Global Mine Planning Software Market By Deployment Type, By Component, By Application, By Mining Method, By Mine Type, By End User, By Enterprise Size, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Mine Planning Software Market encompasses the development, licensing, deployment, and sustainment of specialised digital platforms, geological modelling engines, scheduling solvers, and visualisation environments that enable mining engineers, geologists, and operations planners to translate orebody knowledge into optimised extraction strategies across the full mine life cycle. The market includes geological modelling software for orebody interpretation, resource and reserve estimation tools, pit and underground mine design modules, short term and long term scheduling solutions, drill and blast design platforms, haulage and ventilation optimisation, geotechnical analysis suites, and integrated production reporting dashboards procured by mining majors, mid tier miners, junior explorers, contract mining service providers, and government geological survey organisations worldwide. Deployment models span on premise client installations, hybrid private cloud environments, and fully cloud native SaaS offerings, with licensing structures ranging from perpetual seat licences to subscription based and consumption based pricing tied to processing capacity and concurrent user counts. The market also includes complementary services covering implementation consulting, customisation, integration with fleet management and process control systems, applicator training, certification, and ongoing technical support. End user demand spans metal mining including copper, gold, iron ore, nickel, lithium, and cobalt, alongside coal mining, industrial minerals, and aggregates, with each commodity requiring tailored geostatistical methods, scheduling logic, and reporting frameworks calibrated to regulatory standards including the JORC Code, NI 43-101, SAMREC, and PERC. The study scope captures global revenue dynamics, regional adoption patterns, pricing models, competitive positioning of leading software vendors, and the structural transition toward cloud, automation, artificial intelligence, and digital twin enabled workflows that are reshaping how mining companies plan, schedule, and execute extraction operations across surface and underground assets.

Market Insights

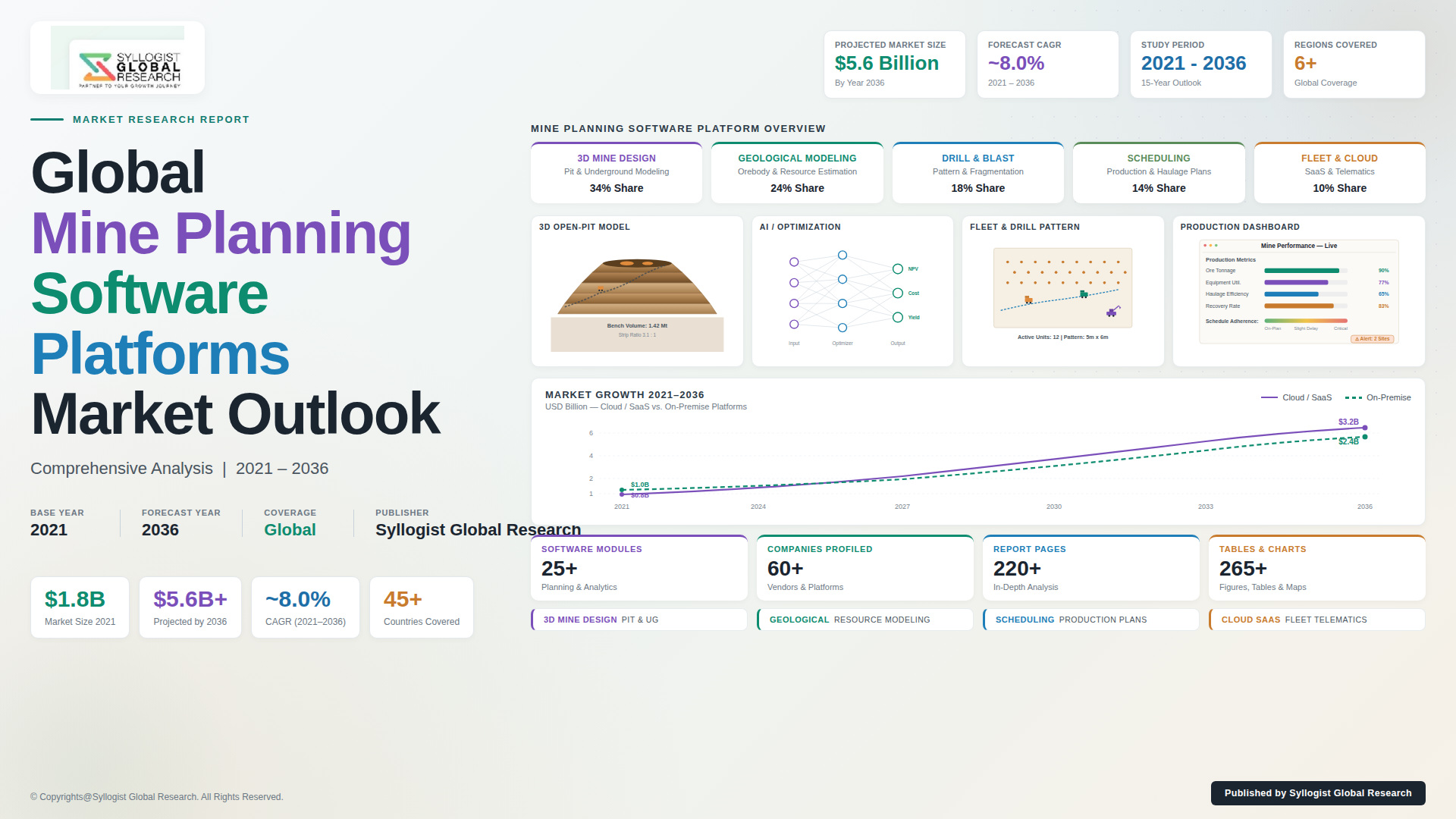

The global mine planning software market is advancing through a pronounced growth phase shaped by intensifying commodity demand from the energy transition, mounting pressure on mining companies to reduce unit costs, and accelerating digital transformation across surface and underground operations. The market was valued at approximately USD 1.6 billion in 2025 and is projected to reach USD 3.2 billion by 2034, advancing at a compound annual growth rate of 8.1% through the forecast period, as mining operators transition from siloed point solutions toward integrated mine planning platforms that connect geological modelling, design, scheduling, and reconciliation in a single decision environment. Demand momentum is reinforced by record global exploration spending exceeding USD 13 billion in 2024, deeper and more complex orebodies requiring advanced geostatistical methods, and the emergence of critical minerals such as lithium, cobalt, nickel, and rare earths as strategic procurement priorities for governments and battery supply chain investors.

Asia Pacific leads the global mine planning software market with a revenue share of approximately 34%, anchored by Australia’s globally dominant mining services ecosystem, China’s vast domestic mining footprint, and accelerating investment across Indonesia, the Philippines, and India in nickel, bauxite, coal, and iron ore. Australia in particular hosts a deep concentration of mine planning software vendors and remains the most mature market for cloud adoption, advanced analytics, and digital twin pilot deployments. North America holds the second largest share at close to 28%, supported by sustained activity across copper, gold, lithium, and coal operations in the United States, Canada, and Mexico, where capital discipline and ESG scrutiny are reinforcing demand for transparent and auditable planning workflows. Latin America, anchored by Chile, Peru, and Brazil, accounts for roughly 18% of global revenue, while Africa is registering the fastest regional growth at a CAGR exceeding 9.4%, propelled by lithium projects in Zimbabwe, copper expansion across the Democratic Republic of Congo and Zambia, and gold development throughout West Africa.

The shift from on premise installations to cloud and SaaS deployments is the single most consequential structural change underway in the market, with cloud and hybrid offerings projected to account for over 55% of new licence revenue by the end of the forecast period. Artificial intelligence and machine learning are being embedded into orebody modelling, grade prediction, blast optimisation, and stochastic scheduling, allowing planners to evaluate hundreds of life of mine scenarios in hours rather than weeks. Digital twin architectures linking mine planning software to fleet management systems, process control historians, geotechnical sensors, and ventilation telemetry are enabling near real time reconciliation between plan and actual production, reducing schedule slippage and unlocking measurable improvements in mill feed grade stability of 4% to 7% across early adopter operations and supporting more predictable downstream metallurgical recovery.

The competitive landscape is moderately concentrated, with the top 3 vendors controlling close to 48% of global revenue and the top 10 accounting for over 75%, while specialised niche providers continue to capture share in geostatistics, stochastic optimisation, and underground mine design. Vendors are differentiating through end to end platform interoperability, open APIs, marketplace ecosystems, and value added services covering implementation, customisation, and certification training. Metal mining, encompassing copper, gold, iron ore, nickel, lithium, and rare earths, accounts for roughly 62% of total software spending, while coal contributes 22%, and industrial minerals and aggregates together account for the remaining 16%. Large enterprises drive close to 78% of revenue through enterprise wide deployments, but the small and medium enterprise segment is registering the highest growth as cloud subscription pricing lowers entry barriers for junior miners, contract operators, and consulting firms supporting feasibility studies across emerging mining jurisdictions.

Key Drivers

Energy Transition and Critical Mineral Demand Driving Accelerated Investment in Mine Planning Software Across Copper, Lithium, Nickel, Cobalt, and Rare Earth Operations

The global push toward electrification, renewable energy, and electric vehicles is generating durable demand for copper, lithium, nickel, cobalt, manganese, graphite, and rare earth elements, with the International Energy Agency projecting that critical mineral demand will grow more than 3.5 times by 2040 under stated net zero pathways. Mining companies are responding by accelerating exploration and project development, which directly translates into expanded software seat counts, premium module adoption, and longer implementation engagements as new orebodies require integrated geological modelling, scenario based scheduling, and reconciliation tooling to deliver bankable feasibility studies and operate at the cost and grade targets set in investment cases approved by boards, lenders, and strategic offtake partners.

Cost Pressure and Productivity Mandates Driving Adoption of AI Enabled Optimisation and Stochastic Scheduling Across Mid Tier and Major Mining Operators

Persistent cost inflation across labour, fuel, explosives, and consumables is forcing mining companies to extract every percentage point of productivity from existing operations, generating durable demand for software modules that optimise pit sequencing, haul truck cycle times, blast design parameters, and stope economics. AI driven optimisation engines have demonstrated the ability to lift net present value by 3% to 8% across published case studies, while stochastic scheduling reduces tonnage and grade variance against plan, supporting more predictable cash flow generation and reduced working capital intensity. These quantifiable returns are translating into faster procurement cycles, multi year enterprise agreements, and growing willingness from chief financial officers to invest in premium analytics modules at full vendor list pricing.

Regulatory Reporting Requirements and ESG Disclosure Mandates Driving Demand for Auditable Digital Planning Workflows and Integrated Reserve Reconciliation

Public reserve reporting under the JORC Code, NI 43-101, SAMREC, and PERC frameworks, combined with sustainability disclosure obligations under TCFD, IFRS S2, and CSRD, requires mining companies to maintain auditable, version controlled, and traceable planning workflows that link geological models to extraction schedules and financial outputs. This regulatory complexity is driving structural demand for software platforms with built in version control, audit trails, competent person sign off workflows, and standardised reporting outputs that reduce audit risk and accelerate quarterly disclosure cycles across multinational operations. Listed mining companies are now embedding reporting compliance capability into vendor evaluation criteria, raising the technical bar for new entrants and reinforcing the competitive position of established platforms with proven regulatory pedigree.

Key Challenges

Long Sales Cycles, Capital Conservative Mining Customers, and Conservative Change Management Cultures Slowing Software Adoption and Module Upgrades

Mining is a capital intensive, risk averse industry where operations directors often resist replacing established planning workflows that have delivered acceptable results over decades. Software replacement cycles regularly span 5 to 7 years, sales cycles for enterprise deployments commonly extend 12 to 24 months, and pilot to production conversion rates remain stubbornly below 60% across many vendor portfolios. Cultural resistance from veteran planners, fragmented IT and operational technology environments, the operational risk of disrupting active mine schedules, and limited internal change management capacity collectively dampen the pace at which vendors can monetise new capability releases, extending payback periods on research and development investment in advanced optimisation and AI modules.

Skilled Mining Engineer and Geostatistician Shortage Limiting the Realised Value of Advanced Mine Planning Software Across Mining Jurisdictions

The global mining sector faces a chronic shortage of mining engineers, geologists, and geostatisticians, with university enrolment in mining related programmes declining by over 30% across major mining nations over the past decade. The realised value of advanced mine planning software depends heavily on skilled users who can configure stochastic models, interpret simulation outputs, and translate optimisation results into operational decisions. Without sufficient depth of skilled talent, mining companies under utilise advanced module capability, default to legacy workflows, and resist premium subscription tiers, capping the addressable revenue opportunity for vendors investing heavily in AI, machine learning, and optimisation features designed to differentiate enterprise platforms in competitive procurement evaluations.

Cybersecurity, Data Sovereignty, and Cloud Adoption Concerns Slowing the Transition from On Premise to SaaS Mine Planning Platforms

Mining companies hold highly sensitive orebody, reserve, and operational data that represents the core valuation of their underlying assets, and growing concern over cyber espionage, ransomware attacks, and regulatory data sovereignty obligations is slowing the migration from on premise installations to multi tenant SaaS environments. Jurisdictions including China, Indonesia, Russia, and the Gulf Cooperation Council have introduced data localisation requirements that complicate cross border cloud deployments, while incidents of ransomware targeting natural resource companies have grown sharply over the past three years, forcing chief information officers to demand robust encryption, in country hosting, granular access controls, and contractual liability clauses before approving full scale cloud migration programmes.

Market Segmentation

- Segmentation By Deployment Type

- On Premise

- Cloud Based

- Hybrid

- Segmentation By Component

- Software (Geological Modelling, Resource Estimation, Mine Design, Scheduling, Drill and Blast, Haulage Optimisation, Geotechnical Analysis, Production Reporting)

- Services (Consulting and Implementation, Integration, Training and Certification, Support and Maintenance)

- Segmentation By Application

- Geological Modelling and Resource Estimation

- Mine Design and Layout

- Short Term and Long Term Scheduling

- Drill and Blast Design

- Haulage and Fleet Optimisation

- Geotechnical and Ventilation Analysis

- Production Reporting and Reconciliation

- Others

- Segmentation By Mining Method

- Surface Mining (Open Pit, Strip Mining, Quarrying)

- Underground Mining (Block Caving, Sublevel Caving, Cut and Fill, Room and Pillar)

- Solution Mining

- Others

- Segmentation By Mine Type

- Metal Mining (Copper, Gold, Iron Ore, Nickel, Lithium, Cobalt, Rare Earths, Others)

- Coal Mining

- Industrial Minerals

- Aggregates and Construction Materials

- Others

- Segmentation By End User

- Mining Majors and Multinational Operators

- Mid Tier Mining Companies

- Junior Explorers and Project Developers

- Contract Mining Service Providers

- Government Geological Survey Organisations

- Mining Consulting and Engineering Firms

- Others

- Segmentation By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- Segmentation By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Mine Planning Software Market in 2025, projected through 2034, disaggregated by deployment type, component, mine type, and region, enabling software vendors, mining operators, and investors to identify the highest growth segments and most durable revenue opportunities across the mining digital value chain?

- How are Asia Pacific, North America, Latin America, and Africa evolving as mine planning software markets in response to differing commodity exposure, exploration spending cycles, regulatory reporting frameworks, and digital transformation maturity, and which country level markets are defining the technical benchmarks and procurement standards for global vendor competition through 2034?

- Which deployment models including on premise, cloud based, and hybrid, alongside pricing structures spanning perpetual, subscription, and consumption based models, are gaining the highest share of new licence revenue, and how should vendors sequence their cloud migration roadmaps, infrastructure investments, and customer success programmes to defend installed base value while capturing greenfield SaaS opportunities?

- Which application modules including geological modelling, resource estimation, mine design, scheduling, drill and blast, and haulage optimisation are delivering the strongest growth, premium pricing power, and customer expansion economics, and how are AI driven optimisation, stochastic scheduling, and machine learning capabilities reshaping competitive differentiation among leading software platforms?

- How are critical mineral demand acceleration, energy transition mandates, and battery supply chain investment translating into incremental software spend by mining commodity, and which commodities including copper, lithium, nickel, cobalt, and rare earths are generating the highest growth in new project module adoption and enterprise agreement renewals through 2034?

- What is the structure of the competitive landscape across global software majors, specialist mining technology vendors, geological niche providers, and emerging cloud native entrants, and what partnership, acquisition, marketplace, and platform extension strategies are reshaping market share, customer lock in, and vendor consolidation dynamics across the value chain?

- How are mining customer procurement behaviours, evaluation frameworks, pilot conversion rates, and change management practices evolving, and what go to market motions covering direct sales, partner networks, consulting led delivery, and vertical specific marketplaces are most effective in shortening enterprise sales cycles and accelerating module expansion in installed accounts?

- Which regulatory developments under JORC, NI 43-101, SAMREC, PERC, TCFD, IFRS S2, and CSRD frameworks are generating new functional requirements within mine planning software, and how should vendors prioritise reserve reporting automation, audit trail capability, and ESG disclosure tooling to maintain compliance positioning across multinational customer footprints?

- What cybersecurity, data sovereignty, integration, and operational technology connectivity considerations are shaping enterprise cloud adoption decisions in mining, and how are leading software vendors addressing in country hosting, encryption, access control, and integration with fleet management and process control systems to remove adoption barriers for SaaS migration?

- Which strategic partnerships, joint ventures, mergers and acquisitions, technology licensing arrangements, and capacity expansions are reshaping the global mine planning software landscape, and what entry barriers, technical know how requirements, regulatory expertise, and customer relationship dynamics face new entrants seeking to scale globally in this specialised vertical software market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Software Supply Chain & Vendor Sourcing Trends

- Deployment & Implementation Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Geological Data Quality, Orebody Uncertainty & Resource Estimation Risk

- Commodity Price Volatility, Capital Expenditure & Mine Project Viability Risk

- Regulatory, Permitting & Cross-Jurisdiction Mining Code Compliance Risk

- Software Integration, Interoperability, Legacy System Migration & Cybersecurity Risk

- Vendor Lock-in, License Continuity & Long-Term Roadmap Risk

- Regulatory Framework & Standards

- National Mining Codes, Mineral Resource Reporting (JORC, NI 43-101, SAMREC, PERC) & Public Disclosure Standards

- Geospatial Data, Coordinate Reference System & Survey Accuracy Standards Applicable to Mine Planning Software

- Health, Safety, Geotechnical Stability & Operational Compliance Standards Encoded in Mine Planning Workflows

- Environmental, Permitting, Mine Closure & Cross-Sector Impact Assessment Regulations for Mine Plan Approvals

- Data Governance, Cybersecurity, Cloud Sovereignty & ESG Disclosure Standards for Mine Planning Platforms

- Global Mine Planning Software Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Licenses, Users & Active Deployments)

- Market Size & Forecast by Software Solution Type

- Open-Pit Mine Planning & Pit Optimisation Software

- Underground Mine Planning, Stope Design & Block Cave Scheduling Software

- Geological Modelling, Resource Estimation & Orebody Block Modelling Software

- Mine Production Scheduling, Strategic & Tactical Planning Software

- Drill & Blast Design, Fragmentation & Pattern Optimisation Software

- Haulage, Truck Dispatch & Fleet Management Software

- Geotechnical, Slope Stability & Subsidence Analysis Software

- Mine Survey, Reconciliation & Volumetric Reporting Software

- Mine Closure, Rehabilitation & Tailings Storage Facility Planning Software

- Integrated Digital Mine, AI-Enabled Planning Platforms & Mine-to-Mill Optimisation Suites

- Market Size & Forecast by Deployment Mode

- On-Premise Licensed Software

- Cloud-Based SaaS Platforms

- Hybrid Deployment & Edge-Connected Solutions

- Market Size & Forecast by Mining Method

- Surface Mining (Open-Pit, Open-Cast, Strip & Quarry Operations)

- Underground Mining (Stoping, Block Caving, Sub-Level Caving, Room & Pillar)

- Placer, Solution & In-Situ Recovery Mining

- Market Size & Forecast by Commodity Type

- Iron Ore, Bauxite & Base Metals (Copper, Zinc, Lead, Nickel)

- Precious Metals (Gold, Silver, Platinum Group Metals)

- Coal & Lignite

- Battery Metals & Critical Minerals (Lithium, Cobalt, Rare Earths, Graphite)

- Industrial Minerals, Aggregates & Non-Metallic Minerals

- Uranium & Other Specialty Commodities

- Market Size & Forecast by Application

- Geological Modelling & Mineral Resource Estimation

- Strategic Mine Design & Pit / Stope Optimisation

- Short, Medium & Long-Term Production Scheduling

- Drill & Blast Design & Fragmentation Optimisation

- Haulage, Logistics & Fleet Optimisation

- Geotechnical & Slope Stability Analysis

- Mine Reconciliation, Reporting & Compliance

- Mine Closure, Rehabilitation & Post-Mining Land Use Planning

- Market Size & Forecast by End-User

- Tier-1 Diversified Mining Majors

- Mid-Tier & Single-Commodity Mining Companies

- Junior Miners & Exploration Companies

- Mining Contractors & Service Providers

- Government Geological Surveys, Mining Ministries & State-Owned Mining Enterprises

- Market Size & Forecast by Sales Channel

- Direct Licensing & Enterprise Software Agreement

- SaaS Subscription & Pay-Per-Use Cloud Channel

- Reseller, Distributor & Regional Partner Channel

- System Integrator, Consulting & Implementation Partner Channel

- North America Mine Planning Software Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Licenses, Users & Active Deployments)

- By Software Solution Type

- By Deployment Mode

- By Mining Method

- By Commodity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Mine Planning Software Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Licenses, Users & Active Deployments)

- By Software Solution Type

- By Deployment Mode

- By Mining Method

- By Commodity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Mine Planning Software Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Licenses, Users & Active Deployments)

- By Software Solution Type

- By Deployment Mode

- By Mining Method

- By Commodity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Mine Planning Software Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Licenses, Users & Active Deployments)

- By Software Solution Type

- By Deployment Mode

- By Mining Method

- By Commodity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Mine Planning Software Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Licenses, Users & Active Deployments)

- By Software Solution Type

- By Deployment Mode

- By Mining Method

- By Commodity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Mine Planning Software Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Licenses, Users & Active Deployments)

- By Software Solution Type

- By Deployment Mode

- By Mining Method

- By Commodity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Block Modelling, Implicit Geological Modelling & Geostatistical Resource Estimation Technology Deep-Dive

- Pit Optimisation Algorithms (Lerchs-Grossmann, Pseudoflow) & Strategic Mine Design Technology

- Mixed-Integer Programming, Heuristic & AI-Based Production Scheduling Technology

- Cloud-Native Mine Planning, SaaS Platform & Multi-Tenant Architecture Technology

- Digital Twin, IoT Sensor Integration & Real-Time Mine Operations Technology

- Artificial Intelligence, Machine Learning & Predictive Analytics in Mine Planning

- Drone, LiDAR, Photogrammetry & High-Resolution Survey Data Integration Technology

- Patent & IP Landscape in Mine Planning Software Technologies

- Value Chain & Supply Chain Analysis

- Specialist Mine Planning Software Vendors & Independent Software Developers

- Geological, Survey & Mining Equipment OEMs Offering Bundled Planning Software

- Cloud Infrastructure Providers, Data Centre & SaaS Hosting Partners

- System Integrators, Mining Technology Consultants & Implementation Service Providers

- Data Providers, Geological Database & Subscription Content Suppliers

- End-User Procurement, Mine Operator & Corporate IT Channel

- Training, Certification & Mining Software Education Ecosystem

- Pricing Analysis

- Perpetual License & On-Premise Software Capital and Maintenance Cost Analysis

- SaaS Subscription, Per-User & Per-Mine-Site Recurring Pricing Analysis

- Modular & Suite-Based Pricing Structure Across Mine Planning Software Categories

- Implementation, Customisation, Training & Professional Services Cost Analysis

- Total Cost of Ownership (TCO) & Return on Investment (ROI) Analysis for Mine Planning Software Deployments

- Benchmarking of Cloud SaaS vs. On-Premise vs. Hybrid Pricing Models

- Sustainability & Environmental Analysis

- Role of Mine Planning Software in Reducing Carbon Footprint, Energy Intensity & Diesel Consumption Across Mining Operations

- Contribution of Optimised Mine Planning to Water Stewardship, Tailings Management & Mine Closure Outcomes

- Mine Planning Software Support for ESG Reporting, GRI, SASB & ICMM Disclosure Alignment

- Biodiversity, Land-Use & Community Impact Considerations Integrated into Mine Planning Workflows

- Alignment of Mine Planning Software Capabilities with SDG 9 (Industry & Innovation), SDG 12 (Responsible Production) & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Software Solution Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Software Solution Type, Deployment Mode & Geography

- Player Classification

- Established Mine Planning Software OEMs & Suite Providers

- Specialist Geological Modelling & Resource Estimation Software Providers

- Pit Optimisation, Scheduling & Strategic Planning Solution Specialists

- Drill, Blast, Survey & Geotechnical Software Providers

- Haulage, Fleet Management & Mine Operations Software Vendors

- Cloud-Native, SaaS & AI-First Mine Planning Platform Providers

- Mining Equipment OEMs Offering Integrated Planning & Operations Software

- System Integrators, Consultancies & Implementation Specialists with Proprietary Tooling

- Competitive Analysis Frameworks

- Market Share Analysis by Software Solution Type, Deployment Mode & Region

- Company Profile

- Company Overview & Headquarters

- Mine Planning Software Products & Solution Portfolio

- Key Customer Relationships & Reference Mine Site Deployments

- R&D Footprint, Development Centres & Engineering Capacity

- Revenue (Mine Planning Software Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Platform Releases, Module Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Software Solution Type, Deployment Mode, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Cloud Migration & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & ESG-Aligned Software Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)