Global Chemical Packaging Materials Market By Packaging Type, By Material, By Capacity, By Application, By Hazard Class, By Reusability, By End User Industry, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

Chemical packaging materials are purpose-engineered industrial packaging products including drums, intermediate bulk containers (IBCs), pails, bottles, cans, bags, and specialty containers designed to safely store, transport, and dispense liquid, solid, powder, and granular chemical products across primary, secondary, and tertiary chemical distribution networks while meeting stringent hazardous materials handling, transport regulatory, and chemical compatibility requirements. The Global Chemical Packaging Materials Market encompasses the design, manufacturing, formulation, distribution, and circular economy management of steel drums, plastic drums, fiber drums, rigid plastic IBCs, composite IBCs, flexible intermediate bulk containers (FIBCs), high-density polyethylene (HDPE) bottles and jerry cans, paper and plastic-lined bags, multi-layer barrier packaging, and associated closures, fittings, and accessories supplied to petrochemical, agrochemical, specialty chemical, pharmaceutical, adhesives, paints and coatings, and cleaning chemical operators globally.

The chemical packaging materials market includes United Nations (UN) certified packaging supporting hazardous materials transport under packing group I, II, and III classifications, alongside non-regulated chemical packaging supporting non-hazardous chemical distribution and intermediate manufacturing transfers. Market participants include integrated industrial packaging manufacturers, specialty drum and IBC producers, bag and pouch manufacturers, closure and fitting suppliers, packaging reconditioners operating returnable container programs, and end-user industries spanning petrochemical refining, agrochemical formulators, specialty chemical producers, pharmaceutical contract manufacturing, adhesive and sealant formulators, paints and coatings manufacturers, and industrial cleaning chemical producers. The chemical packaging materials market also covers value-added services including UN certification testing, custom barrier formulation, container reconditioning, closed-loop returnable container management, and regulatory compliance documentation. The scope explicitly excludes consumer-facing chemical product packaging, food-contact chemical ingredient packaging, and bulk transport tank containers without primary packaging functionality, focusing exclusively on industrial chemical packaging materials globally.

Market Insights

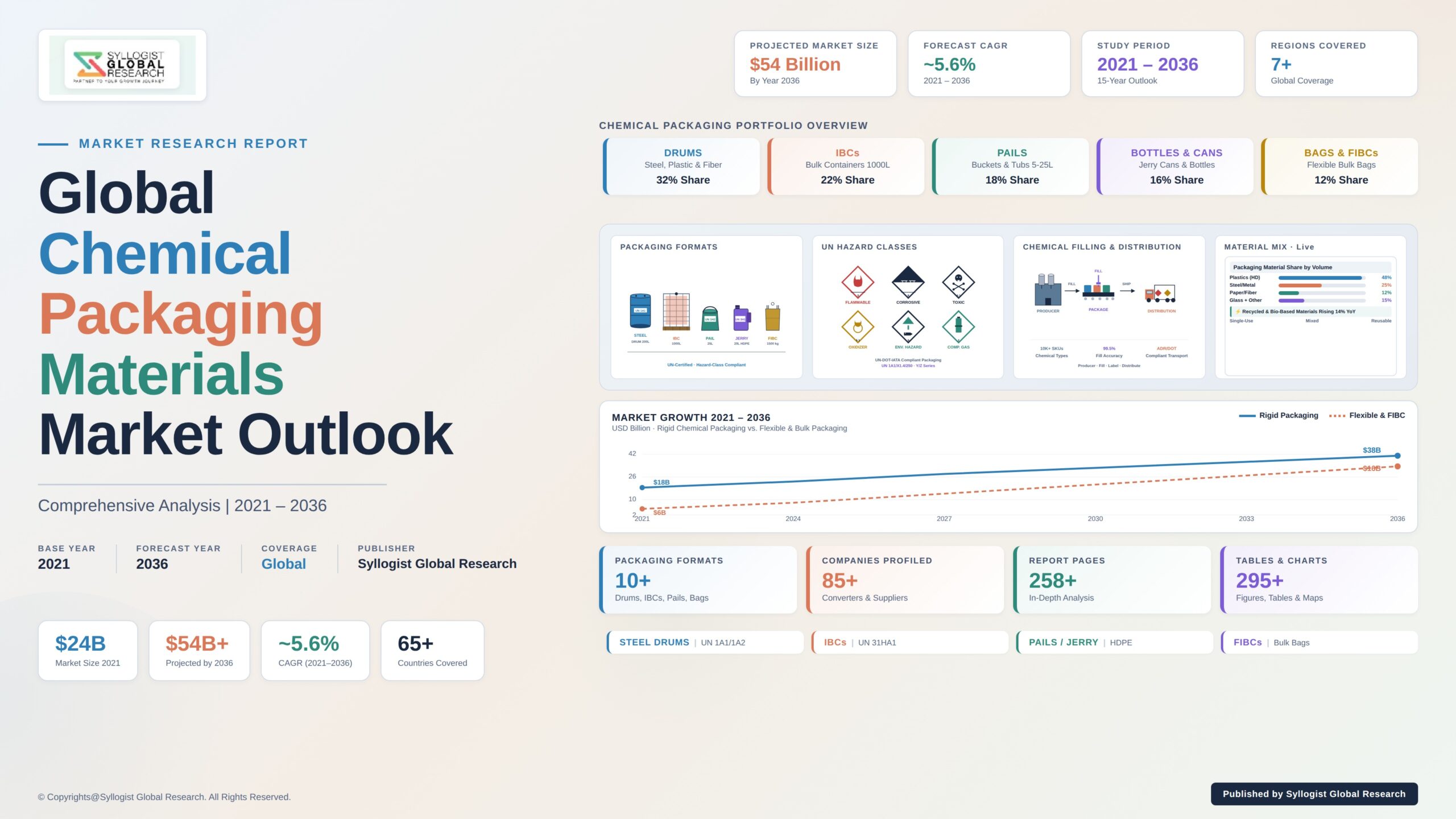

The global chemical packaging materials market is undergoing a sustained expansion phase, shaped by accelerating global chemical manufacturing capacity additions in Asia-Pacific and the Middle East, sustained agrochemical demand supporting global food production requirements, expanding pharmaceutical contract manufacturing capacity, intensifying sustainability mandates favoring recyclable and recycled-content packaging, and tightening hazardous materials transport regulations driving UN-certified packaging procurement across mature and emerging operating regions globally. The chemical packaging materials market was valued at approximately USD 27.8 billion in 2025 and is projected to reach USD 44.6 billion by 2034, advancing at a compound annual growth rate of 5.4% through the forecast period, as petrochemical operators, agrochemical formulators, specialty chemical producers, pharmaceutical contract manufacturers, and industrial chemical distributors scale chemical packaging procurement across global supply chains.

The chemical packaging materials market trajectory is being reshaped by the structural transition toward recycled-content plastics, mono-material packaging supporting recycling stream compatibility, returnable and reusable container programs, and lightweighting initiatives reducing material consumption per packaging unit. Major chemical manufacturers including BASF, Dow, Covestro, Solvay, and SABIC have established corporate sustainability commitments targeting between 30% and 70% recycled content in chemical packaging by 2030, generating sustained procurement preference for packaging suppliers offering verified recycled-content drums, IBCs, and bags within the chemical packaging materials market. Returnable IBC programs operated by integrated reconditioning service providers handle over 50 million IBC reconditioning cycles annually across major operating regions, materially reducing per-trip packaging cost and supporting circular economy compliance commitments among end-user chemical operators. Lightweighting initiatives have reduced steel drum gauge requirements, plastic drum wall thickness, and bag material weight by 8% to 15% across the chemical packaging materials market over the past 5 years.

Plastic drums and pails represent the largest packaging type segment within the chemical packaging materials market, propelled by sustained demand from chemical, agrochemical, and specialty chemical operators requiring chemical-compatible, lightweight, corrosion-resistant packaging at the 5-liter to 220-liter capacity range. Intermediate bulk containers represent the fastest-growing packaging type segment within the chemical packaging materials market, supported by chemical operator preference for IBCs over multiple drum equivalents in operational efficiency, palletization, and reusability programs that reduce per-liter packaging cost and simplify warehouse handling. Petrochemicals represent the largest application segment within the chemical packaging materials market, fueled by sustained demand from base chemical, intermediate chemical, and specialty derivative distribution. Agrochemicals represent the fastest-growing application segment within the chemical packaging materials market, propelled by accelerating crop protection chemical consumption in emerging markets, expanding herbicide, insecticide, and fungicide formulation activity, and continued expansion of biological crop input distribution.

Asia-Pacific represents the largest regional market within the chemical packaging materials market, anchored by extensive chemical manufacturing capacity in China, India, Indonesia, Thailand, and South Korea, sustained agrochemical consumption, growing pharmaceutical contract manufacturing capacity, and expanding domestic chemical packaging materials production capacity. China hosts the largest concentration of chemical packaging materials consumption globally, propelled by sustained chemical capacity additions and continued domestic and export-oriented chemical production. North America represents the second largest regional position within the chemical packaging materials market, supported by mature specialty chemical production, sustained petrochemical exports, accelerating Gulf Coast chemical capacity additions, and continued agrochemical formulation activity. Europe occupies the third major regional position within the chemical packaging materials market, shaped by stringent REACH regulation, the European Union Packaging and Packaging Waste Regulation (PPWR) driving recycled-content procurement preference, mature specialty chemical production, and sustained pharmaceutical contract manufacturing capacity across the chemical packaging materials market value chain.

Key Drivers

Global Chemical Manufacturing Capacity Expansion, Asia-Pacific Petrochemical Buildout, and Specialty Chemical Production Growth Driving Sustained Chemical Packaging Materials Procurement

The structural expansion of global chemical manufacturing capacity, accelerating petrochemical buildout in Asia-Pacific and the Middle East, and sustained specialty chemical production growth are collectively driving durable procurement demand for chemical packaging materials across primary, secondary, and tertiary chemical distribution networks globally. Global chemical industry revenue exceeded USD 5.7 trillion in 2025, with sustained annual capacity additions in petrochemical, specialty chemical, and agrochemical production segments driving sustained chemical packaging materials procurement intensity. China hosts over 40% of global chemical production capacity and continues to add over USD 100 billion annually in chemical manufacturing capital investment, generating sustained demand for plastic drums, IBCs, and FIBC packaging supporting domestic distribution and growing chemical exports within the chemical packaging materials market. Middle Eastern petrochemical capacity additions, including major projects in Saudi Arabia, the United Arab Emirates, and Oman, generate sustained demand for chemical packaging materials supporting downstream specialty chemical distribution. Major chemical manufacturers are structuring multi-year chemical packaging materials supply commitments aligning packaging procurement with manufacturing capacity expansion timelines, generating long-duration revenue commitments that anchor packaging producer capacity scaling decisions across the chemical packaging materials market value chain globally and reinforcing sustained investment in dedicated chemical packaging manufacturing capacity, UN certification testing infrastructure, and regional packaging distribution networks.

Agrochemical Demand Growth, Crop Protection Consumption Expansion, and Biological Crop Input Commercialization Driving Specialty Packaging Procurement

Sustained agrochemical demand growth, accelerating crop protection chemical consumption across emerging operating regions, and the rapid commercialization of biological crop input products are collectively driving substantial procurement of specialty chemical packaging materials within the chemical packaging materials market across global agrochemical formulator and distribution networks. Global agrochemical consumption volumes exceeded 3.7 million tonnes of active ingredients in 2025, with herbicides, insecticides, fungicides, and biological crop input products generating sustained demand for HDPE jerry cans, plastic drums, sachet packaging, and FIBC bulk bags supporting field-application and farmer-level distribution. India, China, Brazil, and Argentina collectively account for over 55% of global agrochemical packaging consumption within the chemical packaging materials market, propelled by sustained crop protection consumption supporting food production requirements across major agricultural operating regions. Biological crop input commercialization is generating new specialty packaging procurement requirements, with microbial and biopesticide products requiring oxygen-barrier packaging, validated shelf-life packaging formats, and contamination-controlled filling environments that exceed conventional agrochemical packaging specifications. Major agrochemical manufacturers are structuring multi-year chemical packaging materials supply agreements aligning packaging supply with seasonal production cycles, generating durable revenue commitments and reinforcing continued capital investment across the chemical packaging materials market value chain.

Sustainability Mandates, Recycled Content Procurement Targets, and Circular Economy Regulation Driving Reformulation and Returnable Container Adoption

Tightening sustainability mandates from major chemical manufacturers, expanding recycled content procurement targets, and accelerating circular economy regulation including the European Union Packaging and Packaging Waste Regulation (PPWR) are collectively driving sustained reformulation and returnable container procurement within the chemical packaging materials market globally. The PPWR, adopted in 2024 and progressively implemented through 2030 and 2040, mandates recycled content thresholds, packaging minimization requirements, and recyclability design standards across packaging types including chemical packaging materials, generating procurement preference for verified recycled-content drums, IBCs, and bags within the chemical packaging materials market. Major chemical manufacturers including BASF, Dow, Covestro, Solvay, and SABIC have established corporate sustainability commitments targeting between 30% and 70% recycled content in chemical packaging by 2030, reinforcing recycled-content procurement preference. Returnable IBC programs operated by integrated reconditioning service providers handle over 50 million IBC reconditioning cycles annually across major operating regions, materially reducing per-trip packaging cost and supporting circular economy compliance commitments among end-user chemical operators. Specialty chemical packaging materials producers are structuring multi-year recycled-content supply commitments and returnable container service contracts aligning with chemical manufacturer sustainability roadmap timelines, generating durable revenue commitments and reinforcing continued capital deployment toward recycled material processing capacity and reconditioning infrastructure within the chemical packaging materials market value chain.

Key Challenges

Raw Material Cost Volatility, Resin Price Fluctuations, and Steel Cost Variability Affecting Chemical Packaging Materials Producers

The chemical packaging materials market continues to face material raw material cost volatility, sustained resin price fluctuations affecting HDPE, polypropylene, and engineering plastic packaging segments, and persistent steel cost variability affecting drum and pail manufacturing economics, all of which generate substantial margin pressure across producers serving global chemical operator customers. HDPE resin prices experienced sustained volatility of 25% to 45% between 2021 and 2024, propelled by feedstock pricing variability, ethylene supply disruptions, and shifting Asian capacity dynamics, generating per-unit margin pressure for plastic drum, IBC, and jerry can producers within the chemical packaging materials market. Steel coil and steel sheet pricing variability has similarly affected steel drum producers, with cost increases of 15% to 35% over the same period requiring producers to renegotiate contracts and complicating long-term pricing commitments to chemical operator customers. Specialty resin sourcing complexity for niche packaging variants including barrier-grade engineering plastics, high-density polyethylene specialty grades, and flame-retardant additives adds further supply chain risk that producers continue to address through supply chain diversification and inventory hedging strategies. The combined effect of resin price fluctuations, steel cost variability, and specialty material sourcing complexity continues to constrain margin stability and complicate strategic capital deployment decisions within the chemical packaging materials market across global operating regions and producer capacity expansion plans.

Stringent UN/DOT/ADR Certification Requirements, Hazardous Materials Compliance Complexity, and Cross-Border Transport Documentation Burdens

The chemical packaging materials market continues to confront stringent United Nations (UN), United States Department of Transportation (DOT), and European Agreement concerning the International Carriage of Dangerous Goods by Road (ADR) certification requirements, sustained hazardous materials compliance complexity, and cross-border transport documentation burdens that collectively elevate certification cost, extend product commercialization timelines, and complicate cross-border supply commitments across producers serving global chemical operator customers. UN certification testing under packing group I, II, and III classifications requires extensive drop testing, leakproofness validation, stacking testing, hydraulic pressure testing, and continuous batch quality monitoring documentation, with new UN-certified packaging variants typically requiring 6 to 18 months of certification testing before commercial release within the chemical packaging materials market. Hazardous materials compliance complexity varies materially across UN, DOT, ADR, IMDG (maritime), IATA (air transport), and emerging Asia-Pacific dangerous goods transport regulations, requiring producers to maintain region-specific certification testing programs, marking and labeling configurations, and customer technical support documentation. Cross-border hazardous materials transport documentation including United Nations dangerous goods declarations, certified packaging documentation, and country-specific import compliance documentation adds substantial administrative burden, complicating multinational supply commitments and elevating per-shipment compliance cost across the chemical packaging materials market value chain globally.

Returnable Container Logistics Complexity, Reconditioning Infrastructure Constraints, and End-of-Life Recovery Variability Affecting Sustainability Outcomes

The chemical packaging materials market continues to face material returnable container logistics complexity, geographic constraints on reconditioning infrastructure capacity, and persistent end-of-life packaging recovery variability that collectively constrain achievable sustainability outcomes and challenge the economics of returnable container procurement models. Returnable IBC and drum programs require extensive reverse logistics infrastructure supporting collection from end-user sites, inspection at consolidation hubs, transport to reconditioning facilities, cleaning and testing, and redistribution back to original equipment manufacturers or chemical operators, with reverse logistics cost ranging materially across geographic markets within the chemical packaging materials market. Reconditioning infrastructure capacity is geographically concentrated, with mature reconditioning capacity in North America and Europe but constrained reconditioning capacity in select Asia-Pacific and Latin American operating regions, limiting the geographic reach of returnable container programs and constraining circular economy adoption rates. End-of-life packaging recovery variability across end-user operating regions, including limited industrial packaging recycling infrastructure in select emerging markets and inconsistent end-user packaging return rates, constrains achievable recycled content sourcing volumes and complicates verification of recycled content claims within the chemical packaging materials market. Producers are responding through reconditioning capacity investment, return logistics partnerships, and recycled material sourcing agreements, but sustained infrastructure constraints continue to limit circular economy outcomes achievable across the chemical packaging materials market value chain globally.

Market Segmentation

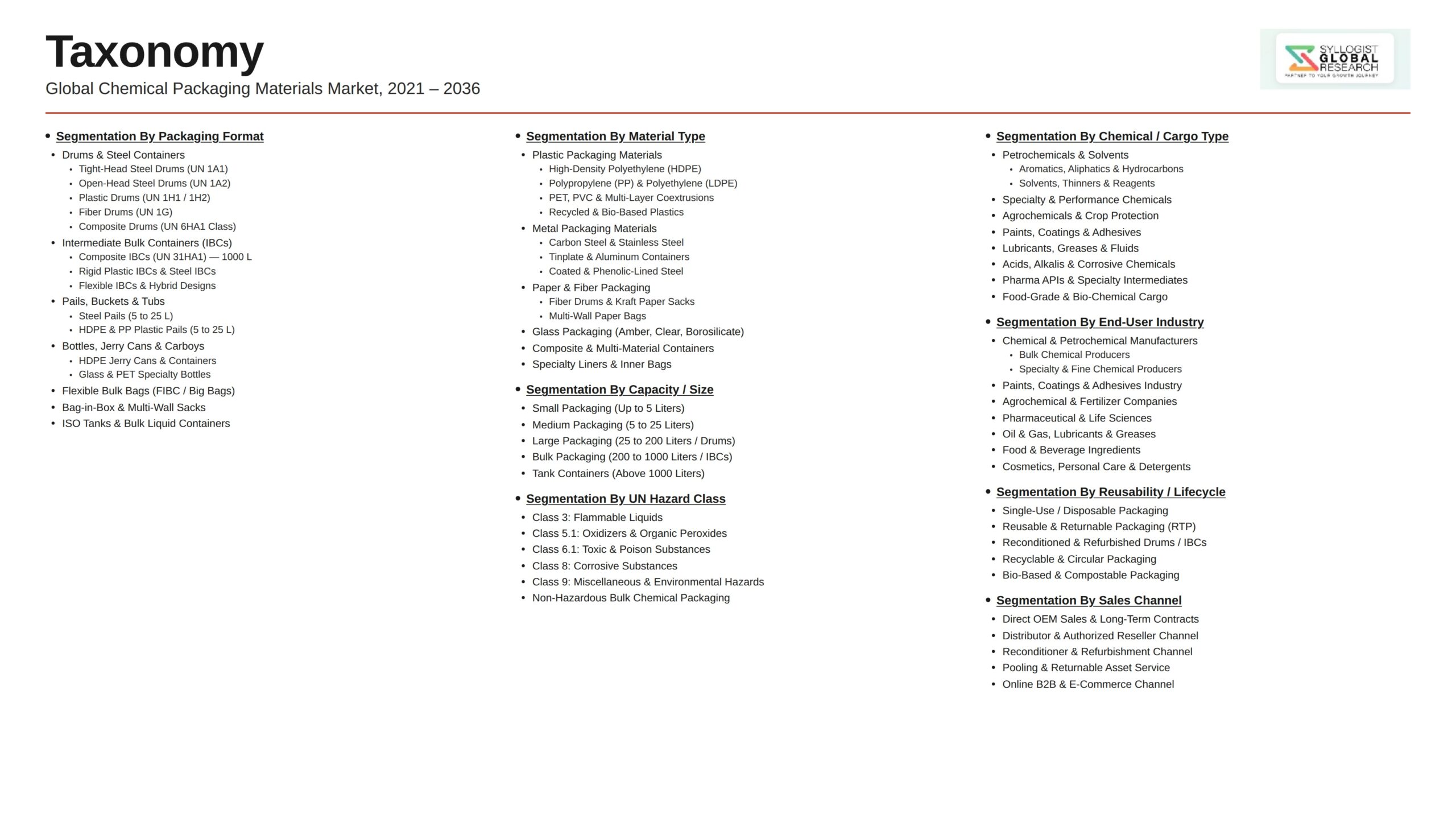

- Segmentation By Packaging Type

- Drums (Steel, Plastic, Fiber)

- Intermediate Bulk Containers (Rigid Plastic IBC, Composite IBC, Stainless Steel IBC)

- Flexible Intermediate Bulk Containers (FIBC/Bulk Bags)

- Pails and Cans

- HDPE Bottles and Jerry Cans

- Bags (Paper, Plastic, Multi-Layer)

- Specialty Containers

- Closures and Accessories

- Others

- Segmentation By Material

- Plastic (HDPE, Polypropylene, Engineering Plastics)

- Steel

- Fiber

- Paper

- Composite

- Stainless Steel

- Others

- Segmentation By Capacity

- Up to 5 Liters

- 5 to 25 Liters

- 25 to 220 Liters

- 220 to 1,000 Liters (IBC Range)

- Above 1,000 Liters (Bulk Range)

- Segmentation By Application

- Petrochemicals and Base Chemicals

- Agrochemicals (Herbicides, Insecticides, Fungicides, Biologicals)

- Specialty Chemicals

- Pharmaceuticals and Active Ingredients

- Adhesives and Sealants

- Paints and Coatings

- Cleaning Chemicals and Surfactants

- Inks and Printing Chemicals

- Lubricants and Industrial Fluids

- Others

- Segmentation By Hazard Class

- UN Packing Group I (High Danger)

- UN Packing Group II (Medium Danger)

- UN Packing Group III (Low Danger)

- Non-Regulated Chemical Packaging

- Segmentation By Reusability

- Single-Use Packaging

- Reconditioned and Returnable Packaging

- Pooled Returnable Container Programs

- Segmentation By End User Industry

- Petrochemical Producers

- Agrochemical Formulators

- Specialty Chemical Manufacturers

- Pharmaceutical Contract Manufacturers

- Adhesive and Sealant Manufacturers

- Paint and Coatings Manufacturers

- Industrial Cleaning Chemical Producers

- Chemical Distributors

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Chemical Packaging Materials Market in 2025, projected through 2034, segmented by packaging type, material, capacity, and application, enabling packaging manufacturers, distributors, reconditioning operators, and chemical industry procurement teams to identify highest-growth segments and most durable revenue opportunities across the chemical packaging materials landscape?

- How are petrochemical operators, agrochemical formulators, specialty chemical producers, pharmaceutical contract manufacturers, and industrial chemical distributors structuring procurement frameworks for chemical packaging materials, and which commercial models, including single-use purchase, reconditioned returnable programs, pooled container service, and outsourced packaging management, are shaping commercial deployment economics within the chemical packaging materials market through 2034?

- What sustainability procurement mandates, recycled content targets, and circular economy regulations including the European Union Packaging and Packaging Waste Regulation are reshaping packaging substitution timelines, returnable container adoption, and recycled-content procurement decisions across mature regulatory jurisdictions?

- Which packaging types, including steel drums, plastic drums, rigid IBCs, composite IBCs, FIBCs, HDPE bottles, and specialty containers, are gaining the strongest procurement traction across petrochemical, agrochemical, specialty chemical, and pharmaceutical applications, and what hazardous materials compliance, total cost of ownership, and sustainability metrics are shaping selection decisions?

- How is the competitive landscape structured among integrated industrial packaging manufacturers, specialty drum and IBC producers, bag and pouch manufacturers, and reconditioning service operators within the chemical packaging materials market, and what partnership, acquisition, and platform expansion strategies are enabling new entrants to compete against incumbent packaging producers?

- What United Nations, DOT, ADR, IMDG, and IATA dangerous goods transport regulations, along with emerging Asia-Pacific hazardous materials frameworks, are reshaping certification testing requirements, packaging documentation expectations, and customer technical support requirements across the chemical packaging materials market globally?

- Which regional markets, including Asia-Pacific, North America, Europe, and the Middle East, are projected to generate the largest incremental chemical packaging materials procurement opportunities through 2034, and what chemical capacity addition, agrochemical demand, pharmaceutical contract manufacturing, and regulatory factors are shaping capability investment priorities and supplier selection decisions in each regional chemical packaging materials market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility, Steel and Plastic Resin Cost Inflation & Specialty Resin Sourcing Risk

- UN Recommendations on the Transport of Dangerous Goods Compliance, Hazardous Container Certification & Testing Burden Risk

- Customer-Specific Container Qualification, Chemical Compatibility Testing & Long Approval Timeline Risk

- Container Reuse, Reconditioning Liability & Cross-Border Returnable Container Logistics Risk

- Sustainability Mandate Compliance, Recycled Content Procurement & Circular Economy Investment Risk

- Regulatory Framework & Standards

- UN Recommendations on the Transport of Dangerous Goods (UN Model Regulations), Performance Testing & Container Certification Standards

- Hazardous Material Transport (US DOT, EU ADR, IMDG, IATA) & Cross-Border Compliance Frameworks

- US EPA Resource Conservation and Recovery Act (RCRA), EU Waste Directive & End-of-Life Container Management Frameworks

- Food-Contact, Pharmaceutical & Cosmetic Container Compliance Standards (US FDA, EU EFSA)

- Sustainability, Recycled Content Mandates & Extended Producer Responsibility (EPR) Frameworks

- Global Chemical Packaging Materials Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Chemical Packaging Consumption in Million Container Units and Number of Active Manufacturing Facilities)

- Market Size & Forecast by Material Type

- High-Density Polyethylene (HDPE)

- Low-Density Polyethylene (LDPE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Steel (Carbon Steel and Stainless Steel)

- Aluminum

- Specialty Composite (Multi-Layer Plastic, Fluorinated, Lined Drum)

- Glass

- Fiber and Paperboard

- Others

- Market Size & Forecast by Container Type

- Steel Drums

- Plastic Drums

- Composite Intermediate Bulk Containers (IBCs)

- Metal Intermediate Bulk Containers

- Plastic Intermediate Bulk Containers

- Jerry Cans and Pails

- Pressurised Cylinders

- Pressurised Tank Containers

- Specialty Sealed Cartridges

- Bulk Bags and Flexible Intermediate Bulk Containers (FIBCs)

- Others

- Market Size & Forecast by Chemical Type

- Industrial Chemicals (Acids, Bases, Solvents)

- Specialty Chemicals

- Petrochemicals and Lubricants

- Agrochemicals and Pesticides

- Paints, Coatings and Adhesives

- Pharmaceutical Intermediates

- Hazardous Chemicals (UN Class 3 to 8)

- Food-Grade and Cosmetic Chemicals

- Others

- Market Size & Forecast by Capacity

- Below 25 Litres

- 25 to 100 Litres

- 100 to 220 Litres (Standard Drum)

- 220 to 1,000 Litres (Intermediate Bulk Container)

- Above 1,000 Litres (Bulk)

- Market Size & Forecast by Wall Construction

- Single-Wall

- Multi-Wall and Layered

- Composite Reinforced

- Insulated

- Others

- Market Size & Forecast by End-User

- Chemical Manufacturers

- Petrochemical and Refining Operators

- Agrochemical Producers

- Coating and Paint Manufacturers

- Pharmaceutical Intermediate Producers

- Industrial Distributors

- Specialty Chemical Distributors

- Others

- Market Size & Forecast by Sales Channel

- Direct Manufacturer-to-Customer Supply Contracts

- Specialty Container Distributor & Trader Channel

- Custom Container Development & Joint Development Partnerships

- Licensed Production & Contract Manufacturing Arrangements

- Aftermarket Container Reconditioning, Recycling & Technical Service Contracts

- North America Chemical Packaging Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Chemical Packaging Consumption in Million Container Units and Number of Active Manufacturing Facilities)

- By Material Type

- By Container Type

- By Chemical Type

- By Capacity

- By Wall Construction

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Chemical Packaging Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Chemical Packaging Consumption in Million Container Units and Number of Active Manufacturing Facilities)

- By Material Type

- By Container Type

- By Chemical Type

- By Capacity

- By Wall Construction

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Chemical Packaging Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Chemical Packaging Consumption in Million Container Units and Number of Active Manufacturing Facilities)

- By Material Type

- By Container Type

- By Chemical Type

- By Capacity

- By Wall Construction

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Chemical Packaging Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Chemical Packaging Consumption in Million Container Units and Number of Active Manufacturing Facilities)

- By Material Type

- By Container Type

- By Chemical Type

- By Capacity

- By Wall Construction

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Chemical Packaging Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Chemical Packaging Consumption in Million Container Units and Number of Active Manufacturing Facilities)

- By Material Type

- By Container Type

- By Chemical Type

- By Capacity

- By Wall Construction

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Chemical Packaging Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Chemical Packaging Consumption in Million Container Units and Number of Active Manufacturing Facilities)

- By Material Type

- By Container Type

- By Chemical Type

- By Capacity

- By Wall Construction

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- High-Density Polyethylene (HDPE), Polypropylene & Polyethylene Terephthalate (PET) Container Manufacturing Technology Deep-Dive

- Steel Drum, Stainless Steel & Specialty Metal Container Manufacturing Technology

- Intermediate Bulk Container (IBC), Composite Container & Multi-Layer Construction Technology

- Returnable, Reusable & Closed-Loop Container Tracking Technology

- Lined Drum, Fluorinated Surface Treatment & Chemical Compatibility Technology

- IoT, Telemetry & Smart Container Tracking Technology

- Recycled Content, Bio-Based Polymer & Circular Economy Container Technology

- Patent & IP Landscape in Chemical Packaging Materials Technologies

- Value Chain & Supply Chain Analysis

- Raw Material (Steel, Polymer Resin, Aluminum, Glass, Fiber) Supply Chain

- Specialty Resin, Fluorinated Liner & Multi-Layer Material Supply Chain

- Container Manufacturing (Drum, IBC, Jerry Can, Cylinder) Supply Chain

- Closure, Valve & Specialty Container Component Supply Chain

- Distributor, Specialty Trader & Regional Channel Partner Network

- Chemical Manufacturer, Petrochemical, Agrochemical & Coating Customer Procurement Landscape

- Aftermarket Container Reconditioning, Recycling & Reuse Service Network

- Pricing Analysis

- HDPE, Polypropylene & PET Plastic Container Pricing Analysis

- Steel Drum, Stainless Steel & Specialty Metal Container Pricing Analysis

- Intermediate Bulk Container & Composite Container Pricing Analysis

- Specialty Lined Drum, Fluorinated Container & Multi-Layer Container Pricing Analysis

- Returnable & Reusable Container Pricing Analysis Across Closed-Loop & Pool Models

- Per Unit Container Pricing Benchmark Analysis Across Standard, Specialty & Premium Categories

- Total Cost of Container Use: Lifecycle Economics, Reconditioning Cycles & Customer Return on Investment Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Chemical Packaging Materials Across Steel, Plastic, Aluminum, Glass & Composite Production Pathways

- Carbon Footprint, Embodied Emissions & Cradle-to-Gate Emissions Analysis Across Container Categories

- Recycled Content Adoption, Bio-Based Polymer Use & Circular Economy Performance

- End-of-Life Container Recycling, Reconditioning & Closed-Loop Reuse Performance

- Regulatory-Driven Sustainability, SDG 9 (Industry, Innovation and Infrastructure) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Material Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Material Type, Container Type & Geography

- Player Classification

- Integrated Chemical Packaging Manufacturers (Established Global Players)

- Steel Drum & Stainless Steel Container Specialists

- HDPE, Polypropylene & Plastic Container Specialists

- Intermediate Bulk Container (IBC) & Composite Container Specialists

- Specialty Lined Drum & Fluorinated Container Specialists

- Returnable Container & Closed-Loop Pool Operators

- Recycling, Reconditioning & Circular Container Service Specialists

- Regional Producers & Distribution-Focused Channel Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Material Type, Container Type & Region

- Company Profile

- Company Overview & Headquarters

- Chemical Packaging Material Products & Technology Portfolio

- Key Customer Relationships & Reference Customer Accounts

- Manufacturing Footprint & Production Capacity

- Revenue (Chemical Packaging Materials Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Material Type, Container Type, Chemical Type, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Chemical Packaging Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)