southeast Asia. The Middle East and Africa, alongside Latin America, contribute incremental demand growth driven by domestic fuel quality upgrade programs and expanding road and air transport infrastructure investment cycles.

Key Drivers

Tightening Global Emission Regulations and Fuel Quality Standards Driving Sustained Adoption of High-Performance Additive Packages

The progressive rollout of Euro 7, EPA Tier 3, China 6, and Bharat Stage VI emission standards, alongside global low-sulfur fuel mandates, is generating durable demand for advanced deposit control, lubricity, cetane, and combustion catalyst chemistries engineered to deliver measurable particulate, nitrogen oxide, and unburned hydrocarbon reductions while preserving engine durability under stringent regulatory test cycles. Refiners and original equipment manufacturers are progressively codifying additive performance into commercial fuel specifications, anchoring multi-year volume commitments across global gasoline, diesel, and jet fuel pools.

Rising Global Vehicle Parc, Aviation Traffic Recovery, and Marine Fuel Demand Sustaining Long-Cycle Additive Consumption

The expanding global vehicle fleet, sustained commercial aviation traffic growth, and resilient marine bunker fuel consumption are reinforcing structural demand for fuel additives across all major end-use applications worldwide. Emerging Asian, African, and Latin American economies continue adding millions of internal combustion passenger and commercial vehicles annually, while air travel and shipping volumes maintain upward trajectories that translate into expanding jet fuel and bunker fuel additive consumption, anchoring multi-decade demand visibility for fuel additive suppliers.

Engine Technology Advancement and Premium Fuel Differentiation Strategies Elevating Per-Liter Additive Intensity Across Branded Fuel Programs

The accelerating deployment of turbocharged direct-injection gasoline engines, high-pressure common-rail diesel platforms, and gasoline particulate filter equipped powertrains is elevating the technical performance threshold required of every liter of finished fuel, increasing per-liter additive treat rates across reference and premium branded fuel grades. Major retail fuel brands continue investing in differentiated performance fuel formulations leveraging proprietary additive packages, supporting durable margin and volume contributions for specialty additive suppliers across global fuel markets.

Key Challenges

Accelerating Vehicle Electrification and Powertrain Decarbonization Pressures Reshaping Long-Term Demand Trajectories for Gasoline and Diesel Additive Categories

Accelerating battery electric and fuel cell vehicle adoption across major automotive markets, combined with progressive internal combustion engine phase-out timelines announced across the European Union, United Kingdom, and several US states, is introducing structural uncertainty into long-term gasoline and diesel additive demand projections, particularly across passenger vehicle applications in mature regulated markets. Suppliers face a strategic imperative to reposition portfolios toward aviation, marine, heavy-duty trucking, off-road, and biofuel-compatible chemistries less exposed to passenger car electrification dynamics globally.

Volatile Petrochemical Feedstock Costs and Specialty Intermediate Supply Chain Disruption Pressuring Additive Manufacturer Margins

Persistent volatility across petrochemical feedstocks including ethylene oxide, isobutylene, naphtha derivatives, and specialty amine intermediates is introducing material cost inflation, lengthening procurement lead times, and elevating working capital requirements for fuel additive manufacturers serving global refiner and marketer customers. Geopolitical disruption affecting global trade routes, regional manufacturing concentration risks across key intermediate chemistries, and tightening logistics capacity are compounding procurement complexity, while ESG-driven scrutiny of feedstock sourcing constrains supplier flexibility across specialty additive portfolios.

Biofuel and Alternative Fuel Compatibility Complexity Driving Reformulation Costs and Performance Validation Burdens

Expanding biodiesel, renewable diesel, sustainable aviation fuel, and ethanol blending mandates are introducing fuel chemistry complexity that conventional additive packages were not engineered to address, creating reformulation and validation requirements spanning oxidative stability, water tolerance, microbial control, and material compatibility under prolonged storage. Suppliers must invest substantial research and development resources in renewable-fuel-compatible chemistries while securing ASTM, EN, and OEM-level performance certifications across multiplying biofuel blend permutations across diverse regional fuel pools globally.

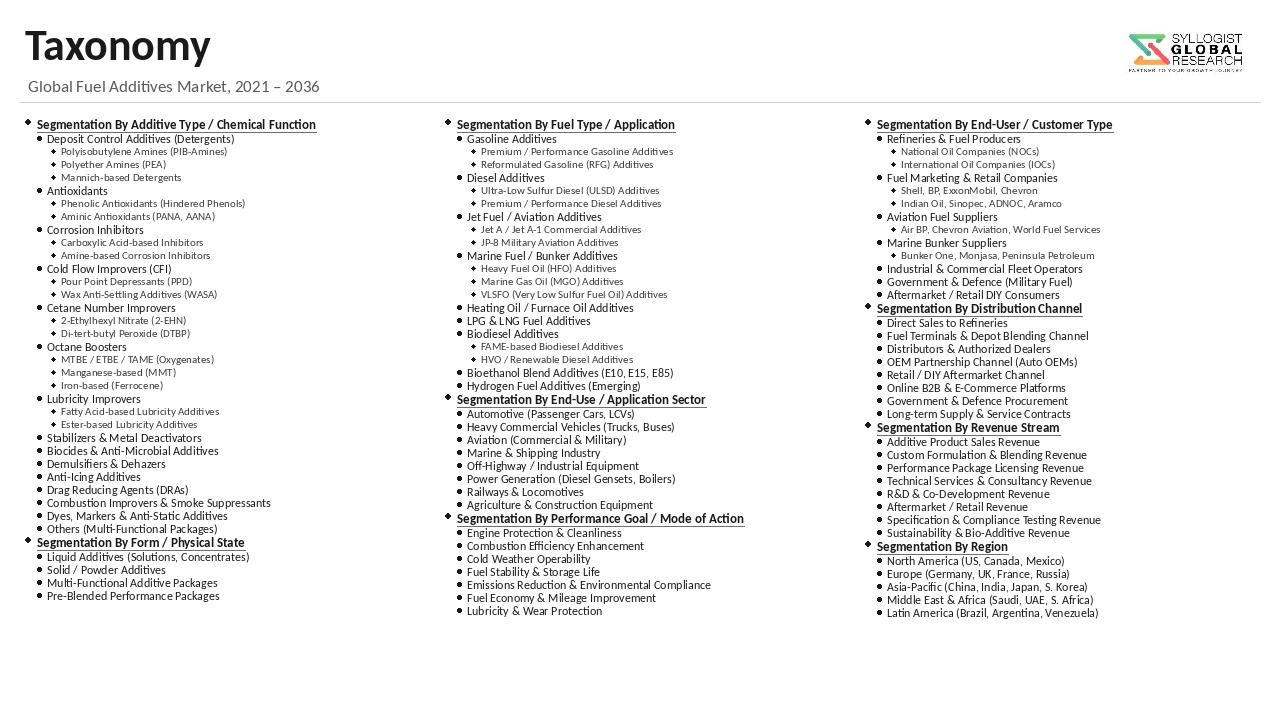

Market Segmentation

- Segmentation By Product Type

- Deposit Control Additives

- Cetane Improvers

- Octane Improvers

- Lubricity Improvers

- Cold Flow Improvers

- Stability Improvers

- Antioxidants

- Corrosion Inhibitors

- Anti-icing Additives

- Dyes and Markers

- Others

- Segmentation By Application

- Gasoline

- Diesel

- Aviation Fuel

- Marine Bunker Fuel

- Biofuels and Renewable Fuels

- Others

- Segmentation By End-Use Industry

- Automotive (Passenger Vehicles and Commercial Vehicles)

- Aviation

- Marine

- Industrial and Off-Road Equipment

- Power Generation

- Others

- Segmentation By Form

- Liquid

- Solid

- Segmentation By Distribution Channel

- Refinery and Terminal Blending

- Retail and Aftermarket Consumer Channels

- Direct Industrial Supply

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Fuel Additives Market in 2025, projected through 2034, disaggregated by product type, application, and end-use industry, enabling additive manufacturers, refiners, fuel marketers, and investors to identify highest-growth segments and most durable revenue opportunities across the global combustion fuel value chain?

- How are emission compliance regimes including Euro 7, EPA Tier 3, China 6, Bharat Stage VI, and IMO low-sulfur bunker fuel rules reshaping fuel additive consumption volumes across gasoline, diesel, aviation kerosene, and marine bunker fuel pools, and which national programs are setting the technical benchmarks shaping global additive demand architecture through 2034?

- Which fuel additive product categories, including deposit control additives, cetane improvers, lubricity improvers, cold flow improvers, octane improvers, and corrosion inhibitors, are recording the highest forecast period growth rates, and what engine technology, fuel quality standard, and regional regulatory factors are shaping demand intensity within each segment?

- How are major automotive electrification timelines, original equipment manufacturer commitments, and internal combustion engine phase-out roadmaps in the European Union, United Kingdom, and United States reshaping long-term demand trajectories for gasoline and diesel-specific additive categories across passenger vehicle and commercial vehicle applications?

- What partnership, vertical integration, and acquisition strategies are dominant fuel additive manufacturers using to consolidate market positions, secure feedstock continuity, and deepen relationships with refiners, fuel marketers, and OEM-branded performance fuel programs across global regions?

- Which regional markets, specifically Asia-Pacific, the Middle East and Africa, and Latin America, are expected to generate the most substantial incremental fuel additives demand through 2034, and what vehicle parc expansion, aviation traffic, and refinery capacity programs are anchoring procurement growth in each region?

- How are biodiesel, renewable diesel, sustainable aviation fuel, and ethanol blending mandates reshaping additive formulation requirements, oxidative stability protocols, and commercial deployment economics across renewable fuel value chains, and which suppliers are best positioned to capture incremental revenue from the global energy transition?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil and Refined Product Price Volatility & Refining Margin Cycle Risk

- Petrochemical Feedstock, Active Ingredient & Specialty Raw Material Price Volatility Risk

- Energy Transition, EV Adoption & Declining Gasoline and Diesel Demand Risk

- Tightening Fuel Specifications, Sulfur Limit & Additive Disclosure Regulation Risk

- Geopolitical, Sanctions, Trade & Cross-Border Supply Risk

- Regulatory Framework & Standards

- National Fuel Quality, Fuel Additive Registration and Use Policy Frameworks (US EPA Fuels and Fuel Additives Program & Equivalents)

- Tier 3, Euro VI/VII, Bharat Stage VI Vehicle Emission and Fuel Specification Standards

- ASTM D975, D4814, D1655 & Equivalent Fuel Performance, Quality and Stability Standards

- Renewable Fuel Standard (RFS), Renewable Energy Directive (RED III) & Biofuel Mandate Compliance Standards

- REACH, TSCA, GHS Chemical Registration & ESG Disclosure Standards for Fuel Additive Manufacturers and Marketers

- Global Fuel Additive Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilo Tons)

- Market Size & Forecast by Additive Type

- Deposit Control Additives & Detergents (Polyetheramine, Polyisobutylene Amine & Mannich Based)

- Cetane Number Improvers (2-Ethylhexyl Nitrate & Di-tert-Butyl Peroxide)

- Antioxidants & Stabilizers (Phenolic & Aminic)

- Corrosion Inhibitors

- Cold Flow Improvers & Pour Point Depressants

- Lubricity Improvers (Ester & Fatty Acid Based)

- Octane Enhancers (Ethers, Aromatic & Metallic)

- Anti-Icing, Anti-Static & Conductivity Improvers

- Biocides, Demulsifiers & Marker Dyes

- Multi-Functional & Specialty Additive Packages

- Market Size & Forecast by Fuel Type

- Gasoline (Motor Spirit including Premium and High-Octane Grades)

- Diesel (Ultra-Low Sulfur Diesel & Off-Road Diesel)

- Aviation Fuel (Jet A, Jet A-1 & Sustainable Aviation Fuel)

- Marine Fuel (VLSFO, MGO & Residual Fuel Oil)

- Heating Oil & Industrial Fuel

- Biofuel & Blended Fuel (Ethanol Blend, Biodiesel & Renewable Diesel)

- Market Size & Forecast by Application Phase

- Refinery & Terminal Additization

- Pipeline & Bulk Distribution Additization

- Aftermarket & Retail Consumer Additization

- Market Size & Forecast by Performance Function

- Performance & Fuel Economy Enhancement

- Emission Reduction & Combustion Improvement

- Storage Stability & Asset Protection

- Cold Weather Operability Improvement

- Fuel Marketing & Brand Differentiation Programmes

- Market Size & Forecast by Vehicle/End-Use Application

- Passenger Cars & Light-Duty Vehicles

- Heavy Commercial Vehicles & On-Highway Trucking

- Off-Highway, Construction & Agricultural Equipment

- Marine Engines & Shipping

- Aviation & Aerospace

- Power Generation & Stationary Engines

- Market Size & Forecast by End-User

- Refiners & Oil Marketing Companies (OMCs)

- Fuel Distributors, Terminal Operators & Blenders

- Fleet Operators (Commercial Trucking, Aviation & Marine Operators)

- Industrial & Power Generation End-Users

- Retail Consumers (Aftermarket Channel)

- Market Size & Forecast by Sales Channel

- Direct Supply to Refiners & Oil Marketing Companies (Long-Term Supply Contract)

- Distributor, Blender & Trading House Channel

- Specialty Additive Service Programme & Performance Contract

- Retail & Aftermarket Distribution Channel

- North America Fuel Additive Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Additive Type

- By Fuel Type

- By Application Phase

- By Performance Function

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Fuel Additive Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Additive Type

- By Fuel Type

- By Application Phase

- By Performance Function

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Fuel Additive Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Additive Type

- By Fuel Type

- By Application Phase

- By Performance Function

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Fuel Additive Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Additive Type

- By Fuel Type

- By Application Phase

- By Performance Function

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Fuel Additive Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Additive Type

- By Fuel Type

- By Application Phase

- By Performance Function

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Fuel Additive Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilo Tons)

- By Additive Type

- By Fuel Type

- By Application Phase

- By Performance Function

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Belgium, Poland, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Australia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Iran, Iraq, Egypt, Algeria, Nigeria, South Africa

- Technology Landscape & Innovation Analysis

- Polyetheramine (PEA) & Modern Direct Injection (DI) Gasoline Deposit Control Technology Deep-Dive

- Polyisobutylene Detergent, Mannich Chemistry & Carrier Oil Technology

- High-Performance Cold Flow Improver, Pour Point Depressant & Wax Anti-Settling Technology

- Cetane Number Improver, Combustion Catalyst & Diesel Smoke Suppressant Technology

- Bio-based, Renewable & Low Toxicity Fuel Additive Chemistry

- Multi-Functional Additive Package Formulation & Brand Differentiation Programme Technology

- Marine Fuel (VLSFO Stability) & Sustainable Aviation Fuel (SAF) Specialty Additive Technology

- Patent & IP Landscape in Fuel Additive Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock, Polyisobutylene, Amine & Specialty Monomer Supply Chain

- Specialty Active Ingredient (PEA, EHN, PPD, Phenolic Antioxidant) Manufacturing Supply Chain

- Additive Package Blending, Formulation & Custom Manufacturing Supply Chain

- Logistics, Bulk Storage, Tank Terminal & Refinery/Terminal Injection Service Network

- Refiner & Oil Marketing Company Procurement, Performance Trial & Long-Term Supply Agreement Landscape

- Distributor, Blender, Trading House & Aftermarket Retail Channel

- Spent Additive, Fuel Tank Sludge Management & Circular Economy

- Pricing Analysis

- Gasoline Deposit Control Additive Average Selling Price and Cost per Litre Analysis

- Diesel Cold Flow Improver, Lubricity Improver & Cetane Improver Cost per Litre Analysis

- Multifunctional Diesel Additive & Premium Performance Package Pricing Analysis

- Marine Fuel & Aviation Fuel Specialty Additive Pricing Analysis

- Long-Term Supply Contract, Performance-Based & Brand Programme Pricing Analysis

- Total Fuel Additive Programme Economics: Cost per Litre and Performance Uplift Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Fuel Additives: Carbon Footprint, Toxicity & Biodegradability Across Additive Routes

- Bio-based & Renewable Fuel Additive Pathway, Low Toxicity Chemistry & Circular Portfolios

- Tailpipe Emission, Particulate Matter & NOx Reduction Contribution of Modern Additive Programmes

- Environmental Compliance, Aquatic Toxicity & Air Quality Consideration in Fuel Additive Manufacturing and Usage

- Regulatory-Driven Sustainability, Decarbonisation Alignment & Green Finance Eligibility of Fuel Marketers

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Additive Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Additive Type, Fuel Type & Geography

- Player Classification

- Integrated Lubricant & Fuel Additive Companies with Full-Spectrum Portfolios

- Specialty Fuel Additive Manufacturers & Pure-Play Producers

- Diversified Specialty & Industrial Chemical Companies with Fuel Additive Divisions

- Petrochemical Majors Supplying Active Ingredients & Base Polymers

- Regional & Local Fuel Additive Formulators

- Bio-based & Renewable Fuel Additive Specialists

- Aftermarket & Consumer Fuel Additive Brands

- Distributors, Blenders, Tolling Partners & Custom Manufacturing Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Additive Type, Fuel Type & Region

- Company Profile

- Company Overview & Headquarters

- Fuel Additive Products & Technology Portfolio

- Key Customer Relationships & Reference Refinery / OMC Programmes

- Manufacturing Footprint & Production Capacity

- Revenue (Fuel Additive Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Additive Performance vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Additive Type, Fuel Type, Application Phase, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)