Global Foam Chemicals Market By Product Type, By Foam Type, By Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Foam Chemicals Market encompasses the manufacture, formulation, distribution, and end-use deployment of chemical building blocks engineered to produce flexible, rigid, and specialty cellular polymer foams across construction insulation, bedding and furniture, automotive interiors, packaging, footwear, appliances, marine, and industrial application categories. The market includes polyols, isocyanates such as toluene diisocyanate (TDI) and methylene diphenyl diisocyanate (MDI), blowing agents covering hydrofluoroolefins (HFOs), hydrocarbons, water-blown systems, and carbon dioxide, silicone and non-silicone surfactants, amine and organometallic catalysts, halogenated and halogen-free flame retardants, cell openers, crosslinkers, and chain extenders. These chemical inputs are procured by polyurethane system houses, expanded polystyrene producers, extruded polystyrene processors, phenolic foam manufacturers, polyolefin foam converters, latex foam producers, and integrated chemical companies serving downstream foam fabrication value chains globally. The market additionally covers reactive intermediates, bio-based and recycled feedstocks entering commercial foam production, and proprietary additive packages developed to address evolving regulatory requirements covering volatile organic compound emissions, fire safety performance, indoor air quality certifications, and end-of-life recyclability mandates across regulated end-use sectors.

Market Insights

The global foam chemicals market is entering a structural growth phase shaped by accelerating demand for energy-efficient building insulation, sustained expansion in lightweight automotive components, premium bedding modernization across emerging consumer economies, and a wholesale formulation transition toward low global warming potential blowing agents driven by international environmental commitments. The market was valued at approximately USD 47.6 billion in 2025 and is projected to reach USD 81.4 billion by 2036, advancing at a compound annual growth rate of 5.0% through the forecast period, as foam producers reformulate product portfolios to comply with the global hydrofluorocarbon phase-down under the Kigali Amendment, accommodate construction sector adoption of stricter thermal performance codes, and scale supply of high-resilience flexible foam systems to meet rebounding furniture and automotive interior demand.

The compositional rebalancing of foam chemical demand toward sustainable feedstocks and next-generation blowing agents is creating differentiated growth pathways across raw material categories. Polyols sourced from natural oil, recycled polyethylene terephthalate streams, and chemically recycled polyurethane recovered through glycolysis or hydrolysis are gaining commercial traction with system house buyers seeking embedded carbon footprint reductions, while methylene diphenyl diisocyanate continues to outpace toluene diisocyanate growth as rigid insulation and specialty elastomer applications absorb incremental MDI capacity additions from China, the United States, and Western Europe. Producers including BASF, Covestro, Dow, Huntsman, Wanhua Chemical, and Tosoh are accelerating capital investment in MDI debottlenecking, HFO blowing agent production, and bio-based polyol units, with announced capacity expansions in the Gulf of Mexico, the Yangtze River Delta, and Saudi Arabia signaling a structural shift in supply geography over the forecast horizon.

Rigid polyurethane foam is the fastest-expanding foam category within the broader market, driven by accelerated retrofit and new construction adoption of polyurethane insulated panels, spray polyurethane foam roofing systems, and high-performance domestic appliance insulation responding to revised minimum energy performance standards in the European Union, the United States, China, and India. Spray polyurethane foam applications, in which contractor-installed two-component systems deliver superior thermal resistance, air sealing, and moisture management within retrofit envelopes, are scaling rapidly as commercial and residential building owners pursue compliance with net-zero operational carbon targets. Within flexible foam, high-resilience and viscoelastic memory foam variants are capturing share from conventional polyether systems, particularly in the bedding category where premium mattress producers integrate gel-infused and copper-infused foam constructions to differentiate against incumbent innerspring formats.

Asia-Pacific is projected to record the highest regional compound annual growth rate through 2036, anchored by Chinese, Indian, and Southeast Asian construction activity, accelerating automotive output across India, Thailand, Indonesia, and Vietnam, and a multi-decade urbanization tailwind sustaining household appliance and bedding demand across the region. North America remains the largest absolute revenue market by foam chemical consumption, supported by sustained spray polyurethane foam adoption, robust automotive seating and acoustic foam pull-through, and an industrial sealants and adhesives ecosystem absorbing rigid foam derivatives. Europe represents the third major regional market, where the Energy Performance of Buildings Directive recast, F-gas regulation tightening, and circular economy action plan compliance obligations are simultaneously driving formulation transitions toward HFO blowing agents, bio-based polyols, and chemically recycled foam feedstocks across regulated end-use applications.

Key Drivers

Tightening Building Energy Performance Standards and Net-Zero Construction Mandates Driving Sustained Demand for Rigid Polyurethane and Polystyrene Insulation Foam Chemistries

The global tightening of building energy performance regulations, including the European Union Energy Performance of Buildings Directive recast establishing zero-emission building requirements by 2030, United States International Energy Conservation Code revisions mandating higher thermal envelope performance, China’s three-step energy efficiency improvement roadmap, and India’s Energy Conservation Building Code 2017 enforcement across commercial floor space, is generating durable multi-decade demand for high-performance foam insulation chemistries that deliver superior R-value per unit thickness relative to mineral wool and cellulose alternatives. Rigid polyurethane spray foam, polyisocyanurate boardstock, and extruded polystyrene insulation systems are capturing share within both new construction and deep retrofit segments, with rigid foam chemicals demand strengthening across MDI, polyester polyol, HFO blowing agent, and flame retardant categories. The European Commission Renovation Wave Strategy targeting a doubling of annual renovation rates, combined with United States Inflation Reduction Act incentives for building envelope upgrades and home energy efficiency rebates, is materially expanding the addressable market for insulating foam chemical formulators serving the construction value chain through 2036.

Automotive Lightweighting Imperatives, Electric Vehicle Production Scale-Up, and Cabin Acoustic Performance Requirements Sustaining Flexible and Specialty Foam Chemical Demand

The automotive industry structural shift toward electric vehicle architectures, combined with regulatory and competitive pressure to reduce vehicle mass for fuel economy and battery range optimization, is generating sustained pull-through demand for foam chemicals deployed in seating systems, headliners, dashboards, acoustic insulation, vibration damping, and thermoplastic polyurethane components engineered to replace heavier conventional materials. Electric vehicle platforms place elevated acoustic management requirements on cabin foam systems, as the absence of internal combustion engine noise increases occupant sensitivity to road, tire, and wind-induced sound transmission, driving incremental specification of high-density viscoelastic foam, melamine acoustic foam, and specialty polyurethane elastomer systems within EV interior packages. Global light vehicle production is projected to exceed 95 million units annually by 2030, with electric vehicles accounting for an expanding share of total volume, and foam chemical content per vehicle is rising as automakers integrate enhanced thermal management foam around battery packs, sound-dampening foam within underbody structures, and premium occupant comfort foam in seating modules across mainstream and luxury segments globally.

Sustainability Mandates, Circular Economy Policies, and Bio-Based Foam Chemical Adoption Reshaping Supply Chains Toward Renewable and Recycled Feedstock Architectures

Global sustainability commitments, including European Union Green Deal targets, corporate scope 3 emission reduction pledges by major furniture, mattress, and appliance brand owners, and circular economy regulatory frameworks mandating recycled content thresholds in construction, packaging, and consumer durable applications, are accelerating commercial adoption of bio-based polyols, chemically recycled polyurethane raw materials, and carbon dioxide-derived polyols across foam chemical portfolios. Producers are commercializing soybean-based polyols, castor oil polyols, recycled polyethylene terephthalate aromatic polyester polyols, and depolymerized polyurethane streams recovered through glycolysis, hydrolysis, and acidolysis routes, while emerging carbon-capture polyol technologies utilizing waste industrial carbon dioxide as a feedstock are entering pilot and commercial-scale deployment. Furniture retailers including IKEA, mattress producers such as Tempur Sealy, and automotive original equipment manufacturers are issuing supplier specifications mandating verified renewable content in foam components, creating procurement leverage that is reshaping foam chemical supply chains and incentivizing capital deployment toward bio-based and recycled feedstock infrastructure through 2036.

Key Challenges

Petrochemical Feedstock Price Volatility, Crude Oil Linkage, and Energy Cost Pass-Through Constraining Foam Chemical Producer Margins and Customer Pricing Stability

Foam chemicals are predominantly derived from petrochemical feedstocks, including benzene, toluene, propylene oxide, ethylene oxide, and aniline, exposing producer cost structures to crude oil price volatility, regional natural gas price differentials, and refining margin fluctuations that have generated material earnings volatility across the industry over the recent operating cycle. Sustained natural gas price elevation in Europe following the 2022 energy crisis has structurally disadvantaged European MDI, TDI, and polyol production economics relative to United States Gulf Coast and Middle Eastern competitors operating on cost-advantaged ethane and propane feedstocks, prompting capacity rationalization announcements by European producers and a long-term competitiveness reassessment across the regional foam chemical value chain. Customer industries including bedding manufacturers, furniture producers, and construction product converters operate on thin margins and limited pricing power against retail and contractor counterparties, constraining the ability of foam chemical producers to fully pass through feedstock and energy cost inflation, periodically compressing producer EBITDA margins during input cost upcycles and limiting capital reinvestment capacity across the formulator base.

Hydrofluorocarbon Phase-Down Compliance, Flame Retardant Restrictions, and Diisocyanate Worker Exposure Regulations Imposing Sustained Reformulation and Capital Cost Burdens

The Kigali Amendment to the Montreal Protocol, the European Union F-gas Regulation, and the United States American Innovation and Manufacturing Act are imposing a phased reduction of hydrofluorocarbon blowing agent consumption that requires foam chemical producers and downstream system houses to invest in reformulation, new equipment compatibility validation, and supply chain transition toward hydrofluoroolefin and hydrocarbon-based blowing agent platforms within compressed compliance timelines. The European Chemicals Agency restriction on diisocyanates applicable from August 2023, requiring mandatory worker training for industrial and professional users of products containing more than 0.1% diisocyanates, has imposed sustained operational and training cost burdens across the polyurethane processor base. Restrictions on halogenated flame retardants under European Union RoHS, REACH, and California Proposition 65 frameworks are simultaneously driving reformulation toward phosphorus-based, mineral-based, and reactive flame retardant alternatives, requiring producers to qualify substitute chemistries against established fire performance benchmarks, recertify foam systems for regulated end-use applications, and absorb the associated reformulation, customer requalification, and capacity reconfiguration costs across multiple product portfolios simultaneously through the forecast horizon.

Polyurethane Recycling Infrastructure Gaps, End-of-Life Foam Disposal Constraints, and Extended Producer Responsibility Compliance Increasing Sustainability Risk Exposure

The historical absence of large-scale commercial polyurethane recycling infrastructure, combined with the thermoset nature of cured polyurethane foam constraining mechanical reprocessing routes and the technical complexity of chemical recycling pathways including glycolysis, hydrolysis, and acidolysis, has created a structural gap between rising regulatory expectations for circular foam supply chains and the actual capacity available to recover, depolymerize, and reintegrate end-of-life foam into virgin-equivalent feedstock streams. Extended producer responsibility frameworks emerging across France, Germany, and the Netherlands covering mattress, furniture, and construction insulation waste streams are imposing collection, sorting, and recycling compliance obligations on foam chemical value chain participants, requiring industry-wide investment in collection logistics, advanced sorting technologies, and chemical recycling capacity to avoid escalating disposal levies and brand reputation risk. Landfill disposal restrictions on polyurethane and polystyrene waste, combined with rising incineration costs and growing public scrutiny of microplastic shedding from foam products in marine environments, are intensifying pressure on foam chemical producers to coordinate with downstream brand owners and waste management operators on closed-loop recovery systems that current market-scale infrastructure does not yet support at commercially viable cost positions.

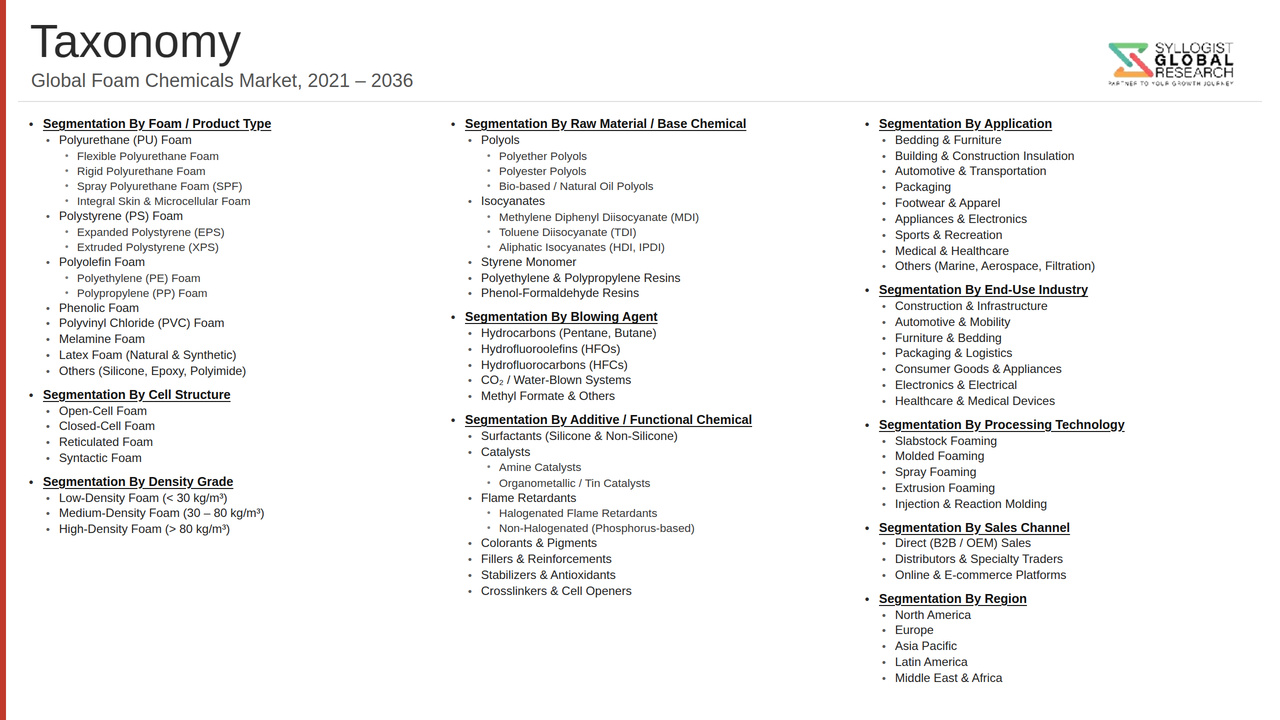

Market Segmentation

- Segmentation By Product Type

- Polyols (Polyether, Polyester, Bio-based)

- Isocyanates (MDI, TDI, Polymeric MDI)

- Blowing Agents (HFOs, Hydrocarbons, Water, Carbon Dioxide, Methylene Chloride)

- Surfactants (Silicone, Non-Silicone)

- Catalysts (Amine, Organometallic)

- Flame Retardants (Halogenated, Halogen-Free)

- Crosslinkers and Chain Extenders

- Others

- Segmentation By Foam Type

- Flexible Polyurethane Foam

- Rigid Polyurethane Foam

- Polystyrene Foam (EPS and XPS)

- Phenolic Foam

- Polyolefin Foam (Polyethylene and Polypropylene)

- Polyvinyl Chloride Foam

- Melamine Foam

- Latex Foam

- Others

- Segmentation By Application

- Bedding and Furniture

- Construction Insulation

- Automotive Interiors and Components

- Packaging

- Appliances

- Footwear

- Marine and Industrial

- Others

- Segmentation By End User

- Building and Construction

- Automotive and Transportation

- Furniture and Bedding

- Consumer Electronics and Appliances

- Industrial and Marine

- Packaging Industry

- Footwear and Apparel

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the total global market valuation of the Foam Chemicals Market in 2025, projected through 2036, disaggregated by product type, foam type, and end-use application, enabling chemical producers, brand owners, investors, and procurement planners to identify highest-growth segments and most durable revenue opportunities across the global foam value chain?

- How are foam chemical producers including BASF, Covestro, Dow, Huntsman, Wanhua Chemical, and Tosoh allocating capital investment across MDI debottlenecking, HFO blowing agent capacity, bio-based polyol units, and chemically recycled feedstock infrastructure through 2036, and which capacity expansion programs are defining future supply geography across the Gulf of Mexico, Yangtze River Delta, and Middle East?

- What hydrofluorocarbon phase-down compliance pathways under the Kigali Amendment, F-gas Regulation, and American Innovation and Manufacturing Act are reshaping blowing agent procurement across rigid foam, appliance insulation, and spray polyurethane foam applications, and how are producers managing the transition toward HFO, hydrocarbon, and water-blown systems within compressed regulatory timelines?

- Which foam chemical categories, including bio-based polyols, recycled polyethylene terephthalate aromatic polyester polyols, halogen-free flame retardants, and carbon dioxide-derived polyols, are generating the highest growth rates through 2036, and what feedstock, processing, and certification capabilities are most critical to commercial scale-up in each category?

- How is the competitive landscape structured among integrated petrochemical producers, specialty foam chemical formulators, and bio-based feedstock entrants pursuing system house and direct end-user contracts, and what partnership, joint venture, and acquisition strategies are enabling new entrants to compete against established producers in next-generation sustainable foam chemistries?

- What end-of-life recycling, extended producer responsibility, and circular economy obligations under European Union, French, German, and Dutch regulatory frameworks are reshaping foam chemical procurement specifications across mattress, furniture, construction insulation, and automotive seating value chains, and how are producers and brand owners building the closed-loop infrastructure required for compliance?

- Which regional foam chemical markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the most substantial incremental demand through 2036, and what construction activity, automotive production, energy efficiency regulation, and consumer durable consumption factors are driving foam chemical capacity investment and supplier selection decisions in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility, Feedstock Availability & Petrochemical Supply Risk

- Regulatory, Chemical Compliance (REACH, TSCA) & Restricted Substances Phase-Out Risk

- Health, Safety & Environmental (HSE) Exposure, VOC & Isocyanate Handling Risk

- Technology Transition, Low-GWP Blowing Agent & Bio-Based Polyol Adoption Risk

- Demand Cyclicality, End-Use Industry Slowdown & Inventory Destocking Risk

- Regulatory Framework & Standards

- Global Chemical Registration, REACH, TSCA & K-REACH Compliance Frameworks for Foam Chemicals

- Blowing Agent Regulations, Kigali Amendment, HFC Phase-Down & Low-GWP Transition Standards

- Flame Retardancy, Fire Safety & Restricted Flame Retardant (PBDE, HBCD) Standards Across End-Use Sectors

- Volatile Organic Compound (VOC), Indoor Air Quality & Emissions Standards for Foam Products

- Sustainability, Circular Economy, Extended Producer Responsibility & Bio-Based Content Certification Standards

- Global Foam Chemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Kilotons)

- Market Size & Forecast by Product Type

- Polyols (Polyether Polyols, Polyester Polyols & Bio-Based Polyols)

- Isocyanates (MDI, TDI & Aliphatic Isocyanates)

- Blowing Agents (Hydrocarbons, HFCs, HFOs, HCFCs & Water-Blown Systems)

- Catalysts (Amine Catalysts & Organotin Catalysts)

- Surfactants (Silicone-Based & Non-Silicone Surfactants)

- Flame Retardants (Halogenated, Phosphorus-Based & Mineral-Based)

- Cross-Linkers & Chain Extenders

- Stabilizers, Pigments & Other Additives

- Market Size & Forecast by Foam Type

- Polyurethane Flexible Foam Chemicals

- Polyurethane Rigid Foam Chemicals

- Polystyrene Foam Chemicals (EPS & XPS)

- Polyolefin Foam Chemicals (Polyethylene & Polypropylene)

- Polyvinyl Chloride (PVC) Foam Chemicals

- Phenolic Foam Chemicals

- Melamine & Other Specialty Foam Chemicals

- Market Size & Forecast by Technology

- Conventional Petrochemical-Based Foam Chemistry

- Bio-Based & Renewable Feedstock Polyol Technology

- Low-GWP & Next-Generation Blowing Agent Technology (HFOs, Hydrocarbons)

- Halogen-Free Flame Retardant Technology

- CO2-Blown & Water-Blown Foam Technology

- Recycled Polyol & Chemical Recycling Technology

- Nano-Enhanced & Functional Additive Technology

- Market Size & Forecast by Foam Density

- Low Density Foam Chemicals

- Medium Density Foam Chemicals

- High Density Foam Chemicals

- Market Size & Forecast by Application

- Bedding & Furniture

- Building & Construction (Insulation, Panels & Sealants)

- Automotive & Transportation (Seating, Headliners & NVH)

- Packaging (Protective & Cold Chain)

- Appliances & Refrigeration

- Footwear & Apparel

- Sports, Leisure & Medical

- Industrial & Marine

- Market Size & Forecast by End-User

- Furniture & Bedding Manufacturers

- Automotive OEMs & Tier-1 Suppliers

- Construction Companies & Insulation Contractors

- Appliance & White Goods Manufacturers

- Packaging Converters & Contract Manufacturers

- Footwear & Sports Goods Manufacturers

- Market Size & Forecast by Sales Channel

- Direct Sales (B2B & Key Account)

- Distributors & Trading Houses

- System Houses & Toll Manufacturers

- Online & E-Commerce Channels

- North America Foam Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Foam Type

- By Technology

- By Foam Density

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Foam Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Foam Type

- By Technology

- By Foam Density

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Foam Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Foam Type

- By Technology

- By Foam Density

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Foam Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Foam Type

- By Technology

- By Foam Density

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Foam Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Foam Type

- By Technology

- By Foam Density

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Foam Chemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Kilotons)

- By Product Type

- By Foam Type

- By Technology

- By Foam Density

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Bio-Based & Renewable Polyol Technology Deep-Dive

- Low-GWP Blowing Agent (HFO & Hydrocarbon) Technology

- Halogen-Free & Sustainable Flame Retardant Technology

- Chemical Recycling & Recycled Polyol Production Technology

- Catalyst & Surfactant Innovation for High-Performance Foams

- CO2-Blown & Water-Blown Rigid and Flexible Foam Technology

- Digital Process Control, Reactive Foam Simulation & AI-Based Formulation Technology

- Patent & IP Landscape in Foam Chemicals Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock (Propylene Oxide, Benzene, Toluene & MDI/TDI Precursors) Supply Chain

- Polyol & Isocyanate Production Capacity & Manufacturing Footprint

- Blowing Agent, Catalyst, Surfactant & Additive Supplier Landscape

- System House, Formulation & Toll Manufacturing Network

- Foam Converter, Fabricator & End-Use Manufacturer Channel

- Distribution, Logistics & Hazardous Chemical Handling

- End-of-Life Foam Collection, Recycling & Circular Economy

- Pricing Analysis

- Polyol Price Trend Analysis (Polyether & Polyester Polyols)

- MDI & TDI Isocyanate Price Trend & Margin Analysis

- Blowing Agent Price Trend Analysis (HFC, HFO & Hydrocarbon)

- Catalyst, Surfactant & Additive Pricing Analysis

- Flame Retardant & Specialty Additive Pricing Analysis

- Bio-Based & Sustainable Foam Chemicals Pricing Premium Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Foam Chemicals: Carbon Footprint, Energy Intensity & Cradle-to-Grave Impact Across Product Routes

- Bio-Based Content, Renewable Feedstock Adoption & Decarbonization Pathway for Foam Chemicals

- Circular Economy: Mechanical Recycling, Chemical Recycling & Recycled Polyol Integration in Foam Production

- Low-GWP Blowing Agent Transition, HFC Phase-Down Compliance & Climate Impact Reduction

- Regulatory-Driven Sustainability, SDG Alignment, Green Chemistry & Eco-Label Eligibility for Foam Products

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Product Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Foam Type & Geography

- Player Classification

- Integrated Petrochemical & Foam Chemicals Producers

- Specialist Polyol & Isocyanate Manufacturers

- Blowing Agent Producers (Fluorochemical & Hydrocarbon Suppliers)

- Catalyst, Surfactant & Specialty Additive Companies

- Flame Retardant & Sustainability Additive Specialists

- Bio-Based Polyol & Renewable Feedstock Innovators

- System Houses & Foam Formulation Specialists

- Chemical Recyclers & Circular Polyol Technology Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Foam Type & Region

- Company Profile

- Company Overview & Headquarters

- Foam Chemicals Products & Technology Portfolio

- Key Customer Relationships & Reference Account Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Foam Chemicals Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Foam Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)