Global Epoxy Curing Agents Market By Curing Agent Type, By Cure Mechanism, By Application, By Form, By Technology, By End User Industry, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

Epoxy curing agents, also referred to as epoxy hardeners, are reactive chemical compounds that initiate and complete the cross-linking polymerization of epoxy resins to form thermoset polymer networks delivering specified mechanical strength, chemical resistance, thermal stability, electrical insulation, and adhesion performance across protective coatings, composites, adhesives, construction materials, and electronic encapsulation applications. The Global Epoxy Curing Agents Market encompasses the development, manufacturing, formulation, distribution, and application of aliphatic amines, cycloaliphatic amines, aromatic amines, polyamides, polyamidoamines, anhydrides, phenolic curing agents, mercaptans, dicyandiamide, imidazoles, and specialty curing agents engineered for ambient cure, heat cure, photo cure, and dual cure activation across regulated and non-regulated epoxy formulation applications globally.

The epoxy curing agents market includes solvent-based, waterborne, solvent-free, low-VOC, and bio-based curing agent formulations engineered for specified pot life, cure profile, glass transition temperature, mechanical performance, and environmental compliance characteristics across protective coatings, structural composites, electrical encapsulation, civil engineering grouts, adhesives, and sealants. Market participants include specialty chemical producers, formulators, contract manufacturers, distributors, and end-user industries spanning marine and industrial protective coatings, wind energy blade composites, automotive structural components, aerospace composites, electronics potting and encapsulation, construction flooring and overlays, civil infrastructure rehabilitation, and consumer electronics adhesives. The epoxy curing agents market also covers value-added services including custom formulation development, application engineering support, regulatory dossier preparation, and technical service support. The scope explicitly excludes epoxy base resins, reactive diluents, modifiers, and pigments supplied without curing functionality, focusing exclusively on the reactive hardener portion of the two-component epoxy system value chain globally.

Market Insights

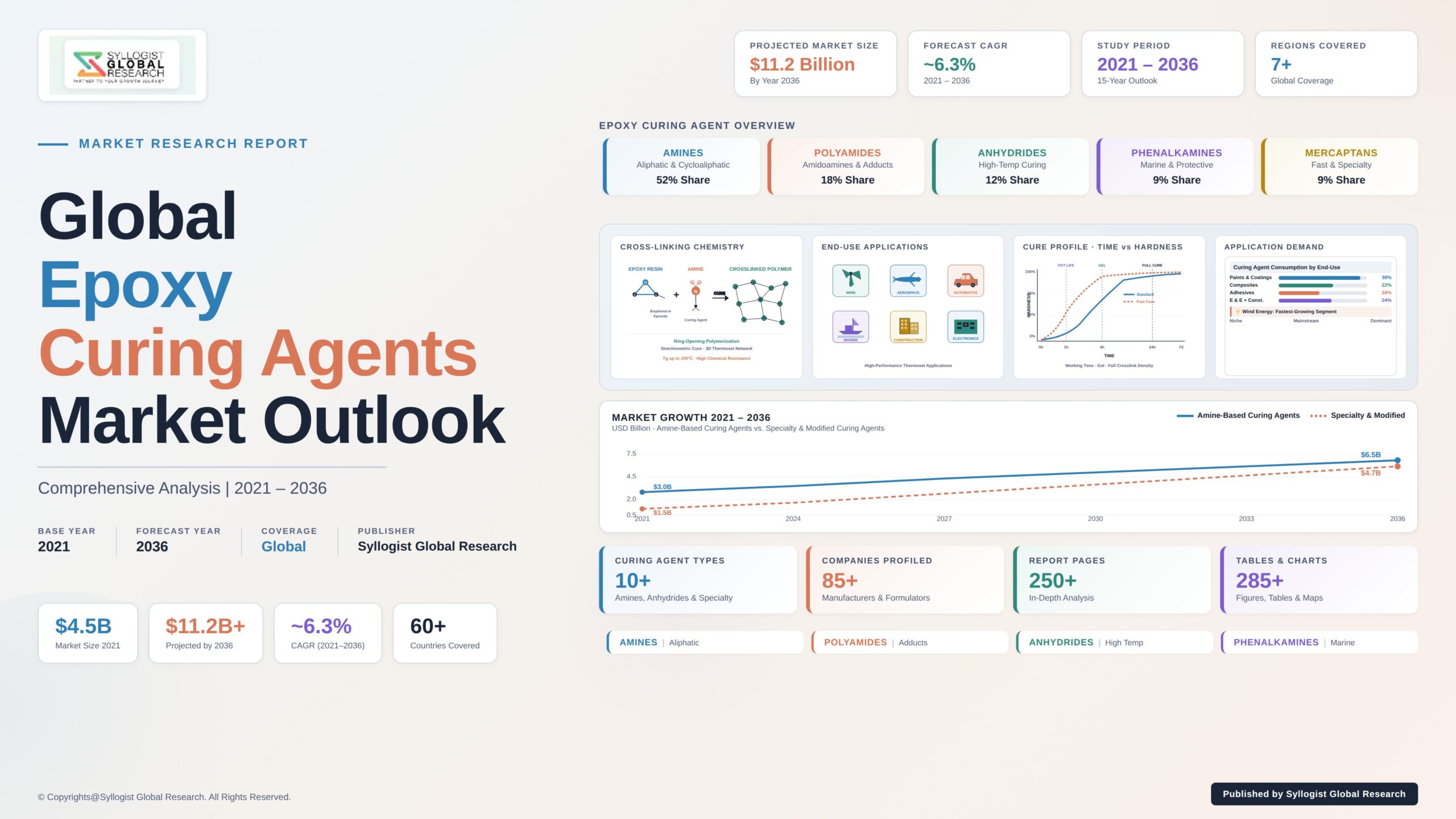

The global epoxy curing agents market is undergoing a structural expansion phase, shaped by sustained demand from wind energy blade composites manufacturing, accelerating electric vehicle structural composite procurement, expansion of marine and industrial protective coatings consumption, continued growth in construction and infrastructure rehabilitation applications, and tightening regulatory mandates favoring low-VOC, solvent-free, and bio-based curing agent formulations across mature operating regions. The epoxy curing agents market was valued at approximately USD 4.2 billion in 2025 and is projected to reach USD 7.1 billion by 2034, advancing at a compound annual growth rate of 6.0% through the forecast period, as paint and coating manufacturers, composite fabricators, adhesive formulators, electronic encapsulation operators, and construction product manufacturers scale epoxy curing agent procurement across mature and emerging operating regions globally.

The epoxy curing agents market trajectory is being reshaped by the structural shift toward waterborne, low-VOC, and bio-based formulations driven by tightening volatile organic compound emission regulations across mature operating regions, the commercial maturation of bio-derived polyamine and polyamidoamine curing agents sourced from renewable feedstocks, and the deployment of latent curing agents engineered for single-component epoxy systems delivering improved storage stability and simplified field application. Waterborne and solvent-free epoxy curing agent formulations accounted for over 45% of new product launches across the epoxy curing agents market in 2024, propelled by REACH, EPA, and California Air Resources Board emission limits constraining solvent-based formulation availability. Bio-based curing agents derived from cardanol, fatty amine chemistries, and lignin-derived precursors have entered commercial production at meaningful scale, supporting sustainability and circular economy procurement targets among major coating, composite, and adhesive customers within the epoxy curing agents market.

Aliphatic amines and modified aliphatic amine curing agents represent the largest curing agent type segment within the epoxy curing agents market, propelled by sustained demand from ambient-cure protective coatings, civil infrastructure applications, and general-purpose adhesive formulations requiring rapid cure profiles and consistent performance characteristics at moderate temperatures. Polyamidoamines and polyamides represent the second largest curing agent type segment within the epoxy curing agents market, supported by marine coating, industrial maintenance coating, and flexible adhesive applications requiring extended pot life and improved film flexibility. Paints and coatings represent the largest application segment within the epoxy curing agents market, fueled by sustained demand from protective coatings, industrial maintenance, marine coatings, and floor coating applications globally. Wind energy composites represent the fastest-growing application segment within the epoxy curing agents market, propelled by accelerating onshore and offshore wind turbine installation, blade size increases driving higher epoxy and curing agent consumption per blade, and structural epoxy composite procurement supporting electric vehicle lightweighting initiatives.

Asia-Pacific represents the largest regional market within the epoxy curing agents market, anchored by substantial epoxy curing agent consumption across protective coatings, composites, adhesives, and electronics applications in China, India, Japan, South Korea, and Vietnam, supported by extensive manufacturing infrastructure, sustained construction activity, and expanding wind energy capacity additions. China hosts the largest concentration of epoxy curing agent consumption globally, propelled by sustained wind turbine blade manufacturing, electronics production, marine coating consumption, and infrastructure investment. North America represents the second largest regional position within the epoxy curing agents market, supported by mature aerospace composite production, sustained oil and gas pipeline coating consumption, and accelerating electric vehicle composite procurement. Europe occupies the third major regional position within the epoxy curing agents market, shaped by REACH regulation driving low-VOC formulation procurement preference, extensive wind energy blade manufacturing capacity in Denmark, Germany, and Spain, and sustained automotive structural composite consumption across major automotive operating regions.

Key Drivers

Wind Energy Blade Composite Manufacturing Expansion, Offshore Wind Capacity Buildout, and Larger Blade Geometry Driving Sustained Epoxy Curing Agents Procurement

The structural expansion of global wind energy capacity, sustained acceleration of offshore wind project commissioning, and progressive scaling of wind turbine blade geometries are driving sustained procurement of structural epoxy curing agents within the epoxy curing agents market across major blade manufacturing operating regions. Global cumulative wind power capacity exceeded 1,000 gigawatts in 2025, with annual installations projected to scale at compound annual rates above 8% through 2030 as nations pursue energy transition commitments, decarbonization mandates, and renewable portfolio expansion targets. Offshore wind project commissioning is accelerating substantially, with offshore turbine blade lengths progressively expanding beyond 100 meters and consuming over 6 to 12 tonnes of epoxy resin and curing agent combined per blade, generating sustained per-blade epoxy curing agents procurement intensity within the epoxy curing agents market. Blade manufacturing capacity expansion across China, India, Vietnam, Germany, Spain, Denmark, Turkey, the United States, and Brazil is driving sustained multi-year supply agreements between blade manufacturers and epoxy system suppliers. Major epoxy system suppliers are structuring multi-year capacity commitment agreements aligning curing agent supply with blade manufacturer capacity expansion timelines, generating durable revenue commitments that anchor specialty chemical producer capacity scaling decisions across the epoxy curing agents market value chain globally.

Marine, Industrial, and Pipeline Protective Coating Procurement, Asset Integrity Investment, and Anticorrosion Specification Driving Epoxy Curing Agent Demand

Sustained marine coating consumption, industrial maintenance protective coating procurement, oil and gas pipeline coating expansion, and tightening asset integrity specification standards are driving sustained procurement of epoxy curing agents within the epoxy curing agents market across protective coatings applications globally. Global protective coatings consumption exceeded 7 million tonnes annually in 2025, with epoxy-based protective coatings representing over 35% of total protective coatings volume by tonnage, supported by sustained marine vessel coating, offshore platform protection, pipeline coating, and industrial maintenance demand. Marine vessel coating procurement has scaled sustainably following the recovery of global shipbuilding activity in China, South Korea, and Japan, with deepwater hull coating, ballast tank coating, and superstructure coating applications requiring high-performance epoxy curing agent formulations supporting extended service life within the epoxy curing agents market. Oil and gas pipeline coating procurement, supported by sustained infrastructure investment across North America, the Middle East, and select Asia-Pacific operating regions, continues to drive sustained demand for high-performance fusion-bonded epoxy and liquid epoxy curing agent formulations. Asset integrity specification standards including NORSOK M-501, ISO 12944, and corporate maintenance frameworks are reinforcing procurement preference for high-performance epoxy curing agent formulations across critical infrastructure and industrial maintenance applications globally.

Tightening VOC Emission Regulations, Sustainability Procurement Mandates, and Bio-Based Curing Agent Commercialization Driving Reformulation Procurement

The tightening of volatile organic compound (VOC) emission regulations across major operating regions, expanding corporate sustainability procurement mandates, and accelerating commercialization of bio-based epoxy curing agents are collectively driving sustained reformulation procurement within the epoxy curing agents market across paint and coating, composite, and adhesive formulators globally. The European Union REACH regulation, United States Environmental Protection Agency National Volatile Organic Compound Emission Standards, California Air Resources Board limits, and emerging Asian VOC regulation frameworks are progressively constraining solvent-based formulation availability, generating procurement preference toward waterborne, solvent-free, and low-VOC epoxy curing agent formulations within the epoxy curing agents market. Corporate sustainability procurement mandates from major coatings, composite, and adhesive customers are reinforcing procurement preference for bio-based epoxy curing agents sourced from cardanol, fatty amine chemistries, lignin-derived precursors, and other renewable feedstocks, with bio-based formulations growing at compound annual rates exceeding 12% across the epoxy curing agents market. Specialty chemical producers are structuring multi-year reformulation programs aligning bio-based curing agent commercialization with customer reformulation timelines, generating long-duration revenue commitments that anchor bio-based curing agent capacity scaling decisions and reinforce continued investment in renewable feedstock production capacity across the epoxy curing agents market value chain.

Key Challenges

Raw Material Cost Volatility, Petrochemical Feedstock Price Fluctuations, and Margin Pressure Across Epoxy Curing Agent Producers

The epoxy curing agents market continues to face material raw material cost volatility, sustained petrochemical feedstock price fluctuations, and persistent margin pressure across producers supplying aliphatic amine, polyamide, polyamidoamine, anhydride, and specialty curing agent products to global epoxy formulation customers. Raw material costs including ethylene oxide, propylene oxide, dimer acid, phthalic anhydride, and specialty amine intermediates experienced sustained price increases of 15% to 35% between 2021 and 2024, generating substantial margin pressure across the epoxy curing agents market and complicating long-term pricing commitments to formulator customers. Petrochemical feedstock price fluctuations driven by crude oil price volatility, natural gas pricing variability, and disruptions to global petrochemical supply chains affecting key raw material availability continue to generate margin uncertainty for epoxy curing agent producers planning multi-year capacity investments and customer supply commitments. Specialty intermediate sourcing complexity for niche curing agent variants including hindered amine, cycloaliphatic amine, and specialty polyamidoamine variants adds further supply chain risk, with limited global production capacity for select intermediates generating supply concentration risk and elevated supplier negotiation leverage. The combined effect of raw material cost volatility, petrochemical feedstock fluctuations, and intermediate sourcing complexity continues to constrain margin stability and complicate strategic capital deployment decisions within the epoxy curing agents market across global operating regions.

Hazard Classification, Regulatory Compliance Complexity, and Skin Sensitization Concerns Constraining Application Expansion for Amine-Based Curing Agents

Amine-based epoxy curing agents continue to face material hazard classification, regulatory compliance complexity, and persistent skin sensitization concerns that collectively constrain application expansion and require sustained reformulation investment within the epoxy curing agents market across global operating regions. Aliphatic amines, aromatic amines, and select polyamine curing agents are classified under European Union Classification, Labelling and Packaging (CLP) regulation as skin sensitizers, eye irritants, and in select cases as suspected reproductive toxicants, generating handling complexity, occupational exposure compliance burdens, and labeling requirements that constrain end-user application breadth within the epoxy curing agents market. Skin sensitization concerns affecting field application of two-component epoxy systems containing amine curing agents continue to limit applicability across consumer-facing, do-it-yourself, and uncontrolled application environments where occupational safety controls cannot be reliably enforced. Regulatory compliance complexity governing classification, labeling, occupational exposure limits, and end-user safety data sheet requirements varies materially across the European Union REACH, United States Toxic Substances Control Act, China Catalogue of Hazardous Chemicals, and emerging Asia-Pacific chemical management frameworks, requiring epoxy curing agent producers to maintain region-specific regulatory dossiers, packaging configurations, and end-user communication materials. The combined effect of hazard classification, regulatory compliance complexity, and sensitization concerns continues to constrain commercial application expansion for amine-based curing agents within the epoxy curing agents market value chain.

Competitive Pricing Pressure from Polyurethane and Polyaspartic Alternatives, Application-Specific Performance Trade-Offs, and Substrate Compatibility Constraints

The epoxy curing agents market continues to face competitive pricing pressure from substitute resin systems including polyurethane, polyaspartic, and acrylic-based coating and adhesive technologies, with application-specific performance trade-offs and substrate compatibility constraints affecting epoxy adoption in select coating and composite applications. Polyurethane and polyaspartic coating systems offer rapid cure profiles, ultraviolet stability superior to standard epoxy systems, and competitive economics that have generated material substitution pressure within marine, industrial, and infrastructure coating applications historically dominated by epoxy curing agents within the epoxy curing agents market. Application-specific performance trade-offs including limited ultraviolet light stability of amine-cured epoxy systems, chalking susceptibility in exterior weathering applications, and inferior color stability compared with polyurethane alternatives continue to constrain epoxy curing agent procurement in select coating applications requiring sustained aesthetic performance. Substrate compatibility constraints including limited adhesion to polyolefin substrates, sensitivity to substrate moisture content during application, and constrained performance over flexible substrates further limit epoxy curing agents adoption in select adhesive and coating applications. Specialty chemical producers are responding through development of modified curing agent formulations, hybrid resin technology partnerships, and dedicated application engineering support, but continued competitive pressure from substitute resin systems constrains market expansion opportunities across the epoxy curing agents market value chain.

Market Segmentation

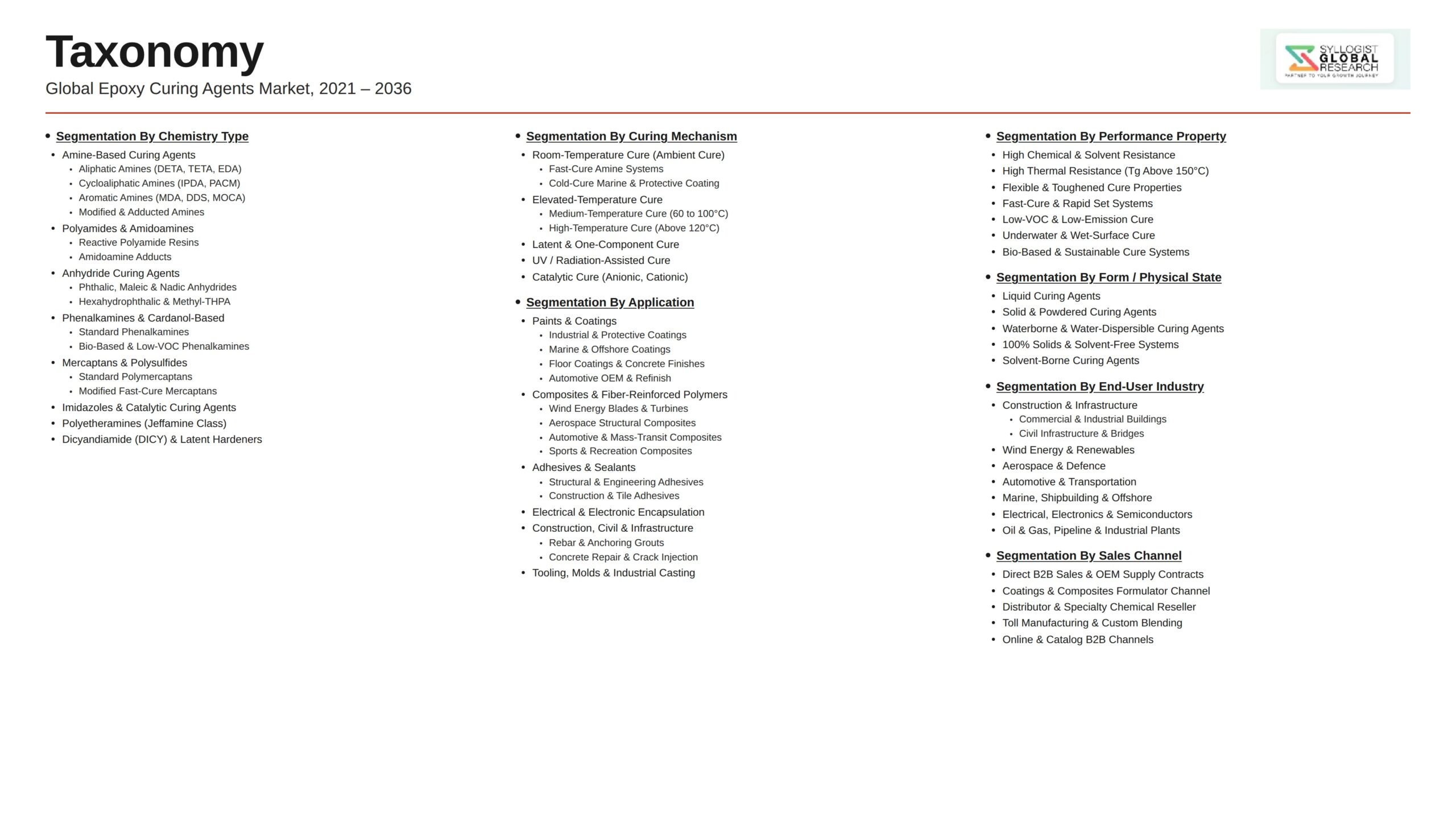

- Segmentation By Curing Agent Type

- Aliphatic Amines

- Cycloaliphatic Amines

- Aromatic Amines

- Polyamides

- Polyamidoamines

- Anhydrides

- Phenolic Curing Agents

- Mercaptans and Polysulfides

- Dicyandiamide and Imidazoles

- Specialty and Other Curing Agents

- Segmentation By Cure Mechanism

- Ambient Cure

- Heat Cure (Thermal Cure)

- Photo Cure (UV/Light Activated)

- Dual Cure Systems

- Segmentation By Application

- Paints and Coatings (Protective, Marine, Industrial)

- Composites (Wind Energy, Automotive, Aerospace, Marine)

- Adhesives and Sealants

- Construction Materials (Flooring, Grouts, Overlays)

- Electrical and Electronic Encapsulation

- Civil Infrastructure Rehabilitation

- Others

- Segmentation By Form

- Liquid Curing Agents

- Solid Curing Agents (Powder and Pellet)

- Pre-Accelerated Formulations

- Others

- Segmentation By Technology

- Solvent-Based Formulations

- Waterborne Formulations

- Solvent-Free and 100% Solids Formulations

- Low-VOC and Compliant Formulations

- Bio-Based and Renewable Formulations

- Segmentation By End User Industry

- Paints and Coatings Manufacturers

- Wind Energy Composite Manufacturers

- Automotive and Transportation

- Aerospace and Defense

- Marine and Shipbuilding

- Construction and Infrastructure

- Oil and Gas

- Electrical and Electronics

- Adhesive and Sealant Formulators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Epoxy Curing Agents Market in 2025, projected through 2034, segmented by curing agent type, cure mechanism, application, and form, enabling specialty chemical producers, formulators, distributors, and end-user industry procurement teams to identify highest-growth segments and most durable revenue opportunities across the epoxy curing agents landscape?

- How are paint and coating manufacturers, composite fabricators, adhesive formulators, electronic encapsulation operators, and construction product manufacturers structuring procurement frameworks for epoxy curing agents, and which commercial models, including spot purchase, multi-year supply agreements, custom curing agent development partnerships, and toll manufacturing arrangements, are shaping commercial deployment economics within the epoxy curing agents market through 2034?

- What volatile organic compound emission regulations, sustainability procurement mandates, and bio-based curing agent commercialization dynamics are reshaping reformulation timelines for solvent-based, waterborne, and bio-based epoxy curing agent technologies across mature regulatory jurisdictions?

- Which curing agent types, including aliphatic amines, cycloaliphatic amines, aromatic amines, polyamides, polyamidoamines, anhydrides, phenolics, mercaptans, dicyandiamide, and specialty curing agents, are gaining the strongest procurement traction across protective coatings, wind composites, electronics, and construction applications, and what cure profile, performance, and total cost of ownership metrics are shaping technology selection?

- How is the competitive landscape structured among established specialty chemical producers, formulators, contract manufacturers, distributors, and emerging bio-based curing agent developers within the epoxy curing agents market, and what partnership, acquisition, and platform expansion strategies are enabling new entrants to compete against incumbent epoxy curing agent producers?

- What wind energy blade manufacturing expansion, electric vehicle structural composite procurement, pipeline coating investment, and infrastructure rehabilitation trends are reshaping epoxy curing agent application engineering, capacity planning, and customer technical support expectations across the epoxy curing agents market globally?

- Which regional markets, including Asia-Pacific, North America, and Europe, are projected to generate the largest incremental epoxy curing agents procurement opportunities through 2034, and what regulatory, application diversity, sustainability mandate, and industrial activity factors are shaping capability investment priorities and supplier selection decisions in each regional epoxy curing agents market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility, Petrochemical Feedstock & Specialty Amine Sourcing Risk

- Wind Energy Project Cycle Volatility, OEM Production Schedule & Blade Manufacturing Capacity Risk

- Regulatory Restriction on Conventional Amines, REACH SVHC Designation & Hazardous Substance Reformulation Risk

- Customer-Specific Formulation Qualification, Long Approval Timeline & Substitution Switching Cost Risk

- Bio-Based Alternative Substitution, Sustainable Coating Specification & Specialty Bio-Curing Agent Investment Risk

- Regulatory Framework & Standards

- REACH Registration, SVHC Designation & EU Chemical Authorisation Frameworks

- US Toxic Substances Control Act (TSCA), EPA Chemical Compliance & Hazardous Substance Reporting Standards

- Globally Harmonised System (GHS), Hazard Communication & Workplace Safety Compliance

- Volatile Organic Compound (VOC) Restriction, Air Quality & Low-VOC Coating Procurement Standards

- Sustainability, Bio-Based Content Certification & Green Chemistry Procurement Standards

- Global Epoxy Curing Agents Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Curing Agent Consumption in Kilotonnes and Number of Active Manufacturing Facilities)

- Market Size & Forecast by Curing Agent Type

- Amine-Based (Aliphatic, Cycloaliphatic, Aromatic, Modified Amines)

- Anhydride-Based

- Polyamide-Based

- Phenolic-Based

- Polythiol-Based

- Isocyanate-Based

- Imidazole-Based

- Latent Hardeners

- Others

- Market Size & Forecast by Chemistry

- Amine Chemistry

- Anhydride Chemistry

- Polyamide Chemistry

- Phenolic Chemistry

- Mercaptan Chemistry

- Others

- Market Size & Forecast by Application

- Coatings (Industrial, Marine, Protective)

- Construction (Adhesives, Flooring, Composites)

- Composites (Wind Energy, Aerospace, Automotive)

- Electrical and Electronics (Encapsulants, Potting Compounds)

- Adhesives and Sealants

- Wind Energy Blade Manufacturing

- Pipeline Lining and Corrosion Protection

- Others

- Market Size & Forecast by Form

- Liquid

- Solid Powder

- Solid Flake

- Others

- Market Size & Forecast by Curing Temperature

- Ambient and Room-Temperature Cured

- Heat-Cured

- Latent (Heat-Activated)

- Market Size & Forecast by Reaction Speed and Pot Life

- Fast-Cure

- Standard-Cure

- Slow-Cure

- Latent Long-Pot-Life Systems

- Market Size & Forecast by Functionality

- Two-Component (2K) Systems

- One-Component (1K) Systems

- Market Size & Forecast by End-User

- Construction

- Automotive

- Aerospace

- Marine

- Electronics and Electrical

- Industrial Manufacturing

- Wind Energy

- Others

- Market Size & Forecast by Sales Channel

- Direct Manufacturer-to-Customer Supply Contracts

- Specialty Chemical Distributor & Trader Channel

- Custom Formulation & Joint Development Partnerships

- Licensed Production & Contract Manufacturing Arrangements

- Aftermarket Technical Service & Application Engineering Contracts

- North America Epoxy Curing Agents Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Curing Agent Consumption in Kilotonnes and Number of Active Manufacturing Facilities)

- By Curing Agent Type

- By Chemistry

- By Application

- By Form

- By Curing Temperature

- By Reaction Speed and Pot Life

- By Functionality

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Epoxy Curing Agents Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Curing Agent Consumption in Kilotonnes and Number of Active Manufacturing Facilities)

- By Curing Agent Type

- By Chemistry

- By Application

- By Form

- By Curing Temperature

- By Reaction Speed and Pot Life

- By Functionality

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Epoxy Curing Agents Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Curing Agent Consumption in Kilotonnes and Number of Active Manufacturing Facilities)

- By Curing Agent Type

- By Chemistry

- By Application

- By Form

- By Curing Temperature

- By Reaction Speed and Pot Life

- By Functionality

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Epoxy Curing Agents Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Curing Agent Consumption in Kilotonnes and Number of Active Manufacturing Facilities)

- By Curing Agent Type

- By Chemistry

- By Application

- By Form

- By Curing Temperature

- By Reaction Speed and Pot Life

- By Functionality

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Epoxy Curing Agents Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Curing Agent Consumption in Kilotonnes and Number of Active Manufacturing Facilities)

- By Curing Agent Type

- By Chemistry

- By Application

- By Form

- By Curing Temperature

- By Reaction Speed and Pot Life

- By Functionality

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Epoxy Curing Agents Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Curing Agent Consumption in Kilotonnes and Number of Active Manufacturing Facilities)

- By Curing Agent Type

- By Chemistry

- By Application

- By Form

- By Curing Temperature

- By Reaction Speed and Pot Life

- By Functionality

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Cycloaliphatic Amine, Modified Amine & Specialty Aliphatic Amine Curing Agent Technology Deep-Dive

- Bio-Based, Renewable Feedstock & Sustainable Curing Agent Technology

- Latent Hardener, One-Component Epoxy & Heat-Activated Curing Technology

- Low-Emission, Low-VOC & Solvent-Free Curing Agent Technology

- Phenalkamine, Phenolic-Modified & Marine Coating Curing Agent Technology

- Polyamide, Polythiol & Specialty Curing Chemistry Technology

- High-Temperature Resistance, Composite & Aerospace-Grade Curing Agent Technology

- Patent & IP Landscape in Epoxy Curing Agents Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock (Ammonia, Ethylene Oxide, Propylene Oxide) Supply Chain

- Specialty Amine, Anhydride & Hardener Intermediate Supply Chain

- Bio-Based Feedstock & Renewable Source Material Supply Chain

- Curing Agent Formulation, Blending & Specialty Compounding Supply Chain

- Distributor, Specialty Chemical Trader & Regional Channel Partner Network

- End-User Industry (Coatings, Construction, Composites, Wind Energy, Electronics) Procurement Landscape

- Aftermarket, Application Engineering & Technical Service Network

- Pricing Analysis

- Aliphatic Amine Curing Agent Pricing Analysis

- Cycloaliphatic Amine Curing Agent Pricing Analysis

- Aromatic Amine & Modified Amine Curing Agent Pricing Analysis

- Anhydride, Polyamide & Phenolic Curing Agent Pricing Analysis

- Polythiol, Imidazole & Specialty Curing Agent Pricing Analysis

- Per Kilogram Curing Agent Pricing Benchmark Analysis Across Standard, Specialty & Bio-Based Grades

- Total Cost of Curing Agent Application: Dosage Economics, Pot Life Trade-Offs & Cured System Performance Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Epoxy Curing Agents Across Petrochemical and Bio-Based Production Pathways

- Carbon Footprint, Energy Intensity & Cradle-to-Gate Emissions Analysis Across Curing Agent Categories

- Bio-Based Curing Agent Adoption, Renewable Content Certification & Substitution Performance

- Hazardous Substance Reformulation, Low-VOC Compliance & Indoor Air Quality Impact

- Regulatory-Driven Sustainability, SDG 9 (Industry, Innovation and Infrastructure) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Curing Agent Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Curing Agent Type, Application & Geography

- Player Classification

- Integrated Specialty Chemical Producers (Established Global Players)

- Specialty Amine Curing Agent Producers

- Anhydride & Phenolic Curing Agent Specialists

- Bio-Based & Renewable Curing Agent Specialists

- Latent Hardener & One-Component Epoxy Specialists

- Phenalkamine, Marine & Protective Coating Curing Agent Specialists

- Composite, Wind Energy & Aerospace-Grade Curing Agent Specialists

- Regional Producers & Distribution-Focused Channel Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Curing Agent Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Epoxy Curing Agent Products & Technology Portfolio

- Key Customer Relationships & Reference Customer Accounts

- Manufacturing Footprint & Production Capacity

- Revenue (Epoxy Curing Agents Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Curing Agent Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Curing Agent Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)